Dean Michael MeadResearch Manager

Governmental Accounting Standards Board

Maryland Association of CPAsApril 30, 2010

GAAP Update

The opinions expressed in this presentation are those of the presenter. Official positions of the GASB are established only after extensive public due process and deliberation.

Overview

Fund Balance Reporting and Governmental Fund Type DefinitionsAgent Multiple-employer OPEB PlansAICPA CodificationFASB Codification ProjectPension Reexamination ProjectStatement 14 Reexamination Project

Statement No. 54

Released March 11, 2009Effective for periods beginning after June 15, 2010

New Fund Balance Classifications

NonspendableRestrictedCommittedAssignedUnassigned

Essentially what is now

reserved

Essentially what is now unreserved

Essentially what is now designated

The classification hierarchy is “based primarily on the extent to which the government is bound to honor constraints on the specific purposes for which amounts…can be spent”

Nonspendable Fund Balance

Not in spendable form, such as– Inventory– Long-term amounts of loans and notes

receivable– Property held for resale

However, if the use of the proceeds from the collection of receivables or sale of the property is restricted, committed, or assigned, then the receivables or property should be reported in those categories

Corpus of a permanent fund

Restricted Fund Balance

Same definition as for net assets in Statement 34 (as amended by Statement 46)—amounts constrained to being used for a specific purpose by– External parties– Constitutional provisions– Enabling legislation

Committed Fund Balance

Constraint on use imposed by the government itself, using its highest level of decision making authorityConstraint can be removed or changed only by taking the same highest-level actionAction to constrain resources should occur prior to end of fiscal year, though the exact amount may be determined subsequently

Assigned Fund Balance

Amounts intended to be used for specific purposesRequired, not optionalIntent is expressed by – The governing body– High-level body or individual authorized by

the governing body

Assigned Fund Balance

Amounts in governmental funds other than the general fund that are not restricted or committed are reported as assigned– The act of transferring resources to another

governmental fund is considered an assignment of those resources to the purpose of that fund

Assigned Fund Balance

Appropriation of existing fund balance to eliminate a projected budgetary deficit in the next year’s budget is an assignment of fund balance– Limited to an amount no greater than the

projected excess of expenditures over revenues

Unassigned Fund Balance

Available for any purposeReported only in the general fund, except in cases of negative fund balance– Negative balances in other governmental

funds are reported as unassigned

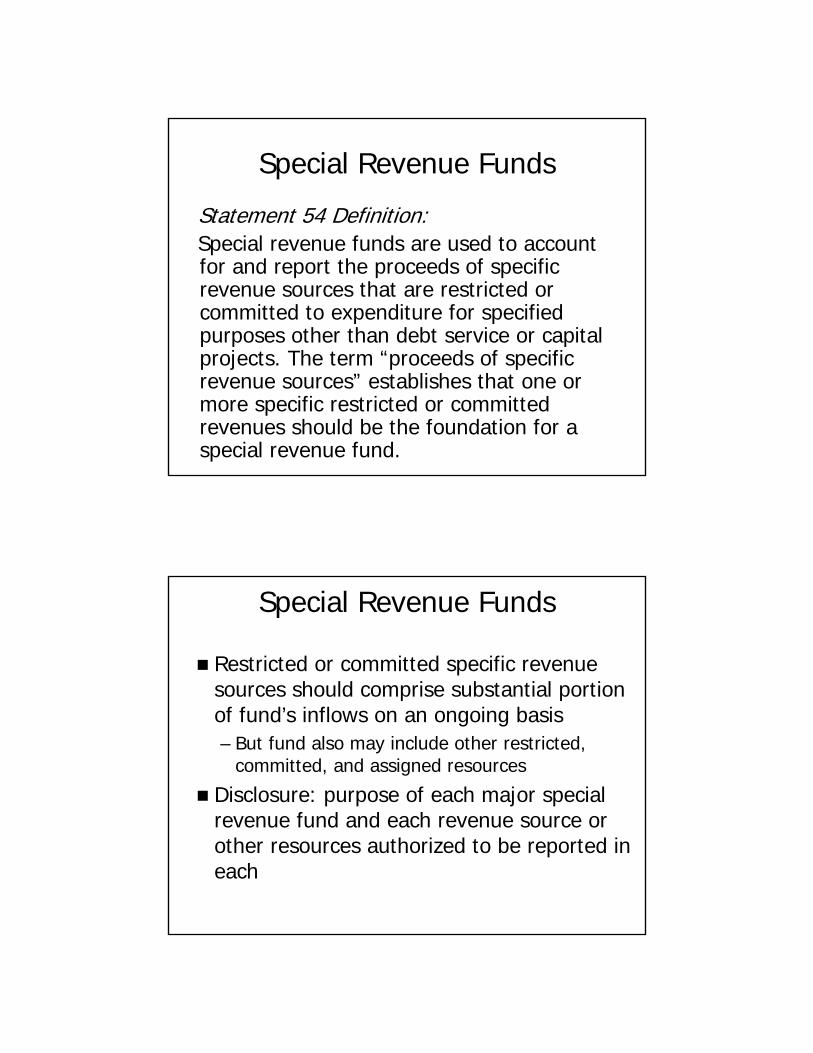

Current Definition:Special Revenue Funds —To account for the proceeds of specific revenue sources (other than trusts for individuals, private organizations, or other governments or for major capital projects) that are legally restricted to expenditure for specified purposes.

Special Revenue Funds

Special Revenue Funds

Statement 54 Definition:Special revenue funds are used to account for and report the proceeds of specific revenue sources that are restricted or committed to expenditure for specified purposes other than debt service or capital projects. The term “proceeds of specific revenue sources” establishes that one or more specific restricted or committed revenues should be the foundation for a special revenue fund.

Special Revenue Funds

Restricted or committed specific revenue sources should comprise substantial portion of fund’s inflows on an ongoing basis– But fund also may include other restricted,

committed, and assigned resources

Disclosure: purpose of each major special revenue fund and each revenue source or other resources authorized to be reported in each

Effect of SRF Clarifications

Less restrictive More restrictive

Current Standards

New Standards

Current Practice

Debt Service & Capital Projects Funds

Text made consistent with other definitionsCapital projects funds broadened from “major capital facilities” to “capital outlays”Should be clearer that debt service funds are required when– Legally mandated– Financial resources are being accumulated for

principal and interest payments maturing in future years

Classifying Residual Balances

Example: The flow assumption for a special revenue fund is to use restricted amounts before unrestricted amounts and to use the default policy for its unrestricted fund balance.

If expenditures incurred exceed the amounts that have been restricted, committed, and assigned to a specific purpose, resulting in a negative residual amount for that specific purpose, then amounts assigned to other purposes in that fund are reduced to eliminate the deficit.

Purpose A Total Restricted Committed AssignedBeginning Balances 5,696 2,000 2,616 1,080AdditionsExpenditures IncurredEnding Balances

Purpose BBeginning Balances 8,871 8,871 0 0AdditionsExpenditures IncurredEnding Balances

Purpose CBeginning Balances 8,040 0 0 8,040AdditionsExpenditures IncurredEnding Balances

What were the balances at the beginning of the year?

Purpose A Total Restricted Committed AssignedBeginning Balances 5,696 2,000 2,616 1,080AdditionsExpenditures IncurredEnding Balances

Purpose BBeginning Balances 8,871 8,871 0 0Additions 1,500 1,500Expenditures IncurredEnding Balances

Purpose CBeginning Balances 8,040 0 0 8,040Additions 120,000 120,000Expenditures IncurredEnding Balances

Were additional amounts restricted, committed, or assigned?

Purpose A Total Restricted Committed Assigned UnassignedBeginning Balances 5,696 2,000 2,616 1,080AdditionsExpenditures Incurred (7,654) (2,000) (2,616) (1,080) (1,958)Ending Balances (1,958) 0 0 0 (1,958)

Purpose BBeginning Balances 8,871 8,871 0 0Additions 1,500 1,500Expenditures Incurred (10,000) (8,871) (1,129)Ending Balances 371 0 0 371

Purpose CBeginning Balances 8,040 0 0 8,040Additions 120,000 120,000Expenditures Incurred (11,223) (11,223)Ending Balances 116,817 0 108,777 8,040

How much was spent for each purpose?

Purpose A Total Restricted Committed Assigned UnassignedBeginning Balances 5,696 2,000 2,616 1,080AdditionsExpenditures Incurred (7,654) (2,000) (2,616) (1,080) (1,958)Ending Balances (1,958) 0 0 0 (1,958)

Purpose BBeginning Balances 8,871 8,871 0 0Additions 1,500 1,500Expenditures Incurred (10,000) (8,871) (1,129)Ending Balances 371 0 0 371

Purpose CBeginning Balances 8,040 0 0 8,040Additions 120,000 120,000Expenditures Incurred (11,223) (11,223)Ending Balances 116,817 0 108,777 8,040

What happens to a negative balance?

Implementation Issues

What if a government is required to report on its reserved and unreserved fund balance or to maintain a certain level of unreserved fund balance?

General rule, according to NCGA Statement 1: laws or regulations do not supersede GAAP

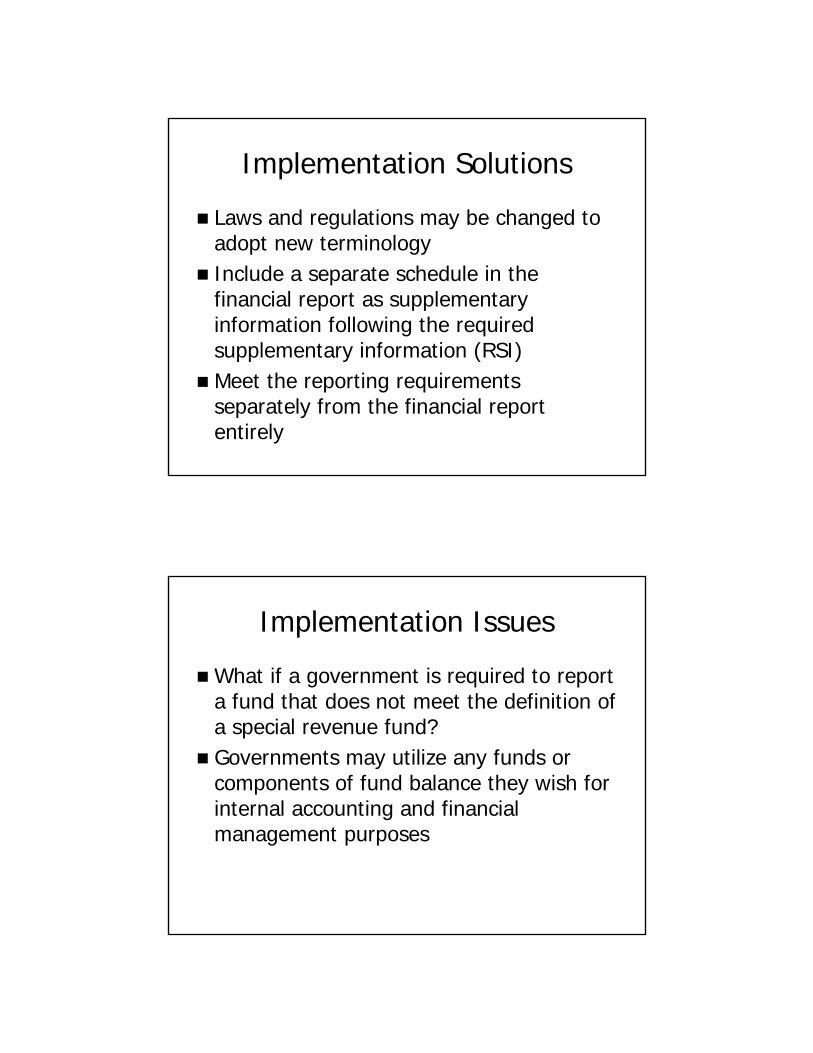

Implementation Solutions

Laws and regulations may be changed to adopt new terminologyInclude a separate schedule in the financial report as supplementary information following the required supplementary information (RSI)Meet the reporting requirements separately from the financial report entirely

Implementation Issues

What if a government is required to report a fund that does not meet the definition of a special revenue fund?Governments may utilize any funds or components of fund balance they wish for internal accounting and financial management purposes

Implementation Issues

Statement 54 holds no sway over internal practices; it does, however, govern what may be reported in GAAP financial statements.Legal or regulatory requirements can be met outside of the financial statements– You cannot be required to do something in

GAAP financial statements that is inconsistent with GAAP

Implementation Solutions

Include a separate schedule reporting the fund, following the RSIMeet the reporting requirements separately from the financial report entirely

Implementation Issues

Q: If a government doesn’t have any committed resources, or doesn’t have a procedure that meets the criteria for committing resources, what should we report?

A: Nothing. Governments are not required to report fund balance classifications that are not applicable to them.

Statement No. 57Accounting and Financial

Reporting by Employers for Postemployment Benefits

Other Than Pensions

Issued December 2009

OPEB Measurements by Agent Employers and Agent Multiple-

Employer PlansObjectives─to address issues related to:– The use of the alternative measurement method – The frequency and timing of measurements by

employers that participate in agent multiple-employer other postemployment benefit (OPEB)

Alternative Measurement Method

Statement 45—amended to permit an agent employer that has an individual-employer OPEB plan with fewer than 100 total plan members to use the alternative measurement method

Alternative Measurement Method

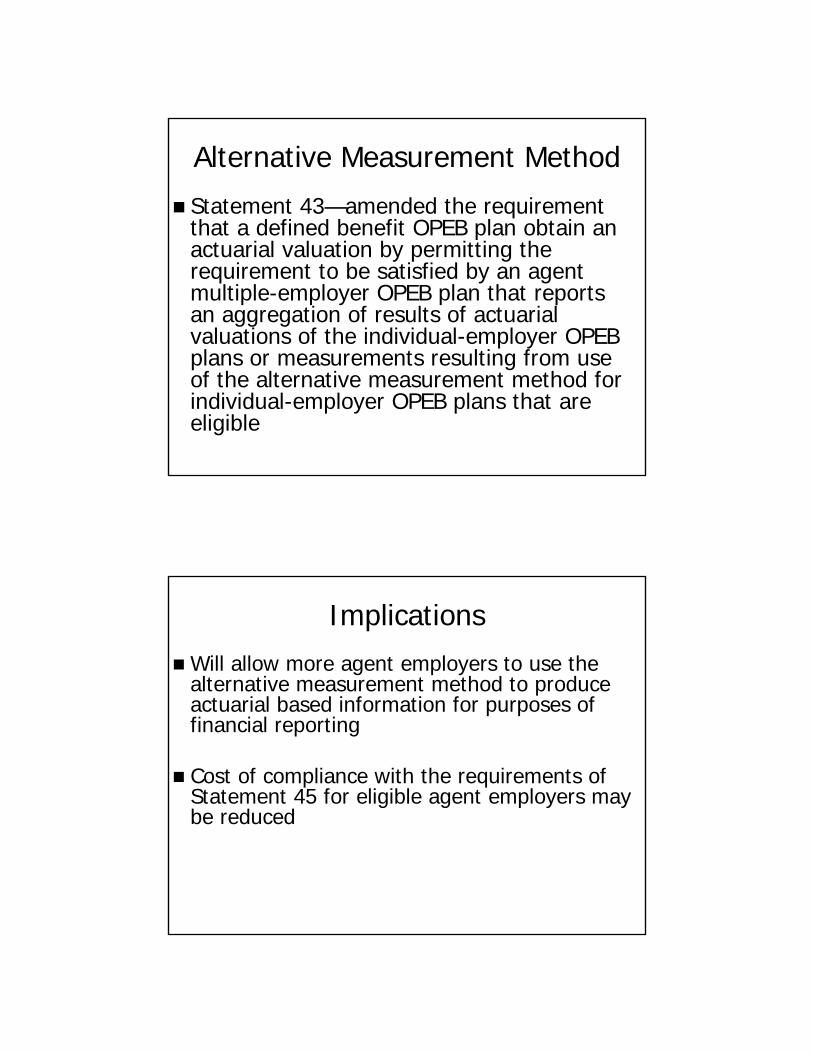

Statement 43—amended the requirement that a defined benefit OPEB plan obtain an actuarial valuation by permitting the requirement to be satisfied by an agent multiple-employer OPEB plan that reports an aggregation of results of actuarial valuations of the individual-employer OPEB plans or measurements resulting from use of the alternative measurement method for individual-employer OPEB plans that are eligible

Implications

Will allow more agent employers to use the alternative measurement method to produce actuarial based information for purposes of financial reporting

Cost of compliance with the requirements of Statement 45 for eligible agent employers may be reduced

Actuarial ValuationsStatement 43—clarifies that when actuarially determined OPEB measures are reported by an agent multiple-employer OPEB plan and its participating employers, those measures should be determined– as of a common date– at a minimum frequency to satisfy the agent

multiple-employer OPEB plan’s financial reporting requirements

Will improve the consistency of reporting with regard to funded status and funding progress information

Effective Date and Transition

Provisions related to the use and reporting of the alternative measurement method are effective immediatelyProvisions related to the frequency and timing of measurements are effective for actuarial valuations first used to report funded status information in OPEB plan financial statements for periods beginning after June 15, 2011Earlier application is encouraged.

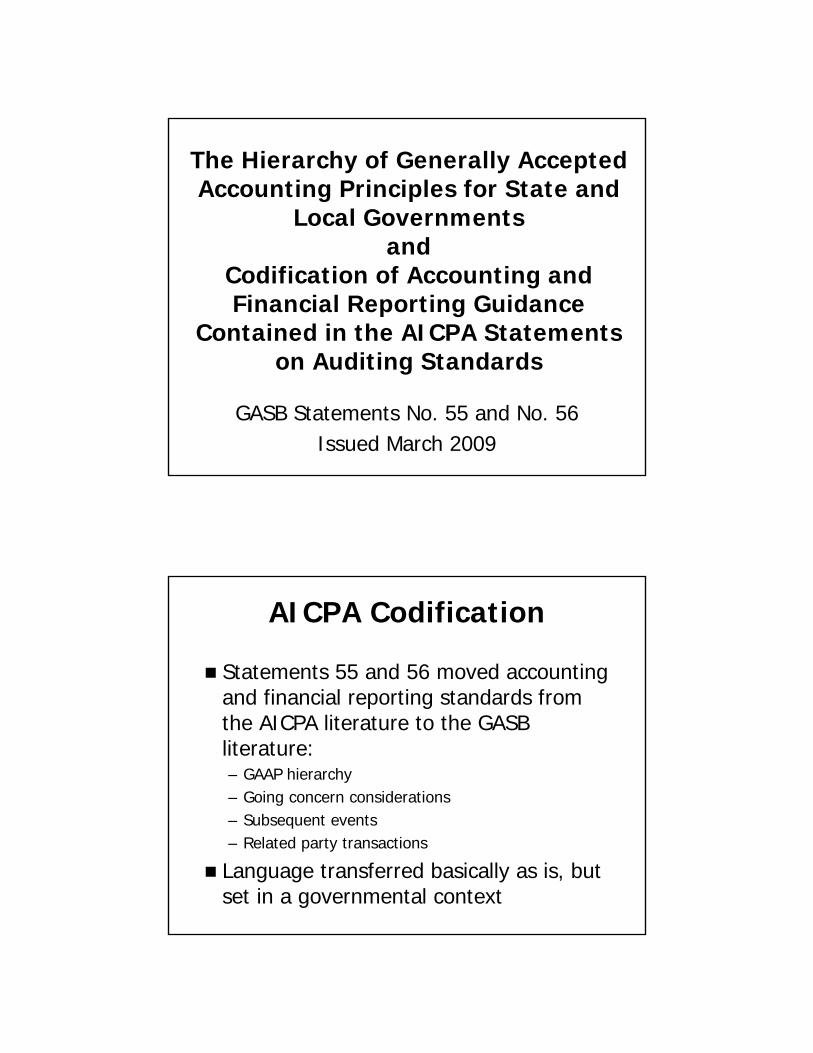

The Hierarchy of Generally Accepted Accounting Principles for State and

Local Governmentsand

Codification of Accounting and Financial Reporting Guidance

Contained in the AICPA Statements on Auditing Standards

GASB Statements No. 55 and No. 56Issued March 2009

AICPA Codification

Statements 55 and 56 moved accounting and financial reporting standards from the AICPA literature to the GASB literature:– GAAP hierarchy– Going concern considerations– Subsequent events– Related party transactions

Language transferred basically as is, but set in a governmental context

Codification of Pre-November 30, 1989

FASB Pronouncements

Exposure Draft Issued January 2010

Overview of the Project

Since FASB introduced its codification, its original pronouncements are nonauthoritativeParagraph 17 of Statement 34 requires application of pre-November 30, 1989, FASB pronouncements, unless they conflict with or contradict GASB pronouncements Project objective: Specifically identify those provisions in FASB Statements and Interpretations, APB Opinions, ARBs, and AICPA Accounting Interpretations, and incorporate those provisions into the GASB’s literature

Tentative DecisionsStatement 20 would be superseded– All applicable pre-11/30/89 standards would be

contained in the GASB’s codification– All potentially applicable post-11/30/89 non-

GASB standards would be “other accounting literature”

Guidance on 29 topics would be brought into the GASB literature, including:– Capitalization of interest costs (FAS 34)– Statement of net assets classification (ARB 43,

APB 12 & FAS 6)

Tentative Decisions– Special and extraordinary items (APB 30)– Comparative financial statements (ARB 43)– Related parties (FAS 57)– Prior-period adjustments (FAS 16 & APB 9)– Accounting changes and error corrections (APB

20 and FIN 20)– Contingencies (FAS 5 & FIN 14)– Extinguishments of debt (APB 26 & FAS 76)– Troubled debt restructuring (FAS 15)– Inventory (ARB 43)– Leases (FAS 13, 22 & 98 & FIN 23, 26 & 27)

Tentative Decisions– Sales of real estate (FAS 66)– Real estate projects (FAS 67)– Research and development arrangements (FAS

68)– Broadcasters (FAS 63)– Cable television systems (FAS 51)– Insurance enterprises (FAS 60)– Lending activities (FAS 91)– Mortgage banking activities (FAS 65)– Regulated operations (FAS 71, 90 & 101)

Due ProcessExposure Draft issued January 29Comment period of six monthsExposure Draft includes:– Crosswalk from original standards to paragraphs

in the Exposure Draft– Listings of FASB and AICPA original

pronouncements (numerically and topically) and their applicability

– Mark-up of the applicable FASB and AICPA original pronouncements

Preliminary Views expectedin June 2010

Postemployment Benefit Accounting and Financial

Reporting Project

Project Objectives

To evaluate existing standards for pension and OPEB accounting and reporting to determine if they effective—in other words, do they:– Provide decision-useful information?– Support accountability?– Assist in assessing interperiod equity?

Project History

Conducted two years of research into current practiceIssued an Invitation to Comment in early 2009 raising issues from the research, considering potential solutions, and seeking public input—over 100 responses, two public hearings, consultations with GASAC, and a task force meetingDeliberations resumed in October

Tentative Decisions So Far

Preliminary Views will focus solely on fundamental employer pension accounting and financial reporting issues presented in the Invitation to Comment. Additional project issues, including accounting and financial reporting by employers for postemployment benefits other than pensions, will be addressed separately.

Tentative Decisions So Far

A sole or agent employer incurs a pension obligation to its employees (however measured) as a part of the exchange between the employer and its employees of salaries and benefits, including defined pension benefits, for employee services (the employment exchange).

Tentative Decisions So Far

The pension plan becomes the primary obligor, and the employer becomes the secondary obligor, for the pension obligation to the extent that plan assets have been accumulated to provide for the payment of benefits to employees or their beneficiaries when due. The employer remains the primary obligor for that pension obligation to the extent that it is unfunded.

Tentative Decisions So Far

The unfunded accrued benefit obligation (however measured) meets the definition of a liability It is measurable with sufficient reliability to be recognized as a liability in the basic financial statements of a sole or agent employer.

Tentative Decisions So Far

The effects of the following projected future changes should be included in the projection of benefits for the purpose of measurement of the pension liability:

Automatic cost-of-living adjustments (COLAs)Projected future ad hoc COLAs, referring in this context to COLAs that are dependent upon a decision to grant by a responsible authority, when certain criteria for inclusion (to be further discussed at a subsequent meeting) are met

Tentative Decisions So Far

The effects of the following projected future changes should be included in the projection of benefits for the purpose of measurement of the pension liability:

Projected future salary increases in circumstances in which the pension benefit formula is based on future compensation levelsProjected future service credits, both in determining an employee’s probable eligibility for benefits and in the projection of benefits in circumstances in which the pension benefit formula is based on years of service.

Tentative Decisions So FarTo the extent current and projected pension plan assets are projected to be sufficient to provide for payment of benefits in future periods, the projected benefit payments should be discounted at the long-term expected yield on plan assets. Additional benefit payments, if any, projected beyond the point at which plan assets are projected to be fully depleted, should be discounted using an appropriate high-quality municipal bond index rate.

Tentative Decisions So FarEntry age actuarial cost method should be used to attribute the present value of expected future benefit payments to financial-reporting periods on a level-percentage-of-payroll basis for liability measurement and expense recognition purposes.

Tentative Decisions So Far

Benefits should be attributed to periods beginning in the first period in which the employee’s services lead to benefits under the plan (whether or not the benefits are conditional on further service, as is the case, for example, with vesting provisions) and ending in the last period in which the employee’s services lead to additional benefits under the plan, as the result of an additional service credit or a change in the final salary or final average salary on which the benefit is based. If the plan terms do not specify a period, benefits should be attributed over the total projected periods of employee service.

Tentative Decisions So Far

Defer and amortize over the remaining service lives of individual plan members:– Differences between assumed and actual

experience with regard to demographic and economic factors affecting the measurement of the employer’s pension liability

– Changes in the demographic and economic assumptions used in the measurement of the employer’s pension liability

– Benefit changes that are applied retroactively to past periods of service of plan members

Tentative Decisions So FarRecognition of pension investment earnings above or below the expected long-term rate of return should be deferred so long as the net cumulative amount of deferred outflow or net cumulative amount of deferred inflow remains within a corridor 15 percent above and below the fair value of assets.However, if the net cumulative deferred balance at the end of a financial reporting period falls outside the corridor, the amount outside the corridor should be recognized as pension expense immediately.

Tentative Decisions So FarWith regard to employers in cost-sharing multiple-employer plans:– The basis for determining liability and expense would be

the employer’s proportionate share of the collective unfunded liability, based on the employers share of the total annual contractually required contributions to the plan

– Plan would use the same approach to measurement of the collective unfunded liability and expense as for sole and agent employers

– A change in the employer’s net pension liability resulting from a change in its proportionate allocation percentage should be recognized as expense immediately

Reexamination ofStatement No. 14

The Financial Reporting Entity

Project Objectives

To evaluate existing standards defining the financial reporting entity to determine if they effective– Are all appropriate entities being included?– Are any inappropriate entities being included?– Are display and disclosure requirements met?– Is the information decision-useful?– Is accountability supported?

Project History

Research into current practiceOriginally included issues related to fiduciary responsibility and reporting units less than a complete reporting entity– Reporting units dropped– Fiduciary responsibility to be dealt with in

separate project

Tentative Decisions So Far

In addition to meeting the fiscal dependency criterion, a financial benefit/burden relationship should be present for a potential component unit to be included in the primary government’s financial statements based on the fiscal dependency criterion.The “misleading to exclude” notion would be retained, but amendments to the guidance will clarify the professional judgment aspect of the guidance.

Tentative Decisions So Far

Component units will be blended if the component unit’s governing body is substantively the same as the governing body of the primary government and either:– a financial benefit/burden relationship exists with

the primary government or– management of the primary government has

operational responsibility for the component unit.

Tentative Decisions So Far

Debt issuing component units would qualify for blending if primary government resources are used to retire their debt. Blending in single column stand-alone business-type activity reports would be done by combining all information into the primary government column, and combining information would be required in the notes.

Tentative Decisions So Far

Acquisitions of the net assets (for example, stock) of a corporation would be reported as equity interestEffective date would be periods beginning after June 15, 2012