May 2015 - Singapore

French Maritime Cluster Committee in Singapore

FMCCS

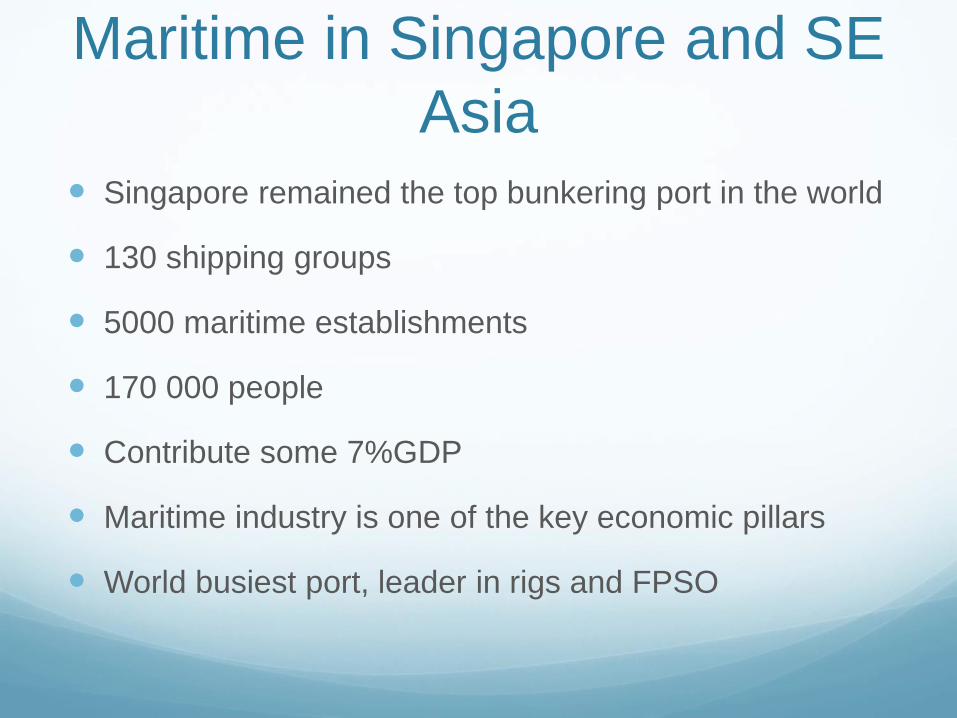

Maritime in Singapore and SE

Asia Singapore remained the top bunkering port in the world

130 shipping groups

5000 maritime establishments

170 000 people

Contribute some 7%GDP

Maritime industry is one of the key economic pillars

World busiest port, leader in rigs and FPSO

Maritime in Singapore and SE

Asia R&D marine and offshore has increased

Develop shipping, port and maritime services, offshore

Innovative technologies, ideas toward sustainability

Safety offshore exploration and production

LNG research and technology (risk, safety, simulation)

Clean and efficient green next generation port

Centre of excellence for maritime research

Agenda

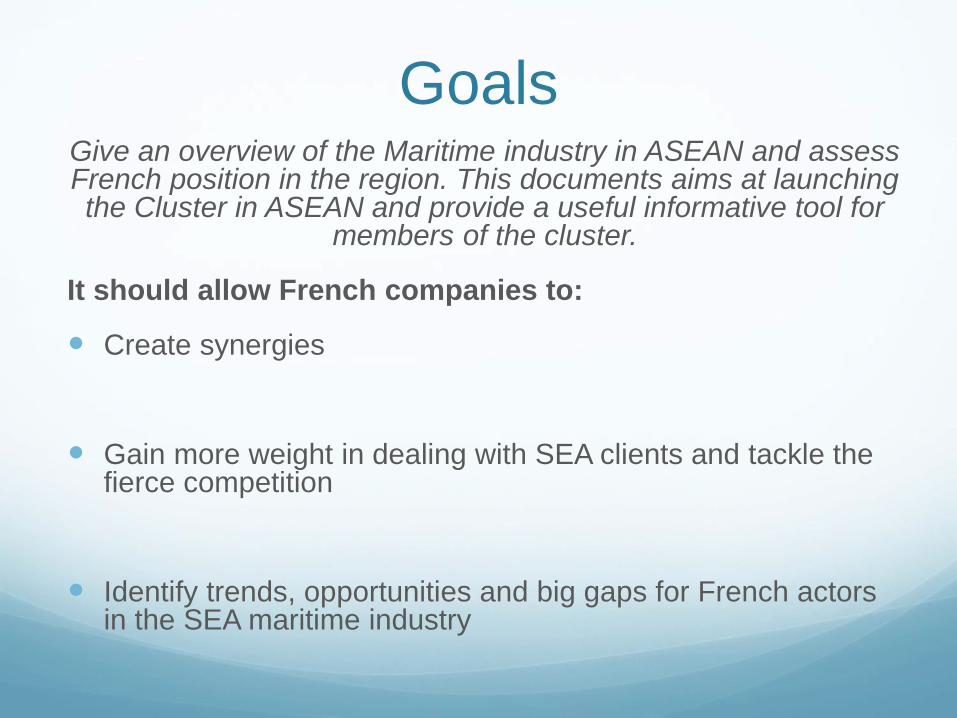

Goals

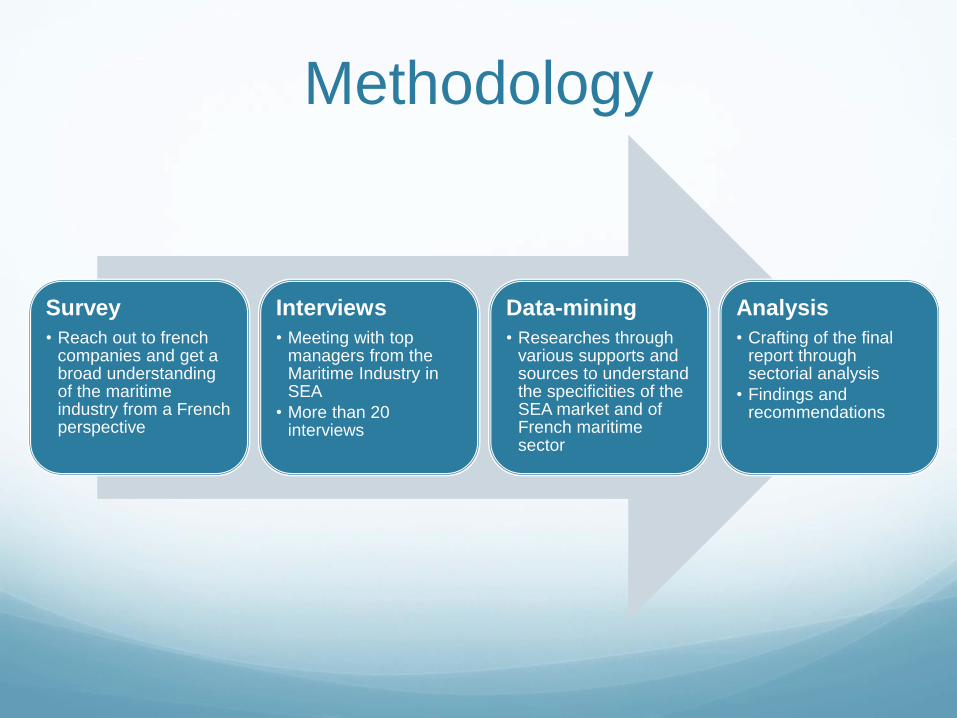

Methodology

Mapping

Identified Sectors

Sectors analysis

Way Ahead

Goals Give an overview of the Maritime industry in ASEAN and assess French position in the region. This documents aims at launching the Cluster in ASEAN and provide a useful informative tool for

members of the cluster.

It should allow French companies to:

Create synergies

Gain more weight in dealing with SEA clients and tackle the fierce competition

Identify trends, opportunities and big gaps for French actors in the SEA maritime industry

Methodology

Survey

• Reach out to french companies and get a broad understanding of the maritime industry from a French perspective

Interviews

• Meeting with top managers from the Maritime Industry in SEA

• More than 20 interviews

Data-mining

• Researches through various supports and sources to understand the specificities of the SEA market and of French maritime sector

Analysis

• Crafting of the final report through sectorial analysis

• Findings and recommendations

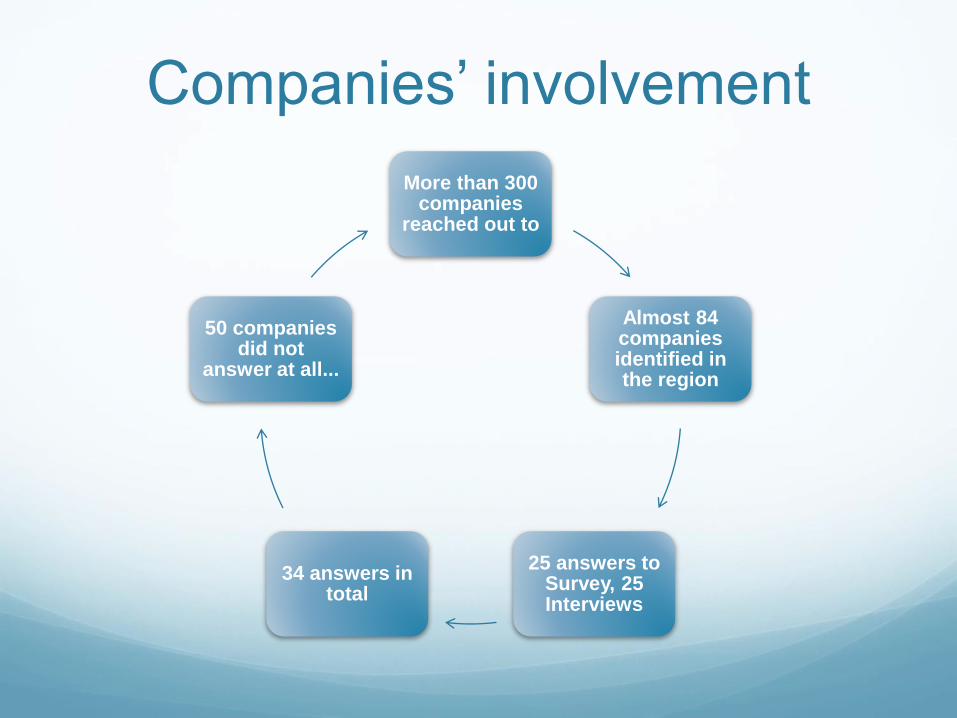

Companies’ involvement

More than 300 companies

reached out to

Almost 84 companies identified in the region

25 answers to Survey, 25 Interviews

34 answers in total

50 companies did not

answer at all...

10

23

9 6

20

11

4

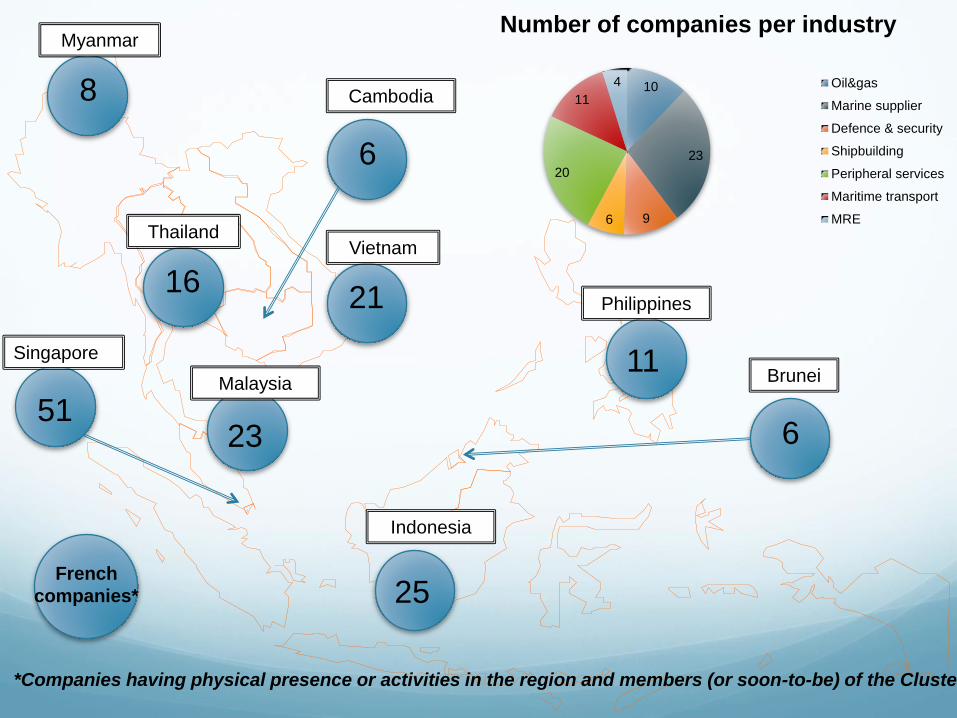

Number of companies per industry

Oil&gas

Marine supplier

Defence & security

Shipbuilding

Peripheral services

Maritime transport

MRE

8

21 16

23 51

25

11

6

Brunei

Singapore

Myanmar

Vietnam Thailand

Indonesia

Philippines

Malaysia

6

Cambodia

French

companies*

*Companies having physical presence or activities in the region and members (or soon-to-be) of the Cluster

MARITIME

INDUSTRY

Security, Safety and Defence activities

1

2

3

4

Shipbuilding

Shipping & Logistics Offshore industries

Ship construction (civilian and repair)

Marine Supplies

Offshore systems,

equipment & services

Maritime renewable

energy

Military shipbuilding & systems

providers

Security & Safety services

Shipping companies

Logistics services

Sectors

Peripheral Services IT and telecomunications Financial services Ship-broking Law Certification

5

Shipbuilding

Definition

World market is estimated between 185 and 190 billion euros between

2013 and 2017

France has less than 5% Market Share worldwide with 8 bn € turnover in

2012

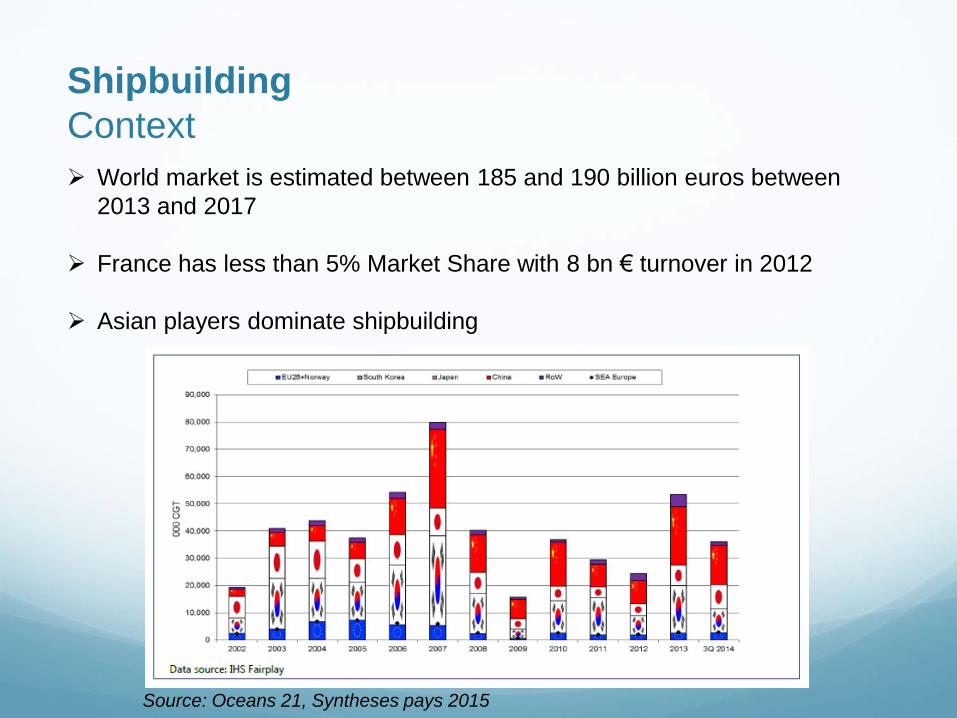

Shipbuilding

Context

World market is estimated between 185 and 190 billion euros between

2013 and 2017

France has less than 5% Market Share with 8 bn € turnover in 2012

Asian players dominate shipbuilding

Source: Oceans 21, Syntheses pays 2015

Shipbuilding

Context ASEAN

35

9

10

20

12

10

30

Number of shipyards: ASEAN countries

Indonesia

Malaysia

Myanmar

Philippines

Singapore

Thailand

Vietnam

ASEAN represents 20% of shipyards worldwide

Small shipyards cover a broad range of services, mailny focused on offshore

The main builders are Chinese, Korean and Japanese

More and more « upgrading » of shipyards

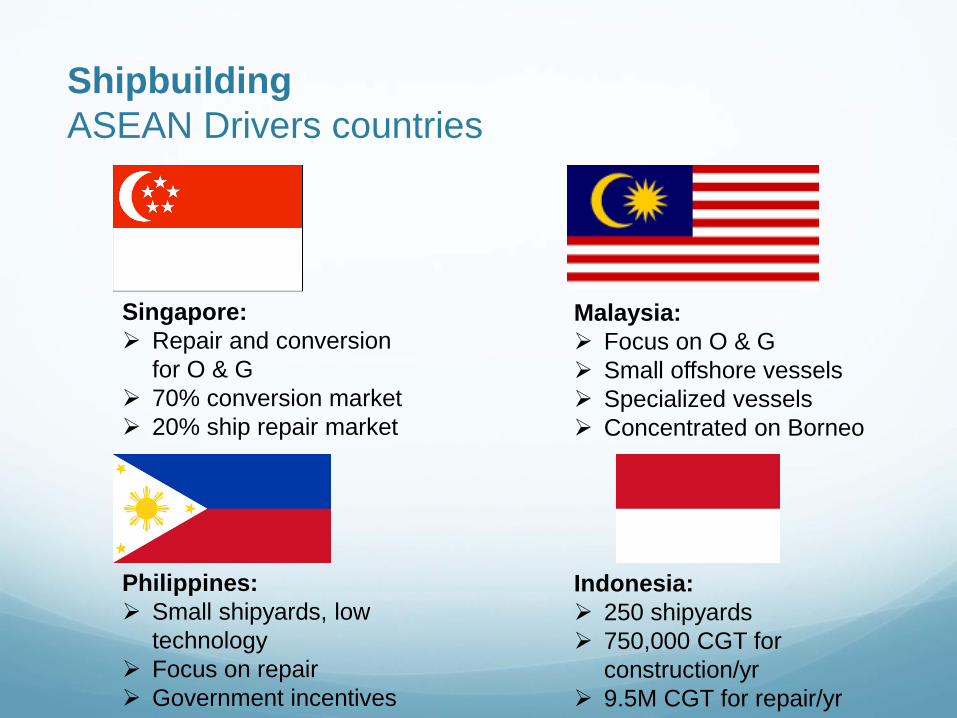

Shipbuilding

ASEAN Drivers countries

Singapore:

Repair and conversion

for O & G

70% conversion market

20% ship repair market

Malaysia:

Focus on O & G

Small offshore vessels

Specialized vessels

Concentrated on Borneo

Philippines:

Small shipyards, low

technology

Focus on repair

Government incentives

Indonesia:

250 shipyards

750,000 CGT for

construction/yr

9.5M CGT for repair/yr

Shipbuilding

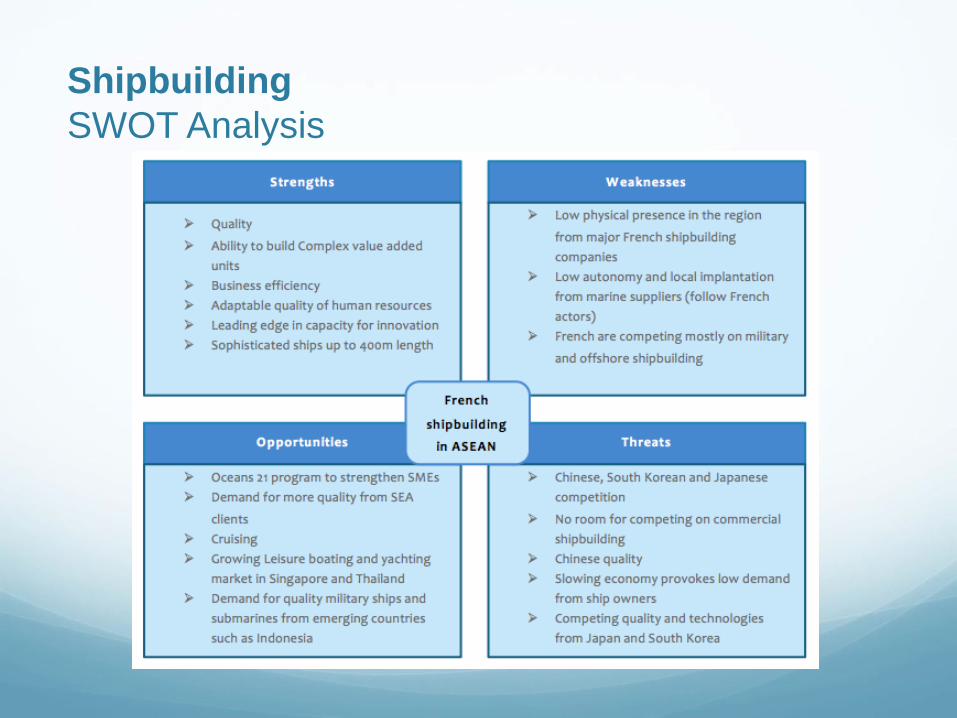

French position analysis

Some French achievements

(Piriou, OCEA…)

Higher prices but reliability

and quality

Partnerships and synergies

Focus on repair and

maintenance

Quality and technology offer

for the high-end market

• Growing demands and

untapped markets in SEA for

the French industry (Cruise

ships, yachting…)

Shipbuilding

SWOT Analysis

Shipbuilding

Recommendations

Seize the opportunities in repair and maintenance (« upgrading » of

the shipyards), cruise shipping and yachting markets

Take into account Chinese strategy of improving quality of their offer

(« up-scaling »)

Export SMEs expertise and technological know-how in the region

(Physical presence) via creating more synergies with French or local

contractors.

• Oceans 21

Insist on technological transfer and production/innovation in the region

(e.g. Thalès and its innovation hub) through building partnerships for

instance.

Market the French products right. Build on image of quality from French

shipbuilding and adapt offer to local clients.

• In this extent having physical presence, proximity with the clients can

be useful

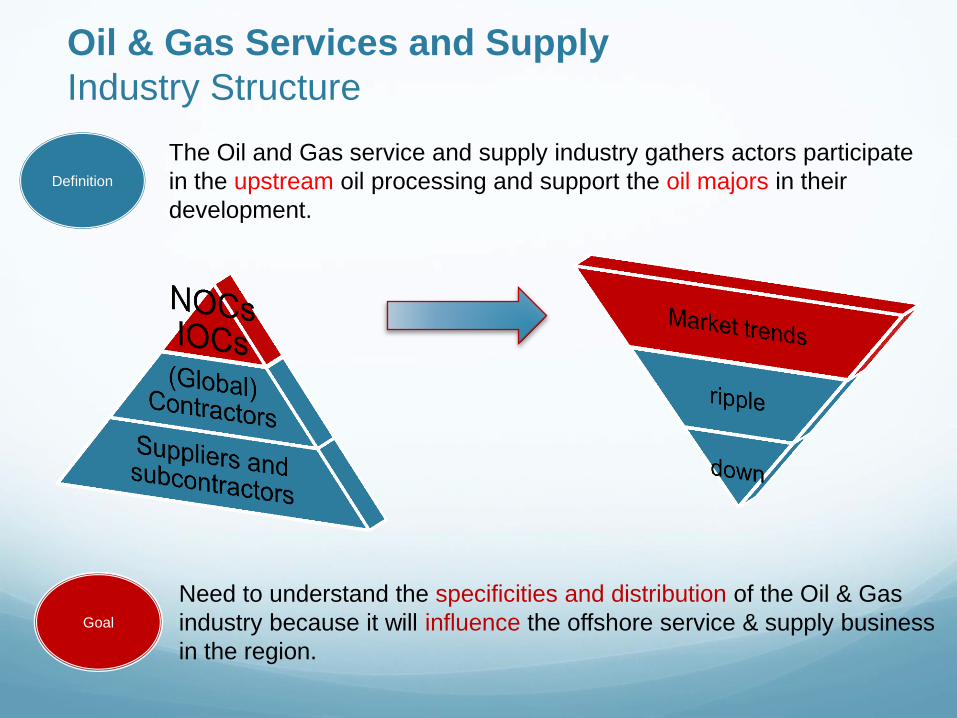

The Oil and Gas service and supply industry gathers actors participate

in the upstream oil processing and support the oil majors in their

development.

Definition

Goal

Need to understand the specificities and distribution of the Oil & Gas

industry because it will influence the offshore service & supply business

in the region.

Oil & Gas Services and Supply

Industry Structure

at end 20133 Surplus Oil Natural Gas

Million tones Million tones OE

Indonesia -31.12 28.78

Malaysia -1.61 31.59

Thailand -33.78 -9.42

Vietnam -0.40 0.00

Other ASEAN -81.21 21.10

Total Asia Pacific -1023.00 -135.12

Sources: (1) Market Line 2014 ; (2) Le Marin review 2015 ; (3) BP Statistics Review 2013

GAS ASEAN is a growing GAS market, offshore and mostly surface.

Oil & Gas Services and Supply

ASEAN Market

Volume

Value

- 30.44%

+4.21%

• Gas-producing and exporting region (soon pivot)

• Offshore2: 60% of oil and 50% of gas production

Sources: BP Statistics Review 2013

Natural Gas

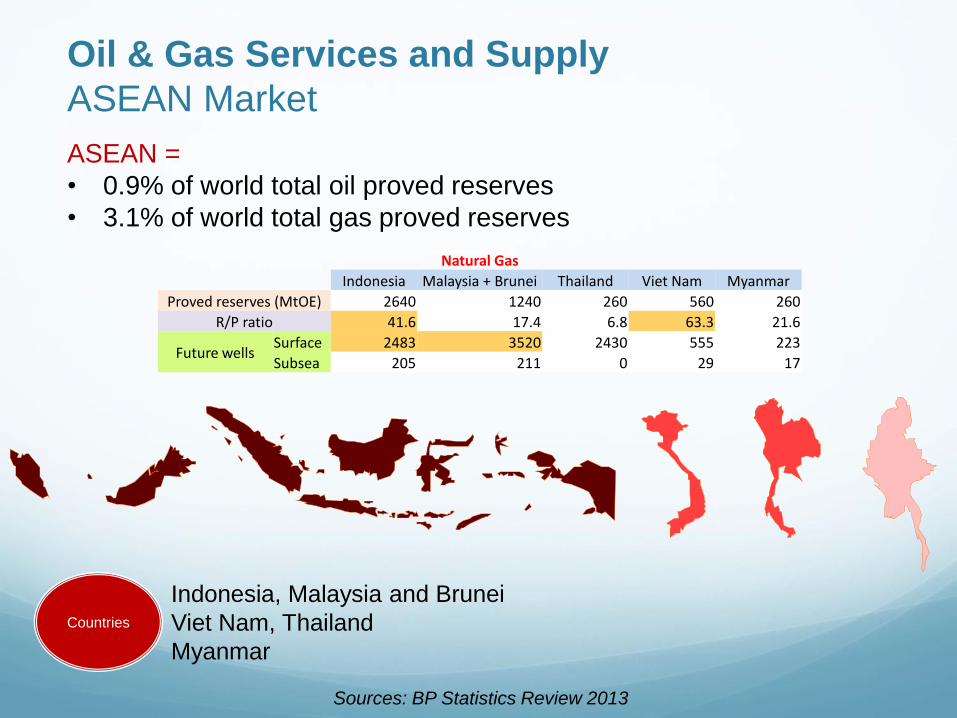

Indonesia Malaysia + Brunei Thailand Viet Nam Myanmar

Proved reserves (MtOE) 2640 1240 260 560 260

R/P ratio 41.6 17.4 6.8 63.3 21.6

Future wells Surface 2483 3520 2430 555 223

Subsea 205 211 0 29 17

ASEAN =

• 0.9% of world total oil proved reserves

• 3.1% of world total gas proved reserves

Oil & Gas Services and Supply

ASEAN Market

Countries

Indonesia, Malaysia and Brunei

Viet Nam, Thailand

Myanmar

Oil & Gas Services & Supply

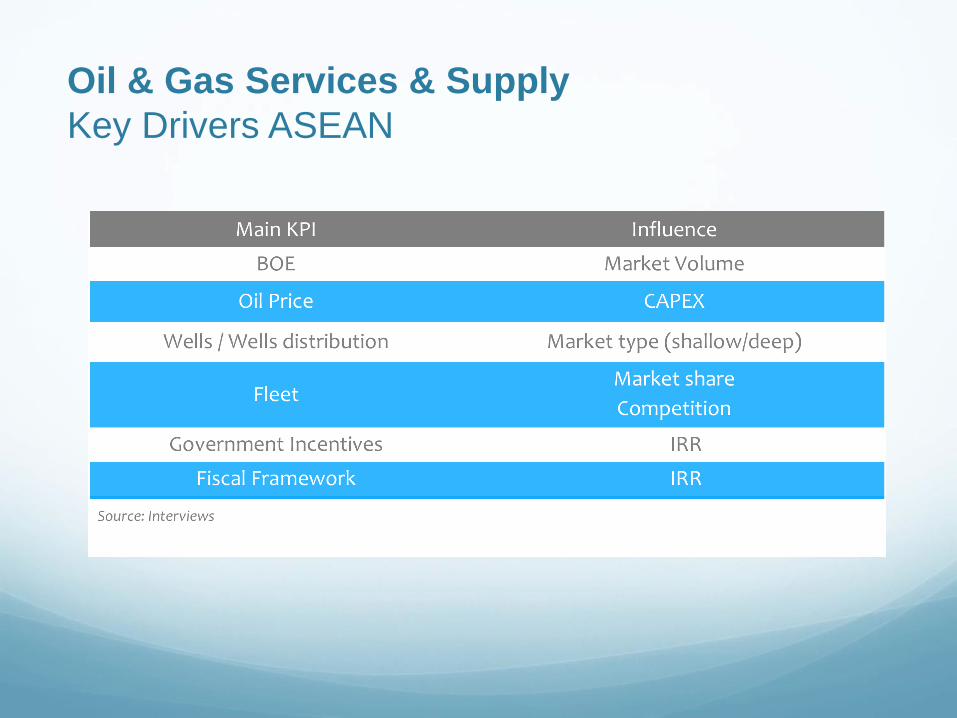

Key Drivers ASEAN

Oil & Gas Services & Supply

Market Trends

Slowdown in the industry because of the low barrel price

Offshore: shallow water wells remain the market majority and deep water wells expected to become operational

Gas sector will gain importance to supply China, Japan and Korea

Fiercer competition in the region

Growing regulatory constraints: « local content »

Opportunities in Myanmar, Brunei & Vietnam

NOC’s are the dominant operators in the region

Oil & Gas Services & Supply

SWOT Strengths

• World leader and the 2nd largest

exporter of offshore extraction support

services.

• Strong and acknowledged expertise in

deep and ultra-deep offshore

operations that is still prevailing over

local players in the region.

Threats • Local competition gaining experience.

even exporting their services

(SAPURA KENCANA - Malaysian

company)

• Low oil price and lack of visibility on the

situation

• Increase of "local content”

Opportunities

• Singapore is the hub for O&G in the

region.

• New oil & gas findings in the region

• Growing gas market

• Strong will from ASEAN countries to

become energy independent

• Services - Inspection, maintenance and

repair contracts - Offshore deep-market

Weaknesses

• French marine contractors are often too

hi-tech and cannot compete pricewise.

• French companies tend to be not local

enough.

French O&G industry

in ASEAN

Oil & Gas Services & Supply

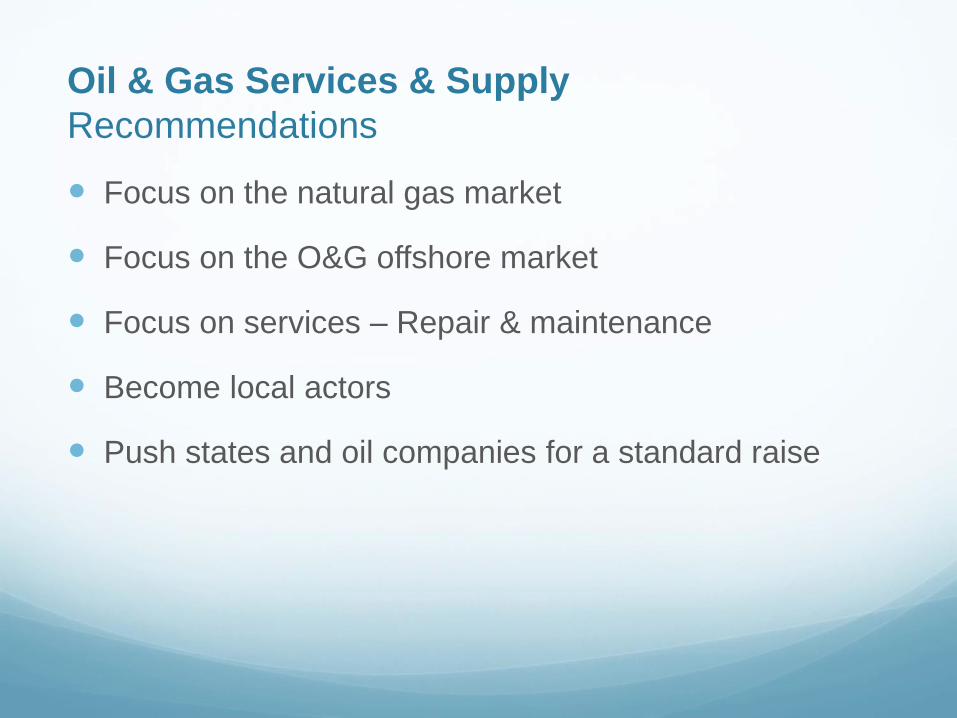

Recommendations

Focus on the natural gas market

Focus on the O&G offshore market

Focus on services – Repair & maintenance

Become local actors

Push states and oil companies for a standard raise

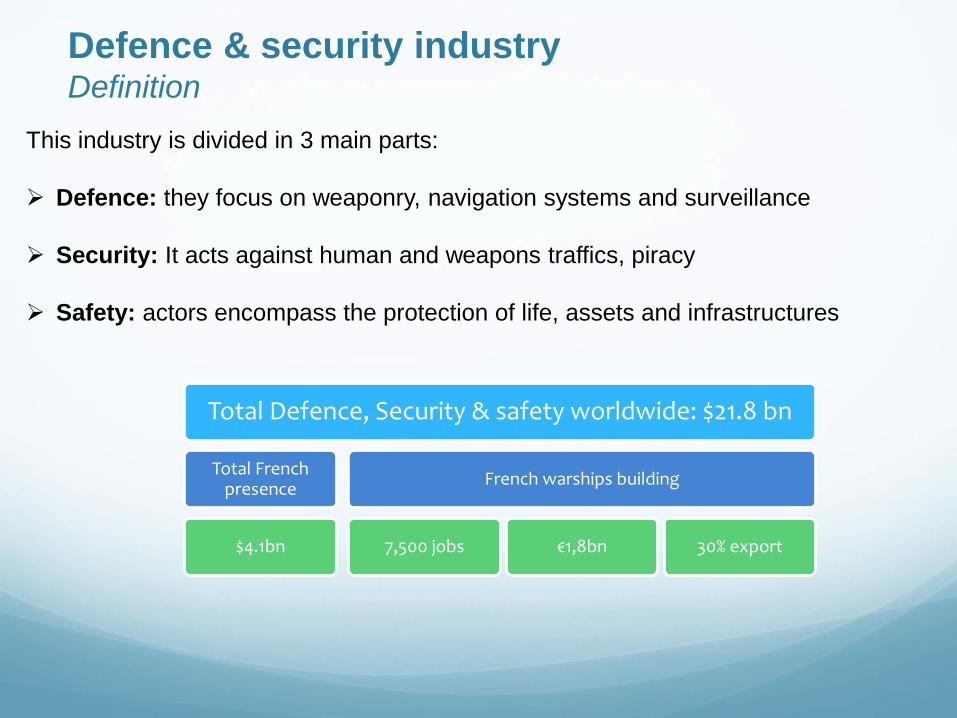

Defence & security industry Definition

Total Defence, Security & safety worldwide: $21.8 bn

Total French presence

$4.1bn

French warships building

7,500 jobs €1,8bn 30% export

This industry is divided in 3 main parts:

Defence: they focus on weaponry, navigation systems and surveillance

Security: It acts against human and weapons traffics, piracy

Safety: actors encompass the protection of life, assets and infrastructures

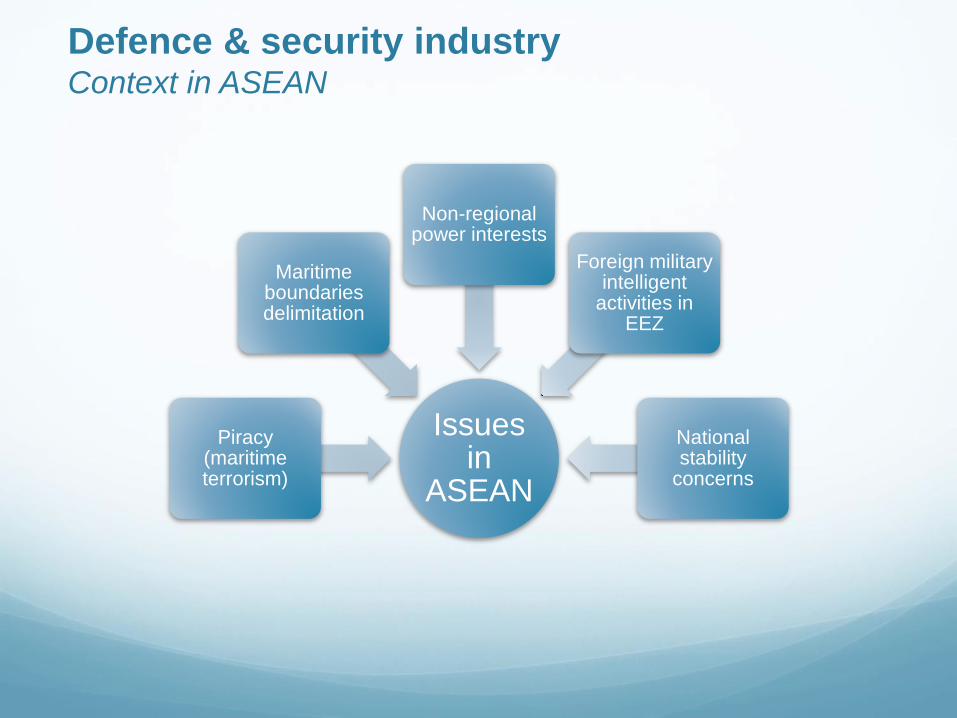

Issues in

ASEAN

Piracy (maritime terrorism)

Maritime boundaries delimitation

Non-regional power interests

Foreign military intelligent

activities in EEZ

National stability

concerns

Defence & security industry Context in ASEAN

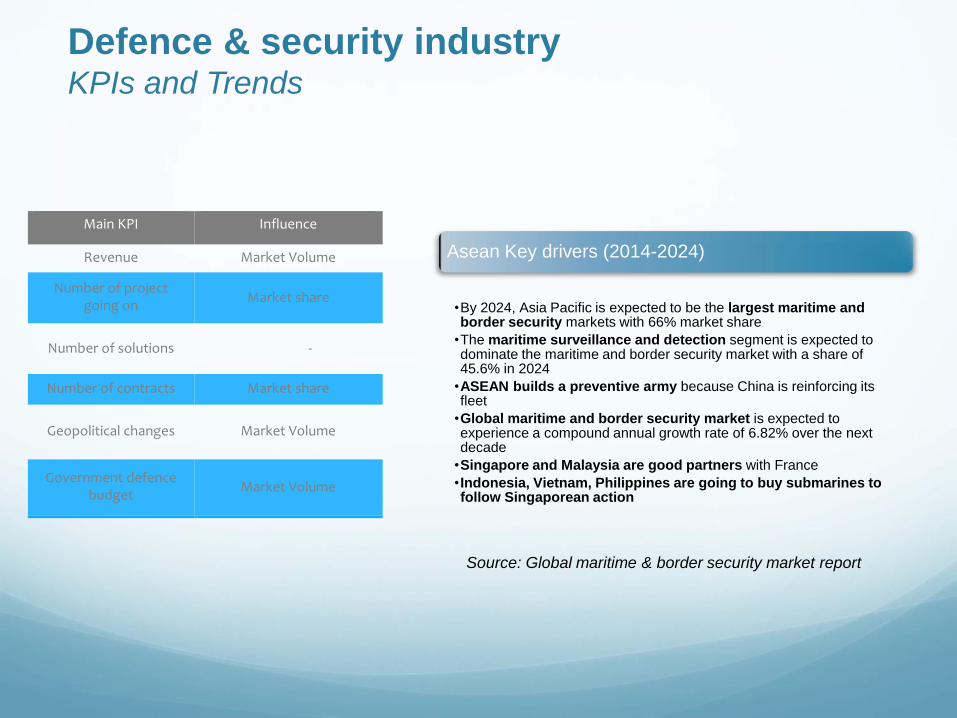

Defence & security industry KPIs and Trends

MainKPI Influence

Revenue MarketVolume

Numberofprojectgoingon

Marketshare

Numberofsolutions -

Numberofcontracts Marketshare

Geopoliticalchanges MarketVolume

Governmentdefencebudget

MarketVolume

Asean Key drivers (2014-2024)

•By 2024, Asia Pacific is expected to be the largest maritime and border security markets with 66% market share

•The maritime surveillance and detection segment is expected to dominate the maritime and border security market with a share of 45.6% in 2024

•ASEAN builds a preventive army because China is reinforcing its fleet

•Global maritime and border security market is expected to experience a compound annual growth rate of 6.82% over the next decade

•Singapore and Malaysia are good partners with France

•Indonesia, Vietnam, Philippines are going to buy submarines to follow Singaporean action

Source: Global maritime & border security market report

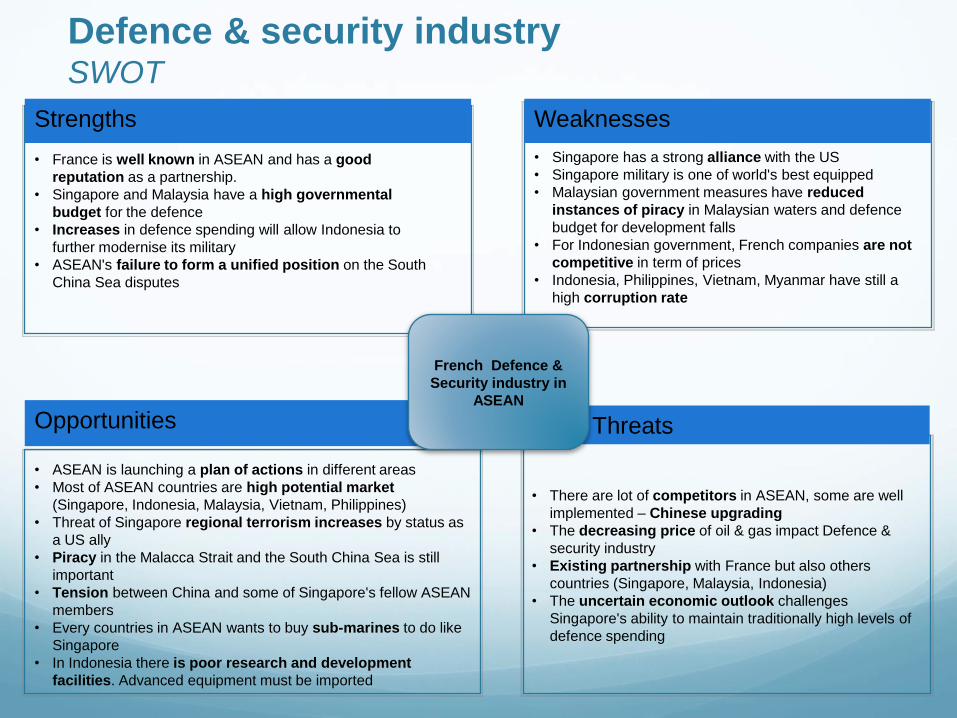

Defence & security industry SWOT

Strengths

• France is well known in ASEAN and has a good

reputation as a partnership.

• Singapore and Malaysia have a high governmental

budget for the defence

• Increases in defence spending will allow Indonesia to

further modernise its military

• ASEAN's failure to form a unified position on the South

China Sea disputes

Threats

• There are lot of competitors in ASEAN, some are well

implemented – Chinese upgrading

• The decreasing price of oil & gas impact Defence &

security industry

• Existing partnership with France but also others

countries (Singapore, Malaysia, Indonesia)

• The uncertain economic outlook challenges

Singapore's ability to maintain traditionally high levels of

defence spending

Opportunities

• ASEAN is launching a plan of actions in different areas

• Most of ASEAN countries are high potential market

(Singapore, Indonesia, Malaysia, Vietnam, Philippines)

• Threat of Singapore regional terrorism increases by status as

a US ally

• Piracy in the Malacca Strait and the South China Sea is still

important

• Tension between China and some of Singapore's fellow ASEAN

members

• Every countries in ASEAN wants to buy sub-marines to do like

Singapore

• In Indonesia there is poor research and development

facilities. Advanced equipment must be imported

Weaknesses

• Singapore has a strong alliance with the US

• Singapore military is one of world's best equipped

• Malaysian government measures have reduced

instances of piracy in Malaysian waters and defence

budget for development falls

• For Indonesian government, French companies are not

competitive in term of prices

• Indonesia, Philippines, Vietnam, Myanmar have still a

high corruption rate

French Defence &

Security industry in

ASEAN

Defence & security industry Recommendations

France is a major actor: Quality, Savoir-faire

The ASEAN plan of actions creates opportunities for the development of

French companies.

Military shipbuilding

o Capacity is more important than quantity of ships

o Submarines armament over every ASEAN countries

o High growth in ASEAN

Surveillance

o Opportunities to develop maritime surveillance in Indonesia (GICAN study)

o Illegal fishing in Indonesia is still huge (1bn €)

o Piracy is still high in Malacca and Singapore Strait

Maritime Transport

Definition

Total trade in ASEAN in 2013: USD 2,511,516.5 M

85% of overall value from containerized segment

1.5% of french trade made in ASEAN

The marine freight sector is defined as consisting of revenues

generated from freight transportation by ship of container and dry bulk

cargo, by sea and ocean going vessels

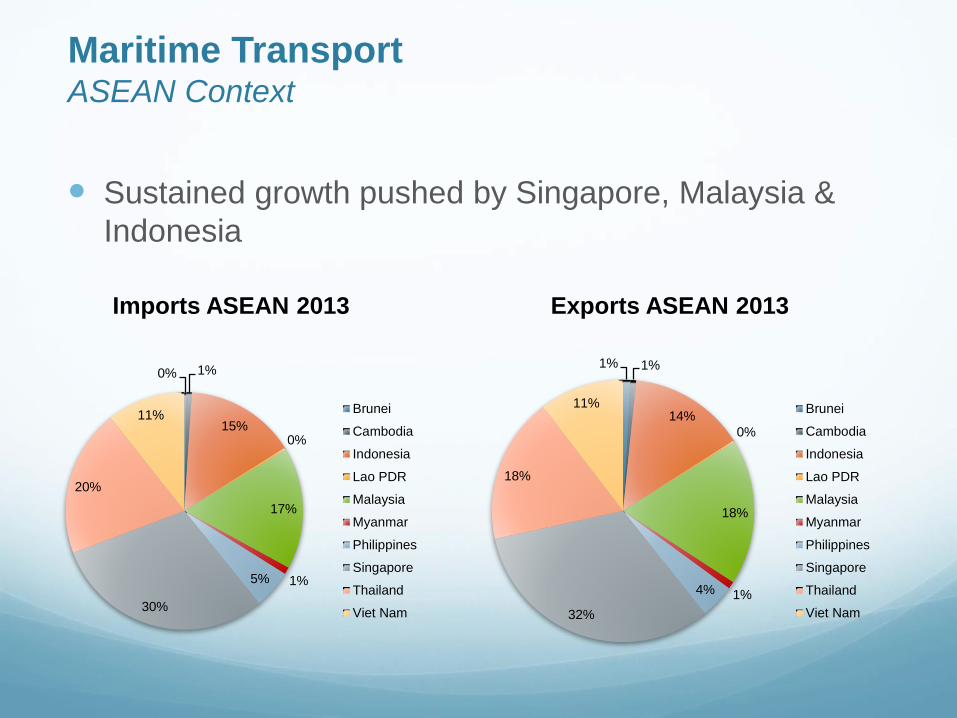

Sustained growth pushed by Singapore, Malaysia &

Indonesia

0% 1%

15% 0%

17%

1% 5%

30%

20%

11%

Imports ASEAN 2013

Brunei

Cambodia

Indonesia

Lao PDR

Malaysia

Myanmar

Philippines

Singapore

Thailand

Viet Nam

1% 1%

14%

0%

18%

1% 4%

32%

18%

11%

Exports ASEAN 2013

Brunei

Cambodia

Indonesia

Lao PDR

Malaysia

Myanmar

Philippines

Singapore

Thailand

Viet Nam

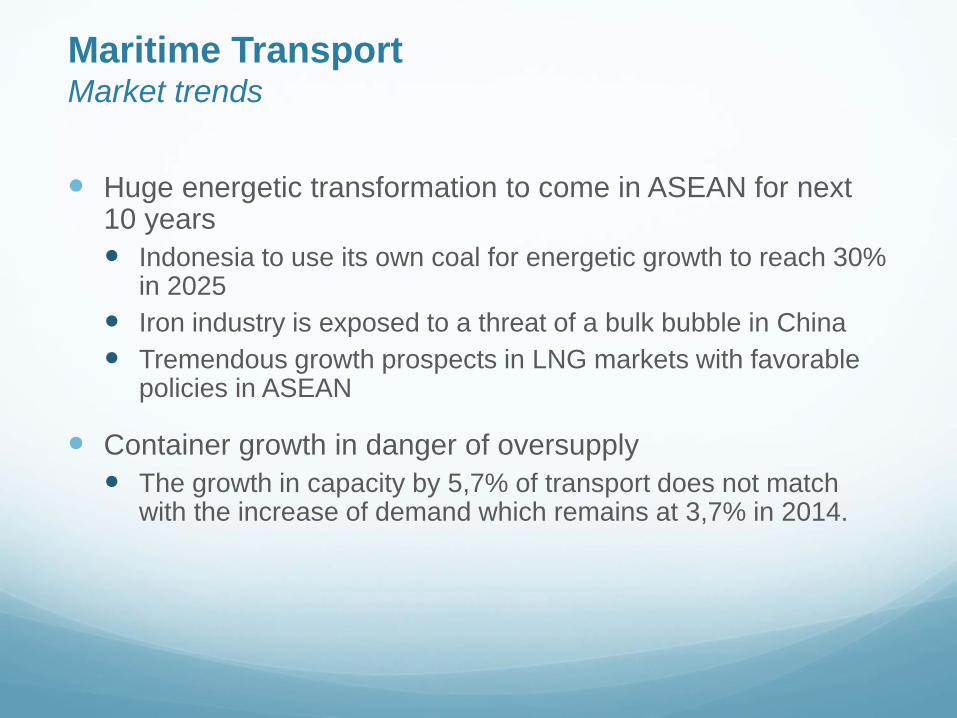

Maritime Transport ASEAN Context

Huge energetic transformation to come in ASEAN for next 10 years

Indonesia to use its own coal for energetic growth to reach 30% in 2025

Iron industry is exposed to a threat of a bulk bubble in China

Tremendous growth prospects in LNG markets with favorable policies in ASEAN

Container growth in danger of oversupply

The growth in capacity by 5,7% of transport does not match with the increase of demand which remains at 3,7% in 2014.

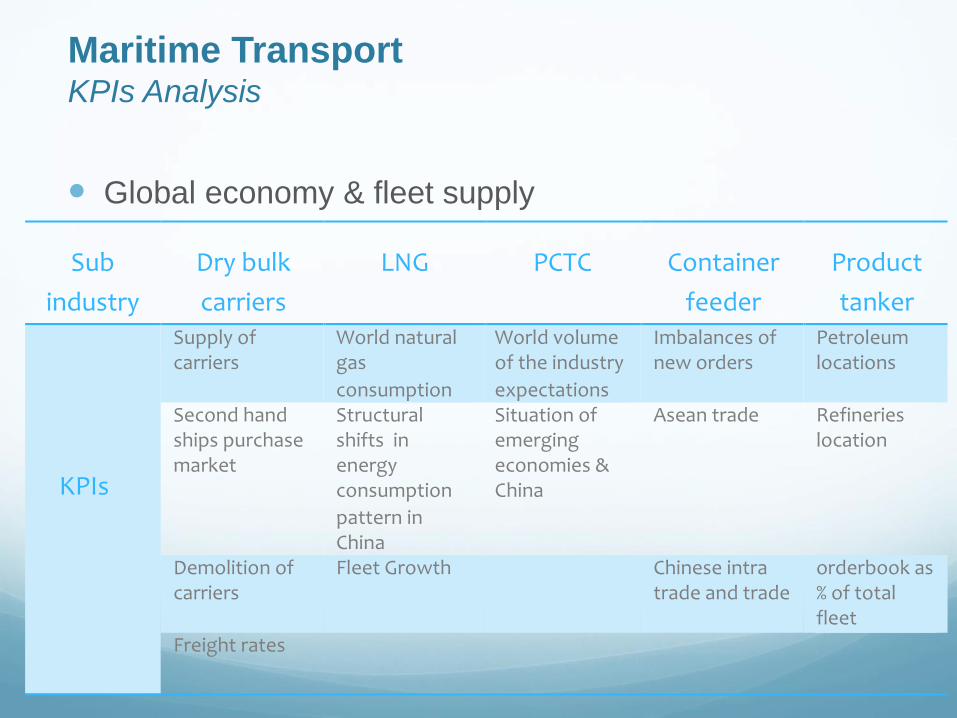

Maritime Transport Market trends

Global economy & fleet supply

Sub

industry

Drybulk

carriers

LNG PCTC Container

feeder

Product

tanker

KPIs

Supplyofcarriers

Worldnaturalgas

consumption

Worldvolumeoftheindustry

expectations

Imbalancesofneworders

Petroleumlocations

Secondhandshipspurchasemarket

Structuralshiftsinenergyconsumption

patterninChina

Situationofemergingeconomies&China

Aseantrade Refinerieslocation

Demolitionofcarriers

FleetGrowth Chineseintratradeandtrade

orderbookas%oftotalfleet

Freightrates

Maritime Transport KPIs Analysis

French Shipping industry should closely follow the

energetic transformations about to happen in ASEAN

(except containers)

Monitor the medium size fleet (3500-5000 EVP) shifting

of market due to crew’s prices to attract potential new

opportunities

Maritime Transport Recommendations

Peripheral activities provide services to other actors of the marine industry like financing,

certification, insurance.

We especially focused on:

Classification and certification:

• follow the ships and their equipment from their building to their decommissioning

• help and ensure compliance with quality, health, safety, and environmental requirements

of the maritime industry.

Insurance:

• insure transporters and operators in international trade

• against the financial consequences of incidents involving the ships and the goods they

carry.

• insurance revenues can be devided into 4 major categories (data from 2012)

• 50% accountable for all types of cargoes

• 20% for hulls

• 15% for yachting

• 15% for 3rd party and transporters

Banking:

• department specialized in shipping finance

• major investors in the marine industry from merchant fleet to aquaculture depending on the

bank.

Peripheral Services Definition

The classification and certification sector:

highly competitive and fragmented with over 20 companies present in the region

5 of them control more than 1/2 of the total market shares

ASEAN Key Findings

• 95% of boat construction is happening in Asia --> importance to be visible

• Offer>Demand in boat construction --> need to find other sources of revenue

• Boats orders are increasing and need specific research before certification

• Classed fleet growth was linked to a strong increase in ships already in service being transferred in 2013 not sustainable for next years

• Increased number of services offered to the companies like research center

ASEAN Opportunities

• shipping : new investments leading to new potential markets

• offshore :

• subsea: big floating units coming from Korea represent new clients

• deepsea: new market to enter

• maintenance: Asset Integrity Management development

Peripheral Services Classification and certification

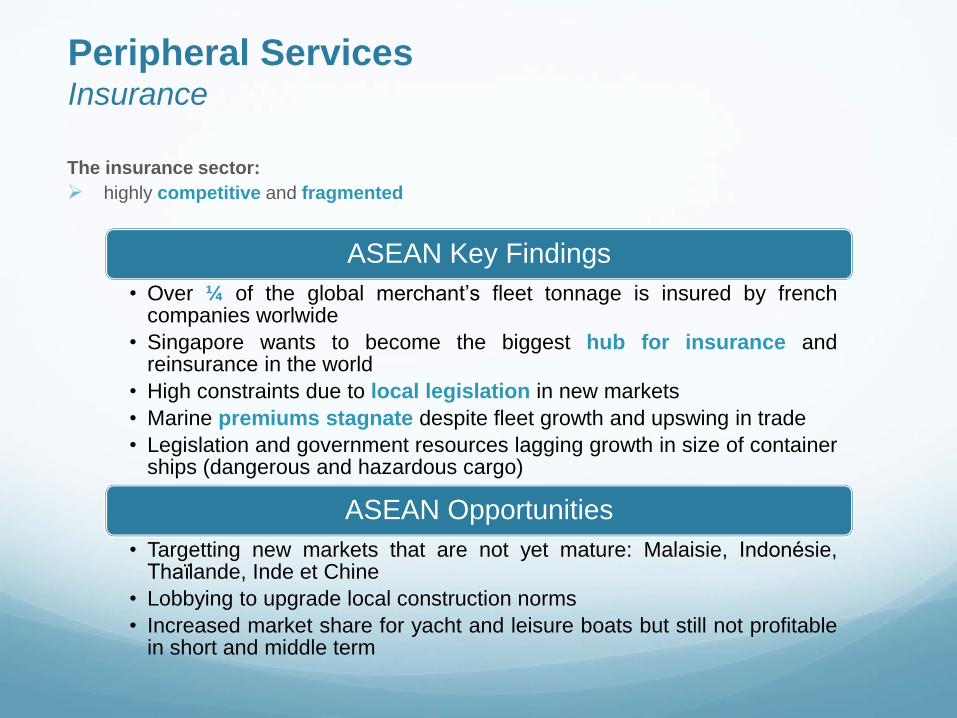

The insurance sector:

highly competitive and fragmented

ASEAN Key Findings

• Over ¼ of the global merchant’s fleet tonnage is insured by french companies worlwide

• Singapore wants to become the biggest hub for insurance and reinsurance in the world

• High constraints due to local legislation in new markets

• Marine premiums stagnate despite fleet growth and upswing in trade

• Legislation and government resources lagging growth in size of container ships (dangerous and hazardous cargo)

ASEAN Opportunities

• Targetting new markets that are not yet mature: Malaisie, Indonesie, Thailande, Inde et Chine

• Lobbying to upgrade local construction norms

• Increased market share for yacht and leisure boats but still not profitable in short and middle term

Peripheral Services Insurance

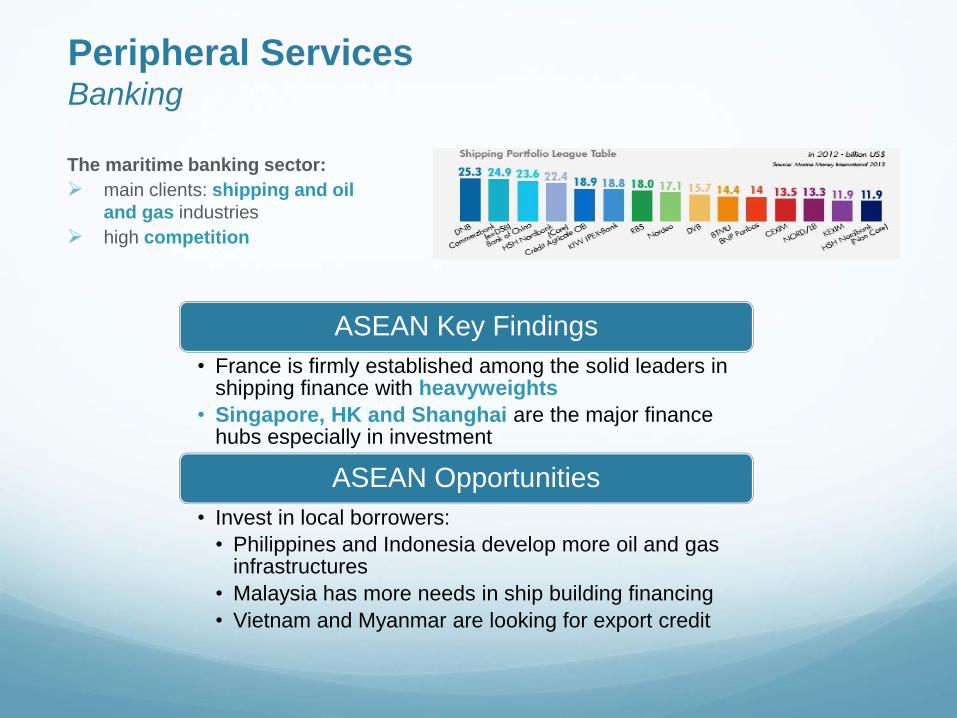

The maritime banking sector:

main clients: shipping and oil

and gas industries

high competition

ASEAN Key Findings

• France is firmly established among the solid leaders in shipping finance with heavyweights

• Singapore, HK and Shanghai are the major finance hubs especially in investment

ASEAN Opportunities

• Invest in local borrowers:

• Philippines and Indonesia develop more oil and gas infrastructures

• Malaysia has more needs in ship building financing

• Vietnam and Myanmar are looking for export credit

Peripheral Services Banking

Way Ahead Recommendations for the future

After gaining a broad understanding of the French Maritime Industry in the

region, we recommend to look into the following topics in the future:

Explore the positioning of French products and services in SEA. Analyse

Marketing strategy of French actors and propose ways to improve it?

Benchmark competition in the region.

Monitor green technologies: How does the competition look like in the region

(Norwegian, German…?) and what are the opportunities in the South East

Asian market?

Politics and lobbying actions: How to create more synergies between the

Cluster and institutional and commercial actors (French government) to

promote French business in the region (Océans 21 program; Bilateral treaties

between French and local governments)?

Monitor political and legal evolutions. stay aware of favourable legislations

and incentives programs from SEA governments and communicate to French

companies