Google = Bank Of The Future;Future Of The Bank = ?

Digital (R)Evolution In The Financial Services Industry

Alexis Eisenhofer, financial.com - Thomson Reuters, 21 January 2015

“Banking Is No Longer Somewhere You Go, But Something You Do.” (Brett King)“Banking Is Essential, Banks Are Not.” (Bill Gates)

The “New World” In 2015

Digital Business Models Aim At A Disintermediation Of The “Man In The Middle”

➢ Producers (brands) and consumers interact directly

➢ "Prosumer": customers influence product design

➢ "Non-physical production" (the core business model of a bank) is ideal for

digital strategies

➢ Innovation in banks has been limited to financial instruments (financial

engineering)

➢ Retail banks in Europe only have 20-40% of their processes digitized (McKinsey,

October 2013)

More And More Customers Expect Changes In Banks

➢ Generations X (1964-1979) and Y (1980-1995) reach the age for wealth creation;

"Millennials" (from 2000) do not want consultation

➢ Millennial Disruption Index: "Banking is at the highest risk of disruption."

(71% would rather go to the dentist than to the bank)

➢ Rising equity markets with no risk-free investment opportunity

➢ "Paradox of choice": Too much supply reduces the total demand

➢ "Disenchantment" of financial advisors by two crises; Bad image of banks

New Technologies Offer Numerous Opportunities

➢ Big data: volume, variety, velocity, veracity

➢ Access: anyone, anything, anytime, anywhere, any device

➢ Social media (Collaboration and sharing)

➢ Technologies disrupt industries faster than ever

(Skype, Uber, WhatsApp, Spotify, YouTube, Google Maps, Digicams etc.)

➢ One million users in 9 years / months / days: AOL / Facebook / Draw Something

➢ $ 3 billion in Venture Capital for Fintechs in 2013 (2008: $ 930 million) is still

small compared to total bank IT costs ($ 485 billion) - but growing fast

Signs Of A Tsunami Are Already Visible

➢ Productivity ratios of retail branches have been deteriorating for a long time

➢ Lower barriers to the provision of financial services

➢ Rising acquisition costs ($ 350 for checking account, $ 2500 for mortgage)

➢ Advertising campaigns are less efficient (declining conversion due to

multichannel sales)

➢ Tsunami: Number of taxis in San Francisco dropped by -65% in a single year

(due to Uber.com)

➢ Accenture expects 30% sales decline in banks by 2020 due to new competitors

(September 2014)

Attacks On Institutional Investment

And Investment Banking

➢ Platform for structured data

➢ All major sources (FRED, ECB, etc.)

➢ Ongoing updates

Quandl.com: 10 Million Free Time Series Of Financial Data (Download, API, Excel & Plotly)

Plot.ly: Free Graphical Data Analysis

➢ Almost as powerful as programming language R

➢ Sharing & Collaboration

➢ Numerous import / export formats

Quantopian.com: Free Algorithmic Trading Community With Live Backtesting / Valuation Of Complex Structures

➢ Source code and risk ratios available

➢ Community of highly specialized professionals

➢ Business model: Seed funding of hedge funds for top users with a revenue share

Rizm.equametrics.com: Drag And Drop Algo Builder & Paper Trading

➢ No programming experience required

➢ Backtesting & Paper Trading

➢ Financing of the platform through introducing broker fees (IB, FXCM)

Estimize.com: Crowdsourced Estimates (4,500+ Analysts)

➢ Wisdom of the crowd (without sell side bias); Better results than Wall Street analysis

➢ Numerous rankings, alerts, calendars

➢ Social Media Features

SeekingAlpha.com: Peer Group Blog For Equity Research With More Than 7,000 Authors

➢ Excellent quality due to intensive discussions

➢ Disclosure of new, non-public facts

➢ Free Transcripts of all earnings calls

No One Could Predict Quotes Better Than Google

➢ 90% of all purchases start with a search (70% thereof Google searches)

➢ Already public search results allow outperformance

➢ Eric Schmidt (Chairman) has implemented a code of conduct for not forecasting the stock market

LimeBrokerage.com - Sub Millisecond Execution & Clearing (880 ns Market Data); 20% Of US Equities Volume

➢ "Discount broker" for algos

➢ Order execution much faster than "normal" brokers

➢ Extensive market data (Level 2)

Attacks On Payment Systems And

Savings Deposits

Paypal Handles A Quarter Of The World's Online Shopping - 148 Million Customers Are Numerically "Germany Plus France"

➢ After 7 years Paypal has more online accounts than all savings banks in Germany

➢ eCommerce doubled in 5 years at 14% market share - with accelerated growth

➢ Possible spin-off of Ebay brings further growth for Paypal

Alipay Is Already The Largest Provider Of Fixed-Term Deposits In China (6.3% Instead Of 3.25% For State Banks)

➢ Payment processors start with deposits

➢ Currently the only bank in China with a positive real interest rate

➢ Alipay has better image than state-owned banks

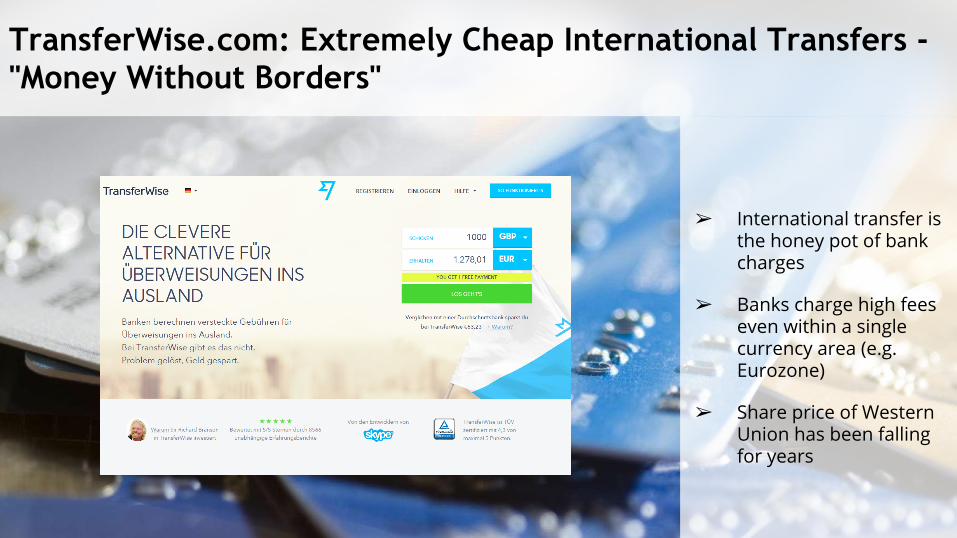

TransferWise.com: Extremely Cheap International Transfers - "Money Without Borders"

➢ International transfer is the honey pot of bank charges

➢ Banks charge high fees even within a single currency area (e.g. Eurozone)

➢ Share price of Western Union has been falling for years

Facebook And MoneyGram: Bank Transfer From The US To Over 200 Countries Via "PicomoPay" App

➢ 25% of all clicks in the USA on Facebook

➢ 73% of Millennials want payment function of Facebook (Millennial Disruption Index)

➢ Not a "chicken and egg" problem (network effect)

Mint.com: Personal Financial Management Service With Multi-Account Aggregation (198 Mln Accounts In US / Canada)

➢ Personal financial planning with savings recommendations by peer group comparisons

➢ Financing through commissions from selling long-term contracts

➢ Founded in 2006, taken over in 2009 by Intuit (170 million USD)

Social Banking "Kaching" Of Australian Commonwealth Bank

➢ Mobile Payment via Facebook / E-Mail / SMS

➢ Complete integration into the timeline of friends

➢ Push Notifications for payments

Attacks On

Lending And Project Finance

Lendingclub.com: Peer-To-Peer Lending ("Social Lending")

➢ Peer-to-peer lending, the world's largest crowd lending platform

➢ Google hold 8% stake, IPO in Q4/2014, market capitalization USD 9.5 bln

➢ Risk management through pre-selection of loan applications (only the top 10%) and diversification

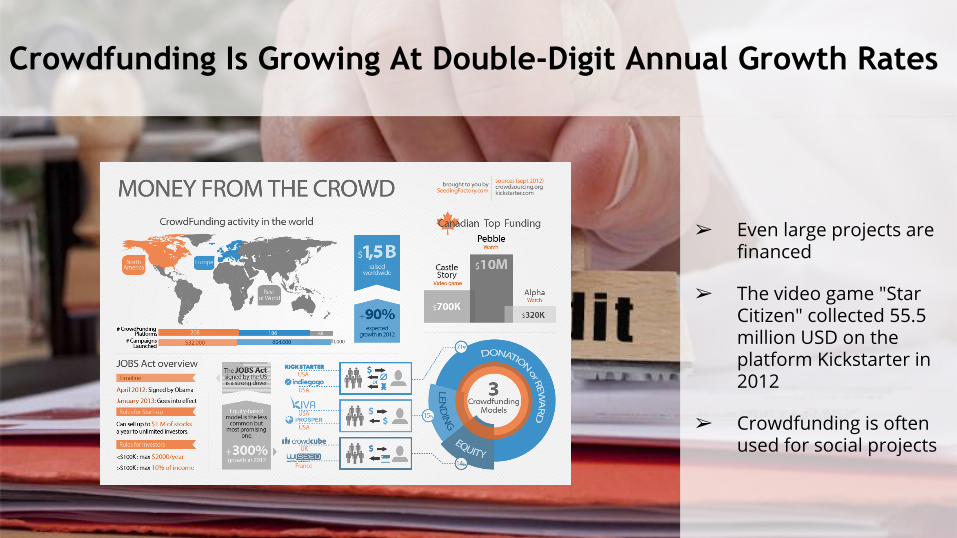

Crowdfunding Is Growing At Double-Digit Annual Growth Rates

➢ Even large projects are financed

➢ The video game "Star Citizen" collected 55.5 million USD on the platform Kickstarter in 2012

➢ Crowdfunding is often used for social projects

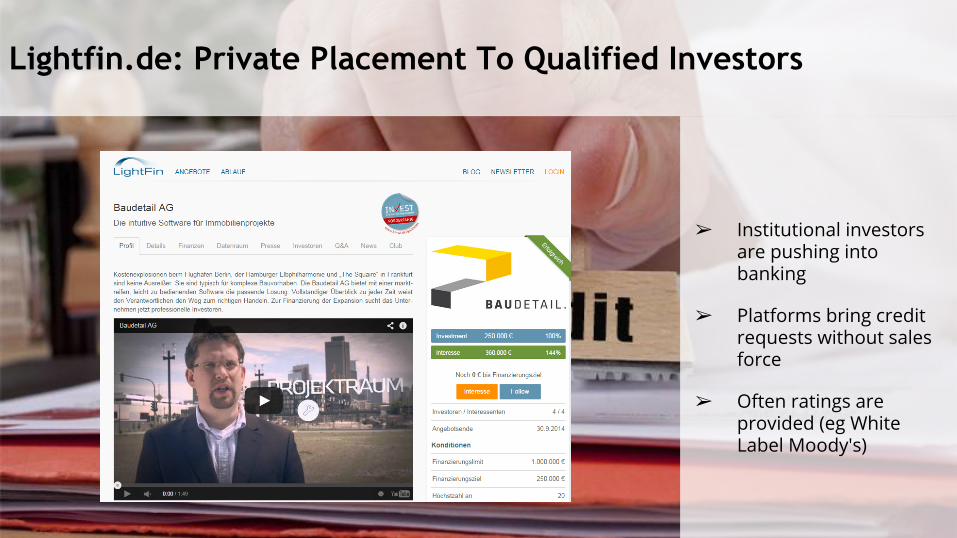

Lightfin.de: Private Placement To Qualified Investors

➢ Institutional investors are pushing into banking

➢ Platforms bring credit requests without sales force

➢ Often ratings are provided (eg White Label Moody's)

Kreditech.com: Big Data For Credit Scoring

➢ Fully automated rating of 15,000 data points

➢ Social graph, browsing behavior and GPS data to explain the bulk of creditworthiness

➢ Forecasting accuracy better than with traditional models

Wonga.com: Short-Term Consumer Loans Up To £ 400 In 5 Minutes

➢ Standardized detection of small consumer loans

➢ Credit statement in less than 5 minutes

➢ Improving efficiency compared to traditional retail banking

Attacks on Asset Management and

Brokerage

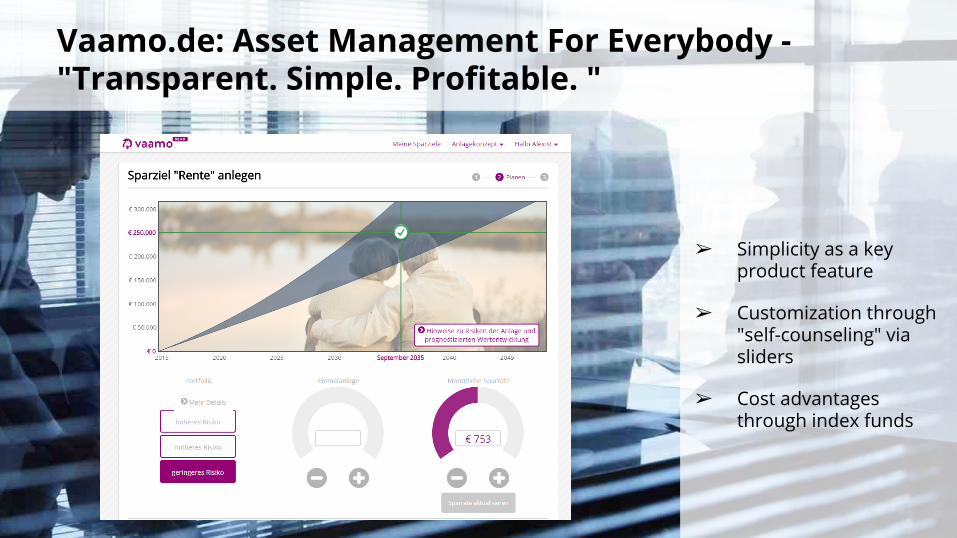

Vaamo.de: Asset Management For Everybody - "Transparent. Simple. Profitable. "

➢ Simplicity as a key product feature

➢ Customization through "self-counseling" via sliders

➢ Cost advantages through index funds

Wealthfront.com: ETF-based, Commission-Free Asset Management (AuM $ 1 Bln In 30 months)

➢ International market leader with 1.8 million visits per month

➢ 3-digit annual growth rates

➢ Far stronger growth than Charles Schwab in their early stage (Direct Brokerage)

Etoro.com: Social Trading - "Friends" Replace Bank Advisors

➢ The world's leading Copy-Trading platform

➢ Nearly 130 million trades since 2007 (with continued strong growth)

➢ Comdirect (German market leader): 5 million trades / quarter

➢ Leading Community for Active Traders for Charting Analysis

➢ Sharing of chart patterns via HTML5 Tool

➢ Subscription Fee for Real Time Data

Tradingview.com: Community Of "Active Traders" For Technical Analysis

Strategies For Defense

Open Architectures, Collaborations And An Innovative Organizational Structure

➢ Open architecture: flexibility and network effects

("If you can’t beat them, join them.")

➢ Software-as-a-Service: Continuous improvements through clickstream analysis

➢ Cooperation: V.me by Visa provides white label online payment processing

➢ Outsourcing of software development to small flexible partners (no

cannibalization, new thinking, no legacy systems)

➢ Takeover of Fintechs (Problem: Valuations up to several billion USD)

➢ Promotion of Digital Natives to the Board of Directors (only 9 out of 206 DAX

supervisory board members with obvious IT background, Handelsblatt 2014)

Social Graph, Peer Group Data, And (Location-Based) Contextualization

➢ Consistent use of the social graph (Facebook, XING, LinkedIn)

➢ Similarity analysis, eg “Customers who have a similar profile bought these

securities."

➢ Value-added services: Cost savings by changing providers (Peer group

information)

➢ Framing concepts ("40-year-old father" etc.)

➢ Right time and right context (Location-based data)

Design, Integration And Differentiation

➢ Design is a key success factor of applications / products (eg iPhone, Nespresso)

➢ "Mobile First": "Less is more" when designing surfaces

➢ Gamification: Use of game mechanics in non-game contexts to engage users

➢ Financial products are seen as commodities by retail customers; distinction to

the competition is key

➢ Paid content can not be accessed through an aggregator like Google

➢ Higher "customer ownership costs": Free content offerings require investments

in added value

➢ Significantly lower distribution costs of paid content

Paid Content And Customer Ownership Costs

Thank You For Your Attention!

“You must unlearn what you have learned...” (Yoda)

de.linkedin.com/in/eisenhofer

xing.com/profile/Alexis_Eisenhofer

twitter.com/eisenhofer

plus.google.com/u/0/+AlexisEisenhofer

slideshare.net/Eisenhofer

youtube.com/user/aeisenhofer