ENGINEERING ECONOMICS ISE460SESSION 15

Rate of Return, June 22, 2015

Geza P. Bottlik Page 1

OUTLINE

• Questions?

• News?

• Quiz Results

• Go over quiz

• Recommendations

• Go over homework

• New homework

• More on stocks

• IRR

ENGINEERING ECONOMICS ISE460SESSION 15

Rate of Return, June 22, 2015

Geza P. Bottlik Page 2

Quiz Results

ENGINEERING ECONOMICS ISE460SESSION 15

Rate of Return, June 22, 2015

Geza P. Bottlik Page 3

Quiz Results

ENGINEERING ECONOMICS ISE460SESSION 15

Rate of Return, June 22, 2015

Geza P. Bottlik Page 4

Quiz Results

ENGINEERING ECONOMICS ISE460SESSION 15

Rate of Return, June 22, 2015

Geza P. Bottlik Page 5

Recommendations

• Tate Britain – a few pictures (mostly Moore) during break

– Turner, Constable, Moore, Blake and many others

– Beautiful building

– Some modern stuff also

– Free, walk from your housing or tube stops Pimlico or

Vauxhall

ENGINEERING ECONOMICS ISE460SESSION 15

Rate of Return, June 22, 2015

Geza P. Bottlik Page 6

Recommendations

• National Portrait Gallery– Annual Competition of portrait

painting

– Wonderful paintings of all kinds with explanations by the

artists

– Selected from thousands of applicants

– Free, by Trafalgar square (we walked)

– No photos allowed

ENGINEERING ECONOMICS ISE460SESSION 15

Rate of Return, June 22, 2015

Geza P. Bottlik Page 7

Recommendations

• Serpentine Gallery– Open Tue- Thu to 6, all free

– Two venues, both in Kensington Gardens, take the tube

to Lancaster Gate walk South through the garden ( worth

the trip in itself)

– On the East side of the lake – life size sculptures by

Duane Hanson (pictures during the break). While there,

peak into the restaurant, The Magazine a fabulous design

by Zaha Hadid – the current darling of the architectural

design world.

– On the West side – Oil paintings by a British painter with

parents from Ghana – I found them very impressive

(pictures at break)

ENGINEERING ECONOMICS ISE460SESSION 15

Rate of Return, June 22, 2015

Geza P. Bottlik Page 8

Recommendations

• Victoria and Albert– free on Cromwell Road

– Take the 14 bus from South of Accent to V&A (1/2 hour)

– Lot’s of different things – mostly decorative arts – we

loved the glass

– Of special interest a small exhibit showing the new

addition in progress

– Special free exhibit : “What is Luxury?”

ENGINEERING ECONOMICS ISE460SESSION 15

Rate of Return, June 22, 2015

Geza P. Bottlik Page 9

Selling short and options

• Definition – stock in street name – the broker holds the stock and

the company does not know that you are the owner

• Selling short – sell someone else’s stock hoping that it goes down

and you can buy it back cheaper and replace it. No actual transfer

of stock ownership happens

• Without dividend – trading a stock without the associated dividend

• Put - An option contract giving the owner the right, but not the

obligation, to sell a specified amount of an underlying security at a

specified price (strike price) within a specified time. This is the

opposite of a call option, which gives the holder the right to buy

shares.

ENGINEERING ECONOMICS ISE460SESSION 15

Rate of Return, June 22, 2015

Geza P. Bottlik Page 10

Standard deviations

• If we have the average and the standard deviation of a

variable, we can calculate the probability of obtaining a

specific value

• To demonstrate what this means, what is the probability that

a member of this class is taller than 5 foot 7?

ENGINEERING ECONOMICS ISE460SESSION 15

Rate of Return, June 22, 2015

Geza P. Bottlik Page 11Contemporary Engineering Economics, 4th edition, © 2007

Incremental Analysis

Lecture No. 13

Chapter 7

Contemporary Engineering Economics

Copyright © 2006

ENGINEERING ECONOMICS ISE460SESSION 15

Rate of Return, June 22, 2015

Geza P. Bottlik Page 12

Comparing Mutually Exclusive Alternatives Based on IRR

• Issue: Can we rank the mutually exclusive projects by the magnitude of its IRR?n A1 A2

0

1

IRR

-$1,000 -$5,000

$2,000 $7,000

100% > 40%

$818 < $1,364PW (10%)

ENGINEERING ECONOMICS ISE460SESSION 15

Rate of Return, June 22, 2015

Geza P. Bottlik Page 13Contemporary Engineering Economics, 4th edition, © 2007

Who Got More Pay Raise?

Bill Hillary

10% 5%

ENGINEERING ECONOMICS ISE460SESSION 15

Annual Equivalent, June 23, 2014

Geza P. Bottlik Page 14

Can’t Compare without Knowing Their Base Salaries

Bill Hillary

Base Salary $50,000 $200,000

Pay Raise (%) 10% 5%

Pay Raise ($) $5,000 $10,000

For the same reason, we can’t compare mutually exclusive projects based onthe magnitude of its IRR. We need to know the size of investment and its timingof when to occur.

ENGINEERING ECONOMICS ISE460SESSION 15

Rate of Return, June 22, 2015

Geza P. Bottlik Page 15

Incremental Investment

• Assuming a MARR of 10%, you can always earn that rate from other investment source, i.e.,

$4,400 at the end of one year for $4,000 investment.

• By investing the additional $4,000 in A2, you would make additional $5,000, which is equivalent to earning at the rate of 25%. Therefore, the incremental investment in A2 is justified.

n Project A1 Project A2

Incremental Investment (A2 – A1)

0

1

-$1,000

$2,000

-$5,000

$7,000

-$4,000

$5,000

ROR

PW(10%)100%

$818

40%

$1,364

25%

$546

ENGINEERING ECONOMICS ISE460SESSION 15

Rate of Return, June 22, 2015

Geza P. Bottlik Page 16

Incremental Analysis (Procedure)

Step 1: Compute the cash flow for the difference between the projects (A,B) by subtracting the cash flow of the lower investment cost project (A) from that of the higher investment cost project (B).Step 2: Compute the IRR on this incremental

investment (IRR ).Step 3: Accept the investment B if and only if

IRR B-A > MARR

B-A

NOTE: Make sure that both IRRA and IRRB are greater than MARR.

ENGINEERING ECONOMICS ISE460SESSION 15

Rate of Return, June 22, 2015

Geza P. Bottlik Page 17

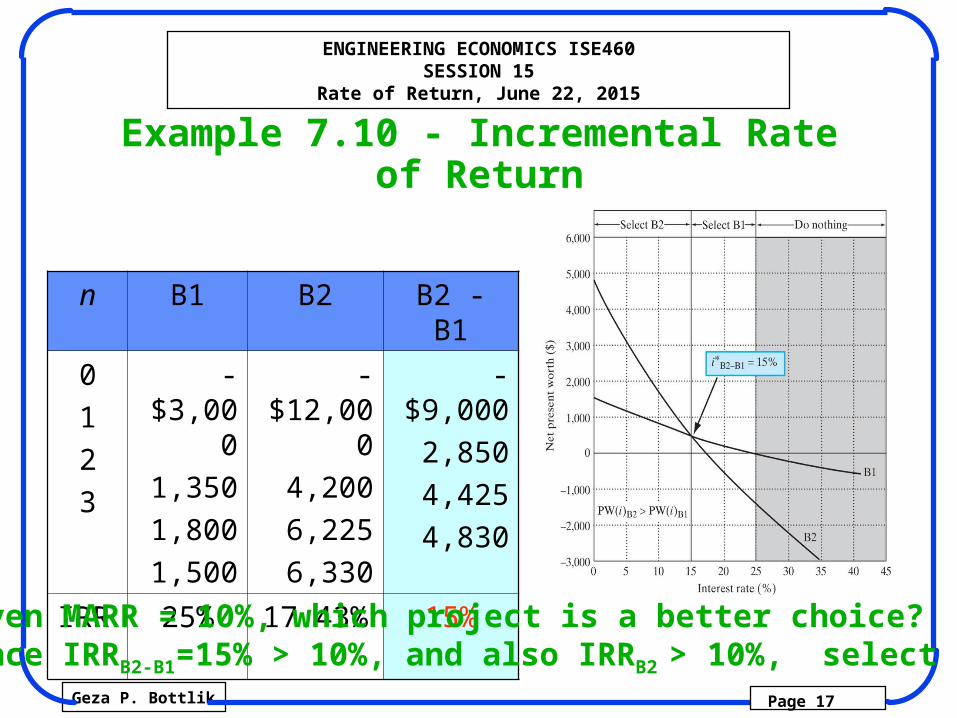

Example 7.10 - Incremental Rate of Return

n B1 B2 B2 - B1

0

1

2

3

-$3,000

1,350

1,800

1,500

-$12,000

4,200

6,225

6,330

-$9,000

2,850

4,425

4,830

IRR 25% 17.43% 15%

Given MARR = 10%, which project is a better choice?Since IRRB2-B1=15% > 10%, and also IRRB2 > 10%, select B2.

ENGINEERING ECONOMICS ISE460SESSION 15

Rate of Return, June 22, 2015

Geza P. Bottlik Page 18

IRR on Increment Investment:Three Alternatives

n D1 D2 D3

0 -$2,000 -$1,000 -$3,000

1 1,500 800 1,500

2 1,000 500 2,000

3 800 500 1,000

IRR 34.37% 40.76% 24.81%

Step 1: Examine the IRR for each project to eliminate any project that fails to meet the MARR.

Step 2: Compare D1 and D2 in pairs. IRRD1-D2=27.61% > 15%, so select D1. D1 becomes the current best.

Step 3: Compare D1 and D3. IRRD3-D1= 8.8% < 15%, so select D1 again.

Here, we conclude that D1 is the bestalternative.

ENGINEERING ECONOMICS ISE460SESSION 15

Annual Equivalent, June 23, 2014

Geza P. Bottlik Page 19

Practice Problem

You are considering

four types of

engineering designs.

The project lasts 10

years with the

following estimated

cash flows. The

interest rate (MARR) is

15%. Which of the four

is more attractive?

Project

A B C D

Initial cost $150 $220 $300 $340

Revenues/Year

$115 $125 $160 $185

Expenses/Year

$70 $65 $60 $80

IRR (%) 27.32 24.13 31.11 28.33

ENGINEERING ECONOMICS ISE460SESSION 15

Rate of Return, June 22, 2015

Geza P. Bottlik Page 20

Items CMS Option FMS Option

Annual O&M costs:

Annual labor cost $1,169,600 $707,200

Annual material cost 832,320 598,400

Annual overhead cost

3,150,000 1,950,000

Annual tooling cost 470,000 300,000

Annual inventory cost

141,000 31,500

Annual income taxes 1,650,000 1,917,000

Total annual costs $7,412,920 $5,504,100

Investment $4,500,000 $12,500,000

Net salvage value $500,000 $1,000,000

Example 7.13 Incremental Analysis for Cost-Only Projects

ENGINEERING ECONOMICS ISE460SESSION 15

Rate of Return, June 22, 2015

Geza P. Bottlik Page 21

n CMS Option FMS Option

Incremental

(FMS-CMS)

0 -$4,500,000 -$12,500,000 -$8,000,000

1 -7,412,920 -5,504,100 1,908,820

2 -7,412,920 -5,504,100 1,908,820

3 -7,412,920 -5,504,100 1,908,820

4 -7,412,920 -5,504,100 1,908,820

5 -7,412,920 -5,504,100 1,908,820

6 -7,412,920 -5,504,100

$2,408,820Salvage + $500,000 + $1,000,000

Incremental Cash Flow (FMS – CMS)

ENGINEERING ECONOMICS ISE460SESSION 15

Rate of Return, June 22, 2015

Geza P. Bottlik Page 22

Solution:

PW i

P A i

P F i

IRR

FMS CMS

FMS CMS

( ) $8, ,

$1,908, ( / , , )

$2, , ( / , , )

.43%

000 000

820 5

408 820 6

0

12 15%,

select CMS.

ENGINEERING ECONOMICS ISE460SESSION 15

Rate of Return, June 22, 2015

Geza P. Bottlik Page 23

Summary Rate of return (ROR) is the interest rate earned on

unrecovered project balances such that an investment’s cash receipts make the terminal project balance equal to zero.

Rate of return is an intuitively familiar and understandable measure of project profitability that many managers prefer to NPW or other equivalence measures.

Mathematically we can determine the rate of return for a given project cash flow series by locating an interest rate that equates the net present worth of its cash flows to zero. This break-even interest rate is denoted by the symbol i*.

ENGINEERING ECONOMICS ISE460SESSION 15

Rate of Return, June 22, 2015

Geza P. Bottlik Page 24

Internal rate of return (IRR) is another term for ROR that stresses the fact that we are concerned with the interest earned on the portion of the project that is internally invested, not those portions that are released by (borrowed from) the project.

To apply rate of return analysis correctly, we need to classify an investment into either a simple or a nonsimple investment.

A simple investment is defined as one in which the initial cash flows are negative and only one sign change occurs in the net cash flow, whereas a nonsimple investment is one for which more than one sign change occurs in the net cash flow series.

Multiple i*s occur only in nonsimple investments. However, not all nonsimple investments will have multiple i*s either.

ENGINEERING ECONOMICS ISE460SESSION 15

Rate of Return, June 22, 2015

Geza P. Bottlik Page 25

• For a pure investment, the solving rate of return (i*) is the rate of return internal to the project; so the decision rule is:

If IRR > MARR, accept the project.

If IRR = MARR, remain indifferent.

If IRR < MARR, reject the project.

IRR analysis yields results consistent with NPW and other equivalence methods.

• For a mixed investment, we need to calculate the true IRR, or known as the “return on invested capital.” However, if your objective is simply to make an accept or reject decision, it is recommended that either the NPW or AE analysis be used to make an accept/reject decision.

• To compare mutually exclusive alternatives by the IRR analysis, the incremental analysis must be adopted.