Download - Joint Revocable Trusts Update

Melinda Merk, Esq.Regional Trust AdvisorSunTrust BankPrivate Wealth ManagementVienna, VA

Logan Helman Winn, Esq.

Family Wealth Strategist

GenSpring Family Offices

Chevy Chase, MD

Jeannette Roegge, Esq.

Counsel

Baker Hostetler

Washington, DC

2

What are joint revocable trusts (JRTs)? Potential planning benefits and pitfalls Drafting considerations Post-mortem administrative issues

3

Single revocable trust to which a married couple transfers their assets for asset management, probate avoidance, and tax planning purposes

Most commonly used in community property states to preserve the community property character of the couple’s assets

Appealing to couples in non-community property states who are reluctant to sever/divide their jointly owned assets between separate revocable trusts for each spouse

4

Avoids probate of assets owned by the decedent/grantor (provided trust is properly funded during grantor’s lifetime)◦ Including ancillary probate of assets owned outside of

the grantor’s state of domicile Provides for ongoing management of assets in

the event of incapacity during the grantor’s lifetime

Provides for the disposition of assets at the grantor’s death, including any ongoing trusts for the benefit of the grantor’s spouse, children and/or other beneficiaries

5

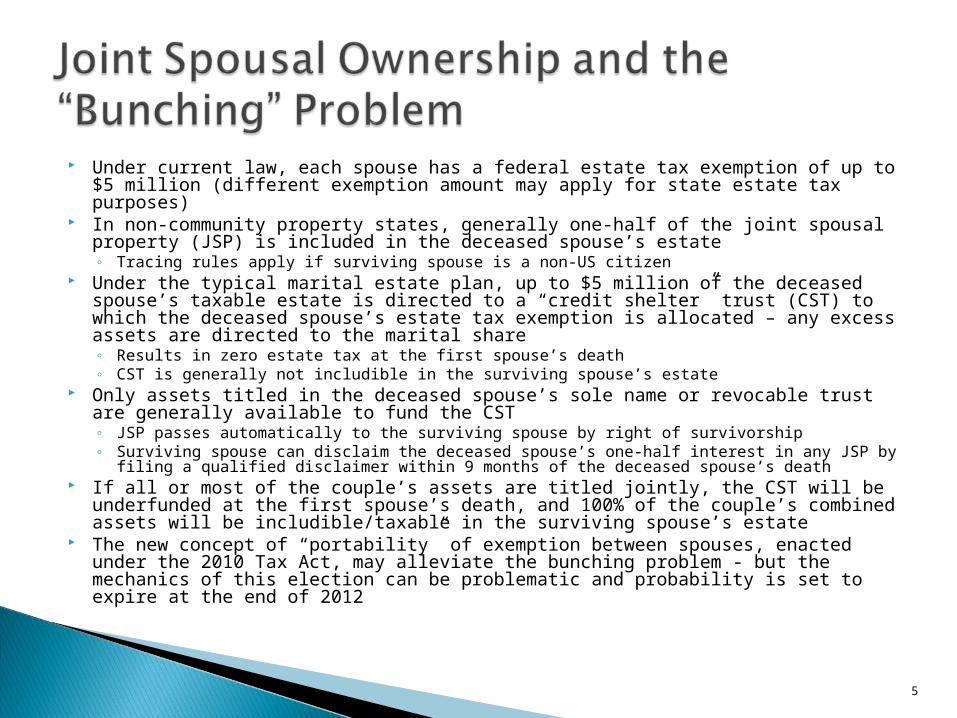

Under current law, each spouse has a federal estate tax exemption of up to $5 million (different exemption amount may apply for state estate tax purposes)

In non-community property states, generally one-half of the joint spousal property (JSP) is included in the deceased spouse’s estate◦ Tracing rules apply if surviving spouse is a non-US citizen

Under the typical marital estate plan, up to $5 million of the deceased spouse’s taxable estate is directed to a “credit shelter” trust (CST) to which the deceased spouse’s estate tax exemption is allocated – any excess assets are directed to the marital share◦ Results in zero estate tax at the first spouse’s death◦ CST is generally not includible in the surviving spouse’s estate

Only assets titled in the deceased spouse’s sole name or revocable trust are generally available to fund the CST◦ JSP passes automatically to the surviving spouse by right of survivorship◦ Surviving spouse can disclaim the deceased spouse’s one-half interest in any JSP by filing

a qualified disclaimer within 9 months of the deceased spouse’s death If all or most of the couple’s assets are titled jointly, the CST will be

underfunded at the first spouse’s death, and 100% of the couple’s combined assets will be includible/taxable in the surviving spouse’s estate

The new concept of “portability” of exemption between spouses, enacted under the 2010 Tax Act, may alleviate the bunching problem - but the mechanics of this election can be problematic and probability is set to expire at the end of 2012

6

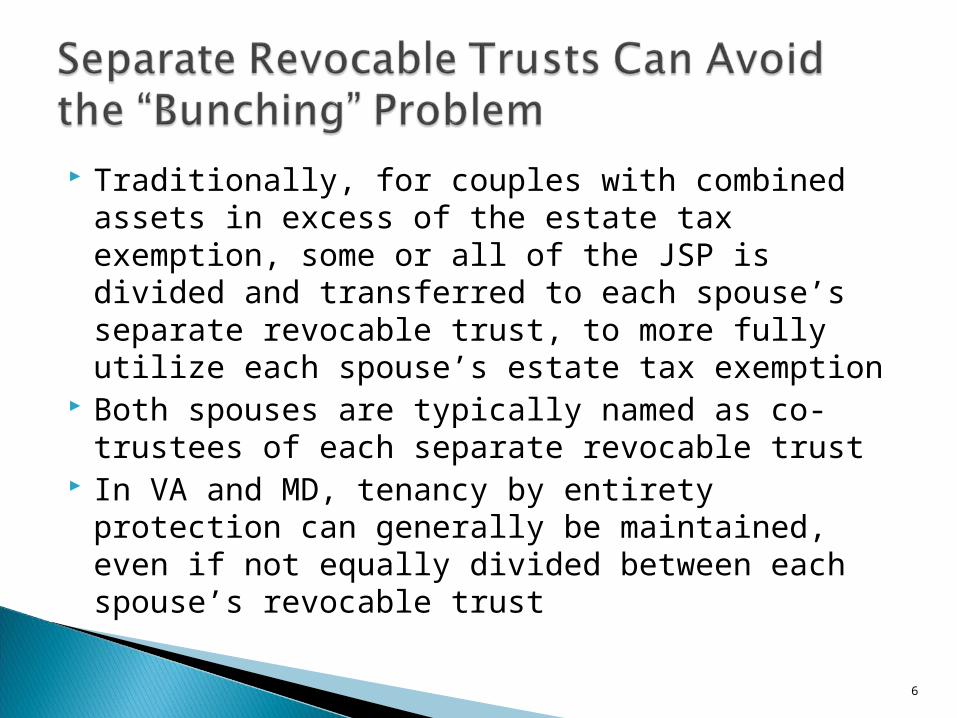

Traditionally, for couples with combined assets in excess of the estate tax exemption, some or all of the JSP is divided and transferred to each spouse’s separate revocable trust, to more fully utilize each spouse’s estate tax exemption

Both spouses are typically named as co-trustees of each separate revocable trust

In VA and MD, tenancy by entirety protection can generally be maintained, even if not equally divided between each spouse’s revocable trust

7

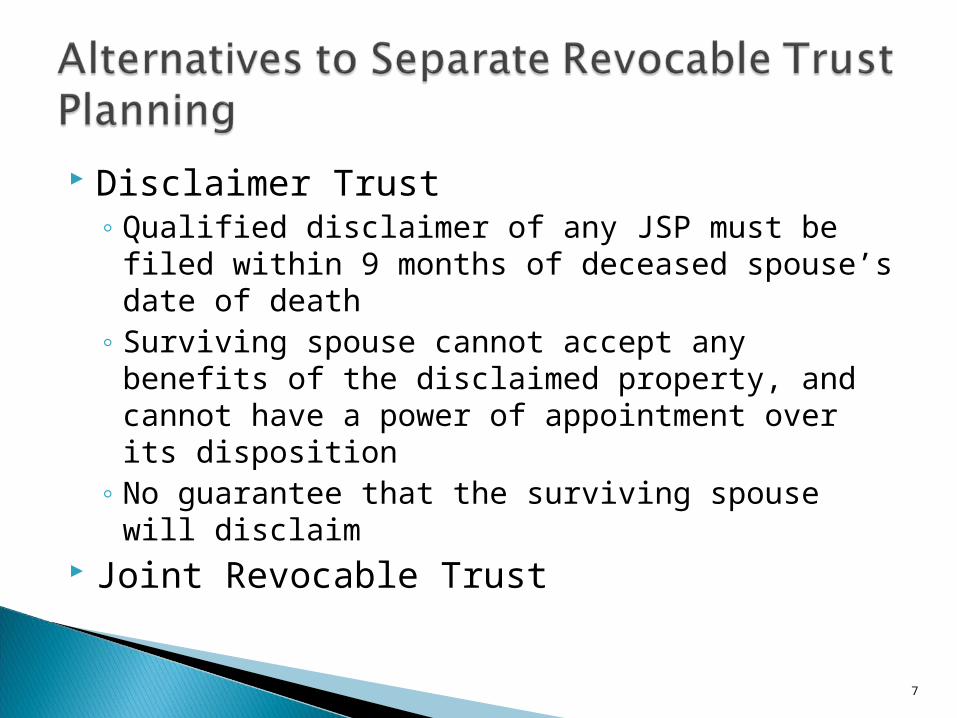

Disclaimer Trust◦ Qualified disclaimer of any JSP must be filed

within 9 months of deceased spouse’s date of death

◦ Surviving spouse cannot accept any benefits of the disclaimed property, and cannot have a power of appointment over its disposition

◦ No guarantee that the surviving spouse will disclaim

Joint Revocable Trust

8

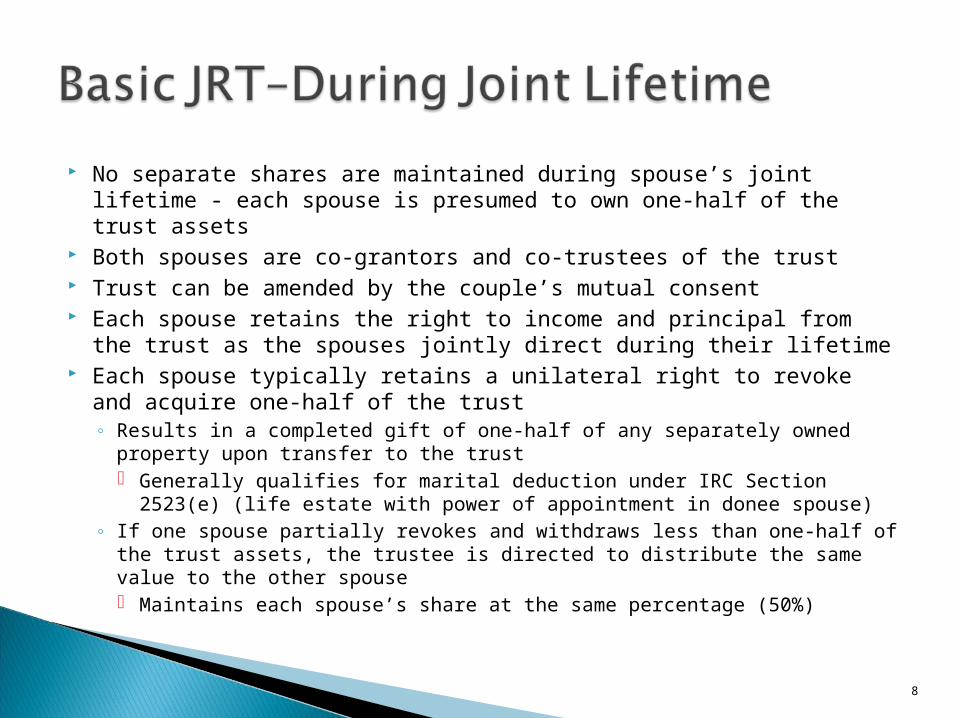

No separate shares are maintained during spouse’s joint lifetime - each spouse is presumed to own one-half of the trust assets

Both spouses are co-grantors and co-trustees of the trust Trust can be amended by the couple’s mutual consent Each spouse retains the right to income and principal from the

trust as the spouses jointly direct during their lifetime Each spouse typically retains a unilateral right to revoke and

acquire one-half of the trust◦ Results in a completed gift of one-half of any separately owned property

upon transfer to the trust Generally qualifies for marital deduction under IRC Section 2523(e)

(life estate with power of appointment in donee spouse)◦ If one spouse partially revokes and withdraws less than one-half of the

trust assets, the trustee is directed to distribute the same value to the other spouse Maintains each spouse’s share at the same percentage (50%)

9

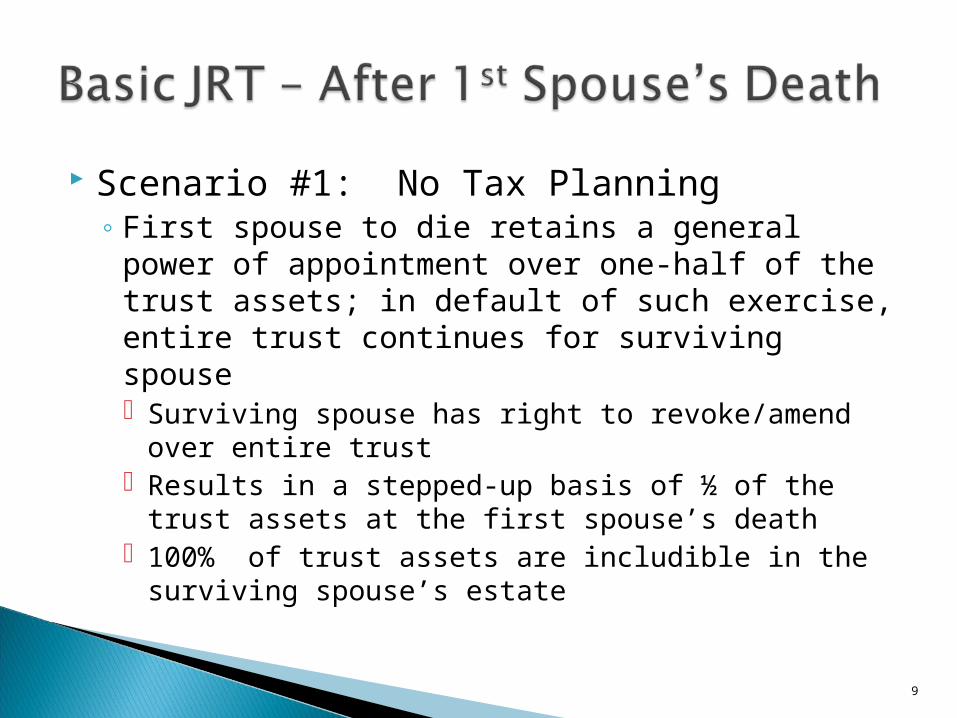

Scenario #1: No Tax Planning◦ First spouse to die retains a general power of

appointment over one-half of the trust assets; in default of such exercise, entire trust continues for surviving spouse Surviving spouse has right to revoke/amend over

entire trust Results in a stepped-up basis of ½ of the trust assets

at the first spouse’s death 100% of trust assets are includible in the surviving

spouse’s estate

10

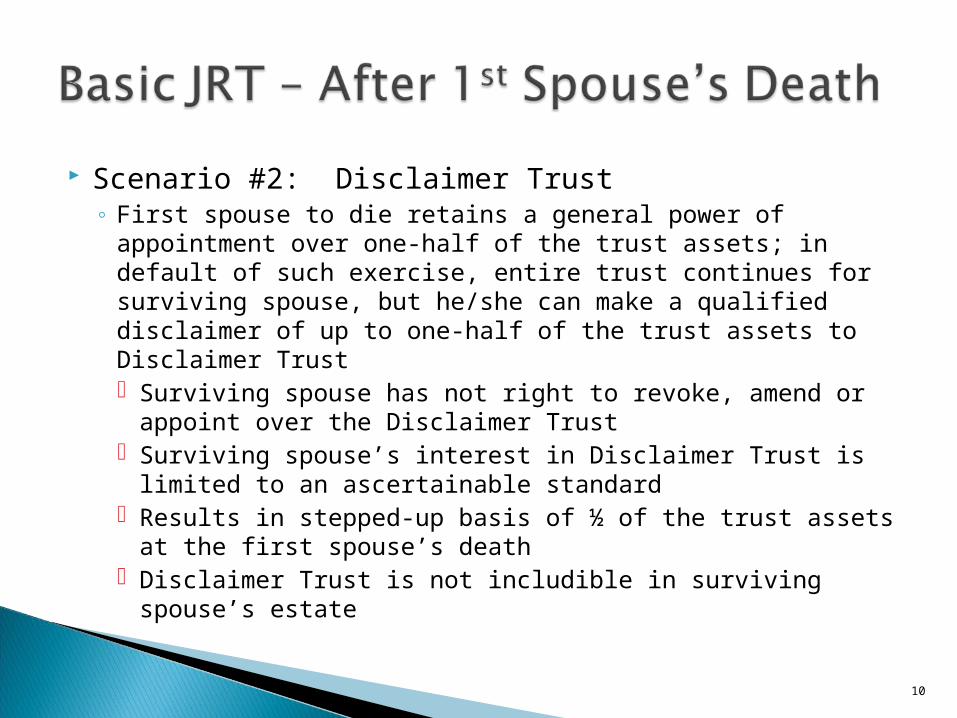

Scenario #2: Disclaimer Trust◦ First spouse to die retains a general power of appointment

over one-half of the trust assets; in default of such exercise, entire trust continues for surviving spouse, but he/she can make a qualified disclaimer of up to one-half of the trust assets to Disclaimer Trust Surviving spouse has not right to revoke, amend or

appoint over the Disclaimer Trust Surviving spouse’s interest in Disclaimer Trust is limited

to an ascertainable standard Results in stepped-up basis of ½ of the trust assets at the

first spouse’s death Disclaimer Trust is not includible in surviving spouse’s

estate

11

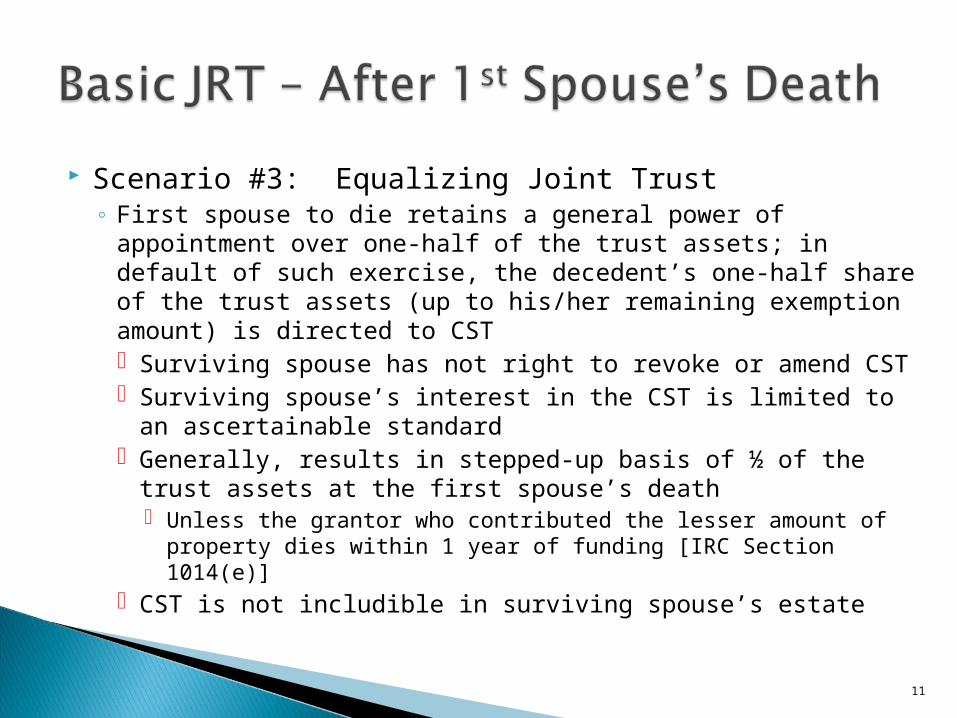

Scenario #3: Equalizing Joint Trust◦ First spouse to die retains a general power of appointment

over one-half of the trust assets; in default of such exercise, the decedent’s one-half share of the trust assets (up to his/her remaining exemption amount) is directed to CST Surviving spouse has not right to revoke or amend CST Surviving spouse’s interest in the CST is limited to an

ascertainable standard Generally, results in stepped-up basis of ½ of the trust

assets at the first spouse’s death Unless the grantor who contributed the lesser amount of

property dies within 1 year of funding [IRC Section 1014(e)] CST is not includible in surviving spouse’s estate

12

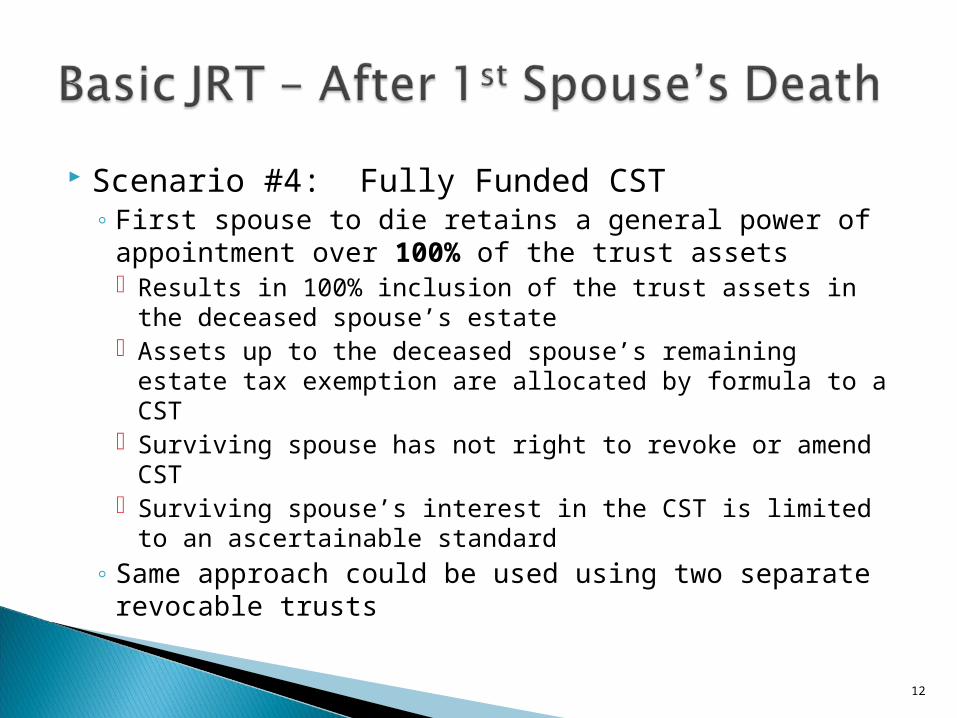

Scenario #4: Fully Funded CST◦ First spouse to die retains a general power of

appointment over 100% of the trust assets Results in 100% inclusion of the trust assets in the

deceased spouse’s estate Assets up to the deceased spouse’s remaining estate

tax exemption are allocated by formula to a CST Surviving spouse has not right to revoke or amend CST Surviving spouse’s interest in the CST is limited to an

ascertainable standard◦ Same approach could be used using two separate

revocable trusts

13

Scenario #4: Fully Funded CST (cont’d)◦ IRS has denied full basis adjustment under IRC Section

1014(e), based on position that the deceased spouse acquired the survivor’s contribution by gift at his/her death, and the survivor then simultaneously reacquired such property from the decedent See PLRs 2001-01-021 and 2002-10-051 Stepped-up basis is only available for the trust assets

allocable to deceased spouse’s contribution to the trust Hard to determine if separate property/unequal contributions

are made to the trust, and separate shares are not maintained

◦ 1st spouse to die is considered the transferor of 100% of the trust assets – as a result, the above rulings held that CST assets were not includible in surviving spouse’s estate

14

Separate shares/schedules are maintained for joint property and for any separate property transferred to the trust

Both spouses are co-grantors and co-trustees of the trust Trust can be amended by the couple’s mutual consent Each spouse retains the right to income and principal from

the joint property, as well as from his or her share of separate property

Each spouse typically retains a unilateral right to revoke and acquire one-half of the joint property, as well as her or her respective share of separate property◦ Renders any interspousal gift of separate property incomplete for gift

tax purposes, so long as separate shares are maintained

15

JRT is typically divided into “Survivor’s Trust” and “Exemption Trust”◦ Survivor’s Trust consists of the surviving spouse’s one-half

interest in the joint property, as well as his or her separate property

◦ Exemption Trust consists of the deceased spouse’s one-half interest in the joint property, as well as his or her separate property – up to the decedent’s remaining exemption amount Any amount in excess of the exemption amount is directed to

the Survivor’s (Marital) Trust Either entire trust becomes irrevocable, or surviving spouse

retains right to revoke/amend Survivor’s Trust only Typical credit shelter and marital trust provisions apply to

each respective share

16

Why do clients (and attorneys) like JRTs?◦ Married couples generally believe their assets are owned

by both spouses (they may object to dividing them to fund two separate revocable trusts) Suggestion: make the spouses co-trustees of the two separate

revocable trusts

◦ Preservation of community property under applicable state law (important for step-up in basis issues)

◦ Some practitioners believe that a JRT is simpler to draft and administer because it’s easier to contribute assets (don’t have to split assets and then contribute to fund two separate revocable trusts) Issue: only true if there is no estate tax planning, because JRTs require

detailed and careful accountings of each spouse’s contributions to avoid adverse tax consequences

17

When to use a JRT?◦ Community Property Clients w/Existing Joint Trusts

Clients have an existing JRT from a community property state

Current Community Property States: Alaska (optional), Arizona, California, Idaho, Louisiana,

Nevada, New Mexico, Texas, Washington, and Wisconsin (and Puerto Rico)

18

Community Property ◦ Generally, property acquired by spouses during their marriage while

domiciled in a community property state is deemed to have been acquired by both equally regardless of which spouse actually contributed the property

◦ Each spouse owns a one-half interest in all such property, regardless of title

Separate Property (in Community Property Jurisdictions)◦ Property acquired before the marriage◦ Property acquired by gift, bequest, devise, or descent◦ Property acquired as separate property while domiciled in a separate

property state remains separate◦ Property bought with, or exchanged for, separate property remains

separate property◦ Property converted from community property through a valid agreement

(transmutation agreement) becomes separate property

19

Community Property at Death ◦ One-half of the value of community property owned by a

married couple is includable in the estate of the deceased spouse for estate tax purposes

◦ However, the value of both spouses' shares of the property is stepped up or down to fair market value at the death of the first spouse An alternate valuation date, six months after the deceased spouse's

death, may also be used

20

The Mobile Community Property Client◦ Uniform Disposition of Community Property Rights at Death Act

(UDCPRDA) Adopted by Alaska, Arkansas, Colorado, Connecticut, Florida, Hawaii,

Kentucky, Michigan, Montana, New York, North Carolina, Oregon, Virginia, and Wyoming

Applies to personal property, wherever situated, that is community property under the laws of a state, as well as to personal property that is traceable to community property

Applies to real property located in the state adopting the UDCPRDA that was acquired with the “rents, issues or income of, or the proceeds from, or in exchange for” community property

21

The Mobile Community Property Client ◦ Community Property Removed to Common Law

Jurisdiction Presumes that property acquired during marriage while the

spouses were domiciled in a community property jurisdiction is community property

Further, personal property generally retains its status (community or separate) regardless of where the spouses move (unless assets are commingled and cannot be traced)

i.e., If spouses acquire property and earn income in a community property state, and then move to a separate property state, the property and income already acquired retains its community property status

22

The Mobile Community Property Client ◦ Existing Joint Revocable Trust

Recent client example: Elder clients moved from New Mexico to Washington, D.C. All of their property is community property and titled in the name of their joint revocable trust. After careful consideration, decided not to sever the trust into separate revocable trusts, in order to not taint any of community property and to maintain the ability to step up the basis of all assets at the first spouse’s death.

23

Trust Funding◦ Clearly define shares of JRT assets (for tracing and

funding purposes) – Example: Share A – H’s separate property Share B – W’s separate property Share C – Community property Share D – Joint property (other than community property (i.e.,

was separate property, but spouses intend to be joint)

24

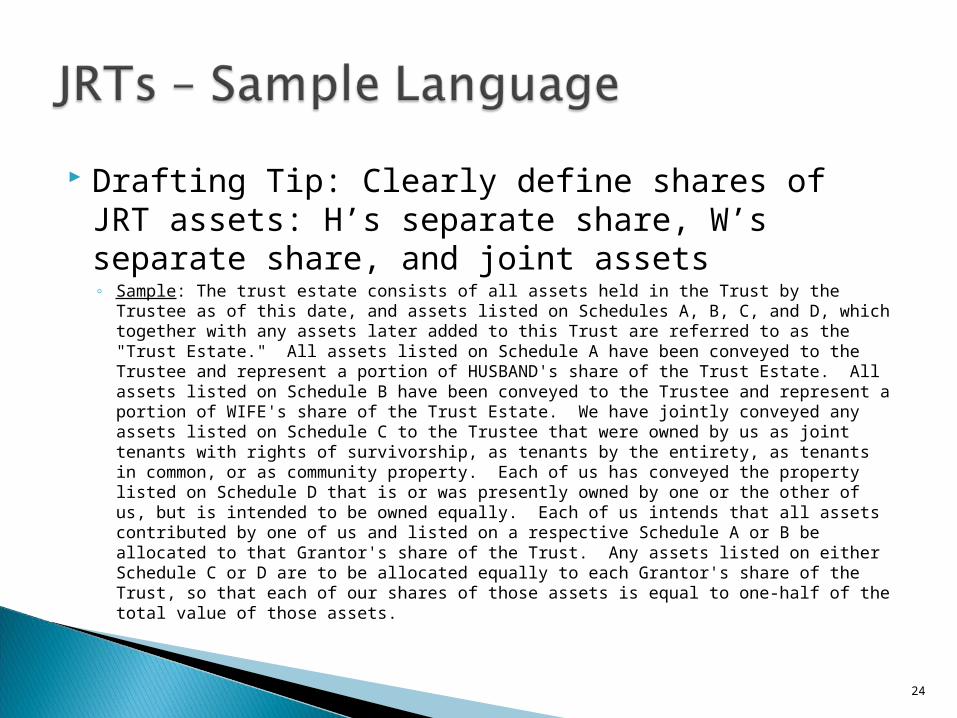

Drafting Tip: Clearly define shares of JRT assets: H’s separate share, W’s separate share, and joint assets◦ Sample: The trust estate consists of all assets held in the Trust by the Trustee as of

this date, and assets listed on Schedules A, B, C, and D, which together with any assets later added to this Trust are referred to as the "Trust Estate." All assets listed on Schedule A have been conveyed to the Trustee and represent a portion of HUSBAND's share of the Trust Estate. All assets listed on Schedule B have been conveyed to the Trustee and represent a portion of WIFE's share of the Trust Estate. We have jointly conveyed any assets listed on Schedule C to the Trustee that were owned by us as joint tenants with rights of survivorship, as tenants by the entirety, as tenants in common, or as community property. Each of us has conveyed the property listed on Schedule D that is or was presently owned by one or the other of us, but is intended to be owned equally. Each of us intends that all assets contributed by one of us and listed on a respective Schedule A or B be allocated to that Grantor's share of the Trust. Any assets listed on either Schedule C or D are to be allocated equally to each Grantor's share of the Trust, so that each of our shares of those assets is equal to one-half of the total value of those assets.

25

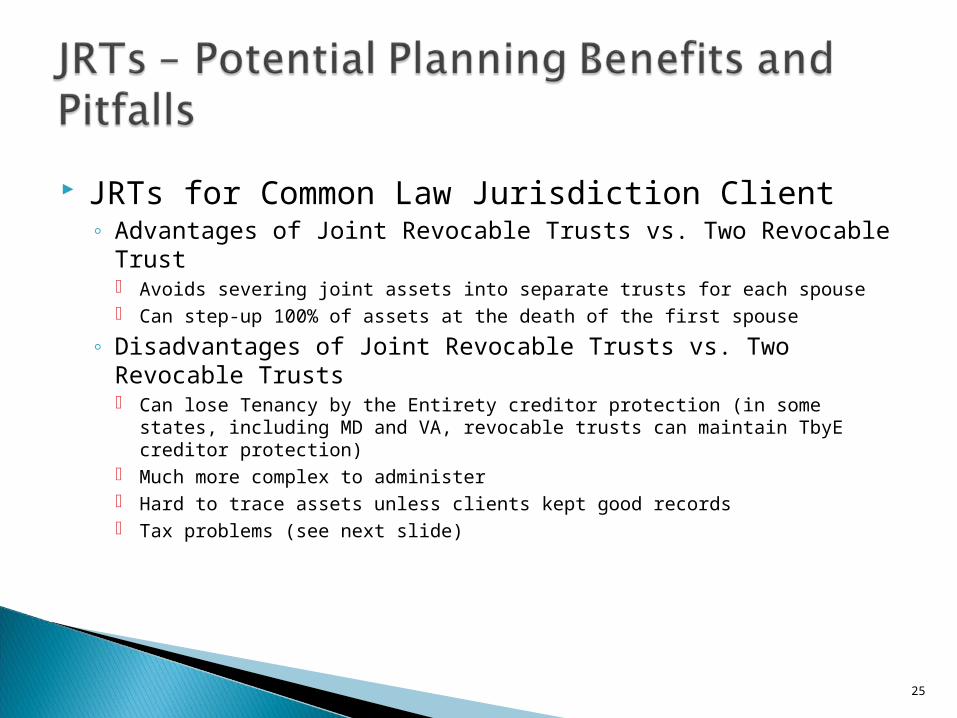

JRTs for Common Law Jurisdiction Client ◦ Advantages of Joint Revocable Trusts vs. Two Revocable Trust

Avoids severing joint assets into separate trusts for each spouse Can step-up 100% of assets at the death of the first spouse

◦ Disadvantages of Joint Revocable Trusts vs. Two Revocable Trusts Can lose Tenancy by the Entirety creditor protection (in some states, including

MD and VA, revocable trusts can maintain TbyE creditor protection) Much more complex to administer Hard to trace assets unless clients kept good records Tax problems (see next slide)

26

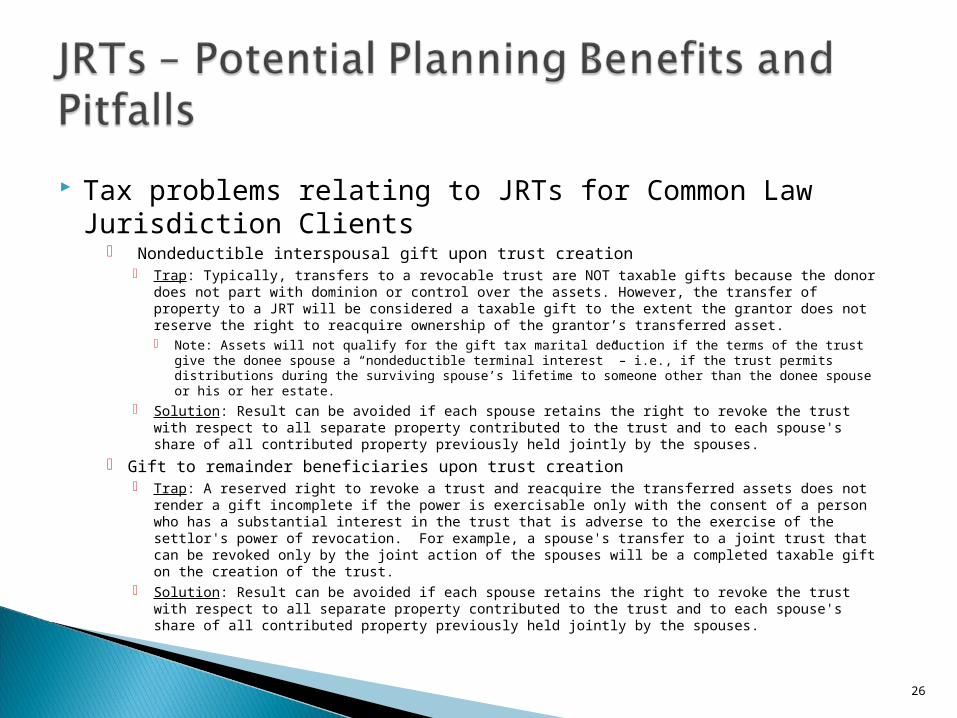

Tax problems relating to JRTs for Common Law Jurisdiction Clients

Nondeductible interspousal gift upon trust creation Trap: Typically, transfers to a revocable trust are NOT taxable gifts because the donor does not

part with dominion or control over the assets. However, the transfer of property to a JRT will be considered a taxable gift to the extent the grantor does not reserve the right to reacquire ownership of the grantor’s transferred asset. Note: Assets will not qualify for the gift tax marital deduction if the terms of the trust give the donee

spouse a “nondeductible terminal interest” – i.e., if the trust permits distributions during the surviving spouse’s lifetime to someone other than the donee spouse or his or her estate.

Solution: Result can be avoided if each spouse retains the right to revoke the trust with respect to all separate property contributed to the trust and to each spouse's share of all contributed property previously held jointly by the spouses.

Gift to remainder beneficiaries upon trust creation Trap: A reserved right to revoke a trust and reacquire the transferred assets does not render a

gift incomplete if the power is exercisable only with the consent of a person who has a substantial interest in the trust that is adverse to the exercise of the settlor's power of revocation. For example, a spouse's transfer to a joint trust that can be revoked only by the joint action of the spouses will be a completed taxable gift on the creation of the trust.

Solution: Result can be avoided if each spouse retains the right to revoke the trust with respect to all separate property contributed to the trust and to each spouse's share of all contributed property previously held jointly by the spouses.

27

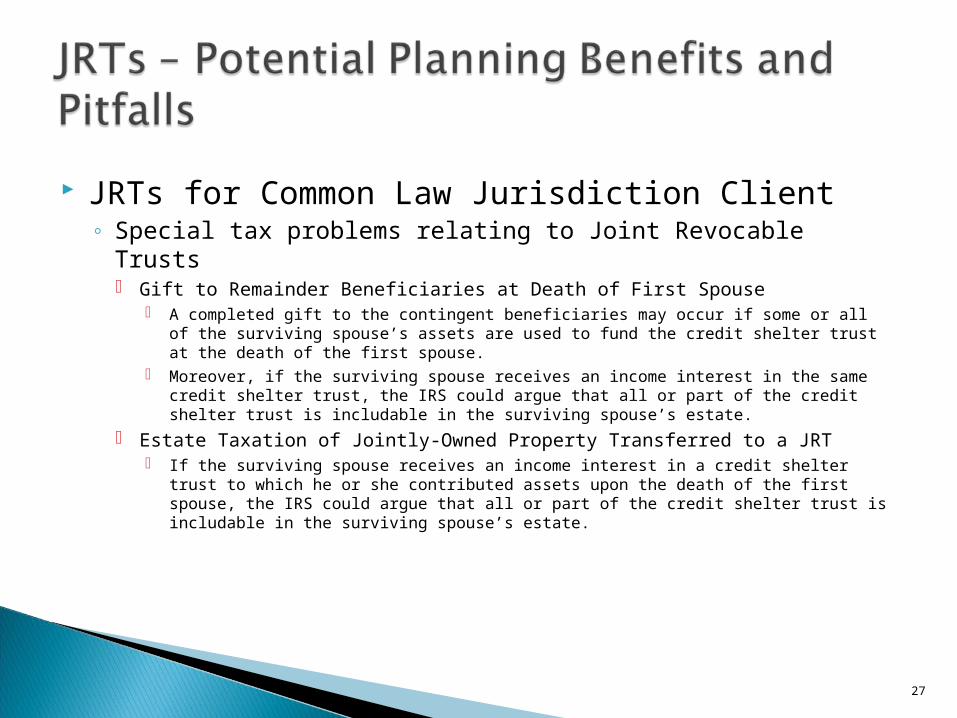

JRTs for Common Law Jurisdiction Client ◦ Special tax problems relating to Joint Revocable Trusts

Gift to Remainder Beneficiaries at Death of First Spouse A completed gift to the contingent beneficiaries may occur if some or all of the surviving

spouse’s assets are used to fund the credit shelter trust at the death of the first spouse. Moreover, if the surviving spouse receives an income interest in the same credit shelter

trust, the IRS could argue that all or part of the credit shelter trust is includable in the surviving spouse’s estate.

Estate Taxation of Jointly-Owned Property Transferred to a JRT If the surviving spouse receives an income interest in a credit shelter trust to which he or

she contributed assets upon the death of the first spouse, the IRS could argue that all or part of the credit shelter trust is includable in the surviving spouse’s estate.

28

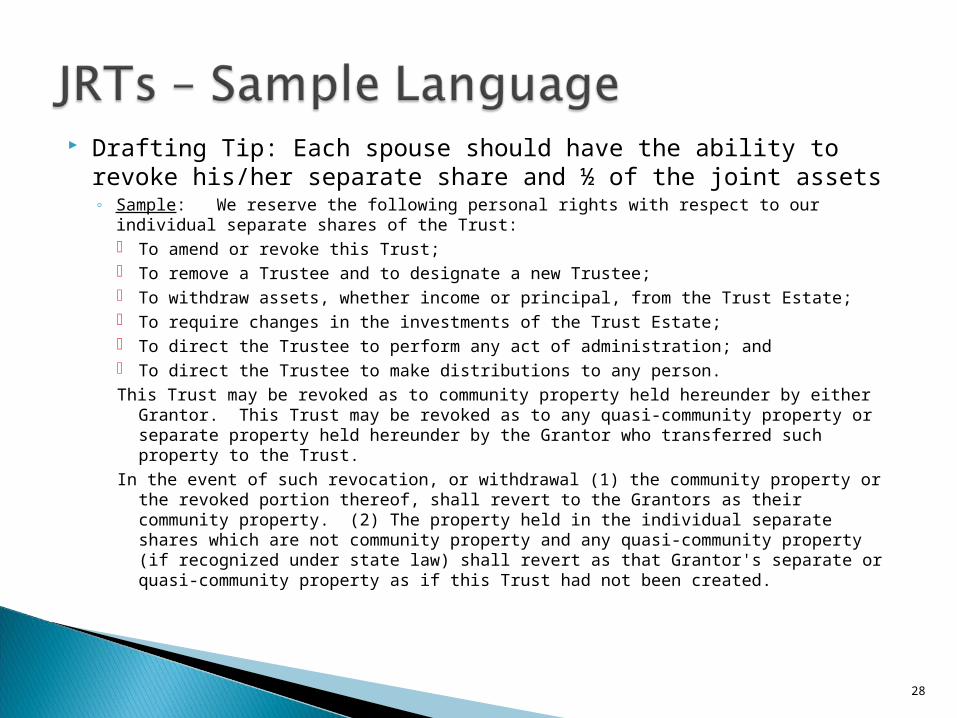

Drafting Tip: Each spouse should have the ability to revoke his/her separate share and ½ of the joint assets◦ Sample: We reserve the following personal rights with respect to our individual

separate shares of the Trust: To amend or revoke this Trust; To remove a Trustee and to designate a new Trustee; To withdraw assets, whether income or principal, from the Trust Estate; To require changes in the investments of the Trust Estate; To direct the Trustee to perform any act of administration; and To direct the Trustee to make distributions to any person.This Trust may be revoked as to community property held hereunder by either Grantor.

This Trust may be revoked as to any quasi-community property or separate property held hereunder by the Grantor who transferred such property to the Trust.

In the event of such revocation, or withdrawal (1) the community property or the revoked portion thereof, shall revert to the Grantors as their community property. (2) The property held in the individual separate shares which are not community property and any quasi-community property (if recognized under state law) shall revert as that Grantor's separate or quasi-community property as if this Trust had not been created.

29

When is it NOT necessarily appropriate to use a JRT?◦ Client has existing JRT from a non-community property

state (i.e., client does NOT have any community property)◦ What to do:

Sever the JRT into two separate revocable trusts Sever client’s assets between two separate revocable trusts

30

Drafting Tip: Clearly define property character of JRT assets◦ Sample: It is the Grantors’ intention that all community property transferred to the

Trust Estate and the proceeds thereof shall retain their character as community property during the joint lifetime of the Grantors subject, however, to all the terms and conditions of this instrument. Similarly, it is the Grantors’ intention that quasi-community (if recognized under state law) and separate property of the Grantors and the proceeds thereof which may hereafter become part of this Trust shall also retain their character during the joint lifetime of the Grantors subject also to all the terms and conditions of this Trust agreement. It is the Grantors’ intention that the Trustee shall have no more extensive power over any community property transferred to the Trust Estate than either of the Grantors would have had under law, had this Trust not been created, and this instrument shall be so interpreted to achieve this intention. This limitation shall terminate on the death of either Grantor.

31

What happens to the assets held in the JRT after the death of the first spouse to die (the “Decedent”)?◦ Look closely at the actual terms of the JRT and the schedules to

the JRT ◦ Typically see 2 scenarios: separate shares or one-half JRT

property◦ Decedent’s Share and Survivor’s Share (1/2 all trust property OR

½ joint property and all Decedent’s separate property)◦ Separate the Survivor’s Share as soon as possible but it make

time to determine such share◦ Although disposition terms for Decedent’s Share may be

familiar (credit shelter trust, marital share), determining Decedent’s Share may be more difficult

◦ • Be prepared to do some forensic work to determine title of assets upon contribution to the trust

32

What trust assets are included in the Decedent’s taxable estate?◦ Look at the powers retained by the Decedent during lifetime

(power to revoke and general power of appointment (“GPOA”) over all trust assets)

◦ The power to revoke during results in inclusion of assets over which Decedent had the power under Section 2038

◦ GPOA over assets at death results in inclusion under §2041◦ GPOA purposely included to trigger inclusion of all assets in

JRT to fully fund credit shelter ◦ There are PLRs which support the GPOA intended result, BUT

you don’t get step up [Section 1014(e)] for Surviving Spouse’s Assets in credit shelter

◦ There is a risk that the IRS’ position could change

33

Other Practical Administrative Concerns◦ Don’t trust Survivor’s recollection of title of assets!!

Check title and ownership at time of contribution early on◦ Fiduciary Returns--Section 645 election is available◦ Get tax ID for Decedent’s Share of trust during

administration ◦ There may be a probate estate◦ Very important to bring the accountant into the process

early so that fiduciary returns and accountings are not overwhelming

◦ Basis issues? There may not be a full step up for assets in Credit Shelter Trust because of Section 1014(e)

34

Consider Having Survivor Restate His or Her Share of JRT ◦ Clean up trust instrument◦ Can do it as a restatement of Survivor’s Share

instead of a revocation◦ May need to revise designations on accounts◦ Make sure surviving spouse’s SSN is on the

accounts

35

Additional resources◦ “Joint Revocable Trusts for Married Couples

Domiciled in Common Law Property States,” Melinda Merk, 32 Real Property, Probate and Trust Journal (Summer 1997)

◦ “The Joint Trust: Estate Planning in a New Environment,” John H. Martin, 39 Real Property, Probate and Trust Journal (Summer 2004)

Questions?