Y E O & Y E OCPAs & BUSINESS CONSULTANTS

Township of Grosse Ile

Financial Statements

March 31, 2020

Table of Contents

Section Page 1 List of Elected and Appointed Officials 1 – 1 2 Independent Auditors’ Report 2 – 1 3 Management’s Discussion and Analysis 3 – 1

4 Basic Financial Statements Government-wide Financial Statements Statement of Net Position 4 – 1 Statement of Activities 4 – 3 Fund Financial Statements Governmental Funds Balance Sheet 4 – 4 Reconciliation of Fund Balances of Governmental Funds to Net Position of

Governmental Activities

4 – 6 Statement of Revenues, Expenditures and Changes in Fund Balances 4 – 7 Reconciliation of the Statement of Revenues, Expenditures and Changes

in Fund Balances of Governmental Funds to the Statement of Activities

4 – 9

Proprietary Funds Statement of Net Position 4 – 10 Statement of Revenues, Expenses and Changes in Fund Net Position 4 – 12 Statement of Cash Flows 4 – 14 Fiduciary Funds Statement of Assets and Liabilities 4 – 16

Component Units Statement of Net position Statement of Activities

4 – 17 4 – 18

Notes to the Financial Statements 4 – 19

Section Page 5 Required Supplementary Information Budgetary Comparison Schedule General Fund 5 – 1 Recreation Fund 5 – 4 Fire Operating Fund 5 – 5

Drain and Storm Fund

Municipal Retirement System of Michigan – Schedule of Employer Contributions Municipal Retirement System of Michigan – Schedule of Changes in Net Pension Liability and Related Ratios Other Postemployment Benefits – Schedule of Employer Contributions Other Postemployment Benefits – Schedule of Changes in Net OPEB Liability and Related Ratios Other Postemployment Benefits – Schedule of investment Returns

5 – 6

5 – 7 5 – 8

5 – 9 5 – 10 5 – 11

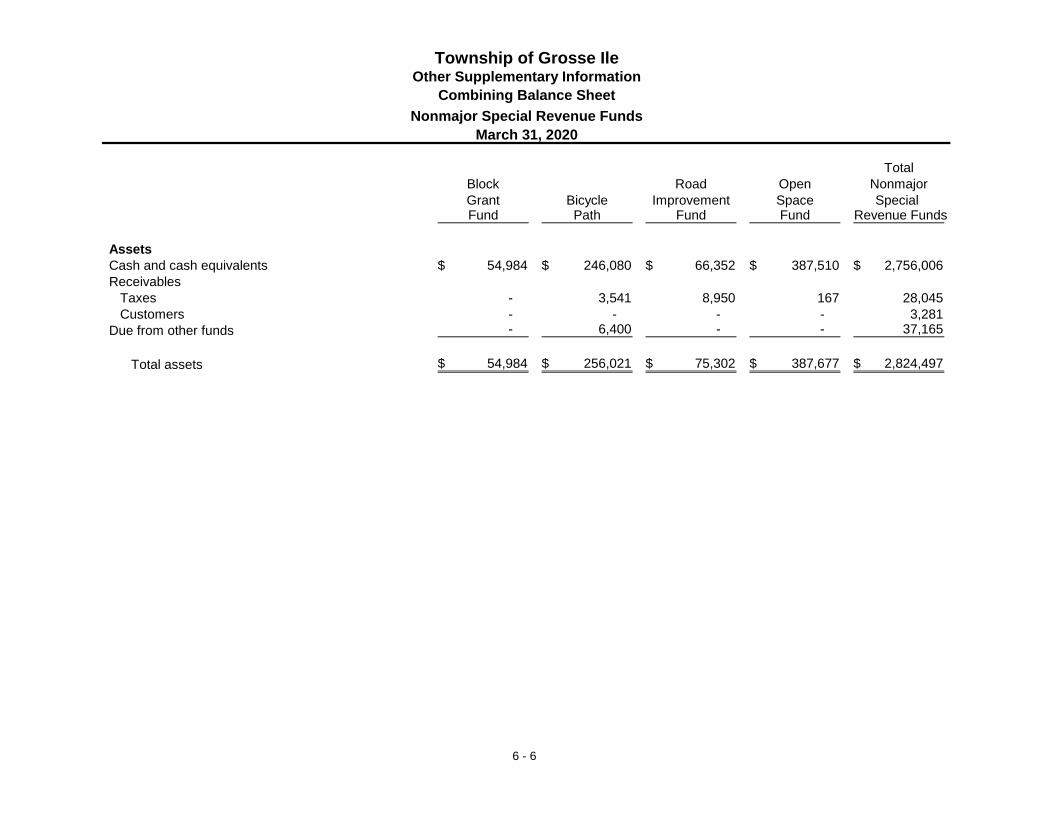

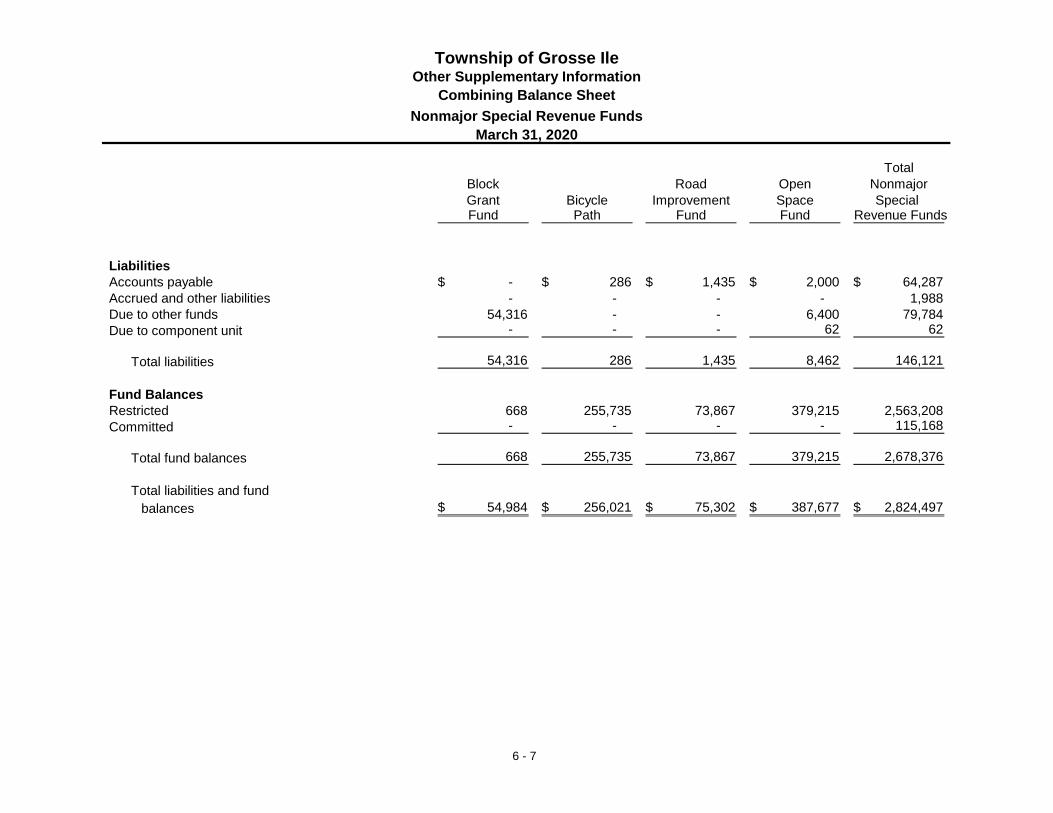

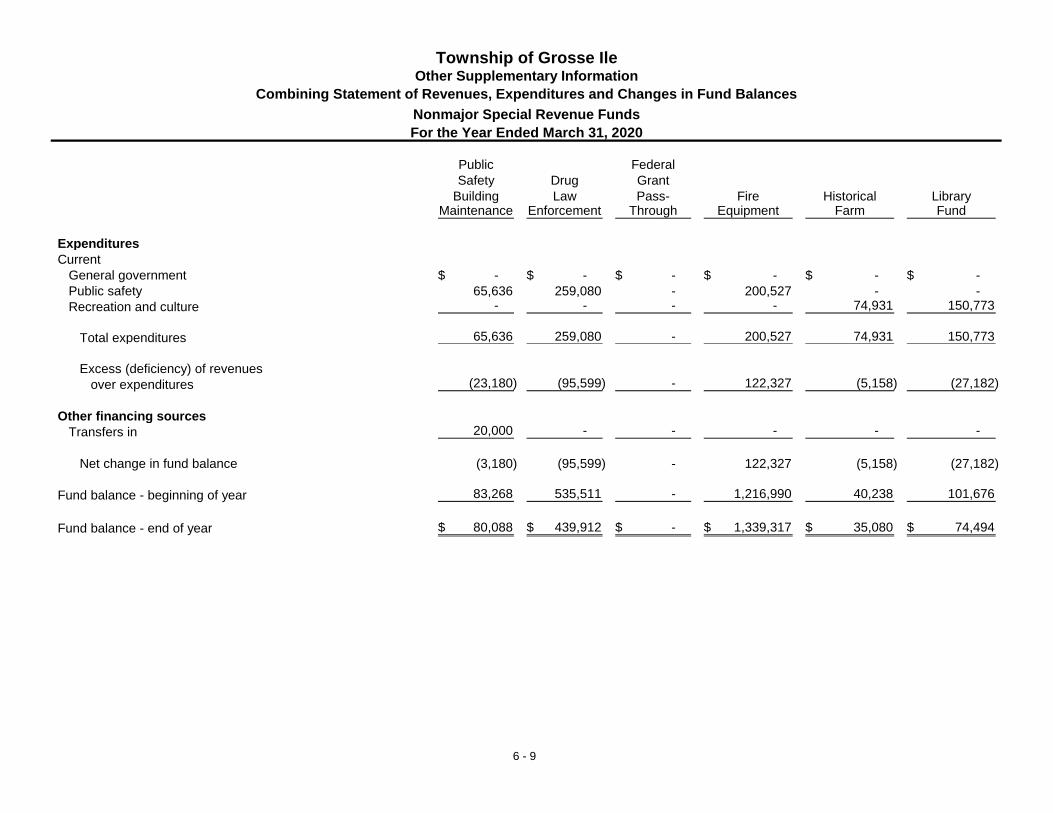

6 Other Supplementary Information Nonmajor Governmental Funds Combining Balance Sheet 6 – 1 Combining Statement of Revenue, Expenditures and Changes in Fund Balance 6 – 2 Nonmajor Special Revenue Funds Combining Balance Sheet 6 – 4 Combining Statement of Revenue, Expenditures and Changes in Fund Balance

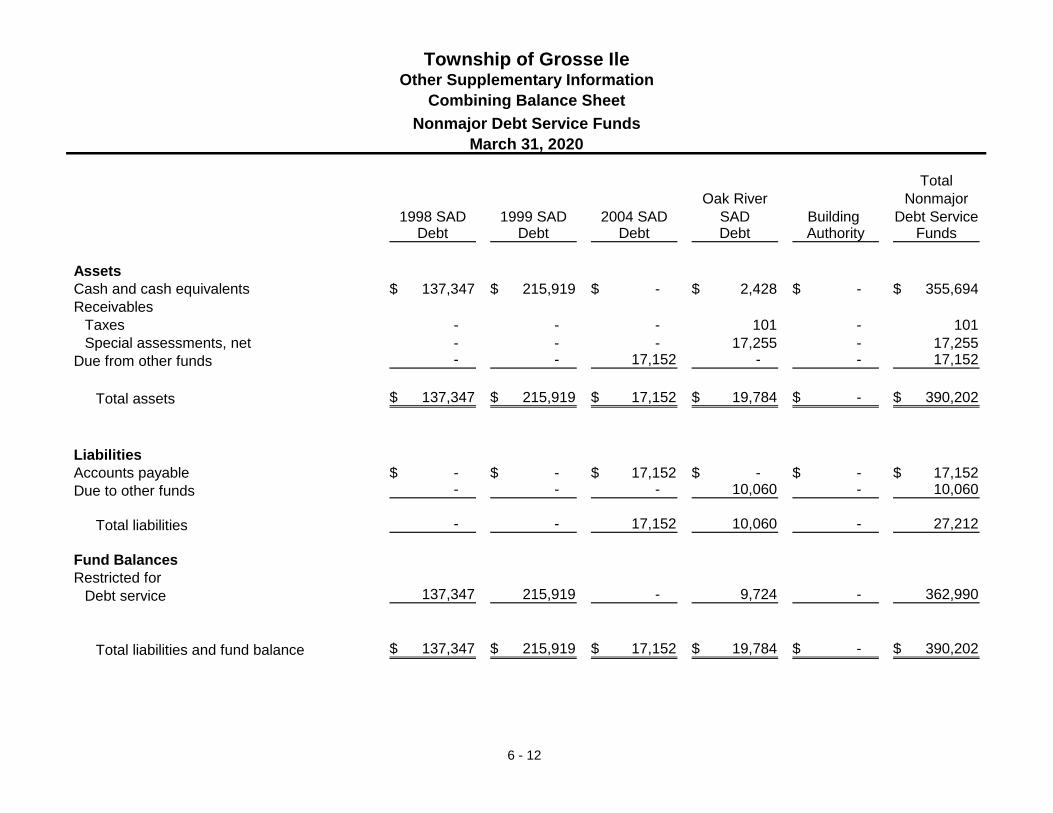

Nonmajor Debt Service Funds Combining Balance Sheet Combining Statement of Revenue, Expenditures and Changes in Fund Balance

6 – 8

6 – 12 6 – 13

1 - 1

Township of Grosse Ile List of Elected and Appointed Officials

March 31, 2020

Board of Trustees

Brian Loftus – Supervisor

Ute O’Connor – Township Clerk

Ted Van Os – Treasurer

James Budny – Trustee

Thomas Malvesto – Trustee

Carl Bloetscher – Trustee

James Nelson – Trustee

2 - 1

Independent Auditors’ Report

Board of Trustees Township of Grosse Ile Grosse Ile, Michigan

Report on the Financial Statements

We have audited the accompanying financial statements of the governmental activities, the business-type activities, the aggregate discretely presented component units, each major fund, and the aggregate remaining fund information of the Township of Grosse Ile, as of and for the year ended March 31, 2020, and the related notes to the financial statements, which collectively comprise the Township’s basic financial statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditors’ Responsibility

Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors’ judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

2 - 2

Opinions

In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, the business-type activities, the aggregate discretely presented component units, each major fund, and the aggregate remaining fund information of the Township of Grosse Ile, as of March 31, 2020, and the respective changes in financial position, and, where applicable, cash flows thereof for the year then ended in accordance with accounting principles generally accepted in the United States of America.

Other Matters

Required Supplementary Information

Accounting principles generally accepted in the United States of America require that the management’s discussion and analysis, budgetary comparison information, municipal employees’ retirement system schedules, and other post-employment benefit schedules, as identified in the table of contents, be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information, because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

Other Supplementary Information

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the Township of Grosse Ile’s basic financial statements. The other supplementary information, as identified in the table of contents, is presented for purposes of additional analysis and is not a required part of the basic financial statements.

The other supplementary information, as identified in the table of contents, is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the basic financial statements. The other supplementary information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the other supplementary information, as identified in the table of contents, is fairly stated, in all material respects, in relation to the basic financial statements as a whole.

Ann Arbor, MI September 28, 2020

Township of Grosse Ile Management’s Discussion and Analysis

March 31, 2020

3 - 1

Our discussion and analysis of the Township of Grosse Ile’s (the “Township”) financial performance provides an overview of the Township’s financial activities for the fiscal year ended March 31, 2020. Please read it in conjunction with the Township’s financial statements. Financial Highlights As discussed in further detail in this discussion and analysis, the following represents the most significant financial highlights for the year ended March 31, 2020:

• State-shared revenue, our second largest revenue source from governmental activities, was increased by the State of Michigan by $46,585 this year, which represents a 5.00% increase from the prior year. During the year, the Township has complied with each component of the State of Michigan’s Transparency and Accountability Initiative Program to preserve the Township’s portion of statutory revenue sharing .

• Property taxes are the Township’s single largest source of revenue. The Township’s taxable value for fiscal year 2019/2020 was $623,346,850 which represents an increase of $17,059,283, or 2.81%.

• During the current fiscal year, building permit revenue decreased by $99,392, which still included 12 new construction permits with an estimated value of $5,186,206. Covid-19 closed the Township in March for several months.

• In February 2020 the Township received $317,635 from Wayne County for the improvements of West River Road from Grosse Ile Parkway to Church Road.

• In 2019/2020 the Recreation Department paid off two separate loans that were previously borrowed internally from the General Fund for capital improvements.

• On October 2019, the Township purchased 1.82 acres of vacant land to preserve as Open Space in the amount of $92,187.

• On December 18, 2019 the Township issued Capital Improvement Bonds in the amount of $6,000,000 for watermain replacements on Parklane and Meridian and major improvements at the Waste Water Treatment Plant. In 2019/2020 the Township spent $1,700,000 to date on these projects.

• In 2019/2020 the Township loaned the Municipal Airport and Commerce Park $860,000 at 3.5% for 18 years for capital improvements. The Municipal Airport and Commerce Park spent over $1,000,000 to date on these projects. The renovations have resulted in tenant occupancy are revitalization.

• In 2019/2020, Township wide pension costs increased by $62,226 or 4.9% and health care costs decreased by $14,590 or 1%, however, unfunded liabilities continue to fluctuate annually due to actuarily calculations and assumptions and extreme changes in interest rates. The Township of Grosse Ile will continue to monitor these two major areas.

Township of Grosse Ile Management’s Discussion and Analysis

March 31, 2020

3 - 2

Using this Annual Report This annual report consists of a series of financial statements. The Statement of Net Position and the Statement of Activities provide information about the activities of the Township as a whole and present a longer-term view of the Township’s finances. This longer-term view uses the accrual basis of accounting so that it can measure the cost of providing services during the current year, and whether the taxpayers have funded the full cost of providing government services. The fund financial statements present a short-term view; they tell us how the taxpayers’ resources were spent during the year, as well as how much is available for future spending. Fund financial statements also report the Township’s operations in more detail than the government-wide financial statements by providing information about the Township’s most significant funds. The fiduciary fund statements provide financial information about activities for which the Township acts solely as a trustee or agent for the benefit of those outside of the government.

Township of Grosse Ile Management’s Discussion and Analysis

March 31, 2020

3 - 3

The Township as a Whole The following table shows, in condensed format, the net position as of March 31, 2020 and 2019 (in thousands of dollars):

Governmental Activities Business-type Activities Total

2020 2019 2020 2019 2020 2019

Assets

Current assets 7,276$ 7,619$ 6,831$ 7,205$ 14,107$ 14,824$

Noncurrent Assets 33,425 33,958 86,156 80,980 119,581 114,938

40,701 41,577 92,987 88,185 133,688 129,762

Deferred outflows of resources 1,314 1,906 174 247 1,488 2,153

Total assets and deferred outflows of resources 42,015 43,483 93,161 88,432 135,176 131,915

Liabilities

Current liabilities 296 306 664 610 960 916

Long-term liabilities 28,082 27,389 34,340 31,355 62,422 58,744

Total liabilities 28,378 27,695 35,004 31,965 63,382 59,660

Deferred inflows of resources 3,930 5,628 675 935 4,605 6,563

Total liabilities and deferred inflows of resources 32,308 33,323 35,679 32,900 67,987 66,223

Net assets

Net investment in -

capital assets 32,325 32,589 55,784 52,165 88,109 84,754

Restricted 4,612 3,444 - 1,287 4,612 4,731

Unrestricted (deficit) (27,230) (25,873) 1,698 2,080 (25,532) (23,793)

Total net position 9,707$ 10,160$ 57,482$ 55,532$ 67,189$ 65,692$

The Township has combined net position of $67.1 million. Business-type activities comprise $57.4 million of the total net position.

Township of Grosse Ile Management’s Discussion and Analysis

March 31, 2020

3 - 4

The following table shows the changes of the net position during the years ended March 31, 2020 and 2019 (in thousands of dollars):

2020 2019 2020 2019 2020 2019

Revenue

Program revenue

Charges for services 1,846$ 1,932$ 6,468$ 6,452$ 8,314$ 8,384$

Capital grants and contributions - - 690 6,239 690 6,239

Operating grants and contributions 204 402 - - 204 402

General revenue

Property taxes 6,073 5,904 3,178 3,389 9,251 9,293

State-shared revenue 977 930 - - 977 930

Unrestricted investment earnings 153 185 101 120 254 305

Gain on sale of capital assets 2 - 1 5 3 5

Miscellaneous - - 106 25 106 25

Total revenue 9,255 9,353 10,544 16,230 19,799 25,583

Program expenses

General government 3,096 3,398 - - 3,096 3,398

Public safety 5,209 5,322 - - 5,209 5,322

Public works - - 7,259 7,121 7,259 7,121

Municipal airport and commerce park - - 1,336 1,240 1,336 1,240

Recreation and culture 1,354 1,339 - - 1,354 1,339

Interest on long-term debt 49 60 - - 49 60

Total program expenses 9,708 10,119 8,595 8,361 18,303 18,480

Change in net position (453)$ (766)$ 1,949$ 7,869$ 1,496$ 7,103$

Governmental Activities Business-type Activities Total

Governmental Activities The Township’s total governmental revenues decreased by approximately $125,148. Property taxes increased in the amount of $168,478, and an overall increase in taxable value of 2.81%. Licenses and Permits decreased in the amount of $99,392, including 12 new construction permits as compared to 9 in the previous year. However, there has been decreased activity with remodeling and home improvement permits. Interest income continues to decrease slowly in the amount of $32,231 due to economic downturn and an overall decline in rate of return of investments. Federal, State and County funding sources decreased by $96,090 due to less participating and activity. Several other sources of revenue have either increased slightly or stayed the same from the prior year including State-Shared Revenue. State-Shared Revenue increased $46,585. Expenses decreased by $499,851 during the year. This decrease, which represents 5%, was due primarily to decreased purchases and construction

Township of Grosse Ile Management’s Discussion and Analysis

March 31, 2020

3 - 5

of capital assets in the current year than in the prior year. Last year, the Drainage Fund expended $517,534 for drainage improvements along West River Road. Last year as well, the Township purchased 30.083 acres of vacant land to preserve as Open Space in the amount of $304,365. Health care costs decreased $14,590 due to the restructuring of the employee’s healthcare benefits. Pension costs increased $62,226 or 4.9% due to additional normal funding requirements. The Township continues to take a conservative effort to reduce spending in all areas. Business-Type Activities The Township’s business-type activities consist of the Department of Public Works and the Municipal Airport and Commerce Park. The Department of Public Works Fund provides water to residents from the Detroit Water System. The Township provides sewage treatment through a Township-owned sewage treatment plant. Refuse collection and recycling services are provided by an outside commercial entity. The operating revenue of the Department of Public Works’ fund decreased by $ 94,328 or 1.7%. The Township imposed a 0% rate increase for water usage and a 15.6% rate increase for sewer usage, even though the Township received a 1.6% increase from the Great Lakes Water Authority for the fiscal year. Water usage was down over the past year. Therefore, in the future, water and sewer rates need to be continuously adjusted on an annual basis to absorb the increase from the Great Lakes Water Authority to pay for current and future capital improvement infrastructure needs. The operating expenses increased by $88,771 or 1.4% due to increasing water costs, increased repairs needed at the waste water treatment plant, and additional water main repairs. The current fiscal year resulted in an overall operating net loss of $868,260, as compared to the prior fiscal year loss of $685,161. Furthermore, the Department of Public Works will continue to make a conservative effort to reduce spending. The Municipal Airport and Commerce Park is used to account for the airport operations and the Commerce Park complex. The operating revenue for this fund increased by $110,423 or 13.77%. The increase resulted from major capital renovation improvements that attracted new tenants to the industrial park area. The Municipal Airport and Commerce Park Commission adjusts rents annually with CPI rate increases and tries to secure additional revenue generated by non-airport related activities such as commercial television shoots. The operating expenses increased by $90,227 or 7.3%. The increase was due to the recognition of future related pension and healthcare obligations, and an increase in depreciation expense associated with the additional capital improvements, furthermore, a conservative approach to reduce Airport related spending has been taken through minimal staffing. The operating loss was $417,564, less than the previous fiscal year loss of $437,761. The Township Funds Our analysis of the Township’s major funds begins on page 4 - 4, following the government-wide financial statements. The fund financial statements provide detail information about the most significant funds, not the Township as a whole. The Township Board creates funds to help manage money for specific purposes as well as to show accountability for certain activities, such as special property tax millages. The Township's major funds for 2020 include the General Fund, the Recreation Fund, the Fire Operating Fund, and the Drain and Storm Maintenance Fund. The General Fund pays for most of the Township’s governmental services. The most significant are general administration and police operations, which incurred expenses of approximately $2.1688 and $3.432 million, respectively, in the current year. The budget in the General Fund is basically a “maintenance” budget, which means it increases modestly from year to year.

Township of Grosse Ile Management’s Discussion and Analysis

March 31, 2020

3 - 6

General Fund Budgetary Highlights Over the course of the year, the Township did not amend the budget. The Township Board’s policy regarding the budget is to avoid making adjustments during the year so that the budget can be used as a financial guide to make financial decisions, and to analyze and maintain the validity of the budget document. As a result, the actual revenues and expenses are usually within 10% of budgeted amounts. Overall, the Township departments were above the original budget amounts, resulting in total revenues less expenditures and transfers of $12,845 under the budgeted amount of $0 for operations. Capital Asset and Debt Administration As of March 31, 2020, the Township had approximately $114.4 million (net of depreciation) invested in a broad range of capital assets, including land, buildings, bike paths, roads, equipment, and water and sewer lines. Major capital improvements for the fiscal year included the purchase of public safety vehicles, police and fire equipment, various road repairs located township-wide, several major improvements to the Waste Water Treatment Plant and the continuation of water and sanitary sewer main replacements. Other capital improvements include various computer and equipment purchases by all departments. Economic Factors and Next Year’s Budgets and Rates Due to the extreme economic conditions that every local community is currently facing, the Township’s 2020-2021 budget was prepared with the following criteria. First, operating millage revenues increased slightly from the prior year with an estimated increase in taxable value of approximately 2.6% due to the slow recovery of the economy, however, stabling out in the future. The statewide Tax Reform Act limits growth in taxable value on any individual property to the lesser of inflation or 5%. Because of the impact of Proposal A, however, the Township needs to continue to watch its budget very closely. Further, the Township incorporated state-shared revenue to increase by 3%, a 3% increase in all employee health insurance premiums, and a 10% increase in liability insurance premiums, as well as, a variable increase for employee pension costs as determined by MERS. Employee wages increased by 1.013 for administrative personnel, 1.75% for police personnel employees, and 1.5% for those general employees who were under an existing union contract. By limiting other categories of discretionary spending and revisiting how certain services are delivered, the Township was able to adopt a balanced budget for the 2020-2021 fiscal year without using prior year resources for the General Fund. As of September 2020, water rates increased by 3.5% and sewer fixed charges increased 8.0% to provide for future bonding of major wastewater treatment capital improvements. Refuse rates remained the same to reflect actual costs. Rates need to be continuously raised and monitored to maintain operations and continue capital improvements with increases as stated above, most of which is driven by the State of Michigan unfunded mandates.

Township of Grosse Ile Management’s Discussion and Analysis

March 31, 2020

3 - 7

Contacting the Township’s Management

This financial report is intended to provide our citizens, taxpayers, customers, and investors with a general overview of the Township’s finances and to show the Township’s accountability for the money it receives. If you have questions about this report or need additional information, we welcome you to contact the Finance Department.

Governmental Business-type ComponentActivities Activities Total Units

Assets

Cash and cash equivalents 5,524,744$ 5,943,246$ 11,467,990$ 369,400$

Receivables

Taxes 222,304 73,507 295,811 -

Customers 118,357 1,528,256 1,646,613 -

Special assessments 17,255 - 17,255 -

Due from other units of government 157,757 317,635 475,392 1,126

Due from fiduciary funds - - - 105,841

Internal balances 1,162,663 (1,162,663) - -

Due from component unit 325 - 325 -

Inventories 4,399 131,039 135,438 -

Prepaid items 68,750 - 68,750 -

Restricted assets

Cash and cash equivalents - 5,224,210 5,224,210 -

Capital assets not being depreciated 14,255,660 7,487,835 21,743,495 507,558

Capital assets, net of accumulated depreciation 19,169,415 73,443,855 92,613,270 766,862

Total assets 40,701,629 92,986,920 133,688,549 1,750,787

Deferred Outflows of Resources

Deferred amount relating to net pension liability 1,203,710 156,260 1,359,970 -

Deferred amount relating to net OPEB liability 109,289 17,987 127,276 -

Total deferred outflows of resources 1,312,999 174,247 1,487,246 -

Township of Grosse IleStatement of Net Position

March 31, 2020

Primary Government

See Accompanying Notes to the Financial Statements

4 - 1

Governmental Business-type ComponentActivities Activities Total Units

Township of Grosse IleStatement of Net Position

March 31, 2020

Primary Government

Liabilities

Accounts payable 175,653$ 297,683$ 473,336$ 7,872$

Accrued and other liabilities 102,183 280,257 382,440 1,251

Due to component unit 62 - 62 -

Due to other units of government - - - 325

Unearned revenue 18,030 56,771 74,801 -

Customer deposits - 29,282 29,282 -

Noncurrent liabilities

Debt due within one year 250,125 3,561,652 3,811,777 -

Debt due in more than one year 1,318,203 26,841,890 28,160,093 -

Net pension liability 13,656,749 1,772,862 15,429,611 -

Net OPEB liability 12,856,699 2,163,881 15,020,580 -

Total liabilities 28,377,704 35,004,278 63,381,982 9,448

Deferred Inflows of Resources

Deferred amount relating to net OPEB liability 3,929,597 674,795 4,604,392 -

Net Position

Net investment in capital assets 32,325,075 55,784,064 88,109,139 1,274,420

Restricted for

Debt service 342,245 - 342,245 -

Other purposes 4,269,803 - 4,269,803 -

Unrestricted (deficit) (27,229,796) 1,698,030 (25,531,766) 466,919

Total net position 9,707,327$ 57,482,094$ 67,189,421$ 1,741,339$

See Accompanying Notes to the Financial Statements

4 - 2

Operating Capital

Charges for Grants and Grants and Governmental Business-type Component

Expenses Services Contributions Contributions Activities Activities Total Units

Functions/Programs

Primary government

Governmental activities

General government 3,095,900$ 986,082$ -$ -$ (2,109,818)$ -$ (2,109,818)$ -$

Public safety 5,208,915 311,274 159,647 - (4,737,994) - (4,737,994) -

Recreation and culture 1,354,308 549,084 44,415 - (760,809) - (760,809) -

Interest and fiscal charges on long-

term debt 49,313 - - - (49,313) - (49,313) -

Total governmental activities 9,708,436 1,846,440 204,062 - (7,657,934) - (7,657,934) -

Business-type activities

Department of public works 7,258,641 5,556,163 - 317,635 - (1,384,843) (1,384,843) -

Municipal airport and commerce park 1,335,752 912,188 - 372,400 - (51,164) (51,164) -

Total business-type activities 8,594,393 6,468,351 - 690,035 - (1,436,007) (1,436,007) -

Total primary government 18,302,829$ 8,314,791$ 204,062$ 690,035$ (7,657,934) (1,436,007) (9,093,941) -

Component unit

Brownfield Authority 200$ -$ -$ -$ - - - (200)

Downtown Development Authority 147,820 780 - - - - - (147,040)

Total component units 148,020$ 780$ -$ -$ - - - (147,240)

General revenues

Property taxes 6,072,800 3,177,608 9,250,408 159,365

State-shared revenue 977,049 - 977,049 -

Unrestricted investment earnings 152,812 100,570 253,382 5,209

Gain on sale of capital assets 2,455 950 3,405 -

Miscellaneous - 106,300 106,300 -

7,205,116 3,385,428 10,590,544 164,574

Change in net position (452,818) 1,949,421 1,496,603 17,334

Net position - beginning of year 10,160,145 55,532,673 65,692,818 1,724,005

Net position - end of year 9,707,327$ 57,482,094$ 67,189,421$ 1,741,339$

Total general revenues

Program Revenues Changes in Net Position

Primary Government

Township of Grosse IleStatement of Activities

For the Year Ended March 31, 2020

Net (Expense) Revenue and

See Accompanying Notes to the Financial Statements

4 - 3

Fire Drain and Nonmajor Total

Recreation Operating Storm Governmental GovernmentalGeneral Fund Fund Maintenance Funds Funds

Assets

Cash and cash equivalents 930,520$ 144,098$ 528,985$ 809,441$ 3,111,700$ 5,524,744$

Receivables

Taxes 133,732 19,475 33,579 7,372 28,146 222,304

Customers 101,908 3,523 9,645 - 3,281 118,357

Special assessments - - - - 17,255 17,255

Due from other units of government 157,757 - - - - 157,757

Due from other funds 79,419 50,991 - - 54,317 184,727

Due from component unit 325 - - - - 325

Inventories 2,182 730 1,487 - - 4,399

Prepaid items 60,000 3,750 5,000 - - 68,750

Advances to other funds 1,132,603 - - - - 1,132,603

Total assets 2,598,446$ 222,567$ 578,696$ 816,813$ 3,214,699$ 7,431,221$

Special Revenue Funds

Township of Grosse IleGovernmental Funds

Balance SheetMarch 31, 2020

See Accompanying Notes to the Financial Statements

4 - 4

Fire Drain and Nonmajor Total

Recreation Operating Storm Governmental GovernmentalGeneral Fund Fund Maintenance Funds Funds

Special Revenue Funds

Township of Grosse IleGovernmental Funds

Balance SheetMarch 31, 2020

Liabilities

Accounts payable 61,454$ 5,154$ 27,606$ -$ 81,439$ 175,653$

Accrued and other liabilities 61,978 9,279 8,193 - 1,988 81,438

Due to other funds 41,123 7,682 16,018 - 89,844 154,667

Due to component unit - - - - 62 62

Unearned revenue - 18,030 - - - 18,030

Total liabilities 164,555 40,145 51,817 - 173,333 429,850

Fund Balances

Non-spendable

Inventories 2,182 730 1,487 - - 4,399

Prepaid items 60,000 3,750 5,000 - - 68,750

Restricted for

Recreation - 177,942 - - - 177,942

Fire operating - - 520,392 - - 520,392

Drain and storm maintenance - - - 816,813 - 816,813

Other special revenue funds - - - - 2,563,208 2,563,208

Debt service - - - - 362,990 362,990

Construction code fees 362,903 - - - - 362,903

Committed - - - - 115,168 115,168

Unassigned 2,008,806 - - - - 2,008,806

Total fund balances 2,433,891 182,422 526,879 816,813 3,041,366 7,001,371

Total liabilities and fund balances 2,598,446$ 222,567$ 578,696$ 816,813$ 3,214,699$ 7,431,221$

See Accompanying Notes to the Financial Statements

4 - 5

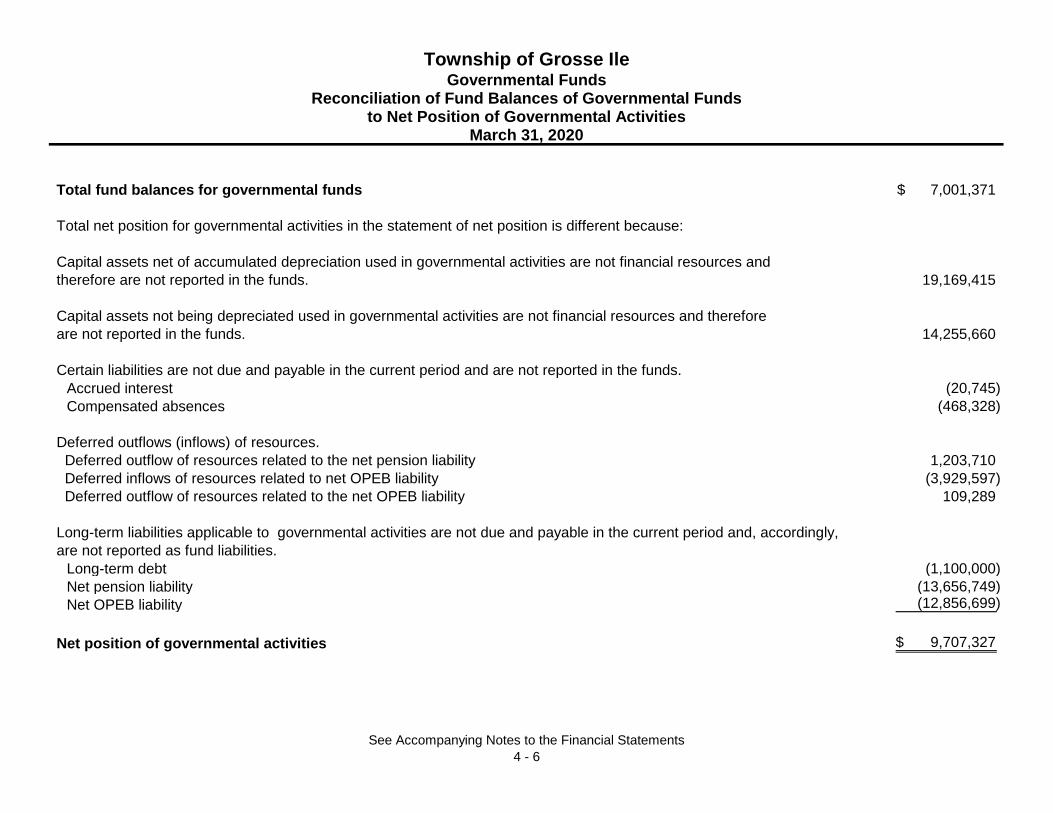

Total fund balances for governmental funds 7,001,371$

Total net position for governmental activities in the statement of net position is different because:

Capital assets net of accumulated depreciation used in governmental activities are not financial resources and

therefore are not reported in the funds. 19,169,415

Capital assets not being depreciated used in governmental activities are not financial resources and therefore

are not reported in the funds. 14,255,660

Certain liabilities are not due and payable in the current period and are not reported in the funds.

Accrued interest (20,745)

Compensated absences (468,328)

Deferred outflows (inflows) of resources.

Deferred outflow of resources related to the net pension liability 1,203,710

Deferred inflows of resources related to net OPEB liability (3,929,597)

Deferred outflow of resources related to the net OPEB liability 109,289

Long-term liabilities applicable to governmental activities are not due and payable in the current period and, accordingly,

are not reported as fund liabilities.

Long-term debt (1,100,000)

Net pension liability (13,656,749)

Net OPEB liability (12,856,699)

Net position of governmental activities 9,707,327$

Township of Grosse Ile

Reconciliation of Fund Balances of Governmental Fundsto Net Position of Governmental Activities

March 31, 2020

Governmental Funds

See Accompanying Notes to the Financial Statements

4 - 6

Fire Drain and Nonmajor Total

Recreation Operating Storm Governmental GovernmentalGeneral Fund Fund Maintenance Funds Funds

Revenues

Taxes 3,652,994$ 535,303$ 917,242$ 202,316$ 764,945$ 6,072,800$

Licenses and permits 729,807 - - - - 729,807

Federal grants - - - - 196,668 196,668

State-shared revenue 977,049 - - - - 977,049

Other state grants 5,921 - - - 750 6,671

Charges for services - 347,056 - - - 347,056

Ambulance fees - - 185,454 - - 185,454

Fines and forfeitures 83,913 - - - - 83,913

Interest income 96,988 - 1,364 9,480 44,980 152,812

Rental income - 49,867 - - 111,513 161,380

Other revenue 267,937 82,555 - - 723 351,215

Total revenues 5,814,609 1,014,781 1,104,060 211,796 1,119,579 9,264,825

Special Revenue Funds

Township of Grosse Ile

Governmental Funds

Statement of Revenues, Expenditures and Changes in Fund Balances

For the Year Ended March 31, 2020

See Accompanying Notes to the Financial Statements

4 - 7

Fire Drain and Nonmajor Total

Recreation Operating Storm Governmental GovernmentalGeneral Fund Fund Maintenance Funds Funds

Special Revenue Funds

Township of Grosse Ile

Governmental Funds

Statement of Revenues, Expenditures and Changes in Fund Balances

For the Year Ended March 31, 2020

Expenditures

Current

General government 2,092,271$ -$ -$ 141,202$ 645,797$ 2,879,270$

Public safety 3,432,173 - 1,131,246 - 525,243 5,088,662

33rd District Court 75,906 - - - - 75,906

Recreation and culture - 965,870 - - 269,575 1,235,445

Debt service

Principal retirement - 28,967 - - 240,000 268,967

Interest and fiscal charges - 579 - - 53,555 54,134

Total expenditures 5,600,350 995,416 1,131,246 141,202 1,734,170 9,602,384

Excess (deficiency) of revenues over expenditures 214,259 19,365 (27,186) 70,594 (614,591) (337,559)

Other financing sources (uses)

Transfers in 76,743 - - - 288,157 364,900

Transfers out (278,157) - (86,743) - - (364,900)

Total other financing sources and uses (201,414) - (86,743) - 288,157 -

Net change in fund balance 12,845 19,365 (113,929) 70,594 (326,434) (337,559)

Fund balance - beginning of year 2,421,046 163,057 640,808 746,219 3,367,800 7,338,930

Fund balance - end of year 2,433,891$ 182,422$ 526,879$ 816,813$ 3,041,366$ 7,001,371$

See Accompanying Notes to the Financial Statements

4 - 8

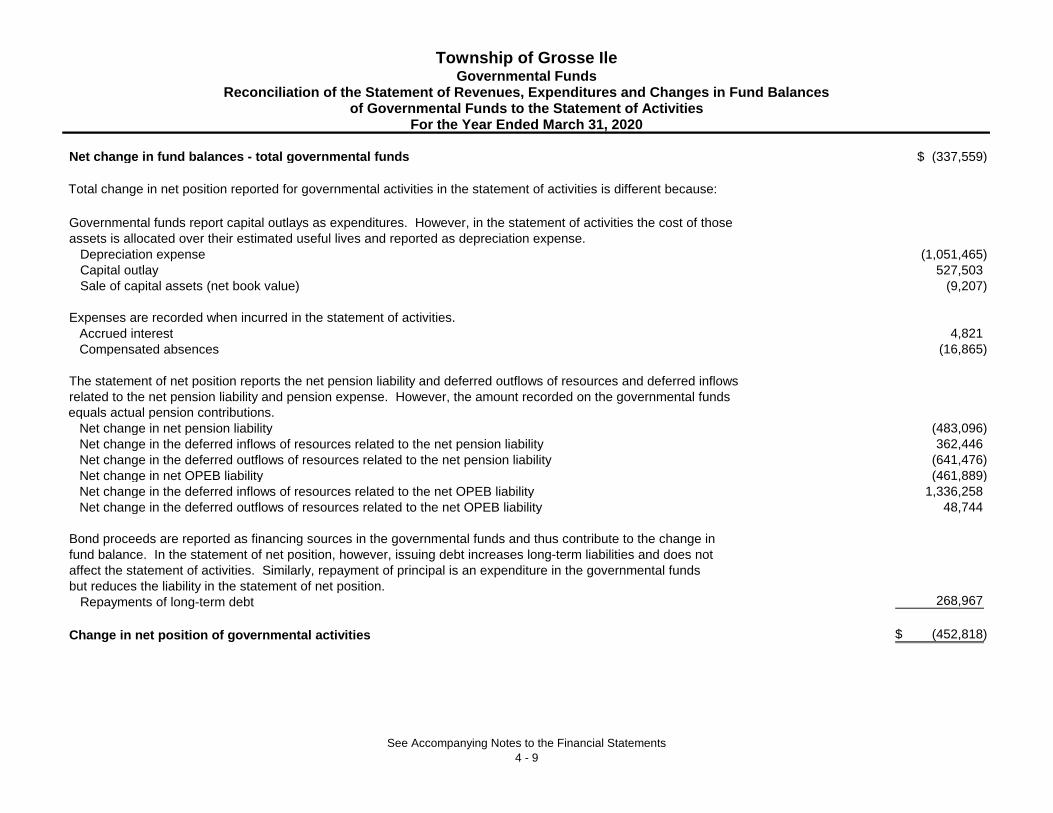

Net change in fund balances - total governmental funds (337,559)$

Governmental funds report capital outlays as expenditures. However, in the statement of activities the cost of those

assets is allocated over their estimated useful lives and reported as depreciation expense.

Depreciation expense (1,051,465)

Capital outlay 527,503

Sale of capital assets (net book value) (9,207)

Expenses are recorded when incurred in the statement of activities.

Accrued interest 4,821

Compensated absences (16,865)

The statement of net position reports the net pension liability and deferred outflows of resources and deferred inflows

related to the net pension liability and pension expense. However, the amount recorded on the governmental funds

equals actual pension contributions.

Net change in net pension liability (483,096)

Net change in the deferred inflows of resources related to the net pension liability 362,446

Net change in the deferred outflows of resources related to the net pension liability (641,476)

Net change in net OPEB liability (461,889)

Net change in the deferred inflows of resources related to the net OPEB liability 1,336,258

Net change in the deferred outflows of resources related to the net OPEB liability 48,744

Bond proceeds are reported as financing sources in the governmental funds and thus contribute to the change in

fund balance. In the statement of net position, however, issuing debt increases long-term liabilities and does not

affect the statement of activities. Similarly, repayment of principal is an expenditure in the governmental funds

but reduces the liability in the statement of net position.

Repayments of long-term debt 268,967

Change in net position of governmental activities (452,818)$

Total change in net position reported for governmental activities in the statement of activities is different because:

For the Year Ended March 31, 2020

Township of Grosse IleGovernmental Funds

Reconciliation of the Statement of Revenues, Expenditures and Changes in Fund Balancesof Governmental Funds to the Statement of Activities

See Accompanying Notes to the Financial Statements

4 - 9

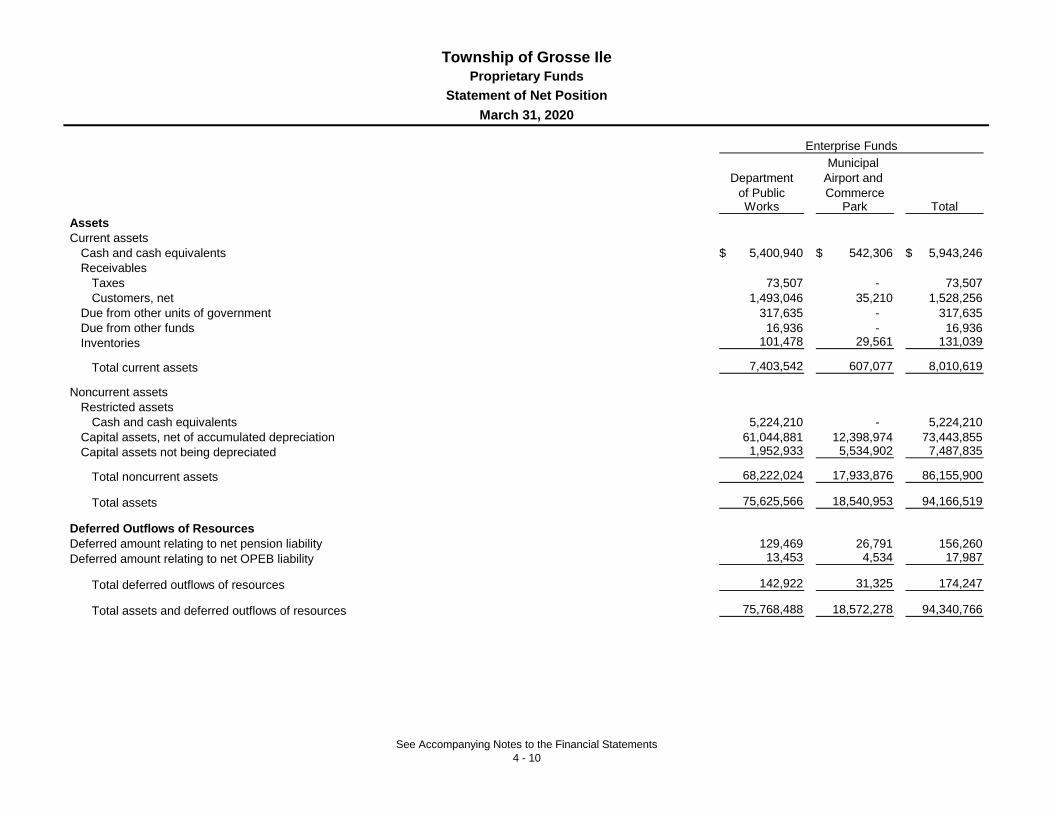

Municipal

Department Airport and

of Public CommerceWorks Park Total

Assets

Current assets

Cash and cash equivalents 5,400,940$ 542,306$ 5,943,246$

Receivables

Taxes 73,507 - 73,507

Customers, net 1,493,046 35,210 1,528,256

Due from other units of government 317,635 - 317,635

Due from other funds 16,936 - 16,936

Inventories 101,478 29,561 131,039

Total current assets 7,403,542 607,077 8,010,619

Noncurrent assets

Restricted assets

Cash and cash equivalents 5,224,210 - 5,224,210

Capital assets, net of accumulated depreciation 61,044,881 12,398,974 73,443,855

Capital assets not being depreciated 1,952,933 5,534,902 7,487,835

Total noncurrent assets 68,222,024 17,933,876 86,155,900

Total assets 75,625,566 18,540,953 94,166,519

Deferred Outflows of Resources

Deferred amount relating to net pension liability 129,469 26,791 156,260

Deferred amount relating to net OPEB liability 13,453 4,534 17,987

Total deferred outflows of resources 142,922 31,325 174,247

Total assets and deferred outflows of resources 75,768,488 18,572,278 94,340,766

Enterprise Funds

Township of Grosse Ile

Proprietary Funds

Statement of Net Position

March 31, 2020

See Accompanying Notes to the Financial Statements

4 - 10

Municipal

Department Airport and

of Public CommerceWorks Park Total

Enterprise Funds

Township of Grosse Ile

Proprietary Funds

Statement of Net Position

March 31, 2020

Liabilities

Current liabilities

Accounts payable 246,402$ 51,281$ 297,683$

Accrued and other liabilities 276,102 4,155 280,257

Due to other funds 24,182 22,814 46,996

Customer deposits - 29,282 29,282

Unearned revenue - 56,771 56,771

Current portion of noncurrent liabilities 3,541,769 19,883 3,561,652

Total current liabilities 4,088,455 184,186 4,272,641

Noncurrent liabilities

Advances from other funds - 1,132,603 1,132,603

Net pension liability 1,468,900 303,962 1,772,862

Net OPEB liability 1,609,780 554,101 2,163,881

Long-term debt net of current portion 26,841,890 - 26,841,890

Total noncurrent liabilities 29,920,570 1,990,666 31,911,236

Total liabilities 34,009,025 2,174,852 36,183,877

Deferred Inflows of Resources

Deferred amount relating to net OPEB liability 499,629 175,166 674,795

Net Position

Net investment in capital assets 37,850,188 17,933,876 55,784,064

Restricted for

Capital projects 5,224,210 - 5,224,210

Unrestricted (deficit) (1,814,564) (1,711,616) (3,526,180)

Total net position 41,259,834$ 16,222,260$ 57,482,094$

See Accompanying Notes to the Financial Statements

4 - 11

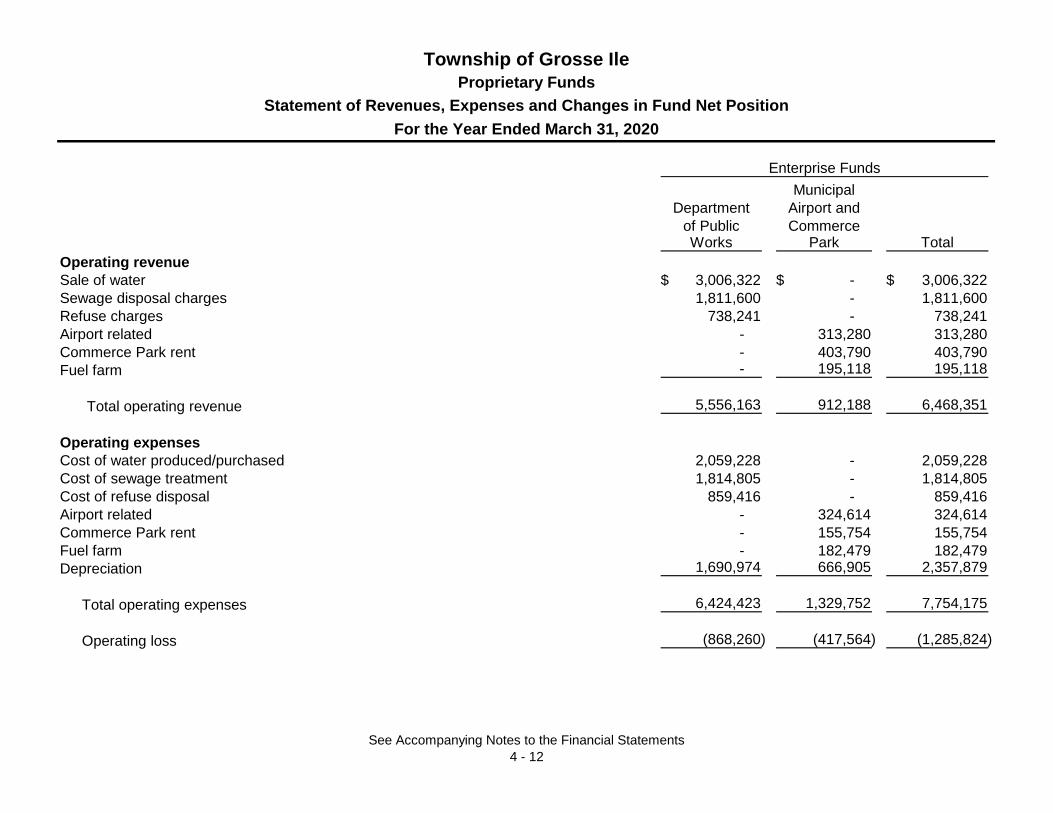

Municipal

Department Airport and

of Public CommerceWorks Park Total

Operating revenue

Sale of water 3,006,322$ -$ 3,006,322$

Sewage disposal charges 1,811,600 - 1,811,600

Refuse charges 738,241 - 738,241

Airport related - 313,280 313,280

Commerce Park rent - 403,790 403,790

Fuel farm - 195,118 195,118

Total operating revenue 5,556,163 912,188 6,468,351

Operating expenses

Cost of water produced/purchased 2,059,228 - 2,059,228

Cost of sewage treatment 1,814,805 - 1,814,805

Cost of refuse disposal 859,416 - 859,416

Airport related - 324,614 324,614

Commerce Park rent - 155,754 155,754

Fuel farm - 182,479 182,479

Depreciation 1,690,974 666,905 2,357,879

Total operating expenses 6,424,423 1,329,752 7,754,175

Operating loss (868,260) (417,564) (1,285,824)

Enterprise Funds

Township of Grosse Ile

Proprietary Funds

Statement of Revenues, Expenses and Changes in Fund Net Position

For the Year Ended March 31, 2020

See Accompanying Notes to the Financial Statements

4 - 12

Municipal

Department Airport and

of Public CommerceWorks Park Total

Enterprise Funds

Township of Grosse Ile

Proprietary Funds

Statement of Revenues, Expenses and Changes in Fund Net Position

For the Year Ended March 31, 2020

Nonoperating revenue (expenses)

Property taxes 3,177,608$ -$ 3,177,608$

Interest income 91,835 8,735 100,570

Gain on sale of assets 950 - 950

Insurance reimbursement - 81,979 81,979

Bond issuance costs (86,355) - (86,355)

Premium amortization 24,321 - 24,321

Interest expense (747,863) (6,000) (753,863)

Total nonoperating revenues (expenses) 2,460,496 84,714 2,545,210

Income (loss) before contributions 1,592,236 (332,850) 1,259,386

Capital contributions 317,635 372,400 690,035

Change in net position 1,909,871 39,550 1,949,421

Net position - beginning of year 39,349,963 16,182,710 55,532,673

Net position - end of year 41,259,834$ 16,222,260$ 57,482,094$

See Accompanying Notes to the Financial Statements

4 - 13

Municipal

Department Airport and

of Public CommerceWorks Park Total

Cash flows from operating activities

Receipts from customers 5,209,477$ 827,925$ 6,037,402$

Receipts from other funds 12,213 18,787 31,000

Payments to suppliers (2,545,667) (541,994) (3,087,661)

Payments to employees (2,063,109) (167,438) (2,230,547)

Net cash provided by operating activities 612,914 137,280 750,194

Cash flows from noncapital financing activities

Property taxes 3,178,876 - 3,178,876

Cash flows from capital and related financing activities

Proceeds from capital debt 6,000,000 - 6,000,000

Capital contributions 317,635 372,400 690,035

Advances from other funds - 832,601 832,601

Purchases/construction of capital assets (2,152,137) (1,452,714) (3,604,851)

Principal and interest paid on long-term debt (3,968,522) (6,000) (3,974,522)

Proceeds from sale of capital assets 950 - 950

Net cash provided (used) by capital and related financing activities 197,926 (253,713) (55,787)

Cash flows from investing activities

Proceeds from insurance - 81,979 81,979

Interest received 92,734 8,735 101,469

Net cash provided by investing activities 92,734 90,714 183,448

Net change in cash and cash equivalents 4,082,450 (25,719) 4,056,731

Cash and cash equivalents - beginning of year 6,542,700 568,025 7,110,725

Cash and cash equivalents - end of year 10,625,150$ 542,306$ 11,167,456$

Enterprise Funds

Township of Grosse Ile

Proprietary Funds

Statement of Cash Flows

For the Year Ended March 31, 2020

See Accompanying Notes to the Financial Statements

4 - 14

Municipal

Department Airport and

of Public CommerceWorks Park Total

Enterprise Funds

Township of Grosse Ile

Proprietary Funds

Statement of Cash Flows

For the Year Ended March 31, 2020

Reconciliation of operating income (loss) to net cash

provided by operating activities

Operating loss (868,260)$ (417,564)$ (1,285,824)$

Adjustments to reconcile operating income to net cash

from operating activities

Depreciation and amortization expense 1,690,974 666,905 2,357,879

Changes in assets and liabilities

Receivables (net) (29,051) (19,866) (48,917)

Due from other units of government (317,635) - (317,635)

Due from other funds (11,688) - (11,688)

Inventories - (11,549) (11,549)

Prepaid items 5,850 - 5,850

Deferred outflows of resources 58,330 14,814 73,144

Accounts payable 89,821 (3,727) 86,094

Accrued and other liabilities 31,465 931 32,396

Due to other funds 23,901 18,787 42,688

Deferred inflows of resources (198,720) (61,077) (259,797)

Other post employment benefits 55,540 18,156 73,696

Net pension liability 86,268 (6,757) 79,511

Unearned revenue - (72,047) (72,047)

Customer deposits payable - 7,650 7,650

Compensated absences (3,881) 2,624 (1,257)

Net cash provided by operating activities 612,914$ 137,280$ 750,194$

See Accompanying Notes to the Financial Statements

4 - 15

TaxGeneral Collection Total

Assets

Cash and cash equivalents 504,296$ 297,026$ 801,322$

Liabilities

Accrued and other liabilities 504,296 118,429 622,725

Due to component unit - 105,841 105,841

Due to other units of government - 72,756 72,756

Total liabilities 504,296$ 297,026$ 801,322$

Held in trust for pension benefits and other purposes

Agency Funds

Township of Grosse IleFiduciary Funds

Statement of Assets and LiabilitiesMarch 31, 2020

See Accompanying Notes to the Financial Statements

4 - 16

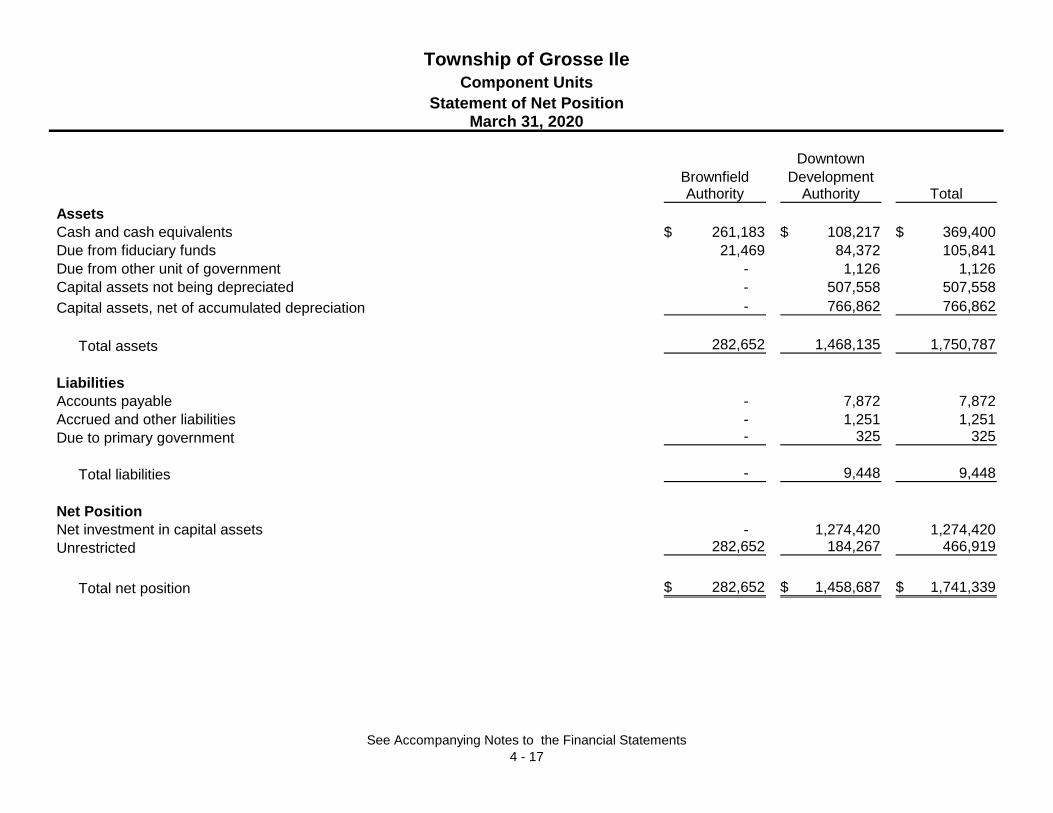

Downtown

Brownfield DevelopmentAuthority Authority Total

Assets

Cash and cash equivalents 261,183$ 108,217$ 369,400$

Due from fiduciary funds 21,469 84,372 105,841

Due from other unit of government - 1,126 1,126

Capital assets not being depreciated - 507,558 507,558

Capital assets, net of accumulated depreciation - 766,862 766,862

Total assets 282,652 1,468,135 1,750,787

Liabilities

Accounts payable - 7,872 7,872

Accrued and other liabilities - 1,251 1,251

Due to primary government - 325 325

Total liabilities - 9,448 9,448

Net Position

Net investment in capital assets - 1,274,420 1,274,420

Unrestricted 282,652 184,267 466,919

Total net position 282,652$ 1,458,687$ 1,741,339$

Township of Grosse Ile

Statement of Net PositionMarch 31, 2020

Component Units

See Accompanying Notes to the Financial Statements

4 - 17

Downtown

Charges for Brownfield Development

Expenses Services Authority Authority Total

Brownfield Authority

Community and economic development 200$ -$ (200)$ -$ (200)$

Downtown Development Authority

Community and economic development 147,820 780 - (147,040) (147,040)

Total component units 148,020$ 780$ (200) (147,040) (147,240)

General revenues

Property taxes 11,288 148,077 159,365

Unrestricted investment earnings 4,356 853 5,209

15,644 148,930 164,574

Change in net position 15,444 1,890 17,334

Net position - beginning of year 267,208 1,456,797 1,724,005

Net position - end of year 282,652$ 1,458,687$ 1,741,339$

Total general revenues

Component Units

Township of Grosse Ile

Statement of ActivitiesFor the Year Ended March 31, 2020

Net (Expense) Revenue and

Program Revenues Changes in Net Position

See Accompanying Notes to the Financial Statements

4 - 18

Township of Grosse Ile Notes to the Financial Statements

March 31, 2020

4 - 19

Note 1 - Summary of Significant Accounting Policies

The accounting policies of the Township of Grosse Ile (the “Township”) conform to accounting principles generally accepted in the United States of America (GAAP) as applicable to governmental units. The following is a summary of the significant accounting policies used by the Township: Reporting entity The Township operates as a General Law Township under the laws of the State of Michigan. The Township is governed by an elected seven-member Board. The accompanying financial statements present the Township and its component units, entities for which the Township is considered to be financially accountable. Although blended component units are legal separate entities, in substance, they are part of the Township’s operations. Each discretely presented component unit is reported in a separate column in the government-wide financial statements to emphasize that it is legally separate from the Township (see discussion below for description). Blended Component Units - The Grosse Ile Building Authority (the “Authority”) is composed of a three-member board appointed by the Township’s Board of Trustees. Although it is a separate legal entity from the Township, the Authority is reported as if it were a part of the primary government because its sole purpose is to finance and construct the Township’s public buildings. Discretely Presented Component Units - The Downtown Development Authority (the “Authority”) was created under Act No. 197 of the Michigan State statutes to correct and prevent deterioration in the downtown district, encourage historical preservation, and to promote economic development within the downtown district. The supervisor, subject to the approval of the Township Board under the supervision and control of a Board consisting of the Township supervisor and eight members, appoints the Authority. A tax incremental financing plan was instituted to finance the activities of the Authority. In addition, the

Authority budget is subject to approval by the Township Board. It is reported within the component unit column in the combined financial statements to emphasize that it is legally separate from the Township. The Brownfield Authority (the "Authority") was created under Michigan Public Act 381 of 1997. Its purpose is to redevelop and reuse the Grosse Ile Airport Commerce Park through the capture of tax revenues generated within the Brownfield District. The tax revenues are used to remediate environmental problems (approved by the Township Board) and for land use and market studies (approved by the State of Michigan Department of Environmental Quality). The members consist of the Airport Commission appointed by the Township Board. A tax incremental financing plan was instituted to finance the activities of the Authority. In addition, the Authority’s budget is subject to approval by the Township Board. It is reported within the component unit column in the combined financial statements to emphasize that it is legally separate from the Township. Jointly Governed Organizations - Jointly governed organizations are discussed in Note 13. Government-wide and fund financial statements The government-wide financial statements (i.e., the statement of net position and the statement of activities) report information on all of the nonfiduciary activities of the primary government and its component units. For the most part, the effect of interfund activity has been removed from these statements. Governmental activities, normally supported by taxes and intergovernmental revenues, are reported separately from business-type activities, which rely to a significant extent on fees and charges for support. Likewise, the primary government is reported separately from certain legally separate component units for which the primary government is financially accountable. The statement of activities demonstrates the degree to which the direct expenses of a given function or segment are offset by program

Township of Grosse Ile Notes to the Financial Statements

March 31, 2020

4 - 20

revenues. Direct expenses are those that are clearly identifiable with a specific function or segment. Program revenues include: (1) charges to customers or applicants who purchase, use, or directly benefit from goods, services, or privileges provided by a given function or segment and (2) grants and contributions that are restricted to meeting the operational or capital requirements of a particular function or segment. Taxes and other items not properly included among program revenues are reported instead as general revenue. Separate financial statements are provided for governmental funds, proprietary funds, and fiduciary funds, even though the latter are excluded from the government-wide financial statements. Major individual governmental funds and major individual enterprise funds are reported as separate columns in the fund financial statements. Measurement focus, basis of accounting, and financial statement presentation The government-wide financial statements are reported using the economic resources measurement focus and the accrual basis of accounting, as are the proprietary fund and fiduciary fund financial statements. Revenues are recorded when earned and expenses are recorded when a liability is incurred, regardless of the timing of related cash flows. Property taxes are recognized as revenues in the year for which they are levied. Grants and similar items are recognized as revenue as soon as all eligibility requirements imposed by the provider have been met. Governmental fund financial statements are reported using the current financial resources measurement focus and the modified accrual basis of accounting. Revenues are recognized as soon as they are both measurable and available. Revenues are considered to be available when they are collectible within the current period or soon enough thereafter to pay liabilities of the current period. For this purpose, the government considers revenues to be available if they are collected within 60 days of the end of the current fiscal period or 90 days for property taxes. Expenditures generally are recorded when a liability is

incurred, as under accrual accounting. However, debt service expenditures, as well as expenditures related to compensated absences and claims and judgments, are recorded only when payment is due. Property taxes, sales taxes, franchise taxes, licenses, and interest associated with the current fiscal period are all considered to be susceptible to accrual and so have been recognized as revenues of the current fiscal period. Only the portion of special assessments receivable due within the current fiscal period is considered to be susceptible to accrual as revenue of the current period. All other revenue items are considered to be measurable and available only when cash is received by the government. The Township reports the following major governmental funds:

General Fund - The General Fund is the Township’s primary operating fund. It accounts for all financial resources of the general government, except those required to be accounted for in another fund. Recreation Fund - The Recreation Fund is used to account for funds from a tax millage for public recreation programs and for fees generated. This Fund was authorized, in part, by a vote of the residents and by management to account for recreation program revenues. This fund also accounts for the Water’s Edge operations and maintenance of the golf course, pool, and marina facilities. The entire facility is open to the public for usage. Fire Operating Fund - The Fire Operating Fund is used to account for funds from a tax millage for the operations of the fire department. The fund was authorized by a vote of the residents approving a tax levy. Another source of funding for this fund is the collection of ambulance fees. Operations include firefighting services, as well as, basic emergency medical services for residents and visitors of the Township.

Township of Grosse Ile Notes to the Financial Statements

March 31, 2020

4 - 21

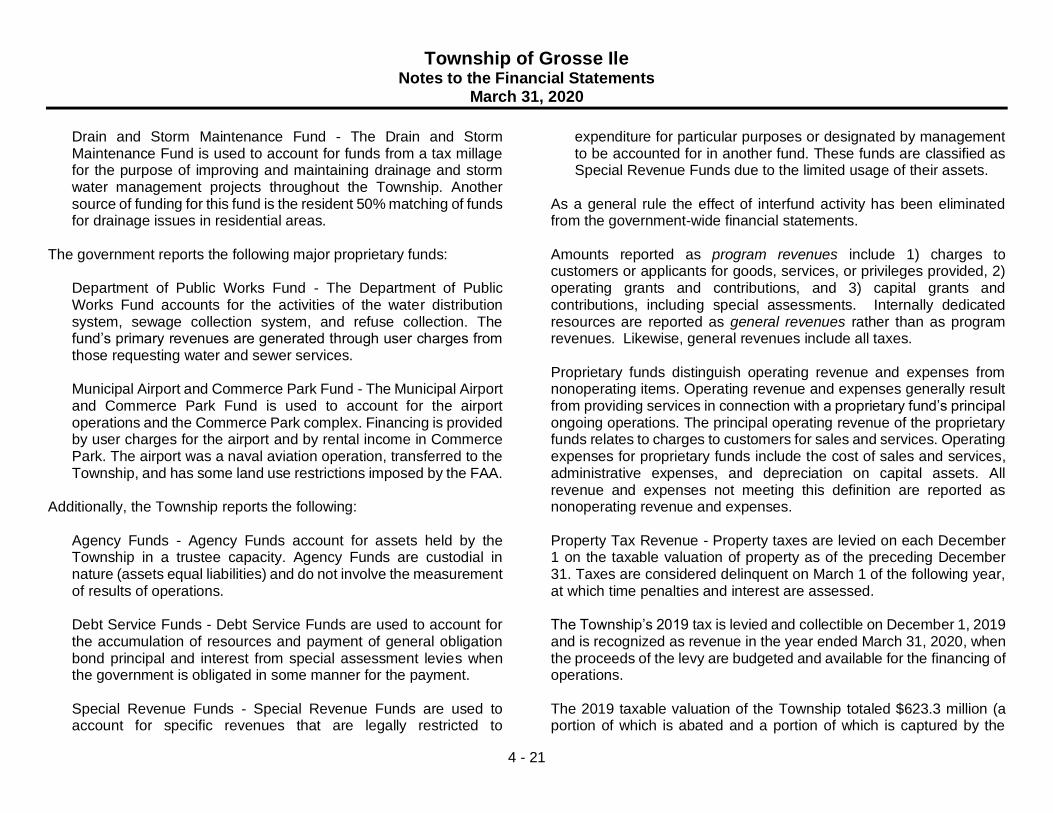

Drain and Storm Maintenance Fund - The Drain and Storm Maintenance Fund is used to account for funds from a tax millage for the purpose of improving and maintaining drainage and storm water management projects throughout the Township. Another source of funding for this fund is the resident 50% matching of funds for drainage issues in residential areas.

The government reports the following major proprietary funds:

Department of Public Works Fund - The Department of Public Works Fund accounts for the activities of the water distribution system, sewage collection system, and refuse collection. The fund’s primary revenues are generated through user charges from those requesting water and sewer services. Municipal Airport and Commerce Park Fund - The Municipal Airport and Commerce Park Fund is used to account for the airport operations and the Commerce Park complex. Financing is provided by user charges for the airport and by rental income in Commerce Park. The airport was a naval aviation operation, transferred to the Township, and has some land use restrictions imposed by the FAA.

Additionally, the Township reports the following:

Agency Funds - Agency Funds account for assets held by the Township in a trustee capacity. Agency Funds are custodial in nature (assets equal liabilities) and do not involve the measurement of results of operations. Debt Service Funds - Debt Service Funds are used to account for the accumulation of resources and payment of general obligation bond principal and interest from special assessment levies when the government is obligated in some manner for the payment. Special Revenue Funds - Special Revenue Funds are used to account for specific revenues that are legally restricted to

expenditure for particular purposes or designated by management to be accounted for in another fund. These funds are classified as Special Revenue Funds due to the limited usage of their assets.

As a general rule the effect of interfund activity has been eliminated from the government-wide financial statements. Amounts reported as program revenues include 1) charges to customers or applicants for goods, services, or privileges provided, 2) operating grants and contributions, and 3) capital grants and contributions, including special assessments. Internally dedicated resources are reported as general revenues rather than as program revenues. Likewise, general revenues include all taxes. Proprietary funds distinguish operating revenue and expenses from nonoperating items. Operating revenue and expenses generally result from providing services in connection with a proprietary fund’s principal ongoing operations. The principal operating revenue of the proprietary funds relates to charges to customers for sales and services. Operating expenses for proprietary funds include the cost of sales and services, administrative expenses, and depreciation on capital assets. All revenue and expenses not meeting this definition are reported as nonoperating revenue and expenses. Property Tax Revenue - Property taxes are levied on each December 1 on the taxable valuation of property as of the preceding December 31. Taxes are considered delinquent on March 1 of the following year, at which time penalties and interest are assessed. The Township’s 2019 tax is levied and collectible on December 1, 2019 and is recognized as revenue in the year ended March 31, 2020, when the proceeds of the levy are budgeted and available for the financing of operations. The 2019 taxable valuation of the Township totaled $623.3 million (a portion of which is abated and a portion of which is captured by the

Township of Grosse Ile Notes to the Financial Statements

March 31, 2020

4 - 22

Brownfield Authority and Downtown Development Authority), on which taxes levied consisted of 3.1551 mills for operating purposes, 2.7334 mills for police operations, 1.9832 mills for fire operations and equipment purchases, .8683 mills for recreation operations, .3966 for road improvement, .2000 mills for library use, .3282 mills for drainage improvements, .1489 mills for bike path maintenance, and 4.0000 mills for sewer-related debt. This resulted in $1.96 million for operating, $1.70 million for police operations, $1.22 million for fire operations and equipment purchases, $535,000 for recreation operations, $244,000 for road improvements, $123,000 for library use, $202,000 for drainage improvements, $92,000 for bike path maintenance, and $3.2 million for sewer-related debt. These amounts are recognized in the respective General Fund, Fire Operating Fund, Recreation Fund, Other Special Revenue Funds, Debt Service Funds, and Enterprise Funds financial statements as tax revenue. Assets, liabilities, and net position or equity Cash and Cash Equivalents - include cash on hand, demand deposits, and short-term investments with a maturity of three months or less when acquired. Investments are stated at fair value. To the extent that cash from various funds has been pooled, pooled investment income is generally allocated to each fund using a weighted average method. Receivables and Payables - In general, outstanding balances between funds are reported as “due to/from other funds”. Any residual balances outstanding between the governmental activities and the business-type activities are reported in the government-wide financial statements as “internal balances”. All trade and property tax receivables are shown as net of allowance for uncollectible amounts. Noncurrent receivables such as special assessments are recorded at full value, and a deferred inflow of resources is recorded for the portion not available for use to finance operations as of year end. Interest income on special assessments receivable is not accrued until its due date.

Inventories and Prepaid Items - Inventories are valued at cost, on a first-in, first-out basis. Inventories of governmental funds are recorded as expenditures when consumed rather than when purchased. Certain payments to vendors reflect costs applicable to future fiscal years and are recorded as prepaid items in both government-wide and fund financial statements. Capital Assets - Capital assets, which include property, plant, equipment, and infrastructure assets, are reported in the applicable governmental or business-type activities column in the government-wide financial statements. Capital assets are defined by the Township as assets with an initial individual cost of more than $1,000 and an estimated useful life in excess of one year. Such assets are recorded at historical cost or estimated historical cost if purchased or constructed. Donated capital assets are recorded at acquisition value at the date of donation. Buildings, equipment, and vehicles are depreciated using the straight-line method over the following useful lives:

Roads and sidewalks 50 years

Bike paths 20 years

Drains 100 years

Water and sewer distribution systems 20 to 100 years

Water and sewer treatment facilities 40 to 50 years

Buildings and building improvements 20 to 50 years

Vehicles 5 to 30 years

Furniture and fixtures 7 to 10 years

Equipment and machines 7 to 20 years

Signs 20 years

Deferred Outflows of Resources - The Township reports deferred outflows of resources as a result of pension and OPEB earnings. This amount is the result of a difference between what the plan expected to earn from plan investments and what is actually earned. This amount

Township of Grosse Ile Notes to the Financial Statements

March 31, 2020

4 - 23

will be amortized over the next four years and included in pension and OPEB expense. Changes in assumptions and experience differences relating to the net pension and OPEB liabilities are deferred and amortized over the expected remaining services lives of the employees and retirees in the plans. The Township also reported deferred outflows of resources for pension contributions made after the measurement date. This amount will reduce net pension liability in the following year. Compensated Absences (Vacation and Sick Leave) - It is the Township’s policy to permit employees to accumulate earned but unused sick and vacation pay benefits. All vacation pay is accrued when incurred in the government-wide and proprietary fund financial statements. A liability is reported in governmental funds where appropriate except in the General Fund, where it is only reported for employee terminations as of year end. Long-Term Obligations - In the government-wide financial statements and the proprietary fund types in the fund financial statements, long-term debt and other long-term obligations are reported as liabilities in the applicable governmental activities, business-type activities, or proprietary fund-type statement of net position. Bond premiums and discounts are deferred and amortized over the life of the bonds using the effective interest method. Bonds payable are reported net of the applicable bond premium or discount. In the fund financial statements, governmental fund types recognize bond premiums and discounts, as well as bond issuance costs during the current period. The face value of debt issued is reported as other financing sources. Premiums received on debt issuances are reported as other financing sources while discounts are reported as other financing uses. Issuance costs are reported as debt service expenditures. Pensions - For purposes of measuring the net pension liability, deferred outflows of resources and deferred inflows of resources related to pensions, and pension expense, information about the fiduciary net position the Municipal Employees Retirement System (MERS) of Michigan and additions to/deductions from MERS’ fiduciary net position

have been determined on the same basis as they are reported to MERS. For this purpose, benefit payments (including refunds of employee contributions) are recognized when due and payable in accordance with the benefit terms. Investments are reported at fair value. Other Postemployment Benefits (OPEB) – For purposes of measuring the net OPEB liability, deferred outflows of resources and deferred inflows of resources related to OPEB, and OPEB expense, information about the fiduciary net position of the Township’s OPEB Plan and additions to/deductions from the Plan’s fiduciary net position have been determined on the same basis as they are reported by the Plan. For this purpose, the Plan recognizes benefit payments when due and payable in accordance with the benefit terms. Investments are reported at fair value, except for money market investments and participating interest earning investment contracts that have a maturity at the time of purchase of one year or less, which are reported at cost. Deferred Inflows of Resources - A deferred inflow of resources is an acquisition of net position by the government that is applicable to a future reporting period. For governmental funds this includes unavailable revenue in connection with receivables for revenues that are not considered available to liquidate liabilities of the current period. The Township reports deferred inflows of resources as a result of changes in assumptions and experience differences relating to the net pension and OPEB liabilities, which are deferred and amortized over the expected remaining service lives of the employees and retirees in the plan.

Township of Grosse Ile Notes to the Financial Statements

March 31, 2020

4 - 24

Fund Equity - In the fund financial statements, governmental funds report the following components of fund balance:

Nonspendable - amounts that are not in spendable form (such as inventory and prepaid items) or are required to be maintained intact. Restricted - amounts that are legally restricted by outside parties, constitutional provisions, or enabling legislation for use for a specific purpose. Committed - amounts that have been formally set aside by the Board of Trustees for use for specific purposes. Commitments are made and can be rescinded only via resolution of the Board of Trustees. Assigned - intent to spend resources on specific purposes expressed by the Township’s Finance Director, who is authorized and approved by the Township’s Board of Trustees to make assignments. Unassigned - amounts that do not fall into any other category above. This is the residual classification for amounts in the General Fund and represents fund balance that has not been assigned to other funds and has not been restricted, committed or assigned to specific purposes in the General Fund. In other governmental funds, only negative unassigned amounts are reported, if any, and represent expenditures incurred for specific purposes exceeding the amounts previously restricted, committed or assigned to those purposes.

When multiple classifications of fund balances are available, fund balance will be used first from the most restrictive category in order, to the least restrictive. Use of Estimates The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the

reported amounts of assets, deferred outflows, liabilities, deferred inflows and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the period. Actual results could differ from those estimates. Adoption of New Accounting Standards Statement No. 92, Omnibus 2020 enhances comparability in accounting and financial reporting and improves the consistency of authoritative literature by addressing practice issues that have been identified during implementation and application of certain GASB Statements. This Statement addresses a variety of topics and includes specific provisions about the following: (1) The effective date of Statement No. 87, Leases, and Implementation Guide No. 2019-3, Leases, for interim financial reports (2) Reporting of intra-entity transfers of assets between a primary government employer and a component unit defined benefit pension plan or defined benefit other postemployment benefit (OPEB) plan. (3) The applicability of Statements No. 73, Accounting and Financial Reporting for Pensions and Related Assets That Are Not within the Scope of GASB Statement 68, and Amendments to Certain Provisions of GASB Statements 67 and 68, as amended, and No. 74, Financial Reporting for Postemployment Benefit Plans Other Than Pension Plans, as amended, to reporting assets accumulated for postemployment benefits. (4) The applicability of certain requirements of Statement No. 84, Fiduciary Activities, to postemployment benefit arrangements. (5) Measurement of liabilities (and assets, if any) related to asset retirement obligations (AROs) in a government acquisition. (6) Reporting by public entity risk pools for amounts that are recoverable from reinsurers or excess insurers. (7) Reference to nonrecurring fair value measurements of assets or liabilities in authoritative literature. (8) Terminology used to refer to derivative instruments. Statement No. 95, Postponement of the Effective Dates of Certain Authoritative Guidance provides temporary relief to governments and other stakeholders in light of the COVID-19 pandemic and provides

Township of Grosse Ile Notes to the Financial Statements

March 31, 2020

4 - 25

postponement of effective dates for certain GASB Statements. This statement was effective upon issuance in May of 2020. Upcoming Accounting and Reporting Changes In addition, the Governmental Accounting Standards Board has released the following Statements. Statement No. 84, Fiduciary Activities improves the guidance regarding the identification of fiduciary activities for accounting and financial reporting purposes and how those activities should be reported. The criteria generally is on (1) is the government controlling the assets of the fiduciary activity and (2) the beneficiaries with whom a fiduciary relationship exists. The four fiduciary funds that should be reported, if applicable: (1) pension (and other employee benefit) trust funds, (2) investment trust funds, (3) private-purpose trust funds, and (4) custodial funds. Custodial funds generally will report fiduciary activities that are not held in a trust or similar arrangement that meets specific criteria. The requirements of this Statement are effective for the fiscal year ending March 31, 2021.

Statement No. 87, Leases increases the usefulness of the Township’s financial statements by requiring recognition of certain lease assets and liabilities for leases that previously were classified as operating leases and recognized as inflows of resources or outflows of resources based on the payment provisions of the contract. It establishes a single model for lease accounting based on the foundational principle that leases are financings of the right to use an underlying asset. A lessee will be required to recognize a lease liability and an intangible right-to-use a lease asset, and a lessor will be required to recognize a lease receivable and a deferred inflow of resources, thereby enhancing the relevance and consistency of information about the Township’s leasing activities. The requirements of this Statement are effective for the fiscal year ending March 31, 2023. Statement No. 89, Accounting for Interest Cost Incurred before the End of a Construction Period enhances the relevance and comparability of

information about capital assets and the cost of borrowing for a reporting period and to simplify accounting for interest cost incurred before the end of a construction period. It requires that interest cost incurred before the end of a construction period be recognized as an expense in the period in which the cost is incurred for financial statements prepared using the economic resources measurement focus. As a result, interest cost incurred before the end of a construction period will not be included in the historical cost of a capital asset reporting in a business-type activity or enterprise fund. Interest cost incurred before the end of a construction period should be recognized as an expenditure for financial statements prepared using the current financial resources measurement. The requirements of this Statement are effective for the fiscal year ending March 31, 2022. Statement No. 90, Majority Equity Interests improves the consistency and comparability of reporting a government’s majority equity interest in a legally separate organization and improves the relevance of financial statement information for certain components. This statement is effective for the year ending March 31, 2021. Statement No. 91, Conduit Debt Obligations provides a single method of reporting conduit debt obligations by issuers and eliminate diversity in practice associated with (1) commitments extended by issuers, (2) arrangements associated with conduit debt obligations, and (3) related note disclosures. This Statement achieves those objectives by clarifying the existing definition of a conduit debt obligation; establishing that a conduit debt obligation is not a liability of the issuer; establishing standards for accounting and financial reporting of additional commitments and voluntary commitments extended by issuers and arrangements associated with conduit debt obligations; and improving required note disclosures. This statement is effective for the year ending March 31, 2023. Statement No. 93, Replacement of Interbank Offered Rates establishes accounting and financial reporting requirements related to the replacement of IBORs in hedging derivative instruments and leases. It

Township of Grosse Ile Notes to the Financial Statements

March 31, 2020

4 - 26

also identifies appropriate benchmark interest rates for hedging derivative instruments. The requirements of this Statement apply to the financial statements of all state and local governments. This statement is effective for the year ending March, 2023. Statement No. 94, Public-Private and Public-Public Partnerships and Availability Payment Arrangements improves financial reporting by addressing issues related to public-private and public-public partnership arrangements (PPPs). As used in this Statement, a PPP is an arrangement in which a government (the transferor) contracts with an operator (a governmental or nongovernmental entity) to provide public services by conveying control of the right to operate or use a nonfinancial asset, such as infrastructure or other capital asset (the underlying PPP asset), for a period of time in an exchange or exchange-like transaction. Some PPPs meet the definition of a service concession arrangement (SCA), which the Board defines in this Statement as a PPP in which (1) the operator collects and is compensated by fees from third parties; (2) the transferor determines or has the ability to modify or approve which services the operator is required to provide, to whom the operator is required to provide the services, and the prices or rates that can be charged for the services; and (3) the transferor is entitled to significant residual interest in the service utility of the underlying PPP asset at the end of the arrangement. This Statement also provides guidance for accounting and financial reporting for availability payment arrangements (APAs). As defined in this Statement, an APA is an arrangement in which a government compensates an operator for services that may include designing, constructing, financing, maintaining, or operating an underlying nonfinancial asset for a period of time in an exchange or exchange-like transaction. This statement is effective for the year ending March 31, 2024. The Township is evaluating the impact that the above GASB Statements will have on its financial reporting.

Note 2 - Stewardship, Compliance, and Accountability