Download - ILCUF - Social Performance

SOCIAL PERFORMANCE

Outline Information for Credit Unions and CreditUnion Apex Bodies

Introduction

Credit Unions and Credit Union Apex Bodies have a social mission. Like all cooperative organisations they seek to bring social benefits to their members and to the wider community.

In order to be sustainable and to achieve their social mission they must all be financially viable.

Credit Unions and their Apex Bodies are accustomed to applying very specific measurement tools to assess their financial performance. In this area they are supported and instructed by legislation and state supervision.

In the social area however they do not always have specific tools or processes for measuring or managing social performance.

This booklet aims to assist them to consider this area. It gives extracts from the wide sectors of Microfinance, where Social Performance Management has become very important in maintaining the sectors social mission.

It also contains extracts from work done by ILCU Foundation under the EC ACP ‘West Africa Credit Unions against Poverty Programme’ (WACUPP). This is the first formal research, training and study carried out by our partner countries in Social Performance Management.

This booklet contains

1. The Universal Standards for Social Performance, as developed by the Social Performance Task Force http://www.sptf.info/

2. Extracts from a study of the levels of Social Performance of Credit Unions in the Gambia. This study was carried out by the National Association of Cooperative Credit Unions of the Gambia (NACCUG)

3. The ILCUF designed Questionnaire to assess Social Performance of a Credit Union

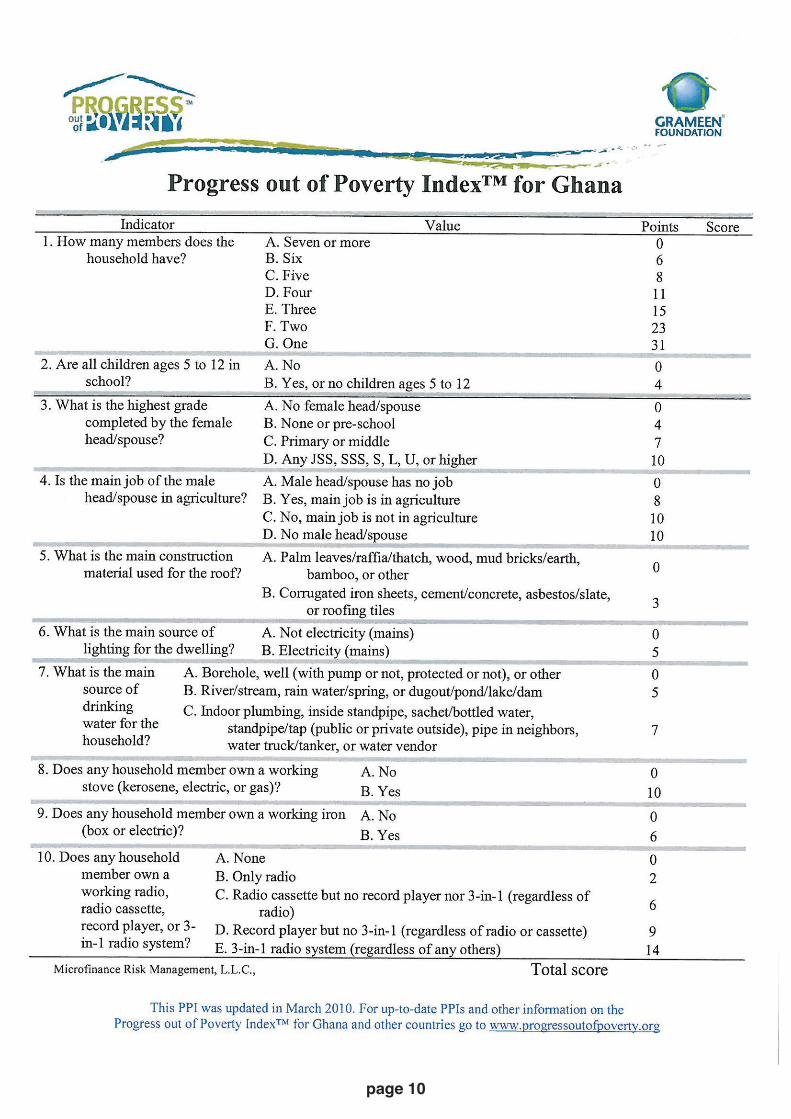

4. The Progress out of Poverty Index household questionnaire which is used to measure household wealth in Ghana. http://www.progressoutofpoverty.org

ILCUF hopes that this knowledge will encourage and assist Credit Union movements

to continue to maintain a strong focus on social mission and to build their capacity in

this area.

page 2

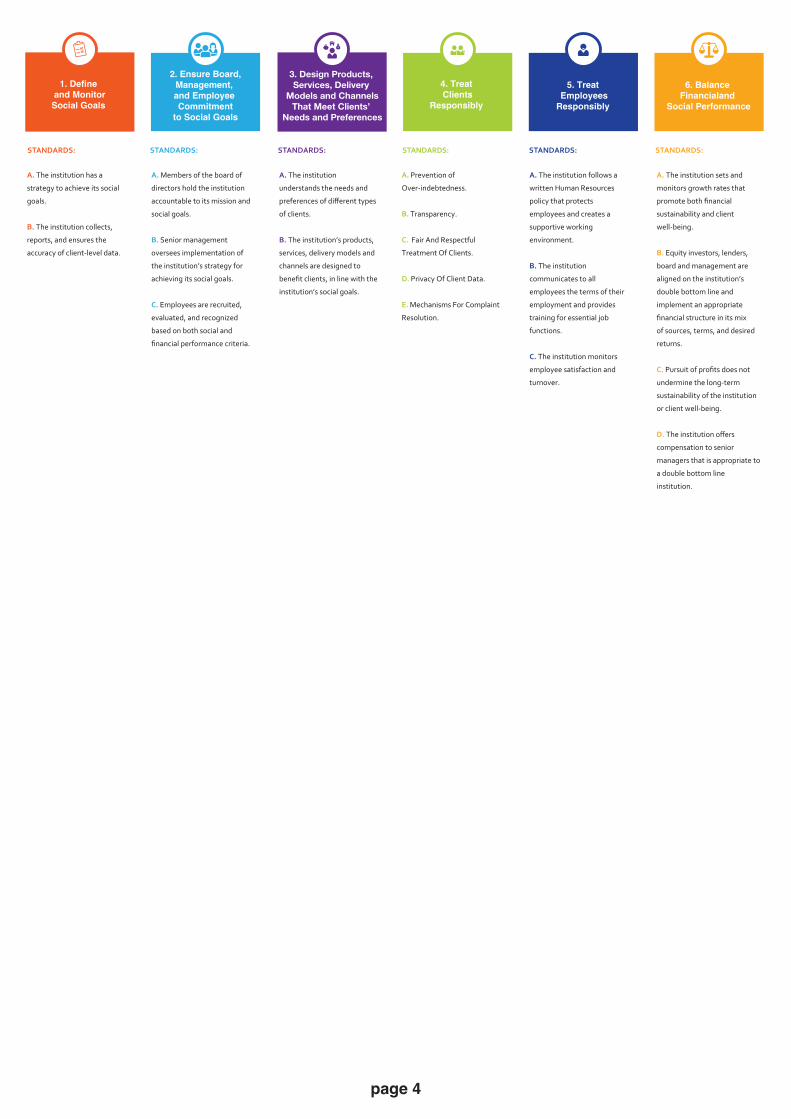

The Universal Standards for Social Performance Management is a comprehensive manual of best practices

created by and for people in microfinance

as a resource to help financial institutions

achieve their social goals. The Universal

Standards can unite the industry behind

a common approach to social

performance management and

enhance its reputation for

responsibly serving people's

financial needs.

UNIVERSAL

STANDARDS

FOR SOCIAL PERFORMANCE MANAGEMENT

DEFINE AND MONITOR SOCIAL GOALS

TREAT CLIENTS

RESPONSIBLY

TREAT EMPLOYEES

RESPONSIBLY

BALANCE FINANCIAL

AND SOCIAL PERFORMANCE

DESIGN PRODUCTS,SERVICES, DELIVERY

MODELS AND CHANNELS

NEEDS AND PREFERENCES

MANAGEMENT, AND EMPLOYEE COMMITMENT TO

ENSURE BOARD,

SOCIAL GOALS

“There are almost as many tools and processes

as there are stakeholders. The Universal Standards

are the first and only resource that draws on the

many processes in the field to create a unified

structure and language for social

performance management.”

Jürgen Hammer, Grameen Crédit Agricole Foundation

For more information, please visit: www.sptf.info

page 3

A. The institution follows a

written Human Resources

policy that protects

employees and creates a

supportive working

environment.

B. The institution

communicates to all

employees the terms of their

employment and provides

training for essential job

functions.

C. The institution monitors

employee satisfaction and

turnover.

A. The institution sets and

monitors growth rates that

sustainability and client

well-being.

B. Equity investors, lenders,

board and management are

aligned on the institution’s

double bottom line and

implement an appropriate

of sources, terms, and desired

returns.

C.

undermine the long-term

sustainability of the institution

or client well-being.

D.

compensation to senior

managers that is appropriate to

a double bottom line

institution.

STANDARDS:

3. Design Products, Services, Delivery

Models and ChannelsThat Meet Clients’

Needs and Preferences

STANDARDS:

STANDARDS: STANDARDS: STANDARDS:

5. Treat

Employees

Responsibly

6. Balance

Financialand

Social Performance

2. Ensure Board,

Management,

and Employee

Commitment

to Social Goals

STANDARDS:

4. Treat

Clients

Responsibly

1. Define

and Monitor

Social Goals

A. The institution has a

strategy to achieve its social

goals.

B. The institution collects,

reports, and ensures the

accuracy of client-level data.

A. The institution

understands the needs and

of clients.

B. The institution’s products,

services, delivery models and

channels are designed to

institution’s social goals.

A. Prevention of

Over-indebtedness.

B. Transparency.

C. Fair And Respectful

Treatment Of Clients.

D. Privacy Of Client Data.

E. Mechanisms For Complaint

Resolution.

A. Members of the board of

directors hold the institution

accountable to its mission and

social goals.

B. Senior management

oversees implementation of

the institution’s strategy for

achieving its social goals.

C. Employees are recruited,

evaluated, and recognized

based on both social and

.

page 4

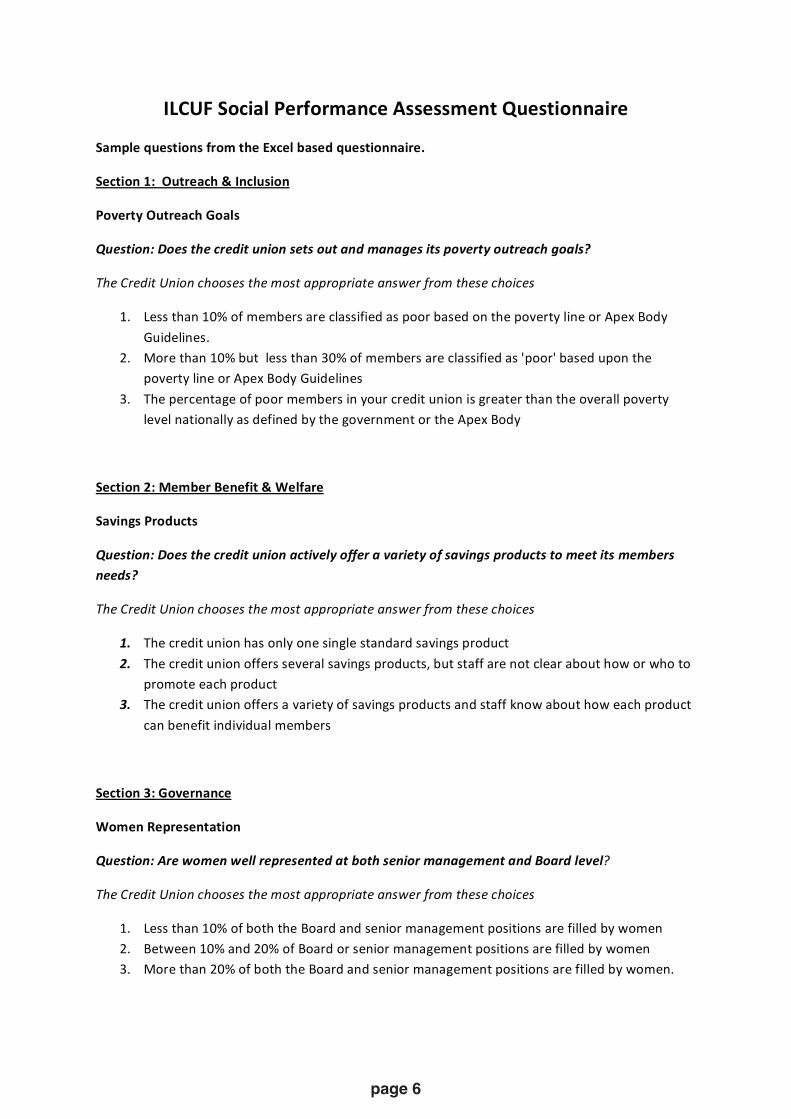

The ILCUF Social Performance Questionnaire is designed to provide a rapid assessment of a credit unions social performance. The toolraises awareness of social performance within Credit Unions and establishes a baseline for individual credit unions. This is moreimportatnt than comparing scores between different credit unions. It is important not to overstate results because the credit union'sboard will primarily be interested in progress and trends, and this will be much harder to show if very high scores are given at the start ofthe process.

There are 6 categories under many questions in each category. It is not expected that credit unions attempt to deal with all the issuesraised in a short period of time. It may choose to work on one or two issue each year.

The tool is designed as follows. A series of questions are asked spanning six key areas of credit union social performance:A Outreach & InclusionB Member Benefit & WelfareC GovernanceD Responsibility to Staff & VolunteersE Community & EnvironmentF Cooperation Amongst Cooperatives

Notes on completing the questionnaire.

1. Under each heading there are a set of questions. These are in bold and represent different themes under each heading. The personcarrying out the interview asks this question to the respondent(s).2. Several possible answers are offered for each question. The respondents select the most appropriate answer . Once they have selectedthe answer that most closely resembles the situation in their credit union (it may not be a perfect articulation of their situation), theyclick on the cell next to the statement and insert 'Yes'.3. The credit union respondent(s) is also asked to provide a comment specific to their own credit union justifying their selected answer.This should explain in a short sentance why they chose the answer they chose. The answer should be based on experience to date in thecredit union and not on plans or aspirations.4. The scores are generated automatically. It is not necessary to do anything with the other columns to the right of 'Enter CommentsJustifying your Comments' (these columns are in red). In fact, it is important not to interfere with these cells as they are programmedwith formulae and entering any data into these columns will affect the programme.

Social PerformanceAssessment Questionnaire

page 5

page 6

•

•

•

•

•

page 7

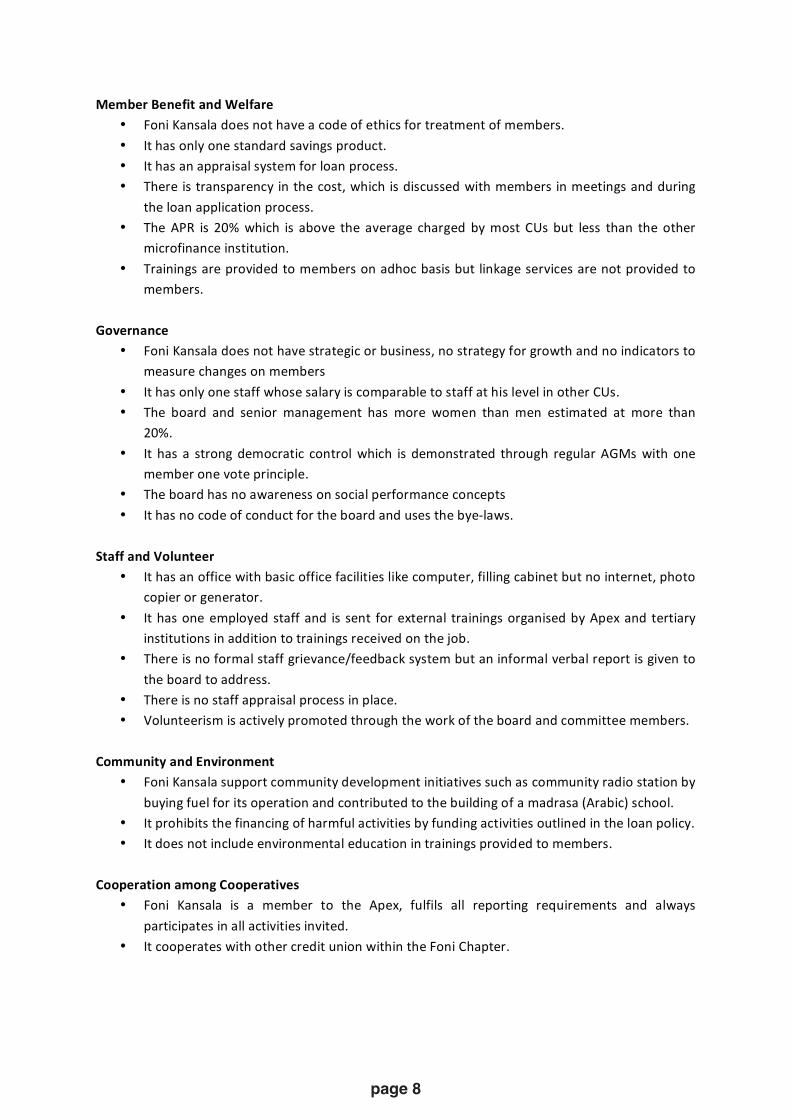

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

•

page 8

PPI Questionnaire

The Progress out of Poverty Index® (PPI®) is a poverty measurement tool for organisations and businesses with a mission to serve the poor. The PPI is statistically-sound, yet simple to use: the answers to 10 questions about a household’s characteristics and asset ownership are scored to compute the likelihood that the household is living below the poverty line – or above by only a narrow margin. With the PPI, organizations can identify the people who are most likely to be poor or vulnerable to poverty, integrating objective poverty data into their assessments and strategic decision-making.

page 9

page 10

page 11

page 12