Download - Msme Ppt Final

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 1/27

Presented by:

Preeti Sagar Mishra(10DF043)

Sudipta Neogi(10DF044)

Glory Sinha(10DF045)

I.Menka(10DF046)

Alok Agarwal(10DF047)

Himanshu S. Sahoo(10DF048)

Nishant Nanda(10DF049)

TM

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 2/27

Flow of presentation Introduction

Market potential

Manufacturing process

Quality control Pollution control

Implementation Schedule

Assumptions

Cost of project

Working Capital Requirement

Means of finance

Profitability Statement

Cash Flow Statement

Projected Balance Sheet

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 3/27

INTRODUCTION Why is the project chosen????

Water is very essential for all living things. Drinking

water contains some useful minerals such as sulphur,iron, manganese, calcium which are essential and

useful for human body to regulate certain body

functions.

It has been provided in survey of WORLD HEALTHORGANISATION(WHO) that 80% of the diseases

are water borne.

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 4/27

In addition to biological and chemical contamination

water sources are often polluted by external sourcesmaking them totally unsafe foe drinking purposes.

The water which is free from physical, chemical and

biological contamination but at the same time having alladequate minerals is called Mineral Water.

Due to health consciousness and living standard there is

great demand of mineral water in hotels, restaurants,

tourism dept. railway dept.

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 5/27

It is also becoming fashion in conferences, parties,

meetings and other celebrations.

Soft drink beverages such as cola type, oranges, lime,lemon, ginger etc. have become very popular in recent

years.

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 6/27

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 7/27

MARKET POTENTIAL Mineral water has tremendous marketing

possibilities.

Middle class of customer segment of the society.

Demand in hotels, restaurants, tourism dept., railways etc.

Demand due to availability of mineral water in pouches of small size like 250ml, 300ml etc.

Demand in mainly marriage parties, picnic, snack shops,

wine shops etc.

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 8/27

Demand for 20 litres jars are consumed mainly in

conferences, marriage parties, offices, hotels and houses.

The customers range from a 5 star hotel to a cinema hall toa small eating place and a pan shop.

In the state of Odissa there are only about 7 to 8 unitsmanufacturing mineral water in small scale sector mainlylocated in Rourkela, Cuttack, Bhubaneswar, Berhampur

and Puri. Still there exists plenty scope for setting up of small scale units for the manufacture of mineral water inthe state.

The proposed scheme is prepared for mineral waterpacked in PET bottels.

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 9/27

MANUFACTURING PROCESSWATER TREATMENT

BOTTLE WASHING AND CHECKING

SUGAR SYRUP MAKINGBLENDING OF INGREDIENTS AND CHIILING

PREPARATION OF CHILLED CARBONATED

WATERFILLING UP SYRUP AND CARBONATED WATER

CROWN CORKING AND SHAKING

INSPECTION

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 10/27

QUALITY CONTROL

Raw material from the proposed source has to be tasted in

laboratory for the presence of various impurities based on

which suitable line of treatment is designed to provide

water free from physical, chemical and biological

contamination.

Energy coservation

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 11/27

Parameter Drinking water

(IS:10500)

Mineral Water

(IS:13428)

1 pH 6.5-8.5 6.5-8.5

2 Colour(Pt-Co units) 5-25 5 Max

3 Turbidity 5-10 5 Max

4 Total dissolved

solids

500-2000 1-500

5 Alkalinity as CaCo3 200-600(H2Co3) 600

6 Chlorides as CI 250-1000 200

7 Sulphates as So4 200-400 250

8 Total hardness as

CaCo3

300-600 300

9 Calcium as Ca++ 75-200 40

10 Magnesium as

Mg++

30-100 20

11 Nitrates as No3 45-100 45 Max

12 Floride as F 1-1.5 1.0 Max

13 Total Iron as Fe 0.3-1 0.3 Max

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 12/27

POLLUTION CONTROL

There is no pollution being emitted in the manufacture of

distilled water as such no pollution control equipment are

required for the manufacture of mineral water. However,the unit should adopt proper storage and handling

practices in various operations.

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 13/27

IMPLEMENTATION SCHEDULE I. Preparation of project report : 1 month

II. Selection of site : 1/2 month

III. Arrangement of finance : 4 ½month

IV. Registration with various authorities : 1 month

V. Procurement of machinery : 1 month

VI. Recruitment of staff : 1/2 month

VII. Trial run : 1/2 month

TOTAL : 9 months

90% capacity utilization.

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 14/27

ASSUMPTIONS1. Means of finance: Debt: Equity- 2:1

2. Sales- 150 1st year to be increased 20% every year

3. Working capital requirement to remain same.4. In order to prevent working capital shortage the

promoter wants margin money for the 1st year to be

included in project cost.

5. Term loan interest rate is 17% to be paid in 5 years.

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 15/27

6. Working capital loan interest is 12%

7. 40% of sales are cost.

8. WDV method is to be followed in depreciation

BUILDING 10%

PLANT AND

MACHINERY

15%

TAX 33%

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 16/27

COST OF PROJECT LAND 25 LACS

BUILDING 32 lacs

PLANT & MACHINERY 90

WOKING CAPITALMARGIN

7.5

TOTAL 155.5

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 17/27

WORKING CAPITAL

REQUIREMENT BANKS FOLLWS NAYAK COMMITE SO ACCRODING

TO THAT WORKING CAPITAL REQUIREMENT FOR THE COMPANY IS 25% OF SALES OF 1ST YEAR!( 150

LACS)

YEAR WCR WCBF MARGIN

1 37.5 30 7.5

2 37.5 30 7.5

3 37.5 30 7.5

4 37.5 30 7.5

5 37.5 30 7.5

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 18/27

MEANS OF FINANCE AS THE COST OF PROJECT IS 155.5 LACS SO

ACCORDING TO 2:1 EQUITY RATIO:

DEBT/ TERM LOAN: 103.67

EQUITY/PROMOTERS CONTRIBUTION: 51.83

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 19/27

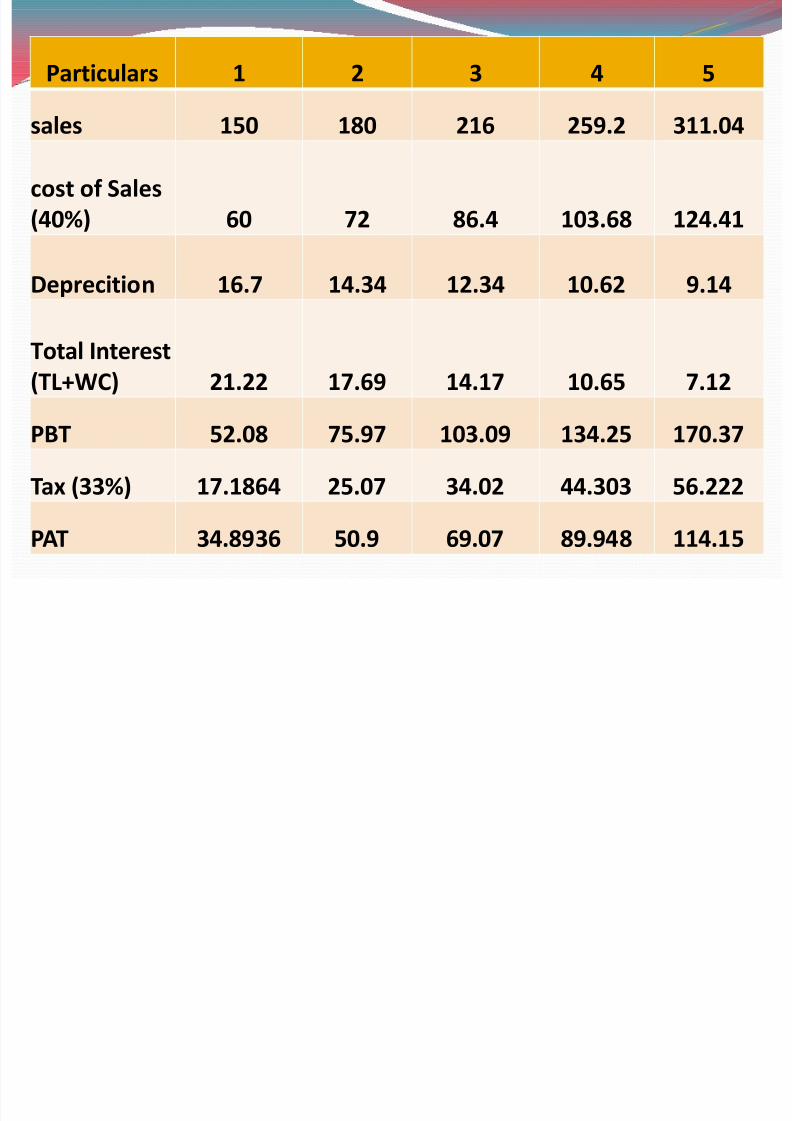

PROFITABILITY STATEMENT

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 20/27

Particulars 1 2 3 4 5

sales 150 180 216 259.2 311.04

cost of Sales

(40%) 60 72 86.4 103.68 124.41

Deprecition 16.7 14.34 12.34 10.62 9.14

Total Interest

(TL+WC) 21.22 17.69 14.17 10.65 7.12

PBT 52.08 75.97 103.09 134.25 170.37

Tax (33%) 17.1864 25.07 34.02 44.303 56.222

PAT 34.8936 50.9 69.07 89.948 114.15

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 21/27

CASH FLOW STATEMENT

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 22/27

PARTICULARS

PREOPERATIVE

YEAR 1 2 3 4 5

INFLOWS

Promoters contribution 51.83

Term Loan 103.67PAT 34.89 50.89 69.07 89.95 114.15

Dep 16.7 14.35 12.34 10.62 9.14

WCBF 30 - - - -

TOTAL INFLOW (A) 155.5 81.59 65.24 81.41 100.57 123.29

OUTFLOWS

Fixed Asset 147

Preoperative exp 1

Repayment of loan 20.73 20.73 20.73 20.73 20.73

Increase in w.c. 37.5 - - - -

TOTAL OUTFLOW (B) 148 58.23 20.73 20.73 20.73 20.73

Opening Balance 0 7.5 30.86 75.37 136.05 215.89

Cash (A-B) 7.5 23.36 44.51 60.68 79.84 102.56

9.14Closing Balance 7.5 30.86 75.37 136.05 215.89 318.45

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 23/27

PROJECTED BALANCE SHEET

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 24/27

ASSET 1 2 3 4 5

FIXED ASSET+ pre

operative 148 131.37 116.95 104.61 93.99

(-)Dep 16.7 14.35 12.34 10.62 9.14Net block 131.3 117.02 104.61 93.99 84.85

W.C.(net current asset) 37.5 37.5 37.5 37.5 37.5

Cash 30.86 75.37 136.05 215.89 318.45

TOTAL ASSET 199.66 229.89 278.16 347.38 440.8

LIABILITIES

Promoters contribution 51.83 51.83 51.83 51.83 51.83Reserve and surplus 34.89 85.79 154.86 244.81 358.96

Term loan 82.94 62.21 41.48 20.75 0.02

WCBF 30 30 30 30 30

TOTAL LIABILITIES 199.66 229.83 278.17 347.39 440.81

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 25/27

CONCLUSION DSCR FOR THE 5YEARS ARE:

YEAR NET DSCR

1 2.49

2 3.14

3 3.92

4 4.855 5.94

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 26/27

8/4/2019 Msme Ppt Final

http://slidepdf.com/reader/full/msme-ppt-final 27/27