Download - Mega Trends Impact on Urban Logistics presented at eyefortransport's 3PL Summit- North America

1 NA99-13

Global Mega Trends and Implications to Urban Logistics

Sandeep Kar

Global Director- Commercial Vehicle Research

2 NA99-13

1. Urbanization 2. Connectivity and

Convergence

4. Future Infrastructure

Development

There Will be 35 Mega

Cities Globally By 2025

Demanding For Unique

City Logistics Solutions

By 2025, each person will

have a minimum of five

connected devices

By 2025, 20% of retail will

happen through online

channels

By 2025, globally over

$800 billion will be spent on

high speed rail projects.

What does this mean for Urban Logistics?

500 million deliveries per

person per day to cities

‘On-the-fly’ deliveries will

have to made anywhere,

anyhow, faster and

quicker

Demand for urban parcel

deliveries will increase –

shipments to become

smaller and frequent

Multi-modal, low carbon

footprint, mission critical

utilization of road, rail,

marine, and air

infrastructure

3. Bricks & Clicks

Source: United Nations, Department of Economic and Social Affairs, Population Division

(2012). World Urbanization Prospects: The 2011 Revision , Frost & Sullivan, 2012

Mega Trends Driving Urban Logistics Industry

3 NA99-13

Urbanization Trends Influencing Urban Logistics Development of Mega Cities, Mega Regions, Mega Corridors, and Mega Slums to Drive Demand for

Logistics Services in Urban Areas

MEGA REGIONS

Cities combining with

suburbs to form regions

(Population of over 15

million) (21 Mega Regions

in 2025)

EXAMPLE: National capital

region of Delhi (includes

New Delhi, Noida, Greater

Noida, Ghaziabad,

Gurgaon, Faridabad)

MEGA

CORRIDORS

The corridors connecting

two major cities or Mega

Regions (60 km or more

apart, and with a

combined population of 25

million or more) (37 Mega

Corridors in 2025

EXAMPLE: Guangzhou-

Shenzhen-Hong Kong

Corridor

MEGA CITY

City with a minimum

population of 8 million and

a GDP of $250 billion in

2025 (12 Mega Cities in

2011 and 35 Mega Cities in

2025)

EXAMPLE: Greater Tokyo

(Population of over 27

million by 2025)

MEGA SLUMS

1 billion urban poor live in

an area measuring just 1.5

square miles

Source: Frost & Sullivan Analysis. Image Source: Dreamstime

Urbanization Trends, Global, 2011–2025

4 NA99-13

The Future of Urban Distribution The Hub-and-Spoke Logistics Model In Urban Environment Will Feature Mega Size Warehouses on Outskirts of

Cities, with Smaller Decentralized Warehouses Inside the City Perimeter

The Spokes: Drop off delivery points for

double-trailer trucks

Heavy commercial

vehicles (double-

trailer trucks) will carry

goods to big warehouses

at outskirts

Macro to Micro Implications

The Hub: Central Distribution Centers

• All trucks to operate at 80%–

100% capacity (load factor)

• New technologies in tracking

deliveries, such as track and

trace, RFID in warehouses to

evolve

• New business models, such as

in-night services, special

delivery, and self-collection

points, to grow in popularity

• ~50% reduction in trucks going

in and out of cities

• Ensures “on-time delivery” for

retailers

Medium and

light CVs will

deliver goods to

warehouses within

city

Outer Ring Road

~ 25 miles from

City Center

Source: Frost & Sullivan Analysis.

Illustration of Global Urban Distribution in 2025

5 NA99-13

Multimodal Trends Influencing Urban Logistics Road and Rail Accounted for Nearly 60% of Total Domestic Freight Traffic in Large Trading Regions, Such as

EU and US in 2010

Modal Split of Domestic Freight, % (Million tonne per km), Global, 2010

Source: Eurostat, US Bureau of Transportation Statistics

29%

31%

12%

8%

Road Rail Water Air

49%

10%

38%

0%

Road Rail Water Air

Modal Split of Domestic Freight, United States, %

(Million tonne per km), 2010

Modal Split of Domestic Freight, EU-27, % (Million

tonne per km), 2010

6 NA99-13

Multimodal Trends Influencing Urban Logistics — High Speed Rail High-speed Rail To Improve Logistics By Freeing Up Space For Freight and Offering Exclusive High-speed

Logistics Solutions

Source: Frost & Sullivan Analysis

Freeing up space for freight on road

and standard rail tracks as more

people move to high-speed mobility

High-speed freight trains that

transport cargo exclusively at the

same service cost as air, but at lesser

carbon cost

High-speed Mobility High-speed Logistics

• Congestion zones, low

emission zones

• Multimodal access point

• Reliable and convenient

• Reduction in delay and

commutation time

• Transport up to 300 km/h

in some countries

• Night time transportation:

no non-peak hours

restrictions

• Short transport time and

lesser truck trips

• Green in comparison to

planes

Impact of High-speed Rail on Logistics, Global

Image Source: Dreamstime

7 NA99-13

Connectivity Trends Influencing Urban Logistics — Location-based

Services (LBS) Over 40% of the connected devices globally will be LBS enabled by 2020

2011

Non-LBS Devices

5.58 Billion

Non-

Internet

Users

Total: 6.00 Billion

Connected Devices

LBS Devices

0.42 Billion

(7% of total)

LBS Devices

35.20 Billion

(44% of total)

2020

Total: 80.00 Billion

Connected Devices

Source: Frost & Sullivan

Subscriber Forecast of LBS Devices, Global, 2011 and 2020

Non-LBS Devices

44.80 Billion

• Navigation services will continue to drive growth in this market

• Core navigation features include voice-guided turn-by-turn directions with updated maps, 3D moving maps, and automatic rerouting for missed turns

• Enhanced features include integration with contacts; multiple route capability; real-time traffic; gas prices and weather information; voice recognition for address input; traffic-optimized routing; intelligent navigation rerouting and updated estimated time of arrival based on current traffic flow, among others

8 NA99-13

Bricks and Clicks: Growth in Online Retail to 2025 Global Online Retail Sales To Reach $4.3 Trillion By 2025 Accounting for 19% of Total Retail

Source: Frost & Sullivan analysis.

1.320 1.300

0.210 0.170 0.090

0

0.2

0.4

0.6

0.8

1

1.2

1.4

United States China UnitedKingdom

Japan Germany

$11.8 Trillion

$23.0Trillion

Retail Market

Size

Retail Market

Size

$0.550

Trillion

$11.250

Trillion

$4.300

Trillion

$18.700

Trillion

24% 18%

26% 10%

15%

5%

19%

2011 2025 Online Retail Top Markets, 2025

Online Sales Non-Online Sales % share of online in

total retail

1 2 3 4 5

9 NA99-13

Bricks and Clicks: Impact of Bricks and Clicks on Store Formats Retail Formats Are Becoming Smaller and Unique With More Emphasis Being Placed on the Concept and

Urban Location of the Store

0

20000

40000

60000

80000

100000

120000

140000

Pre-1970s 1970s 1980s 1990s 2000 2010 2011 2012

Av

era

ge S

tore

Siz

e (

Sq

ft)

Grocery

Stores

Convenience

Stores

Supermarkets

Club

Warehouses

Hypermarkets

Concept Stores

Express Stores

Store Format Average

Size

Grocery Store: Small market for

basic groceries

8,000

Convenience Store: A small

store selling basic items and

over-the-counter medicines

10,000

Supermarket: Large-size grocery

and basic items

80,000

Club Warehouse: Large store

selling only bulk quantities (e.g.

Sam’s Club)

100,000

Hypermarket: Large stores

combining a supermarket and a

department store (e.g., Carrefour

in UK; Wal-Mart Supercenter in

United States)

120,000

Concept Stores: Small- to

medium-sized manufacturer

stores (e.g., Apple)

50,000

Express Store: Small

convenience stores (e.g., Wal-

Mart Express)

12,000

Era of Expansion Era of Contraction

Source: RetailNet and Frost & Sullivan Analysis.

Evolution of Retail Formats, Global, 1970–2012

10 NA99-13

Bricks and Clicks: From Big-Box to Small Box Retailer Store Size to be 15%–20% Less than the Current Average Store Size by 2020

Size: 200,000 Sqft Size: 10,000 Sqft

Location: Semi-urban areas—less dense areas with small

populations.

Accessibility: Car drives–5 to 6 miles from city centers and urban

hubs.

Building Format: Leased/owned, large scale standalone

properties.

Shelf Capacity: 120,000 items Shelf Capacity: 12,000 items

15%–20%

smaller

Location: Urban shopping centers—a minimum of 1,000

urban population per sqkm

Accessibility: Walkable distance–2 to 3 miles from city

centers and urban hubs

Building Format: Leased small stores fit into existing city

buildings.

Big-Box Small Box

Source: Frost & Sullivan Analysis. Image Source: Dreamstime

11 NA99-13

Bricks and Clicks: New Retailing Business Models Case Study: Tesco Virtual Store Sparks New Generation of Grocery Shopping

1

2 3

4

Choose

grocery item

from “virtual

shelves”

Smartphone app registers

product of choice The product lands in

customer’s “virtual cart”

The product is

delivered to the

customer at a time

and date of his

choice

Number 1 shopping app in Korea,

with over 900,000 downloads

Online sales increased by 130%

since launch in 2011

Home plus online membership increased

by 76% since launch in 2011.

Virtual Store—The Fourth-

generation Retail Store

Virtual Store: Tesco Virtual Store Sparks New Generation of Grocery Shopping

Single virtual store opened in a subway

Source: RetailNet and Frost & Sullivan Analysis. Image Source: Tesco

12 NA99-13

Regional Distribution Center to Shop

(In-House)

Bricks (pre-2000) +Advent of Clicks (post-2000)

Source: Frost & Sullivan Analysis.

Impact of Bricks and Clicks on Logistics Evolution of Bricks and Clicks Model in Logistics

Central Distribution Center to Customer

(Packing and Last Mile Delivery Outsourced)

Bricks and Clicks (2012 and Beyond) Hub and Spoke For Faster Deliveries

(Special Delivery Options Such as Same-Day Outsourced)

E.g. Wal-Mart US E.g. Amazon US

Same-Day Night Time Robotic Warehouses Stores as DCs Locker Boxes

Each distribution

center supports 90

to 100 stores in a

200-mile radius.

Closest Central

Distribution center

identifies and sorts

product which then

packed and

delivered by UPS

Image Source: Dreamstime, Wal-Mart, Amazon and Tesco

13 NA99-13

Urban Logistics

14 NA99-13

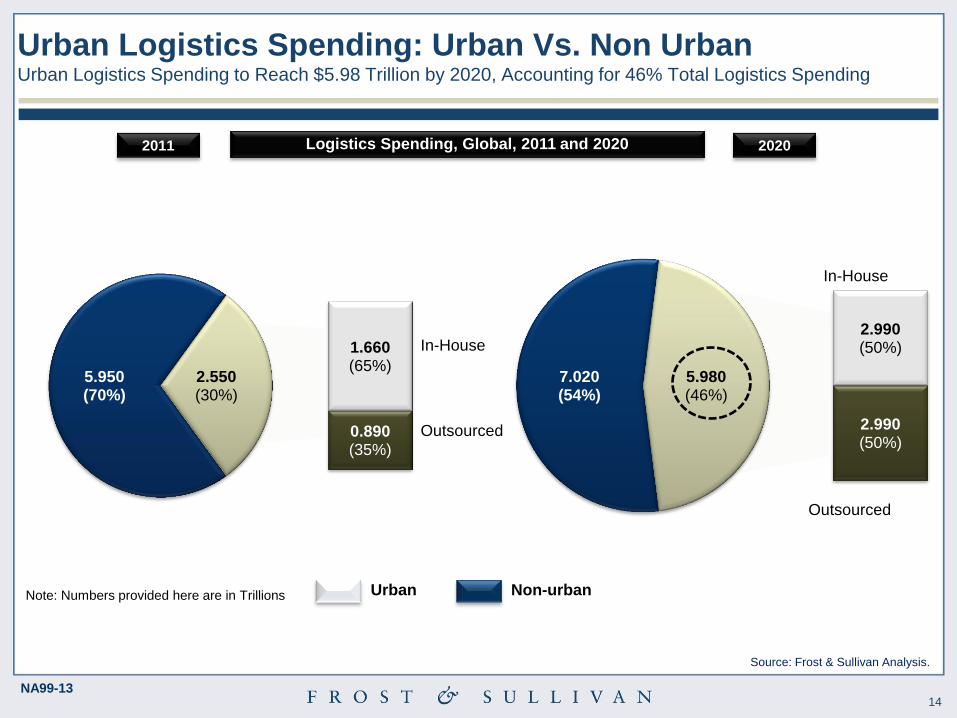

5.950 (70%)

1.660 (65%)

0.890 (35%)

2.550 (30%)

Urban Logistics Spending: Urban Vs. Non Urban Urban Logistics Spending to Reach $5.98 Trillion by 2020, Accounting for 46% Total Logistics Spending

7.020 (54%)

2.990 (50%)

2.990 (50%)

5.980 (46%)

2011 2020

In-House

Outsourced

In-House

Outsourced

Urban Non-urban

Logistics Spending, Global, 2011 and 2020

Source: Frost & Sullivan Analysis.

Note: Numbers provided here are in Trillions

15 NA99-13

Retail Pharmaceutical Food & Beverages

Smaller Stores Generic Medicines

More regulations

Chilled and Frozen

Food Industry Trend

Urban Logistics

Implication

Smaller shelf size –

need for constant

replenishment

No more

homogenous single

supply chain model

Need for Cold Supply

Chain Services

Urban Logistics

Services

Retail Consolidation

Centres Pack-to-order

Refrigerated Locker

Boxes

Top Industries Leveraging Urban Logistics Services in Future

Source: Frost & Sullivan Analysis.

16 NA99-13

$2.55

trillion

$5.98

Trillion

50% 55% Transportation & Distribution

Warehousing

Value-Added

2011 2020

2.5x Urban Logistics Spending

32%

18%

23%

22%

Urban Logistics Spending by Segments Transportation Costs will Rise and Account for Majority of Urban Logistics Costs while Warehousing Costs

Decline

17 NA99-13

Examples of Key Cities That Have Trialed City Logistics Policies: Time Windows, Vehicle Weight Restrictions, and Multimodal Initiatives Emerge As Most Popular Measures

Implemented For City Logistics Management

City Low

Emission

Zones

Time

Windows

Vehicle

Weight

Restrictions

Pricing /

Subsidies

Loading

and

unloading

zones

Special

Lanes

Urban

Consolidation

centers

Multimodal

Initiatives

London

Barcelona

Berlin

New York

Paris

Tokyo

Utrecht

Beijing

Mexico City

Mumbai

Seoul

Source: Turblog, World Bank, International Transportation Forum, MDS Transmodal Limited, Frost & Sullivan

Measures by City Authorities to Manage Urban Logistics, Global, 2005–2012

Highly Active / Implemented

18 NA99-13

Examples of Urban Logistics Business Models From LSPs* Targeted Deliveries, Hybrid Fleets, and Bundling of Consignments Emerge As Most Popular Measures

Implemented For City Logistics Management

Off-peak

Deliveries

(Night

Deliveries/

Early-morning

Deliveries)

Green

Vehicles

(Electric,

Hybrid,

Natural Gas)

Non-

conventional

modes of

Delivery

(Trams, Foot,

Bicycles)

Urban

Consolidation

centers

Locker Boxes

(Automated

Locker Boxes)

Pick-up Vans/

Outlets

(Parked Vans;

Store-pick-

ups)

Smart routing

and

Scheduling

(sensors, GPS,

telematics,

real-time

monitoring)

DHL

UPS

FedEx

TNT

Kuehne-

Nagel

DB

Schenker

*The above examples are tactics and strategies trialed/piloted by LSPs in certain cities only (mainly in Europe). These are currently not offered

in all cities as full-time services. These examples have been collated here for illustration purposes only.

Source: Frost & Sullivan Analysis.

Business Models by LSPs Targeting Urban Logistics, Global, 2005–2012

Highly Active / Implemented

19 NA99-13

Urban Logistics Trends : Trends in Urban Freight Distribution Distribution will be Shared and become more Consolidated

Deliveries to cities travel

from warehouses directly

to distribution points,

making multiple trips and

resulting in high

congestion and rising

C02 emissions in urban

areas

Consolidation centers in

cities will sort and

dispatch goods

intelligently, avoiding the

need for multiple trips

and thereby reducing

congestion and C02

levels

Without Consolidation Centers

With Consolidation Centers

Source: Frost & Sullivan Analysis.

20 NA99-13

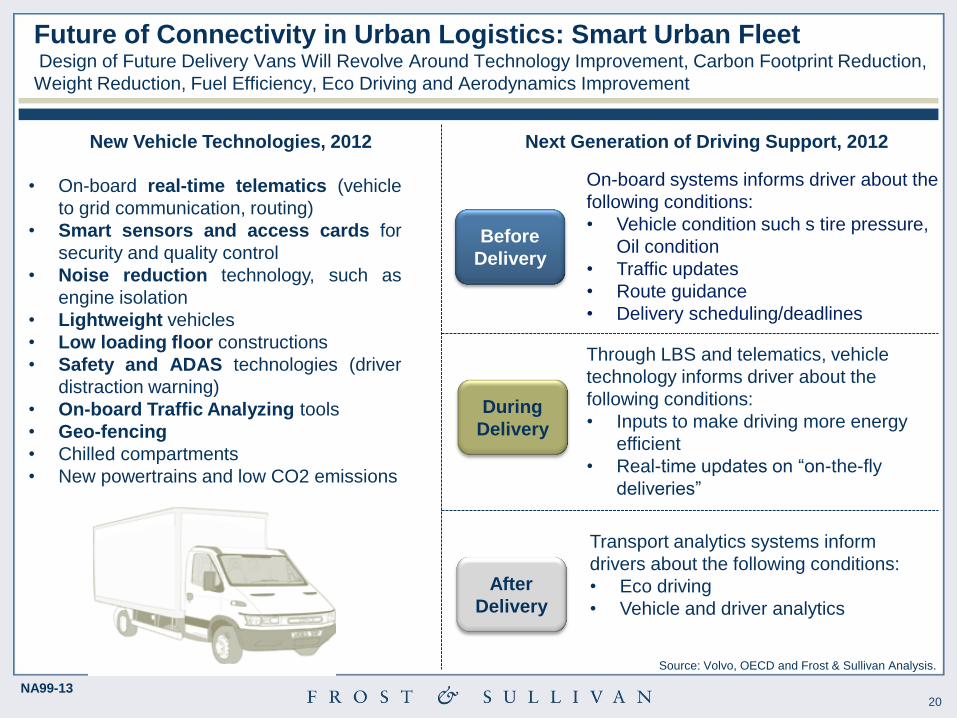

Future of Connectivity in Urban Logistics: Smart Urban Fleet Design of Future Delivery Vans Will Revolve Around Technology Improvement, Carbon Footprint Reduction,

Weight Reduction, Fuel Efficiency, Eco Driving and Aerodynamics Improvement

Before

Delivery

During

Delivery

After

Delivery

• On-board real-time telematics (vehicle

to grid communication, routing)

• Smart sensors and access cards for

security and quality control

• Noise reduction technology, such as

engine isolation

• Lightweight vehicles

• Low loading floor constructions

• Safety and ADAS technologies (driver

distraction warning)

• On-board Traffic Analyzing tools

• Geo-fencing

• Chilled compartments

• New powertrains and low CO2 emissions

New Vehicle Technologies, 2012 Next Generation of Driving Support, 2012

On-board systems informs driver about the

following conditions:

• Vehicle condition such s tire pressure,

Oil condition

• Traffic updates

• Route guidance

• Delivery scheduling/deadlines

Through LBS and telematics, vehicle

technology informs driver about the

following conditions:

• Inputs to make driving more energy

efficient

• Real-time updates on “on-the-fly

deliveries”

Transport analytics systems inform

drivers about the following conditions:

• Eco driving

• Vehicle and driver analytics

Source: Volvo, OECD and Frost & Sullivan Analysis.

21 NA99-13

A minimum of 500 Million deliveries per day will be made within cities by 2025.

Urban logistics spending will more than double to

$5.98 Trillion over the next decade, with

transport and distribution activities accounting for

the majority of the cost.

So What ?

Over 60% of the world’s

population will live in cities

by 2025 The world will be

connected through a

network of 80 billion

connected devices by

2020

Online retail is accelerating

at an tremendous rate and

will grow to account for

nearly 20% of total retail in

2025

The parcel and express market will innovate and realign supply chains to deliver smaller and more frequent shipments in shorter time windows.

City municipalities are

encouraging the

development of intermodal

freight deliveries for

medium- to long-distance

flows

Logistics service providers will offer unique urban logistics solutions, including targeted deliveries, hybrid fleets and the bundling of consignments, smart trucks, and advanced warehouse management systems.

Governments will use ICT, including smart cards and e-tags, to enforce access restrictions to cities and to allow the use of dedicated parking/loading zones.

City governments are also

encouraging the development

and take-up of low emission

vehicles for “last-mile”

deliveries

So What?

Conclusions and Future Outlook Mega Trends, Such As Urbanization, Bricks and Clicks, and Access to Multimodality, Will Drive Demand for

Time- sensitive Deliveries Resulting in Stricter Demands Being Placed on Shippers and LSPs

Urban Logistics, Key Findings and Future Outlook, Global, 2020

Source: Frost & Sullivan Analysis.

22 NA99-13

Thank You

Sandeep Kar Global Director- Commercial Vehicle Research

Direct: +1. 416.490.7796

Fax: +1.416.490.1533

Email: [email protected]