MinEx Consulting Strategic advice on mineral economics & exploration

- Gloom or Boom ?

Richard SchoddeManaging Director, MinEx Consulting

Adjunct Professor, University of Western Australia

Geological Society of South AfricaGeoForum 2013 Conference2nd – 5th July 2013, Johannesburg

MinEx Consulting Strategic advice on mineral economics & exploration

Overview: Gloom or Boom?

1. Trends in global exploration spendForecast future spend out to 2020 & financing issues for Junior Companies

2. Trends in discovery ratesWhere were the discoveries made? Current “Hot Spots” for exploration

3. Trends in discovery performanceWhich Regions did better? Factors impacting on discovery performance

4. Trends in the types of exploration methods usedGeophysics versus geochemistry versus “nearology”

5. Trends in discovery costsUnit discovery costs ($/oz, c/lb) are rising

6. Are we finding enough metal?To be sustainable we need to find enough to replace what we mine

7. Conclusions

2

MinEx Consulting Strategic advice on mineral economics & exploration

Exploration expenditures reached an all-time high in 2012

3

MinEx Consulting Strategic advice on mineral economics & exploration

Exploration expenditures: Worldby Commodity : 1975-2012

$0

$5

$10

$15

$20

$25

$30

1975 1980 1985 1990 1995 2000 2005 2010

Other Bulk

Coal

Iron Ore

Other

Diamonds

Uranium

Base Metals

Gold

4

2012 US$ billion

Sources: MinEx Consulting estimates © April 2013, based ondata from ABS, NRCan, MLR (China), OECD and MEG SNL

$29.4Bin 2012

$2.9Bin 2002

$7.9Bin 1997

Spend is at anall-time high

Spend is at anall-time high

10x real increasein the last decade

MinEx Consulting Strategic advice on mineral economics & exploration

Exploration expenditures: Worldby Commodity : 1975-2012

0%

20%

40%

60%

80%

100%

1975 1980 1985 1990 1995 2000 2005 2010

5

Percentage of total spend

34%

23%

3%2%

13%

14%

11%

1%

Gold continuesto be the main

target

Gold continuesto be the main

target

Other - Bulk

Iron Ore

Coal

Other – Non Bulk

UraniumBase Metals(Cu, Ni, Zn, Pb)

Gold

Diamonds

Major increase inspend on Bulk

Minerals

Major increase inspend on Bulk

Minerals

Sources: MinEx Consulting estimates © April 2013, based ondata from ABS, NRCan, MLR (China), OECD and MEG SNL

MinEx Consulting Strategic advice on mineral economics & exploration

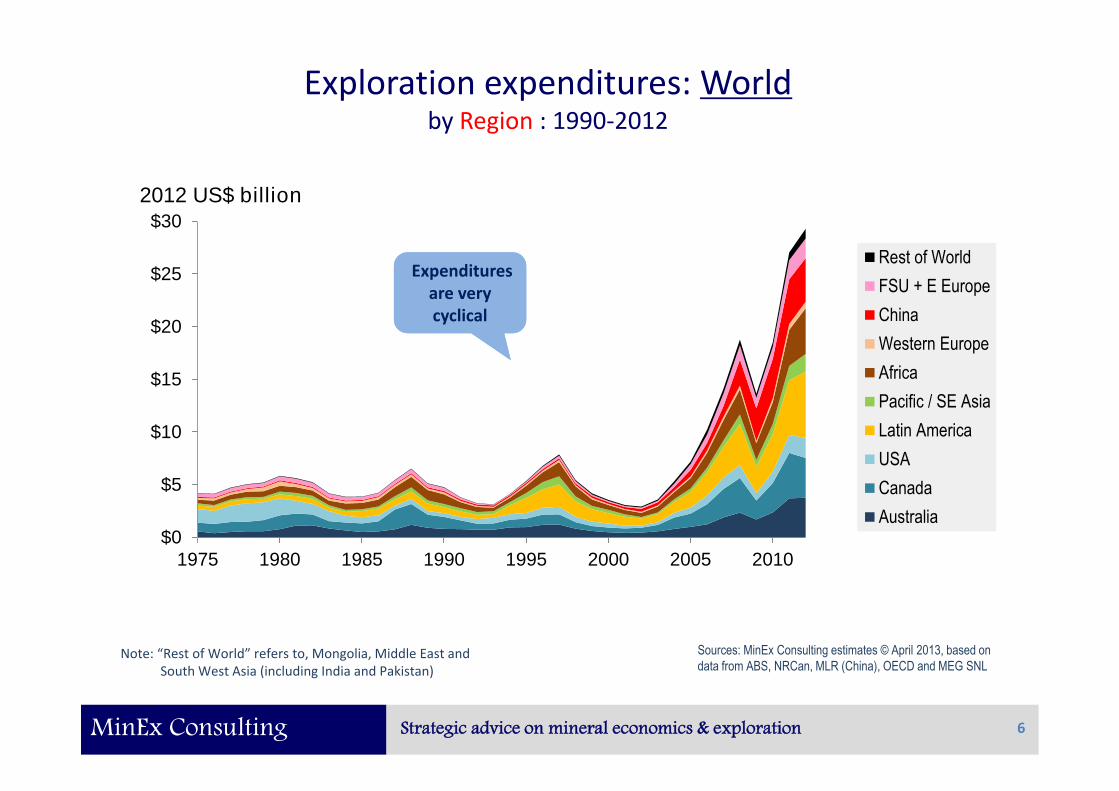

Exploration expenditures: Worldby Region : 1990-2012

$0

$5

$10

$15

$20

$25

$30

1975 1980 1985 1990 1995 2000 2005 2010

Rest of World

FSU + E Europe

China

Western Europe

Africa

Pacific / SE Asia

Latin America

USA

Canada

Australia

6

2012 US$ billion

Expendituresare verycyclical

Expendituresare verycyclical

Note: “Rest of World” refers to, Mongolia, Middle East andSouth West Asia (including India and Pakistan)

Sources: MinEx Consulting estimates © April 2013, based ondata from ABS, NRCan, MLR (China), OECD and MEG SNL

MinEx Consulting Strategic advice on mineral economics & exploration

Exploration expenditures: Worldby Region : 1990-2012

0%

20%

40%

60%

80%

100%

1975 1980 1985 1990 1995 2000 2005 2010

Rest of World

FSU + E Europe

China

Western Europe

Africa

Pacific / SE Asia

Latin America

USA

Canada

Australia

7

Note: “Rest of World” refers to, Mongolia, Middle East andSouth West Asia (including India and Pakistan)

Percentage of total spend

13%

13%

7%

21%

6%

15%

2%

14%

6%

3%

China spends moreon exploration thanany other country in

the World

China spends moreon exploration thanany other country in

the World

Can+USA+Ausmarket share has

halved in the last 2decades

Can+USA+Ausmarket share has

halved in the last 2decades

Sources: MinEx Consulting estimates © April 2013, based ondata from ABS, NRCan, MLR (China), OECD and MEG SNL

MinEx Consulting Strategic advice on mineral economics & exploration

Exploration spend is closely linked to commodity pricesWorld gold exploration expenditures versus gold price

$0

$400

$800

$1,200

$1,600

$2,000

$2,400

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

8

Exploration Expenditures(June 2012 US$m)

Gold Price(June 2012 US$/oz)

Gold Price(RHS>)

ExplorationSpend (<LHS)

Source: MinEx Consulting © July 2013Forecasts from Consensus Economics © June 2013

BrokersForecasts(June 13)

BrokersForecasts(June 13)

Since 1990s there hasbeen a strong correlationbetween Gold Price and

Exploration Spend

Since 1990s there hasbeen a strong correlationbetween Gold Price and

Exploration Spend

See a similar trendfor other metals

MinEx Consulting Strategic advice on mineral economics & exploration

Forecast exploration expenditures: Worldby Commodity : 1975-2020

$0

$5

$10

$15

$20

$25

$30

1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Other

Coal

Iron Ore

Uranium

Base Metals

Gold

9

2012 US$ billion

Note: Forecast based on a Multiple-Regression analysis of datafrom 1997-2012 with R2 = 0.95

Gold is projected tofall the most

Gold is projected tofall the most

Source: MinEx Consulting estimates © July 2013, based oncommodity price forecasts from Consensus Economics June 2013

$29Bin 2012

$19Bin 2020

Down35%

Spend on uranium isprojected to increaseSpend on uranium isprojected to increase

Forecast

MinEx Consulting Strategic advice on mineral economics & exploration

$0

$5

$10

$15

$20

$25

$30

1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

FSU + EE + ROW

China

Western Europe

Africa

Pacific / SE Asia

Latin America

USA

Canada

Australia

Forecast exploration expenditures: Worldby Region : 1975-2020

10

2012 US$ billion$29B

in 2012

Note: “Rest of World” refers to, Mongolia, Middle East andSouth West Asia (including India and Pakistan)

$19Bin 2020

Down35%

CAUTION:Forecast assumes nochange in Country Riskand tax rules

Source: MinEx Consulting estimates © July 2013, based oncommodity price forecasts from Consensus Economics June 2013

MinEx Consulting Strategic advice on mineral economics & exploration

The Junior sector is facing severe funding problems. This willmost felt in-terms of reduced “money into the ground”

Cash and Expenditures for the MEDIAN Australian Junior company: 1998-2012r

$0

$1

$2

$3

$4

$5

Dec-98 Dec-00 Dec-02 Dec-04 Dec-06 Dec-08 Dec-10 Dec-12

11

June 2012 A$ Million(annualised basis)

Source: MinEx Consulting © February 2013based on Quarterly Reports to the ASX

Note: Expenditure data is reported on a Quarterly basis, but has beenannualised to be comparable with Cash Reserves

Administration Costs

Exploration + Development Costs

Cash Funds atend of Quarter

Large amount of fundsraised in 2006-2007

Large amount of fundsraised in 2006-2007

Funding dried up duringthe GFC. To preserve

cash, Junior Companiesseverely cut back on

expenditures in the field

Funding dried up duringthe GFC. To preserve

cash, Junior Companiesseverely cut back on

expenditures in the field

The 2013 “bust”could be moresevere than the

2008 GFC

The 2013 “bust”could be moresevere than the

2008 GFC

Funding dried up againin 2012. Key problem isthat the starting cash

reserves are low

Funding dried up againin 2012. Key problem isthat the starting cash

reserves are low

Because ofthis …

MinEx Consulting Strategic advice on mineral economics & exploration

Exploration expenditures reached an all-time high in 2012

12

MinEx Consulting Strategic advice on mineral economics & exploration

Number of deposits found each year – by RegionMineral deposits# found in the World: 1975-2012

13

0

20

40

60

80

100

1975 1980 1985 1990 1995 2000 2005 2010

China+FSU+EE+ME

Western Europe

Africa

Pacific / SE Asia

Latin America

USA

Canada

Australia

Number

N = 2161

Source: MinEx Consulting © July 2013

Note: # Discoveries are for deposits >0.1 Moz Au, >5 kt U3O8, >10 kt Ni, >0.1 Mt Cu-equivExcludes satellite deposits within existing CampsExcludes bulk mineral discoveries

Caution:Incomplete data inrecent years

Due to delays in reporting ofdiscoveries, expect the final

number to be 2-3x larger

Due to delays in reporting ofdiscoveries, expect the final

number to be 2-3x larger

MinEx Consulting Strategic advice on mineral economics & exploration

Number of deposits found each year – by RegionMineral deposits# found in the World: 1975-2012

14

0%

20%

40%

60%

80%

100%

1975 1980 1985 1990 1995 2000 2005 2010

China+FSU+EE+ME

Western Europe

Africa

Pacific / SE Asia

Latin America

USA

Canada

Australia

Share of discoveries made

Note: # Discoveries are for deposits >0.1 Moz Au, >5 kt U3O8, >10 kt Ni, >0.1 Mt Cu-equivExcludes satellite deposits within existing CampsExcludes bulk mineral discoveries

Caution:Incomplete data inrecent years

Source: MinEx Consulting © July 2013

MinEx Consulting Strategic advice on mineral economics & exploration

Tier 1, 2 & 3 discoveries in the world: 2002-Present

15

Au BaseMetal

U3O8 Other

Tier 2

Tier 3

Tier 1

Alaska/Yukon NorthernOntario

Latin America

Ten current“Hot Spots”Ten current“Hot Spots”

West AfricaCentral Africa

China

Australia

Far EastRussia

Saskatchewan(Uranium)

SW USA/ Mexico

Source: MinEx Consulting © July 2013

MinEx Consulting Strategic advice on mineral economics & exploration

Spend & performance by Region: 2003-12

Region ExplorationSpend (2012 $b)

Number ofDiscoveries #

Tier 1+2Discoveries

Australia $12 (10%) 83 (16%) 13 (15%)

Canada $22 (18%) 65 (12%) 16 (19%)

USA $9 (8%) 20 (4%) 9 (10%)

Latin America $28 (23%) 118 (23%) 15 (17%)

Pacific / SE Asia $6 (5%) 23 (4%) 2 (3%)

Africa $17 (14%) 116 (22%) 19 (22%)

Western Europe $3 (3%) 22 (4%) 1 (1%)

China+FSU+EE+RoW $22 (19%) 77 (15%) 11 (13%)

----- ------- ------ -------- ------ --------

TOTAL $116 (100%) 524 (100%) 86 (100%)

16

Africaperformed

the best

Africaperformed

the best

Note: # Discoveries are for deposits >0.1 Moz Au, >5 kt U3O8, >10 kt Ni, >0.1 Mt Cu-equivExcludes satellite deposits within existing CampsExcludes bulk mineral discoveries Source: MinEx Consulting © July 2013

MinEx Consulting Strategic advice on mineral economics & exploration

Due to rising input costs and deeper targets It is become more expensiveto make a discovery

17

MinEx Consulting Strategic advice on mineral economics & exploration

Discovery rate versus spendWestern World non-ferrous exploration spend and discoveries

18

$0

$5

$10

$15

$20

0

50

100

150

200

1975 1980 1985 1990 1995 2000 2005 2010

Estimated No of unreported discoveries

Number of Discoveries

Exploration Expenditures

Number of Discoveries

Note: Excludes expenditures and discoveries for Bulk MineralsDiscoveries are for deposits >0.1 Moz Au, >5 kt U3O8, >10 kt Ni, >0.1 Mt Cu-equiv

2012 US$ Billion

Even after adjusting forunreported discoveries , inthe last 5 years a large gap

has opened up betweenexpenditures and number of

deposits found

Even after adjusting forunreported discoveries , inthe last 5 years a large gap

has opened up betweenexpenditures and number of

deposits found

Estimate

… Gap due to higherinput costs (labour,drilling and admin)

Source: MinEx Consulting © July 2013

Between 2002 & 2012 WWspend went up 8x anddiscovery rate up ~3x

Between 2002 & 2012 WWspend went up 8x anddiscovery rate up ~3x

$2.4b

$18.5b

MinEx Consulting Strategic advice on mineral economics & exploration

Input costs for exploration have doubledin the last decade

2000nominal

2000real

2012real

% realincrease

$ of the Day 2012 $ 2012$

Average Diamond Drilling Cost (US$/metre)- Canada- Australia

$84$77

$112$102

$210$229

88%125%

Average salary for an Exploration Manager(US$ per annum)- Canada- Australia

$70,000$75,000

$93,000$100,000

$170,000$250,000

83%150%

Median Administration Cost for a JuniorExploration Company (US$m per annum)- Australia $0.34 $0.44 $1.19 170%

19

Source: MinEx Consulting © July 2013

MinEx Consulting Strategic advice on mineral economics & exploration

Higher costs impact on the amount of drilling doneExploration spend and drilling in Canada and Australia: 1997-2012

-3

2

7

12

$0$1$2$3$4$5$6

1997 2002 2007 2012

20

(2012 US$ Billion)

Data: NRCan, ABS

(million metres)

-3

2

7

12

$0$1$2$3$4$5$6

1997 2002 2007 2012

Canada

Australia

Metres Drilled

Metres Drilled

Exploration Expenditures

Exploration Expenditures

Between 2002-2011,Expenditures rose 8.0x

but drilling only rose 3.9x

Between 2002-2011,Expenditures rose 8.0x

but drilling only rose 3.9x

Between 2002-2012,Expenditures rose 9.3x

but drilling only rose 2.4x

Between 2002-2012,Expenditures rose 9.3x

but drilling only rose 2.4x

MinEx Consulting Strategic advice on mineral economics & exploration

… and we are exploring under deeper coverDepth of cover for Gold and Base Metal discoveries in the World: 1900-2012

0

500

1000

1500

2000

1900 1920 1940 1960 1980 2000 2020

21

Discovery Year

Depth of Cover (Metres)

Note: Excludes satellite deposits within existing CampsExcludes gold deposits in South Africa

It is difficult to finddeposits under deep

cover

It is difficult to finddeposits under deep

cover

… end-result is that wehave to drill more metres

per discovery

… end-result is that wehave to drill more metres

per discovery

Source: MinEx Consulting © July 2013

MinEx Consulting Strategic advice on mineral economics & exploration

Average depth of cover for discoveries - all metalsWestern World: 2003-2012

204

126122

9882

68

3212

74

0

50

100

150

200

250

55

22

AverageLatinAm

Africa(excl Sth Africa) Aust

WEurope Canada USA

PacificSE Asia

Restof WW

Metres

If you exclude SouthAfrica, the average

depth of cover falls from55 to 12 metres

If you exclude SouthAfrica, the average

depth of cover falls from55 to 12 metres

Note: Based on deposits >0.1 Moz Au, >5 kt U3O8, >10 kt Ni, >0.1 Mt Cu-equivExcludes bulk mineral discoveries Source: MinEx Consulting © July 2013

MinEx Consulting Strategic advice on mineral economics & exploration

There have been several innovations in the exploration tools used tomake discoveries

23

MinEx Consulting Strategic advice on mineral economics & exploration

Trends in exploration methods

The preferred search method used varies by commodity type,

depth of cover and “scale”

24

Continental-Scale

Province-Scale

District-Scale

Project-Scale

Prospect-ScaleMinEx has carried out a detailedanalysis of the discovery history of1750 deposits at these two scales

MinEx has carried out a detailedanalysis of the discovery history of1750 deposits at these two scales

MinEx Consulting Strategic advice on mineral economics & exploration

Primary search method used at the project-scaleGOLD discoveries (>0.1 Moz) in the World: 1900-2012

0%

20%

40%

60%

80%

100% Serendipity

Prospector

Other

Visual

Conceptual/Geological

Geological Mapping

Extrapolated from KnownMineralisationGeochem

Geophysics + Geochem

Geophysics

25

Percentage of total discoveries

Note: Analysis based on detailed analysis of 993 gold projects (out of 1779 known discoveries)

ie What method wasused to decide where

to peg the leases

ie What method wasused to decide where

to peg the leases

Source: MinEx Consulting © July 2013

MinEx Consulting Strategic advice on mineral economics & exploration

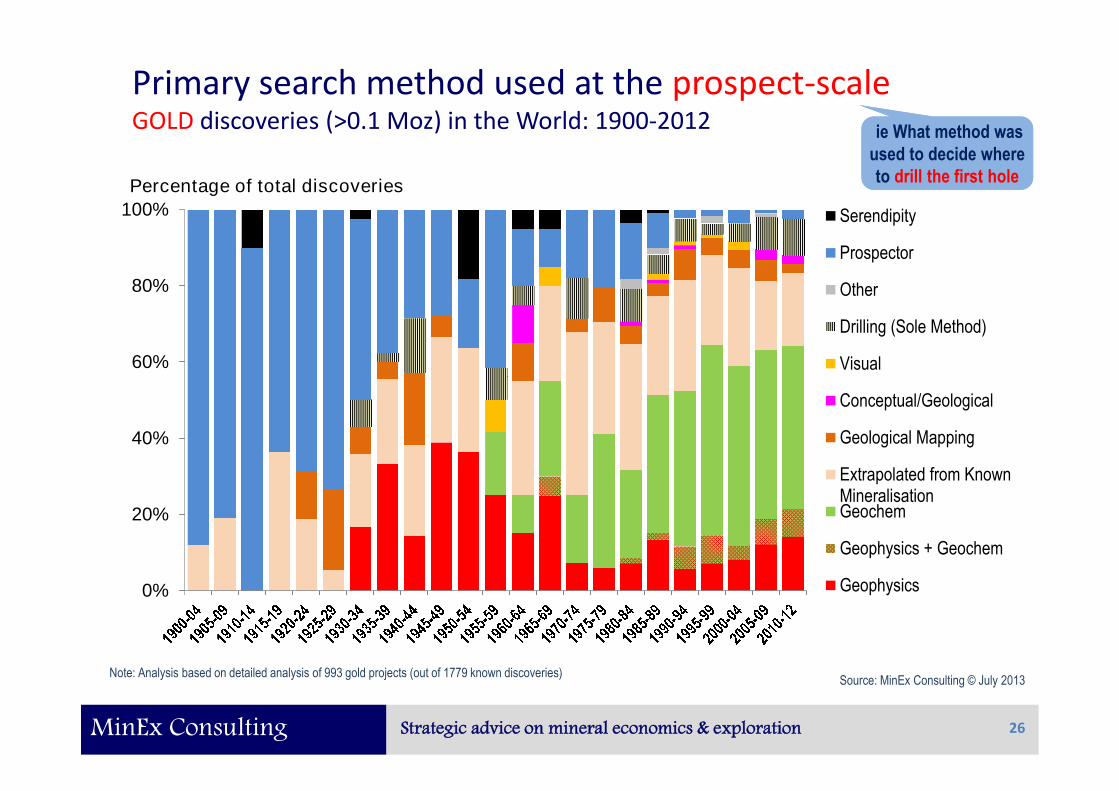

Primary search method used at the prospect-scaleGOLD discoveries (>0.1 Moz) in the World: 1900-2012

0%

20%

40%

60%

80%

100% Serendipity

Prospector

Other

Drilling (Sole Method)

Visual

Conceptual/Geological

Geological Mapping

Extrapolated from KnownMineralisationGeochem

Geophysics + Geochem

Geophysics

26

Percentage of total discoveries

Note: Analysis based on detailed analysis of 993 gold projects (out of 1779 known discoveries)

ie What method wasused to decide whereto drill the first hole

ie What method wasused to decide whereto drill the first hole

Source: MinEx Consulting © July 2013

MinEx Consulting Strategic advice on mineral economics & exploration

Primary search method used at the project-scaleBASE METAL discoveries (>0.1 Mt Cu-eq) in the World: 1900-2012

0%

20%

40%

60%

80%

100% Serendipity

Prospector

Other

Visual

Conceptual/Geological

Geological Mapping

Extrapolated from KnownMineralisationGeochem

Geophysics + Geochem

Geophysics

27

Percentage of total discoveries

Note: Analysis based on detailed analysis of 757 Cu+Ni+Zn+Pb projects (out of 1344 known discoveries)

ie What method wasused to decide where

to peg the leases

ie What method wasused to decide where

to peg the leases

Source: MinEx Consulting © July 2013

MinEx Consulting Strategic advice on mineral economics & exploration

Primary search method used at the prospect-scaleBASE METAL discoveries (>0.1 Mt Cu-eq) in the World: 1900-2012

0%

20%

40%

60%

80%

100% Serendipity

Prospector

Other

Drilling (Sole Method)

Visual

Conceptual/Geological

Geological Mapping

Extrapolated from KnownMineralisationGeochem

Geophysics + Geochem

Geophysics

28

Percentage of total discoveries

Note: Analysis based on detailed analysis of 757 Cu+Ni+Zn+Pb projects (out of 1344 known discoveries)

ie What method wasused to decide whereto drill the first hole

ie What method wasused to decide whereto drill the first hole

Source: MinEx Consulting © July 2013

MinEx Consulting Strategic advice on mineral economics & exploration

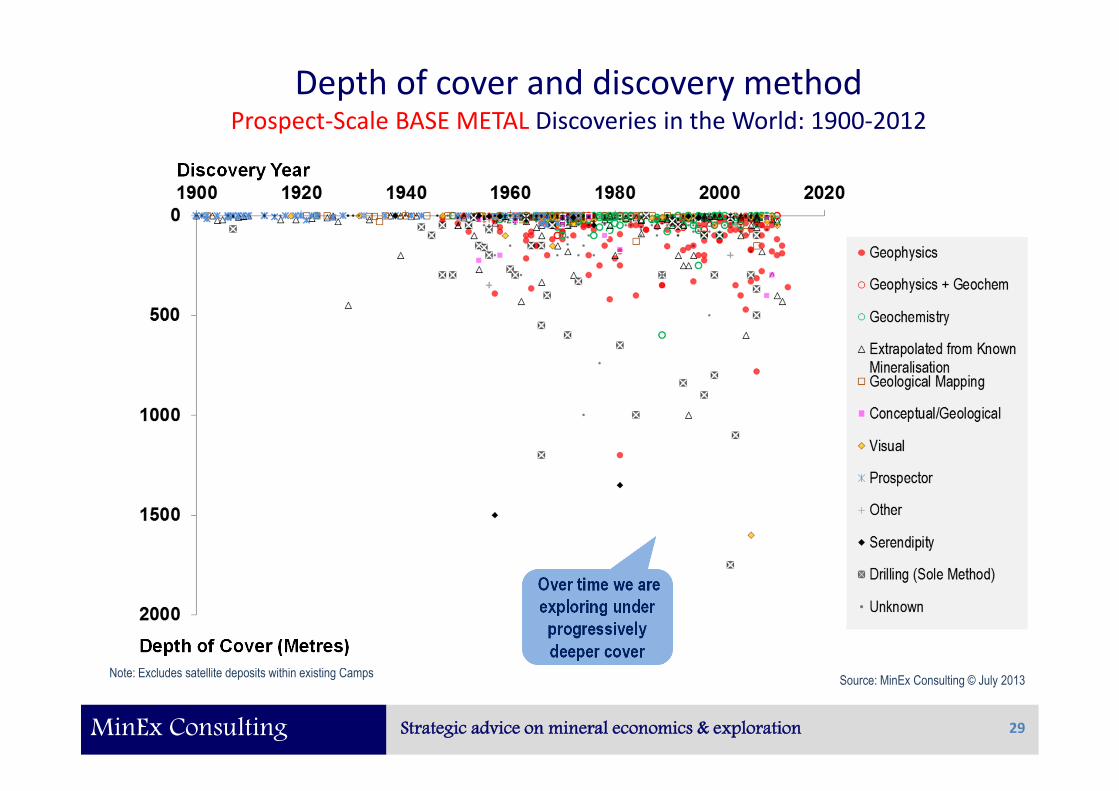

Depth of cover and discovery methodProspect-Scale BASE METAL Discoveries in the World: 1900-2012

29

Discovery Year

Depth of Cover (Metres)

Note: Excludes satellite deposits within existing Camps

Over time we areexploring underprogressivelydeeper cover

Over time we areexploring underprogressivelydeeper cover

Source: MinEx Consulting © July 2013

MinEx Consulting Strategic advice on mineral economics & exploration

Depth of cover and discovery methodProspect-Scale GOLD Discoveries in the World: 1900-2012

30

Discovery Year

Depth of Cover (Metres)

Note: Excludes satellite deposits within existing CampsSource: MinEx Consulting © July 2013

MinEx Consulting Strategic advice on mineral economics & exploration

Depth of cover and discovery methodProspect-Scale GOLD Discoveries in the World: 1900-2012

31

EXCLUDING South Africa

Discovery Year

Depth of Cover (Metres)

Note: Excludes satellite deposits within existing Camps

Gold exploration is generallydone under shallower cover …

only because we don’t have anygood tools to look deep !!

Gold exploration is generallydone under shallower cover …

only because we don’t have anygood tools to look deep !!

Source: MinEx Consulting © July 2013

MinEx Consulting Strategic advice on mineral economics & exploration

The cost per unit of metal found has been rising

32

MinEx Consulting Strategic advice on mineral economics & exploration

Exploration expenditures and amount of copper foundPrimary copper deposits >0.5 Mt Cu-eq found in Western World: 1950-2012

33

$0

$1

$2

$3

$4

$5

0

50

100

150

200

1950 1960 1970 1980 1990 2000 2010

Exploration Expenditures

Estimate

Western World Discoveries

Mt Cu-eq

Note: Estimate includes adjustments for deposits with no discovery yearand deposits missing from the database

Expenditures (2012 US$B)

Source: MinEx Consulting © June 2013

MinEx Consulting Strategic advice on mineral economics & exploration

Until recently, copper discovery costs were fairly steadyUnit discovery costs for primary copper in the Western World: 1950-2012

34

US Cents per lb Cu-eq in 2012$

3 Year rolling average

Estimate

# Equal to 3.0 ¢/lbexcluding by-product credits

Assume 2.5 ¢/lb # Cu-eqgoing forward

Assume 2.5 ¢/lb # Cu-eqgoing forward

1995-2005 Average= 0.9 ¢/lb Cu-eq

1995-2005 Average= 0.9 ¢/lb Cu-eq

Source: MinEx Consulting © June 2013

MinEx Consulting Strategic advice on mineral economics & exploration

Gold exploration expenditures and ounces foundPrimary gold found in the Western World: 1950-2011

35

$0

$2

$4

$6

$8

$10

0

100

200

300

1950 1960 1970 1980 1990 2000 2010

Exploration Expenditures

Estimate

Western World Discoveries

Moz Expenditures (2012 US$B)

Source: MinEx Consulting © June 2012

MinEx Consulting Strategic advice on mineral economics & exploration

Discovery costs for gold are risingUnit discovery costs for primary gold in the Western World: 1950-2011

36

Estimate

Discovery Cost (June 2012 US$/oz)

1995-2005Average = $25/oz

1995-2005Average = $25/oz

Assume $32/ozgoing forwardAssume $32/ozgoing forward

3 Year rolling average

$113

Source: MinEx Consulting © June 2012

MinEx Consulting Strategic advice on mineral economics & exploration

Average discovery costs for uranium are risingUnit discovery costs for uranium in the Western World: 1950-2011

37

Discovery Cost (US$/lb U3O8)

5 Year rolling average

Estimate

Assume $2.50/lbgoing forward

Assume $2.50/lbgoing forward

1995-2005Average = $1.63/lb

1995-2005Average = $1.63/lb

$11.09

Source: MinEx Consulting © June 2012

MinEx Consulting Strategic advice on mineral economics & exploration

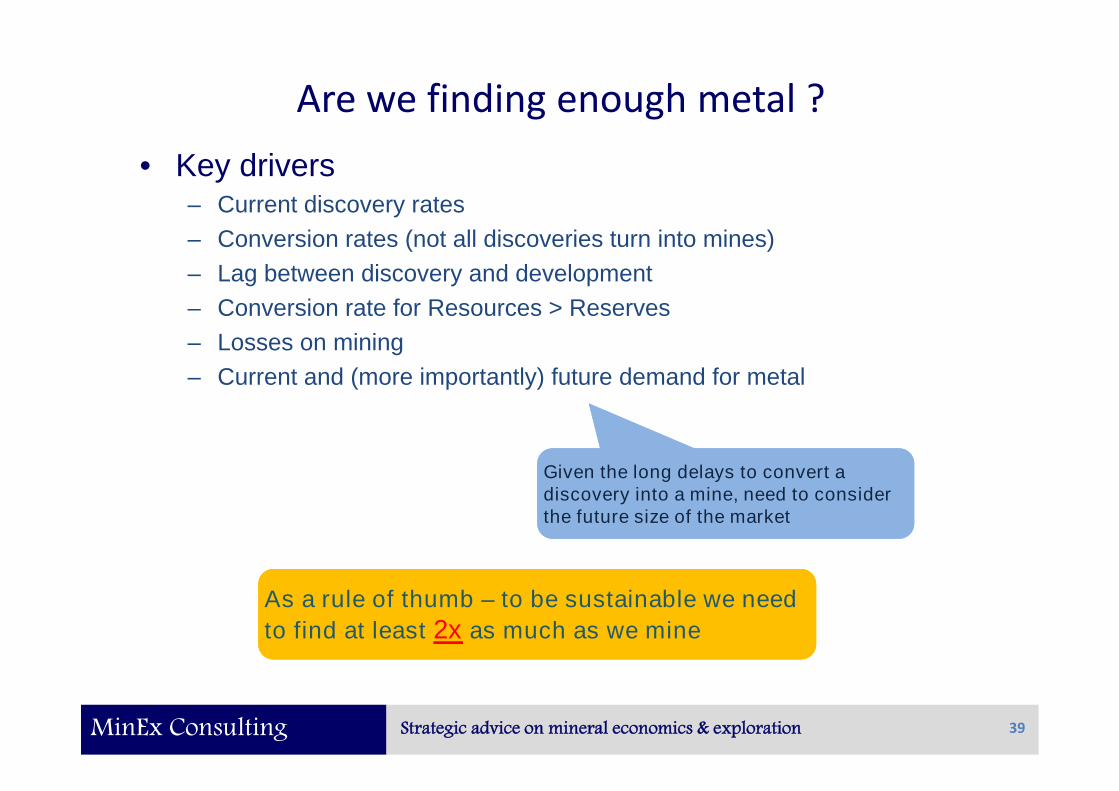

6. ARE WE FINDING ENOUGH METAL ?

For the industry to be sustainable it needs to replace what it mines

38

MinEx Consulting Strategic advice on mineral economics & exploration

Are we finding enough metal ?

• Key drivers– Current discovery rates

– Conversion rates (not all discoveries turn into mines)

– Lag between discovery and development

– Conversion rate for Resources > Reserves

– Losses on mining

– Current and (more importantly) future demand for metal

39

Given the long delays to convert adiscovery into a mine, need to considerthe future size of the market

Given the long delays to convert adiscovery into a mine, need to considerthe future size of the market

As a rule of thumb – to be sustainable we need

to find at least 2x as much as we mine

As a rule of thumb – to be sustainable we need

to find at least 2x as much as we mine

MinEx Consulting Strategic advice on mineral economics & exploration

Mining & discovery rates for goldAmount of gold found and mined in the World: 1950-2010

40

0

100

200

300

400

1950 1960 1970 1980 1990 2000 2010

Discoveries

World Production

Estimate

Moz

Note: Chart include minor adjustment for deposits missing from the databaseIs based on discoveries > 0.1 Moz

Sources: MinEx Consulting © Nov 2011.Production data from USGS

Exploration Spend $

Unit Discovery Costs

Total Metal Found

Future Mine Production

Discovery/Prodn Ratio in 2026 1.5x

“Tight”“Tight”

Outlook

MinEx Consulting Strategic advice on mineral economics & exploration

Mining & discovery rates for copperAmount of primary copper found and mined in the World: 1950-2011

41

0

20

40

60

80

100

120

140

160

1950 1960 1970 1980 1990 2000 2010

Discoveries - Estimated

Discoveries - By-Product

Discoveries - Primary

Mine Production

Mt Cu

Estimate

Exploration Spend $

Unit Discovery Costs

Total Metal Found

Future Mine Production

Discovery/Prodn Ratio in 2026 1.7x

Note: By-Product metal refers to copper found in Ni, Au and Zn/Pb depositsSource: MinEx Consulting © March 2012

“in-Balance”“in-Balance”

Outlook

MinEx Consulting Strategic advice on mineral economics & exploration

Mining & discovery rates for uraniumAmount of Primary U3O8 found and mined in the World: 1950-2010

0

200

400

600

1950 1960 1970 1980 1990 2000 2010

Discoveries

World Production

Note: Chart excludes Olympic Dam (Cu-U-Au deposit) found in 1975 – contains 2545 kt U3O8

kt U3O8

Estimate

Note: Chart include minor adjustment for deposits missing from the databaseIs based on discoveries > 0.5 kt U3O8

Sources: MinEx Consulting © July 2012Production data from USGS

42

Exploration Spend $

Unit Discovery Costs

Total Metal Found

Future Mine Production

Discovery/Prodn Ratio in 2026 2.0x

“in-Balance”“in-Balance”

Outlook

MinEx Consulting Strategic advice on mineral economics & exploration

Mining & discovery rates for zincAmount of Primary Zinc found and mined in the World: 1950-2011

43

0

10

20

30

40

50

1950 1960 1970 1980 1990 2000 2010

Discoveries - Estimated

Discoveries - Known

Mine Production

Mt Zn

Estimate

Exploration Spend $

Unit Discovery Costs

Total Metal Found

Future Mine Production

Discovery/Prodn Ratio in 2026 0.7x

Sources: MinEx Consulting © Feb 2012Production data from USGS

“Major Shortfall”“Major Shortfall”

Outlook

MinEx Consulting Strategic advice on mineral economics & exploration

Mining & discovery rates for leadAmount of Primary Lead found and mined in the World: 1950-2011

44

0

10

20

30

1950 1960 1970 1980 1990 2000 2010

Discoveries - Estimated

Discoveries - Known

Mine Production

Mt Pb

Estimate

Exploration Spend $

Unit Discovery Costs

Total Metal Found

Future Mine Production

Discovery/Prodn Ratio in 2026 0.5x

Sources: MinEx Consulting © Feb 2012Production data from USGS

“Severe Shortfall”“Severe Shortfall”

Outlook

MinEx Consulting Strategic advice on mineral economics & exploration

7. CONCLUSIONS

The industry is facing a number of challenges and opportunities

45

MinEx Consulting Strategic advice on mineral economics & exploration

Conclusions: Gloom or Boom? [1/3]

1. Trends in global exploration spend– Over last decade world exploration spend rose from $2.9b to $29.4b

– Exploration spend reached an all-time high in 2012

– Due to lower commodity prices, exploration spend is forecast to drop 20% in2013, with a further 15% out to 2020

– Junior Companies facing a cash-crisis. Expect a big cut-back on “money-in-the-ground” until the situation stabilises

2. Trends in discovery rates– Over the last decade industry spend $116b (in 2012$) and found

524 significant deposits, including 86 Tier 1&2 deposits

– The are currently ten “Hot Spots” for exploration around the world.Two of those are in Africa (Central Africa and West Africa)

46

Industry has gonethrough a “boom”Industry has gonethrough a “boom”

“Industry faces severalyears of “gloom”

“Industry faces severalyears of “gloom”

Good opportunitiesstill available

Good opportunitiesstill available

MinEx Consulting Strategic advice on mineral economics & exploration

Conclusions: Gloom or Boom? [2/3]

3. Trends in discovery performance– In terms of bang-per-buck, Africa was the best Region. Over the last decade

it accounted for 14% of global spend and found 22% of the deposits.

– Even though non-ferrous spending in the Western world rose by x8 over thelast decade, the discovery rate only rose ~3x. This was due to a doubling inthe cost of drilling, staff and admin. Industry is also having to exploreunder deeper cover.

4. Trends in the types of exploration methods used– Varies by commodity, scale and depth of cover. Even so, brownfields

exploration (i.e. “nearology”) and geophysics are becoming much moreimportant.

47

In terms of discovery,Africa is “the place to be”

In terms of discovery,Africa is “the place to be”

Input costs should fall in medium term. The challenge of being ableto explore under deeper cover will get more severe

Input costs should fall in medium term. The challenge of being ableto explore under deeper cover will get more severe

Innovations in geophysics, computing and drilling willhelp boost discovery performance

Innovations in geophysics, computing and drilling willhelp boost discovery performance

MinEx Consulting Strategic advice on mineral economics & exploration

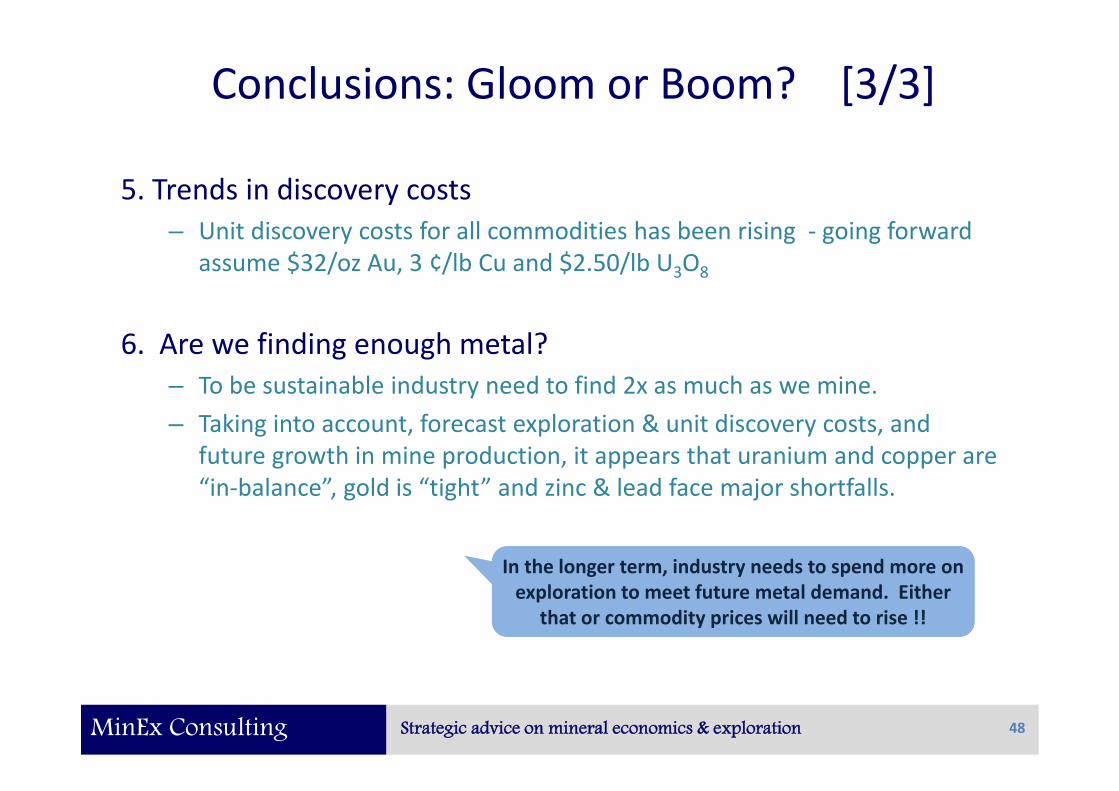

Conclusions: Gloom or Boom? [3/3]

5. Trends in discovery costs– Unit discovery costs for all commodities has been rising - going forward

assume $32/oz Au, 3 ¢/lb Cu and $2.50/lb U3O8

6. Are we finding enough metal?– To be sustainable industry need to find 2x as much as we mine.

– Taking into account, forecast exploration & unit discovery costs, andfuture growth in mine production, it appears that uranium and copper are“in-balance”, gold is “tight” and zinc & lead face major shortfalls.

48

In the longer term, industry needs to spend more onexploration to meet future metal demand. Either

that or commodity prices will need to rise !!

In the longer term, industry needs to spend more onexploration to meet future metal demand. Either

that or commodity prices will need to rise !!

MinEx Consulting Strategic advice on mineral economics & exploration 49

Contact details

Richard SchoddeManaging DirectorMinEx ConsultingMelbourne, Australia

Email: [email protected]: MinExConsulting.com

Copies of this and other similarpresentations can be downloaded

from my website

Copies of this and other similarpresentations can be downloaded

from my website

MinEx Consulting Strategic advice on mineral economics & exploration

APPENDIX – ESTIMATED FUTURE MINEPRODUCTION AND DISCOVERY RATES

Background data for assessing the sustainability of the mining industry

50

MinEx Consulting Strategic advice on mineral economics & exploration

How much metal do we need to find ?

51

To ensure no supply interruptions in the longer term the industryneeds to be finding at least 2x as much metal as it currently minesTo ensure no supply interruptions in the longer term the industry

needs to be finding at least 2x as much metal as it currently mines

MinEx Consulting Strategic advice on mineral economics & exploration

Estimated Discovery/Production ratios

Gold Copper Uranium

Unit discovery costs ~$32/oz ~3 c/lb ~$2.50/lb

World exploration spend rate(2012 US$m pa)

[A] = $5100m[P] = $9980m[F] = $4400m

[A] = $2280m[P] = $4870m[F] = $2800m

[A] = $680m[P] = $1110m[F] = $1500m

Expected amount of metal tobe found [F] = 138 Moz [F] = 42 Mt [F] = 270 kt

Mine Production(in 15 years time)

2011 = 84 Moz2026 = 95 Moz

2011 = 16 Mt2026 = 25 Mt

2011 = 64 kt2026 = 133 kt

Discovery/Production Ratios [F] [F] [F]

At 2011 Production Rate 1.6x 2.6x 4.2x

At 2026 Production Rate 1.5x 1.7x 2.0x

52

Target is >2xTarget is >2x

Source: MinEx Consulting © July 2013

[A] = Average exploration spending rate over last decade (2003-12)[P] = Peak exploration spending rate (in the last decade)[F] = Forecast spend in 2020, based on June 2013 Consensus Economics commodity price forecast

MinEx Consulting Strategic advice on mineral economics & exploration

Estimated Discovery/Production ratiosZinc Lead Comments

Unit discovery costs ~3 USc/lb Actually refers to Zn-eq

World exploration spendrate (2012 US$m pa)

[A] = $650m[P] = $1040m[F] = $1100m

Assumes that FSU+China makeup 15% of total world spend

Expected amount of metalto be found [F] = 12.2 Mt [F] = 2.7 Mt

Assumes that the Zn-eq is madeup of 67% zinc, 16% lead and17% other by-product credits

Mine Production 2011 = 12.4 Mt2026 = 16.7 Mt

2011 = 4.5 Mt2026 = 5.2 Mt

Assumes 2% & 1% pa growth

Discovery/ProductionRatios

[F] [F]

At 2011 Production Rate 1.0x 0.6x

At 2026 Production Rate 0.7x 0.5x Target is > 2x

53

[A] = Average exploration spending rate over last decade (2003-12)[P] = Peak exploration spending rate (in the last decade)[F] = Forecast spend in 2020, based on June 2013 Consensus Economics commodity price forecast

Required for industryto be sustainable

Required for industryto be sustainable

Source: MinEx Consulting © July 2013