Managing HFAs’ Financial Health in the Face of UncertaintyNCSHA Annual Conference

October 21, 2014Ping Hsieh, Vice President – Senior Analyst

2NCSHA, October 2014

Rebounding from the Financial Crisis

• Positive trend continues with strong financial matrices amid deleveraging

• Better positioned to address variable rate risks

• More diversified business model

• Profitability is central to our credit analysis but Mortgage Interest Income to General Expense Ratio is also important

3NCSHA, October 2014

Profitability and Equity Are Growing

Source: Moody’s adjusted audited state HFA financial statements

4NCSHA, October 2014

HFAs Are Better Positioned To Address Potential Variable Rate Challenges

Source: HFA Surveys

5NCSHA, October 2014

Increasing Spread Between Mortgage Income and Bond Costs Increases Profitability

Source: Moody’s adjusted audited state HFA financial statements

6NCSHA, October 2014

Mortgage Funding Shifted From Bonds To TBA

Source: HFA Surveys

7NCSHA, October 2014

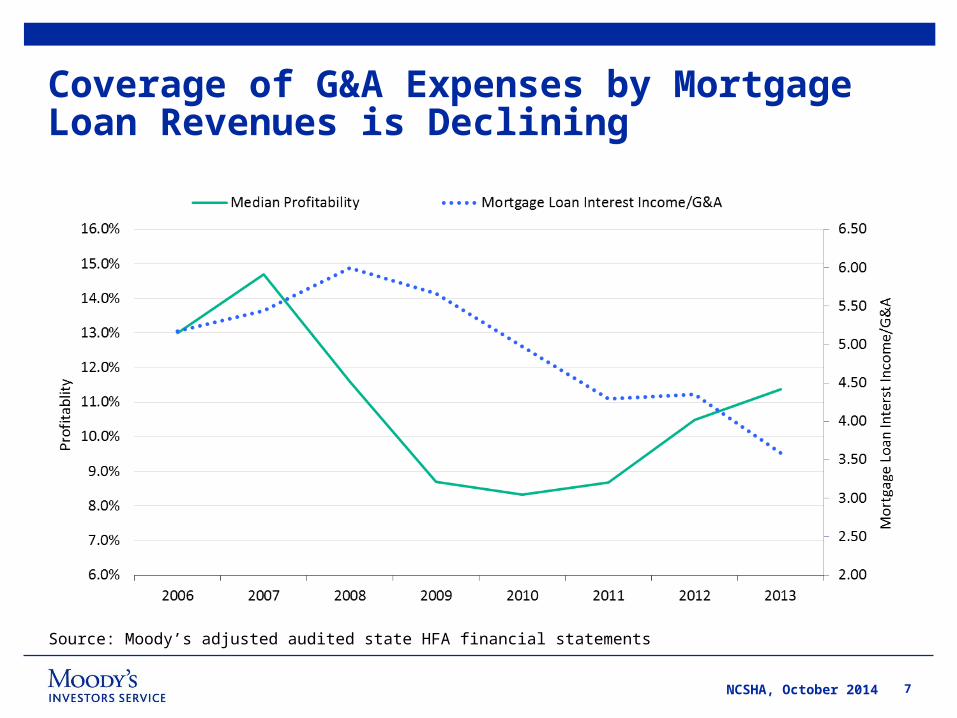

Coverage of G&A Expenses by Mortgage Loan Revenues is Declining

Source: Moody’s adjusted audited state HFA financial statements

8NCSHA, October 2014

Ping HsiehVice President – Senior Analyst [email protected] (212) 553-4461

Florence ZemanAssociate Managing Director [email protected](212) 553-4836

Kendra SmithManaging Director [email protected] (212) 553-4807

9NCSHA, October 2014