“Innovative use of ICT by PSUs for Customer’s Benefits”

Project

Financial Inclusion@PNB

1

As per Rangarajan Committee Report

Financial Inclusion is the process of ensuring access to appropriate financial products and services needed by vulnerable groups such as weaker sections and low income groups, at an affordable cost, in a fair and transparent manner by mainstream institutional players.

2

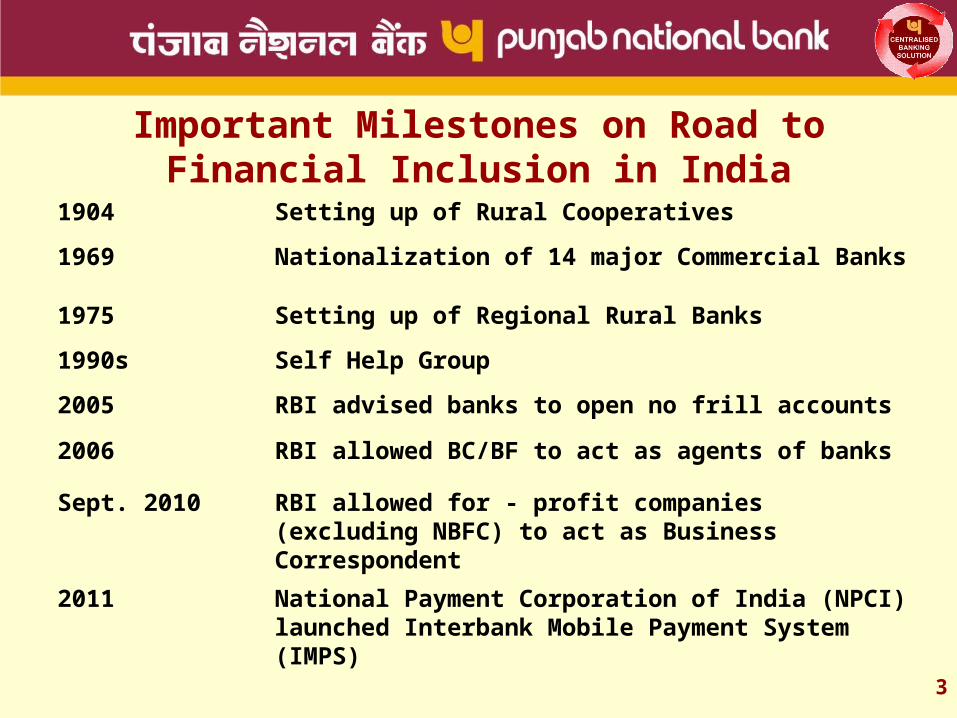

Important Milestones on Road to Financial Inclusion in India

1904 Setting up of Rural Cooperatives

1969 Nationalization of 14 major Commercial Banks

1975 Setting up of Regional Rural Banks

1990s Self Help Group

2005 RBI advised banks to open no frill accounts

2006 RBI allowed BC/BF to act as agents of banks

Sept. 2010 RBI allowed for - profit companies (excluding NBFC) to act as Business Correspondent

2011 National Payment Corporation of India (NPCI) launched Interbank Mobile Payment System (IMPS)

3

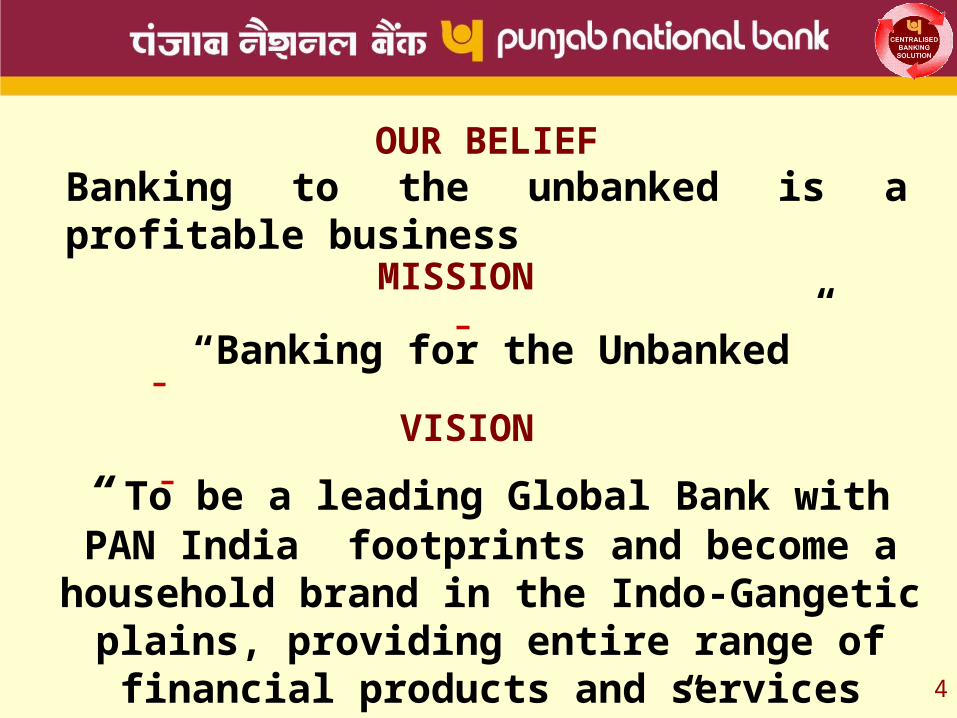

MISSION

VISION

“Banking for the Unbanked”

“ To be a leading Global Bank with PAN India footprints and become a

household brand in the Indo-Gangetic plains, providing entire range of

financial products and services under one roof ”

4

OUR BELIEFBanking to the unbanked is a profitable business

Financial Inclusion Models Adopted by the Bank

ICT (Information & Communication Technology)

Model– Base Branch acts as a focal point

for Business Correspondents (BCs)– BCs are engaged by the

Bank/technology providers– BC Agents (BCAs) contact the

customers for enrollment and issue biometric smart cards.

– BCAs use laptops and POS in Off Line mode.

– Relaxed KYC norms

5

Brick & Mortar Model - Opening PNB MITRA-No frill

accounts (Zero balance accounts) with relaxed KYC norms

- Launched PNB Mitra ATM card; withdrawal limit : upto Rs. 5,000 per day.

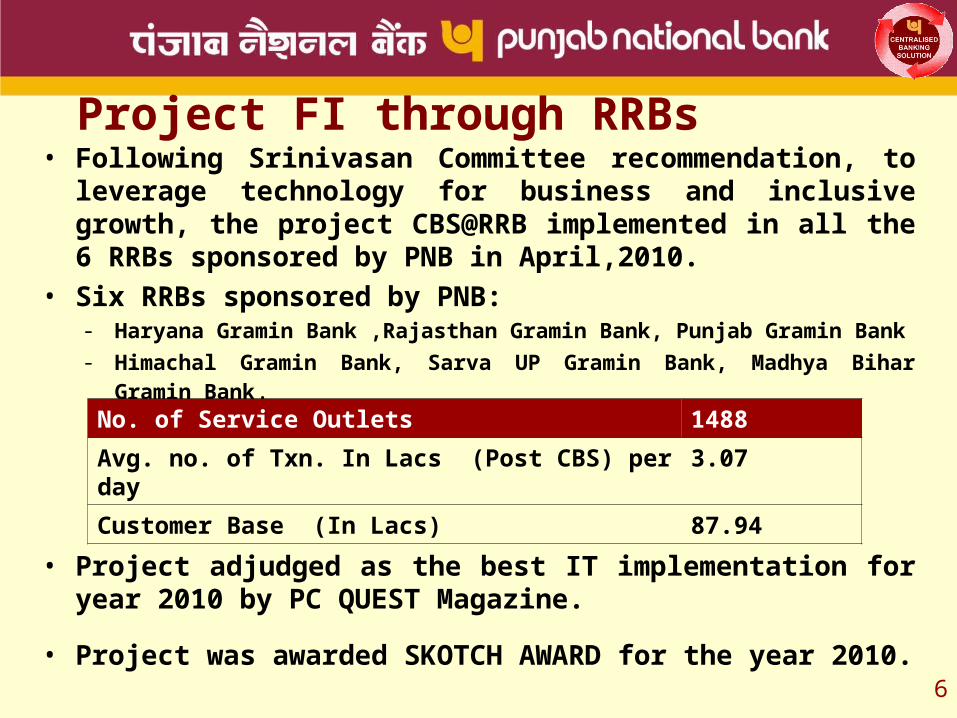

• Following Srinivasan Committee recommendation, to leverage technology for business and inclusive growth, the project CBS@RRB implemented in all the 6 RRBs sponsored by PNB in April,2010.

• Six RRBs sponsored by PNB:- Haryana Gramin Bank ,Rajasthan Gramin Bank, Punjab Gramin Bank- Himachal Gramin Bank, Sarva UP Gramin Bank, Madhya Bihar

Gramin Bank.

• Project adjudged as the best IT implementation for year 2010 by PC QUEST Magazine.

• Project was awarded SKOTCH AWARD for the year 2010.

Project FI through RRBs

6

No. of Service Outlets 1488

Avg. no. of Txn. In Lacs (Post CBS) per day

3.07

Customer Base (In Lacs) 87.94

7

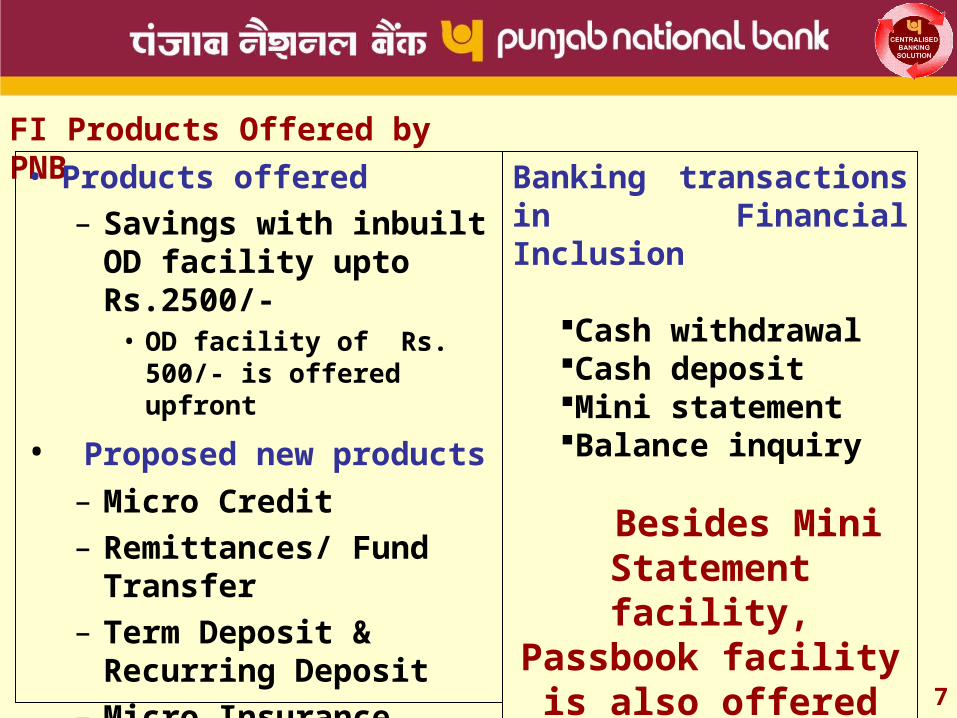

FI Products Offered by PNB • Products offered

– Savings with inbuilt OD facility upto Rs.2500/-

• OD facility of Rs. 500/- is offered upfront

• Proposed new products– Micro Credit– Remittances/ Fund

Transfer– Term Deposit &

Recurring Deposit– Micro Insurance– Micro Mutual Fund

Banking transactions in Financial Inclusion

Cash withdrawalCash depositMini statementBalance inquiry

Besides Mini Statement facility, Passbook facility is also offered to

FI customer.

Web Camera for Photograph

Biometric scanner for Fingerprints

Pad for Signature capturing

Battery Power back-up for undisrupted enrolment

Customer Enrollment Process

8

FI Intermediary server

Vendor Intermediary server

Data conversion

Back Office 1

Back Office 3

Back Office n

Back Office 2

Validation of Data

External Firewall External

Firewall

FINCBS Server at DCFINCBS Server at DC

FI Vendor

Card personalizationcentre

Card distributioncentre

ENROLLMENT PROCESS

9

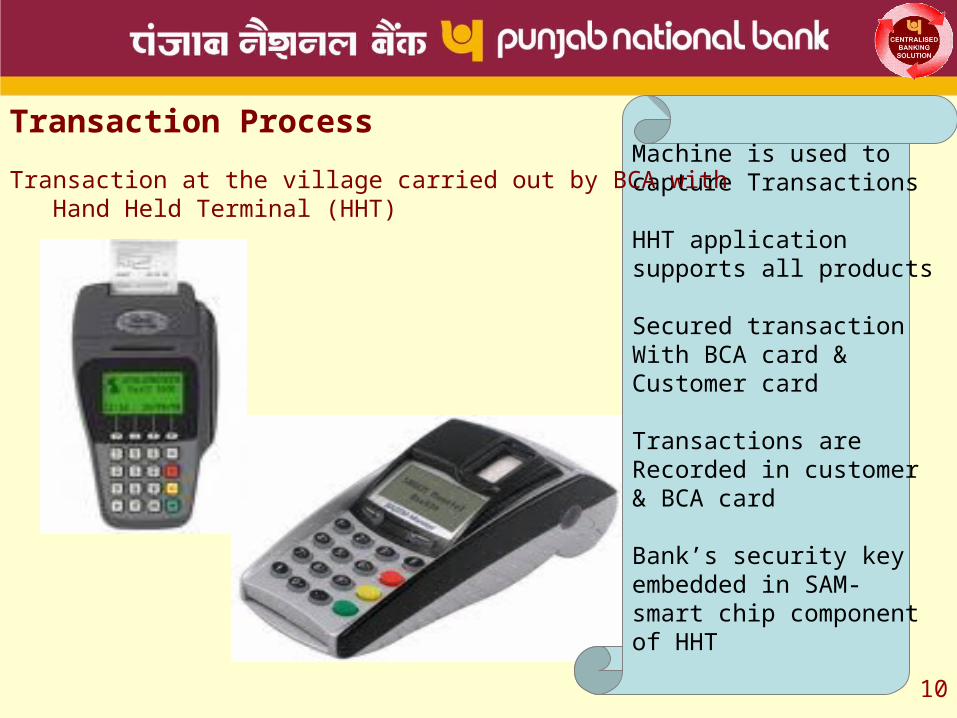

Machine is used to capture Transactions

HHT application supports all products

Secured transaction With BCA card &Customer card

Transactions are Recorded in customer& BCA card

Bank’s security key embedded in SAM-smart chip component of HHT

Transaction Process

Transaction at the village carried out by BCA with Hand Held Terminal (HHT)

10

Uniqueness of project FI @PNB

•PNB has adopted branchless banking model supported with smart card based technology.•It has independent CBS setup for FI server at data centre with DRS setup.•The management and control of whole setup is done by PNB team.•Data validation, upload and other activities are performed by exclusive FI back Offices.•The complete system is secured with symmetric key based Key Management System( owned and managed by Bank) as per IDRBT open standards for FI. •Financial transaction happens at HHT only after authentication of BC agent’s smartcard and customer’s smartcard followed by finger print authentication. •On completion of any transaction, the HHT prompts transaction amount and the resultant balance of the customer in local language

11

Uniqueness of project FI @PNB Contd.

•An instant receipt generated from the HHT is given to the customer•Data transmission is done in encrypted form.•Interoperability is achieved through use of centralized KMS facilitating the FI customers to avail banking facilities anywhere within the district/state.•Necessary Information security system and policies including Firewall system has been put in place for FI project.•FI disaster recovery site has been put in place to meet the challenge of any failure at Data centre.

12

BCP in FI (Business Continuity Plan):

•Customer Finger print fails to match

• BCA can manually perform the transaction

( override)Within the customer wise, day wise limit fixed by Bank

It is controlled through the HHT application

New smart card will be issued if the failures are

continuous

•HHT is lost before the transaction uploadCopy of the transactions are stored in BCA card

Retrieved from the BCA card and uploaded

•HHT is lost and BCA card is also lostSecond copy of the receipt with the BCA sent to FI

back office

Transaction created in FINCBS

13

BCP in FI (Business Continuity Plan) cont.•BCA fails to turn up

Alternate BCA sent to village Customer card read and the transaction retrieved Uploaded to FINCBS after validation

•Customer card lost New card is issued with the data already available with the Bank

•Weekly reconciliation between Bank’s account and BC account.

Cash management• BC maintains main account with bank

- Provides cash to each BCA within the limit- Cash held with the BCA is insured for loss and fidelity- BCA to remit the net amount and the data to Bank atleast once in

48 hours- HHT application will not permit further transaction without sync

with TSP server14

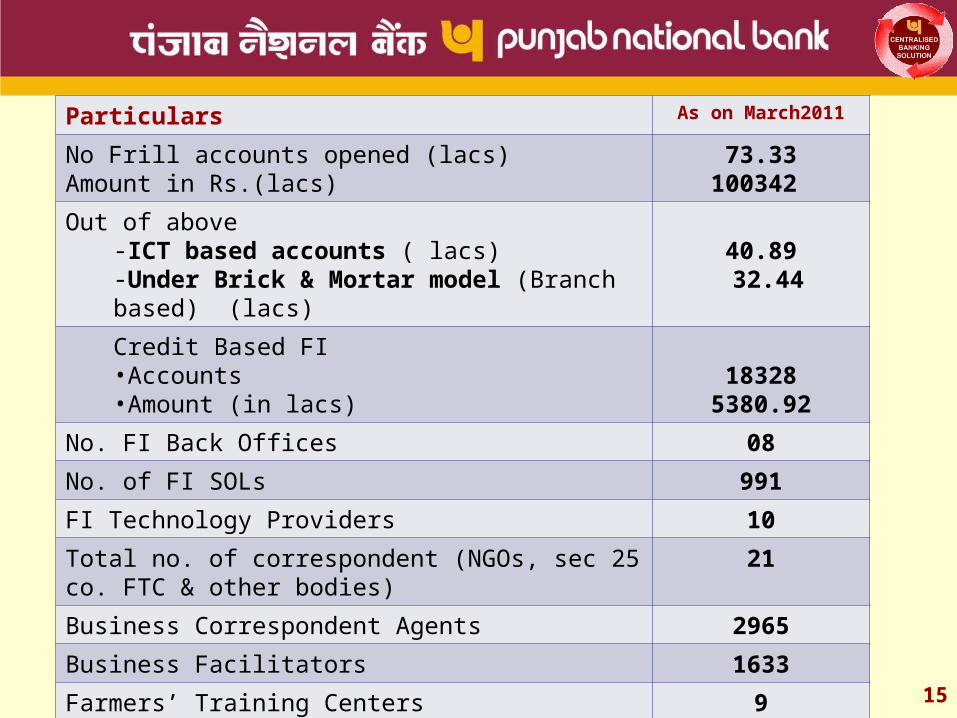

Particulars As on March2011

No Frill accounts opened (lacs)Amount in Rs.(lacs)

73.33100342

Out of above -ICT based accounts ( lacs)-Under Brick & Mortar model (Branch based) (lacs)

40.89 32.44

Credit Based FI•Accounts •Amount (in lacs)

183285380.92

No. FI Back Offices 08

No. of FI SOLs 991

FI Technology Providers 10

Total no. of correspondent (NGOs, sec 25 co. FTC & other bodies)

21

Business Correspondent Agents 2965

Business Facilitators 1633

Farmers’ Training Centers 9 15

Projects Number

States

Projects in Rural Area

28 Bihar, Rajasthan, HP, Uttarakhand, UP, Punjab, Jharkhand, MP, Orissa, West Bengal

Projects in Urban Area

06 Punjab, Delhi, J&K, Chandigarh, Bihar

NREGA/Social Security

05 AP, Haryana, UP, Chattisgarh

Total ( ICT projects)

39 14 STATES (Indo Gangetic Plain) + Andhra Pradesh

Project ‘BHAMASHAH’

01 Rajasthan

Credit Driven Projects ( Non ICT )

06 UP, Chhatisgarh, North East, Bihar , Karnataka

GRAND TOTAL 46 17 States (14 in Indo Gangetic Plain + AP, Karnataka and North East)

16

Major Financial Inclusion Projects

Reach under Financial Inclusion

17

Particulars As on March

2011Number of villages with Population > 2000 through Bank Branches (Brick & Mortar Model)

2013

Number of villages with population > 2000 through BC Model (ICT model)

2186

Number of villages with population < 2000 through BC Model (ICT model)

3219

No. of NO Frill a/cs opened in 2010-11 in villages with population over 2000.

10.09 lac

PNB’s Jana Mitra Rickshaw Project

Making Rickshaw Pullers Rickshaw Owners

•Launched in Varanasi on Feb 2, 2008 in association with Centre for Rural Development•Extended to Agra, Allahabad, Kanpur, Meerut, Lucknow, Patna•Targets to cover 10000 rickshaw pullers• 9503 Rickshaws are financed under Rickshaw Projects with outstanding credit of Rs. 9.88 Crore (as on June 2011)

18

Financing Farmers in Bulandsahar in Collaboration with Mother Dairy

•ICT Based Financial Inclusion with Credit Driven Project

•Farmers supply milk to Mother Dairy and get fair price

•No dependency on local milk vendors

•Mother Dairy pays back through the accounts (smart card based) on weekly basis

•BC agent makes payment to the farmers through smart card

•Farmers get loan for milch cattle at affordable interest rate

•More than 30000 farmers have been covered under this project

19

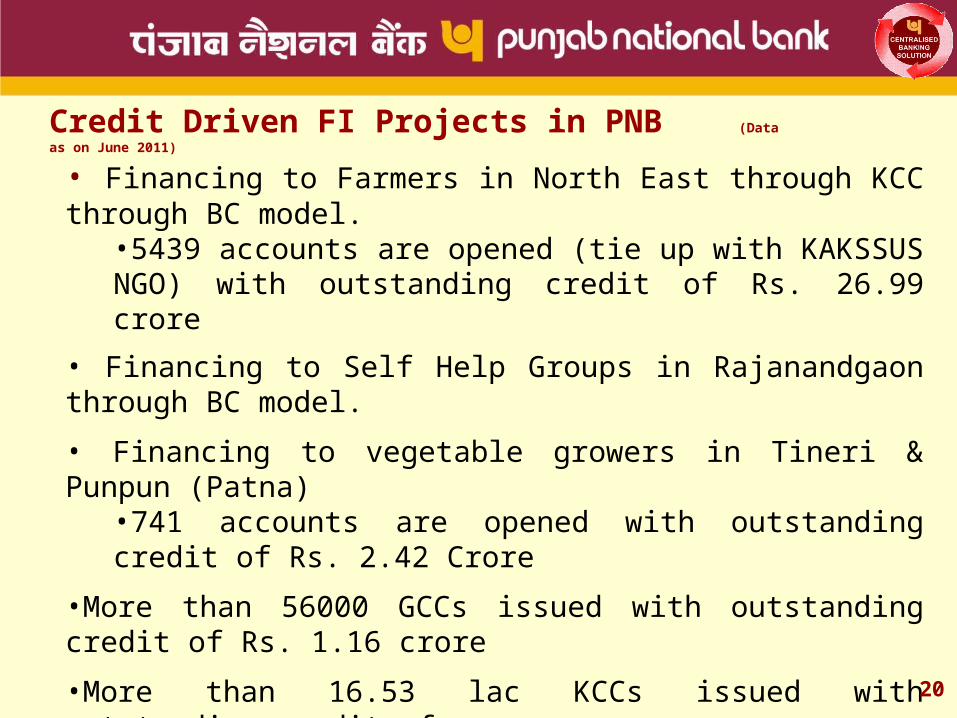

Credit Driven FI Projects in PNB (Data as on

June 2011)

• Financing to Farmers in North East through KCC through BC model.

•5439 accounts are opened (tie up with KAKSSUS NGO) with outstanding credit of Rs. 26.99 crore

• Financing to Self Help Groups in Rajanandgaon through BC model.

• Financing to vegetable growers in Tineri & Punpun (Patna)

•741 accounts are opened with outstanding credit of Rs. 2.42 Crore

•More than 56000 GCCs issued with outstanding credit of Rs. 1.16 crore

•More than 16.53 lac KCCs issued with outstanding credit of Rs. 134.46 crore

•2322 accounts are opened under Weaver’s Project, Varanasi with outstanding credit of Rs. 11.61 Crore

•190 accounts are financed to Common Service Centres with outstanding credit of Rs. 1.95 Crore

20

Capacity Building Officials of the bank have been trained under the “Train the Trainer” programme of (Indian Institute of Banking & Finance) IIBF

A. Training to BC agents•On-locations training programmes are organized for BC agents •Bank provides training on its products & processes.•Technology related training is provided by concerned TSP

B. Financial Literacy Counseling Centre (FLCC)58 FLCCs have been established for spreading Financial LiteracyRural Libraries have been setup for dissemination of Information in remote rural areas. C. 9 Farmer Training Centres (FTCs) have been established under PNB Farmers Welfare Trust to provide customized training to local farmers.

D.PNB has established 30 Rural Self Employment Training Institute (RSETI) for organizing employment generation oriented training programmes.

21

The Way Forward

22

• With the improvement of connectivity, online transaction model to be implemented.

• Web based kiosk/ mobile based model to be made available at villages

• Introduction of combo card (smart chip with magnetic stripe) to enable payments through ATMs.

• Integration with UIDAI project.

Replicability of the project FI@PNB

23

• The PNB offline FI model can be replicated to offer doorstep banking services in remote rural areas where last mile connectivity is still a challenge.

• Credit delivery through smart card model can be implemented to reach a larger section of the society.

• FI model will help in minimizing the transaction cost.

• This model can be integrated with RSBY, PDS, payment of social security benefits and wages to the MGNREGA.

•E-Governance ‘GOLD Award 2010’ under award category “Innovative use of ICT by PSUs for Customer’s Benefits” by Government of India.

•Special Technology Award for Financial Inclusion from IDRBT for the years 2008-09 & 2009-10 respectively.

•SKOTCH AWARD for the year 2010.

Third Party Assessment/Awards

24

Thanks – TEAM IT PNB

25