1

Analyzing the Structure of Jordanian Pharmaceutical Industry

By

Mohammad Alomari1, Nahil Saqfalhait2

The University of Jordan

ABSTRACT

This paper aims to analyze the structure of pharmaceutical industry in Jordan

during the period 2004 – 2012 by investigating the level of industrial concentration, the

industrial entry barriers, and the product differentiation within the industry. Additionally,

determinants for the pharmaceutical industry in Jordan were examined. The questions of this

study are: do firms in pharmaceutical industry in Jordan have satisfactory level of competition

or some firms dominate the market with large market power? How these issues have

developed over time? What are the main characteristics of the structure of this industry?

The concentration measures have revealed that the pharmaceutical industry in Jordan

has oligopoly market structure in which few large firms dominate the market. Those firms are

characterized by the acquisition of the largest market share, as well as possessing high

production capabilities that help them to differentiate their products and to reduce production

costs.

Key Words: Pharmaceutical Industry, Market Share, Market Structure,

Concentration.

1. Introduction

Jordan pharmaceutical industry was established since 1962, and has become

one of the most important Jordanian industrial strategic sectors that support the

1 - Assistant Professor, Economics and Administrative Sciences Department, University of Nizwa,

Sultanate of Oman . Email: [email protected] 2 - Associate Professor, Department of Business Economics, University of Jordan, Jordan. E-mail:

2

national economy by its contribution in GDP and the total national exports. The

ranking of this sector came in the second place in the total Jordanian exports for the

year 2012 (Jordanian General Statistics Department, 2013). Consequently, Jordan has

become the only country in the geographical surroundings that exports more than its

imports of medicine (Jordan Chamber of Industry, 2013). So, this sector is considered

as one of the leading sectors, which began manufacturing in the beginning of sixties

and developed continually until it become a symbol of national industry.

Most of the production of local pharmaceutical firms is exported to the

Middle East and the Arab world countries as a result of its good quality and

conformity to the best international standards and specifications. Jordanian market is

characterized by its openness and competition, where no restrictions on foreign

ownership or capital transfers. In addition, Jordan is one of the most countries that has

an obligation to protect intellectual property rights, which is very important for such

industry. Moreover, the availability of qualified labor and efficient specialists in this

field is considered one of the most important advantages for this sector.

During the last fifty years, many changes have occurred in the

pharmaceutical industry and the market for pharmaceutical products. The questions of

this study are: do firms in pharmaceutical industry in Jordan have satisfactory level of

competition or some firms dominate the market with large market power? How these issues

have developed over time? What are the main characteristics of the structure of this industry?

In light of this, the aim of this paper is to investigate and analyze Jordan’s

pharmaceutical industry. A historical development of the pharmaceutical industry in

Jordan will be briefly covered in the next section. This is followed by an analysis of

the determinants of the pharmaceutical industry in Jordan. Afterward, the structure of

Jordanian pharmaceutical industry is examined including the three major dimensions:

3

concentration, entry barriers and product differentiation. The final section provides

overall conclusions and recommendations.

2. The historical development of the pharmaceutical industry in Jordan

Jordan pharmaceutical industry has achieved remarkable growth since the

first factory for Jordanian medicine was established in 1962. By the end of 2012, there

exist 17 firms for human medicines, in addition to seven research consulting

companies that support pharmaceutical factories in Jordan (JAPM. 2013).

The first firm for manufacturing human medicines, Al-Arabiya Company

for Pharmaceutical Products was established in 1962, and it has represented the

entire Jordanian pharmaceutical industry until mid-seventies. In the second half of the

seventies, new firms have entered: Dar Al Dawa'a for Development and

Investment was created in 1975, followed by Al-Hikma Pharmaceuticals in 1977,

and then the Jordanian Company for the Production of Drugs in 1978. During the

eighties, the Arab Center for Pharmaceutical Industries was established in 1983

followed by Amman Company and United Company which were created in 1989.

Throughout the nineties, the pharmaceutical industry has witnessed a significant

expansion; eight firms were created: Ram Company for the Pharmaceutical

Industry was created in 1992, followed by Philadelphia and the Middle East

Company in 1993. In 1994 the International Company for Drug was created, in

addition to Hayat Company, then Jordan Swedish Company in 1996, followed by

Al-kindy Company in 1997, and Jordan River Company in 1999. In 2003, Al-

Techania for Pharmaceutical Industries company was created which was known as

the "TREMFARMA", followed by “IFADA” for pharmaceutical industries in 2005.

4

3. Determinants of the pharmaceutical industry in Jordan

There are many factors affecting the pharmaceutical industry in Jordan. This

section briefly introduces the main determinants and obstacles facing this industry.

3.1 Availability of marketing channels

Although the pharmaceutical industry in Jordan has achieved success in

entering foreign markets through its exports which constitutes about 71% of its

production, the share of the industry from the local market is still relatively small, as

it constitutes about 29% of its total sales.(Jordanian Chamber of Industry, 2013),

which is actually a small percentage.

This industry has well-established markets in many Arab and foreign

countries, where the Jordanian medicine had scored in accordance with international

standards in about 65 countries in the continents of Asia, Africa, Europe and North

America (Jordanian General Statistics department, 2013).

However, the industry should pay attention to the local market in addition to

the export markets, with the necessity of realizing that the success of this mission

relies to a large extent on its ability to provide pharmaceutical products that meet local

market needs which are not currently fulfilled. This implies that the Jordanian

pharmaceutical industry should provide diversified products which meet the local

market needs. Even though the fact that Jordan's exports of pharmaceutical products

worth more than the value of its imports, the Jordanian pharmaceutical market is still

a net importer for most of its needs of medicines. This represents a large gap between

supply and demand in the domestic market, which provides a good opportunity to

increase the share of the Jordanian medicine in the local market by applying import

substitution policy.

5

3.2 Technical and technological knowledge

The Jordanian pharmaceutical industry owns a good level of knowledge and

expertise compared with the industry standards in the region and in developing

countries, where Jordan has become among qualified exporting countries that can

provide technical assistance for the pharmaceutical industry in many Arab and

African countries. It is worth mentioning that more than half of the current

pharmaceutical factories have been built and equipped with advanced equipment and

industrial technology, which offers significant productivity prospective (JAPM,

2010). On the other hand, the failure to best use this level of technical and

technological knowledge that is available for the pharmaceutical industry would lead

to wastage in production capacity.

3.3 Availability of human resources

The availability of trained and qualified human resources is one of the main

factors that have contributed in the development of the pharmaceutical industry in

Jordan. Statistics for the year 2012 indicate the presence of nine university colleges

that teach pharmaceutical sciences for about 7,500 students. There are also about

14,000 students in Jordanian universities who are studying medical science support

majors, in addition to community colleges that teach certain disciplines related to

medical science (JAPM, 2013). Consequently, these human resources can meet most

of pharmaceutical industry needs if these experiences do not leak into other countries.

Indeed, pharmaceutical firms should offer competitive and encouraging

working conditions, and must provide appropriate domestic working environment in

order to reduce the leakage of Jordanian qualified medical manpower into abroad.

6

3.4 Research and development

After tracing the pharmaceutical industry in Jordan, it can be observed that

the requirements of scientific research and development are still incomplete. Most

pharmaceutical products produced by pharmaceutical firms in Jordan are imitation for

original foreign pharmaceutical products which are manufactured given the approval

from the multinational companies, and this is a clear indication that the manufacturing

of drug policy in Jordan does not support scientific research.

The proportion of spending on research and development was about 4%

of total sales in the pharmaceutical industry in 2011, and the estimated number of

employees in research and development is about 5% only of the total workforce in

this sector (JAPM, 2010).

It is worth mentioning in this regard that the Committee of Economic

Conversation headed by Minister of Industry and Commerce in Jordan had

recommended in 2011 the need to strengthen the pharmaceutical industry sector

exports through increasing competitiveness of Jordanian pharmaceutical industry and

encouraging research and development in this sector .

3.5 Energy prices and costs of production

During 2010–2012, Jordan have experienced a continuing rises in the prices

of oil derivatives and energy; which had resulted in higher production costs, and

lower profit margins among producers.

In fact, high energy prices represent a major impediment to the development

of the pharmaceutical industry and to the level of its competitiveness; especially it

represents an important export industry.

7

4. Analysis of the structure of pharmaceutical industry in Jordan

The concept of industry structure is used to express the basic characteristics

of the market that could have an impact on the behavior and performance of firms.

Consideration could be given to the structure of the industry in terms of the nature and

shape of the market and the extent of the existence of monopolistic factors or

competitive factors in the market. The most important factors affecting the market

structure include the following (Al-Ma'mari. 2010):

1- The level of industrial concentration.

2- The industrial entry barriers.

3- Product differentiation within the industry.

4.1 The industrial concentration

Industrial concentration refers to the extent to which the production of the

industry is concentrated in the hands of a limited number of firms. This index is based

on the number of firms in the industry and their relative sizes. It measures the relative

distribution of total output of the industry among firms within that industry. Thus, the

basic elements in the measurement of industrial concentration are: the number of

establishments in the industry, the size of each one represented by its market share

and the percentage of their contribution to the overall size of the industry.

One visual general measure is the so-called (Concentration Curve), where

the cumulative percentage of the industry's output, represented by the total market

share of the firms is express on the vertical axis, and the cumulative number of firms

arranged from largest to smallest is express on the horizontal axis, as can be shown in

figure (1).

8

Figure 1: Concentration curve for three industries A, B, C

According to the definition of market concentration, it can be inferred

that if the concentration curve of the industry is higher than the other curves, then it

will have higher concentration compared to other industries. In figure 1, it can be said

that industry A has the highest concentration among the three industries.

The relative size of the firm can be measured through (Market Share),

where the firm's market share is calculated by dividing the value of its sales on total

sales of the industry, as indicating by equation (1) (David and Bernadette, 2001):

Market Share (MS) =

……..…….. (1)

After the market shares of the largest r firms in the industry are calculated,

then the concentration ratio can be measured as indicated by equation (2) as follows:

Concentration Ratio (CRr) = ; (i=1, 2, .., r) … . (2)

Where i refers to each firm within the industry, and r refers to the largest

firms in the industry. The most commonly used is "CR4".

9

An increase in the degree of concentration (CR≈1) means increasing the

extent of monopoly in the market. Conversely, the low degree of concentration

(CR≈0) means an increase in the level of competition in the market.

To calculate the concentration coefficient for all operating firms in an

industry, Herfindahl Index (HI) is used, which is equal to the sum of squared market

shares for all operating firms in the industry, as indicated by equation(3) as follows:

2 ; (i = 1, 2, …….,n) ……(3)

Where n refers to the number of firms in the industry. If the concentration

ratio using the HI index is less than 10%, then it is referred to be low concentration,

which indicates the presence of competition between firms that are operating in the

industry. However, if the value of HI index is greater than 18%, then it is referred to

be high concentration in the industry, which indicates the presence of some

monopolistic power for some firms in the industry.

4.1.1 Measuring the degree of concentration in the Jordanian pharmaceutical

market

This paper measures the industrial concentration for pharmaceutical firms

that are members in the Jordanian Association of Pharmaceutical Manufacturers

(JAPM) for the two years 2004 and 20083. The number of these firms is 13 out of 17

firms in the Jordanian pharmaceutical market. The industrial concentration will also

be calculated for the seven pharmaceutical firms listed on the Amman Stock

Exchange according to the latest data available for the year 2013. The industrial

concentration will be calculated based on each firm’s market share of total sales using

the concentration indicators that have been mentioned previously.

3- Data is not available after 2008.

11

4.1.2 Concentration indicators for pharmaceutical firms that are members in the

JAPM in 2004

Pharmaceutical firms registered in the JAPM are 13; seven of them are listed

in the Amman Stock Exchange, while six are not listed. Table 2 shows the total sales

value for pharmaceutical firms that are members in the JAPM in 2004.

Table (1): The value of total sales for pharmaceutical firms that are members in

the JAPM in 2004

Firms that are members in the JAPM and listed in Amman Stock Exchange

Total Sales (JD) Exports (JD) Domestic Sales (JD) Firm No.

10,335,000 9,027,000 1,308,000 Jordanian

Company 1

28,410,000 22,444,000 5,966,000 Dar Al-dawa'a 2

2,014,000 783,000 1,231,000 Alhayah Company 3

3,308,000 1,903,000 1,405,000 Middle East

company 4

1,584,000 1,072,000 512,000 Philadelphia 5

NA NA NA Alkindy company 6

4,013,000 2,127,000 1,885,000 Arab Center 7

49,664,000 37,356,000 12,307,000 Subtotal

Firms that are members in the JAPM and not listed in Amman Stock Exchange

Total Sales (JD) Exports (JD) Domestic Sales (JD) Firm No.

24,993,000 16,154,000 8,839,000 Al-Arabiya

Company 8

68,033,000 58,546,000 9,487,000 Al-Hikma 9

7,927,000 NA NA United Company 10

6,391,000 4,197,000 2,194,000 International

Company 11

1,452,000 347,000 1,105,000 Jordan Swedish

Company 12

556,000 223,000 333,000 Jordan River

Company 13

109,352,00

0 79,467,000 21,958,000 Subtotal

159,016,00

0

116,823,00

0 34,265,000

Total

0.31 0.31 0.35 The proportion of Sales of listed firms

to the total aggregate sales Reference: Jordanian Association of Pharmaceutical Manufacturers, 2010 data base.

After arranging firms by sales from the largest to the smallest, market shares

were calculated as shown in Table (2).

11

Table (2): The market shares for pharmaceutical firms that are members in the

JAPM in 2004

Market Share

(MS)* Total Sales (JD) Firm No.

42.70% 68,033,000 Al-Hikma 1

17.80% 28,410,000 Dar Al-dawa'a 2

15.70% 24,993,000 Al-Arabiya Company 3

6.40% 10,335,000 Jordanian Company 4

4.90% 7,927,000 United Company 5

4% 6,391,000 International Company 6

2.5% 4,013,000 Arab Center 7

2% 3,308,000 Middle East company 8

1.20% 2,014,000 Alhayah Company 9

0.90% 1,584,000 Philadelphia 10

0.90% 1,452,000 Jordan Swedish Company 11

0.30% 556,000 Jordan River Company 12

NW NW Alkindy company 13

159,016,000 Total

* calculated by researchers based on the MS equation.

To calculate the concentration index CR2, market shares of the two biggest

firms in the industry (Al-Hikma Pharmaceuticals, and Dar Al Dawa'a) were

calculated.

CR2 = 0.427+ 0.178 = 0.605

Thus, it can be said that the two biggest pharmaceutical firms control 60.5 %

of the total market, which indicates the existence of monopoly power in the

pharmaceutical market in 2004.

The four largest firms in the market are: Al-Hikma Pharmaceuticals, Dar Al

Dawa, Al-Arabiya, and Jordanian Company. Based on that, the concentration index

CR4 was calculated as follows:

CR4= 0.427 + 0.178 + 0.157 +0.064 = 0.826

12

That is, the market share of the four largest firms in pharmaceutical market

equals to 82.6% which indicates the presence of monopoly power in the

pharmaceutical market. By calculating the cumulative percentage of the market share

for pharmaceutical firms that are members in the JAPM in 2004, a concentration

curve can be drawn as shown in Figure (2).

Figure 2: Concentration curve for pharmaceutical firms that are members

in the JAPM in 2004

Clearly, the concentration curve in Figure (2) has a convex shape as a

result of the large discrepancy among the sizes of firms expressed in market share.

This implies an increase in the contribution of large firms in the overall size of the

industry, and thus a higher degree of concentration and monopoly power.

The HI index was calculated as previously stated by the sum of squares of

market shares for pharmaceutical firms that are members in the JAPM, as can be

shown in table (3).

0

10

20

30

40

50

60

70

80

90

100

0 1 2 3 4 5 6 7 8 9 10 11 12 13

Cu

mu

lati

ve P

erce

nta

ge

of

Mar

ket

Shar

e %

Cumulative Number of Firms Ranking From Largest to Smallest

13

Table 3: HI index for pharmaceutical firms that are members in the JAPM in

2004

(MS)2

Market

Share (MS)* Firm No.

18.23% 42.70% Al-Hikma 1

3.16% 17.80% Dar Al-dawa'a 2

2.46% 15.70% Al-Arabiya Company 3

0.40% 6.40% Jordanian Company 4

0.20% 4.90% United Company 5

0.10% 4% International Company 6

0.06% 2.50% Arab Center 7

0.04% 2% Middle East company 8

0.01% 1.20% Alhayah Company 9

0.008% 0.90% Philadelphia 10

0.008% 0.90% Jordan Swedish

Company 11

0.0009% 0.30% Jordan River Company 12

NW NW Alkindy company 13

HI=24% Total

Consequently, the ratio of the concentration using the HI index equals to

24%, which means that there is a monopoly power in the pharmaceutical market,

because (HI > % 18).

4.1.3 Concentration indicators for pharmaceutical firms that are members in the

JAPM in 2008

Concentration indices were calculated for pharmaceutical firms that are

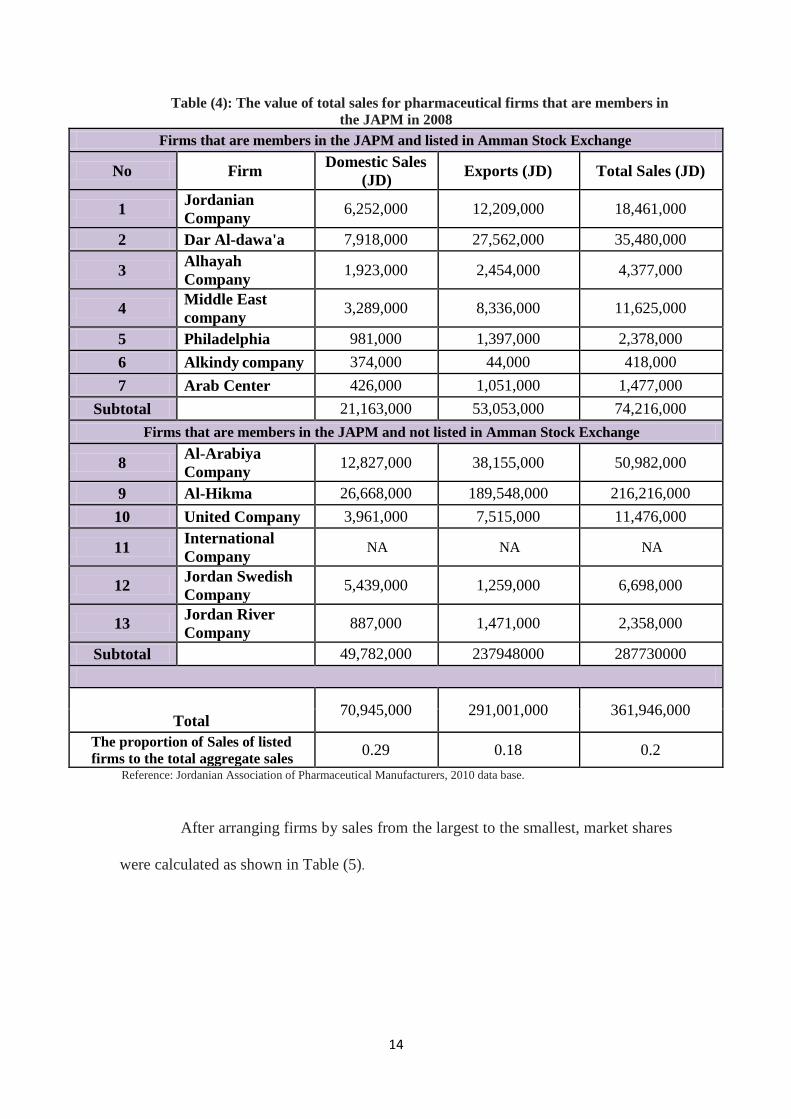

members in JAPM in 2008, using the value of total sales, as table (4) shows.

14

Table (4): The value of total sales for pharmaceutical firms that are members in

the JAPM in 2008

Firms that are members in the JAPM and listed in Amman Stock Exchange

Total Sales (JD) Exports (JD) Domestic Sales

(JD) Firm No

18,461,000 12,209,000 6,252,000 Jordanian

Company 1

35,480,000 27,562,000 7,918,000 Dar Al-dawa'a 2

4,377,000 2,454,000 1,923,000 Alhayah

Company 3

11,625,000 8,336,000 3,289,000 Middle East

company 4

2,378,000 1,397,000 981,000 Philadelphia 5

418,000 44,000 374,000 Alkindy company 6

1,477,000 1,051,000 426,000 Arab Center 7

74,216,000 53,053,000 21,163,000 Subtotal

Firms that are members in the JAPM and not listed in Amman Stock Exchange

50,982,000 38,155,000 12,827,000 Al-Arabiya

Company 8

216,216,000 189,548,000 26,668,000 Al-Hikma 9

11,476,000 7,515,000 3,961,000 United Company 10

NA NA NA International

Company 11

6,698,000 1,259,000 5,439,000 Jordan Swedish

Company 12

2,358,000 1,471,000 887,000 Jordan River

Company 13

287730000 237948000 49,782,000 Subtotal

361,946,000 291,001,000 70,945,000

Total

0.2 0.18 0.29 The proportion of Sales of listed

firms to the total aggregate sales Reference: Jordanian Association of Pharmaceutical Manufacturers, 2010 data base.

After arranging firms by sales from the largest to the smallest, market shares

were calculated as shown in Table (5).

15

Table (5): The market shares for pharmaceutical firms that are members in the

JAPM in 2008

Market

Share (MS)*

Total Sales

(JD) Firm No

59.70% 216,216,000 Al-Hikma 1

14% 50,982,000 Al-Arabiya Company 2

9.80% 35,480,000 Dar Al-dawa'a 3

5.10% 18,461,000 Jordanian Company 4

3.20% 11,625,000 Middle East company 5

3.10% 11,476,000 United Company 6

1.80% 6,698,000 Jordan Swedish Company 7

1.20% 4,377,000 Alhayah Company 8

0.60% 2,378,000 Philadelphia 9

0.60% 2,358,000 Jordan River Company 10

0.40% 1,477,000 Arab Center 11

0.10% 418,000 Alkindy company 12

NA NA International Company 13

361,946,000 Total * calculated by researchers based on the MS equation.

To calculate the concentration index CR2, market shares of the two biggest

firms in the industry (Al-Hikma Pharmaceuticals, and Al-Arabiya) were calculated.

CR2 = 0.597+ 0.140= 0.737

Thus, it can be said that the two biggest pharmaceutical firms control 73.3

% of the total market, which indicates the existence of monopoly power in the

pharmaceutical market in 2008.

The four largest firms in the market are: Al-Hikma Pharmaceuticals, Al-

Arabiya, Dar Al Dawa'a, and Jordanian Company. Based on that, the concentration

index CR4 was calculated as follows:

CR4= 0.597+ 0.140 + 0.098 +0.051 = 0.886

That is, the market share of the four largest firms in pharmaceutical market

equals to 88.6% which indicates the presence of monopoly power in the

pharmaceutical market. By calculating the cumulative percentage of the market share

16

for pharmaceutical firms that are members in the JAPM in 2008, a concentration

curve can be drawn as shown in Figure (3).

Figure 3: Concentration curve for pharmaceutical firms that are members

in the JAPM in 2008

Clearly, the concentration curve in Figure (3) has a convex shape as a

result of the large discrepancy among the sizes of firms expressed in market share.

This implies an increase in the contribution of large firms in the overall size of the

industry, and thus a higher degree of concentration and monopoly power.

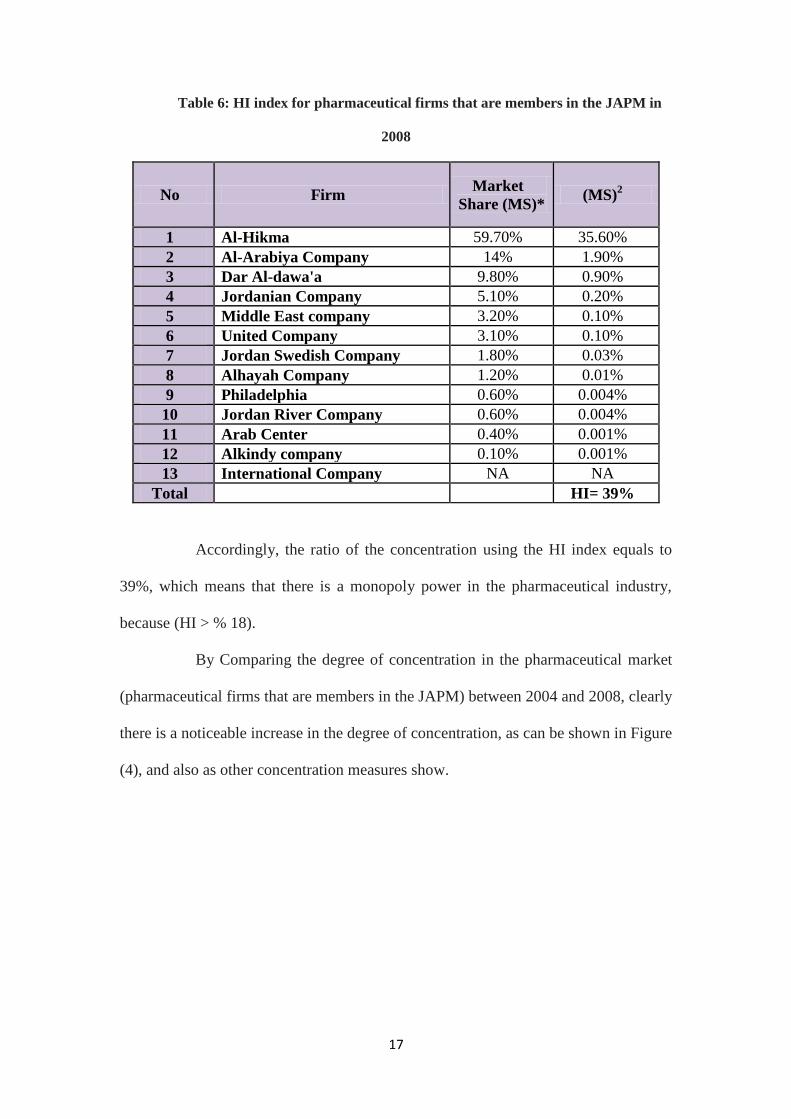

The HI index was calculated as previously stated by the sum of squares of

the market shares for pharmaceutical firms that are members in the JAPM, as can be

shown in table (6).

0

10

20

30

40

50

60

70

80

90

100

0 1 2 3 4 5 6 7 8 9 10 11 12 13

Cu

mu

lati

ve P

erce

nta

ge

of

Mar

ket

shar

e %

Cumulative Number of Firms Ranking from Largest to Smallest

17

Table 6: HI index for pharmaceutical firms that are members in the JAPM in

2008

(MS)2

Market

Share (MS)* Firm No

35.60% 59.70% Al-Hikma 1

1.90% 14% Al-Arabiya Company 2

0.90% 9.80% Dar Al-dawa'a 3

0.20% 5.10% Jordanian Company 4

0.10% 3.20% Middle East company 5

0.10% 3.10% United Company 6

0.03% 1.80% Jordan Swedish Company 7

0.01% 1.20% Alhayah Company 8

0.004% 0.60% Philadelphia 9

0.004% 0.60% Jordan River Company 10

0.001% 0.40% Arab Center 11

0.001% 0.10% Alkindy company 12

NA NA International Company 13

HI= 39% Total

Accordingly, the ratio of the concentration using the HI index equals to

39%, which means that there is a monopoly power in the pharmaceutical industry,

because (HI > % 18).

By Comparing the degree of concentration in the pharmaceutical market

(pharmaceutical firms that are members in the JAPM) between 2004 and 2008, clearly

there is a noticeable increase in the degree of concentration, as can be shown in Figure

(4), and also as other concentration measures show.

18

Figure 4: Concentration curve for pharmaceutical firms that are members

in the JAPM in 2004 and 2008

Based on the (HI) index, the degree of concentration increased from 24% in

2004 to 39% in 2008. This apparent increase in the level of concentration indicates an

increase in the monopoly power in the pharmaceutical market as a result of the

increase in Al-Hikma Pharmaceuticals market share from 42.7 % in 2004 to 59.7 % in

2008, in addition to the large market share for other firms like Al-Arabiya, Dar Al

Dawa'a, and Jordanian Company compared with other firms in the market. In contrast,

the market share for some firms tended to decline, which may threaten the continuity

of these firms in the Jordanian pharmaceutical market. It can be noted that Al-Hikma

has achieved apparent success in entering the local and international markets, and it

was able to establish a well-built investment base at the local and global levels. Al-

Arabiya company also has expanded its investment size at local and global levels

(these two firms are globally listed).

0

10

20

30

40

50

60

70

80

90

100

0 1 2 3 4 5 6 7 8 9 10 11 12 13

Cu

mu

lati

ve P

erce

nta

ge

of

Mar

ket

Shar

e %

Cumulative Number of Firms Ranking From Largest to Smallest

Concentration Curve in 2008

Concentration Curve in 2004

19

4.1.4 Concentration indicators for the listed pharmaceutical firms in Amman

Stock Exchange in 2012

Concentration indicators can be measured for listed pharmaceutical firms in

Amman Stock Exchange by using industry’s sales value as in the table (7), and the

market share for each firm, as in the table (8).

Table (7): The value of total sales for pharmaceutical companies listed in

Amman Stock Exchange in 2012

Total Sales

(JD)

Exports

(JD)

Domestic

Sales (JD) Firm No

35,853,042 23,836,068 12,016,974 Jordanian Company 1

52,448,416 42,727,786 9,720,630 Dar Al-dawa'a 2

8,443,660 3,446,625 4,997,035 Alhayah Company 3

10,111,306 6,366,852 3,744,454 Middle East company 4

1,255,254 844,960 410,294 Philadelphia 5

299,976 42,103 257,873 Alkindy company 6

1,744,587 1,487,005 257,582 Arab Center 7

110,156,241 78,751,399 31,404,842 Total Reference: Amman Stock Exchange, companies' disclosures, the pharmaceutical sector,

annual reports 2012.

After arranging the firms by sales from the biggest to the smallest, market

shares can be calculated as shown in Table (8).

Table (8): The market shares for listed pharmaceutical firms in 2012

Market

share

)MS)*

Total Sales (JD) Firm No

47.60% 52,448,416 Dar Al-dawa'a 1

32.50% 35,853,042 Jordanian Company 2

9.10% 10,111,306 Middle East company 3

7.60% 8,443,660 Alhayah Company 4

1.50% 1,744,587 Arab Center 5

1.10% 1,255,254 Philadelphia 6

0.20% 299,976 Alkindy company 7

110,156,241 Tota

l * calculated by researchers based on the MS equation.

21

To calculate the concentration index CR2, market shares for the two biggest

firms in the industry (Dar Al Dawa'a, and Jordanian Company) were calculated as

follows:

CR2 = 0.476+ 0.325= 0.801

Thus, the two biggest pharmaceutical listed companies control 80.1% of

the industry among the listed firms.

Given the market shares for the four biggest firms in the industry, the

concentration ratio CR4 was also calculated using the industrial concentration index as

follows:

CR4= 0.476 +0.325 +0.091 +0.076 = 0.968

That means that industrial concentration ratio CR4 among the listed

pharmaceutical firms equals to 96.8 %, which highly indicates the presence of

monopoly power in the pharmaceutical industry. By calculating the cumulative

percentage of the market share for listed pharmaceutical firms in 2012; a

concentration curve can drawn as shown in Figure (5).

Figure 5: Concentration curve for listed pharmaceutical companies in 2012

0

10

20

30

40

50

60

70

80

90

100

0 1 2 3 4 5 6 7

Cu

mu

lati

ve P

erce

nta

ge

of

Mar

ket

Shar

e %

Cumulative Number of Firms Ranking From Largest to Smallest

21

The shape of the concentration curve in Figure (5) tends to convexity

due to the large disparity among firms in terms of market share, which led to a huge

contribution for the biggest firms in the overall size of the industry, resulting in a

higher degree of monopoly power.

HI index also was calculated as can be shown in table (9) which was equal

to 33%, representing high level of concentration and monopoly power among

pharmaceutical companies that are listed in Amman Stock Exchange in 2012, where

(HI> 18%).

Table 9: HI index for listed pharmaceutical companies in 2012

(MS)2

Marke

t share (MS)* Firm

N

o

22.60% 47.60% Dar Al-dawa'a 1

10.50% 32.50% Jordanian Company 2

0.80% 9.10% Middle East company 3

0.50% 7.60% Alhayah Company 4

0.02% 1.50% Arab Center 5

0.01% 1.10% Philadelphia 6

0.00% 0.20% Alkindy company 7

HI =

%33

T

otal

In short, the pharmaceutical market in Jordan is highly concentrated, where

it controlled by small number of pharmaceutical firms which have the biggest market

share, and therefore it can be classified as oligopoly. The excessive concentration in

the industry may be attributed to the increase in aggregate demand for pharmaceutical

products, leading to a widening market share by the biggest firms. Additionally, some

firms merged together which have increased the market share of the resulting firms as

in 2004 when Al-Razi company merged with the Jordanian company, also Al-

Motatawera company merged with the Al-Arabiya company (JAPM, 2010), such type

of merging leads to the increase of the degree of industrial concentration. Besides, the

22

decrease in the prices of competing imported pharmaceutical products in the domestic

market could lead some firms to exit from the industry because their inability to

compete, leading to the increase in the degree of concentration too. As well, the

existence of entry barriers in pharmaceutical market supports the increase in

concentration trend.

4.2 Entry barriers to pharmaceutical market

Entry barriers constitute the second dimension of the market structure. It

involves all the obstacles and reasons that prevent or limit the entry of new firms to a

specific industry. Actually, more obstacles will lead to the decrease of the number of

firms in an industry, leading to the increase of the concentration and the monopoly

power in the industry. The most important entry barriers can be summarized as

follows (Michael, 1998):

4.2.1 Legal barriers

These include the presence of legal barriers by government or law that

prevent the entry of new firms to the market. In pharmaceutical sector in Jordan, there

are no legal barriers to new entrants to the industry or market, as there are no

privileges granted by the Jordanian government for pharmaceutical firms to do its

business.

23

4.2.2 Large scale of production necessary to take advantage of economies of

scale

Some industries especially heavy industries are characterized by large

production volume in order to reach optimal size, which achieves the minimum

average cost.

In the pharmaceutical industry in Jordan, it can be seen the rise in the

volume of production for some firms (Dar Al Dawa'a, and the Jordanian company),

where the market share of these two firms was equal 47.6 %, 32.5 % respectively of

the total sales of the pharmaceutical firms listed in Amman Stock Exchange in 2012.

That is, these two firms cover about 80% of total industry sales, which could

constitute a barrier to entry of new firms to the market. Moreover, if the unlisted firms

are taken into account, it is notable that the pharmaceutical market is dominated by

the excessively growing two globally listed companies: Al-Hikma and Al-Arabiya,

which together acquired about 74 % of the pharmaceutical market in 2008, as stated

previously, which makes entry to the pharmaceutical industry by new firms extremely

difficult.

4.2.3 Advantages for already existing firms in the industry

There are advantages which make the average cost of production for

incumbent firms less than the average cost facing new potential entrants to the

industry. This may be attributable to several reasons such as: first, possession of

patents by old firms, second, the ability of old firms to get factors of production (such

as land and raw materials) at lower cost in comparison with the new firms, and third,

the ability of old firms to easily access financial sources at lower cost in comparison

with the new firms because of their financial strength and experience.

24

Even though there is no clear evidence regarding these factors in Jordanian

pharmaceutical industry, new firms stopped entering the market since the beginning

of 2000; which obviously may indicate the existence of barriers that limit the entry of

new firms to the pharmaceutical market.

4.2.4 Pricing policies by existing firms in the industry to impede the entry of new

firms

Sometimes the existing firms in the industry intend to reduce the price of the

products such that the lower price will not encourage new firms to enter the industry.

They may adopt predatory pricing policy in which price is less than or equal to the

average cost per unit. Actually, they may accept a temporary loss in order to prevent

the entry of new firms. But in Jordan, the prices of pharmaceutical products are set by

the Food and Drug institution based on certain criteria, so there is no intervention by

pharmaceutical firms in pricing of medicines.

In short, there are some barriers to entering the pharmaceutical industry in

Jordan resulting basically from the existence of monopoly power held by a few

number of pharmaceutical firms. These firms are characterized by acquiring large

market share and possessing strong production capabilities that help them to produce

at lower average cost compared with the new potential entrants.

4.3 Product Differentiation within the pharmaceutical industry

The third feature of the industry structure is the degree of product

differentiation, such that products that are sold in the same market are not fully

alternatives. Thus, product differentiation may result in acquiring monopolistic power

25

by some firms because of consumers’ loyalty to their products due to the exclusivity

of some features of their products that are not offered by other competitors. It is worth

mentioning that there is specialization of Jordanian pharmaceutical firms in the

production of various types of medication, such that the production of one

pharmaceutical firm is not a substitute for other local products, while it is an

alternative to foreign products. So, it can be said that there is a substantial level of

product differentiation in Jordanian pharmaceutical industry, which can be considered

as one of the barriers to entry for the industry and one of the main distinguishing

features of the structure of this industry.

5. Conclusions and recommendations

Pharmaceutical industry is considered as one of the most important strategic

industries in Jordan which constitutes one of the fundamental pillars for the national

economy by its effective contribution in the overall national exports. This sector is

one of the leading sectors, which began manufacturing in the early sixties and

continued to develop continually to become a symbol of national industry. In fact, the

Jordanian pharmaceutical industry was able to overcome many obstacles and

challenges, and have achieved considerable success.

After analyzing the structure of Jordanian pharmaceutical industry, it can be

inferred that it is characterized by large degree of concentration, and by the existence

of entry barriers that may be due to the increase of market size of firms and their

merging, which have resulted in more monopoly power such that few large

pharmaceutical firms produce the largest market share. Furthermore, firms in this

industry focus on specialization and product differentiation. Accordingly, this

industry is closer to oligopoly with huge market power.

26

Based on these results, it is recommended that government and parties who

are in charge of this sector should facilitate the entrance of Jordanian producers and

support them in order to be able to compete with the already existing international

producers. A good chance still available for new producers, or new producing

channels for already existing ones to focus on medical products that can meet

domestic demand which is still poorly met or completely not fulfilled. In heart of

this, attention should be paid toward research and development.

References

- Al-Ma'mari, Abdul Ghafour (2010), industrial production economies, 1st edition,

Dar Wael for publication, Amman - Jordan.

- Amman Stock Exchange (2012), companies' disclosures, the pharmaceutical sector,

annual reports, Amman, Jordan.

- David Jacobson and Bernadette Andreosso (2001), “Industrial Economics and

Organization”, (Hand Book), the McGraw-Hill Book Company, Uk.

-JAPM “Jordanian Association of Pharmaceutical Manufactures” (2010),

Pharmaceutical Industry Data Bank, Amman, Jordan.

- JAPM “Jordanian Association of Pharmaceutical Manufactures” (2013), Website:

http// www.JAPM.com

- Jordan Chamber of Industry (2013), industrial sectors, therapeutic industries and

medical supplies, Amman, Jordan.

- Jordanian general Statistics Department. Economic Survey, foreign trade statistics

2013, Website: .http// www.DOS.gov.jo.

- Michael Porter (1998), “Competitive Strategy”, (Hand Book), Free Press House,

Mumbai.