Marketing of agricultural products in rainfed regions

P Parthasarathy RaoPrincipal ScientistGT-IMPI, ICRISAT

Key note address at the 23rd National Conference on Agricultural Marketing, CRIDA, Hyderabad

12th November, 20091

Importance of rainfed agriculture, India

65% of cultivated area80% of oilseeds, pulses, and coarse cereals production75% cotton, and 50% fruits and vegetables production50% of large ruminant and poultry populationMore than 50% of small ruminant population50% of human population and the incidence of poverty is relatively high

2

Agricultural growth and poverty reduction

There is a close correspondence between agricultural growth and poverty reductionThe transmission mechanisms include:Higher rural incomesCheaper foodOpportunities in non-farm sectorShift from primary crops to allied sectors

Markets are vital for the transmission mechanisms to bring about poverty reduction

3

Importance of markets:Markets and agricultural productivity

Not only do HYVs and inputs (fertilizer, irrigation) increase agricultural productivity, but market density, well-connected road networks, and other infrastructure also promote aggregate agricultural productivity

Free trade across regions within a country also contributes to higher aggregate agricultural productivity. For example, the elimination of Food Zones in India

Continued…

4

Markets and agricultural productivityRegions/sub-regions with good market access have higher productivity per unit of land compared to areas with poor market access

Higher productivity is due toDiversified cropping patternsBetter access to inputsBetter informed cropping and marketing decisions

Thus, investments in markets, related infrastructure, and removal of trade restrictions would enhance agricultural productivity over space and time

5

6

Traditional market characteristics

Localized and thin Smallholder dominated– low individual marketed surplusesPrice discovery process often times is non-transparentPrice is a function of instantaneous demand and supplyMulti-level with many intermediaries; high transaction / marketing costsInterlinked markets (credit/input and output markets)Lack of storage facilitiesQuality specification not standardized / lack of gradingLack of information on market intelligence

Distress sales, high transaction costs,& low prices

Post harvest losses of food commodities

Type of food commodity

Proportion lost of production (%)

Monetary value of loss (Rs. in crores)

Durables (cereals, pulses, etc)

10 23,000

Semi-perishables (potato, onion, etc)

15 1,800

Perishables (fruits, vegetables, milk, etc)

20 63,000

Total 14.8 87,800

Losses occur at various stages including marketing, storage, and transportationSource: Kachru ???

7

Low level of processing in perishables

Product Organized(%)

Unorganized(%)

Total(%)

Fruits & Vegetables

1.4 0.8 2.2

Dairy products 13 22 35

Buffalo meat 21 - 21

Poultry meat 6 - 6

Marine products 8 - 8

8

Constraints to food processing

Poor capacity utilization (<50%): inadequate raw material supplyCumbersome procedures discourage the entry of potential agro-processors (20 laws; 12 ministries)High excise and sales duties on processed foodSome food commodities still reserved for the small scale sector which are unable to exploit economies of scale and have no incentive to cultivate farm-firm linkagesHigh tax incidence (15-21%) and packaging cost (12-20%) Stringent SPS measures for exports

9

Changing food basket

Rural Urban1983 2004/05 1983 2004/05

Cereals 49.5 32.8 32.9 23.8Pulses 5.8 5.8 5.8 5.3Edible oil 6.2 8.4 8.2 8.1Sugar 4.3 4.3 4.2 3.5Dairy products 11.5 15.4 15.7 18.6Meat, egg, fish 4.6 6.0 6.1 6.4Fruits & Vegetables 9.3 14.5 12.0 15.8Beverages 5.0 8.2 11.6 14.6Total HVCs 30.4 44.1 45.3 55.3Food share in total 65.6 55.0 58.7 42.5

Year

Percentage of different food types to total household expenditure

Commodity

10

Changing commodity shares in VOP

14.5

12.83.4

32.6

5.33.6

18.7

16.7

4.3

26.2

7.64.1

0%

20%

40%

60%

80%

100%

1 2

Fruits and vegetables MilkMeat FoodgrainsOilseeds Sugar

TE1981/82 TE2005-06

11

Changing context of marketsA move away from subsistence agricultureIncreasing marketed surpluses with more than half being marketedDiversification of agriculture to horticulture, livestock, fisheries, cash crops (demand driven)Niche markets (pre specified or organic products, basmati rice, vegetables)Alternative uses of coarse cereals (poultry feed , alcohol)Plough to plate linkages (Cost and quality imperatives)Emergence of supermarketsExports (gherkins, grapes)Consolidation of the processing sector

12

Factors driving changes

Population growthIncome growthIncome and price elasticity of demandUrban population growth (urbanization)Change in tastes and preferences

13

Income and animal protein consumption

y = 1.311Ln(x) - 0.1871R2 = 0.53

0

1

2

3

2.0 2.5 3.0 3.5 4.0Income per capita (US $ )

Anim

al p

rote

in

per c

apita

Data on 19 zones in India (SAT (log scale)), 200014

Global urban population projections

Source: UN, World Population Assessment 2002

0

1

2

3

4

5

6

1950 1960 1970 1980 1990 2000 2010 2020 2030

Billi

on p

eopl

e

Urban

Rural

expectedactual

35 to 40% of the population in India will live in cities by 2020

15

Urban population and poultry activityData on 19 zones in India (SAT (log scale)), 2000

y = 1.6194Ln(x) + 1.708R2 = 0.5562

0.5

1.5

2.5

3.5

4.5

0.5 1.5 2.5 3.5

Urban population (million )

Pou

ltry

activ

ity

(mill

ion

rupe

es)

16

Organized food retailing is taking off

600000

610000

620000

630000

640000

650000

2004 2005 2006

Tota

l mar

ket s

ize

(Rs.

Cr.)

2500

3500

4500

5500

6500

7500

Orga

nize

d m

arke

t (Rs

.Cr.)

Total market size Organized markets

Organized chain stores are emerging and expanding rapidly, but at present account for only about 1 percent of food sales.Retail food market estimated at $133 billion, small “Pop & Son” shops still dominate retail food sales in India

Source: Gulati (2007)

17

An efficient marketing system shouldReduce post-harvest lossesEnhance farmers’ realizationReduce consumer pricesPromote grading and food safety practicesInduce demand-driven productionEnable higher value additionFacilitate exports

Marketing is the key not only to catalyze agricultural development but to foster inclusive growth

18

Emerging commodity marketsContract farming (several models)Direct marketing (rythu bazaars, apni mandi) Cooperative marketing (milk)Bulk marketing (farmers’ associations)Forward markets / futures markets ICT enabled supply chainsSpecialized wholesalers

Horizontal and vertical integration to reduce transaction costs and improve market efficiency

19

Consumer driven supply chains

Product oriented (push) vs. market oriented (pull) supply chainsProduct oriented or consumer driven supply chains require product homogeneity, continuous deliveries, quality upgrades, large volumes

Supplying the right product, of the right quality and quantity, at the right place and right time

Such chains are successful when organized in a flexible, responsive and efficient way

20

Dynamics of coarse cereal utilizationDecline in food usePoultry sector in India expanding at 10% per annumRising demand for grains in poultry feedProspects for alternative uses (poultry and cattle feed, alcohol, ethanol etc.) on the increase in recent yearsSmall and scattered production, low productivity, poor quality and lack of assured supplies may constraint non-food industrial uses Link production with processors through innovative supply chains

How to link supply with demand centers?

Common paradox: Buyers complain of inadequate supply while farmers complain of lack of markets

21

Efficiency of coarse grain marketing chain

Questions1. Does the regulated marketing system for coarse cereals

represent a constraint on increased utilization of the crop as a food grain?

2. Could the regulated marketing system constrain utilization with prospect of much increased demand for from industry (starch, feed, alcohol, etc)

Answers1. No evidence that food grain utilization is compromised by

regulated marketing system2. Some capacity for expansion given existing marketing

arrangements, However as industrial demand increases, marketing system will have to change: new institutions linking producers will be required.

22

Plough to plate interventions

Past Interventions

Improved Cultivars

Production technology

Increase in Yield

Bulk marketing

Better prices Reduced MKTcosts

Input linkage

Output linkage

Credit linkage

Improved seeds and production technology

Increase in yield

Quality standards

Crop and warehouse loans

Cheaper capital

Cash need after harvest

23

Farmer 1

Farmer 2 Farmer 3

Bulk marketing: Innovation in production-supply chain

24

Farmers Federation

Bulking and grading

Poultry feed manufacturers

Input linkage

Farmers Associations/

groups

Credit linkages

Warehouse/Community storage structure

Poultry producers

Poultry Federation

Crop Research institutes

Poultry nutrition

Fruits, vegetables, and livestock productsThere are common characteristics that link the marketing of livestock products (milk, meat), fruits, and vegetables. These are Highly perishableProduction located close to demand centers (urban orperi-urban areas) (milk is an exception)Very dependant on basic infrastructure (roads, cold storage, packaging), implying that diffusion to remote areas is not viableSeasonal fluctuations in prices

25

Contract farming for perishablesPerishable markets are transforming from an open to vertical coordinated structures, like cooperatives, producers’ associations and contract farmingMain advantage of contract farming, is an assured access to market and pricesFirms provide quality inputs, technology, extension service and credit to producers and thus contribute to improving production efficiency.

26

Contract farming: Vegetables

SAFAL (now MDFVL)- an integrated supply chain(i) to cater to the growing demand for fruits and vegetables in Delhi Metro, and (ii) adequate returns to producers.

The chain is depicted here:

Farmers - Producers’ Associations - SAFAL complex -SAFAL retail outlets - Consumers

Encourages farmers to form associations forHighly perishable commoditiesLess perishable commodities

27

Economics of contract spinach productionContract Independent %

differenceYield (t/ha) 8.6 8.3 4.0

Production cost (Rs/t) 1,485 1,630 -8.9Transaction and marketing cost (Rs/t)

35 437 -92

Total cost (Rs/t) 1,520 2,067 -26.5

Price (Rs/t) 3,311 3,074 7.7

Net revenue (Rs/t) 1,791 1,007 77.9

Source: PS Birthal et al 200528

PoultryMarkets for poultry are better organized but the number of intermediaries is largePrices of broilers and eggs are largely determined by market forces. There is considerable seasonality in demand for poultry products, and their prices fluctuate considerablySmall scale poultry production is becoming unviableContract forming has emerged in a big way, providing an assured market and returns to the small-scale producers

29

Contract farming in broiler production

Contract Independent % difference

Marketing cost (Rs/t)

38 90 58

Net revenue (Rs/t) 2,255 2,003 13

CV across production cycles (%)

3.4 69.5

40% broiler production is under contract with Tamil Nadu, AndhraPradesh, Karnataka and Maharashtra as the leading states

Source: PS Birthal et al 200530

31

05

1015202530354045

1-Jan

1-Feb

1-Mar

1-Apr

1-May

1-Jun 1-Jul

1-Aug

1-Sep

1-Oct

1-Nov

1-Dec

Rs/kg

Sharing price riskBroiler prices

MilkNearly 45 per cent of the milk produced in country is marketedMilk, in India, is largely consumed as raw milk (about 60 % of output) Two-third of market surplus is sold in informal markets and rest through cooperatives and private sectors.Vendors and milk dealers dominate the informal market. Vendors operate on small scale.Only 15 per cent of the milk output is commercially processed.

Continued..

32

Economics of contract milk production

Contract Independent % difference

Milk yield (kg) 11.9 11.4 4.4

Production cost (Rs/t)

5,586 5,782 -2.5

Marketing cost (Rs/t)

100 1,442 -93.1

Total cost (Rs/t) 5,686 7,170 -20.7

Price (Rs/t) 9,337 8,991 3.8

Net revenue (Rs/t) 3,651 1,821 100.5

Source: PS Birthal et al 200533

Milk (dairy cooperatives)

Gujarat, Maharashtra, Karnataka and TamilNadu account for two-third of the milk procured by cooperatives The share of these states in total milk production in the country is only about 25 per cent.In most other states, cooperatives procure less than 5 per cent of milk output like UP, Punjab and Haryana, here private sector has a sizable presence in milk market

34

Contract farming – some issues

Contract farming is partnership oriented not transaction oriented

Economic rationale alone would sustain such models in the long-term. This could be through

Higher productivity and better value realization for farmers and sponsor

Lower overall risk for farmers and sponsor

Good communication and trust building

35

Markets for live animals

Live animalsMarkets not well developed.- Segmented, thin and irregular markets, - Lack of associated activities like housing for animals, and basic facilities Considerable proportion of live animals are exchanged amongst livestock producers, between producers and itinerary traders Data on prices and numbers transacted not recordedDirect sale to slaughter houses and butchers

36

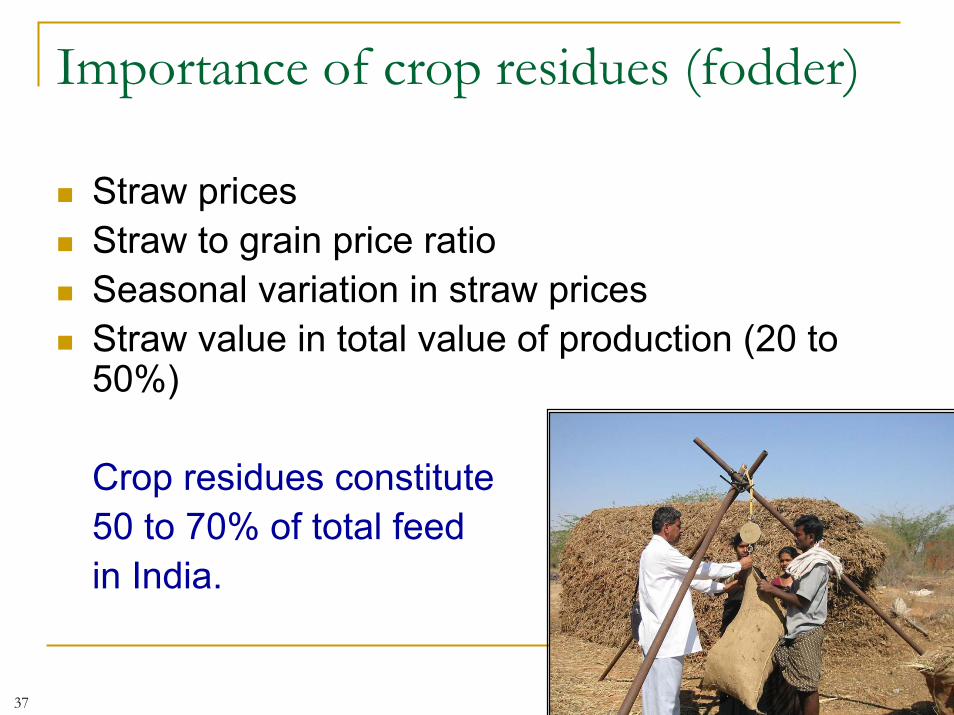

Importance of crop residues (fodder)

Straw pricesStraw to grain price ratio Seasonal variation in straw prices Straw value in total value of production (20 to 50%)

Crop residues constitute50 to 70% of total feed in India.

37

Feed and fodder marketsLivestock revolution driving fodder / feed demandFeed prices raising faster than milk and meat product prices Considerable seasonal fluctuations and regional variation in fodder prices Thin markets for grasses and forage crops Markets for crop residues -- informal and located in urban centers

38

Share of straw/stover in total

76.00

56.16

42.80

28.31 25.49

83.15

0

10

20

30

40

50

60

70

80

90

Gumalkunta Jalalpuram

Paddy Sorghum Groundnut

Data from Anantapur village

Anantapur dist. Village survey39

Flow of paddy straw, Anantapur district

40

Coastal districts

Sorghum stover marketing: HyderabadSorghum fodder arrivals to Hyderabad takes one the following channels:Un-chopped sorghum stover coming from a distance of 50-100 km on carts and from 100-150 km on lorries and sold in informal fodder markets located in 3-4 places through middlemen. Chopped sorghum fodder in lorry loads from 400-500 km.The chain that is followed is commission agent –trader- diary owners/ retailers

41

Upgrading livestock and fodder markets

Bring the existing markets under a proper regulatory frameworkImprove facilities related to infrastructure, animal feed and healthBring transparency in transactionsEstablish a few model markets for further replicationMaintain records of transactions (prices, animal characteristics, etc.)Establish rural meat production centresRegulate the slaughterhouses

42

Scaling upScaling up of emerging market linkages should be possible if political, institutional, legal, and regulatory environment are market orientedPolicy initiatives under agricultural marketing

Model Marketing Act 2003Agmarknet portalInternet connectivity between wholesale marketsConstruction of rural warehousesStrengthening marketing infrastructure, grading and standardizationSFAC venture capital

43

Model Marketing Act, India, 2003Key additions and improvements:Setting up of new markets by private or other parties Separate markets for special commoditiesDirect marketing by farmers to agro-processors Provision for contract farming Futures or forward marketing Prohibition of commission agency in transactions with producersFormation of Farmers’ Associations for bulk marketingPledge financing and instituting a system of negotiable warehouse receiptsEnsuring complete transparency in the pricing system and transactions Providing market-led extension services to farmers

Continued…

44

Model Marketing Act, India, 2003Dissemination of market intelligence information (arrivals and prices data) Promote public–private partnerships in the management of agricultural marketsWider role of State Marketing Boards in training & extension in market related areasConstitution of Standards Bureau at State levelMarket committees are permitted to establish required infrastructure facilities in market yards using their fundsImposition of single-point levy of market fee on the sale of notified agricultural commodities in any market area

Several states amending marketing acts to include provisions of Model Marketing Act

45

Role of governmentBuilding efficient marketing networks

Implement Model Marketing ActDismantling government monopoly

Increasing investments in infrastructureRoads, cold storage, bulk coolersFoster improved linkages between rural-urban markets

Setting up information kiosks on prices, arrivals, quality standards, etcPromoting horizontal and vertical integration through innovative institutional linkages

Harness private sector innovations in food marketingEstablish effective mechanisms for dispute settlement

Continued…

46

Role of government

Adding value through processingSimplify procedures for setting up food processing industries Reduction in excise on processed food products duties

Incentives to agro-processing industry to strengthen backward and forward linkages

Market fee, taxes on processed foods Enhancing access to formal credit

Enhancing access to formal credit and insuranceEnabling public-private partnershipsEstablishment of Agricultural Exports Zones

47

48

Thank you!

Thank you!

Smallholders are a big deal

56.0

19.3

22.8

10.5

62.8

17.8

18.1

7.4

69.7

16.3

13.2

5.0

0%

20%

40%

60%

80%

100%

1981/82 1991/92 2002/03

Upto 1.0ha 1-2 ha 2-4 ha Above 4haN

umbe

r

11.5

16.6

23.6

48.3

15.6

18.7

24.1

41.6

22.6

20.9

22.5

34.0

0%10%20%30%40%50%60%70%80%90%

100%

1981/82 1991/92 2002/03

Are

a

49

Contract farming - Definition and models“Contract Farming" means farming by a person called "Contract Farming Producer" (farmer or association of farmers) under a written agreement with another person called "Contract Farming Sponsor" to the effect that his farm produce shall be purchased as specified in the agreement

Various models possible:Centralized modelNucleus estate modelMulti-partite modelInformal or individual developed modelIntermediary model

Source: Eton & Shepherd, FAO 2001

50

Model Marketing Act, India, 2003

In 2000 Ministry of agriculture appointed an Expert Committee and an Inter Ministerial Task Force to review the present system of agricultural marketing and recommend measures to make the system more efficient and competitive.

A Standing Committee of State Ministers was constituted to review the recommendations in January 2003.

The committee finalized the draft model legislation titled the State Agricultural Produce Marketing (Development and Regulation) Act, 2003.

51

Enabling policy environment‘Operation Flood’ initiated in 1970 by the NDDB to provide market access to the producer through cooperativesDairy industry de-licensed in 1991 Milk and Milk Products Order enacted in 1992 to regulate the production and maintain the quality of milk and milk productsThe import of dairy products was de-canalized during 1994 under WTO regimeLicensing procedures have been simplified. Quantitative restrictions (QRs) on all dairy products removed from April 2001In 2002 removed restrictions on setting up the new capacity Other reforms - Creation of export promotion zones - Reduction in tariffs and custom duties on

machinery etc

52

Contract farming -models

Centralized model

Sponsor purchases crop, processes it and markets the productDistribution of production quotaQuality tightly monitored

Examples in India

Practised in sugar, gherkin, bought-leaf factories in teaAppachi Cotton

53

Contract farming -models

Nucleus estate model

Sponsor demonstrates through his own operationsTransfer technology and management to ‘satellite’ growers

Examples in India

Stevia,& medicinal plants, grapes for wine

54

Contract farming -models

Multi-partite modelJoint participation of farmers, sponsors and statutory bodies

Examples in IndiaPunjab Agro-Industries Corporation Limited – UBL in barley

55

Contract farming -models

Informal or individual developed model

Individual or small companies make informal short term contracts on a seasonal basisBulk of contract farming in the Indian context follows this

Examples in IndiaFood World – for fruits and vegetablesTomato purchase by individual or small companies inBangaloreTinna Oil on soybean

56

Contract farming -models

Intermediary model

Sponsor is not in direct contract with farmers but in association of farmers

Examples in IndiaKASAM – NGO in Phulbani, Orissa on Turmeric

57

Poultry Production

Small-scale poultry production is becoming unviable due to high production and market risks

Reduce feed costs through technology/alternative feeds/price interventionsReduce production risks by imparting skills to the producers for better managementIntegration of small poultry with agriculture production of millets in rainfed areasEncourage contract farming/cooperatives/producers’associations for risk sharing Poultry activity should be appropriately placed either as an industrial or agricultural activity

58

Broiler and Egg Marketing

Producers are exploited by intermediaries in the supply chain. Seasonal fluctuation in prices also act against the producers.

Increase competition in the domestic marketVertical integration through contract farming Horizontal integration of producers Standardization and grading of produceInfrastructure for reducing losses, better price management and value addition NECC should improve its coverage Create a web-site for dissemination of information on prices, production and quality

59

Export markets

At present India’s trade in livestock products is miniscule, but is growing

Check import threats through suitable fiscal and regulatory measuresIdentify a few value added products with niche markets for exports and chart out a road mapImprove efficiency in production and processing to improve competitivenessExplore new markets and quality standards required by importing countriesExplore possibilities for organic production and exports

60