Fred KemmererAccess Architecture & Strategy

Lucent [email protected]

June 1998

Residential Access Network Evolution

Current Environment

• Data is a primary driver for network upgrades

• There are a number of technology choices for broadband data access

• Access competition is focused around data

• Keys to the industry’s success:

– Building on existing networks (at least in the short term)

– Supporting technologies

– New business models to support data services, particularly addressing the customer interface challenges

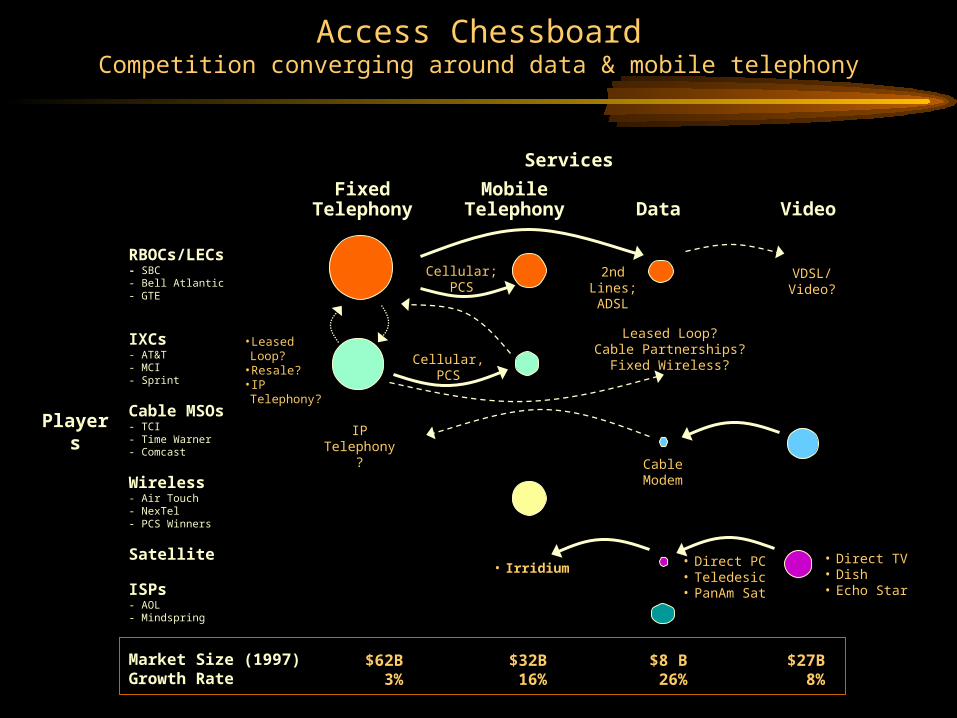

Access ChessboardCompetition converging around data & mobile telephony

RBOCs/LECs- SBC- Bell Atlantic- GTE

IXCs- AT&T- MCI- Sprint

Cable MSOs- TCI- Time Warner- Comcast

Wireless- Air Touch- NexTel- PCS Winners

Satellite

ISPs- AOL- Mindspring

Market Size (1997)Growth Rate

Players

Fixed Telephony

Mobile Telephony Data Video

Services

2nd Lines;ADSL

VDSL/Video?

Cellular,PCS

IP Telephony?

• LeasedLoop?

• Resale?• IP Telephony?

CableModem

• Irridium• Direct PC• Teledesic• PanAm Sat

• Direct TV• Dish• Echo Star

$62B3%

$32B16%

$8 B26%

$27B8%

Cellular;PCS

Leased Loop?Cable Partnerships?

Fixed Wireless?

Household Data Demand

0

20

40

60

80

100

120

1993 1994 1995 1996 1997

FixedVoiceLines

Cable TV

PCs

Internet

Source: Veronis and Suhler, IDC, CTIA FCC

Subscribersmillions

Cellular/PCS

CPECost ($)

$20-60

$0-300 (DBS)

$1,000-3000

$0-200

Avg. ServiceExpenditure

($/mo.)

$100-250

$27 (local)$26 (LD)

$42

-

$56

$20-$40

Total US households = 102M

Wide Range of Projections for Success

0

5

10

15

1998 1999 2000 2001 2002

ADSLmillions

High

Medium

Low

• One winner or zones-of-advantage based winners?

• Wireless, satellite?

0

5

10

15

1998 1999 2000 2001 2002

Cable Modemmillions Hig

h

Medium

Low

Source: Cowles/Simba, Forrester Research, IDC, Yankee Group, Dataquest

DSL Business Model – Early Market View

A positive business model for DSL exists for business and is emerging in high-end residential/SOHO.

1

10

100

1,000

0.1 Mbps

Downstream Speed (log scale)

$ perMonth

(log scale)

T1Frac T1

ISDN

IDSL

HDSLADSL

Incremental Cost(vs. Analog Modem)

Small/MediumBusiness• Based on nearest

alternative currently in use

Emerging High-End Residential Opportunity

Existing Business

Market Opportunity

1 Mbps 10 Mbps

Top 25% of Residential Market• Based on range of

current market research

• Potentially higher if businesses subsidize (As in early cellular business model)

Willingness-to-pay

Source: Mercer management Consulting

• Loop Technologies– Leverage existing copper and coax loops

– Wideband base stations for wireless

• Dollars

• Supporting Technologies

– CPE

– Applications enablers

– Core Network Capacity

• Focus on Customer Interface

• Industry Cooperation

• Encouraging Regulation

What’s Required?

ADSL via MetallicDistribution

Cable Modems viaCoaxial Distribution

CircuitPacket

CircuitPacket

CableModemTerminatingSystem

DLC w/IntegratedDSLAM

Switch Line Unitw/ Integrated DSLAM

Integrated Voice/Data NetworksExisting Infrastructure

Fixed Wireless

Circuit

Packet

Circuit

Packet

Integrated Voice/Data NetworksNew Build

Fiber-to-the-Home

New Access Networks Are ExpensiveLeveraging existing infrastructures is a critical advantage

Cumulative Investment in Residential Access Plant

$92

$54

$32

0

10

20

30

40

50

60

70

80

90

100

PSTN Cable TV Wireless

$Billion

Source: FCC, CTIA, Kagan

High First-Costs favor:• Incremental Upgrades - ADSL, Cable Modems• Focused Builds - CAPs• Variable Cost Approaches - Satellite

Expected Cable MSO HFC Upgrade Path

0%

10%

20%

30%

40%

50%

60%

70%

80%

1996 1997 1998 1999 2000 2001 2002

2-way HFC Upgrade% of Homes Passed

Source: Average view of Forrester, Jupiter, Datapro, Company Announcements

0%

25%

50%

75%

100%

Bandwidth Likely to Bring Newand Increased Usage

% of Internet Users Who Would Start/Increase Use if the Net Were Much Faster and Had

Better Audio-visual Quality

Use More

Start Using

MakeVideoCalls

WatchVideos

PurchaseGoods orServices

PlayGames

BroadcastVideos

Surf/Browse

MakeVoiceCalls

Source: Mercer management Consulting Internet Lead user Study

Key Related Technologies toSupport Applications

• Always On/Permanent NetworkConnection

• IP Telephony

• Streaming Audio/Video Hardwareand Software

• Push

• New classes of Plug and Play Data-Enabled Devices/Modems in Consumer Devices

• Home LANs

Quick-use applications; real-time communications

Flat-rate long distance; E-mail & Voice Mailintegration

High quality gaming, Video clip newsfeeds, Sports replays, Video-on-demand, Video-mail

Personalized information, targeted advertising to help fund network costs

Internet access via TV, smart appliances, ease of use

Reduced cost for multiple broadband modems; Intra-home networking; Home Management

Technology Some Applications/Benefits

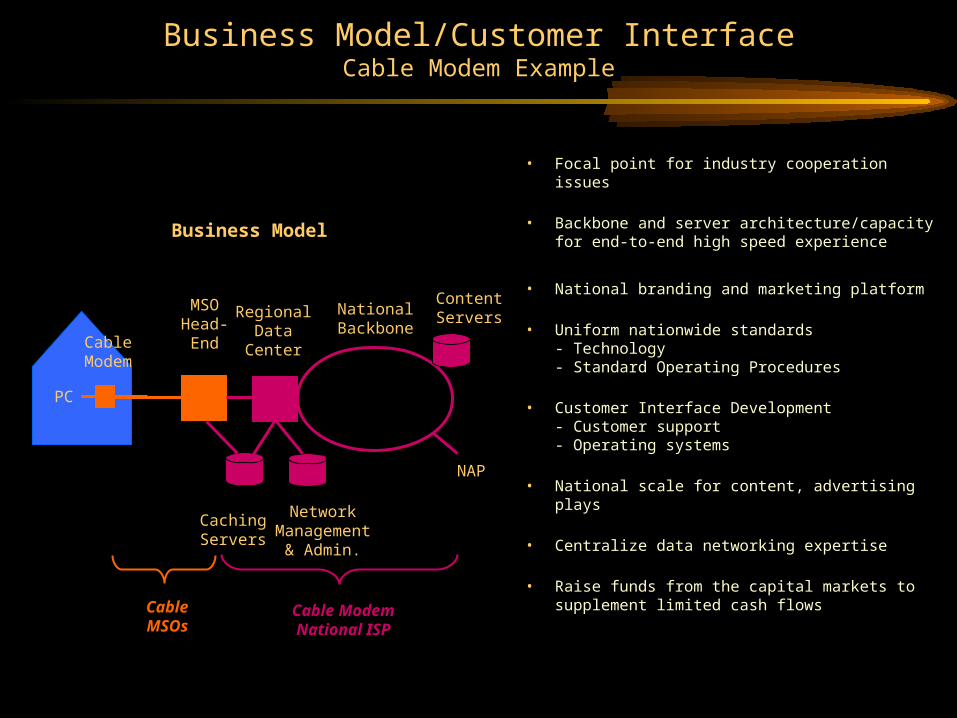

Business Model/Customer InterfaceCable Modem Example

• Focal point for industry cooperation issues

• Backbone and server architecture/capacityfor end-to-end high speed experience

• National branding and marketing platform

• Uniform nationwide standards- Technology- Standard Operating Procedures

• Customer Interface Development- Customer support- Operating systems

• National scale for content, advertising plays

• Centralize data networking expertise

• Raise funds from the capital markets tosupplement limited cash flows

Business Model

RegionalData

Center

ContentServers

MSOHead-EndCable

Modem

PC

CachingServers

NetworkManagement

& Admin.

CableMSOs

Cable ModemNational ISP

NationalBackbone

NAP

Broadband Access Lift-Off EnablersCable Modems on the inside track?

Cable Modem

StandardsCustomer Coverage

Trials-ProvenTechnology

Business Model/Customer InterfaceCost

ADSL

Wireless

Satellite

Full Service Network/FTTH

•HFC upgrades on track

•Spectrum available, but infrastructure build can be time consuming

•Need satellite launch

•Can ramp to 100% quickly

• Focused demand• High cost for new network builds• Current applications dominate

– PC

– Internet

• Sow the seeds for new broadband applications

• VF modems continue to dominate• Incremental upgrade technologies

– Cable Modems & ADSL

• Pull Fiber to the Neighborhood• Wireless as a Wild-Card

• Broad Demand• Cost curves decline• Data, Video and Voice

• Always-on, Many devices

• Fiber Close-to and Into the Home

What Will the Access Landscape Look Like?

Near Term Long Term

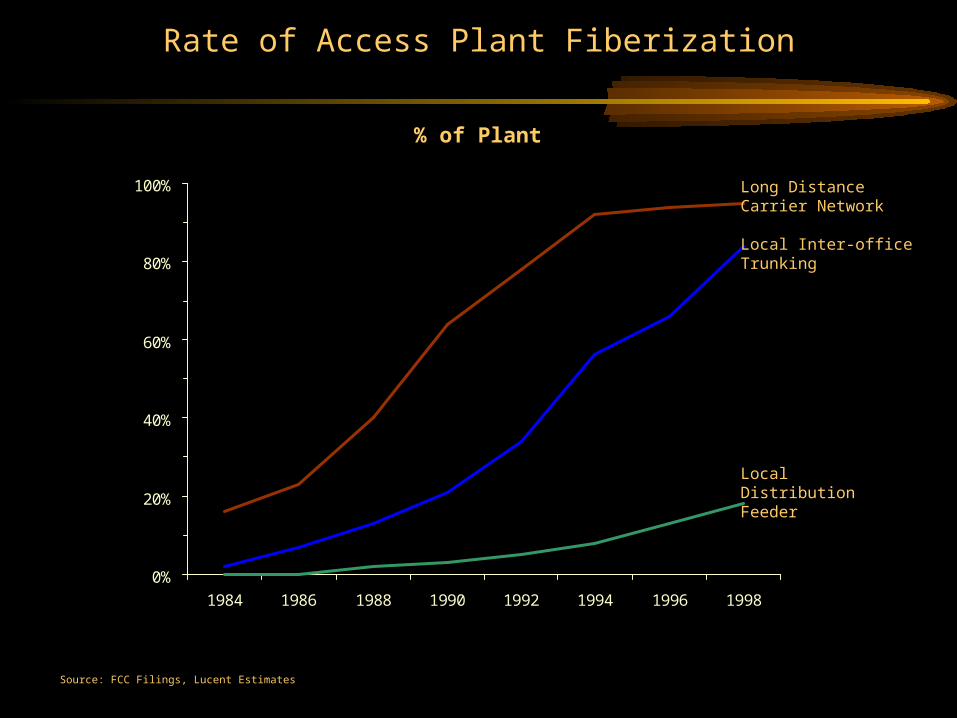

Rate of Access Plant Fiberization

0%

20%

40%

60%

80%

100%

1984 1986 1988 1990 1992 1994 1996 1998

Source: FCC Filings, Lucent Estimates

% of Plant

Long DistanceCarrier Network

Local Inter-officeTrunking

LocalDistributionFeeder

Thank You!!