AFRICAN DEVELOPMENT BANK ADB/BD/WP/2014/136

28 August 2014

Prepared by: ORNA/MAFO Original: French

Probable Date of Presentation to the Committee

Operations/ Development Effectiveness (CODE)

TO BE DETERMINED

FOR CONSIDERATION

MEMORANDUM

TO : THE BOARD OF DIRECTORS

FROM : Cecilia AKINTOMIDE

Secretary General

SUBJECT : MOROCCO - COMBINED 2012-2016 COUNTRY STRATEGY PAPER

MID-TERM REVIEW AND 2014 COUNTRY PORTFOLIO

PERFORMANCE REVIEW*

Please find attached the above-mentioned document.

Attch.

cc. : The President

* Questions on this document should be referred to:

Mr. J. KOLSTER Regional Director ORNA Extension 2065

Ms. Y. FAL Resident Representative MAFO Extension 7301

Mr. V. CASTEL Chief Country Economist ORNA/MAFO Extension 6572

Mr. O. BRETECHE Principal Portfolio Officer ORNA/MAFO Extension 6533

SCCD:C.H

-i-

AFRICAN DEVELOPMENT BANK

COMBINED REPORT

COUNTRY STRATEGY PAPER (2012-2016 CSP) MID-TERM REVIEW

&

2014 COUNTRY PORTFOLIO PERFORMANCE REVIEW

MOROCCO

Editorial

Team Regional Director:

Resident Representative:

Design Team:

Team Members:

J. KOLSTER, Regional Director, ORNA

Y. FAL, Resident Representative, MAFO/ORNA

V. CASTEL, Chief Country Economist, MAFO/ORNA

O. BRETECHE, Principal Portfolio Officer, MAFO/ORNA

D. CHARRIER-RACHIDI, Economist, ORNA

S. MANSOUR, Economist, ORNA

A. MOUAFFAK, Economist, ORNA

A. MOUSSA, Electrical Engineer, MAFO/ONEC

A. TARSIM, Senior Macro-economist, OSGE.1

B. BEN SASSI, Chief Water and Sanitation Expert, OWAS

C. AMBERT, Principal Strategist, OPSM

C. MOLLINEDO, Chief Strategist, COPS

D. KHIATI, Agricultural Expert, MAFO/OSAN

E. DIARRA, Principal Financial Economist, MAFO

F. RODRIGUES, Senior Investment Officer, OPSM2

L. JAAFOR-KILANI, Social Development Expert, MAFO/OSHD

L. LANNES, Principal Health Economist, OSHD.3

M. BOUZGARROU, Principal Portfolio Officer, ORNA

M. EL ARKOUBI, Procurements Officer, MAFO/ORPF.1

M. EL OUAHABI, Water and Sanitation Expert, MAFO/OWAS

M. GUEYE, Principal Education Economist, OSHD.2

M. YARO, Financial Management Regional Coordinator, ORPF.2

O. BEN ABDELKARIM, Chief Education Expert, OSHD.2

P. MORE NDONG, Senior Transport Engineer, MAFO/OITC

R. MAROUKI, Chief Agricultural Economist, OSAN

T. RAJHI, Chief Training Expert, EDRE.0

W. DAKPO, Principal Procurements Expert, ORPF.1

W. RAIS, Principal Financial Analyst, MAFO

Reviewers A. A. BA, Resident Representative, BIFO

R. KANE, Resident Representative, CMFO

M. NDONG NTAH, Resident Chief Country Economist, ORNA

S. KAMARA, Principal Portfolio Officer, DIRA/ORWA

K. EGUIDA, Principal Portfolio Officer, SNFO

C. CALVOSA, Country Risk Officer, FEMA

K. ABDERAHIM, Country Risk Officer, FEMA

K.HASSAMAL, Energy Expert, ONEC.2

uuu

AFRICAN DEVELOPMENT BANK

COMBINED REPORT

COUNTRY STRATEGY PAPER (2012-2016 CSP) MID-TERM REVIEW

AND

2014 COUNTRY PORTFOLIO PERFORMANCE REVIEW

MOROCCO

ORNA/MAFO

August 2014

Translated Document

-ii-

TABLE CONTENTS

TABLE CONTENTS ...................................................................................................................... i

LIST OF ACRONYMS ................................................................................................................. iv

CONVERSION RATES ................................................................................................................ v

FISCAL YEAR ............................................................................................................................... v

Executive Summary ........................................................................................................................ vi

I. Introduction ............................................................................................................................. 1

II Country Context and Developments ........................................................................................ 1

2.1 Political Developments ................................................................................................................. 1

2.2 Economic and Social Developments ............................................................................................. 1

III. CSP 2012-2016 Implementation and outcomes ....................................................................... 4

3.1. Country Development Context .................................................................................................... 4

3.2 Bank’s Positionning ...................................................................................................................... 5

3.3 Resource Allocation ..................................................................................................................... 5

3.4. CSP Implementation Status ......................................................................................................... 6

3.5. CSP Implementation Results ....................................................................................................... 6

3.6 Other Effects of the Strategy ........................................................................................................ 8

3.7. Implementation of Paris Declaration, Accra Agenda for Action and Busan Partnership

commitments ........................................................................................................................................... 10

IV. Country Portfolio Performance Review ........................................................................... 10

4.1 Current Portfolio ....................................................................................................................... 10

4.2 Portfolio Monitoring and Evaluation ......................................................................................... 11

4.3 PPIP Implementation Status ...................................................................................................... 13

4.4 Bank Group Performance ......................................................................................................... 13

4.5 Country Performance Outcomes Based on the Questionnaire on Portfolio Quality ................. 13

4.6 Conclusions of Meetings with Stakeholders ............................................................................... 14

4.7 Revised PPIP .............................................................................................................................. 14

V. Experience and Lessons ..................................................................................................... 14

5.1 Bank Group ............................................................................................................................... 14

5.2 Government ............................................................................................................................... 20

5.3 Partners...................................................................................................................................... 20

VI. Conclusion and Recommendations .................................................................................... 20

6.1 Summary of Conclusions ........................................................................................................... 20

6.2 Key Recommendations .............................................................................................................. 20

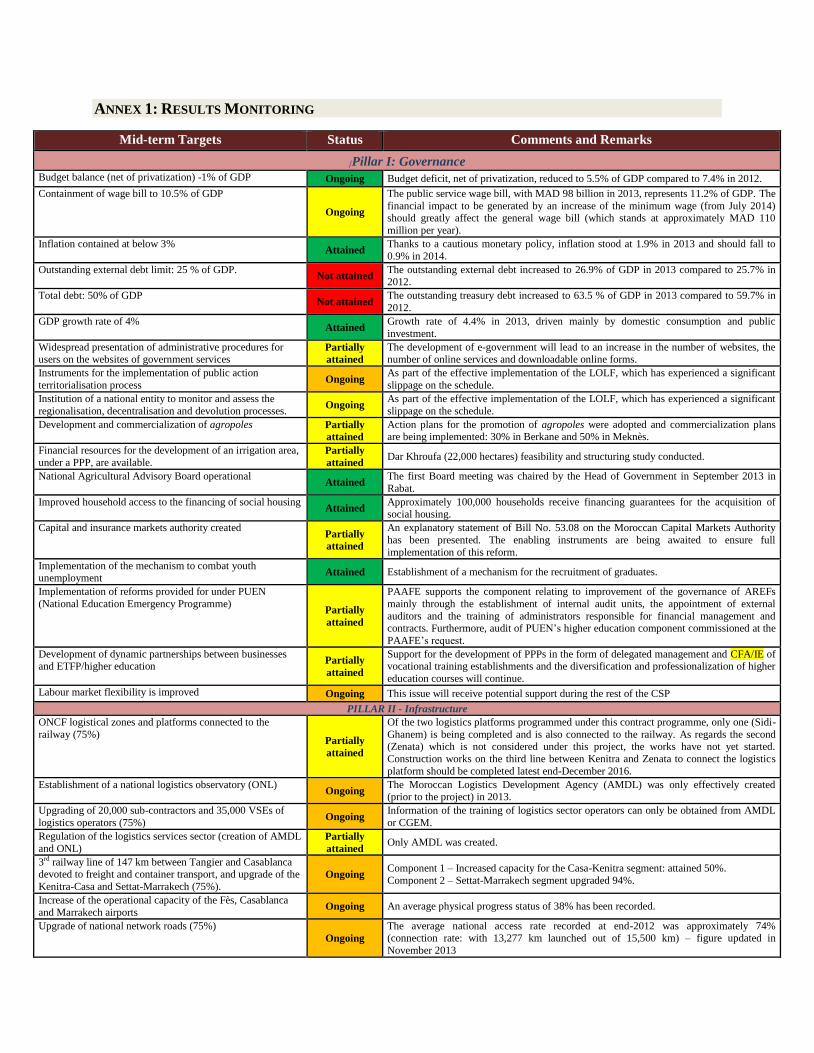

Annex 1: Results Monitoring ...................................................................................................... 21

Annex 2: Implementation of the 2012-2013 Lending Programme ............................................ 23

Annex 3: Potential Lending Programme (2014-2016) and Scenarios ..................................... 25

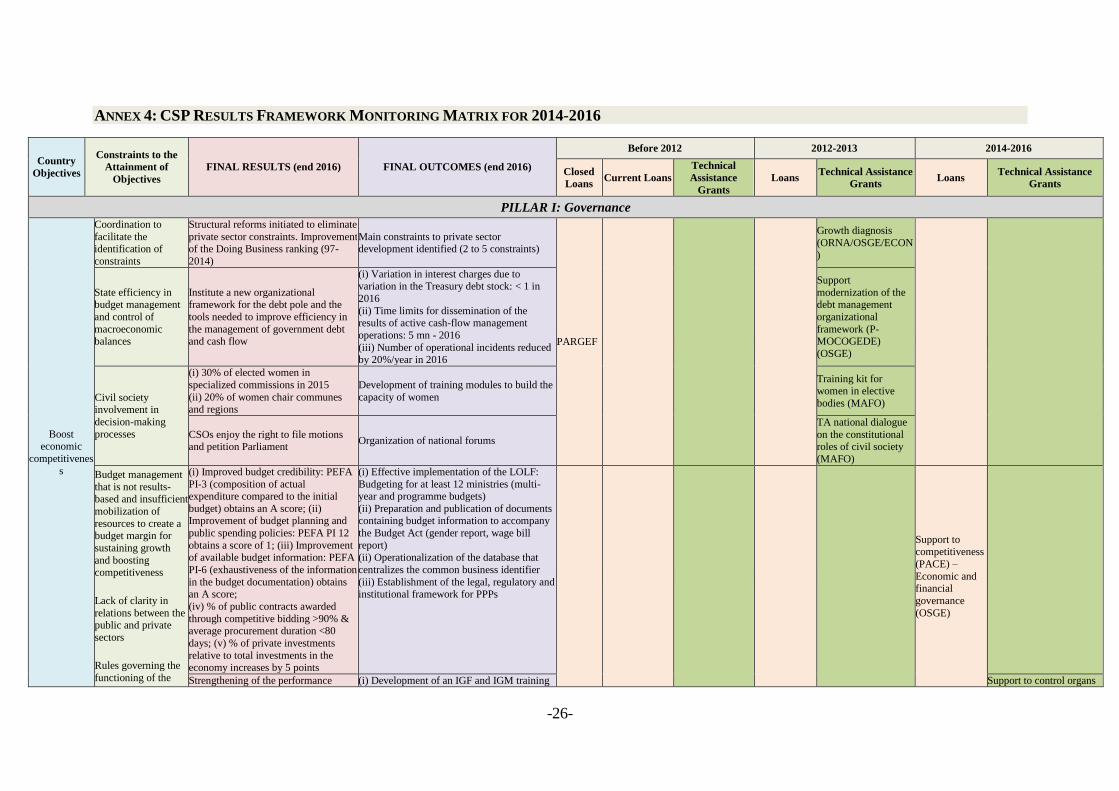

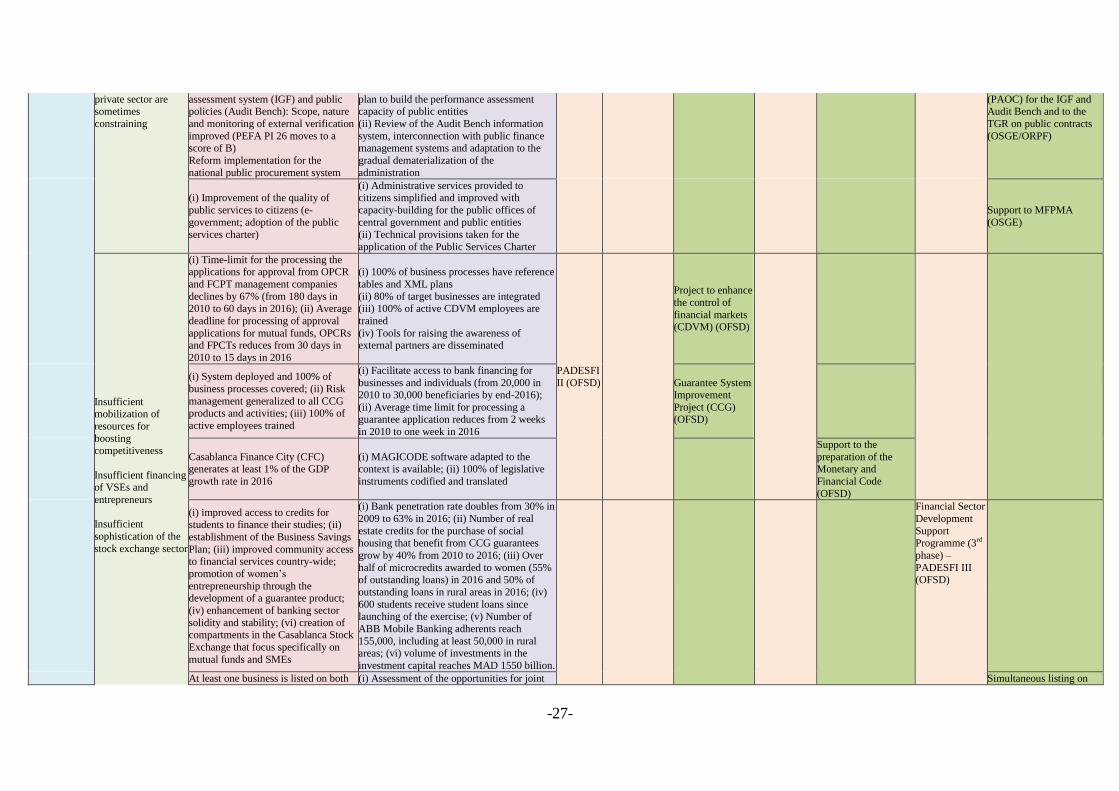

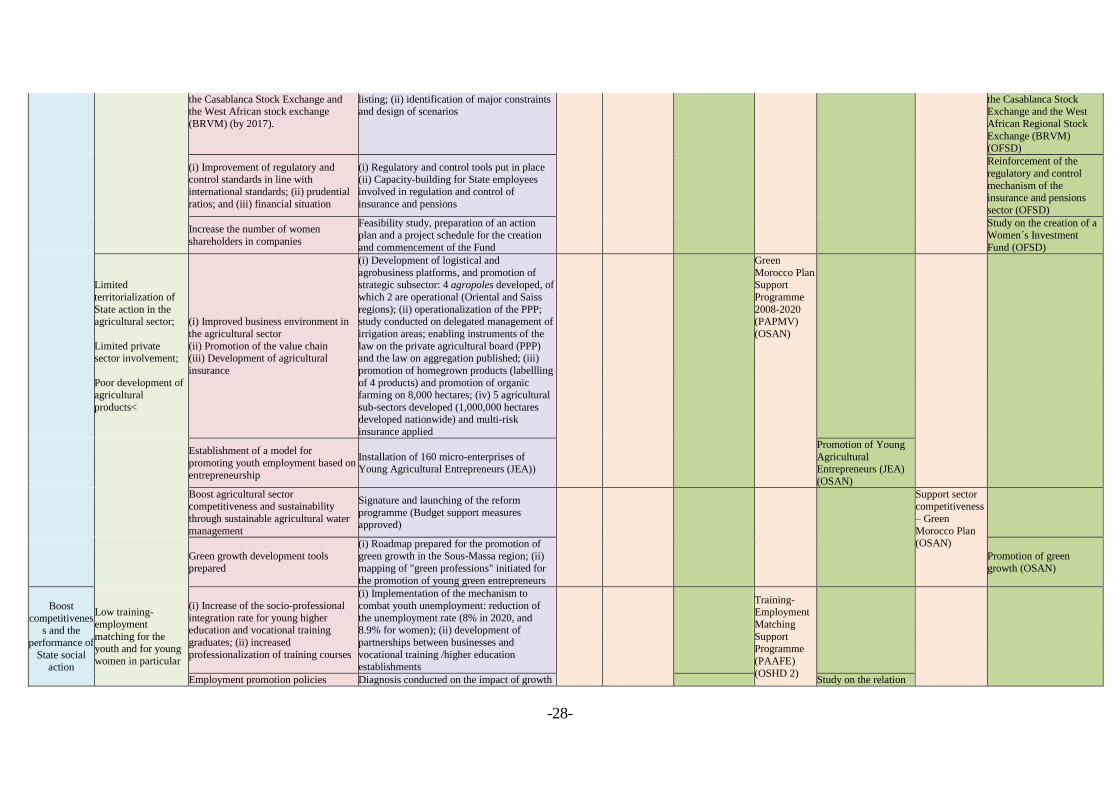

Annex 4: CSP Results Framework Monitoring Matrix for 2014-2016 ................................... 26

Annex 5: Key Social Indicators .................................................................................................... 34

Annex 6 : Key data on Ongoing Bank Group Portfolioo Operations as at 30 June 2014 ........ 35

Annex 7: Scoring of the Indicators of Public Window Active Projects in 2014 ........................ 36

-iii-

Annex 8: Monitoring of Development Progress and Results ................................................... 37

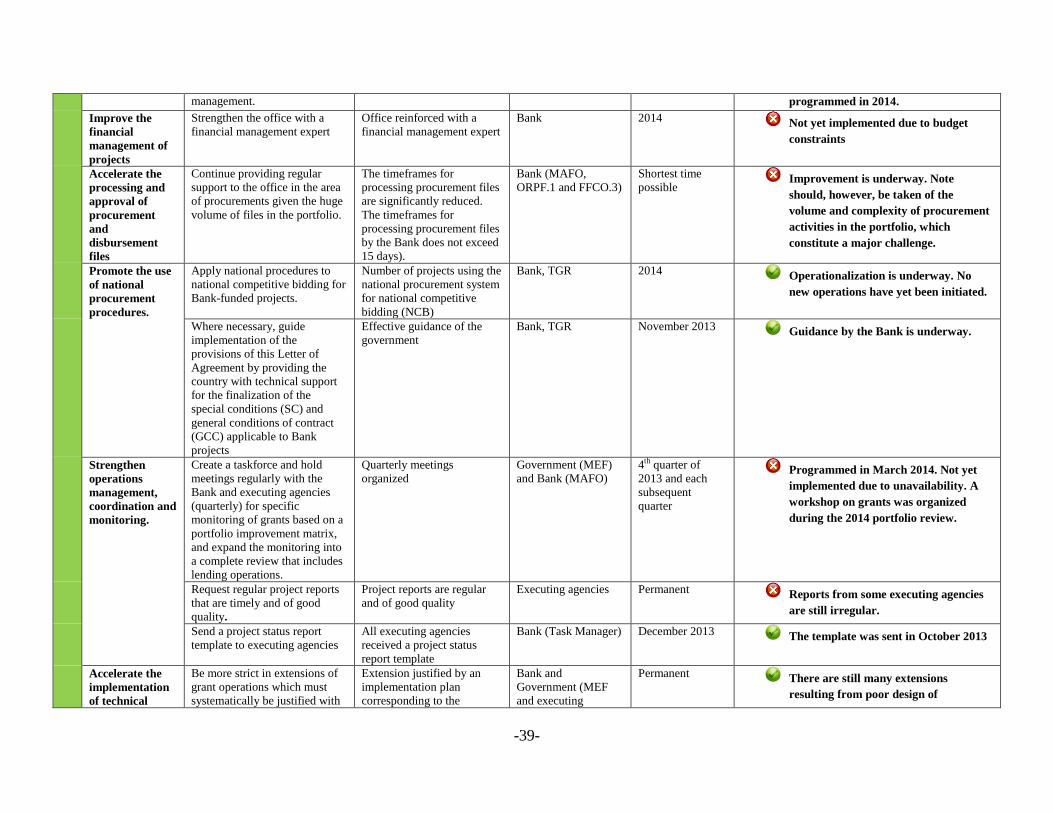

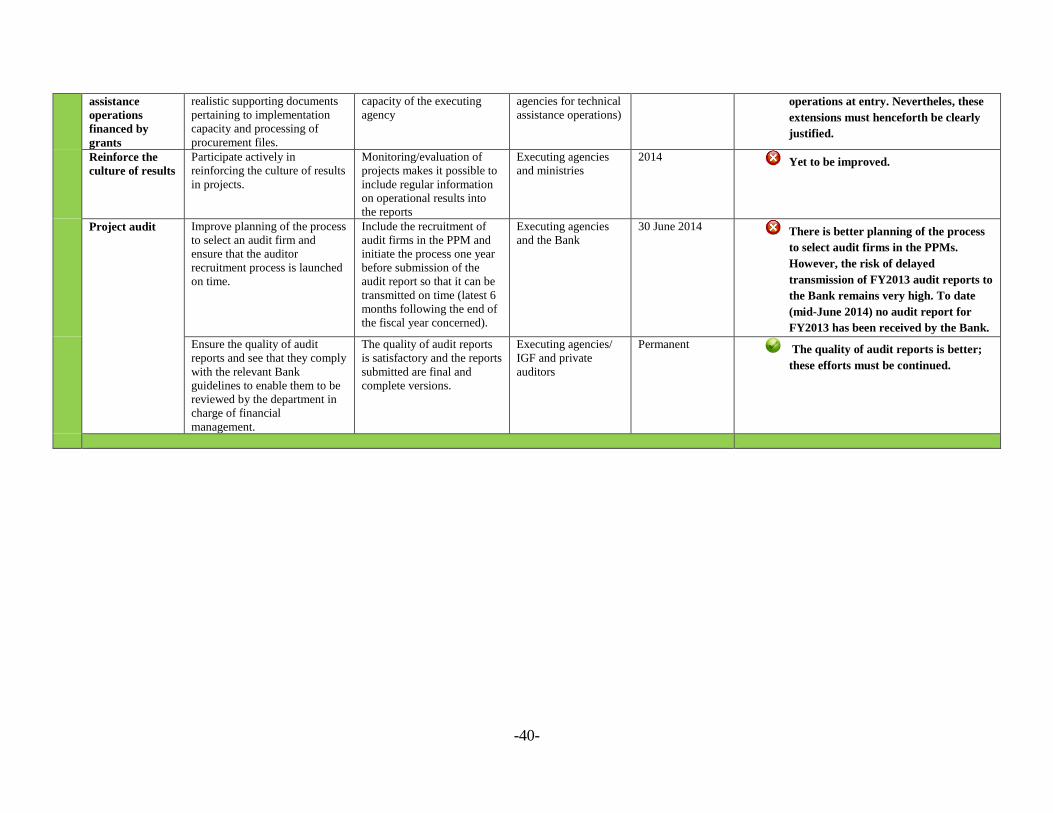

Annex 9: Implementation Status of the Country Portfolio Performance Improvement Plan

2013 ................................................................................................................................................ 38

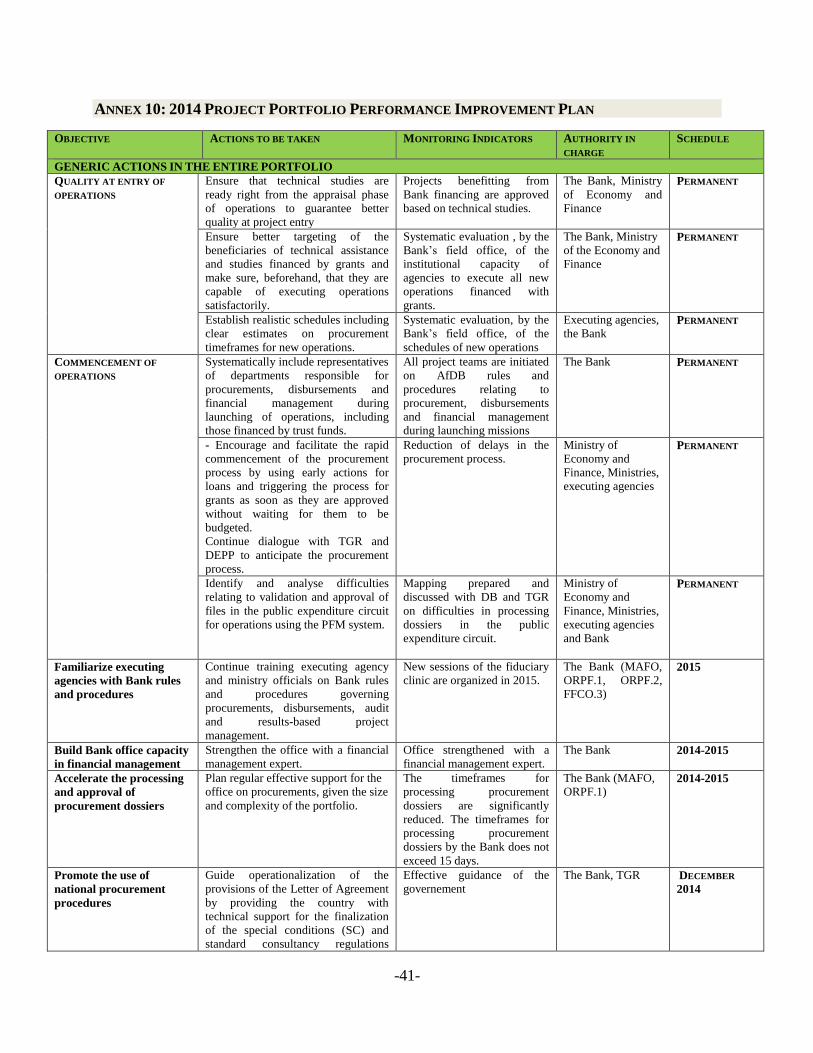

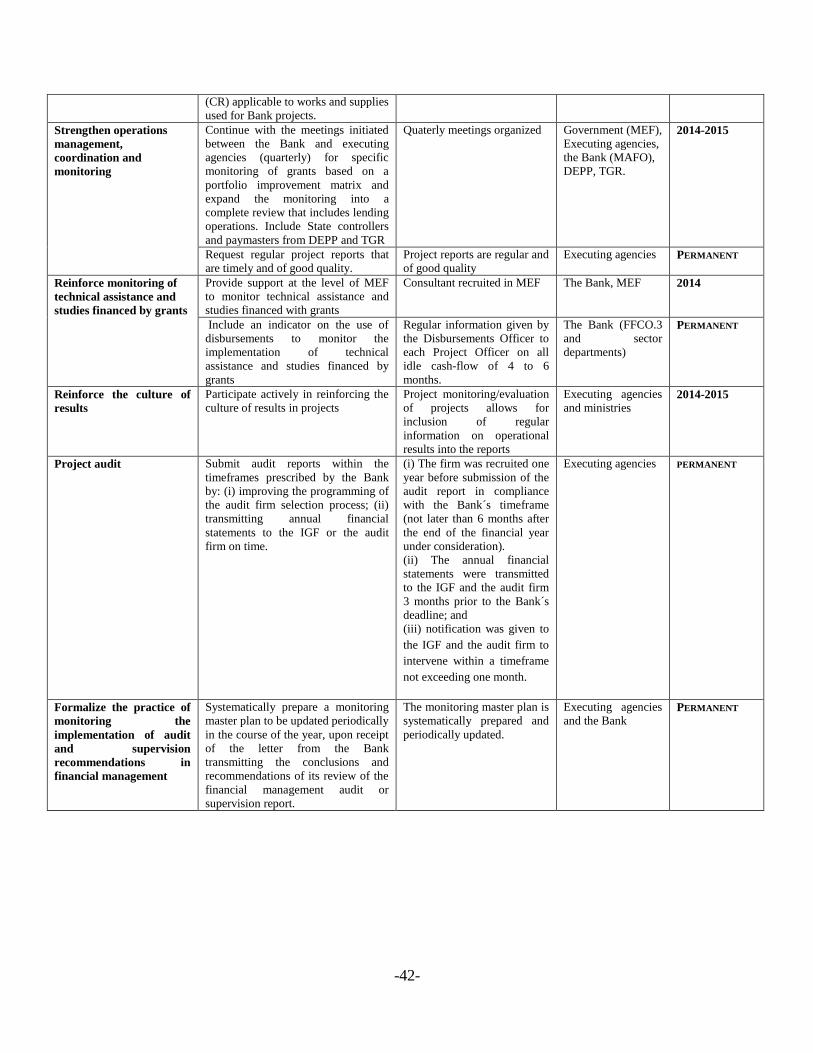

Annex 10: 2014 Project Portfolio Performance Improvement Plan........................................ 41

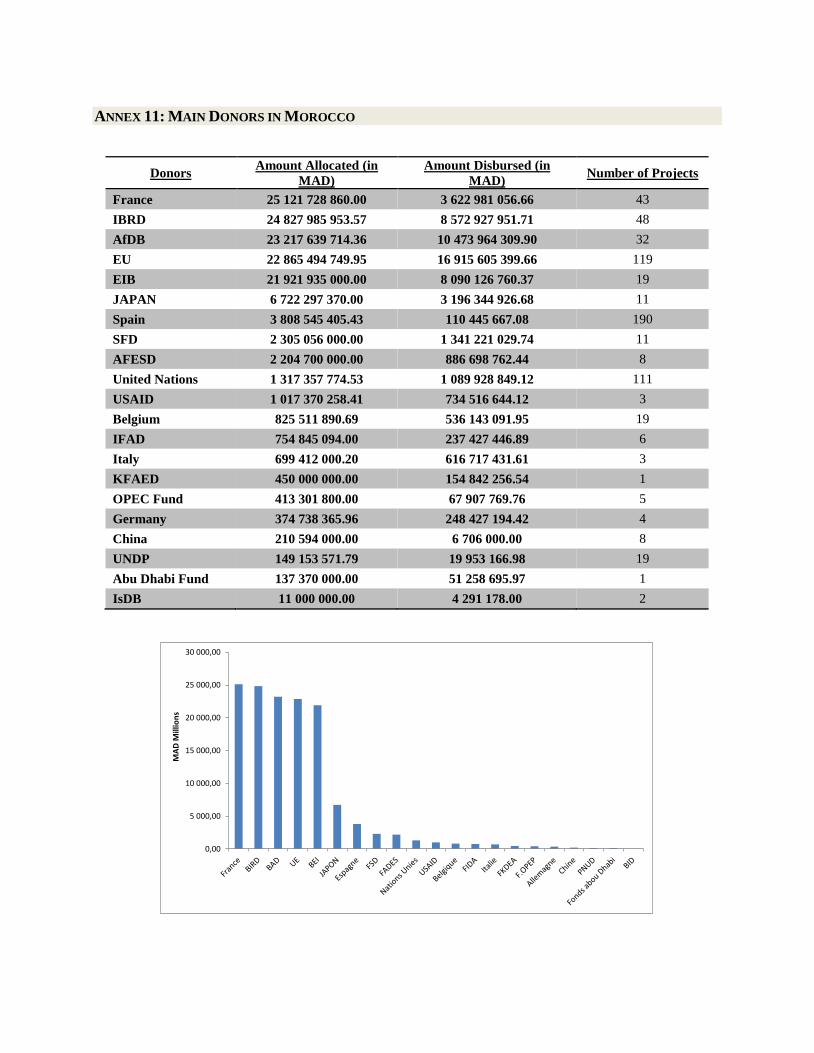

Annex 11: Main Donors in Morocco ........................................................................................... 43

Annex 12: Team ............................................................................................................................ 44

Annex 13: Subsidiary Funds Financed by the Bank and Located in Morocco ........................ 45

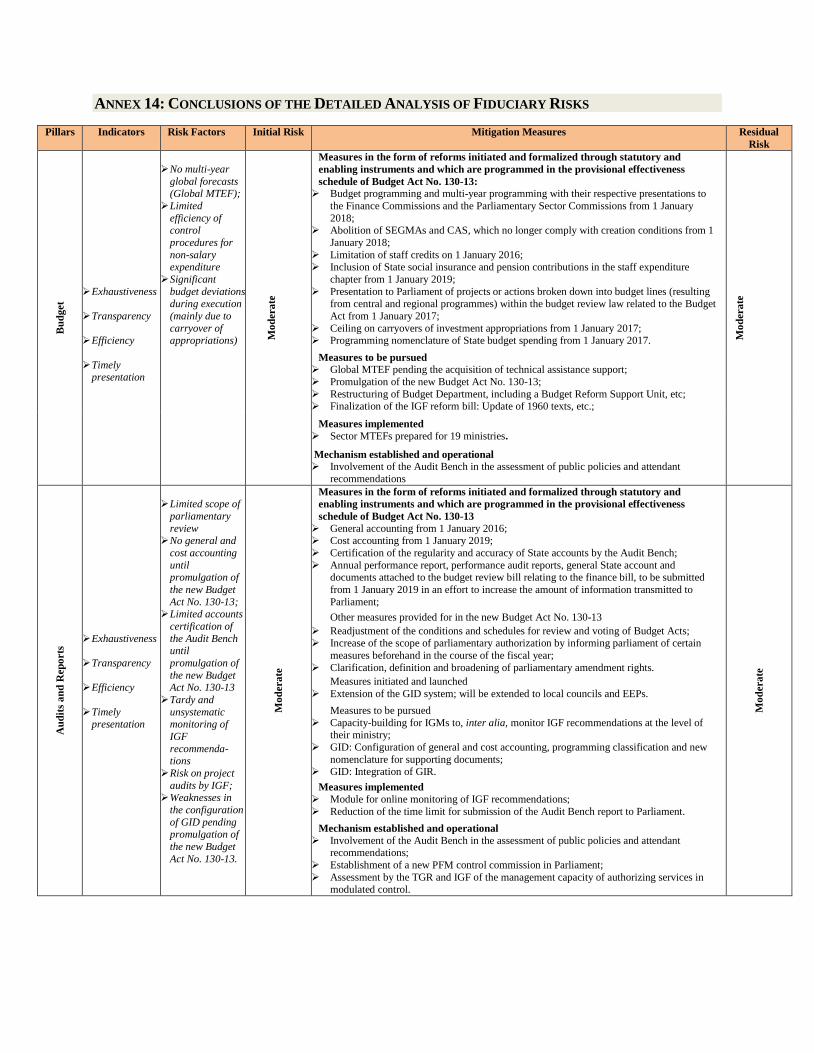

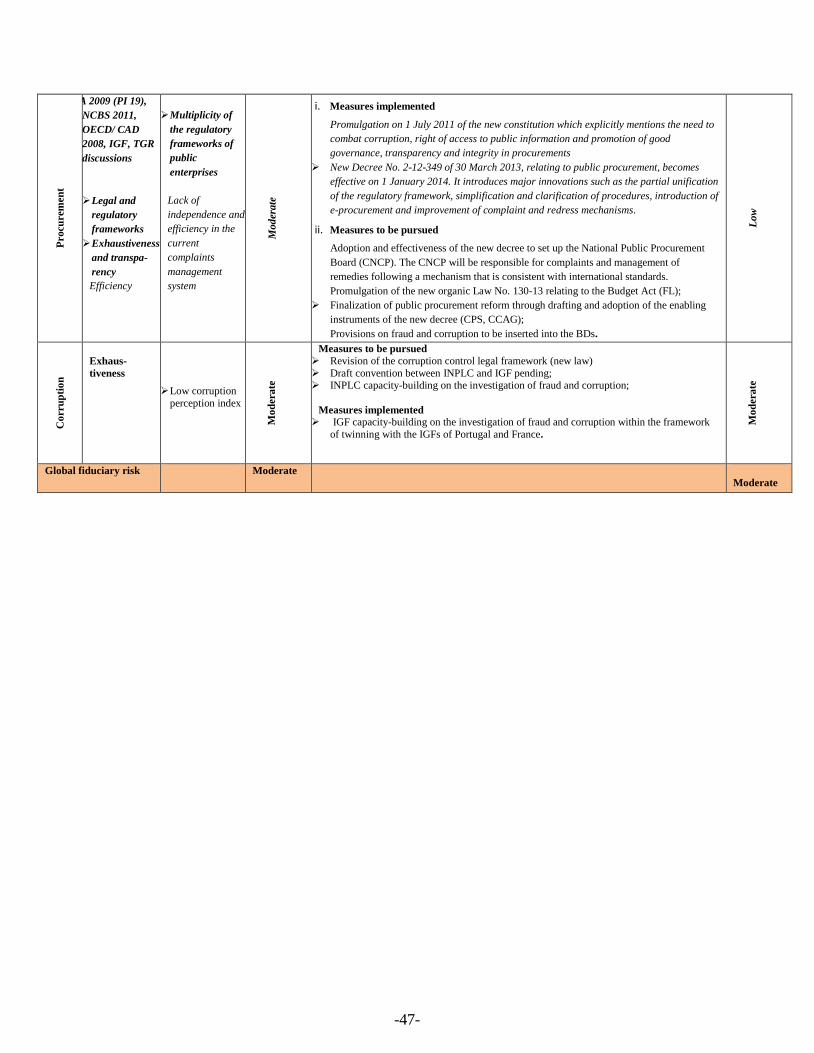

Annex 14: Conclusions of the Detailed Analysis of Fiduciary Risks ......................................... 46

Annex 15: Importance of the Role of the Country Office (MAFO) at Each Stage of the

Operations Cycle of its Portfolio in Morocco .............................................................................. 48

Annex 16: Endnotes ...................................................................................................................... 49

-iv-

LIST OF ACRONYMS

AFD French Development Agency AfDB African Development Bank AGTF Africa Growing Together Fund AMDL Moroccan Agency for Logistics Development ANPME National Agency for the Promotion of Small- and Medium-Sized Enterprises ATM Automated teller machines CODE Committee on Development Effectiveness CPO Country Programme Officer CPPR Country Portfolio Performance Review CS Construction sector CSP Country Strategy Paper CTF Clean Technologies Fund DEPF Directorate of Studies and Financial Forecasts DEPP Directorate for Public Enterprises and Privatisation DWSS Drinking Water Supply and Sanitation EIB European Investment Bank EU European Union FA Formal approval FFCO Financial Control GDP Gross domestic product IGF General Inspectorate of Finance ISR Report on Implementation Status and Results LOLF Organic Law on Finance MAD Moroccan Dirham MAFO Morocco Field Office (of the AfDB) MCC Millenium Challenge Corporation MDGs Millennium Development Goals MEF Ministry of Economy and Finance MIC Middle-income country MIC TAF Middle-Income Country Technical Assistance Fund MSP Moroccan Solar Programme OCP Moroccan Phosphates Authority OFSD Financial Sector Development Department (of the AfDB) OITC Transport and Infrastructure Department (of the AfDB) ONCF National Railways Authority ONEC Energy, Environment and Climate Change Department (of the AfDB) ONEE National Electricity and Water Authority ORPF Procurements and Fiduciary Services Department (of the AfDB) OSAN Agriculture and Agro-Industry Department (of the AfDB) OSGE Governance and Financial Management Department (of the AfDB) OSHD Human Development Department (of the AfDB) OWAS Water and Sanitation Department (of the AfDB) PAAFE Training-Employment Matching Support Programme PACE Competitiveness Support Programme PADESFI Financial Sector Development Support Programme PAPMV Green Morocco Plan Support Programme PAPNEEI National Programme for Irrigation Water Conservation Support Project PARCOUM Medical Coverage Reform Support Programme PARGEF Economic and Financial Governance Revitalization Support Programme

-v-

PDRTE Transport Networks and Electricity Distribution Development Programme PEFA Public Expenditure and Financial Accountability PFM Public finance management PIEHER Integrated Wind Energy, Hydro Power and Rural Electrification Programme PJD Justice and Development Party PMV Green Morocco Plan PNEEI National Programme for Irrigation Water Conservation II PNRR National Rural Roads Programme PPIP Portfolio Improvement Plan PPP Category Category – Potentially problematic project PRP Procurement Plan RAMED Medical Assistance Regime RSP Regional Strategy paper SLL Sustainable lending limit SME Small- and medium-sized enterprises TFT Multi-Donor Trust Fund for Countries in Transition TGR General Treasury of the Kingdom UA billion UA billion UA million UA million UN United Nations USD million USD million VSE Very small enterprises

CONVERSION RATES April 2014

UA 1 = MAD 12.6

UA 1 = USD 1.55

UA 1 = EUR 1.12

FISCAL YEAR

1 January – 31 December

-vi-

EXECUTIVE SUMMARY

1. The 2012-2016 Country Srategy Paper (CSP)

for the Kingdom of Morocco was approved by

the AfDB Board of Directors on 11 April 2012.

The strategy focuses on two pillars, namely: (i)

enhanced governance and social inclusion; and

(ii) support for the development of “green”

infrastructure.

2. The country enjoys good political stability as

it implements far-reaching reforms. From the

economic standpoint, Morocco has solid

performance with an average annual growth rate

of 4.2% over the 2009-2013 period despite a

difficult international and regional context. Since

2011, successive authorities have striven to

improve government efficiency and public

finance management, while seeking to preserve

macro-economic stability.

3. The indicative budget for the 2012-2014 work

programme projected a total of UA 1.191 billion

for 2012-2013 and UA 391 million in 2014. The

amount for the Bank’s approved projects from

January 2012 to April 2014 (UA 1.108 million)

is consistent with this target.

4. The Bank’s overall portfolio performance

remains satisfactory overall, with an average

score of 2.53 on 3 in 2014. This score has

remained stable since 2012.

5. The mid-term review made it possible to

update the Portfolio Performance Improvement

Plan (PPIP). The main recommendations

include continuing the organisation of quarterly

workshops and reviewing the possibility of

establishing technical assistance at MEF for close

monitoring of grants. As regards

recommendations of previous reviews, this new

PPIP repeats those aimed at guaranteeing good

quality-at-entry of loan and grant operations and,

specifically, stricter targeting of grants aligned

with lending operations as well as systematic

assessment of the management capacity of new

partners.

6. Lessons from a growth diagnosic, related to

the constraints that undermine the country’s

capacity to tackle its challenges, enabled the

Bank to confirm the two pillars and fine-tune

its support under these pillars for the remaining

period. Under the governance pillar, the Bank’s

support for 2014-2016 will focus on boosting

competitiveness, coordinating stakeholders and

streamlining social spending. Under the

infrastructure pillar, it will focus on boosting

economic competitiveness and reducing regional

disparities.

7. Furthermore, alignment on the 2013-2022

strategy was enhanced and operational

arrangements adjusted to take account of

financing constraints. In particular, the

mobilization of additional resources will be

reinforced and private sector support improved.

Special emphasis will also be laid on: (i)

increased communication on Bank operations;

(ii) selection/formulation of projects through a set

of indicators that reflect the objectives of the

strategy; (iii) civil society involvement; and (iv)

implementation of analytical work to enhance the

Bank’s consultancy role.

8. The following proposals were also retained

by the authorities to improve the performance

of Bank operations: (i) respect the deadlines for

submission of project audit reports; (ii) continue

holding quarterly meetings between the Bank,

MEF and executing agencies on the monitoring

of grants and expand such monitoring into a

comprehensive review; (iii) examine the

possibility of supporting MEF in monitoring

grant implementation; and (iv) request for regular

and quality project reports.

-1-

I. INTRODUCTION

1.1 The 2012-2016 Country Strategy Paper

(CSP) for the Kingdom of Morocco was

approved by the AfDB Board of Directors on

11 April 2012. Through this strategy, the Bank

supports Morocco’s efforts to lay the foundation

for an attractive economy by helping the

country to develop its assets. This strategy

focuses on two pillars: (i) enhanced governance

and social inclusion; and (ii) supporting the

development of “green” infrastructure.

1.2 The CSP ends in December 2016, and

pursuant to the guidelines issued in April

20131, this combined CSP 2012-2016 Mid-

Term Review and the 2014 Country Portfolio

Performance Review (CPPR) was prepared.

Continuous dialogue with the Government and

other partners, as well as a broadbased

consultative mission organized in June 2014

(including workshops with civil society and

development partners) brought confirmation that

the Bank's intervention strategy remains

relevant.

1.3 The two pillars of the strategy have been

maintained. Under the governance pillar, the

Bank’s support for 2014-2016 will focus on

boosting competitiveness and streamlining

social spending. Under the infrastructure pillar,

it will focus on enhancing economic

competitiveness and reducing regional

disparities. The objectives of green and

inclusive growth have been addressed under the

two pillars.

II COUNTRY CONTEXT AND DEVELOPMENTS

2.1 Political Developments

2.1.1 The country enjoys good political stability

as it implements far-reaching reforms. The

constitution was revised by referendum in July

2011 to consolidate multiparty democracy,

human rights and individual freedoms. The

elections of November 2011 were won by the

Justice and Development Party (PJD) whose

Secretary-General was appointed to head the

Government. A first coalition government was

formed on 3 January 2012 and a second in

October 2013 following the withdrawal of the

Istiqlal Party from the governing coalition. The

next regional and municipal elections will be

organized in June 2015 and elections for the

chamber of advisers in September 2015.

2.1.2 At the international level, commitment to

the reform process was rewarded in 2011 with

obtainment of the status of Partner for

Democracy from the Council of Europe.

Furthermore, Morocco was a non-permanent

member of the Security Council from 2012 to

2013. During this period, it also joined the

United Nations Human Rights Council for three

years, as well as the United Nations Committee

against Torture and the UNESCO Council.

2.1.3 Morocco’s security situation remains

under control, despite a disturbing regional

context.

2.2 Economic and Social Developments2

2.2.1 From the macroeconomic standpoint,

Morocco has posted solid performance with an

average annual growth rate of 4.1% over the

2009-2013 period, despite a difficult

international and regional context. After a

slowdown in 2012 (+2.7%), the economy rallied

again in 2013 (4.4%). This bounce stems in

particular from the excellent performance of the

agricultural sector (+19%). Meanwhile, non-

agricultural activities, which had grown by 4.5%

on average over the decade, remained less

bouyant (+2.3%)3 Nonetheless, the new

automobile and aeronautic industries

experienced strong export growth (+20% and

+14% in 2013). Inflation remained low from

2009 to 2012 (1%), and stood at only 1.9% in

2013, despite the spike in the prices of some

energy products on which subsidies were

reduced. Growth prospects are good: 4% and

5% in 2014 and 2015 (AEO, 2014).

2.2.2 With regard to public finance, Morocco

tightened budget discipline to curb the deficit

that has been growing since 2009. The

authorities took several key measures to contain

this deficit in 2013, such as: (i) the reduction of

subsidies by almost 2% of GDP after the

introduction in September of a partial price

indexation mechanism for some petroleum

products; (ii) the reduction of wage costs by

about 0.4% of GDP; and (iii) the non-deferment

of investments in October 2013. Hence, the

budget deficit reduced to -5.5% of GDP in 2013

-2-

compared to -7.4% in 2012. However, total

revenue declined by 0.5% in 20134. In 2014,

these measures continued with the suspension of

fuel-oil and petrol subsidies in January5, in an

effort to curtail the deficit to 3% of GDP by

2016. Furthermore, although the external debt

increased recently (from 24.4% of GDP in 2009

to 30.9% in 2013), it remains sustainable and

should decline from 2016. At the end of April

2014, Fitch Ratings affirmed Morocco’s credit

risk rating for its long-term debt in foreign

exchange and local currency at BBB- and BBB,

with a stable outlook6. Deficit reduction and

structural reforms account for this improvement.

2.2.3 The external current account balance

improved to -7.6% from -9.7% in 2012, despite

the decline in exports in 2013, due to a 23%

contraction in phosphate exports7. This trend

can be explained by a greater reduction in the

value of imports (-2%) than in the value of

exports (-0.8%). Foreign exchange reserves

reached 4 months and 9 days of imports in

20138, thanks to a contraction of the trade deficit

and a strong growth in FDI (+23.2% in 2013) as

well as access to international bond markets at

favourable conditions (USD 750 million raised

in May 2013).

2.2.4 Nonetheless, the geographic

concentration of exports to Europe (66%) does

not encourage the expansion of Morocco’s

market share in a context of low growth.

Furthermore, sub-regional integration remains

less dynamic. Hence, Morocco considers the

consolidation of economic cooperation ties with

Sub-Saharan Africa to be a priority. Morocco is

the second African investor on the continent and

has a growing presence in the services sector

(banking, telecommunications). In addition to

the recent visit of the King in 2013 and 2014,

which led to bilateral agreements in Africa,

Morocco is currently negotiating strategic

partnership agreements with WAEMU,

ECOWAS and CEMAC. Furthermore, the

country is building a range of infrastructure

for services (such as Casa Finance City) or

for transport to underpin these plans.

2.2.5 Morocco's banking sector is one of the

most efficient on the continent. Outstanding

credits to the economy grew in 2013 by 3.2%

compared to 5.4% in 20129. This better access

to financial services stems from a substantial

increase in the bank penetration rate and wider

geographic coverage (5,711 branches and 5,893

ATMs). However, challenges remain in terms of

financing of VSEs and SMEs as well as access

to basic banking services for communities with

modest income, the youth, women in business

and rural households.

2.2.6 Boosting global competitiveness is a core

concern. The business environment has

improved and Morocco is ranked 87th in Doing

Business 2014. Specifically, the country is

ranked 39th as regards starting a business (+14

spots)10

. On governance, however, Morocco

regressed by three spots in the 2013

“Transparency International” classification to

the 91st position. The country is ranked 77

th (70

th

in 2012) in the 2013 Global Competitiveness

Report which identifies bureaucracy as the main

private sector constraint. The report underscores

the need to pursue reforms, especially in the

following areas: (i) protection of intellectual

property (90th out of 148); (ii) innovation

(106th); (iii) labour market regulation (122

nd);

and (iv) higher education quality (102nd

).

Morocco experienced an improvement in its

logistical performance under the logistics

-300 000

-200 000

-100 000

0

100 000

200 000

300 000

2005 2006 2007 2008 2009 2010 2011 2012 2013

Figure 1: Revenue, Expenditure and Overall Balance (in MAD billion)

Recurrent revenue (net of VAT) Recurrent expenditure

Investment expenditure Overall balance

Source: Ministry of the Economy and Finance, DEPF, Morocco

107,3

151 148,4

182,8

202,1 196,4

47,8

42,8

50,2

48,9

47,848,2

40

42

44

46

48

50

52

0

50

100

150

200

250

2008 2009 2010 2011 2012 2013

Mil

lia

rds

de

Dir

ha

m

Figure 2: Trade Deficit and Cover Rate Trends

Trade deficit Cover rate (%)

Source : Office des Changes, Maroc

-3-

performance index, improving its ranking from

113th in 2007 to 50

th in 2012 (out of 150).

However, efforts still have to be made in the

development of logistical poles to ensure higher

volume flows, reduce goods transport costs and

create jobs in the hinterland.

Table 1: Business Environment (DB-2014)

Domain 2014 2013 ∆ Starting a business 39 53 14

Dealing with construction permits 83 81 -2

Getting electricity 97 95 -2

Registering property 156 166 10

Getting credit 109 105 -4

Protecting investors 115 113 -2

Paying taxes 78 115 37

Trading across borders 37 34 -3

Enforcing contracts 83 83 0

2.2.7 Hence, the low competitiveness of

Moroccan exports is the primary challenge

of the economy. This probably stems more

from their inadequate technological content than

their cost11

.

2.2.8 Limited private sector dynamism and lack

of SMEs is the second challenge. Small

businesses tend to remain small and big

businesses remain big due to “the missing

middle". Because of distorsions in the market,

small businesses tend to rely on traditional

revenue sources while avoiding new

investments in innovative industries12

.

2.2.9 Youth unemployment remains a

constraint on social and economic stability. The unemployment rate was 9.2% in 2013

(19.3% among those aged 15-24 years, 16.3%

among graduates and 4.5% among non-

graduates). Job growth is weak partly due to

distorsions that stem from the distribution of

value-added between capital and labour.

2.2.10 Poverty and regional disparities

constitute another constraint. The poverty rate

was 6.2% in 2011 and the vulnerability rate

13.3%. Furthermore, poverty remains a rural

phenomenon. Morocco’s scores in terms of

human development and GDP per capita are

lower than those of comparable countries13

.

However, the State has undertaken many actions

to address this problem. The water and

sanitation access rates increased in urban areas

(100% in 2011). In rural areas, these rates grew

from 70% in 2005 to 92% in 2011. The

electrification plan seems to have succeeded

with a rural coverage rate of 98.1% in 2012

compared to 22% in 1996. Indeed, some MDGs

were achieved before 2015 and the others will

be attained by then (Annex 8).

2.2.11 Gender disparities in access to human

and economic development opportunities

remain strong but have markedly reduced. At

the institutional level, this trend was supported

by the gender-sensitive budgeting process in

2003 and the new Constitution of July 2011.

The Government has undertaken to increase

women’s representation in all areas, using the

Government Equality Plan as reference

framework. Efforts made to encourage primary

education for girls raised the enrolment rate to

97% in 2012. Nevertheless, in 2012, 38% of

women remained illiterate14

compared to 23.5%

of men. Moreover, the employment rate for

women stood at 26.1% in 2012. From the

gender standpoint, the reduction of

unemployment favoured men (from 13.6% to

8.4%) more than women (from 12.8% to

10.2%). This situation is reflected in the 2013

gender equality report of the World Economic

Forum which ranks Morocco 129th out of 136

countries. According to the 2013 Global Gender

Gap Report, major gender inequalities persist in

parliament, appointments to ministerial posts,

number of magistrates, directors and senior

executives in public or private companies as

well as in income. In 2013, the proportion of

women in public administration was 38%

(compared to 26% in 2009). Hence, there are

still numerous challenges that must be addressed

to reduce inequalities, especially those related to

gender.

2.2.12 The fragility of the environment and the

risks caused by climate change account for the

weak development of the Moroccan economy.

Water resources in particular are the focus of

all attention. Groundwater is reaching

saturation point and the significance threshold

has already been attained due to

overexploitation, driven sometimes by the

shortage or even absence of surface water, while

water demand is increasing. The 2011

Constitution recognised access to a healthy

environment as a fundamental right of citizens.

-4-

Several strategies were formulated15

and

implemented through actions that improve areas

directly related to the health and living

conditions of citizens, especially: (i) protection

of water quality; (ii) regulation of air-polluting

emissions; (iii) waste management; and (iv)

impact assessments of public and private

environmental projects. The Green Morocco

Plan (PMV) is one of the pillars. It seeks to

provide sustainable support to agriculture

because this sector contributes 15% to 20% of

GDP and employs 4 million people.

III. CSP 2012-2016 IMPLEMENTATION AND

OUTCOMES

3.1. Country Development Context

3.1.1 Morocco is a middle-income country with

a GDP per capita of USD 2 924.94. Since

2011, it has also become a transition economy

that enjoys support from the Deauville

Partnership and which, since adopting the new

2011 Constitution, has been implementing

numerous reforms and speeding up the

implementation of its new development

strategies and policies.

3.1.2 In January 2012, the Government

presented the priorities of its programme

through its General Policy Statement. These

priorities mainly focus on: (i) the State’s social

action performance; (ii) improvement of

education and research; (iii) modernization of

the agricultural sector; and (iv) economic and

financial governance. During formation of the

second government of October 2013, emphasis

was also laid on improving the business

environment and boosting the competitiveness

of the national industrial fabric.

3.1.3 Since 2011, the authorities have

especially striven to improve government

efficiency and public finance management

while seeking to preserve macro-economic

stability. This led to the adoption of a new

Organic Law in relation to the Budget Act. The

Government has striven to enhance transparency

and accountability in public resource

management mainly through: (i) enhancement

of performance-based budgeting with

stakeholder involvement16

, thanks to better

access to financial information and the conduct

of PEFA; (ii) more coherent implementation

of public procurement rules; (iii)

development of electronic tools for integrated

expenditure management and administrative

simplification, which facilitate access to

common administrative services; and (iv)

improvement of the financial governance and

control of public enterprises and

establishments. Furthermore, to improve

macroeconomic balances, the Government’s

commitment to reform and budget discipline

was underscored by observers (for example,

during the energy subsidy reforms in late 2013

and 2014).

3.1.4 With regard to competitiveness, Morocco

launched the 2014-2020 Logistics Acceleration

Plan and the National Industrial Acceleration

Plan in 2014 to replace the National Pact for

Industrial Emergence launched in 2008 (which

enabled the country to develop new industries

such as aeronautics or car manufacturing). The

objectives of this plan are to: (i) increase the

share of industrial GDP in overall GDP from

14% to 23%; (ii) build new synergies between

large enterprises and SMEs (corporate

ecosystem); (iii) enhance the role of industry as

the purveyor of jobs, especially for the youth

(creation of 500,000 jobs); and (iv) optimize the

social and economic fallout from public

procurement through industrial compensation.

The new plan will also be used to guide the

transition from the informal to formal economy

through the establishment of a complete

mechanism for the integration of a very small

enterprises (VSEs) and the creation of a public

industrial investment fund that will have a

budget of MAD 20 million by 2020. With

regard to the agricultural sector, boosting

competitiveness is the core concern under the

Green Morocco Plan.

3.1.5 In a bid to combat poverty and insecurity,

the Government plans to expand social

protection while improving the targeting and

efficiency of services rendered to citizens. This

led to the generalization of the medical

assistance scheme in 2012, for instance. The

Government is working to streamline its social

action by enhancing the efficiency of transfers

and establishing a single identifier. Reform of

-5-

the pension system is one of the next challenges.

3.1.6 As regards education and vocational

training, the emergency programme that

sought to: (1) extend the duration of

mandatory schooling in Morocco to 15 years;

(ii) put more resources at the disposal of

pupils; and (iii) guarantee better vocational

training for them, ended in 2012. The

Government is currently preparing strategies on

vocational training (2014) and education (2015).

These strategies have to address issues such as

job-relevant training, competitiveness,

entrepreneurship and elimination of skills

development constraints.

3.1.7 From 2011, Morocco initiated the second

phase of the process to institute the advanced

regionalisation system. In this regard,

decentralisation and devolution should help to

modernise State structures in the regions and

promote sustainable and integrated

development. The organic law is expected in

2014/2015. The reduction of regional disparities

also begins with investments in various regions

of the Kingdom to increase access to social

infrastructure and services.

3.2 Bank’s Positionning

3.2.1 The Bank is one of Morocco’s leading

development partners. Its active portfolio in

Morocco currently has 33 operations (loans and

grants) for net commitments of approximately

UA 1.8 billion. Apart from the Bank, the main

financial partners are: France, World Bank, EU

and EIB, which all have an equivalent level of

commitment (approximately UA 1.5 to 1.8

billion - Annex 11).

3.2.2 The Bank’s strategy for the 2012-2016

period focuses on two pillars, namely: (i)

enhanced governance and social inclusion;

and (ii) support for the development of “green”

infrastructure. These operational pillars are a

continuation of government action aimed at

consolidating the foundation of “green” and

inclusive growth by: supporting economic

competitiveness; developing the private sector;

diversifying the sources of economic growth;

increasing the State’s social support and

reducing disparities.

3.2.3 The Bank has initiated an in-depth

dialogue with the authorities on operations

identification and public reforms and policies,

shored up by budget support. Furthermore, the

presence of a field office (MAFO) facilitates

almost daily interactions with sector ministries

and bodies involved in project implementation.

In this regard, two portfolio performance

reviews were conducted in December 2012 and

2013, and a fiduciary clinic held in 201417

.

Besides, the active participation of MAFO in

events organized by the Government, civil

society, the private sector and partners helps to

provide a fuller understanding of stakeholder

needs.

3.3 Resource Allocation

3.3.1 The indicative budget of the 2012-2014

work programme projected a total of UA 1.191

billion for the 2012-2013 period18

and UA 391

million in 2014.

3.3.2 The amount for projects approved by the

Bank from January 2012 to April 2014 is

consistent with this objective and stands at UA

1.108 billion (Annex 2). This budget was

allocated to 22 projects, including four budget

support programmes, three investment

operations, two operations financed by the

Clean Technologies Fund (CTF), seven grants

from the Middle-Income Country Technical

Assistance Fund (MIC TAF) and six operations

of the Trust Fund for Countries in Transition

(TFT).

3.3.3 In particular, budget support stood at UA

391.4 million in 2012 and 2013. It included: (i)

the Green Morocco Plan Support Programme

(PAPMV-July 2012); (ii) the Economic and

Financial Governance Revitalization Support

Programme (PARGEF-July 2012); (iii) the

Training-Employment Matching Support

Programme (PAAFE-July 2013); and (iv) the

Medical Coverage Reform Support Programme

(PARCOUM-December 2013).

3.3.4Meanwhile, investment operations

amounted to UA 712 million and included: (i)

the Ouarzazate Solar Power Station Project

(May 2012); (ii) the Integrated Wind Energy,

Hydro Power and Rural Electrification

Project (PIEHER-June 2012) and; (iii) the 12th

-6-

Drinking Water Supply Project in the

Marrakesh Region (12th DWS-November 2012).

This budget also covers 2 operations financed

by the CTF (USD 100 million – Ouarzazate

Project; USD 125 million – Wind Energy

Programme).

3.4. CSP Implementation Status

3.4.1 Pillar I of CSP 2012-2016 namely,

“Enhanced governance and social inclusion”

provides for the funding of 14 operations,

including 12 in 2012-2013. Its objective is to

build on achievements in the areas of

governance and inclusive growth. In keeping

with the new constitution of 2011 which places

governance at the core of public action, the

authorities wish to channel reforms increasingly

towards grassroots management, participation

and accountability.

3.4.2 For Pillar I, the volume of operations in

2012 and 2013 exceeded the expectations of

the indicative lending programme (UA 396.1

million compared to UA 393.9 million). The

entire lending programme was implemented.

Two grants (MIC TAF) for infrastructure were

cancelled (and taken over by the EU and CTF),

but seven additional grants were formulated

(one MIC TAF and 6 TFTs to strengthen

support in the social sector (Annex 2)). Two

studies on the public sector and competitiveness

were replaced with a growth diagnostic study.

3.4.3 Pillar II, namely “Support to green

infrastructure development” provides for the

funding of 14 operations, including 10 in

2012-2013. It seeks to rely on infrastructure

development to promote green growth, which is

the priority objective of Moroccan authorities.

Although these actions preserve natural

resources, they are aimed at boosting

competitiveness and the diversification of

growth sources.

3.4.4 For this pillar, the volume of operations

in 2012 and 2013 fell below the expectations of

the provisional loan programme (UA 712.2

million compared to UA 797.5 million). Lending operations in the energy sector

exceeded projections, partly due to the early

formulation of activities for the Tangier Wind

Farm (initially scheduled for 2014). This was

counterbalanced by postponement of the

formulation of PNEEI-II (since PNEEI-I was

not yet completed due to financing constraints at

the level of the Bank) and of the Logistic

Support Project (since the Moroccan Logistics

Development Agency (AMDL) was only

created in 2013). As far as grants are concerned:

the Rural Roads Programme Impact Study was

taken over by the EU, support to the National

Logistics Observatory was delayed pending the

creation of AMDL, while the Green Growth

Study is being prepared.

3.5. CSP Implementation Results

3.5.1 An assessment of the attainment of

results set at mid-term is presented in Annex 1.

For the first pillar, the macroeconomic targets

were ambitious and the Government initiated

reforms to meet them. Reforms on access to

information, the creation of an authority in

charge of capital and insurance markets as well

as regionalisation are being pursued. For the

second pillar, objectives related to the

performance improvement and coverage of

transport, water and sanitation infrastructure are

being pursued, while those related to energy

have been met.

Execution of Pillar 1 - Governance

3.5.2 As regards governance, PARGEF (UA

100 million – September 2012) made it possible

to support the "Hakama" multi-year reform

programme. This programme seeks to improve

State efficiency in budget management and

provision of public services to promote robust

and inclusive economic growth19

. It has helped

to improve budget forecast and management

efficiency, the establishment of an institutional

framework for e-government, the reduction of

time-limits for customs clearance of goods from

40 days to 3 days and the adoption of the new

public procurements code. Furthermore, these

activities were supported with technical

assistance for "the modernisation of the debt

management organisational framework." The

financial sector was supported by the "support

project for the preparation of the Moroccan

Monetary and Financial Code”, which is a

technical assistance approved in 2012 to

strengthen capital market governance. However,

-7-

the two technical assistance operations are still

at the start-up phase. Lastly, the conduct of a

growth diagnosic with the authorities and the

Millennium Challenge Corporation (MCC)

helped to identify the main constraints to private

sector development and the structural reform

options.

3.5.3 Furthermore, as regards civil society, the

two technical assistance operations (TFT-

2013) have contributed to enhance women’s

representation in elected councils and boost the

national public consultation policy. They indeed

facilitated the organisation of the national

conferences of 2014.

3.5.4 In an effort to strengthen social

inclusion, the Bank continued its support for

better training-employment matching,

particularly in connection with the

employability of the youth and young women.

In this regard, the Bank supported the

implementation of the Training-Employment

Matching Support Programme (PAAFE) with

budget support (UA 101.9 million – July 2013).

The objective of this programme is to

improve the employability of graduates from

the educational system through: technical

education and vocational training that is more

rooted in the productive environment, improve

the relevance and management of higher

education, and provide better sector

coordination and governance. PAAFE has

specifically led to: (i) review of the training

referentials in technical education; (ii)

preparation of a bill to establish a national

agency for the assessment of higher

education; (iii) establishment of a mechanism

for the recruiment of graduates; (iv)

establishment of regimes for the delegated

management of vocational training; and (v)

improvement of governance. Concerning

training, the Bank also financed four technical

assistance operations (3 TFTs and 1 MIC TAF),

all in the start-up phase, for: (i) the creation of a

national mechanism to promote the

employability of graduates; (ii) the

establishment of an integrated system to

evaluate the quality of vocational training; (iii)

the identification of skills needs in the

construction sector by 2015; and (iv) the

creation of an e-university within the

International University of Rabat. Lastly, to gain

a better understanding of job promotion policies,

the Bank financed technical assistance (MIC

TAF, 2003) to the Ministry of the Economy and

Finance to conduct a study on inclusive growth

and employment.

3.5.5 Social inclusion was also supported

through operations in the social protection

sector. In this regard, PARCOUM III seeks to

extend basic medical coverage and broaden

access to healthcare. An initial disbursement of

EUR 70 million was made after: (i) the

establishment of an inter-ministerial committee

for medical coverage; (ii) the proposal of

scenarios for the coverage of self-employed

workers; and (iii) the mobilisation of resources

allocated to RAMED. Two technical assistance

operations approved in 2013 and in the start-up

phase have consolidated these reforms through

the preparation of: (i) a health mapping

decision-making information system for

Morocco (PRI); and (ii) the health sector

financing strategy (TFT).

Execution of Pillar II - Infrastructure

3.5.6 In the energy sector, two Bank operations

help to combat climate change and ensure

diversification of the energy mix. The

Ouarzazate Solar Power Station (23% physical

implementation rate) is being financed under the

Moroccan Solar Programme, which seeks to

install 2,000 MW of solar energy capacity by

2020. The Integrated Wind Energy, Hydro

Power and Rural Electrification Programme

(PIEHER) has already electrified 2,223 villages

(out of 7,000), representing 61,824 households.

The financing of these two operations has also

made it possible to mobilise CTF resources.

3.5.7 In the water sector, the 12th

Marrakech

Drinking Water Supply (DWS) Project (UA

125 million – November 2012), at the start-up

phase, seeks to satisfy drinking and industrial

water needs in the Marrakech region up to 2030.

The Bank also financed the study on the

drinking water supply master plan for

communities of the Moulouya river basin. The

purpose of the plan is to ensure steady drinking

water supply and sanitation in this region and

-8-

thus preserve the quality of water resources.

3.5.8 In agriculture, the Green Morocco Plan

Budget Support Programme (PAPMV) (UA

87.5 million-July 2012), which adopted an

inter-sector approach involving 5

departments20

, made it possible to implement

key measures such as irrigation water

planning21

, promotion of value chains22

,

establishment of regional environmental

observatories and the national irrigation map. In

this regard, six laws were adopted. At the same

time, the Bank instituted technical assistance for

the promotion of young farmers (MIC TAF)

with a view to addressing the problem of youth

employment in rural areas (with emphasis on

young women). Lastly, a South-South grant is

aimed at developing agricultural production by

supporting the use of biotechnologies.

3.6 Other Effects of the Strategy

Pillar I - Governance

3.6.1 Several operations initiated under the

previous CSP in the financial sector also

contribute to the attainment of Pillar I

objectives. PADESFI II made it possible to

support: (i) the financial inclusion of households

by raising the bank penetration rate from 35% in

2008 to 60% in 2013; and (ii) efforts to diversify

the economy and enhance its resilience by

increasing the number of SVEs benefitting from

a guarantee of 25% and paring down the risky

portfolio from 40% in 2008 to 6% in 2013.

Furthermore, two MIC TAF grants contribute to

the attainment of the objectives of improving

financial sector governance, namely: (i) the

project to strengthen the control of financial

markets with the Securities Ethics Board (which

is being implemented) and; (ii) the Project to

Improve the Guarantee System with the Central

Guarantee Fund (the survey conducted among

users reveals that the services rendered are

highly satisfactory).

3.6.2Lastly, the Private Education

Establishments Development Strategy Support

was approved in 2011 in the form of a grant

(MIC TAF) and its implementation has only just

started. It seeks to prepare an integrated strategic

plan for the development of private higher,

secondary and technical education and to

increase the supply of private education.

Pillar II - Infrastructure

3.6.3 As regards energy, improvement of the

energy reliability and efficiency of the

electricity network is supported by the

programme to develop electricity transmission

and distribution networks (2009). The

programme has led to the procurement of three

shielded substations and 76 km of evacuation

lines, which have protected the interconnection

with Spain. This operation is reinforced by the

implementation of technical assistance (Finish

Trust Fund) which made it possible to conduct

an energy audit of 50 companies to institute

energy efficiency plans.

3.6.4 Concerning transport, three sub-sectors

are concerned. The National Rural Roads

Programme (PNRR 2, 2007 - UA 37.5 million)

focuses on upgrading a number of roads on the

national network with a view to improving rural

road access for the population from 54% in

2005 to 80% on completion (in 2015). The

average national access rate recorded at the end

of 2013 was approximately 74%, with 13,277

km launched out of 15,500 km. In the airport

sub-sector, a UA 200 million loan approved in

April 2009, should help to increase airport

operational capacity through infrastructure

upgrade, extend the air navigation system and

reinforce ground safety facilities in the Fès,

Marrakesh, Agadir and Oujda airports. The

physical implementation status of the project

stands at 38%. Lastly, under the 2010-2015

contract-programme between the ONCF and the

State for the upgrade and modernization of

transport infrastructure and services, the Bank

granted a loan to expand the capacity of the

Tangier-Marrakech railway line (UA 250

million -2010). The physical implementation

status of the project stands at 63%.

3.6.5 In the water sector, the Bank is the

leading partner in Morocco with ongoing

commitments of over UA 429 million. In 2006,

the Bank initiated a new management method in

the water sector under the 9th DWS Project (UA

67.5 million - closed in 2013). This project

which was implemented in rural areas initiated

the decentralized management of resources. It

-9-

helped to: (i) ensure regular water supply for

380,000 rural dwellers, thus raising the national

access rate by 2.8%; and (ii) develop sanitation

in 3 towns, thus improving the national

sanitation rate by 1.5%. Subsequently, the 10th

DWS Project (2008) improved regular drinking

water supply in the major cities, while the

Rabat-Casablanca 11th DWSS Project (2011) led

to the construction of one of the biggest

treatment plants in Africa, with a capacity to

serve 9 million inhabitants. These projects have

contributed to improve water access, quality and

sustainability.

3.6.6 In the agricultural sector, the National

Irrigation Water Conservation Programme

Support Project (PAPNEEI 2009) helped to

improve water use efficiency mainly through

conversion of the irrigation mode on

approximately 5,000 hectares (out of the 20,000

scheduled) from sprinkling to drip irrigation.

Two technical support operations were

provided, namely: (i) a programme for the

protection, conservation and development of the

oases in the South (POS) (MIC TAF, from 2009

to 2013) that led to the implementation of four

rural community development plans (project

closed); and (ii) support for the development of

irrigation infrastructure (MIC TAF in 2011) for

the establishment of strategic, operational and

innovative tools (ongoing)23

.

Private Sector Support

3.6.7 AfDB support to the private sector led to

an improvement of the business environment,

thanks to reforms and the infrastructure set

up. In terms of reforms, this improvement is

characterized by the establishment of a more

transparent framework (especially in public

procurement), improved access to financing (for

small business owners) and greater access to

human capital. With regard to infrastructure, the

private sector benefits from an environment that

facilitates trade (roads and airports) and more

stable access to inputs (water and electricity).

3.6.8 The AfDB supports the private sector

through direct and indirect financing.

Financing support to the ten-year investment

programme of the Moroccan Phosphates

Authority (OCP) should in the long run lead to

the creation of 9,000 direct jobs in industrial

SMEs. Furthermore, the Bank intervenes

indirectly through investment funds. Its

interventions are fully focused and diversified

from the sector standpoint (pharmacy, agro-

industry, infrastructure, banking) (Annex 13).

Through these funds, the Bank has disbursed

close to UA 16 million as indirect participation

in the capital of Moroccan business. The Bank

also intervenes indirectly by providing financing

through regional lines of credit and participation

in pan-African initiatives24

.

3.6.9. Furthermore, the Bank´s operations

have supported a PPP approach. This is the

case in the energy sector with the Ouarzazate

Solar Power Station Project and within

PIEHER with the Tangier Wind Farm. The

same also applies in the agricultural sector under

the Green Morocco Plan (PMV): the study for

delegated management in irrigation areas and

the enabling instruments of the law on the

private agricultural board (PPP).

Other Economic and Sector Work

3.6.10 In addition, studies were conducted to

focus the Bank´s dialogue on AfDB’s

operational objectives and pillars, while

nurturing thinking on the reforms supported

in Morocco. These studies yielded the following

publications: (i) Labour Market Reforms in

North Africa; (ii) Promoting Crisis-Resilient

Growth in North Africa; (iii) The Quest for

Inclusive Growth in North Africa; (iv)

Development of Financial Markets in North

Africa; (v) Tackling Youth Unemployment in

the Maghreb; (vi) Poverty and Inequality in

Tunisia, Morocco and Mauritania; (vii)

Comparative Study on Export Policies in Egypt,

Tunisia and South Korea; and (viii) The

Political Economy of Food Security in North

Africa. Presentations were organized in the

region to facilitate dissemination.

Pan-African Dialogue

3.6.11 The holding of the 48th Annual

Meetings of the AfDB at Marrakech in 2013

enabled the Bank to initiate dialogue with the

authorities in a pan-African context. This led

Morocco to reaffirm its willingness in 2013-

2014 to position itself as a leading player in

-10-

promoting trade with Africa.

3.7. Implementation of Paris Declaration,

Accra Agenda for Action and Busan

Partnership commitments

3.7.1 The AfDB field office in Morocco

(MAFO) plays a key role in consolidating

dialogue with the Government and other

development partners. Since starting its

activities in 2006, the Bank´s partnership with

the country and coordination with other

development partners have significantly

improved. Regular dialogue between MAFO

and the authorities helps to identify problems

and the priority actions that need to be

implemented to improve on project execution.

MAFO’s role in providing close oversight

highlights all the advantages of decentralization

and of the Bank´s physical presence on the

ground. However, the fact that the new MAFO

premises are located outside Rabat since 2013

has had a profound impact on the Bank´s

capacity to implement sustained dialogue over

this period.

3.7.2 Coordination among partners is

conducted by the Moroccan Government.

However, there are thematic groups that allow

fluid exchange of information. These groups

are either chaired by the partners or the

Government. The Bank is the lead agency for

civil society and should be the lead agency for

education in 2015. It participates in all social

sector thematic groups (health, youth, migration,

social protection). Furthermore, the water sector

group, created in 2002 by EU member states,

has been open to other donors since 2005. Co-

chaired by the EU, AFD and the ministry

delegate for water, it provides a forum for sector

dialogue twice a year (the last was held in

March 2014).

3.7.3 Nevertheless, some weaknesses persist.

The Government wishes to see enhanced

coordination in the agricultural sector through

the organization of joint missions. In the social

domain, the Bank´s dialogue should be

expanded to include themes such as social

protection, social transfers and governance. The

Ministry of Transport is currently restructuring

its mode of coordination with donors in order to

pool multilateral actions (previous piloted by the

director) and bilateral actions (previously piloted

by a unit) within a central unit. The Bank will

strive to provide its assistance for the creation of

this thematic group.

3.7.4 In accordance with the Paris

Declaration, Morocco became the first country

in 2014 for which the Bank will use the

national procurement system25

.

IV. COUNTRY PORTFOLIO PERFORMANCE

REVIEW

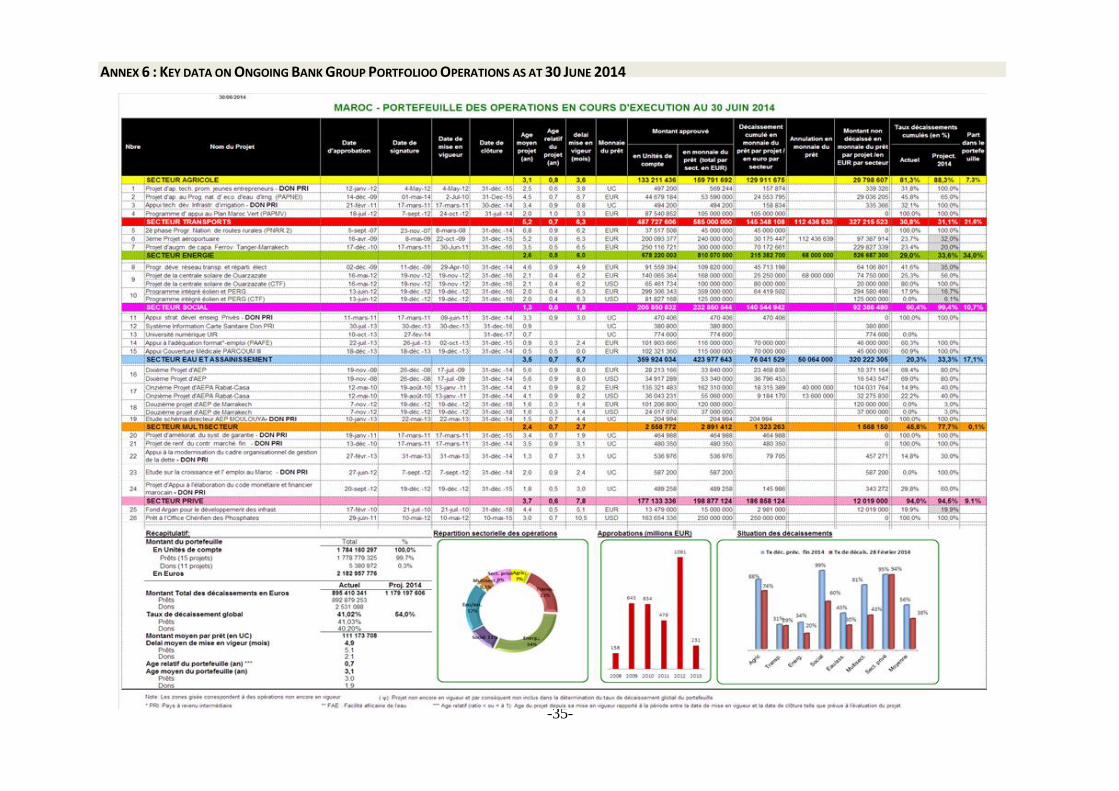

4.1 Current Portfolio

4.1.1 The Bank´s active portfolio in Morocco

comprises 3326

ongoing operations for net

commitments of approximately UA 1.78 billion

(see Annex 6). Loans amount to UA 1.77 billion

(99.7%), or 15 projects and programmes worth

an average of approximately UA 111 million

per operation.

4.1.2 The portfolio covers six intervention

sectors: energy (34%), transport (22%), water

and sanitation (17%), social sector (11%),

private sector (9%), agriculture (7%) as well as

multisector operations (0.1%). There is a high

concentration of operations in the infrastructure

sector (90% of commitments), particularly

energy and transport (56%).

4.1.3 Public sector loans (sovereign

operations) amount to UA 1.7 billion for 13

projects. Furthermore, the portfolio includes 18

technical assistance operations: 11 with MIC

TAF financing (UA 5.4 million) and 7 with the

resources of the Trust Fund for Countries in

Transition (TFT—UA 1.4 million in 2013).

4.1.4 The portfolio includes two non-

sovereign operations (a loan to the

Moroccan Phosphates Authority and an

equity participation in the Argan Fund for

Infrastructure Development) for a total of

UA 177 million.

4.1.5 Over 25% of the Bank´s portfolio

commitments in Morocco are implemented

through co-financing arrangements. Most of

the budget support operations, such as

PARCOUM III and PAAFE, are co-financed

with other donors. For investments, specific

-11-

examples are the Ouarzazate Solar Power

Station Project, PDRTE and PNRII for which

co-financing was satisfactorily implemented.

Working documents and meeting minutes are

transmitted to the Bank for approval and

comment, while Bank missions systematically

meet with development partners. A number of

missions are conducted jointly, especially in the

financial sector where the Bank carries out

frequent short-term consultations with the EU

and WB. Lastly, in the case of the Ouarzazate

Solar Power Station Project, AfDB rules apply

to the audits while WB rules apply to

procurements. This attests to the excellent

collaboration between both institutions.

4.2 Portfolio Monitoring and Evaluation

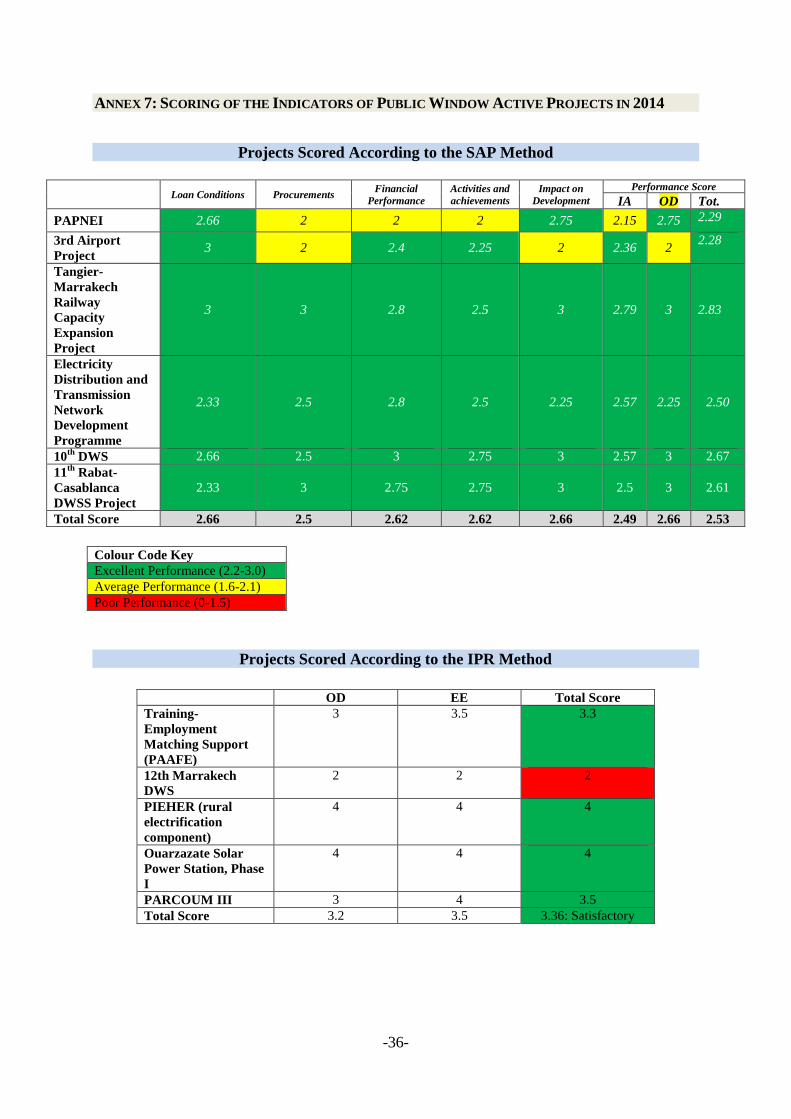

4.2.1 The overall performance of the Bank´s

portfolio remains satisfactory overall, with a

total average score of 2.53 on 3 in 2014. This

score has been stable since 2012. Its rating

under the new EER methodology ranges from

satisfactory to highly satisfactory (3.36/4)27

. The

overall rating of the portfolio, including the two

scoring methods, has evolved favourably. The

average age of operations has increased since

2012 from 2.3 to 3.1 years (2.2 to 3 years for

loans and 2.3 to 1.9 years for grants). The

portfolio has no aged projects according to the

Bank´s definition.

Table 2: Portfolio Rating

2002 2007 2009 2011 2012 2013 2014

2.4 2.4 2.6 2.7 2.5 2.56 2.53

4.2.2 The overall disbursement rate reached

41% in mid-2014 (36.3% in 2013, 32% in

2012) following measures implemented by

the Bank and the executing agencies28

for the

following projects: (i) 10th

and 11th

DWS; (ii)

PAPNEI; and (iii) the Ouarzazate Solar

Power Station. Similarly, the disbursement rate

for grants remains appropriate (51.1%) despite

the exit of 3 grants from the portfolio in March

2014. The target of 54% by the end of 2014 is

attainable because a number of disbursements

are expected on these operations.

Analysis of the Key Performance Indicators

of Public Sector Projects

4.2.3 Compliance with Conditions.

Performance in compliance with loan

conditions remains globally satisfactory in

2014. The average deadline for effectiveness

declined from 6 to 5.1 months for loans and

from 2.6 to 2.1 months for grants since the 2013

review. In 2013, the effectiveness timeframe

was below 3 months for PAAFE (July),

immediate for PARCOUM III (December), and

4 months for the grant on the Moulouya Master

Plan Study. The reduction in the timeframe

since 2011 stems from the rapidity with which

compliance is ensured for budget support

programmes. The timeframes observed for

energy projects approved in 2012 stem from

their higher complexity, the multiplicity of

donors involved (with their respective

conditionalities) and certain prerequisites

contingent on the nature of these operations

(economic and social impact assessments;

selection of a developer under a PPP29

). For

PIEHER in particular, this will affect the

implementation of the operation and

consequently the portfolio performance30

.

Nevertheless, the “rural electrification”

component of this project is highly effective.

4.2.4 Furthermore, the transmission of

quarterly reports, including interim financial

reports, remains irregular. The quality and

regularity of report transmission has certainly

improved following: (i) the recommendations of

the last CPPR in 2013; and (ii) the transmission

of a template to executing agencies. However,

operations such as PMV or PAPNEI must

conform to the requirements.

4.2.5 In general, project financial audits have

been conducted according to the Bank´s Terms

of Reference. Besides, there is better planning

of the process to select audit firms at the level of

PPMs. Although the deadlines have not been

respected, all FY2012 audit reports for

investment projects have been transmitted to the

Bank, which endorsed them. For FY2013, 15

audit reports were still expected by the Bank as

of mid-June 2014. This situation stems from: (i)

the slow execution of the adversarial and final

approval procedure of reports drafted and filed

on time by the IGF to the project execution

agencies concerned; and (ii) the schedule

-12-

programming the transmission of financial

statements to audit firms. To resolve this

problem, the executing agencies must transmit

their annual financial statements to the IGF or

their audit firm 3 months before the requested

deadline, and request the IGF or audit firm to

intervene within one month31

.

4.2.6 Procurement Arrangements. The

overall procurement performance remains

satisfactory with an average score of 2.5 on 3

(2.6 in 2013). This performance is the result of

the close support provided in the form of

training on rules and procedures, through

workshops and targeted coaching. An example

of the highly satisfactory procurement

performance is the Tangier-Marrakech Railway

Capacity Expansion Project in which all

procurements planned for 2013 were executed

according to schedule. Nevertheless, a number

of operations and especially the 11th and 12

th

DWS Projects, the 3rd Airport Project, and the

Electricity Transmission and Distribution

Networks Development Programme (PDRTE)

experienced procurement slippages. These

delays stem from several factors including the

difficulty of expropriating land for certain

projects (PDRTE)32

or long timeframes for

adopting standard Bank documents by the

executing agencies. For most of the grants, the

procurement difficulties identified during the

last CPPR in 2013 were addressed mainly

through training, targeted support and support to

MEF.

4.2.7 Operations performance will also

improve with: (i) the operationalisation of the

letter of agreement on the use of national

procurement procedures for national

competitive bidding for the procurement of

goods and services in AfDB-funded projects;

and (ii) the outcomes of the fiduciary clinics

organized from March 201433

.

4.2.8 The overall portfolio performance is

significantly better. There is, indeed, a notable

increase in the speed of financial execution and

disbursement rates, especially in the water and

sanitation sector (10th and 11th DWS) since

early 2014, except for the 12th Marrakech

DWS. The quality of audit reports has improved,

thanks in part to the accuracy of the financial

information presented in the audited annual

financial statements for FY2012. In general,

auditors´ opinions on these financial statements

were acceptable to the Bank and the number of

Bank reservations were fewer compared to

FY2011. Nonetheless, the Bank remains

concerned by the poor scores for the annual

financial statements transmitted by executing

agencies and external auditors. Furthermore, the

transmission of interim financial reports remains

irregular. The procedure for monitoring audit

recommendations and Bank supervision

missions is neither systematic nor formalized

through a regularly updated master plan. This

situation stems from the fact that 83% of the

administrative, financial and accounting

management services of projects are not

informed by audit review recommendations at

the level of their executing agencies.

4.2.9 Activities and Achievements:

activities and achievements are generally better

than in 2013, mainly due to progress in DWS

projects. Nonetheless, the number of project

extensions, especially those financed with

grants, has increased. These extensions result

from delays in the recruitment of consultancy

firms or approval of terms of reference

(Technical Support Project for the Promotion of

Young Entrepreneurs and Technical Support

Project for the Development of Irrigation

Infrastructure). The extension of

implementation deadlines also results from the

complexity of certain projects such as the 11th

DWS. For certain loans, the non-completion of

works and/or payments (PNR II, 3rd Airport

Project) have caused additional delays34

.

4.2.10 During the workshop on grants held as

part of the review, it was proposed that a more

rigorous monitoring indicator on physical

progress status be included. It is true that

operations could have an adequate disbursement

rate and yet be inefficient in terms of physical

execution.

4.2.11 As regards exposure to risks, in 2013 the

Bank streamlined its portfolio through partial

cancellation of funds allocated to two projects

and amounting to UA 141.3 million. In 2013,

the portfolio no longer had any risky projects.

Nonetheless, in March 2014, the 12th DWS was

-13-

classified as a PPP, since its commencement

was delayed by the cancellation of AFD

financing, among other reasons. The Bank is

working with ONEE to speed up procurements

and ensure a first disbursement in July 2014 (17

months after its approval) so that the project can

be removed from the PPP category35

.

4.2.12 A number of operations finalized end-

December 2013 were financially closed as of

31 March 2014, namely two grants: POS,

Haouz Groundwater Replenishment, and the 9th

DWS loan. These projects show satisfactory

results and their balances were either cancelled

or are in the process of cancellation (9th DWS).

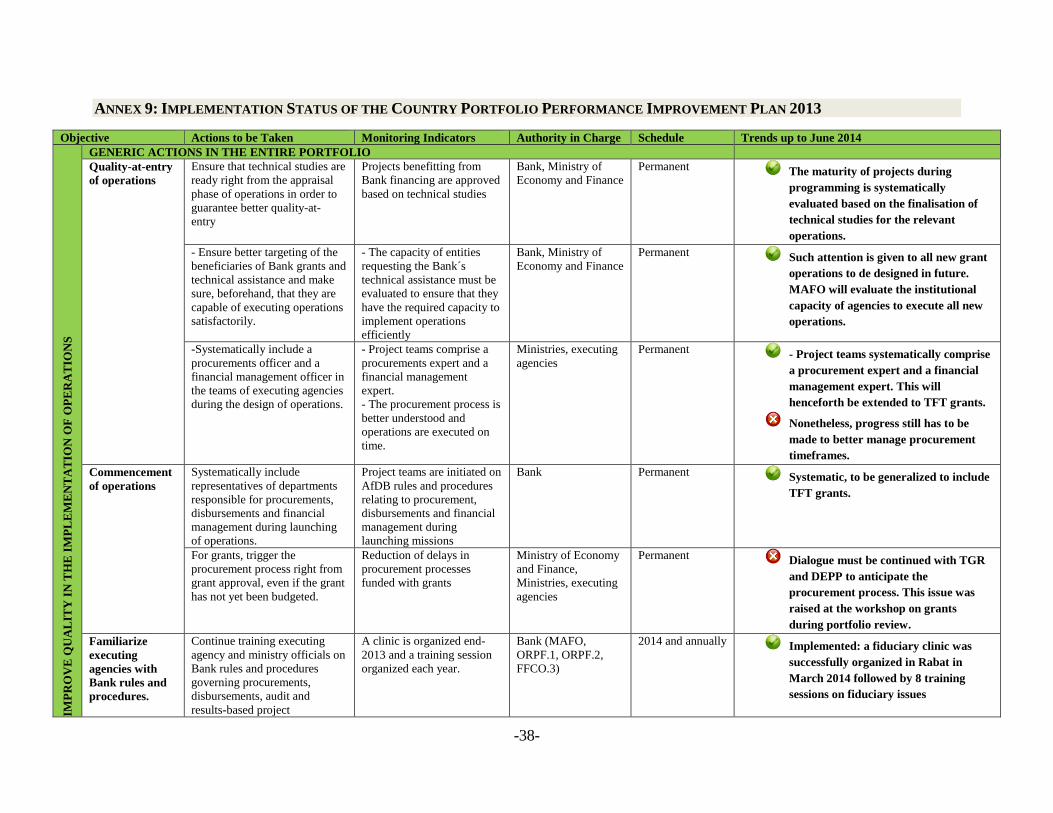

4.3 PPIP Implementation Status

4.3.1 The implementation of the 2013 PPIP is

satisfactory: project quality-at-entry and

monitoring have improved. The project

portfolio has also been enhanced. Portfolio

operations have experienced no supervision

delays. The maturity of projects in conducting

programming is analysed in terms of the

finalisation of technical studies36

. Teams

responsible for project design currently coopt

procurement and financial management experts.

4.3.2 Since March 2014, there has been an

upsurge in training thanks to the fiduciary

clinics organised to acquaint the executing

agencies with Bank rules and procedures.

4.3.3 Since the last portfolio review in 2013,

the Bank has significantly restructured its

operations with a view to streamlining its

portfolio and generating financing margins for

new operations. This pro-activeness led to the

cancellation of UA 141 million through

restructuring of the 3rd

Airport Project, as well

as the partial cancellation of the loan for the 11th

DWS Project37

. These cancellations of non-

performing components were motivated by

enhanced dialogue with partners, savings

generated during the procurement process, or

the use of new and cheaper technologies while

maintaining the initial project targets (11th

DWS). These cancellations freed up resources

for the financing of PARCOUM III (approved

by the Board approved in late 2013).

4.4 Bank Group Performance

4.4.1 The Bank’s performance remains

satisfactory. MAFO’s proactiveness helped to

improve certain project performance indicators,

including those relating to compliance with

conditionalities and financial performance.

Project supervision (over 74% undertaken by

MAFO) as well as proximity to partners and the

many training sessions attest to MAFO’s

dynamism through the entire project cycle.

Upstream, the programming of fully mature

projects has been well mastered thanks to a

constant dialogue with the authorities and

partners whose involvement should be increased

at various stages of the project cycle. Active

attention to quality-at-entry will help to achieve

significant progress for future operations

identified. More realistic conditionalities for

operations, submission of documents that fulfill

the requisite Bank conditions, reduction of

timeframes for forwarding such documents and

dialogue with the authorities remain crucial

determinants.

Table 3: Portfolio Performance

Indicators 2011 2012 2013 Mid-

2014 Portfolio of Operations

Number of projects 27 27 28 33(

Projects managed by MAFO (%) 50% 58% 74% 74%

Total commitments (UA billion) 1.8 2 2.3 1.8(2)

Risky projects (%) 0 1 0 1(3)

Risky commitments (%) 0 15.5 0 7%

Rate of audit submission (%) 100 100 038 NA

Portfolio Management Average effectiveness timeframe (month)

6.9 6.4 6 4.9

Proactivity index (%) - - 100 NA Projects supervised at least twice/year

(%) - 50 70 100

Number of grant proposals initiated by

MAFO and approved - - 6 2

Number of files processed on time /

total number of files received -

-

62/11

4

23/47

Sector experts posted to MAFO 4 6 7 7

Fiduciary experts posted to MAFO 1 2 2 2

Projects approved in the course of the year Project 3 8 5 4

Commitment (UA million) 421 947 204 245

4.5 Country Performance Outcomes Based

on the Questionnaire on Portfolio Quality

4.5.1 The answers to the questionnaire on

portfolio quality were discussed with the

executing agencies present at the feedback

workshop. Quality-at-entry as well as the

conditions precedent to effectiveness and first

disbursement were deemed appropriate.

-14-

Although the executing agencies deemed

MAFO´s procurement service to be competent,

they still expressed the wish to shorten the time

limit for processing Notices of No Objection

(NNO). The agencies expressed their

satisfaction with the disbursement and audit

processes.

4.5.2 The proposals identified by the executing

agencies to improve portfolio quality include:

(i) anticipation of land-related problems during

operations design; (ii) simplification of

procurement procedures by focusing on ex post

controls; (iii) increase of NNO thresholds to

strengthen the validation of procurements at

MAFO level; and (iv) the possibility of

introducing an information system and

ultimately an electronic signature for

disbursement requests.

4.6 Conclusions of Meetings with

Stakeholders

4.6.1 Two workshops and one fiduciary clinic

session (specifically on the consultant

recruitment process) were organized during the

review. These workshops were: a specific

workshop on grants as well as the dialogue and

feedback workshop on the 2014 portfolio