GROWTH BY COMBINING BEST PRACTICES

L. Lovaglio

General Manager at Bank Pekao

2

AGENDA

Poland macroeconomic and banking sector scenario

The creation of New Pekao

New Pekao strategic initiatives

Strategy for Ukraine

Closing remarks

3Source: UniCredit-NE Research Network(1) CEE 16 aggregate includes PL, HU, CZ, SK, SI, EE, LV,LIT, HR, BG, RO, TK, RU, Serbia, BiH

and UA

BIGGEST NEW EU MEMBER WITH STRONG ECONOMIC GROWTH DRIVEN BY INVESTMENTS AND CONSUMPTION

GDP per capitaEUR ths

Investment growth (29% Y/Y)FDI standing for 4.4% of GDP in 2006EU funds earmarked for Poland in 2007-2013 reaching 67 EUR bn

Personal consumptionRapidly decreasing unemployment rate (from 18.2% in 05.2005 to 13.0% in 05.2007)Dynamically growing wages (10% increase in 2007 expected)

EURO 2012 triggering further acceleration in investment

... driven by:

Poland

Eurozone

Strong GDP growth

5.4

4.7

2.1

1.42003-06

2007F-09F

GDP avg. growth%

New EU MembersPoland

GDP per capita below EU average

Good risk profile:A-/Stable by S&P;

A2/Stable by Moody’s

Biggest New EU Member

Population

7.15.2

27.7

PolandEU 15 CEE 16(1)

62% 38%

4

LOW BANKING PENETRATION DRIVING FUTURE GROWTH – RETAIL TO DELIVER MOST OPPORTUNITIES

+x% CAGR ’06-’09Note: Data provided by CEE Division Macroeconomic Department

Banking penetration

EurozonePoland

Retail banking

Corporate banking

+22%

SAVINGSLOANS

Total volume EUR bn

Total volume EUR bn

11%

Mutual FundsDeposits

Total volume EUR bn

Total volume EUR bn

DEPOSITSLOANS

+12%

Strong growth of asset managementIncreasing demand forconsumer and mortgageloansBoost in SME lendingHigh demand for e-bankingsolutions

Further development of cash management and FX transactionsIncreasing role of capital market in corporate financing (eg. Syndicated loans)

2006 figures

90

49

2006 2009

2541

66

123

2006

82

2009

91

4533

2006 2009

5137

20092006

97

6838

AuM/GDPMortgage/GDP

4134

96119

Deposits/GDP

Loans/GDP

+11%

5

AGENDA

Poland macroeconomic and banking sector scenario

The creation of New Pekao

New Pekao strategic initiatives

Strategy for Ukraine

Closing remarks

6

BPH SPIN-OFF STRONGLY CONTRIBUTING TO THE NEW PEKAO

SPIN-OFF ASSETS TO BE MERGED WITH PEKAO

Corporate business with customers

Corporate

TreasuryOnly limited ALM and Treasury functions to maximize synergies generation

IT and Operations supportOperational systems and staff selected across divisions to ensure functioning of both new Pekao and new BPH without any disruption to customersLimited cost of restructuring required after the merge

PROCESS RUN BY ESTABLISHED MANAGEMENT TEAM

Retail285 retail branches, with employees and customersNo need to close overlapping branches after the deal~350 partner agencies

Part of BPH to be merged with Pekao

7

INTEGRATION ON TRACK, WITH SUCCESSFUL ACHIEVEMENTS

Management structure and senior team defined combining key talents

Refined business model leveraging best practices

Enhanced IT platform beyond combined service levels

Strong business focus maintained: very limited customer and employee churn

After spin-off announcement(2)

0.41%

Before spin-off announcement(1)

0.48%

After spin-off announcement(2)

0.73%0.76%

Before spin-off announcement(1)

(1) Monthly average of period April 2005 – March 2006(2) Monthly average of period April 2006 – March 2007

ACHIEVEMENTS SO FAR

Legal integration/spin-off of BPH 285:Operational integration:

~30 days after regulatory approval

Up to 6 months after the legal integration

RETAINED TALENTS

Turnover of employees of both banks %

RETAINED CLIENTS

Churn of customer accounts%

8

NEW PEKAO WILL BECOME TOP BANK IN POLAND

Source: Companies Annual Report

(1) Deposits + Mutual funds managed by entities in Group(2) Nominal value: Net loans

30.7New Pekao

23.9PKO BP

13.4ING BSK

10.8BZ WBK

6.4Citibank

16.4New Pekao

15.5PKO BP

6.2BRE Bank

4.8BZ WBK

4.1Bank Millennium

1,239PKO BP

1,067New Pekao SA

384BZ WBK

379Bank Millennium

359Kredyt Bank

NOTE: December 2006

Customer funds(1)

EUR blnLoans(2)

EUR bln# of Branches

9

AGENDA

Poland macroeconomic and banking sector scenario

The creation of New Pekao

New Pekao strategic initiatives

Strategy for Ukraine

Closing remarks

10

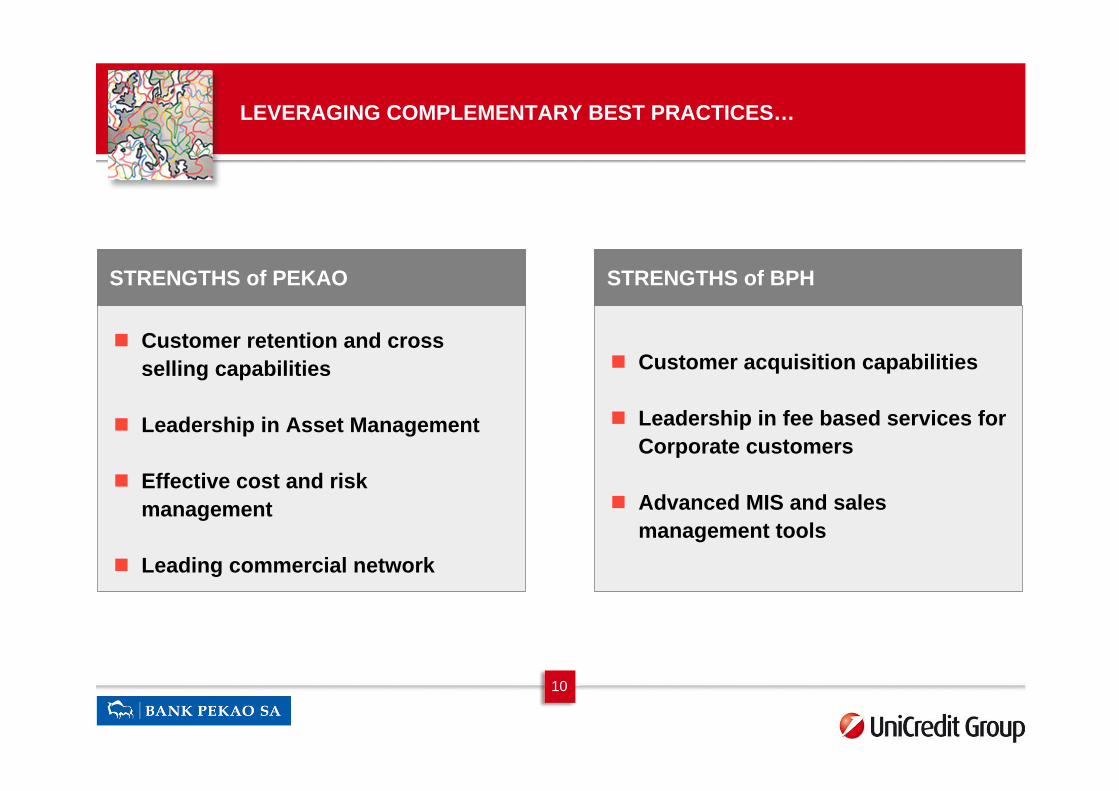

LEVERAGING COMPLEMENTARY BEST PRACTICES…

Customer retention and cross selling capabilities

Leadership in Asset Management

Effective cost and risk management

Leading commercial network

STRENGTHS of PEKAO

Customer acquisition capabilities

Leadership in fee based services for Corporate customers

Advanced MIS and sales management tools

STRENGTHS of BPH

11

Driving both, customer acquisition and cross-selling, based on innovative products/services in most attractive segments:

Retail family by focusing on mortgages & consumer loansAffluent by enhancing the advisory proposition & investment products SMEs by further improving service and loans processesCorporate by combining financing and transactional capabilities

Best practice in cost management

IT platform enhancement supporting offer enrichment

Leveraging strongest distribution reach with multi-channel approach: Offering nationwide physical network (branches and ATMs)Further developing multi-channel platform

…ACCELERATING NEW PEKAO FOR GROWTH

STRATEGIC INITIATIVES

12

RETAIL FAMILY: FOCUS ON MORTGAGES AND CONSUMER LOANS LEVERAGING UCI’S PRODUCT FACTORIES

Results so far (Old Pekao) Key actions, products & services

Mortgage sales volume, EUR mn

681

204

2003 2006

CAGR 2006-09:

+26%

Expected market growth

MORTGAGES

Consumer loans sales volume, EUR mn

2003 2006

CAGR 2006-09:

+19%

CONSUMER LOANS

539

60

Mortgage as acquisition tool

Product enhancement to exploit market shift towards zloty; no FX mortgages

Strengthening of largest mortgage advisors network and 3rd party channels

Next generation process improvement

Capture cross-selling potential combining best from both banksTap non-captive customers through customized products and intense marketingEnrichment of tailored insurance as attractive packages

13

Results so far (Old Pekao) Key actions, products & servicesExpected market growth

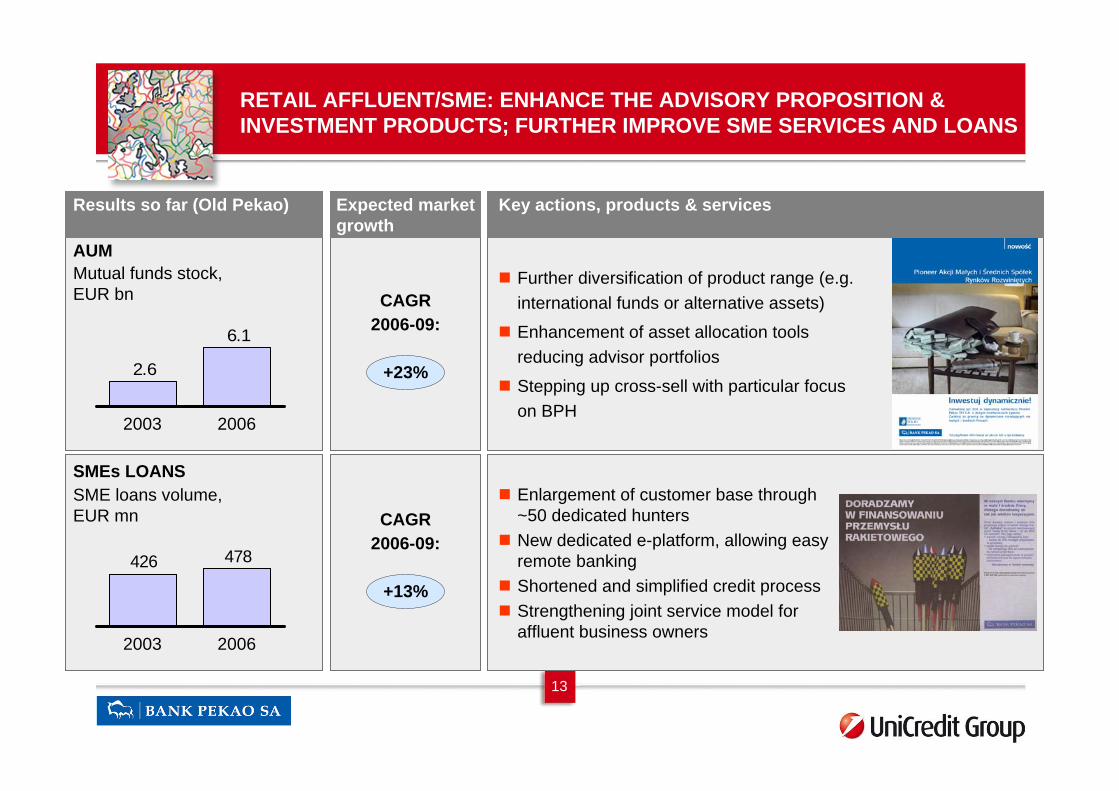

RETAIL AFFLUENT/SME: ENHANCE THE ADVISORY PROPOSITION & INVESTMENT PRODUCTS; FURTHER IMPROVE SME SERVICES AND LOANS

CAGR 2006-09:

+23%

AUMMutual funds stock, EUR bn

6.1

2.6

20062003

Further diversification of product range (e.g. international funds or alternative assets)

Enhancement of asset allocation tools reducing advisor portfolios

Stepping up cross-sell with particular focus on BPH

Enlargement of customer base through ~50 dedicated hunters New dedicated e-platform, allowing easy remote bankingShortened and simplified credit process Strengthening joint service model for affluent business owners

CAGR 2006-09:

+13%

SME loans volume, EUR mn

478426

20062003

SMEs LOANS

14

Results so far (Old Pekao) Key actions, products & servicesExpected market growth

CORPORATE: COMBINE FINANCING AND TRANSACTIONAL CAPABILITIES

6.84.7

(1) Source: Global Revenue and Value Pool

CAGR 2006-09:

+11%

LOANSLoans volume, EUR bn

20062003

CAGR 2006-09(1):

+13%

No of customers, ths

20062003

TRANSACTIONAL SERVICES

Service model with single point of entry and multilevel relationship

Best product offering based on both banks best practices (e.g. Multioption line)

Advanced functionalities of supporting systems and tools (e.g. MIS with profitability by product/ customer)

Leverage BPH expertise in transactional products (liquidity management and x-border pooling)

Implementation of advanced CRM system to ensure successful cross selling of value added products

Enhanced internet based trade finance and transactions products

7.810.4

15

STRONG NATIONWIDE PRESENCE – ROOM FOR FURTHER EXPANSION IN SELECTED REGIONS

(1) Including only Banking Branches

N° of branches

Geographic presence: 1,067(1) branches and the biggest network of 2,716(2) ATMs

N°1 in branch market share

32

26

35

66

50

7120

1981

108

26

7788

222

57

89

N°2 in branch market share

N°3 in branch market share

N°4 in branch market share

(2) Including Euronet ATMs

16

IT PLATFORM ENHANCEMENT SUPPORTING OFFER ENRICHMENT

Integration of the brokerage system allowing for the introduction of security products sales in branches and via internet platform

Introduction of an enhanced automatic scoring system for SMEs allowing for strengthened and simplified credit decisions

Introduction of integrated performance management tool allowing for deep profitability overview: by product, customer, portfolio

Key initiatives

17

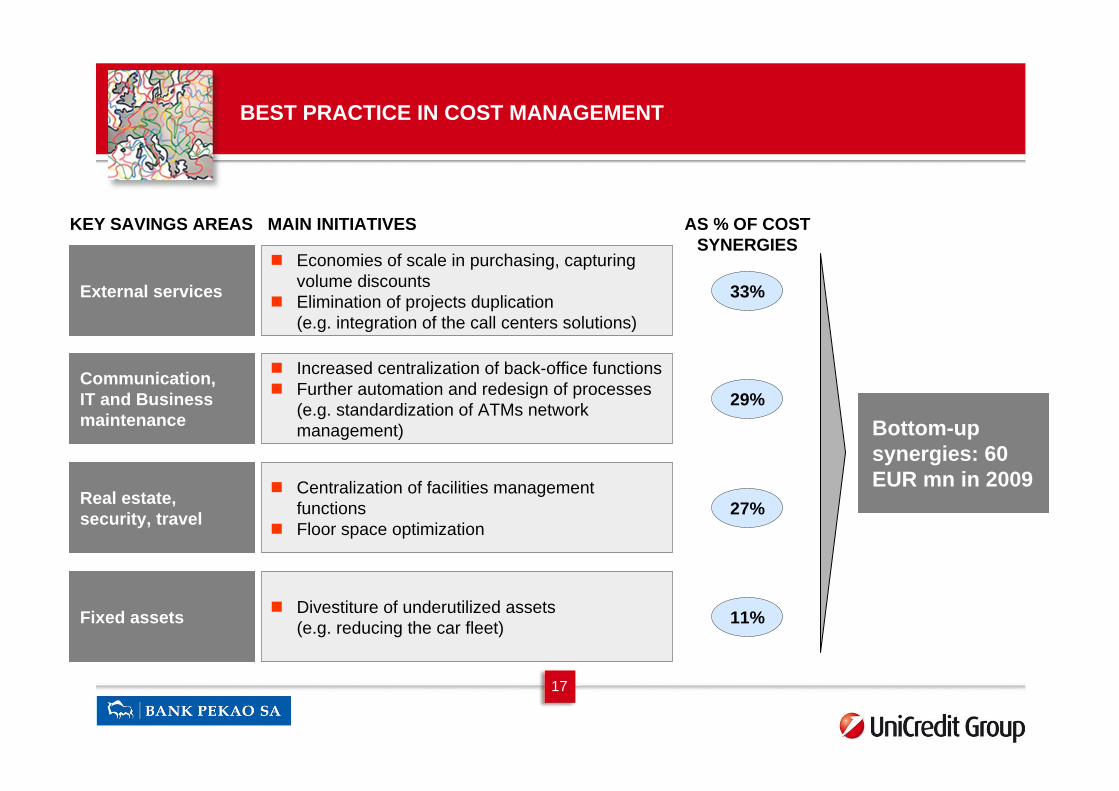

Bottom-up synergies: 60 EUR mn in 2009

AS % OF COST SYNERGIES

Communication, IT and Businessmaintenance

Increased centralization of back-office functionsFurther automation and redesign of processes (e.g. standardization of ATMs network management)

29%

External services

Economies of scale in purchasing, capturing volume discountsElimination of projects duplication(e.g. integration of the call centers solutions)

33%

Real estate,security, travel

Centralization of facilities management functionsFloor space optimization

27%

Fixed assets Divestiture of underutilized assets(e.g. reducing the car fleet) 11%

MAIN INITIATIVESKEY SAVINGS AREAS

BEST PRACTICE IN COST MANAGEMENT

18

AGENDA

Poland macroeconomic and banking sector scenario

The creation of New Pekao

New Pekao strategic initiatives

Strategy for Ukraine

Closing remarks

19

UKRAINE – HUGE, FAST GROWING AND UNDERSERVED MARKET

Low labor cost, attracting foreign investments

Low penetrationvs. EU and Poland, with significant room for growth in all products

Manageable riskreflected in ratings S&P BB-, Moody’s B1

With strong GDP growth…%

Huge market2006

GDP per capitaThs EUR

1.85.2

27.7

EU 15 CEE(1) Ukraine

Very promising outlook

Source: UniCredit-NE Research Network(1) Data as of December 31, 2006

47

389381

CEE 16(1) UkraineEU 15

Population Mln

… and banking low market penetration(1)

%

Ukraine

Eurozone1.4

5.7

7.9

2.12007F-09F(avg)

2003-06(avg)

3446

96119

Deposits/GDP

Loans/GDP

Ukraine

Eurozone

20

STRATEGY FOR UKRAINE: MERGER OF GREENFIELD START-UP AND HVB FOLLOWING AN AMBITIOUS DEVELOPMENT PLAN

MERGER FOR GROWTH STARTING IN 2007

Top 15 Ukrainian bank setting the basis for future ambitious growth

New Bank

Total assets: EUR mln 169

Total loans: EUR mln 52

Number of clients: 16,700

Number of branches: 24

Total assets: EUR mln 454

Total loans: EUR mln 344

Number of clients: 946 (2)

Number of branches: 6

UniCredit Bank – a greenfield retail bank (1) HVB Ukraine – a corporate bank (1)

(1) Data as of end of April 2007(2) Only Corporate Clients

21

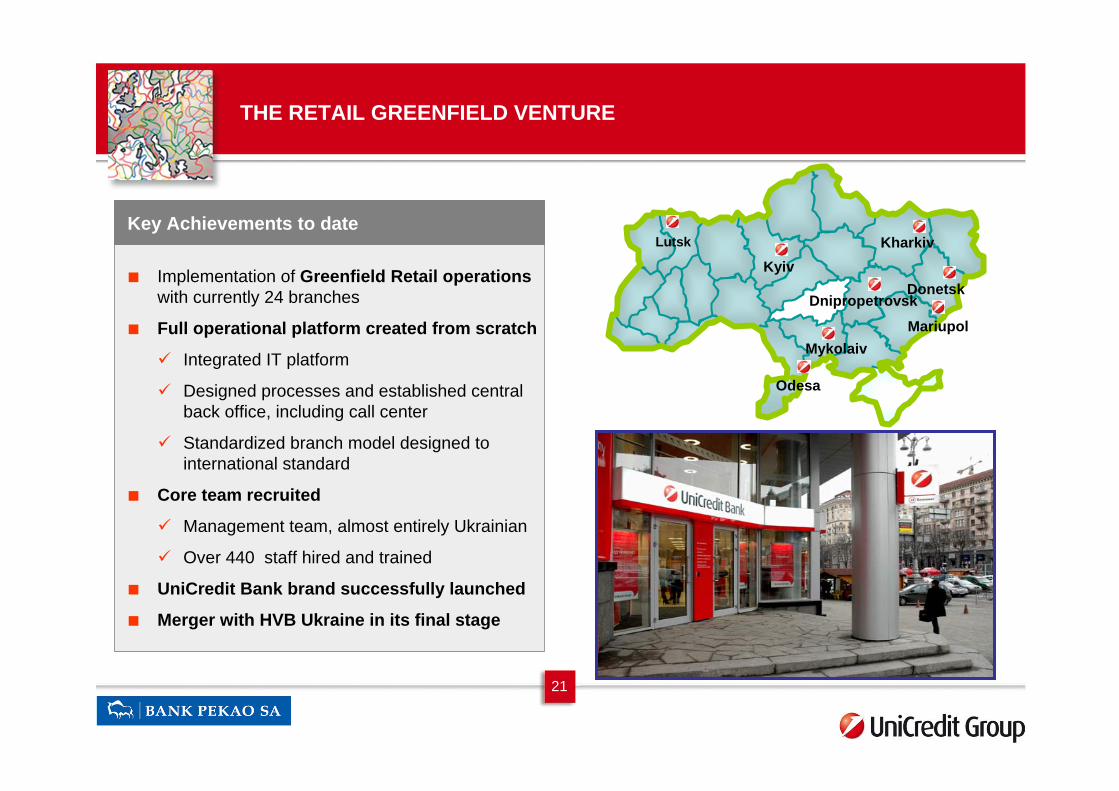

THE RETAIL GREENFIELD VENTURE

Kyiv

Odesa

DnipropetrovskDonetsk

Kharkiv

MariupolMykolaiv

Lutsk

Implementation of Greenfield Retail operationswith currently 24 branches

Full operational platform created from scratch

Integrated IT platform

Designed processes and established central back office, including call center

Standardized branch model designed to international standard

Core team recruited

Management team, almost entirely Ukrainian

Over 440 staff hired and trained

UniCredit Bank brand successfully launched

Merger with HVB Ukraine in its final stage

Key Achievements to date

22

UKRAINIAN BANK STRATEGY

RETAIL BUSINESS CORPORATE BUSINESS

Open 160 branches in two years reaching country-wide presence till 2008

Leverage UniCredit Group know-how and expertise in Retail

Develop a wide range of lending products, leveraging credit cards(including gold/platinum cards)

Increase product sales: current accounts with ATM debit cards, savings plans and term deposits (both local and foreign currency)

Ensure selective growth in mid-cap market

Leverage international network of the Group

Develop best practice transactional services and trade finance products

23

AGENDA

Poland macroeconomic and banking sector scenario

The creation of New Pekao

New Pekao strategic initiatives

Strategy for Ukraine

Closing remarks

24

LEVERAGING ON PEKAO’S SUCCESSFUL TRACK RECORD ...

ROE (%) C/I (%) EPS (EUR)

13.1

2003

21.1

2006

56.7

2003

50.3

2006

2.8

1.4

2003 2006

+26%

Market capitalizationEUR bn

4.7

2003

6.0

2004

7.6

2005

9.8

2006

11.1

1Q’07

+27%

+x% CAGR ’03-’06

25

... ACCELERATING GROWTH COMBINING BEST PRACTICES AND EXPLOITING HEALTHY ENVIRONMENT

Attractive macroeconomic perspectives with solid country risk profile

Expansion in Ukraine as second home market

Ready for integration: ambitious management team, waiting for regulatory approval

Aspirational growth initiatives combining joint strengths in attractive segments:Retail family by focusing on mortgages & consumer loansAffluent by enhancing the advisory proposition and investment productsSMEs by further improving service and loans processesCorporate by combining financing and transactional capabilities