June 2014, IDC Energy Insights #EI249425

IDC MarketScape

IDC MarketScape: Worldwide Oil and Gas Professional Services 2014 Vendor Assessment

Jill Feblowitz

IDC MARKETSCAPE FIGURE

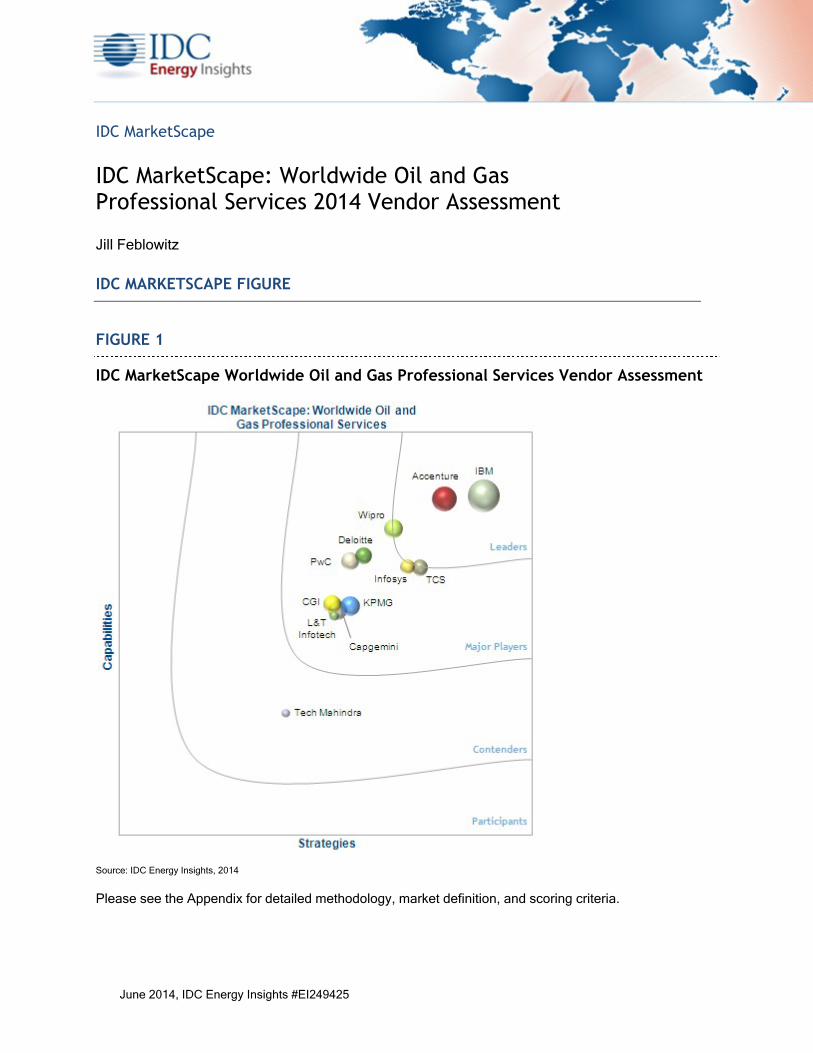

FIGURE 1

IDC MarketScape Worldwide Oil and Gas Professional Services Vendor Assessment

Source: IDC Energy Insights, 2014

Please see the Appendix for detailed methodology, market definition, and scoring criteria.

©2014 IDC Energy Insights #EI249425 1

IDC OPINION

A new cost consciousness has oil and gas (O&G) companies looking to professional services firms to

help them reduce costs. This does not mean, however, oil and gas companies are willing to sacrifice

quality or abandon innovation. Majors and supermajors have set the bar high for their service providers

to have oil and gas subject matter expertise. National oil companies look to their providers to help

them follow the best practices in the industry and tap local talent. Oilfield services companies ask their

service providers to develop new products built on 3rd Platform technologies. These are tall orders for

an industry that experiences a gap between entry-level and seasoned experts that will not be easy to

close. This IDC MarketScape is intended to provide oil and gas companies with insight into the current

capabilities and future strategies of professional service firms and guidance on how to approach

building a stable of trusted service providers. In detail:

The demand and market for professional service firms in oil and gas continues to grow at a healthy pace.

Leaders in professional services in oil and gas have a commitment to the oil and gas industry

that is backed at the executive level of their companies. This is demonstrated through investment in research and development, oil and gas centers of excellence in major oil and gas hubs, and oil and gas subject matter experts. Leaders are viewed as trusted advisors that

work with their clients and other service providers in the oil and gas ecosystem to drive innovation.

A substantial stable of major players have had impressive growth over the past two years. Of note are firms that were once considered commodity IT players that are now moving into more

business-critical areas such as petro-technical application and data management.

IDC MARKETSCAPE VENDOR INCLUSION CRITERIA

IDC collected and analyzed data on 12 professional service firms. While the market arena for

professional services is very broad and there are many suppliers that offer these services, IDC

narrowed down the field of players that participate based on the following criteria:

Service capability. Each service provider must have an established reputation working in the

oil and gas industry, with revenue from at least two of the following services that are geared specifically to oil and gas: business consulting, IT consulting, systems integration, IT

outsourcing, and business process outsourcing.

Solutions for oil and gas. Firms must establish that they have a variety of "solutions" that are

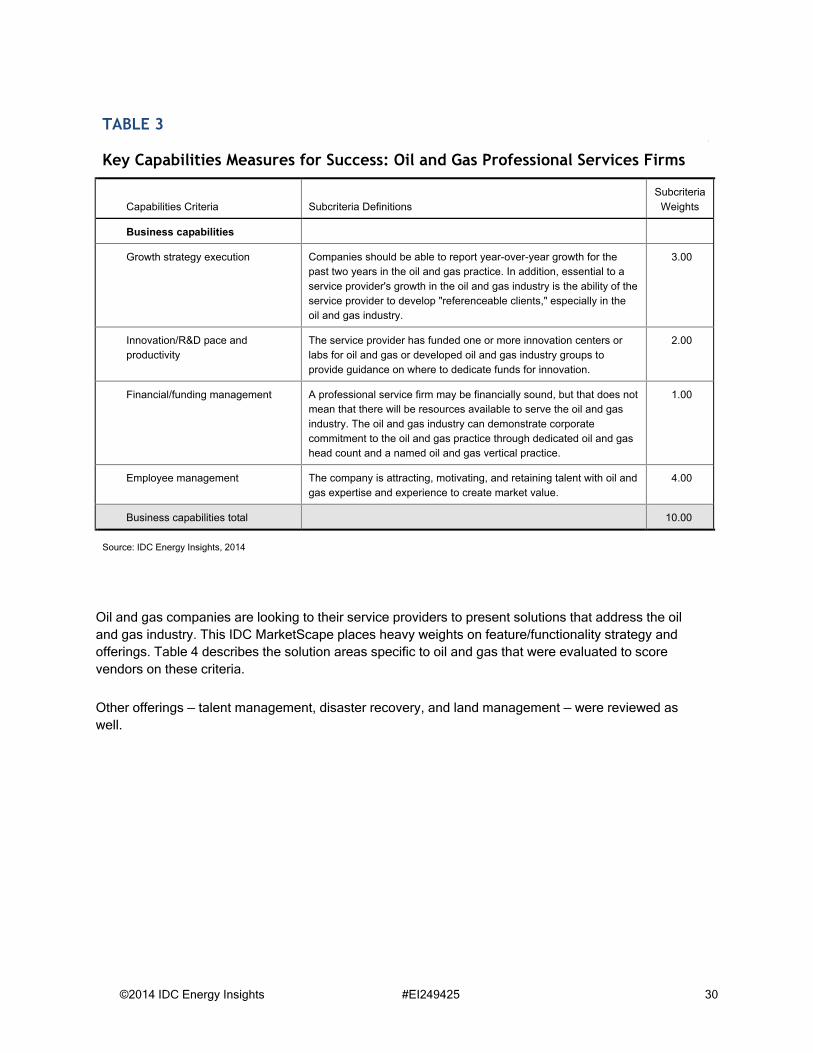

unique and specific in the oil and gas industry. Firms that have only one solution are not considered (refer to Table 4 for a list of solutions considered in this report).

Geographic presence. Firms must have presence delivering services to O&G companies in

multiple regions (Asia/Pacific, Western Europe, Central and Eastern Europe, North America, Latin America, and Middle East and Africa).

©2014 IDC Energy Insights #EI249425 2

ESSENTIAL BUYER GUIDANCE

This IDC MarketScape is a starting point to guide oil and gas companies in their selection of service

providers. For most oil and gas companies, the selection will be primarily based on what these firms

can do to improve performance, achieve IT-enabled business benefits, and reduce costs. For this

industry that means speeding time to first oil, mitigating drilling risk, optimizing production, adapting to

new delivery channels, hedging risks, leveraging opportunities in the commodities market, preventing

accidents, streamlining refining, and serving the retail customer. For oilfield services companies, there

is an added dimension — co-innovating to deliver IT-enabled services to the owners/operators that are

their customers.

Oil and gas companies should pay particular attention to the following decision factors:

Determine which attributes are most important in project-related initiatives and in ongoing

services. Depending on the assignment, the level of importance will vary for the need for oil and gas expertise and experience, knowledge of local regulations, value/cost, geographic coverage, bench for handling niche oil and gas applications, and petro-technical data.

Attributes that are consistently important are security and protection of information and excellence in meeting service-level agreements and timelines.

Technical complexity in the O&G sector has increased and will continue to do so in the next few years with the further digitization of the industry and new techniques for the pursuit of

unconventional resources. Look for demonstrated experience in deploying Big Data and analytics to support business objectives.

Leading oil and gas companies are pushing their professional services firms to help them innovate. Set clear expectations on the type of innovation you expect. Evaluate vendor

performance on how well the vendor is able to work with you or other service providers to delivering innovation.

Look for vendors that are able to deliver repeatable solutions to your company but still accommodate your unique requirements. A vendor that can demonstrate experience with only

one customer may not be able to translate that to your company easily. Ask to understand what commitment the service provider has made to investing in templating the solutions.

Ask vendors to show you how they have helped their customers reduce the cost of IT. Cloud-based services are one way to achieve cost reduction and reduce capital investment. In

addition, vendors should be able to help automate processes or provide templates to speed implementation.

VENDOR SUMMARY PROFILES

This section briefly explains IDC's key observations resulting in a vendor's position in the IDC

MarketScape. Vendors included in this IDC MarketScape are:

Accenture

Capgemini

CGI

©2014 IDC Energy Insights #EI249425 3

Deloitte

IBM

Infosys

KPMG

L&T Infotech

PwC

TCS

Tech Mahindra

Wipro

While every vendor is evaluated against each of the criteria outlined in the Appendix, the description

here provides a summary of each vendor's strengths and opportunities. Table 1 provides a snapshot of

the vendors reviewed including main geographies, key customers, key solution and services for oil and

gas, primary sources of oil and gas revenue, and what IDC Energy Insights believes to be particularly

noteworthy.

©2014 IDC Energy Insights #EI249425 4

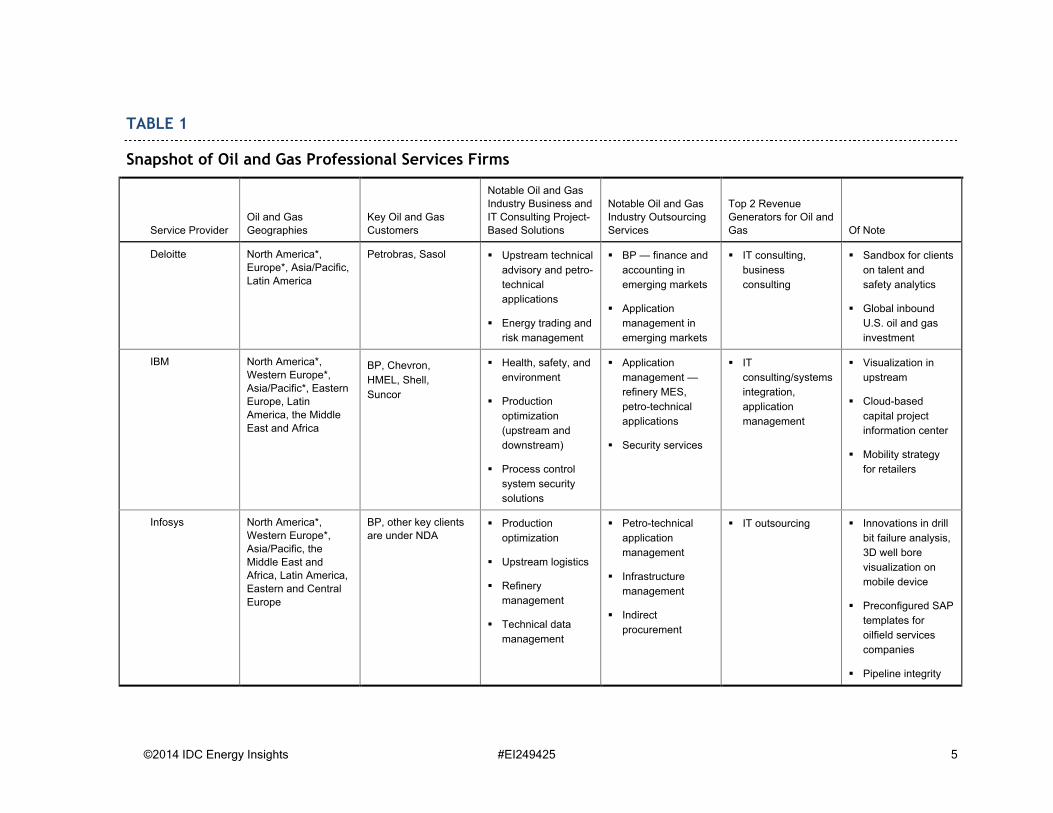

TABLE 1

Snapshot of Oil and Gas Professional Services Firms

Service ProviderOil and Gas

Geographies

Key Oil and Gas

Customers

Notable Oil and Gas Industry Business and

IT Consulting Project-

Based Solutions

Notable Oil and Gas Industry Outsourcing

Services

Top 2 Revenue Generators for Oil and

Gas Of Note

Accenture Western Europe*, North America*,

Eastern and Central

Europe, Asia/Pacific, Latin America, the

Middle East and

Africa

Apache Energy, Baker Hughes, BP,

Chevron, China

National Offshore Oil Corp, ENI, Hess,

Petrobras, Royal

Dutch Shell, Schlumberger,

Sinopec and Statoil,

Total

Capital project

management

Logistics and

supply chain

Production

optimization

(upstream and

downstream)

Forecourt (retail)

Cloud-enabled

versions of most

solutions

BP including

production revenue

accounting and

capital project

management

Systems

integration,

business

consulting

Logical operational

model for initiative

evaluation

Global "Energy

Hub"

Capgemini Western Europe*, North America*, Eastern and Central

Europe, Asia/Pacific,

Latin America

Statoil, Total, Marine Well Containment, Schlumberger,

SubSea7, GDFSUEZ,

Centrica

Templated

implementation of

SAP for oil and gas

reducing costs

PM as an advisory

service

IT outsourcing,

systems

integration

Substantial

number of oil and

gas subject matter

experts

CGI North America*, Western Europe*,

Asia/Pacific*, theMiddle East and

Africa, Latin America

Range Resources, Shell International

E&P, Statoil, TOTAL, BP, Exxon, Chevron,

Neste Oil, Devon

Canada, Encana,

Cenovus

Energy trading and

risk management

Fuel retail

payments and

loyalty

Well and asset

integrity

Refinery

operations

Halliburton-

Landmark and

Schlumberger

application

management

Fuel card and

production and

revenue

accounting BPO

Upstream

application

management,

business process

outsourcing

Human resources

with oil and gas

expertise in region

Cloud platform for

compliance and

data sharing —

North Sea

©2014 IDC Energy Insights #EI249425 5

TABLE 1

Snapshot of Oil and Gas Professional Services Firms

Service Provider

Oil and Gas

Geographies

Key Oil and Gas

Customers

Notable Oil and Gas Industry Business and

IT Consulting Project-

Based Solutions

Notable Oil and Gas Industry Outsourcing

Services

Top 2 Revenue Generators for Oil and

Gas Of Note

Deloitte North America*, Europe*, Asia/Pacific,

Latin America

Petrobras, Sasol Upstream technical

advisory and petro-

technical

applications

Energy trading and

risk management

BP — finance and

accounting in

emerging markets

Application

management in

emerging markets

IT consulting,

business

consulting

Sandbox for clients

on talent and

safety analytics

Global inbound

U.S. oil and gas

investment

IBM North America*, Western Europe*,

Asia/Pacific*, Eastern Europe, Latin

America, the Middle

East and Africa

BP, Chevron,

HMEL, Shell,

Suncor

Health, safety, and

environment

Production

optimization

(upstream and

downstream)

Process control

system security

solutions

Application

management —

refinery MES,

petro-technical

applications

Security services

IT

consulting/systems

integration,

application

management

Visualization in

upstream

Cloud-based

capital project

information center

Mobility strategy

for retailers

Infosys North America*, Western Europe*,

Asia/Pacific, the

Middle East andAfrica, Latin America,

Eastern and Central

Europe

BP, other key clients

are under NDA Production

optimization

Upstream logistics

Refinery

management

Technical data

management

Petro-technical

application

management

Infrastructure

management

Indirect

procurement

IT outsourcing Innovations in drill

bit failure analysis,

3D well bore

visualization on

mobile device

Preconfigured SAP

templates for

oilfield services

companies

Pipeline integrity

©2014 IDC Energy Insights #EI249425 6

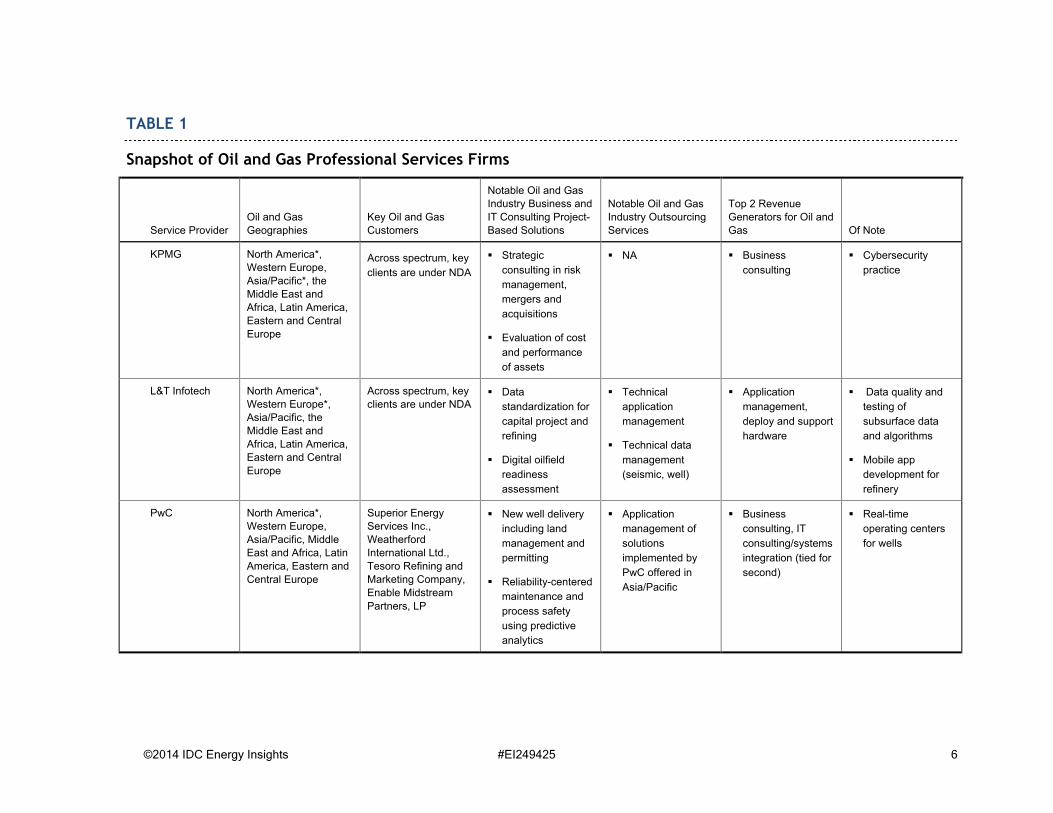

TABLE 1

Snapshot of Oil and Gas Professional Services Firms

Service Provider

Oil and Gas

Geographies

Key Oil and Gas

Customers

Notable Oil and Gas Industry Business and

IT Consulting Project-

Based Solutions

Notable Oil and Gas Industry Outsourcing

Services

Top 2 Revenue Generators for Oil and

Gas Of Note

KPMG North America*, Western Europe,

Asia/Pacific*, the Middle East and

Africa, Latin America,

Eastern and Central

Europe

Across spectrum, key

clients are under NDA

Strategic

consulting in risk

management,

mergers and

acquisitions

Evaluation of cost

and performance

of assets

NA Business

consulting

Cybersecurity

practice

L&T Infotech North America*, Western Europe*, Asia/Pacific, the

Middle East and

Africa, Latin America, Eastern and Central

Europe

Across spectrum, key

clients are under NDA Data

standardization for

capital project and

refining

Digital oilfield

readiness

assessment

Technical

application

management

Technical data

management

(seismic, well)

Application

management,

deploy and support

hardware

Data quality and

testing of

subsurface data

and algorithms

Mobile app

development for

refinery

PwC North America*, Western Europe, Asia/Pacific, Middle

East and Africa, Latin

America, Eastern and

Central Europe

Superior Energy Services Inc., Weatherford

International Ltd.,

Tesoro Refining and Marketing Company,

Enable Midstream

Partners, LP

New well delivery

including land

management and

permitting

Reliability-centered

maintenance and

process safety

using predictive

analytics

Application

management of

solutions

implemented by

PwC offered in

Asia/Pacific

Business

consulting, IT

consulting/systems

integration (tied for

second)

Real-time

operating centers

for wells

©2014 IDC Energy Insights #EI249425 7

TABLE 1

Snapshot of Oil and Gas Professional Services Firms

Service Provider

Oil and Gas

Geographies

Key Oil and Gas

Customers

Notable Oil and Gas Industry Business and

IT Consulting Project-

Based Solutions

Notable Oil and Gas Industry Outsourcing

Services

Top 2 Revenue Generators for Oil and

Gas Of Note

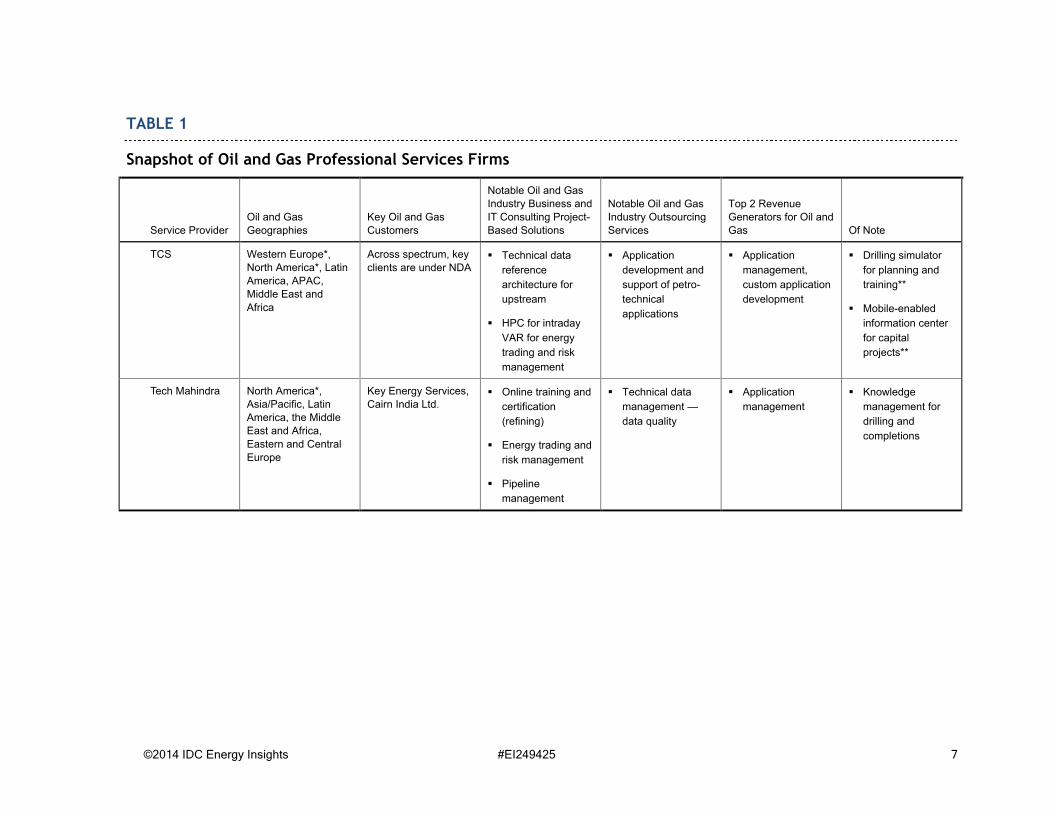

TCS Western Europe*, North America*, Latin

America, APAC, Middle East and

Africa

Across spectrum, key

clients are under NDA Technical data

reference

architecture for

upstream

HPC for intraday

VAR for energy

trading and risk

management

Application

development and

support of petro-

technical

applications

Application

management,

custom application

development

Drilling simulator

for planning and

training**

Mobile-enabled

information center

for capital

projects**

Tech Mahindra North America*, Asia/Pacific, Latin America, the Middle

East and Africa,

Eastern and Central

Europe

Key Energy Services,

Cairn India Ltd. Online training and

certification

(refining)

Energy trading and

risk management

Pipeline

management

Technical data

management —

data quality

Application

management

Knowledge

management for

drilling and

completions

©2014 IDC Energy Insights #EI249425 8

TABLE 1

Snapshot of Oil and Gas Professional Services Firms

Service Provider

Oil and Gas

Geographies

Key Oil and Gas

Customers

Notable Oil and Gas Industry Business and

IT Consulting Project-

Based Solutions

Notable Oil and Gas Industry Outsourcing

Services

Top 2 Revenue Generators for Oil and

Gas Of Note

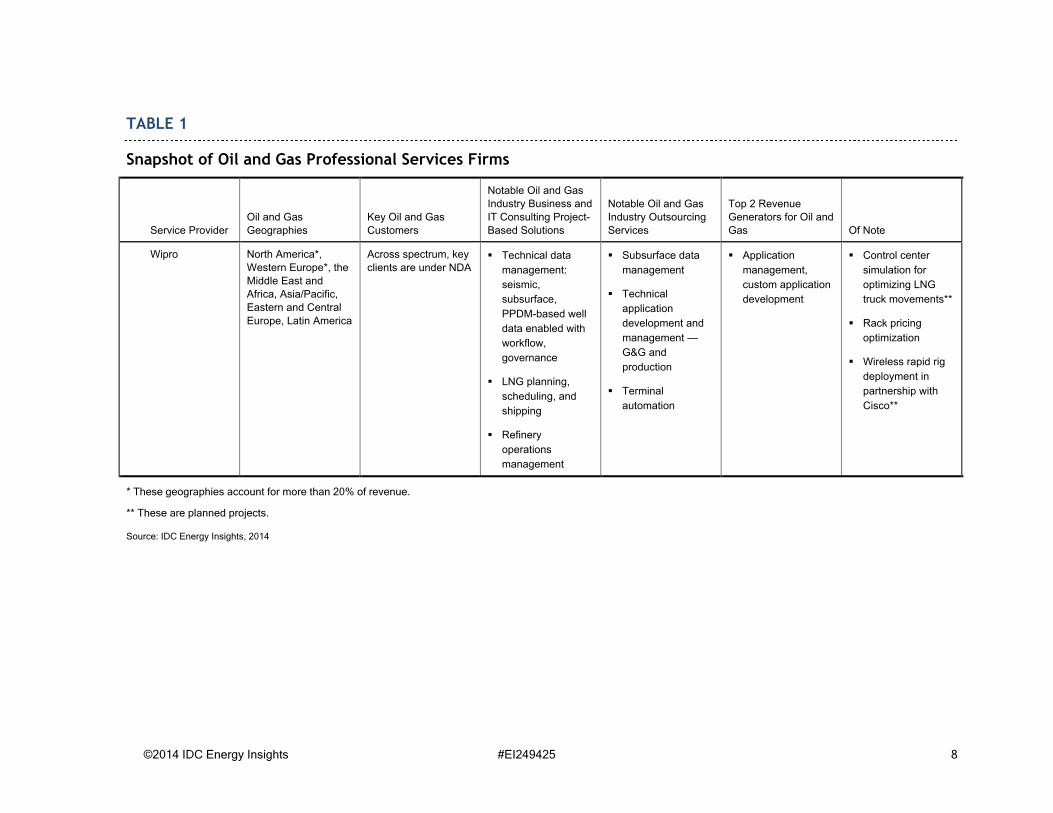

Wipro North America*, Western Europe*, the

Middle East and Africa, Asia/Pacific,

Eastern and Central

Europe, Latin America

Across spectrum, key

clients are under NDA Technical data

management:

seismic,

subsurface,

PPDM-based well

data enabled with

workflow,

governance

LNG planning,

scheduling, and

shipping

Refinery

operations

management

Subsurface data

management

Technical

application

development and

management —

G&G and

production

Terminal

automation

Application

management,

custom application

development

Control center

simulation for

optimizing LNG

truck movements**

Rack pricing

optimization

Wireless rapid rig

deployment in

partnership with

Cisco**

* These geographies account for more than 20% of revenue.

** These are planned projects.

Source: IDC Energy Insights, 2014

©2014 IDC Energy Insights #EI249425 9

Accenture — High Performance Delivered

Accenture has a growing business in oil and gas covering upstream, downstream, pipelines, and

unconventionals. Since the last IDC MarketScape, solutions have continued to improve with the

addition of 3rd Platform technologies and other capabilities. Oil and gas industry revenue is second

among the service firms evaluated in this IDC MarketScape and in the top 3 in client engagement.

Accenture is rated as a Leader in this IDC MarketScape.

Accenture's focus for oil and gas follows closely with the company's reorganization to capture market

share:

Develop business strategies in response to critical business issues (choke points)

Develop digital solutions and services to appropriate business processes

Optimize operations across all segments

Leverage functional services including procurement, ERP, IT transformation, and finance

Run global operations through multiclient delivery centers, enabling them to increase

operational efficiencies and exploit cross-industry synergies

Deploy industry capability globally

Strengths

Accenture continues to be a leader in developing solutions for the oil and gas industry that are well

conceived and start from a business standpoint. The company has robust industry solutions — many

are cloud enabled — and plans for the future in each of the categories chosen for evaluation in this IDC

MarketScape. Through a combination of investments and partnerships, the latest in technology are

brought to bear in these solutions. An example illustrates this assessment. Accenture, in partnership

with GE, has developed a cloud-based analytics and visualization solution for viewing pipeline

segments, status, and conditions with a Google-like menu of views using industry-recognized filters

(MAOP, SMYS, pipe grade, coating type, and piggable/unpiggable). There are also tools for dynamic

risk analysis and volumetric system balance. Another example is Accenture's joint solution with SAP

for production optimization and production revenue accounting.

Large oil and gas companies consider Accenture a trusted advisor and hire the company for its

industry expertise and professionalism. Accenture is a preferred vendor for most large oil and gas

companies. The company's ability to bring together strategy, digital, information technology, and

business process outsourcing is unique in the marketplace. For example, strategic advice to oil and

gas leadership has led to new operating models on one end of the spectrum. On the other end of the

spectrum is the ability to handle business processes, such as finance and procurement, for global oil

and gas clients. Tools, methodologies, and templates make for a consistent approach to development

and delivery across the globe. A system of sharing knowledge — "energy hubs" — opens up access to

oil and gas expertise through conversation threads. These approaches put the company at a

competitive advantage over service firms operating on a partner model that oftentimes struggle to

maintain global consistency.

©2014 IDC Energy Insights #EI249425 10

Challenges

The IT industry, operational technology, and the oil and gas industry are all going through massive

changes. As a professional service firm with a long history in the industry, Accenture now faces more

competition from Indian firms that are steadily building more domain expertise. Accenture has already

tackled labor arbitrage by standing up offshore services. The company is also trying to stay out ahead

by moving toward "everything as a service." The provider/alliance relationship between Indian firms

and the traditional petro-technical applications offered by Schlumberger and Halliburton also offers

competition through platform offerings in upstream.

Capgemini — Committed to Success

Capgemini offers its project-based and managed services to the oil and gas industry. Headquartered in

France, the company takes advantage of Indian-based resources for labor arbitrage and leadership

and has oil and gas centers of excellence in major oil and gas locales (Houston; Aberdeen,

Washington; and Stavanger, Norway). The company is well respected in the oil and gas industry as a

thought leader, especially in Europe. Capgemini is rated as a Major Player in this IDC MarketScape.

2013 was a strong year for Capgemini. For the past two years, the company has worked to strengthen

its commitment and expand its solutions for oil. That has paid off in major new wins — Statoil is an

example — and revenue growth. In terms of project-based client count, Capgemini is among the top 4

for project-based IT-related services. At the same time, the company is recognizing improved

profitability, especially as solutions have matured and become more "industrialized."

EnergyPath — a templated approach to shortening the implementation of SAP ERP — is one solution

that has matured. EnergyPath is built to speed implementation of SAP ERP and non-ERP SAP

applications using templates designed for the oil and gas industry. So far, the company has

implemented for refineries and oilfield service companies. Of note as well is the four-month

implementation by drilling company Pacific Drilling for a cloud-based suite on HANA using

EnergyPath. Beyond EnergyPath, Capgemini's recent acquisition of SSP builds on the EnergyPath

and also provides joint venture accounting capability. Capgemini is adding to its ERP capabilities with

Oracle projects.

Although cost reduction is a big theme — the Statoil project was won based on taking out additional

savings above and beyond labor arbitrage — Capgemini continues to build on its consulting and

solutions legacy. The company is currently working with a client to reengineer technical data

management. Asset life-cycle management and logistics are also areas where the company continues

to serve the industry.

Capgemini continues to invest in new solutions for oil and gas through its partnership with MIT and in

conjunction with recognized oil and gas industry players. For example, an asset life-cycle

management solution is being developed with partner AVEVA. Document management for technical

documents is being developed in partnership with EMC — the Documentum-based offering is called

WildCAT — and IBM and its FileNet application. Another solution under development is a reservoir

monitoring tool.

©2014 IDC Energy Insights #EI249425 11

Strengths

Capgemini is noted for its ability to execute projects successfully. It is a company value to serve the

customer well, and it is an essential part of how Capgemini perceives opportunities. The strategy is to

build the business through deepening the relationship with clients. Clients report that staff engages

well with their internal team and other service providers.

Capgemini demonstrates commitment to its clients in contract terms and pricing arrangements.

Performance-based managed service contracts are set up so that Capgemini takes on risk. Contracts

are also set up so that the oil and gas company can walk away with virtually no cost except for the

stranded investment.

Challenges

Capgemini has a long history in oil and gas, especially with anchor client TOTAL, but its approach

lacked focus up until recently. Capgemini will need to act quickly to "catch up." For further growth, the

company needs to accelerate its marketing and sales and the development of oil and gas–specific

project-based and outsourced service offerings. There will need to be multiple paths beyond ERP

design, build, and run to grow outsourced services. Efforts focused on outsourced services that are

independent of an anchor project will help grow Capgemini's business.

CGI — Experience the Commitment

CGI, with the acquisition of Logica in 2012, has done more than increase its installed base and

geographic reach. CGI has gained experience and expertise. The company now has a substantial

stable of oil and gas subject matter experts with degrees in economics, petroleum engineering,

geology, and geophysics. IDC Energy Insights' worldwide IDC MarketScape on professional service

firms in 2012 did not include CGI because it was too early in the acquisition to be evaluated. CGI is

rated as a Major Player in this IDC MarketScape.

CGI is embedded in the domain. Like IBM, CGI also offers software products that are used in the oil

and gas industry — hydrocarbon accounting, mobile workforce, and land management. In fact, the

company has services revenue associated with support of those products. The company is

experienced in energy trading and risk management (ETRM), with over 40 implementations in the past

15 years. CGI also runs a wells center of excellence for real-time monitoring and well integrity.

Experience in logistics is applied in tanker and fuel movements and emergency response. A recently

formed security practice focusing on process control will be applicable to the oil and gas industry,

especially in refining. A land management solution is being upgraded for the North American

unconventional requirements.

Strengths

IT outsourcing and business process outsourcing are areas where the company has seen much

success. CGI manages petro-technical applications typically used in upstream, such as geology and

geophysics and well management. This is a plus for independent upstream companies that may not

have access to staff to support these applications. A business process outsourcing offering for oil and

gas provides production and revenue accounting. Liscense2share is a cloud-based solution CGI runs

©2014 IDC Energy Insights #EI249425 12

for joint venture stakeholders in the North Sea off the Norwegian Continental Shelf. A substantial fuel

cards business that includes loyalty schemes provides a constant stream of revenue for the company.

The company has worked hard to develop partnerships that fit with line-of-business offerings. In the

upstream, close working relationships with Halliburton, Schlumberger SIS, and Baker Hughes make

sense given that CGI provides application management services for applications provided by these

oilfield service companies. CGI subscribes to the MURA upstream architecture initiated by Microsoft.

Other partnerships include OLF in trading, AspenTech and OSISoft in refining, and FleetCor in retail.

Challenges

CGI has yet to firmly establish the new identity of its extended capabilities in oil and gas since the

acquisition of Logica. It has made a good start over the past year, but with publicity about CGI in other

areas in the news, it needs to work harder to articulate its solutions and broadcast its capabilities under

a unifying theme that appeals to the industry.

Deloitte — Deloitte Knows Oil and Gas

Deloitte's approach to the oil and gas industry is to become deeply involved in long-term relationships

with its clients. That means offering a range of services to clients, including portfolio management,

strategy, risk management, finance, IT, tax, and sustainability. Deloitte's oil and gas practice has

experienced substantial growth in the past year. Deloitte is rated as a Major Player in this IDC

MarketScape.

Deloitte's business model is an advisory-led model, not an outsourcing- or managed services–led

model, with a heavy emphasis on business consulting. Where the company does offer IT

implementation and outsourcing (in the areas of application maintenance and security and business

process outsourcing), these offerings are a natural extension of existing advisory relationships.

Deloitte believes its degree of commitment to outsourcing (both AMS and BPO services) is consistent

with its business model, nondisruptive but additive to its service portfolio. Deloitte aims to serve oil and

gas clients wherever they operate with high-quality services that they need. The need for outsourced

services (especially in developing markets) is on the increase, and Deloitte is building out outsourced

services based on client expectation and demand in addition to its core service offerings.

Deloitte's current engagement with Petrobras demonstrates the breadth of its offerings, from advisory

on unconventional and presalt to oil and gas–specific ERP implementation. The rapid growth of the oil

and gas industry in Brazil has led Deloitte to develop a center of excellence in Rio and make a

commitment to expand its relationships with Brazilian universities and government and trade

associations.

Acquisitions point to Deloitte's growth strategy. The acquisition of MarketPoint brought energy market

simulation and price forecasting to its breadth of offerings. Deloitte's Resource Evaluation & Advisory

practice was created with the acquisition of Canadian-based AJM Petroleum Consultants in 2010.

More recent acquisitions are Vigilant for security — an important area for oil and gas — and Monitor for

strategy, specifically the science of innovation.

©2014 IDC Energy Insights #EI249425 13

Deloitte has expertise in advising oil and gas companies in exploration, particularly in new ventures

and business development. The company offers subscription-based data products — external

"technical data management" — that display oil and gas information from spatial, financial, and

reporting perspectives and advisory services to support strategic planning, market analysis, fiscal and

regulatory reviews, transactions, and data management.

Strengths

Deloitte is set apart from other service firms in oil and gas in the way it brings together technical and

financial expertise. An example is analytics-based advisory to help oil and gas companies assess

conventional and unconventional reservoirs, including reservoir modeling, production and economic

forecasting, M&A technical due diligence, and other engineering/geoscience analyses. Optimizing well

profitability is another area. In its advisory services, Deloitte deploys (proprietary) models to assess

profitability by modeling the supply chains for the energy at the asset level and benchmarking costs of

assets. In this area, it can compete with the consulting offerings of oilfield services companies.

Another differentiator is in commitment to training. Deloitte has a full range of strategies for recruitment

and development of staff. For recruitment, the company has relationships with universities with

petroleum degrees, student internships, and target hiring. Once employees are recruited, there are oil

and gas training courses, cross-training opportunities, mentors, collaboration hubs, codevelopment

with clients, awards, and innovation opportunities. These are re-enforced by "industry nerve centers" —

global, virtual networks for knowledge sharing that also support service delivery teams by sourcing

internal thoughtware, SMEs, and industry information.

Challenges

Deloitte has extensive oil and gas analytics that have already been built and tested. Much of Deloitte's

work involves using analytics to support advice to clients, which fits well with an advisory model. There

is benefit to oil and gas companies to receive independent counsel, especially when it comes to

making large investment decisions. However, with the current focus on analytics, Deloitte may be

facing competition that will offer a low-touch and low-cost model of analytics as a service.

The presalt efforts with Petrobras show off Deloitte's ability to provide technical and financial advice on

a complex scale. There will likely be much expertise gained. Deloitte needs to pay attention to the

diversification of its portfolio of clients to mitigate the risk involved as it is likely presale plays will be

limited to the region.

IBM — Dedication to Every Client's Success

IBM has been involved with the oil and gas industry for over 50 years, selling services, hardware, and

software. IBM Global Services is well known for its work in downstream. Recently, the company has

been devoting more resources to upstream with a focus on exploration, production optimization, and

drilling. Over the past two years, IBM has grown and developed a global oil and gas pool of experts

and expanded partnerships. The company saw significant growth in its oil and gas services business,

especially in emerging economies. IBM is rated as a Leader in this IDC MarketScape.

©2014 IDC Energy Insights #EI249425 14

IBM has a well-developed and wide-ranging set of solutions for upstream, midstream, downstream,

and retail. Solutions that have been in the portfolio for at least a decade, such as asset management,

have been further developed to take advantage of 3rd Platform technologies — Big Data and analytics,

cloud, mobility, and social business. For example, a new engineered solution from IBM — PQM —

combines predictive analytics, decision management, and visualization and reporting with enterprise

asset management (EAM) and integrates with mobile-enabled operator and engineering work

processes. Big Data and analytics are being explored for drilling optimization, land management,

seismic interpretation, production optimization, logistics, and equipment scheduling and safety. In

addition, advanced analytics tools and techniques augment IBM's core technologies to create digital

security solutions.

Strengths

Solutions can often be easier to articulate than to deploy. From conception to deployment, IBM Global

Services has an edge in what it has delivered in terms of hardware (high-performance computing) and

software (application integration, telemetry, analytics, and business applications) together with

services to the oil and gas industry. One area where IBM has excelled is in assembling the technology

for Big Data and analytics. For example, IBM developed a way to simulate well performance, using the

model Prosper and multiple downhole data sources for pressure, volume, and temperature across 500

wells. Results were delivered within seven seconds to those who needed it. Another example is the

use of analytics for environmental monitoring, which uses high-frequency and subsea data to alert of

potential incidents.

That said, IBM works with other vendors and applications that are in place. Integration is a key focus

for IBM. One major oil and gas company has been pleasantly surprised that IBM has not tried to push

its product set but approached challenges with "whatever works best in the situation." The company

has an impressive set of partners chosen for each of its solution offerings and devotes resources to

supporting these partnerships.

Challenges

IBM is perceived to be a strong downstream player but somewhat late to the market in upstream. As it

continues to make investments in upstream, IBM needs to direct marketing efforts to ensure clients

understand its upstream expertise and offerings and dispel the notion that it is late to the market in

upstream. Promoting positive case studies in this area will help. The company is perceived to be a

high-cost provider; however, most large oil and gas companies recognize the value that IBM brings

and understand that IBM is working through strategies to reduce costs — automation, cloud, offshoring.

For example, a customer may decide to use cloud-based services to select and configure the

hardware stack supporting implementation for a specific application. Majors and supermajors are

willing to pay for value, although they were more cost conscious in the past year. Oil and gas

companies in the midtier will need to be convinced that IBM is the right provider.

Infosys — Ready for the Future

Infosys has been involved in providing a range of services to the oil and gas industry for 16 years. The

company has a good complement of project-based and outsourced services and has made inroads

into the midtier market, especially with independent upstream oil and gas companies. Infosys has a

©2014 IDC Energy Insights #EI249425 15

well-conceived strategy for expanding into regions and market segments where there is room for

growth. The company is investing in local resources in geographies like Iraq, Azerbaijan, and Brazil as

well as using local partners in these regions for capabilities, local language, and cultural fit. Infosys is

rated as a Major Player in this IDC MarketScape.

Infosys has a large contingent of employees dedicated to the oil and gas industry. Facing the same

obstacles in building up a staff of experts in oil and gas, Infosys is addressing skills shortages by

recruiting petroleum engineering graduates and training them in information technology. There are 5

levels of oil and gas training, the top 2 in conjunction with universities for upstream. Employees

typically advance through each level to acquire competencies.

Partnerships and alliances are important. Infosys is building on top of the Oracle high-performance

data management computing stack, which includes Exadata and Exalytics. Use cases have been built

for drilling and production. Infosys also works with SAP on midtier deployments and has a solution in

development for drilling equipment and tool reliability on SAP HANA. There are a large number of

alliances with niche vendors related to specific competencies. Commitment to oil and gas is shown

through participation in the data standards group Energistics, PPDM, Pipeline Open Data Standards

(PODS) (pipelines), and the Society of Petroleum Engineers (SPE) and use of industry standards in

data models.

Strengths

Infosys has worked with its clients to develop solutions that have strengthened its oil and gas

credentials in the space. Technical data management is an area where Infosys has good experience

particularly with well (Prosource, Recall, Petra, OpenWorks) and production data. The company has

also deepened its knowledge of upstream through work with oilfield services companies to develop

software products for production optimization and real-time well data acquisition and management.

Production optimization work extends to owner/operators as well. For example, for one oil and gas

supermajor, Infosys has built a toolkit on top of Gap, Prosper, and HYSES that simulates and

optimizes producing assets. This effort helped the client increase production by 2–4%. In midstream,

work has involved automation of volumetric allocations for a pipeline company.

Infosys has an impressive model for customer engagement. For large accounts, Infosys has three tiers

of review that occurs at regular intervals. The Infosys CEO meets every six weeks with executive

leadership. There are six-month reviews of the governance process as well as six-month reviews with

CIOs to discuss what has gone well and what needs to be improved. There is also a performance

review every six months at the portfolio level — trading, upstream, refining, and marketing. Infosys

employees are measured on client satisfaction, performance, and personal improvement. Customers

report that Infosys has brought innovation to projects. This puts the company in a strong position for

being awarded managed services contracts once the project is implemented.

Challenges

By definition, professional services companies create solutions that are fitted to the client. Successful

companies choose solutions with a sizable market potential and make investments to enhance these

solutions but also create templates for repeatability wherever possible to improve profitability and

lower costs for the customer. Infosys has experience with many different projects. As a company,

©2014 IDC Energy Insights #EI249425 16

Infosys has developed platforms for analytics and mobility. If it can demonstrate that it can build on

these as repeatable elements of custom-fitted solutions, this will benefit the industry in the long run.

KPMG — Advisory Excellence

KPMG is known for its excellence in financial advisory services (tax advisory, portfolio planning,

acquisitions, divestitures, etc.), but it is also experiencing growth in IT consulting, systems integration,

network consulting and integration, and IT education and training — practices that are increasingly

integrated across its portfolio. Financial advisory relationships with upper management in oil and gas

help drive its IT business. Centers of excellence in oil-producing regions help too. KPMG is rated as a

Major Player in this IDC MarketScape.

KPMG's mantra is to help energy and natural resources companies in four areas — risk and regulation,

portfolio, innovation, and performance. For oil and gas companies, risk and regulation means focusing

on Dodd-Frank, cybersecurity, and environmental health and safety. In portfolio, the focus is on

acquisitions and divestitures, joint ventures and partnerships, and data and records quality.

Performance is achieved with attention to talent management, maximizing uptime, and increasing

productivity and efficiency. Innovation includes digital oilfield, advanced drilling and exploration, and

access to more data.

KPMG currently serves a diverse portfolio of clients, with a focus on the large oil and gas corporations

(over 10,000 employees). Growth is expected to come from emerging economies that need a full

range of services, starting with strategy. Of course, that requires investment, and KPMG has made a

significant investment to build out local capabilities, delivery centers, and sales in those regions,

organizing these around functional capabilities. The oil and gas industry group provides go-to-market

direction and develops solutions for oil and gas. It leverages functional groups to contribute to delivery.

Strengths

KPMG's understanding of the oil and gas business informs recommendations on implementation of

technology. The company has solid competencies in hydrocarbon accounting and energy trading and

risk management. Knowledge of regulations in each of those areas and the variations in each country

helps speed up projects. Knowledge of the industry is also being applied in two solution areas being

rolled out now — predictive maintenance and talent management.

KPMG invests in thought leadership in oil and gas, with regular publications and events geared toward

the industry. The KPMG Global Energy Institute (GEI) is a worldwide knowledge-sharing forum on

current and emerging industry issues. The company promotes women in leadership in energy and

provides networking and education opportunities for women. Recently completed research done in

partnership with Rigzone provides data on the demographics of the current oil and gas labor force

(years of experience, education levels) that KPMG is parlaying into an oil and gas–specific talent

management offering.

Challenges

Although still developing its IT implementation business in oil and gas, KPMG has a good start on its

competencies. It has done well in CIO advisory and automating manual generic processes. There is

©2014 IDC Energy Insights #EI249425 17

room to grow in systems integration and application development. KPMG has also been relatively slow

to the market with oil and gas Big Data and analytics solutions and engagements. On a positive note

are recent acquisitions of Wise Windows (sentiment analytics) and Link Analytics (communications

analytics), although these will take work to adapt to the needs of the oil and gas industry. KPMG's

approach to innovation is to use catalyst companies to accelerate innovation, and that will be an

interesting model to watch.

L&T Infotech — IT, Engineering, Automation

L&T Infotech is a part of the Larsen & Toubro Group of companies, a $14 billion plus technology,

engineering, construction, manufacturing, and financial services organization with global operations.

L&T Infotech's oil and gas engagements are primarily in the area of IT outsourcing — application

development and management. The company has engagements with supermajors, majors, and

national oil companies. Many of the engagements bring cost reductions through automating manual

processes. L&T Infotech is ranked as a Major Player in this IDC MarketScape.

In addition to having ERP implementation and application management work under its belt, L&T

Infotech has experience specific to the oil and gas industry. Of note are technical architectures for

business and operational intelligence (upstream, pipeline, refining), deployment of pipeline monitoring

and leak detection, and implementation of reliability-centered maintenance (RCM). Application

management services cover petro-technical applications such as Openwell, OpenWorks, Petrotech,

Petrel, and WellView. Downstream experience includes Lab Information Management System (LIMS)

and Manufacturing Execution System (MES).

L&T Infotech is currently developing enhancements in several solution areas: capital projects

integration to support management of multiple projects using a consistent set of processes; a GIS-

based system for pipeline construction, inspection, and maintenance; and mobile apps for

collaboration and compliance data capture.

Strengths

L&T Infotech aims to reduce professional service costs for its oil and gas clients, and it shows. The

company has delivered the labor arbitrage that comes from offshore resources. One customer

reported a savings of 3:1 through the use of managed services. For project-based work, the company

has developed over 1,700 business process templates that help speed project development. For oil

and gas companies, there are 10 frameworks including digital oilfield, integrated refinery, gas

management, and pipeline management. It is not just about cost reduction. L&T Infotech has

developed a successful governance approach that includes quarterly client sessions and reports on

useful innovation accomplishments that shows promise for the oil and gas industry.

The pedigree that L&T Infotech has, in particular in instrumentation, engineering, and construction, will

become even more useful in the future in informing IT for automation and capital project management.

Parent company L&T generates 40% of its $14.0 billion revenue from the energy sector as an

engineering, procurement, and construction (EPC) vendor performing feed engineering, plan design,

ocean engineering, facilities engineering, reservoir engineering, and capital projects. L&T Infotech

benefits from the migration of some L&T personnel in oil and gas to the IT service side of the business.

Experience in instrumentation has helped L&T Infotech customers land technical projects. For

©2014 IDC Energy Insights #EI249425 18

example, L&T Infotech won a contract with an oil and gas company to upgrade refinery lab systems to

be Windows 7 compliant. In this case, L&T Infotech was able to leverage development into a contract

to not only maintain applications but also perform all the mobile application development related to the

systems.

Challenges

Each of L&T Infotech's meetings with oil and gas companies starts with a safety moment. These are

not just a list of exits but provide valuable safety-related tips. The company has demonstrated it works

well with the industry and has developed frameworks in conjunction with its clients. Of particular note

are frameworks in digital oilfield readiness and petro-technical data management. The challenge for

L&T Infotech is to communicate the value of these frameworks, using its clients as references to gain

further petro-technical work. This challenge is not unique to L&T Infotech; in fact, our research has

shown that this is a challenge faced by other firms that operate in the oil and gas segment.

PwC — Building Relationships, Creating Value

PwC has been serving the oil and gas industry for over a 100 years. In the past 4 years, the company

has redoubled its efforts in its IT services business for oil and gas companies. A series of

benchmarking studies launched in 2013 will help oil and gas companies move into the future. PwC is

rated as a Major Player in this IDC MarketScape.

PwC sees its mission as helping oil and gas companies increase their free cash flow performance.

Despite the common perception that oil and gas profits are substantial, when compared with other

industries, on a P/E basis, the multiples are relatively smaller for the oil and gas industry. Companies

are measured on free cash flow performance, and this is an area that PwC addresses with the C-suite,

functional and IT leadership, and operations/field management. It is not about strategy alone. PwC

works with clients to understand how strategy informs the operating model that is tied to business

processes and technology within the context of the technology portfolio.

PwC does project-based services. The approach is to start with strategic business consulting, develop

an operating model, and then enable that model through technology. It typically sells projects in

phases. This strategy has proved to be successful for PwC so far. Clients usually opt for all phases. At

this point, the company delivers few IT outsourcing services.

PwC has more than tripled the percentage of its staff with oil and gas experience and expertise in the

past three years. The increase in oil and gas experts has come in part organically through experienced

hires, recruitment efforts at universities, and acquisitions, such as the recent acquisition of Booz &

Company (now Strategy&). There are oil and gas centers of excellence in all the right places for oil and

gas — Houston, Calgary (Alberta, Canada), the United Kingdom, Norway, the Middle East, Russia,

Australia, and Brazil, with one being developed in China.

Strengths

When PwC works a solution, the company goes deep. Each solution is based on an expert

understanding of the regulatory and economic environment associated with the solution, best practice

business processes, and forward-looking IT. Well-conceived approaches to land management and

©2014 IDC Energy Insights #EI249425 19

well development set PwC apart from other service providers. For example, oil and gas companies are

focused on shortening the time from drilling to well construction. There are many hand-offs necessary,

and the lack of common processes has lengthened the time to production. Land management has

become extremely important in unconventional shale gas and tight oil where horizontal drilling means

acquisition of land or mineral rights of multiple blocks before drilling can occur, and many wells need to

be drilled to understand the geology and formations, develop the reservoir, and reach sufficient

production volumes to justify the investment. If not managed properly, leases can expire, leaving the

exploration and production company at risk. PwC understands the context — local property laws,

jurisdictions, mineral laws, state and federal regulations, and lease accounting standards — and knows

how to integrate applications and data services that inform oil and gas companies of their options. For

downstream, energy trading, risk management, reliability-centered maintenance, and process safety

are areas where PwC brings substantial experience.

PwC has a matrix approach to delivering services to its clients. Competency breaks down as 40% from

oil and gas subject matter experts, 40% competencies aligned with energy, and 20% from the

horizontal, such as supply chain management and logistics. Sharing of insights and data is done

through a collaboration platform. Delivery is not dependent on a global delivery team, which is a plus

for those national oil companies that want to see a representation of locals on projects. A feedback

mechanism is in place to ensure quality in the deliverables. An independent team within PwC

periodically performs "cold eye reviews" that are reported back to the client and the PwC client team.

Challenges

Professional service firms with roots in tax advisory are typically a collection of local and regional firms

under one corporate umbrella. This arrangement has inherent challenges, as many can attest to.

PwC has made good strides in building up its marketing approach. Over the past two years, PwC has

participated in more events and developed thought leadership pieces. There is still room to grow,

especially in sharing PwC's future road map of solutions if the company wants to increase its share of

the market.

TCS — Engineering-Led Reimagination

TCS has the pedigree of the Tata group with major industrial businesses — in Engineering Products

and Services, Materials, Energy, Chemicals, and Defense and Aerospace. TCS is a preferred or

strategic partner for several divisions at oil and gas companies. Since the IDC MarketScape on

professional service firms in 2012, TCS has made substantial progress on its journey to become

embedded in the industry. TCS is rated as a Major Player in this IDC MarketScape.

TCS' oil and gas business has above-average profitability. What is interesting about this is that the

company has also been able to reduce costs to customers through streamlining IT processes and

developing a delivery model that drives collaboration across highly experienced industry leaders and

industrialized service delivery. For example, when it took over application management at a major oil

and gas company (a fourth-generation outsourcer), TCS helped to take out nearly 20% of the already

optimized cost base, beyond labor arbitrage benefits. Of course, labor arbitrage helps, although TCS is

quick to point out that the company is keen on keeping close to the business — "not sacrificing

business intimacy for efficiency."

©2014 IDC Energy Insights #EI249425 20

The oil and gas practice is a strategic focus at TCS, and the company is investing heavily in research and

development and recruitment. Collaboration efforts with Rice University, Texas A&M, and MIT and

across TCS' customers are in line with TCS' ambitions to be a catalyst for co-innovation in the industry.

Of note is the work that TCS is doing with 3rd Platform technology with Big Data and analytics, social

business, mobile, and cloud. Social business scans detect supply chain disruptions. Mobile apps provide

refining scorecards and track crude tankers. Big Data work includes the implementation of infrastructure

and data management including open source technology. Multiple industries can take advantage of TCS'

analytics framework for consumption and analysis of sensor data — and eventually real-time data.

Strengths

TCS has demonstrated that it can bring its engineering, oil and gas, and IT competencies together.

Having TRDDC, the engineering and design labs for the Tata group, hosted in TCS helps. Work in

engineering and construction has proven useful in developing a capital project management solution to

manage resource allocation, payment schedules, and project slippage. Expertise with aerospace and

manufacturing has contributed to visualization of refinery plant operations and well data. TCS has

worked with an oilfield services company to engineer software products to improve drilling and

completions. For the future, the oil and gas industry is changing the methods used for simulation, so

TCS' engineering and design knowledge and expertise in high-performance computing can be helpful

in areas such as reservoir simulation.

TCS is versatile enough to grow within a company, something that is critical to success in an industry

with a relatively limited number of customers. For example, for one oilfield services company, TCS has

provided services for product life-cycle management (PLM), technical data management, analytics

(mean time to failure, reliability improvement), CAD libraries, and regression testing. At a major oil and

gas company, TCS supports application maintenance of well engineering applications, capital project

management, asset maintenance, production operations integration, energy trading, and data

management services. In part, this is due to the success that TCS has had in recruiting industry

experts that have experience and expertise in geology, physics, petroleum engineering, hydrocarbon

production accounting, and so forth.

Challenges

The key to future success in the industry is through the ability to innovate and transform. TCS is putting

itself in the right circles to germinate innovative ideas through its collaboration efforts with academia.

By structuring innovation into the customer engagement model, TCS can bring new ways of doing

things to each of its clients. More and more oil and gas companies are looking to their vendors to work

together to deliver innovation, and it is important that service providers take an active role in making

this happen.

Like other professional service firms relatively new to the industry, TCS needs to educate the market

on the value of what it brings to the industry. TCS is building a reputation for bringing oil and gas

business expertise to the technical IT work it does, building new architectures that are informed by

domain expertise. Given the industry's need to marshal data resources to achieve business value,

domain and engineering informed IT will end up bringing increasingly more value to the industry.

Professional services firms providing these capabilities will be considered trusted advisors. There is

much education that needs to be done in this area.

©2014 IDC Energy Insights #EI249425 21

Tech Mahindra — Connected Oil and Gas

Tech Mahindra has been providing IT services to the oil and gas business for about 12 years, albeit in

a small scale. The company now operates vertically in North America but has plans to extend

verticalization to other regions with additions to sales force and delivery centers in targeted regions.

The acquisition of Complex IT, a Latin America–based services company, will help in expansion in that

region. Tech Mahindra is ranked as a Contender in this IDC MarketScape.

Tech Mahindra utilizes its own as well as third-party platform technologies to develop solutions for the

oil and gas industry. Currently in development is a cloud-based pipeline integrity management solution

in conjunction with Microsoft. Built on top of Azure using the PODS database, the solution has

potential for markets where pipeline companies are primarily small to midsize. Also in development in

the Big Data and analytics category is a means of accessing downhole pressure, volume, temperature,

and other conditions for analysis as well as a solution for water management for shale gas. The

company is also actively working with telecommunications companies to develop network solutions for

M2M automation.

Strengths

Tech Mahindra's strengths lie in foundational capabilities that it has applied in the oil and gas setting —

data quality management, support of design and GIS applications, implementation of ERP systems,

and infrastructure management (datacenters, hosting). Tech Mahindra also develops spot solutions

that can be slotted into a broader enterprise strategy. For product quality, there is a lubes quality

management system developed for lubes marketing companies. For safety, the company is

developing a solution to monitor driver behavior.

Of note are Tech Mahindra's solutions for energy trading and risk management and pipelines. There is

a strong bench for ETRM applications, plus a training program to continue to feed that business. For

pipelines, current work includes development of applications and Web-based portals, application

development and management for legacy applications, application implementation and integration with

control systems, migration to Pipeline Open Data Standards, ADMS projects for legacy and proprietary

applications, and geospatial mapping.

Challenges

Tech Mahindra has a relatively small footprint in oil and gas. In particular, the company has room to

grow in project-based work. Contract size is relatively low in this area. The company has made a good

start with the adoption of Agile. This and other methodologies for implementation will need to be

embedded into the way business is done on every project. That said, Tech Mahindra is making all the

right moves to develop its workforce for the future. It has delivered competency-based learning and

development solutions for upstream, midstream, and downstream as well as delivered Web-based and

class room training, mentoring and mobile training, and simulators. The company's long-standing

relationships with some of the current oil and gas companies should provide a good list of

qualifications to use in pursuing new customers. Tech Mahindra is also going in the right direction with

its partnership strategy.

©2014 IDC Energy Insights #EI249425 22

Wipro — Taking on the Value Chain

With the acquisition of SAIC's Oil and Gas practice in 2011 for approximately $150 million came an oil

and gas business in technical application management, technical data management, and digital

oilfield, plus 1,450 employees. While complementing Wipro's downstream business, this acquisition

added depth in the upstream and scale to consulting. Since that time, Wipro has integrated the

acquisition and continues to grow its business; it ranks in the top 4 of firms reviewed in this report in

revenue associated with oil and gas. Wipro is rated as a Major Player in this IDC MarketScape.

While its stable of experts is impressive, Wipro continues to build domain expertise. The company is

preparing for the future by concentrating on development of local domain experts in conjunction with its

oil and gas clients in the Middle East, Canada, Australia, and other growth markets. When this type of

development is targeted to low-cost labor areas, the client gets a combination of local "content" and

lower cost resources with a blend of domain and functional expertise. Development of local resources

is also part of Wipro's growth strategy.

Wipro leverages partnerships for innovation and product development. Currently in development is an

SAP HANA–based data analytics for production data. Of note is a solution developed in partnership

with Cisco for rapid wireless connectivity of rigs for the unconventional environment. Wipro provides

program management and network architecture. Partnerships go beyond innovation and production

development. For example, Schlumberger SIS and Wipro jointly market SIS products in combination

with Wipro services. To the buyers of the technology — oil and gas owners/operators — this is attractive

as it establishes a level of trust that Wipro understands how to support these products.

For the future, Wipro is enhancing the way it organizes to deliver client services, as well as sales and

marketing. Wipro has established a global P&L for oil and gas to ensure that there are no

complications with the local regions and for global consistency. A service catalogue will ensure that

appropriate resources are assigned appropriate to the tasks. There are domain oil and gas services in

ETRM, HSE, upstream, downstream, pipelines, capital projects, LNG, and EAM. The matrix also

includes "horizontal" technology services in ERP, BPO, testing, and infrastructure services.

Strengths

Wipro is highly regarded in the industry for its domain expertise, especially in upstream. Experience in

application development and maintenance of petro-technical applications and strategic alliances, such

as the one with Schlumberger, has given Wipro a "leg up" in technical data management and an

understanding of upstream workflows. For example, Wipro is currently acting as the PMO for a project

to standardize subsurface and reservoir development processes across multiple regions for one major

oil and gas company.

Having now fully integrated the SAIC acquisition, Wipro has a strong and well-articulated set of product

offerings supported by marketing. The "marriage" has also brought cloud enablement in support of

ETRM (test assurance services, knowledge process outsourcing), upstream production analytics,

security (identity access management, secure file transfer), and customer analytics.

©2014 IDC Energy Insights #EI249425 23

Challenges

Wipro has established its position in the oil and gas industry, especially with its major clients where it is

a preferred provider. As the reorganization becomes established, there will be means to execute on a

growth strategy. Oil and gas is a fast-moving business, so Wipro, like other firms, must stay ahead of

where the business is going. This also means development of a well-articulated growth strategy.

APPENDIX

Situation Overview

As it becomes more expensive to pursue resources in the face of stable oil prices, the oil and gas

industry is looking to streamline operations. Even leaders that have the strongest asset bases know

that they need to make changes in order to maintain position. According to the president of Total,

"Costs to develop have increased dramatically since 2005, Total's ROCE dropped from 16% in 2012 to

13% in 2013." As Shell CEO says, "We need a tighter grip on performance."

This new cost consciousness has oil and gas companies looking to professional services firms to help

them reduce costs. BP led the way in reducing IT costs when it executed on a strategy to outsource

65% of its annual IT opex in 2009 to reduce costs and streamline operations. Most of these cost

reductions came from reducing the number of providers in the stable and implementing cost reduction

strategies in "generic" IT. Now oil and gas–specific deployment of solutions and services are under

consideration for streamlining the business as well as reducing IT and engineering support costs.

That said, value still takes priority over cost on high-value projects and ongoing services. The majors

and supermajors have set the bar high for their service providers to have oil and gas subject matter

expertise. National oil companies look to their providers to help them follow the best practices in the

industry. Providers must also use local partners and develop local talent. These are tall orders for an

industry that experiences a gap between entry-level and seasoned experts that will not be easy to

close.

Professional service firms are rising to the occasion deepening their capabilities in upstream,

midstream, downstream, and retail, offering solutions that address industry business objectives and

services such as application development and maintenance of petro-technical applications. Even

service providers relatively new to oil and gas IT have developed oil and gas–specific solutions and

invested in hiring and growing oil and gas talent.

The Size of the Market

The market for professional services in the oil and gas industry is significant. According to IDC Energy

Insights' Worldwide Oil and Gas IT Spending Guide, the global market for IT services to the O&G

industry totaled $15.1 billion in 2013. IT services is expected to grow to $19.1 billion in 2017 at a

CAGR of 6%. The market for business process outsourcing is not included in this estimate.

©2014 IDC Energy Insights #EI249425 24

Essential Service Provider Guidance

Use this IDC MarketScape to understand where you need to target your efforts going forward. In detail:

Build your stable of subject-matter experts and keep them engaged. Successful professional

service firms have programs in place that support a multipronged strategy to contribute to theoverall development of SMEs and oil and gas IT experts. Relationships with universities with petroleum engineering degrees and internships can provide a source of young employees.

Demonstrated ability to grow local expertise to leadership positions will help you meet localrequirements in some countries and also provide a career path for employees that will help reduce turnover. To attract senior personnel, offer challenging engagements and opportunities

to contribute to innovation. In a situation where you are gaining SMEs through acquisition, the first few months are critical to keeping employees from moving on. Concentrate on providing clear direction and proactive programs to integrate these valuable contributors into your

organization.

Work to extend your oil and gas centers of excellence in regions of the world where oil and

gas companies are expected to be most active. Centers of excellence allow you to showcase your solutions to clients and prospect, provide hubs for knowledge sharing and global

discipline, and act as "in region" oil and gas support. Even if you do not have a center of excellence in an emerging region such as West Africa, be sure you can demonstrate your ability to deploy oil and gas expertise in-region quickly when necessary.

Establish a well-articulated set of solutions for the industry. You should be able to demonstrate

success in deploying the solution. Marketing and sales efforts will be most successful when you understand which solutions are most closely aligned with the oil and gas company's maturity and objectives (refer to Table 4).

Develop solutions and services in partnership with others. Complexity in the oil and gas

industry is only increasing and demands an ecosystem to meet the needs of the industry.Work with partners to support greater digitization of the oilfield, pipeline, and refinery and that have the ability to incorporate communications with devices and control systems. Demonstrate

effective partnerships with ISVs, technology vendors, oilfield service companies, engineering,procurement, and construction vendors, or other service firms to deliver a comprehensive project or managed service.

Work with the industry to develop advanced pricing models. Oil and gas companies are still

tied to fixed price contracts and rate cards. However, they are becoming more receptive to gain/share. The supermajors are currently working out what it would take to set up and measure a win-win business outcome contract. Be ready with models that you can offer that

include ways to measure, validate, and allocate bonus or onus.

Continue to provide excellent service to your customers. Oil and gas companies are not unlike

other companies engaging services firms. They expect excellent service — meeting timelines and service-level agreements. Everyone recognizes that there will be difficulties; what is

important is having mechanisms in place for identification and resolution.

Reading an IDC MarketScape Graph

For the purposes of this analysis, IDC divided potential key measures for success into two primary

categories: capabilities and strategies.

©2014 IDC Energy Insights #EI249425 25

Positioning on the y-axis reflects the vendor's current capabilities and menu of services and how well

aligned the vendor is to customer needs. The capabilities category focuses on the capabilities of the

company and product today, here and now. Under this category, IDC analysts look at how well a

vendor is building/delivering capabilities that enable it to execute its chosen strategy in the market.

Positioning on the x-axis, or strategies axis, indicates how well the vendor's future strategy aligns with

what customers will require in three to five years. The strategies category focuses on high-level

decisions and underlying assumptions about offerings, customer segments, and business and go-to-

market plans for the next three to five years.

The size of the individual vendor markers in the IDC MarketScape represents the market share of each

individual vendor within the specific market segment being assessed.

What Makes a Leader

Leaders in professional services in oil and gas have a commitment to the oil and gas industry that is

backed at the executive level of their companies. This is demonstrated through investment in research

and development, oil and gas centers of excellence in major oil and gas hubs, and oil and gas subject-

matter experts. Leaders are viewed as trusted advisors that work with their clients and other service

providers in the oil and gas ecosystem to drive innovation. Providers have a set of well-developed

solutions that are specific to oil and gas, a stable of experts in oil and gas industry disciplines and with

extensive experience working in oil and gas business-related IT, a strong set of disciplines to enable

the global workforce at the firm to access a common set of best practices, and demonstrated

capabilities in incorporating 3rd Platform technologies into their services.

Major Players Continue to Advance

A substantial stable of major players have had impressive growth over the past two years. Of note are

firms that were once considered commodity IT players that are now moving into more business-critical

areas such as petro-technical application and data management. These players are extending their

reach into new geographies and establishing oil and gas centers of excellence to support sales and

marketing, as well as client innovation, and deliver a combination of horizontal (supply chain, ERP)

and vertical (energy trading and risk management, production optimization, petro-technical data

management, capital project management) services to the oil and gas industry. Later entrants to the

market have engineering capabilities but need to demonstrate how effectively they can bring expertise

to IT-related project-based and services work.

IDC MarketScape Methodology

IDC MarketScape criteria selection, weightings, and vendor scores represent well-researched IDC

judgment about the market and specific vendors. IDC analysts tailor the range of standard characteristics

by which vendors are measured through structured discussions, surveys, and interviews with market

leaders, participants, and end users. Market weightings are based on user interviews, buyer surveys, and

the input of a review board of IDC experts in each market. IDC analysts base individual vendor scores,

and ultimately vendor positions on the IDC MarketScape, on detailed surveys and interviews with the

vendors, publicly available information, and end-user experiences in an effort to provide an accurate and

consistent assessment of each vendor's characteristics, behavior, and capability.

©2014 IDC Energy Insights #EI249425 26

Market Definition

For this IDC MarketScape, IDC Energy Insights is reviewing professional services firms that are

providing the following services to the upstream, midstream, downstream, and trading segments of the

O&G industry:

Business consulting. Business consulting involves advisory and implementation services

related to management issues. It often includes defining an organization's strategy and goals and designing and implementing the structures and business processes that help the

organization reach its goals. Business consulting includes three main areas: strategy consulting, operational improvement consulting, and change and organization consulting.