Download - M&a Lessons- Sanjay Bakshi

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 1/91

16 lessons i learnt

about M&A

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 2/91

Lesson # 1:

Most acquisitions will fail to

beat aaa bond yield

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 3/91

Wealth Destruction on a Massive Scale? A Study of Acquiring-Firm ...

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 4/91

“The sad fact is that most major

acquisitions display an egregious

imbalance: They are a bonanza

for the shareholders of theacquiree

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 5/91

“they increase the income and

status of the acquirer's

management; and they are a

honey pot for the investmentbankers and other professionals

on both sides

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 6/91

“But, alas, they usually reduce the

wealth of the acquirer's

shareholders, often to a

substantial extent. That happensbecause the acquirer typically gives

up more intrinsic value than it

receives.”

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 7/91

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 8/91

For this amount today, RBS

could buy:

Citibank $22.5bn,

Morgan Stanley $10.5bn,

Goldman Sachs $21.0bn,Merrill Lynch $12.3bn,

Deutsche Bank $13.0bn and

Barclays $12.7bn,

And still have $8bnchange !

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 9/91

Lesson # 2:

Don’t forget diseconomies of

scale

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 10/91

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 11/91

Lesson # 3:

be wary of people with “grand

visions”

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 12/91

No corporate planningdepartment actively

looking for acquisitions

reliance on serendipity

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 13/91

“We have no view of the future that dictates what business or industries wewill enter. Indeed, we think it's usually

poison for a corporate giant'sshareholders if it embarks upon new ventures pursuant to some grand vision.

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 14/91

“We prefer instead to focus on the economic characteristics of businesses that we wish to ownand the personal characteristics of managers withwhom we wish to associate - and then hope we

get lucky in finding the two in combination.”

SERENDIPITY

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 15/91

“Even so, we do have a few advantages, perhapsthe greatest being that we don't have a strategic

plan. Thus we feel no need to proceed in anordained direction (a course leading almost

invariably to silly purchase prices) but can instead simply decide what makes sense for our owners.

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 16/91

“In doing that, we always mentally compare any move we are contemplating with dozens of other opportunities open to us, including the purchase

of small pieces of the best businesses in theworld via the stock market.

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 17/91

“Our practice of making this comparison of acquisitions against passive investments is adiscipline that managers focused simply on

expansion seldom use.”

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 18/91

Lesson # 4:

low price can offset

advantages of control

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 19/91

“The Competitive nature ofM&A activity almost

guarantees the payment of afull - frequently more thanfull - price when 100% of a

company changes hands.

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 20/91

“But, less than 100% of thesame company can frequentlytrade in the stock market at

deep discounts to prices they

would command in negotiatedtransactions involving theentire business.

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 21/91

Why?

In the auction-like natureof the stock market, prices

are set by individuals andgroups of individuals whoare frequently irrational,

resulting in irrational

prices

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 22/91

“Our favorite acquisition is thenegotiated transaction that

allows us to purchase 100% of

such a business at a fair price.

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 23/91

“But we are almost as happywhen the stock market offersus the chance to buy a modestpercentage of an outstanding

business at a pro-rata pricewell below what it would taketo buy 100%.

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 24/91

“Advantage of buying non-controlling blocks atbargain prices, often

counterbalances thedisadvantage, if any, fromthe lack of control.”

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 25/91

Lesson # 5:

great businesses rarely make

great acquisitions

there are exceptions

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 26/91

More often than not,buying poor performers

with plenty of room for

improvement is a betterstrategy

Restructuring Potential

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 27/91

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 28/91

Lesson # 6:

don’t get over-impressed by

high replacement cost

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 29/91

http://en.wikipedia.org/wiki/Tobin's_q

Tobin’s Q

Is it worth replacing?

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 30/91

Lesson # 7:

be extremely wary of open bid

auctions

Envy + DSRS + Authority + Dopamine + Incentive-caused

bias + Overconfidence + Social Proof + Low Contrast =

Winners’ Curse

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 31/91

Buffett Does not engage inbidding contests.

“The smarter side to take in a biddingwar is often the losing side.”

Knows when to walk away from a deal

Usage of time fuse on bids

breakup fee

co-relation with stock marketshutdown

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 32/91

Lesson # 8:

acquiring to diversify is

generally a bad idea.

there are exceptions e.g. when

you get deals that others

won’t

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 33/91

Buffett on

Scott-Fetzer

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 34/91

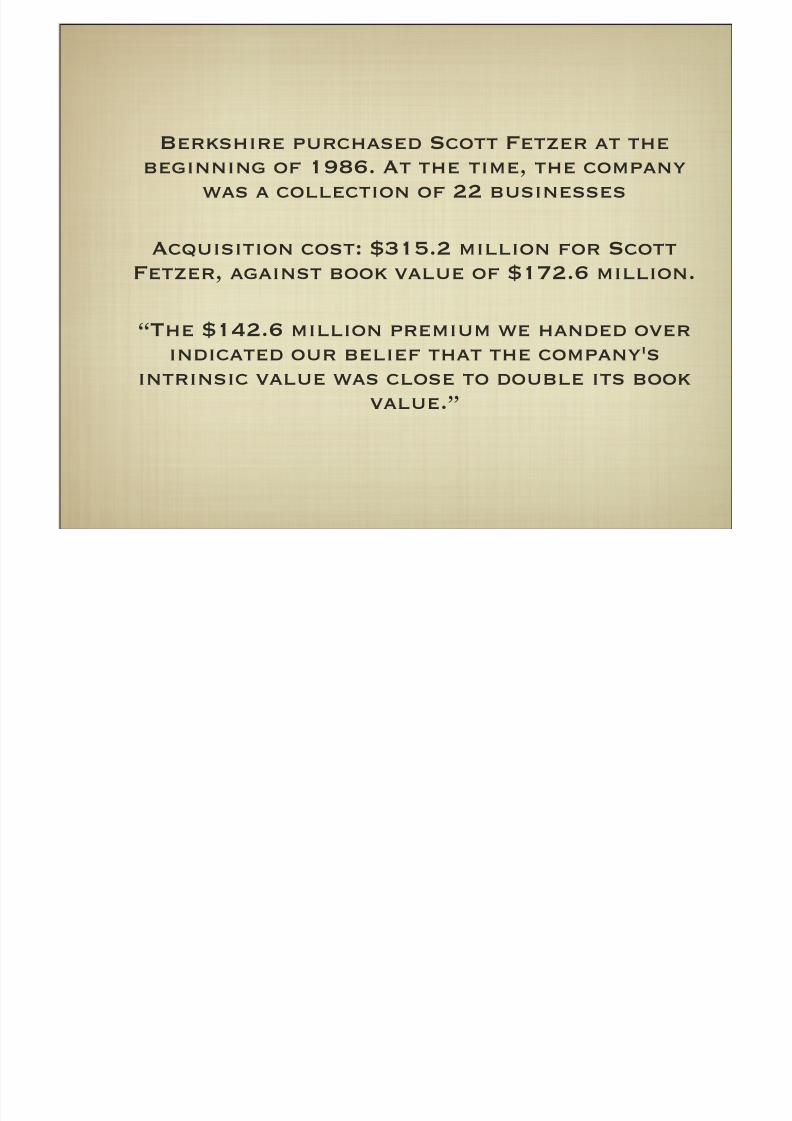

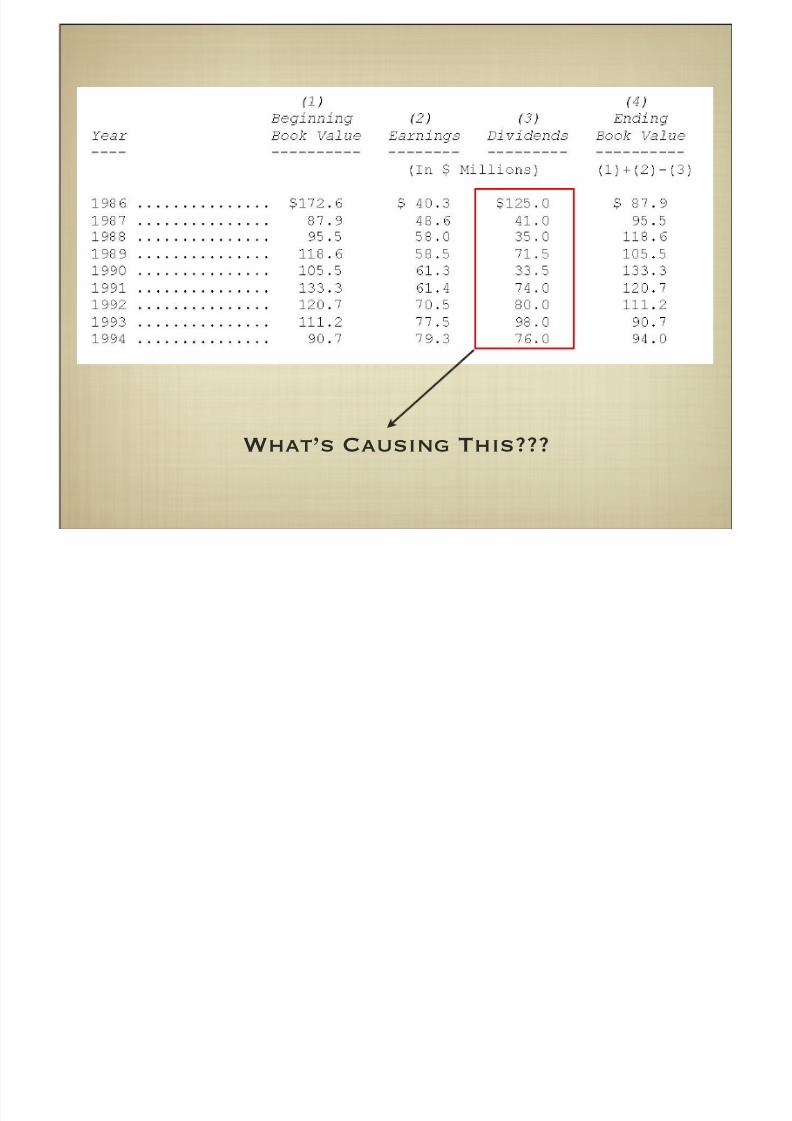

Berkshire purchased Scott Fetzer at thebeginning of 1986. At the time, the company

was a collection of 22 businesses

Acquisition cost: $315.2 million for Scott

Fetzer, against book value of $172.6 million.

“The $142.6 million premium we handed over

indicated our belief that the company's

intrinsic value was close to double its book

value.”

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 35/91

What’s Causing This???

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 36/91

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 37/91

The Math Behind Swap Ratios

3 key factors:

A.Prospects

B.Mix of Operating and Non operating assets

C.capital structure

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 38/91

Lesson # 10:

Don’t ask a barber if you needa haircut

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 39/91

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 40/91

Lesson # 11:

Price is what you pay (now)

value is what you get (later)

Or

Beware of “Synergy Trap”

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 41/91

Net valueadded =

Total Value

Received -Total Value

Paid

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 42/91

ValueReceived =

Stand alone

value +synergy

value

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 43/91

Value paid =target’s pre-

acquisition

market value+ control

premium

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 44/91

nva= synergy

value -

controlpremium

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 45/91

“Synergy: a term widelyused in business to

explain an acquisition

that otherwise makes nosense.”

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 46/91

Ways to Create value

for buyers

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 47/91

1. Find cheap targets

and buy them for a

song

unrealistic

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 48/91

2. ensure synergy exceedscontrol premium

control premium is a fact

synergy is an estimate

enter social psychology

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 49/91

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 50/91

3. buy relative value

Pay for anacquisition using a

relatively over-

priced currency

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 51/91

Using/Misusing Stock

as a Currency

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 52/91

4. Expropriate minoritystockholders

Overpay for acquiring a

partial stake and thenexpropriate value from

minority shareholders and

creditors of the target

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 53/91

Lesson # 12:

be wary of “serial acquirers”

who use stock as currency

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 54/91

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 55/91

The Story of Able, Baker, and Charlie

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 56/91

Lesson # 13:

don’t forget dilution

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 57/91

“In a trade, what you are giving

is just as important as what you

are getting. This remains true

even when the final tally on

what is being given is delayed.

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 58/91

“Subsequent sales of common stock or

convertible issues, either to complete

the financing for a deal or to restore

balance sheet strength, must be fully

counted in evaluating the fundamental

mathematics of the original acquisition.

(If corporate pregnancy is going to be

the consequence of corporate mating,

the time to face that fact is before the

moment of ecstasy.)”

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 59/91

Lesson # 14:

there is no such person as an

“independent valuer”

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 60/91

Lesson # 15:

remember cash flow

shenanigans using m&a

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 61/91

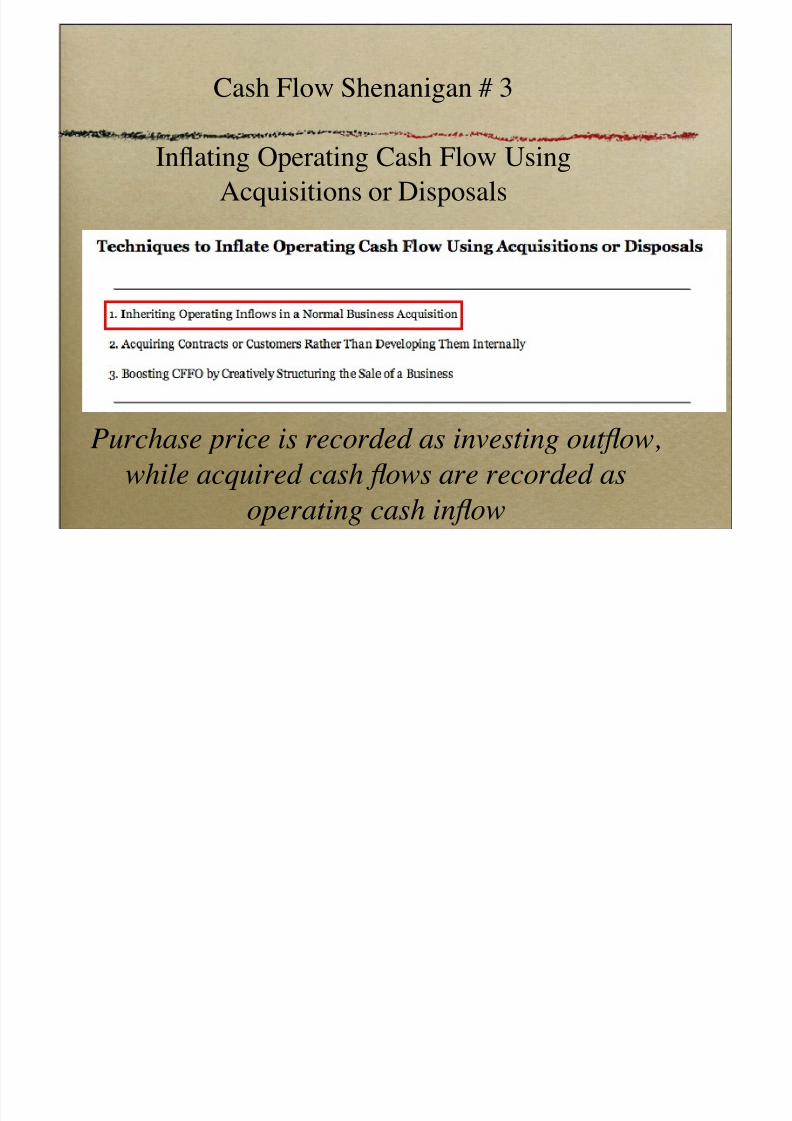

Cash Flow Shenanigan # 3

Inflating Operating Cash Flow Using

Acquisitions or Disposals

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 62/91

Cash Flow Shenanigan # 3

Inflating Operating Cash Flow Using

Acquisitions or Disposals

Purchase price is recorded as investing outflow,

while acquired cash flows are recorded as

operating cash inflow

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 63/91

¥85 million split into ¥45 sale proceeds and ¥40

million as “advance on future revenue”

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 64/91

Lesson # 16:

accounting goodwill is not the

same as economic goodwill

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 65/91

cases in M&A

Case on Gesco

Carol Loomis on AOL-Time Warner Merger

Carol Loomis on Carly Fiorina, Sandy Weill,

and others

Warren Buffett on M&A

Ajay Piramal on M&A

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 66/91

Case on Ajay Piramal

Piramal Enterprises, atextile company,

founded in 1933.

1984: acquired Gujarat

Glass.

1988: Acquired

Nicholas Laboratories

Name changed to

Nicholas Piramal India

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 67/91

Case on Ajay Piramal

1991: Merged GujaratGlass into Nicholas

Piramal

1993: Acquired Roche

Products

1995: Acquired Sumitra

Pharmaceutical

1997: Acquired

Boehringer Mannhiem

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 68/91

Case on Ajay Piramal

1998: Merger ofNicholas Piramal,

Roche Products &

Boehringer Mannhiem

2002: Acquired Rhone-poulenc

2004: Spun off Gujarat

Glass

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 69/91

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 70/91

Rs 5,400 invested in 1998

has become approximately

Rs 11 lacs

Return of 28% p.a.

Sensex Return: 17%

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 71/91

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 72/91

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 73/91

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 74/91

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 75/91

Ajay Piramal on

M&A

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 76/91

Building Global Critical Care business

J 2005 PHL

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 77/91

January 2005, PHL

acquired the

Inhalation

Anaesthetics business

of Rhodia for Rs 58

cr.

revenues of Rs 71 cr

in FY06.

So the acquisitionprice was 0.8 times

sales.

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 78/91

“With this

acquisition, we have

become a dominant

global player in

Halothane and have

gained a significant

entry in the

Isoflurane market,

besides gainingaccess to the

business marketing

and distribution

network in over 90

countries.”- Ajay

Piramal, Fy06letter to

shareholders

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 79/91

“We

successfullyshifted

production of

Inhalation

Anesthetic

products from

Rhodia UK

facilities to our

plant at Digwal,

Hyderabad.”- FY

07 letter

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 80/91

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 81/91

March 2009:

Acquired Minrad

and Rx Elite

Minrad was

acquired for $40

mil and RxElite

for $7 mil.

Stockholders of

Minrad were

bought out at

just $0.12 per

share.

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 82/91

March 2009:

Acquired Minrad

and Rx Elite

Minrad was

acquired for $40

mil and RxElite

for $7 mil.

Stockholders of

Minrad were

bought out at

just $0.12 per

share.

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 83/91

2009: Acquired

Heamaccel Brandfor $ 12 mil

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 84/91

These three

acquisitions cost

a total of $59

mil

(approximately

Rs 271 cr.)

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 85/91

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 86/91

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 87/91

April 2010:

Acquired Bharat

Serum’s

Anesthetic

Product

Business

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 88/91

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 89/91

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 90/91

8/3/2019 M&a Lessons- Sanjay Bakshi

http://slidepdf.com/reader/full/ma-lessons-sanjay-bakshi 91/91

Thank you