FinScope South Africa 2012 Consumer Survey

1

October 30th 2012

Banking

Credit

Savings

Insurance

Contents

2

1

3 4

Who we spoke with

And what about people’s financial lives?

What has changed since 2004?

2 What do people’s lives look like today?

Banking

Credit

Savings

Insurance

Contents

3

1

3 4

Who we spoke with

And what about people’s financial lives?

What has changed since 2004?

2 What do people’s lives look like today?

Where: 16 African countries, including South Africa.

Objective: To measure and profile levels of access to and use of financial services by all adults in South Africa, across income ranges and other demographics, in order to inform stakeholders.

FinMark Trust and FinScope SA

FinMark Trust is an independent trust with the

purpose of “Making financial markets work for

the poor” across Africa in order to increase access

to financial services for the unserved and

underserved that ultimately lead to the

development of inclusive financial systems that

can benefit all people

FinScope SA is an annual representative study of

the demand for, usage of and access to financial

services in South Africa. The FinScope SA survey is

used to better understand money matters in

South Africa, with an emphasis on the market

needs and attitudes to both informal and formal

financial offerings and usage. The FinScope SA

survey further sheds light on consumers and

behaviour by exploring individuals’ interactions

with the financial sector as a whole

4

The syndicate members

form an integral part of

the FinScope SA

questionnaire design and

offer valuable insight into

consumer demand

behaviour

The syndicate members

also use the annual

FinScope SA results to

develop new products or

processes and to enrich

the overall objective of

increasing financial

inclusion in South Africa

2012 South African syndicate members

5

Sampling and methodology

6

Respondent profile Coverage and methodology

Sample and fieldwork validation

Universe: Adult population in South Africa

South African residents 16 years and older

Fieldwork conducted from May 2012 to July 2012

Questionnaire translated into isiXhosa, isiZulu, Sesotho, Setswana, Sepedi and Afrikaans

3 900 interviews conducted by TNS

Nationally representative sample (weighted / benchmarked to

Stats SA 2011

mid-year population estimates)

Banking

Credit

Savings

Insurance

Contents

7

1

3 4

Who we spoke with

And what about people’s financial lives?

What has changed since 2004?

2 What do people’s lives look like today?

South Africa is a country of extremes…

8

LSM 1-2 LSM 3 LSM 4 LSM 5 LSM 6

LSM 7 LSM 8 LSM 9 LSM 10

LSM breakdown

1.2m 1.5m 4.5m 8.6m 9.1m 3m 1.7m 2.4m 1.8m

7

29

33

Don’t get money

Government grants

Money from others

Sources of money

29% of adults work full-time

4

37

29

18

12 16 – 17

18 – 29

30 – 44

45 – 59

60+

41% of adults in SA are younger

than 30

2012 Age

n=3900

21% in LSM 1-4 R1 000 PMI

52% in LSM 5-6 R1 800 PMI

26% in LSM 7-10 R8 000 PMI

15% work part-time

… and impoverished pockets still persist

9

TOTAL adults in SA

33.7 million

LSM 1-2 in SA (adults) 1.2 million

LSM 3-4 in SA (adults)

No tap water in home or on stand

No toilet facilities in home

No electricity in home

No tap water No toilet No electricity

4% 4% 10%

6 million

23% 27% 88%

No tap water No toilet No electricity

14% 11% 30%

Tough circumstances = 21% of South Africa (7.2m adults)

62% of this group live in tribal lands. Only 21% get salaries or wages. 45% are younger than 30.

Impoverished pockets take twice as long to access basic facilities

10

Public transport

Supermarket

ATM

Petrol station or garage

Post office

Bank branch

Social grant ID point

Insurance branch

Min.

Min.

Min.

Min.

Min.

Min.

Min.

Min.

Average South African LSM 1-4

Min.

Min.

Min.

Min.

Min.

Min.

Min.

Min.

South Africans are generally positive about their lives

11

67%

There are concerns over personal educational achievement as well as social capital.

claim they are in perfect health

expect their life to be better in 2 years’ time

60%

believe they will achieve their goals in future

61%

are happy with their current lifestyle

are happy with their level of education

53%

41%

People are positive about People are concerned about

Only

Can rely on neighbours to help out 37%

Only

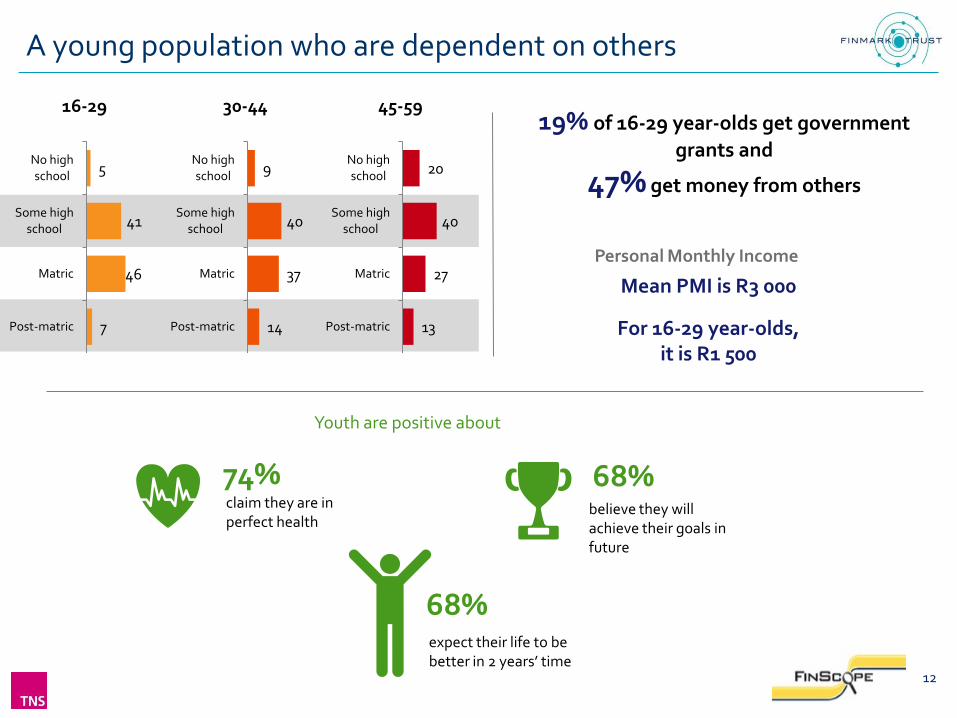

A young population who are dependent on others

12

Personal Monthly Income

19% of 16-29 year-olds get government

grants and

47% get money from others

Mean PMI is R3 000

For 16-29 year-olds, it is R1 500

74% claim they are in perfect health

expect their life to be better in 2 years’ time

68%

believe they will achieve their goals in future

68%

Youth are positive about

5

41

46

7

No high school

Some high school

Matric

Post-matric

16-29

9

40

37

14

No high school

Some high school

Matric

Post-matric

30-44

20

40

27

13

No high school

Some high school

Matric

Post-matric

45-59

Banking

Credit

Savings

Insurance

Contents

13

1

3 4

Who we spoke with

And what about people’s financial lives?

What has changed since 2004?

2 What do people’s lives look like today?

More people have been brought into banking in 2012

67

63

63

6

5

5

8

5

9

19

27

23

2012

2011

2010

Banked

Formal other (non-bank products)

Informally served only

Not served

2012 (33 739 399) 2011 (33 739 399) 2010 (33 441 893)

Banked 22 514 009 21 184 871 20 956 844

Formal other (non-bank products) 1 946 316 1 605 519 1 667 456

Informally served only 2 726 132 1 852 518 3 000 903

Not served 6 552 944 9 096 492 7 816 691

14

Almost 40% have a product portfolio stretching across the strand

15

Banked, Formal and Informal 13.1m = 39% 52% burial 34% formal funeral 22% life insurance 35% formal retirement 24% savings clubs 15% credit card

2%

3%

1%

3%

24%

8%

Banked only 0.7m = 2%

Banked and Formal 8.2m = 24% 22% store card 21% formal funeral 17% formal retirement 13% life insurance 10% asset insurance

Formal only 0.9m = 3% 8% store card 25% buy on credit from store

Informal only 2.7m = 8% 61% burial 11% stokvel 29% use loyalty points

Formal and Informal 1m = 3% 50% burial 24% stokvel 16% store card

Banked and Informal 0.5m = 1% 91% burial 10% savings club

NOT SERVED 6.5m = 19%

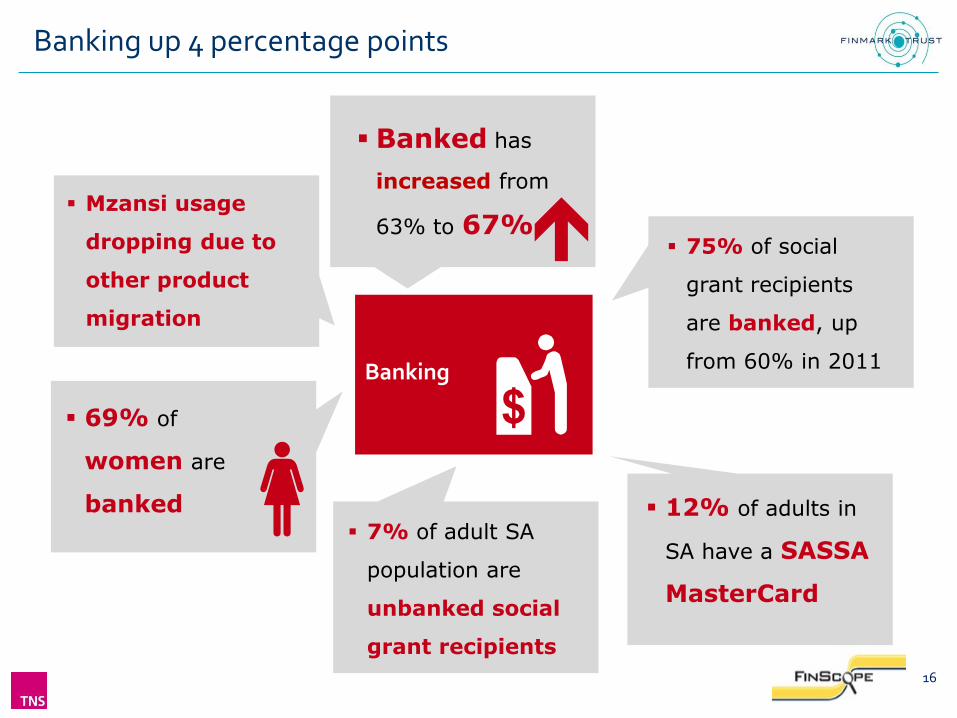

Banking up 4 percentage points

16

Banking

Banked has

increased from

63% to 67% 75% of social

grant recipients

are banked, up

from 60% in 2011

12% of adults in

SA have a SASSA

MasterCard

7% of adult SA

population are

unbanked social

grant recipients

69% of

women are

banked

Mzansi usage

dropping due to

other product

migration

We need to get people to deepen engagement with banking

Full service banking

Unbanked

Monthly cash withdrawal at store till using bank card /

Prefer bank card purchases to cash

Do NOT withdraw all at once every

month

Basic banking – withdraw all at

once every month

Size: 9.6m

Size: 11.2m

Size: 5.8m

Size: 3.4m

Size: 3.7m

Avg. personal monthly income

R7 600

R2 000

R1 900

R1 400

R 750

52% agree that it only makes sense to have bank a/c if get money regularly and reliably;

36% banking fees too expensive

43% take out all money as soon as deposited

17% unsure which bank account best

57% not enough money for bank account;

22% unsure which bank account best;

18% too complicated to open bank a/c

High

Low

Attitudes to banking

14% unsure which bank account best;

8% too complicated to open bank a/c

26% claim to be borrowing

18

don’t like borrowing money

embarrassed to borrow

would go to a mashonisa as a last resort

claim that this is to buy food - lower income skew

Of those who do borrow,

76%

43%

22%

32%

claim to borrow from formal places or have formal cards or credit facilities 26% claim to borrow from informal places 15%

claim to borrow from family or friends 12%

There is a desire to borrow to start a business

19

Avg. personal monthly income

Other borrowing

Do not borrow

Cards or overdraft

Informal borrowing

Family / friends

borrowing

Size: 22m

Size: 5.7m

Size: 1m

Size: 2.2m

R5 600

R1 800

R1 600

R1 300

High

Low

Formal secured

Size: 2m

R16 000

Borrowing attitudes

Reasons for borrowing (definitely borrow for)

19% friends or family

34% friends or family

43% embarrassed if had to borrow

20% often spend more than have 32% would borrow from mashonisa

40% house 35% car

37% start own business 35% car

39% for emergency 38% pay for friend’s funeral

Formal unsecured

Size: 1m

R5 600 52% store card 9% friends or family

74% easier to get loan if have bank account 16% considered seeking help with debt problems

45% house 41% for emergency 15% for wedding / lobola

41% start own business 34% for emergency 31% pay for friend’s funeral

Personal obstacles to saving

20

claim they have enough money to save after covering all spending needs

worried won’t have enough money for old age or retirement

of people do not own a retirement, pension or provident product

25%

83%

48%

Those without savings skew to

unbanked and under 30 years old

4 in 5 of those who had cancelled a savings product said

could no longer afford – skew 30-44 years, low education and low income

Those who cancelled savings products due to recession skew R8 000+ income

Long-term savings opportunity amongst formal savers

21

Avg. monthly savings

High

Low

Other savings products

Avg. personal monthly income

Key priorities (extremely important)

Key barriers to formal insurance for those without

Education, investment or endowment

policies

Not served savings

Retirement policies

Informally served savings

Saving with others or

keeping money at home

Size: 1.4m

Size: 22.7m

Size: 3m

Size: 2m

Size: 1.7m

R10 500

R8 500

R1 800

R2 000

R1 400

Deposit or call a/c

Size: 1.7m

R9 000

R1 200

Tradable investments (shares etc.)

Size: 0.7m

R18 000

R1 200

R1 900

R350

R80

R700

R330

43% retirement annuity

55% pension fund

10% stokvel

37% deposit a/c 59% pension fund

20% no reason for no HH insurance

50% pay school fees 34% pay back loans

43% buy house / car 52% pay funeral

22% don’t want HH insurance 21% no HH insurance because premiums too high

49% buy house / car 36% pay back loans

40% no life insurance due to affordability

45% find language used in financial paperwork confusing

11% no HH insurance because cheaper to self-replace

52% pay funeral

26% buy clothes

14% no reason for no HH insurance 14% do not want HH insurance

38% buy house 27% pay back loans 43% pay funeral

Burial and funeral cover dominates insurance

22

Reasons for no household contents insurance:

People earning R3 000+ – premiums / costs / fees are too high

1 in 5 university-educated say don’t want it

1 in 5 earning R1 000 to R3 000 say earn too little

have life cover have medical cover

covered by burial society

funeral cover through funeral parlour or undertaker

have funeral cover with bank

have funeral cover with insurance company

Reasons for no funeral cover:

Higher income or educated people say – family will look after funeral

Low LSM or income – cannot afford

60 years + – too poor

Reasons for no life insurance:

Low income – earn too little

Older people – prefer funeral or burial cover

People earning R3 000 to R8 000 – don’t believe / never thought about / don’t want

28%

12% 10%

10%

7%

8%

Note: All figures quoted for direct cover in own name. Indirect cover not included in these figures.

Low take-up of formal retirement amongst non-salaried

12

22

15

6

4

1

Life insurance

Pension fund

Retirement annuity

Salaried (n=375) Non-salaried (n=192)

23

R2 000 – R6 000 personal monthly income

34

28

40

27

41

30

41

10

Life insurance

Medical aid

Pension fund

Retirement annuity

Salaried (n=103) Non-salaried (n=33*)

R6 000 – R8 000 personal monthly income

49

41

56

47

19

45

42

29

20

35

Life insurance

Medical aid

Pension fund

Retirement annuity

Household contents

Salaried (n=238) Non-salaried (n=61)

R8 000 – R17 000 personal monthly income

26

67

63

59

49

9

76

65

19

31

Loan from a bank

Life insurance

Medical aid

Pension fund

Provident fund

Salaried (n=99) Non-salaried (n=27**)

R17 000+ personal monthly income

* Caution: small base size ** Caution: very small base size

Scope for targeted education and selling of income cover and more extensive retirement

24

High

Low

Avg. personal monthly income

Key priorities (extremely important)

Key barriers to insurance take-up

Other insurance products

Others with life

Not served

Asset

Formal funeral

Burial

Size: 1.3m

Size: 17.8m

Size: 0.6m

Size: 4.5m

Size: 5.7m

R6 000

R6 500

R2 700

R1 700

R1 200

Others with

disability

Size: 0.6m R14 500

18% don’t want HH insurance; 18% no HH insurance because fees too high

52% pay school fees 64% provide for family if pass away

Others with

medical

Size: 2.2m

R18 000 62% money for old age / retirement

61% provide for family if pass away

Others with

income

Size: 0.6m

Income, Medical ,

Disability & Life

Size: 0.4m

R9 000

R15 000

15% no HH insurance because excess too high

31% no HH insurance because don’t trust pay-out

21% no HH insurance because value of things too low; 14% no HH insurance because don’t believe in insurance; 29% no life insurance – fear missing payment and losing money paid

60% money for old age / retirement

67% burial

41% formal funeral

67% formal funeral

70% life 56% asset

66% asset 70% life

33% medical 49% life

79% asset 84% formal funeral

Note: All figures quoted for direct cover in own name. Indirect cover not included in these figures.

49% provide for family if pass away 34% old age / retirement

Banking

Credit

Savings

Insurance

Contents

25

1

3 4

Who we spoke with

And what about people’s financial lives?

What has changed since 2004?

2 What do people’s lives look like today?

Banking, funeral cover and formal retirement products are star performers

26

46%

5%

15% 20%

6% 6% 9% 7% 11%

67%

8%

26% 28%

9% 10% 12% 11% 13%

2004 % 2012 %

Banked

13m → 22.5m

Formal funeral cover

4.2m → 8.7m

Burial society membership

6m → 9.5m

Stokvel, savings or investment

club membership

2.1m → 3.6m

Retirement annuity

2.1m → 3.1m

Provident fund

1.8m → 3.5m

Pension fund

2.7m → 4m

Life insurance

3.2m → 3.9m 1.5m → 2.6m

Credit card

Another 3% of adults in South Africa claim to have life insurance through someone else

Note: All figures quoted for direct cover in own name. Indirect cover not included in these figures.

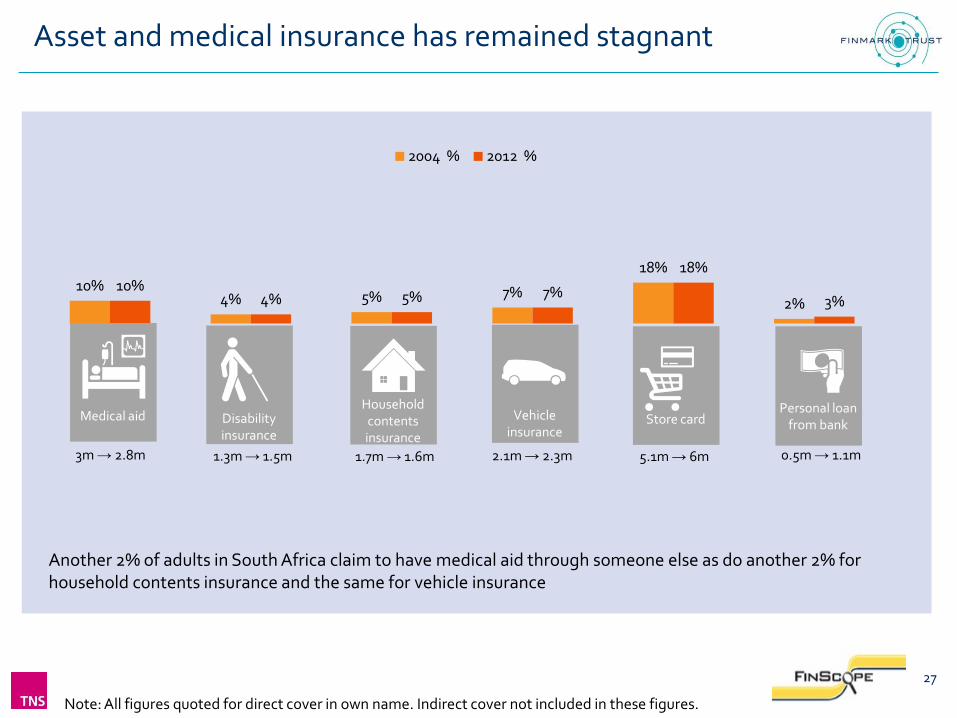

Asset and medical insurance has remained stagnant

27

10% 4% 5% 7%

18%

2% 10%

4% 5% 7%

18%

3%

2004 % 2012 %

Medical aid

3m → 2.8m

Disability insurance

1.3m → 1.5m

Household contents insurance

1.7m → 1.6m

Vehicle insurance

2.1m → 2.3m

Store card

5.1m → 6m

Personal loan from bank

0.5m → 1.1m

Another 2% of adults in South Africa claim to have medical aid through someone else as do another 2% for household contents insurance and the same for vehicle insurance

Note: All figures quoted for direct cover in own name. Indirect cover not included in these figures.

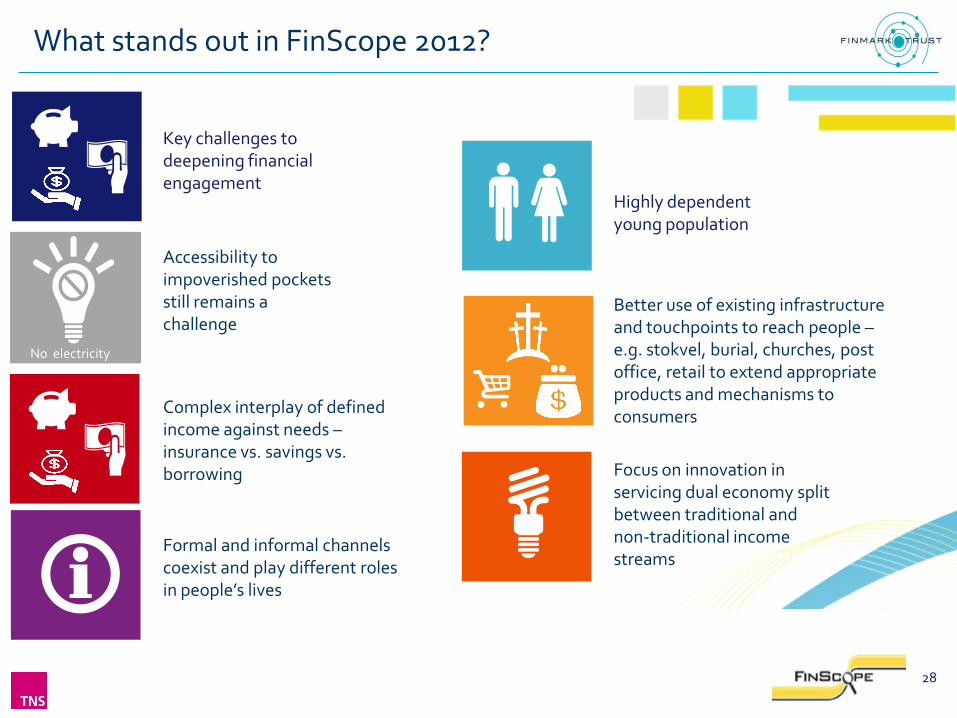

What stands out in FinScope 2012?

28

Complex interplay of defined income against needs – insurance vs. savings vs. borrowing

Better use of existing infrastructure and touchpoints to reach people – e.g. stokvel, burial, churches, post office, retail to extend appropriate products and mechanisms to consumers

Formal and informal channels coexist and play different roles in people’s lives

Focus on innovation in servicing dual economy split between traditional and non-traditional income streams

No electricity

Accessibility to impoverished pockets still remains a challenge

Highly dependent young population

Key challenges to deepening financial engagement