HOUSING SUMMIT 2013HOUSING SUMMIT 2013Thursday 17 October 2013Thursday 17 October 2013

The Mortgage and Housing MarketsThe Mortgage and Housing Markets

Adrian Coles

Director-General

The Building Societies Association

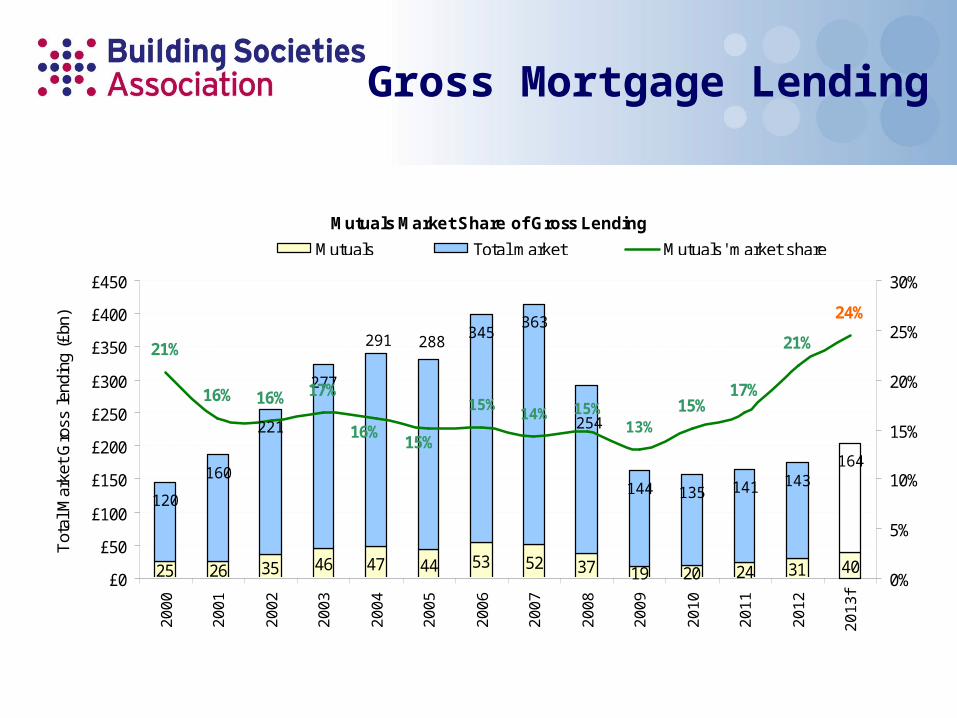

Gross Mortgage Lending

Mutuals Market Share of Gross Lending

25 26 35 46 47 44 53 52 37 19 20 24 31 40

135 141 143164

363

254

120

160

221

277

291 288345

144

15%17%

21%

24%

15%13%

14%

15%

17%16%16%

21%

15%

16%

£0

£50

£100

£150

£200

£250

£300

£350

£400

£450

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

f

Tot

al M

arke

t G

ross

lend

ing

(£bn

)

0%

5%

10%

15%

20%

25%

30%

Mutuals Total market Mutuals' market share

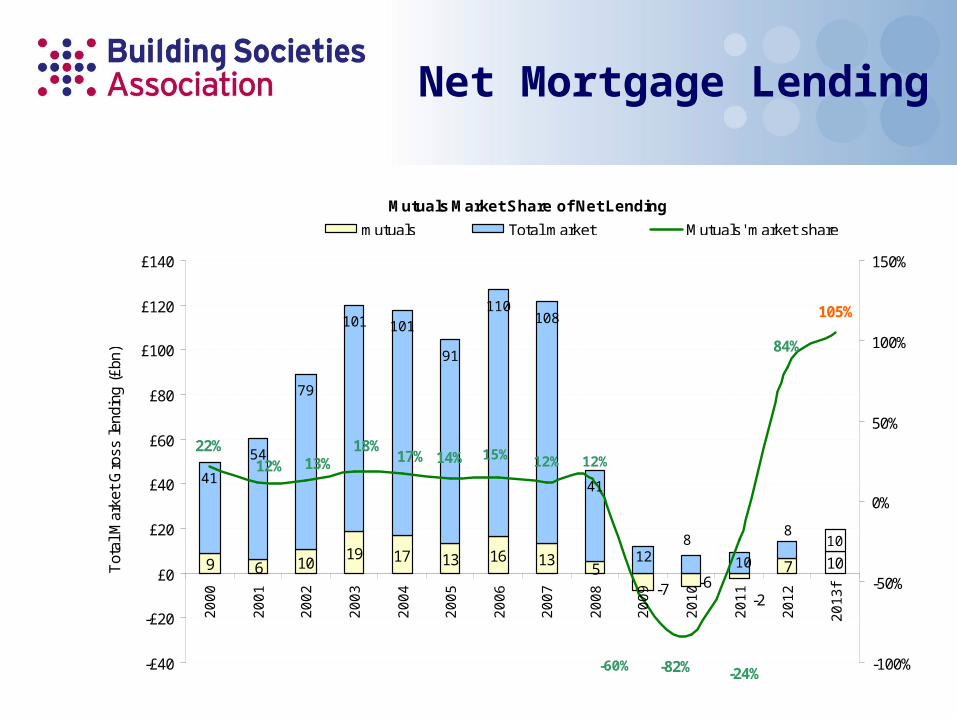

Net Mortgage Lending

Mutuals Market Share of Net Lending

9 6 1019 17 13 16 13

5 7 10

-2-6-7

108

108

4141

54

79

101 101

91

110

12 10

8

84%

105%

12%

-60%

12%14%18%

13%12%22%

15%17%

-82% -24%-£40

-£20

£0

£20

£40

£60

£80

£100

£120

£140

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

f

Tot

al M

arke

t G

ross

lend

ing

(£bn

)

-100%

-50%

0%

50%

100%

150%

mutuals Total market Mutuals' market share

Net lending by institutions participating in the Funding for Lending Scheme (£bn) July 2012 - June 2013

£11.3

-£13.6

-£15.0

-£10.0

-£5.0

£0.0

£5.0

£10.0

£15.0

Mutuals Other Lenders

Funding for Lending Scheme

90%+ LTV loans by mutuals Jan-Aug in each year

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

2006 2007 2008 2009 2010 2011 2012 2013

0%

2%

4%

6%

8%

10%

12%

14%

16%Number of loans

Proportion of all loans

BSA

High LTV Lending by Mutuals

Help to Buy: Mortgage Guarantees – Issues for

Lenders

• Cost• Complexity• Certainty (of continuation of scheme)• Existing market relationships• Business model• Capital relief – PRA – sound underwriting – safety of

institutions• Consumer understanding of costs and benefits – FCA –

safety of consumers• Other regulatory priorities – eg MMR, ring-fencing

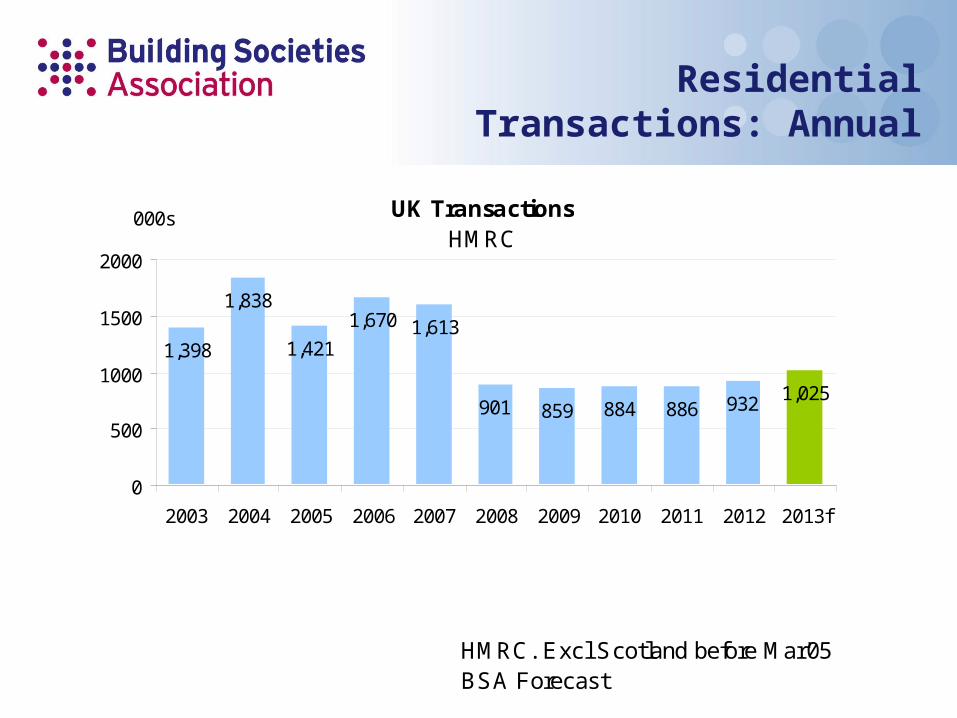

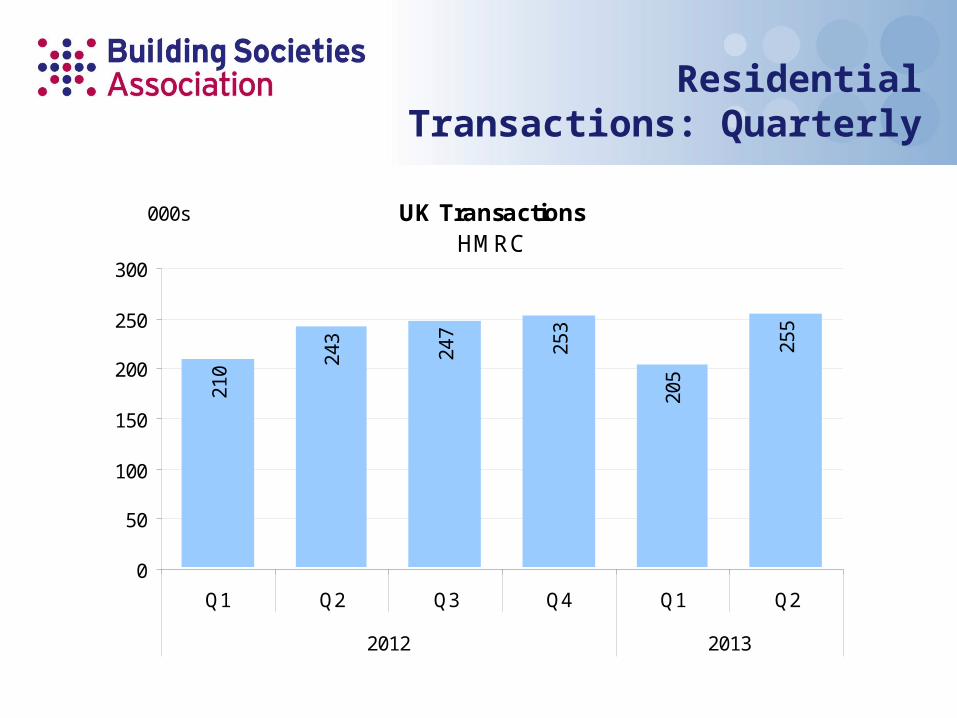

UK TransactionsHMRC

1,398

1,838

1,421

1,670 1,613

901 859 884 886 932 1,025

0

500

1000

1500

2000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013f

000s

HMRC. Excl Scotland before Mar'05BSA Forecast

Residential Transactions: Annual

UK TransactionsHMRC

210 24

3

247

253

205

255

0

50

100

150

200

250

300

Q1 Q2 Q3 Q4 Q1 Q2

2012 2013

000s

Residential Transactions: Quarterly

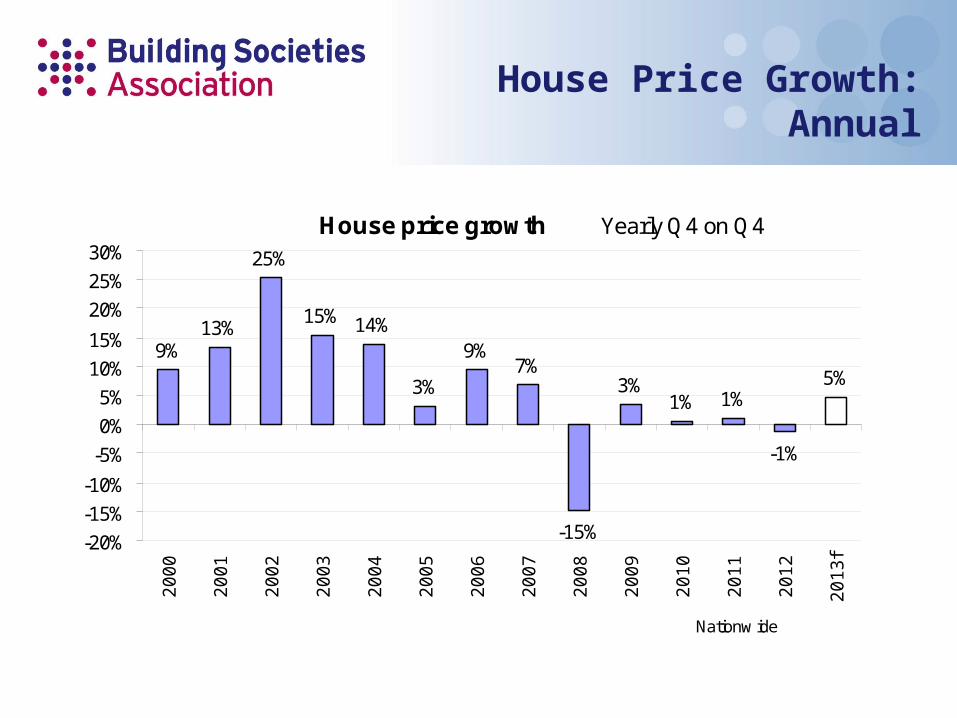

House Price Growth: Annual

House price growth Yearly Q4 on Q4

9%13%

25%

15% 14%

3%

9%7%

-15%

3%1% 1%

-1%

5%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

f

Nationw ide

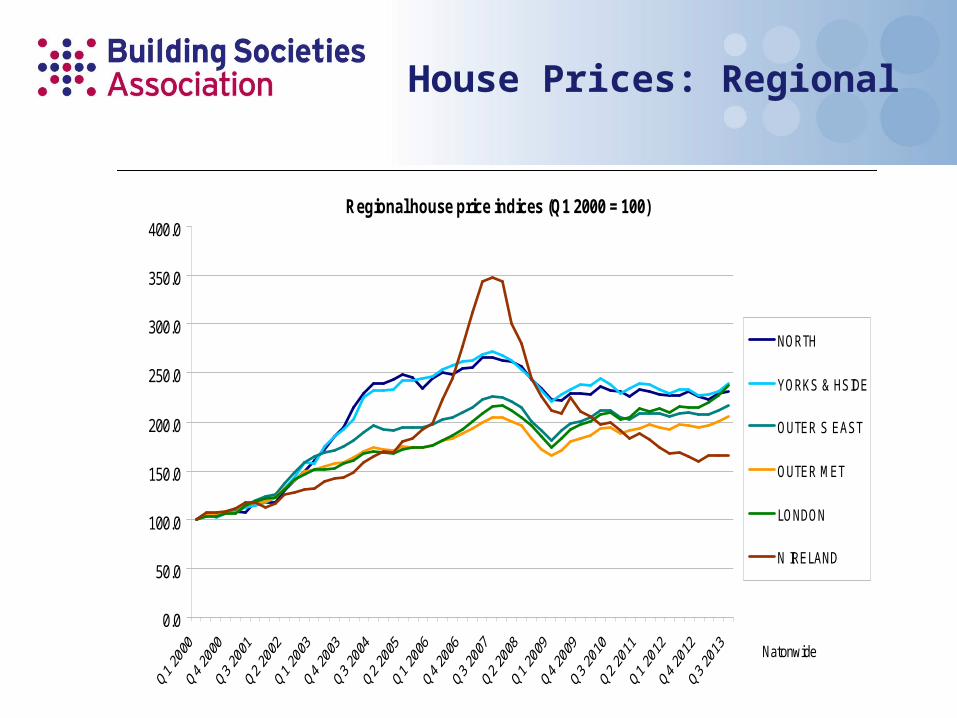

Regional house price indices (Q1 2000 = 100)

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

NORTH

YORKS & HSIDE

OUTER S EAST

OUTER MET

LONDON

N IRELAND

Natonwide

House Prices: Regional

House price growth Quarterly yoy %

0.2%

-1.1%-1.6%

-1.1%

0.2%

1.4%

4.3%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

20

12

Q1

20

12

Q2

20

12

Q3

20

12

Q4

20

13

Q1

20

13

Q2

20

13

Q3

Nationw ide

House Price Growth: Quarterly

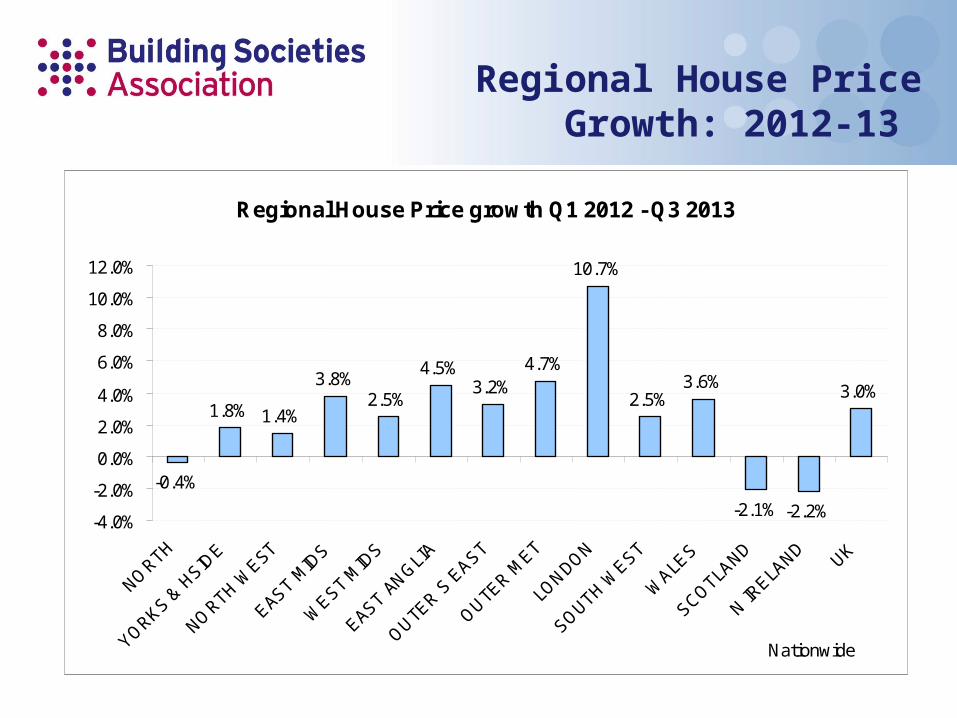

Regional House Price growth Q1 2012 - Q3 2013

-0.4%

1.8% 1.4%

3.8%2.5%

4.5%3.2%

4.7%

10.7%

2.5%3.6%

-2.1% -2.2%

3.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

NORTH

YORKS & H

SIDE

NORTH W

EST

EAST MID

S

WEST M

IDS

EAST ANGLI

A

OUTER S

EAST

OUTER M

ET

LONDON

SOUTH WEST

WALE

S

SCOTLAND

N IRELA

NDUK

Nationwide

Regional House Price Growth: 2012-13

Real House Prices

£40,000£60,000£80,000

£100,000£120,000£140,000£160,000£180,000£200,000£220,000£240,000

2000

Q1

2002

Q1

2004

Q1

2006

Q1

2008

Q1

2010

Q1

2012

Q1

Trend Real House Price

Nationwide Building Society

Real House Prices

House Price to Earnings Ratio

5.66

4.48

3.00

3.50

4.00

4.50

5.00

5.50

6.00

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

House Price to Earnings Ratio

Long run average Apr 1983 - Aug 2013

Halifax / Lloyds Banking Group

House Price to Earnings Ratio

Mortgage payments as % of Income

16.8

21.1

23.5

18.3

10.0

12.0

14.0

16.0

18.0

20.0

22.0

24.0

26.0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

%

All buyers First-time buyers

ONS

Mortgage Payments as % of Income

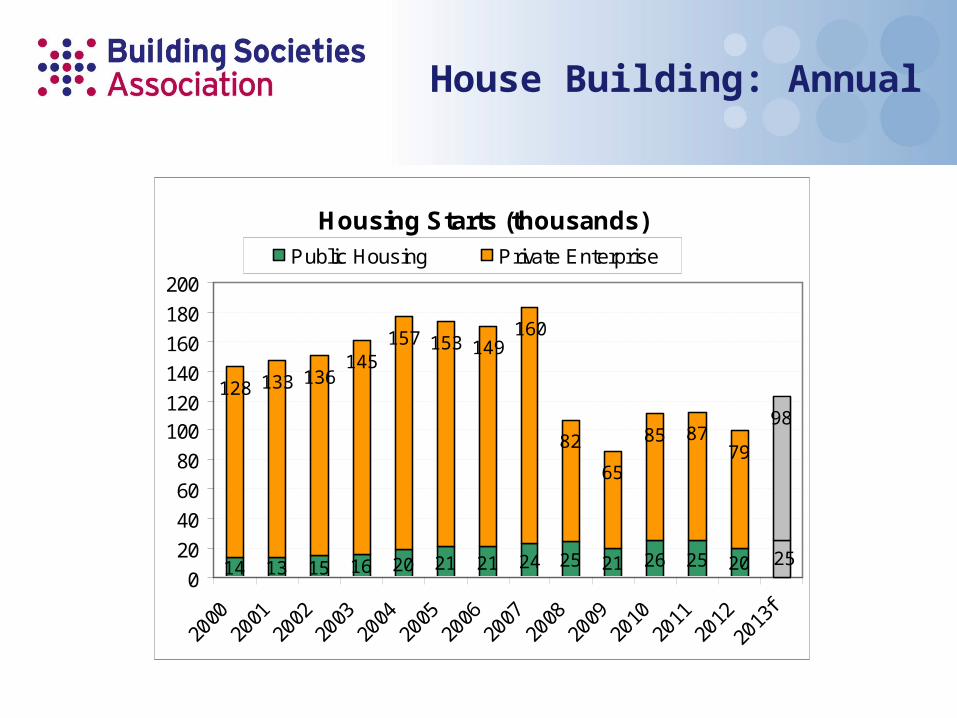

Housing Starts (thousands)

14 13 15 16 20 21 21 24 25 21 25 20

128 133 136145

157 153 149160

82

65

85 8779

98

25260

20

40

60

80

100120

140

160

180

200

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

f

Public Housing Private Enterprise

House Building: Annual

Housing Starts (thousands)

5 5 6 5 5 6

20 2022

1722

27

0

5

10

15

20

25

30

35

2012 Q1 Q2 Q3 Q4 2013 Q1 Q2

Public Housing Private Enterprise

House Building: Quarterly

The FPC View – 18 September 2013

"... the recovery in the housing market appeared to have

gained momentum and to be broadening. Mortgage approvals

in July were 30% higher than a year earlier and average

house prices in August were 5% higher than a year earlier and

had risen more in some parts of the country, particularly

London. Nevertheless, activity in the housing market and loan-

to-value ratios on new mortgage lending remained below their

historic averages. Households’ debt servicing costs were low

and the ratio of house prices to earnings was at its level of a

decade ago. In view of that, the Committee judged that it

should closely monitor developments in the housing market

and banks' underwriting standards….

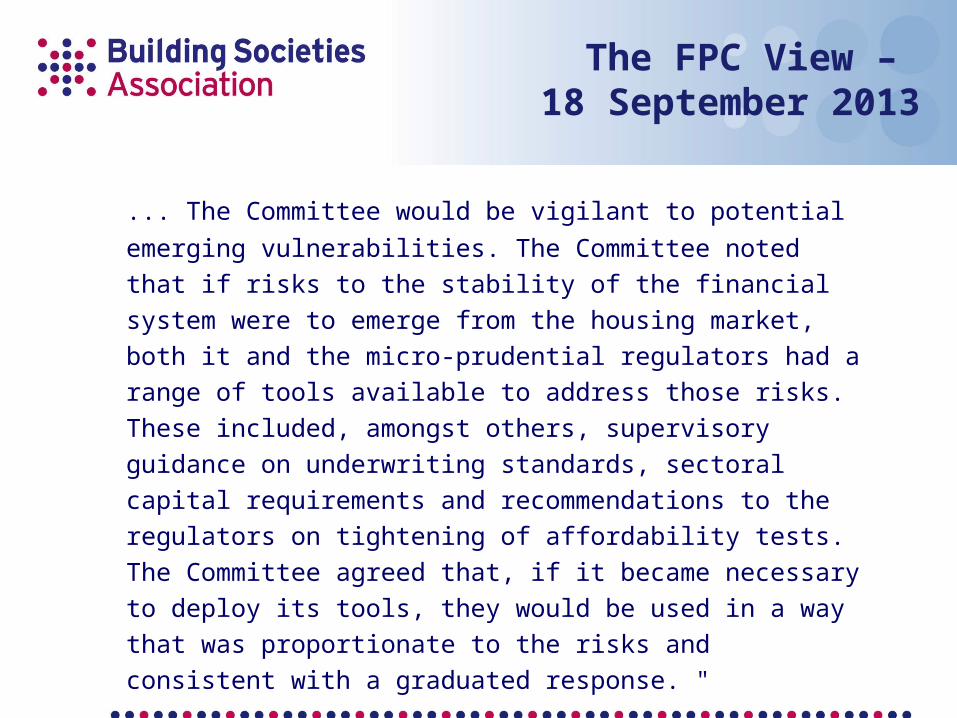

The FPC View – 18 September 2013

... The Committee would be vigilant to potential emerging

vulnerabilities. The Committee noted that if risks to the stability

of the financial system were to emerge from the housing

market, both it and the micro-prudential regulators had a

range of tools available to address those risks. These

included, amongst others, supervisory guidance on

underwriting standards, sectoral capital requirements and

recommendations to the regulators on tightening of

affordability tests. The Committee agreed that, if it became

necessary to deploy its tools, they would be used in a way that

was proportionate to the risks and consistent with a graduated

response. "

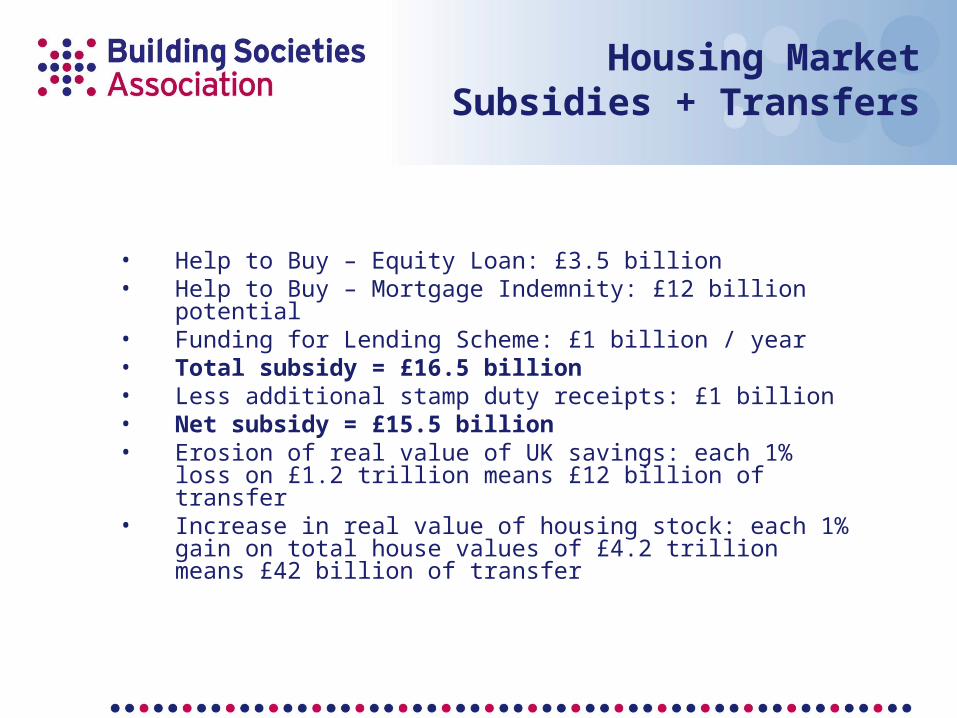

Housing Market Subsidies + Transfers

• Help to Buy – Equity Loan: £3.5 billion• Help to Buy – Mortgage Indemnity: £12 billion potential• Funding for Lending Scheme: £1 billion / year• Total subsidy = £16.5 billion• Less additional stamp duty receipts: £1 billion• Net subsidy = £15.5 billion• Erosion of real value of UK savings: each 1% loss on

£1.2 trillion means £12 billion of transfer• Increase in real value of housing stock: each 1% gain on

total house values of £4.2 trillion means £42 billion of transfer

Housing market subsidies from….to….

• Savers to borrowers (old to young) – low interest rates.

• Home buyers to home sellers (young to old) – rising house prices

• To house builders – higher prices and activity• To lenders – wider margins and more loans• To transactional agents• Borrowers to tax-payer – or the reverse?• Overall beneficiaries are?

HOUSING SUMMIT 2013HOUSING SUMMIT 2013Thursday 17 October 2013Thursday 17 October 2013

The Mortgage and Housing MarketsThe Mortgage and Housing Markets

Adrian Coles

Director-General

The Building Societies Association