. . . . . .

1

Dynamic Pricing and Inventory Managementunder Fluctuating Procurement Costs

Philip (Renyu) Zhang

(Joint work with Guang Xiao and Nan Yang)

Olin Business SchoolWashington University in St. Louis

June 20, 2014

. . . . . .

2

Motivation

Inventory management: To mitigate the demand uncertainty risk.

Current global market: Prices of many commodities are now fluctuatingas much in a single day as they did in a year in the early 1990s (Wigginsand Blas 2008).

. . . . . .

2

Motivation

Inventory management: To mitigate the demand uncertainty risk.

Current global market: Prices of many commodities are now fluctuatingas much in a single day as they did in a year in the early 1990s (Wigginsand Blas 2008).

. . . . . .

2

Motivation

Inventory management: To mitigate the demand uncertainty risk.

Current global market: Prices of many commodities are now fluctuatingas much in a single day as they did in a year in the early 1990s (Wigginsand Blas 2008).

. . . . . .

3

Motivation (Cont’d)

I Dynamic Pricing: Dynamically adjust the sales price in each period.

1. Demand control effect.

2. Risk-pooling effect.

I Dual-Sourcing: spot purchasing + forward-buying.

1. Cost-responsiveness tradeoff: differentiated costs and leadtimes.

2. Portfolio effect among different sourcing channels.

I Goal of our paper: To understand how to coordinate the dynamicpricing and dual-sourcing strategies to hedge against demanduncertainty and procurement cost fluctuation risks.

. . . . . .

3

Motivation (Cont’d)

I Dynamic Pricing: Dynamically adjust the sales price in each period.

1. Demand control effect.

2. Risk-pooling effect.

I Dual-Sourcing: spot purchasing + forward-buying.

1. Cost-responsiveness tradeoff: differentiated costs and leadtimes.

2. Portfolio effect among different sourcing channels.

I Goal of our paper: To understand how to coordinate the dynamicpricing and dual-sourcing strategies to hedge against demanduncertainty and procurement cost fluctuation risks.

. . . . . .

3

Motivation (Cont’d)

I Dynamic Pricing: Dynamically adjust the sales price in each period.

1. Demand control effect.

2. Risk-pooling effect.

I Dual-Sourcing: spot purchasing + forward-buying.

1. Cost-responsiveness tradeoff: differentiated costs and leadtimes.

2. Portfolio effect among different sourcing channels.

I Goal of our paper: To understand how to coordinate the dynamicpricing and dual-sourcing strategies to hedge against demanduncertainty and procurement cost fluctuation risks.

. . . . . .

4

Research Questions

1. What is the impact of procurement cost volatility?

2. How to optimally respond to the cost fluctuation?

3. How does the dual-sourcing flexibility affect the optimal policy?

4. What is the relationship between dynamic pricing and dual-sourcing?

. . . . . .

4

Research Questions

1. What is the impact of procurement cost volatility?

2. How to optimally respond to the cost fluctuation?

3. How does the dual-sourcing flexibility affect the optimal policy?

4. What is the relationship between dynamic pricing and dual-sourcing?

. . . . . .

4

Research Questions

1. What is the impact of procurement cost volatility?

2. How to optimally respond to the cost fluctuation?

3. How does the dual-sourcing flexibility affect the optimal policy?

4. What is the relationship between dynamic pricing and dual-sourcing?

. . . . . .

4

Research Questions

1. What is the impact of procurement cost volatility?

2. How to optimally respond to the cost fluctuation?

3. How does the dual-sourcing flexibility affect the optimal policy?

4. What is the relationship between dynamic pricing and dual-sourcing?

. . . . . .

5

Outline

I Related Literature

I Model

I Impact of Cost Volatility

I Impact of Dual-Sourcing

I Conclusion: Takeaway Insights

. . . . . .

6

Literature Review

I Inventory management under fluctuating costs:I Kalymon (1971),I Berling and Martınez-de-Albeniz (2011),I Chen et al. (2013).

I Joint price&inventory control:I Federgruen and Heching (1999),I Zhou and Chao (2014).

I Our paper: Joint pricing & inventory management under demanduncertainty, cost fluctuation, and dual-sourcing.

. . . . . .

6

Literature Review

I Inventory management under fluctuating costs:I Kalymon (1971),I Berling and Martınez-de-Albeniz (2011),I Chen et al. (2013).

I Joint price&inventory control:I Federgruen and Heching (1999),I Zhou and Chao (2014).

I Our paper: Joint pricing & inventory management under demanduncertainty, cost fluctuation, and dual-sourcing.

. . . . . .

6

Literature Review

I Inventory management under fluctuating costs:I Kalymon (1971),I Berling and Martınez-de-Albeniz (2011),I Chen et al. (2013).

I Joint price&inventory control:I Federgruen and Heching (1999),I Zhou and Chao (2014).

I Our paper: Joint pricing & inventory management under demanduncertainty, cost fluctuation, and dual-sourcing.

. . . . . .

6

Literature Review

I Inventory management under fluctuating costs:I Kalymon (1971),I Berling and Martınez-de-Albeniz (2011),I Chen et al. (2013).

I Joint price&inventory control:I Federgruen and Heching (1999),I Zhou and Chao (2014).

I Our paper: Joint pricing & inventory management under demanduncertainty, cost fluctuation, and dual-sourcing.

. . . . . .

7

Model Formulation: Basics

I A risk-neutral firm modeled as a T−period stochastic inventorysystem, labeled backwards, with discount factor α ∈ (0, 1).

I Maximize the total expected profit over the planning horizon.

I Endogenous pricing.

I Dual-sourcing:I Spot market: immediate delivery, fluctuating cost ct .

I Forward-buying contract: postponed delivery, with unit cost Ft(ct).

. . . . . .

7

Model Formulation: Basics

I A risk-neutral firm modeled as a T−period stochastic inventorysystem, labeled backwards, with discount factor α ∈ (0, 1).

I Maximize the total expected profit over the planning horizon.

I Endogenous pricing.

I Dual-sourcing:I Spot market: immediate delivery, fluctuating cost ct .

I Forward-buying contract: postponed delivery, with unit cost Ft(ct).

. . . . . .

7

Model Formulation: Basics

I A risk-neutral firm modeled as a T−period stochastic inventorysystem, labeled backwards, with discount factor α ∈ (0, 1).

I Maximize the total expected profit over the planning horizon.

I Endogenous pricing.

I Dual-sourcing:I Spot market: immediate delivery, fluctuating cost ct .

I Forward-buying contract: postponed delivery, with unit cost Ft(ct).

. . . . . .

8

Sequence of Events

I The firm reviews inventory It and spot market price ct .

I The firm makes the following decisions:I xt − It ≥ 0: spot-purchasing, delivered immediately;

I qt ≥ 0: forward-buying, delivered at the beginning of the next period;

I pt ∈ [p, p]: sales price in the customer market.

I Demand Dt(pt) realized, revenue collected.

I Net inventory fully carried over to the next period:I Excess inventory fully carried over with unit cost h;

I Unsatisfied demand fully backlogged with unit cost b.

. . . . . .

8

Sequence of Events

I The firm reviews inventory It and spot market price ct .

I The firm makes the following decisions:I xt − It ≥ 0: spot-purchasing, delivered immediately;

I qt ≥ 0: forward-buying, delivered at the beginning of the next period;

I pt ∈ [p, p]: sales price in the customer market.

I Demand Dt(pt) realized, revenue collected.

I Net inventory fully carried over to the next period:I Excess inventory fully carried over with unit cost h;

I Unsatisfied demand fully backlogged with unit cost b.

. . . . . .

8

Sequence of Events

I The firm reviews inventory It and spot market price ct .

I The firm makes the following decisions:I xt − It ≥ 0: spot-purchasing, delivered immediately;

I qt ≥ 0: forward-buying, delivered at the beginning of the next period;

I pt ∈ [p, p]: sales price in the customer market.

I Demand Dt(pt) realized, revenue collected.

I Net inventory fully carried over to the next period:I Excess inventory fully carried over with unit cost h;

I Unsatisfied demand fully backlogged with unit cost b.

. . . . . .

8

Sequence of Events

I The firm reviews inventory It and spot market price ct .

I The firm makes the following decisions:I xt − It ≥ 0: spot-purchasing, delivered immediately;

I qt ≥ 0: forward-buying, delivered at the beginning of the next period;

I pt ∈ [p, p]: sales price in the customer market.

I Demand Dt(pt) realized, revenue collected.

I Net inventory fully carried over to the next period:I Excess inventory fully carried over with unit cost h;

I Unsatisfied demand fully backlogged with unit cost b.

. . . . . .

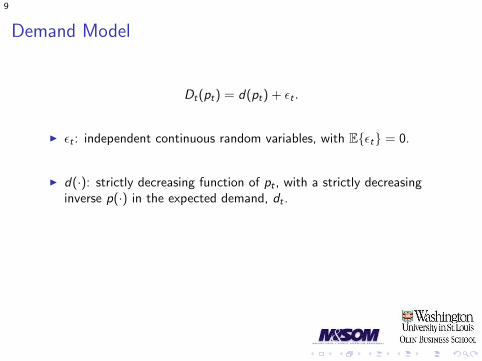

9

Demand Model

Dt(pt) = d(pt) + ϵt .

I ϵt : independent continuous random variables, with E{ϵt} = 0.

I d(·): strictly decreasing function of pt , with a strictly decreasinginverse p(·) in the expected demand, dt .

I We use dt = d(pt) ∈ [d , d ] as the decision variable.

Assumption 1

R(dt) := p(dt)dt is continuously differentiable and strictly concave.

. . . . . .

9

Demand Model

Dt(pt) = d(pt) + ϵt .

I ϵt : independent continuous random variables, with E{ϵt} = 0.

I d(·): strictly decreasing function of pt , with a strictly decreasinginverse p(·) in the expected demand, dt .

I We use dt = d(pt) ∈ [d , d ] as the decision variable.

Assumption 1

R(dt) := p(dt)dt is continuously differentiable and strictly concave.

. . . . . .

9

Demand Model

Dt(pt) = d(pt) + ϵt .

I ϵt : independent continuous random variables, with E{ϵt} = 0.

I d(·): strictly decreasing function of pt , with a strictly decreasinginverse p(·) in the expected demand, dt .

I We use dt = d(pt) ∈ [d , d ] as the decision variable.

Assumption 1

R(dt) := p(dt)dt is continuously differentiable and strictly concave.

. . . . . .

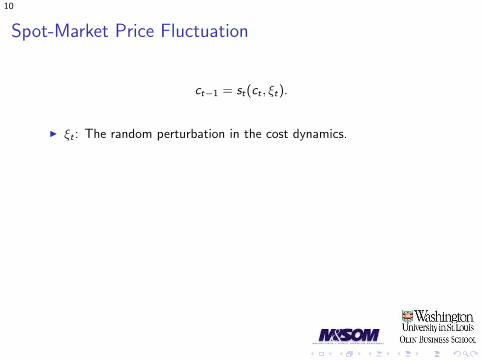

10

Spot-Market Price Fluctuation

ct−1 = st(ct , ξt).

I ξt : The random perturbation in the cost dynamics.

I st(·, ·) > 0 a.s., and st(ct , ξt) ≥s.d. st(ct , ξt) for any ct > ct .

I µt(ct) := E{st(ct , ξt)} < +∞ is increasing in ct .I Perfect market: µt(ct) = ct/α.

I Examples: GBMs, mean-reverting processes.

I Inventory resale is not allowed: no room for arbitrage.

. . . . . .

10

Spot-Market Price Fluctuation

ct−1 = st(ct , ξt).

I ξt : The random perturbation in the cost dynamics.

I st(·, ·) > 0 a.s., and st(ct , ξt) ≥s.d. st(ct , ξt) for any ct > ct .

I µt(ct) := E{st(ct , ξt)} < +∞ is increasing in ct .I Perfect market: µt(ct) = ct/α.

I Examples: GBMs, mean-reverting processes.

I Inventory resale is not allowed: no room for arbitrage.

. . . . . .

10

Spot-Market Price Fluctuation

ct−1 = st(ct , ξt).

I ξt : The random perturbation in the cost dynamics.

I st(·, ·) > 0 a.s., and st(ct , ξt) ≥s.d. st(ct , ξt) for any ct > ct .

I µt(ct) := E{st(ct , ξt)} < +∞ is increasing in ct .I Perfect market: µt(ct) = ct/α.

I Examples: GBMs, mean-reverting processes.

I Inventory resale is not allowed: no room for arbitrage.

. . . . . .

10

Spot-Market Price Fluctuation

ct−1 = st(ct , ξt).

I ξt : The random perturbation in the cost dynamics.

I st(·, ·) > 0 a.s., and st(ct , ξt) ≥s.d. st(ct , ξt) for any ct > ct .

I µt(ct) := E{st(ct , ξt)} < +∞ is increasing in ct .I Perfect market: µt(ct) = ct/α.

I Examples: GBMs, mean-reverting processes.

I Inventory resale is not allowed: no room for arbitrage.

. . . . . .

10

Spot-Market Price Fluctuation

ct−1 = st(ct , ξt).

I ξt : The random perturbation in the cost dynamics.

I st(·, ·) > 0 a.s., and st(ct , ξt) ≥s.d. st(ct , ξt) for any ct > ct .

I µt(ct) := E{st(ct , ξt)} < +∞ is increasing in ct .I Perfect market: µt(ct) = ct/α.

I Examples: GBMs, mean-reverting processes.

I Inventory resale is not allowed: no room for arbitrage.

. . . . . .

11

Forward-Buying Contract

I To mitigate cost volatility at the expense of responsiveness.

I Forward-buying contract: (ft , qt):I The firm pays ftqt to the supplier in period te ;I The supplier delivers qt to the firm in period te ;I For technical tractability, te = t − 1.

I ft = γct/α.I Effective unit cost: γct .I Perfect market: γ = 1.I In general, ft is determined through bilateral negotiations.I Most results hold for general ft = Ft(ct).

I Focus on the operational effect of forward-buying.I The contract cannot be traded in the derivatives market.

. . . . . .

11

Forward-Buying Contract

I To mitigate cost volatility at the expense of responsiveness.

I Forward-buying contract: (ft , qt):I The firm pays ftqt to the supplier in period te ;I The supplier delivers qt to the firm in period te ;I For technical tractability, te = t − 1.

I ft = γct/α.I Effective unit cost: γct .I Perfect market: γ = 1.I In general, ft is determined through bilateral negotiations.I Most results hold for general ft = Ft(ct).

I Focus on the operational effect of forward-buying.I The contract cannot be traded in the derivatives market.

. . . . . .

11

Forward-Buying Contract

I To mitigate cost volatility at the expense of responsiveness.

I Forward-buying contract: (ft , qt):I The firm pays ftqt to the supplier in period te ;I The supplier delivers qt to the firm in period te ;I For technical tractability, te = t − 1.

I ft = γct/α.I Effective unit cost: γct .I Perfect market: γ = 1.I In general, ft is determined through bilateral negotiations.I Most results hold for general ft = Ft(ct).

I Focus on the operational effect of forward-buying.I The contract cannot be traded in the derivatives market.

. . . . . .

11

Forward-Buying Contract

I To mitigate cost volatility at the expense of responsiveness.

I Forward-buying contract: (ft , qt):I The firm pays ftqt to the supplier in period te ;I The supplier delivers qt to the firm in period te ;I For technical tractability, te = t − 1.

I ft = γct/α.I Effective unit cost: γct .I Perfect market: γ = 1.I In general, ft is determined through bilateral negotiations.I Most results hold for general ft = Ft(ct).

I Focus on the operational effect of forward-buying.I The contract cannot be traded in the derivatives market.

. . . . . .

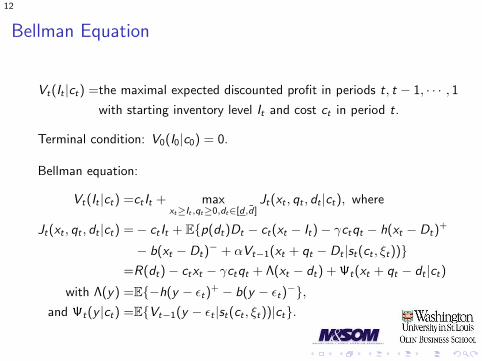

12

Bellman Equation

Vt(It |ct) =the maximal expected discounted profit in periods t, t − 1, · · · , 1with starting inventory level It and cost ct in period t.

Terminal condition: V0(I0|c0) = 0.

Bellman equation:

Vt(It |ct) =ct It + maxxt≥It ,qt≥0,dt∈[d,d ]

Jt(xt , qt , dt |ct), where

Jt(xt , qt , dt |ct) =− ct It + E{p(dt)Dt − ct(xt − It)− γctqt − h(xt − Dt)+

− b(xt − Dt)− + αVt−1(xt + qt − Dt |st(ct , ξt))}

=R(dt)− ctxt − γctqt + Λ(xt − dt) + Ψt(xt + qt − dt |ct)with Λ(y) =E{−h(y − ϵt)

+ − b(y − ϵt)−},

and Ψt(y |ct) =E{Vt−1(y − ϵt |st(ct , ξt))|ct}.

. . . . . .

12

Bellman Equation

Vt(It |ct) =the maximal expected discounted profit in periods t, t − 1, · · · , 1with starting inventory level It and cost ct in period t.

Terminal condition: V0(I0|c0) = 0.

Bellman equation:

Vt(It |ct) =ct It + maxxt≥It ,qt≥0,dt∈[d,d ]

Jt(xt , qt , dt |ct), where

Jt(xt , qt , dt |ct) =− ct It + E{p(dt)Dt − ct(xt − It)− γctqt − h(xt − Dt)+

− b(xt − Dt)− + αVt−1(xt + qt − Dt |st(ct , ξt))}

=R(dt)− ctxt − γctqt + Λ(xt − dt) + Ψt(xt + qt − dt |ct)with Λ(y) =E{−h(y − ϵt)

+ − b(y − ϵt)−},

and Ψt(y |ct) =E{Vt−1(y − ϵt |st(ct , ξt))|ct}.

. . . . . .

13

Optimal Policy

I (x∗t (It , ct), q∗t (It , ct), d

∗t (It , ct)): the optimal decisions in period t.

I ∆∗t (It , ct) := x∗

t (It , ct)− d∗t (It , ct): the optimal safety stock.

I The cost-dependent order-up-to/pre-order-up-to list-price policy.

I If It ≤ xt(ct), order from both channels and charge a list price.

I If It ∈ [xt(ct), I∗t (ct)], order via the forward-buying contract only and

charge a discounted price.

I If It ≥ I ∗t (ct), order nothing and charge a discounted price.

. . . . . .

13

Optimal Policy

I (x∗t (It , ct), q∗t (It , ct), d

∗t (It , ct)): the optimal decisions in period t.

I ∆∗t (It , ct) := x∗

t (It , ct)− d∗t (It , ct): the optimal safety stock.

I The cost-dependent order-up-to/pre-order-up-to list-price policy.

I If It ≤ xt(ct), order from both channels and charge a list price.

I If It ∈ [xt(ct), I∗t (ct)], order via the forward-buying contract only and

charge a discounted price.

I If It ≥ I ∗t (ct), order nothing and charge a discounted price.

. . . . . .

14

Impact of Cost Volatility

I Higher demand variability −→ lower profit.

I Surprisingly, the prediction is reversed for cost volatility.

Theorem 1

For two procurement cost processes {ct}1t=T and {ct}1t=T , assume thatfor every t = T ,T − 1, · · · , 1, st(ct , ξt) and st(ct , ξt) are concavelyincreasing in ct for any realization of ξt . The following statements hold:

(a) Vt(It |ct) is convexly decreasing in ct , for any It .(b) If {ct}1t=T and {ct}1t=T are identical except that

sτ (cτ , ξτ ) ≥cx sτ (cτ , ξτ ) for some cτ and τ , Vt(It |ct) ≥ Vt(It |ct) foreach (It , ct) and t, where ≥cx refers to larger in convex order, and{Vt(It |ct)}1t=T are the value functions associated with {ct}1t=T .

. . . . . .

14

Impact of Cost Volatility

I Higher demand variability −→ lower profit.

I Surprisingly, the prediction is reversed for cost volatility.

Theorem 1

For two procurement cost processes {ct}1t=T and {ct}1t=T , assume thatfor every t = T ,T − 1, · · · , 1, st(ct , ξt) and st(ct , ξt) are concavelyincreasing in ct for any realization of ξt . The following statements hold:

(a) Vt(It |ct) is convexly decreasing in ct , for any It .(b) If {ct}1t=T and {ct}1t=T are identical except that

sτ (cτ , ξτ ) ≥cx sτ (cτ , ξτ ) for some cτ and τ , Vt(It |ct) ≥ Vt(It |ct) foreach (It , ct) and t, where ≥cx refers to larger in convex order, and{Vt(It |ct)}1t=T are the value functions associated with {ct}1t=T .

. . . . . .

15

Impact of Cost Volatility (Cont’d)

I Higher cost volatility −→ higher profit.

I The fundamental difference between demand and cost risks:I Demand risk: decisions made prior to demand realization.

I Betting on demand uncertainty.

I Cost risk: decisions made posterior to cost realization.

I Responding to cost volatility.

I The impact of decision timing with respect to uncertainty realizationin capacity management and newsvendor network models withresponsive/postponed pricing: Van Mieghem and Dada (1999),Chod and Rudi (2005) and Bish et al. (2012).

. . . . . .

15

Impact of Cost Volatility (Cont’d)

I Higher cost volatility −→ higher profit.

I The fundamental difference between demand and cost risks:I Demand risk: decisions made prior to demand realization.

I Betting on demand uncertainty.

I Cost risk: decisions made posterior to cost realization.

I Responding to cost volatility.

I The impact of decision timing with respect to uncertainty realizationin capacity management and newsvendor network models withresponsive/postponed pricing: Van Mieghem and Dada (1999),Chod and Rudi (2005) and Bish et al. (2012).

. . . . . .

15

Impact of Cost Volatility (Cont’d)

I Higher cost volatility −→ higher profit.

I The fundamental difference between demand and cost risks:I Demand risk: decisions made prior to demand realization.

I Betting on demand uncertainty.

I Cost risk: decisions made posterior to cost realization.

I Responding to cost volatility.

I The impact of decision timing with respect to uncertainty realizationin capacity management and newsvendor network models withresponsive/postponed pricing: Van Mieghem and Dada (1999),Chod and Rudi (2005) and Bish et al. (2012).

. . . . . .

15

Impact of Cost Volatility (Cont’d)

I Higher cost volatility −→ higher profit.

I The fundamental difference between demand and cost risks:I Demand risk: decisions made prior to demand realization.

I Betting on demand uncertainty.

I Cost risk: decisions made posterior to cost realization.

I Responding to cost volatility.

I The impact of decision timing with respect to uncertainty realizationin capacity management and newsvendor network models withresponsive/postponed pricing: Van Mieghem and Dada (1999),Chod and Rudi (2005) and Bish et al. (2012).

. . . . . .

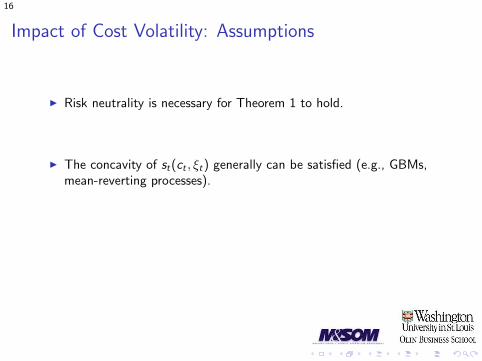

16

Impact of Cost Volatility: Assumptions

I Risk neutrality is necessary for Theorem 1 to hold.

I The concavity of st(ct , ξt) generally can be satisfied (e.g., GBMs,mean-reverting processes).

I When st(ct , ξt) is not concave in ct , the result holds for the majorityof numerical cases (except when the initial cost is low), in particularwhen the initial cost follows the stationary distribution.

. . . . . .

16

Impact of Cost Volatility: Assumptions

I Risk neutrality is necessary for Theorem 1 to hold.

I The concavity of st(ct , ξt) generally can be satisfied (e.g., GBMs,mean-reverting processes).

I When st(ct , ξt) is not concave in ct , the result holds for the majorityof numerical cases (except when the initial cost is low), in particularwhen the initial cost follows the stationary distribution.

. . . . . .

16

Impact of Cost Volatility: Assumptions

I Risk neutrality is necessary for Theorem 1 to hold.

I The concavity of st(ct , ξt) generally can be satisfied (e.g., GBMs,mean-reverting processes).

I When st(ct , ξt) is not concave in ct , the result holds for the majorityof numerical cases (except when the initial cost is low), in particularwhen the initial cost follows the stationary distribution.

. . . . . .

17

Optimal Response to Cost Volatility

I Optimal sales price: d∗t (It , ct) ↓ ct , i.e., p

∗t (It , ct) ↑ ct . The firm

passes (part of) the cost risk to customers.

Jt(xt , qt , dt |ct) =[R(dt)− ctdt ] + [Λ(∆t)− (1− γ)ct∆t ]

+ [Ψt(∆t + qt |ct)− γct(∆t + qt)].

I Three objectives: (a) generating revenue, (b) hedging againstdemand uncertainty, and (c) speculating on future costs.

I Optimal safety-stock and spot-purchasing: ∆t(ct), xt(ct) ↓ ct , ifγ ≤ 1; ∆t(ct) ↑ ct , if γ > 1.

I Optimal forward-buying quantity: generally not monotone in ct .

I Higher future cost trend −→ d∗t (It , ct) ↓, x∗t (It , ct) ↑, ∆∗

t (It , ct) ↑,and q∗t (It , ct) ↑.

. . . . . .

17

Optimal Response to Cost Volatility

I Optimal sales price: d∗t (It , ct) ↓ ct , i.e., p

∗t (It , ct) ↑ ct . The firm

passes (part of) the cost risk to customers.

Jt(xt , qt , dt |ct) =[R(dt)− ctdt ] + [Λ(∆t)− (1− γ)ct∆t ]

+ [Ψt(∆t + qt |ct)− γct(∆t + qt)].

I Three objectives: (a) generating revenue, (b) hedging againstdemand uncertainty, and (c) speculating on future costs.

I Optimal safety-stock and spot-purchasing: ∆t(ct), xt(ct) ↓ ct , ifγ ≤ 1; ∆t(ct) ↑ ct , if γ > 1.

I Optimal forward-buying quantity: generally not monotone in ct .

I Higher future cost trend −→ d∗t (It , ct) ↓, x∗t (It , ct) ↑, ∆∗

t (It , ct) ↑,and q∗t (It , ct) ↑.

. . . . . .

17

Optimal Response to Cost Volatility

I Optimal sales price: d∗t (It , ct) ↓ ct , i.e., p

∗t (It , ct) ↑ ct . The firm

passes (part of) the cost risk to customers.

Jt(xt , qt , dt |ct) =[R(dt)− ctdt ] + [Λ(∆t)− (1− γ)ct∆t ]

+ [Ψt(∆t + qt |ct)− γct(∆t + qt)].

I Three objectives: (a) generating revenue, (b) hedging againstdemand uncertainty, and (c) speculating on future costs.

I Optimal safety-stock and spot-purchasing: ∆t(ct), xt(ct) ↓ ct , ifγ ≤ 1; ∆t(ct) ↑ ct , if γ > 1.

I Optimal forward-buying quantity: generally not monotone in ct .

I Higher future cost trend −→ d∗t (It , ct) ↓, x∗t (It , ct) ↑, ∆∗

t (It , ct) ↑,and q∗t (It , ct) ↑.

. . . . . .

17

Optimal Response to Cost Volatility

I Optimal sales price: d∗t (It , ct) ↓ ct , i.e., p

∗t (It , ct) ↑ ct . The firm

passes (part of) the cost risk to customers.

Jt(xt , qt , dt |ct) =[R(dt)− ctdt ] + [Λ(∆t)− (1− γ)ct∆t ]

+ [Ψt(∆t + qt |ct)− γct(∆t + qt)].

I Three objectives: (a) generating revenue, (b) hedging againstdemand uncertainty, and (c) speculating on future costs.

I Optimal safety-stock and spot-purchasing: ∆t(ct), xt(ct) ↓ ct , ifγ ≤ 1; ∆t(ct) ↑ ct , if γ > 1.

I Optimal forward-buying quantity: generally not monotone in ct .

I Higher future cost trend −→ d∗t (It , ct) ↓, x∗t (It , ct) ↑, ∆∗

t (It , ct) ↑,and q∗t (It , ct) ↑.

. . . . . .

18

Impact of Dual-Sourcing Flexibility

I γ: the cost ratio between forward-buying and spot-purchasing.Lower γ implies higher dual-sourcing flexibility.

I Intuition suggests q∗t (It , ct) ↓ γ.Due to procurement costfluctuation, this may not be true in general:

I γ ↓ −→ d∗t (It , ct) ↑, x∗

t (It , ct) ↓, ∆∗t (It , ct) ↓.

I q∗t (It , ct) may not be monotone in γ, because lower γ also decreases

the marginal value of inventory in future periods.

I When γ is big enough (γ ≥ sup{αµt(ct)ct

}), the model is reduced toone with sole-sourcing from spot market alone.

I Dual-sourcing −→ d∗t (It , ct) ↑, x∗

t (It , ct) ↓, ∆∗t (It , ct) ↓ (Zhou and

Chao, 2014).

. . . . . .

18

Impact of Dual-Sourcing Flexibility

I γ: the cost ratio between forward-buying and spot-purchasing.Lower γ implies higher dual-sourcing flexibility.

I Intuition suggests q∗t (It , ct) ↓ γ.

Due to procurement costfluctuation, this may not be true in general:

I γ ↓ −→ d∗t (It , ct) ↑, x∗

t (It , ct) ↓, ∆∗t (It , ct) ↓.

I q∗t (It , ct) may not be monotone in γ, because lower γ also decreases

the marginal value of inventory in future periods.

I When γ is big enough (γ ≥ sup{αµt(ct)ct

}), the model is reduced toone with sole-sourcing from spot market alone.

I Dual-sourcing −→ d∗t (It , ct) ↑, x∗

t (It , ct) ↓, ∆∗t (It , ct) ↓ (Zhou and

Chao, 2014).

. . . . . .

18

Impact of Dual-Sourcing Flexibility

I γ: the cost ratio between forward-buying and spot-purchasing.Lower γ implies higher dual-sourcing flexibility.

I Intuition suggests q∗t (It , ct) ↓ γ.Due to procurement costfluctuation, this may not be true in general:

I γ ↓ −→ d∗t (It , ct) ↑, x∗

t (It , ct) ↓, ∆∗t (It , ct) ↓.

I q∗t (It , ct) may not be monotone in γ, because lower γ also decreases

the marginal value of inventory in future periods.

I When γ is big enough (γ ≥ sup{αµt(ct)ct

}), the model is reduced toone with sole-sourcing from spot market alone.

I Dual-sourcing −→ d∗t (It , ct) ↑, x∗

t (It , ct) ↓, ∆∗t (It , ct) ↓ (Zhou and

Chao, 2014).

. . . . . .

18

Impact of Dual-Sourcing Flexibility

I γ: the cost ratio between forward-buying and spot-purchasing.Lower γ implies higher dual-sourcing flexibility.

I Intuition suggests q∗t (It , ct) ↓ γ.Due to procurement costfluctuation, this may not be true in general:

I γ ↓ −→ d∗t (It , ct) ↑, x∗

t (It , ct) ↓, ∆∗t (It , ct) ↓.

I q∗t (It , ct) may not be monotone in γ, because lower γ also decreases

the marginal value of inventory in future periods.

I When γ is big enough (γ ≥ sup{αµt(ct)ct

}), the model is reduced toone with sole-sourcing from spot market alone.

I Dual-sourcing −→ d∗t (It , ct) ↑, x∗

t (It , ct) ↓, ∆∗t (It , ct) ↓ (Zhou and

Chao, 2014).

. . . . . .

19

Value of Dynamic Pricing and Dual-sourcing

I Dynamic pricing and dual-sourcing are strategic complements, i.e.,the application of one strategy increases the value of the other.

I When sourcing from the less responsive forward-buying channel, theflexibility to control demand via pricing becomes more valuable.

I In Zhou and Chao (2014), they are strategic substitutes.

I Compared with Zhou and Chao (2014), cost volatility renders thevalue of dynamic pricing and dual-sourcing significantly higher.

. . . . . .

19

Value of Dynamic Pricing and Dual-sourcing

I Dynamic pricing and dual-sourcing are strategic complements, i.e.,the application of one strategy increases the value of the other.

I When sourcing from the less responsive forward-buying channel, theflexibility to control demand via pricing becomes more valuable.

I In Zhou and Chao (2014), they are strategic substitutes.

I Compared with Zhou and Chao (2014), cost volatility renders thevalue of dynamic pricing and dual-sourcing significantly higher.

. . . . . .

19

Value of Dynamic Pricing and Dual-sourcing

I Dynamic pricing and dual-sourcing are strategic complements, i.e.,the application of one strategy increases the value of the other.

I When sourcing from the less responsive forward-buying channel, theflexibility to control demand via pricing becomes more valuable.

I In Zhou and Chao (2014), they are strategic substitutes.

I Compared with Zhou and Chao (2014), cost volatility renders thevalue of dynamic pricing and dual-sourcing significantly higher.

. . . . . .

20

Conclusion: Takeaway Insights

I A risk-neutral firm benefits from the procurement cost volatility.I Timing of decision making and uncertainty realization.

I Dynamic pricing and dual-sourcing are strategic complements.I Dynamic pricing dampens both demand and cost risks, while

dual-sourcing mitigates the cost risk but intensifies the demand risk.

. . . . . .

20

Conclusion: Takeaway Insights

I A risk-neutral firm benefits from the procurement cost volatility.

I Timing of decision making and uncertainty realization.

I Dynamic pricing and dual-sourcing are strategic complements.I Dynamic pricing dampens both demand and cost risks, while

dual-sourcing mitigates the cost risk but intensifies the demand risk.

. . . . . .

20

Conclusion: Takeaway Insights

I A risk-neutral firm benefits from the procurement cost volatility.I Timing of decision making and uncertainty realization.

I Dynamic pricing and dual-sourcing are strategic complements.I Dynamic pricing dampens both demand and cost risks, while

dual-sourcing mitigates the cost risk but intensifies the demand risk.

. . . . . .

20

Conclusion: Takeaway Insights

I A risk-neutral firm benefits from the procurement cost volatility.I Timing of decision making and uncertainty realization.

I Dynamic pricing and dual-sourcing are strategic complements.

I Dynamic pricing dampens both demand and cost risks, whiledual-sourcing mitigates the cost risk but intensifies the demand risk.

. . . . . .

20

Conclusion: Takeaway Insights

I A risk-neutral firm benefits from the procurement cost volatility.I Timing of decision making and uncertainty realization.

I Dynamic pricing and dual-sourcing are strategic complements.I Dynamic pricing dampens both demand and cost risks, while

dual-sourcing mitigates the cost risk but intensifies the demand risk.

. . . . . .

21

Q&A

Thank you!

Questions?