Download - New Brunswick Transmission & Market Issues

New Brunswick Transmission & Market Issues

NPCC Annual MeetingHalifax - Sept 18, 2003

Bill MarshallDirector - Strategic PlanningNew Brunswick Power Corporation

Ø Market Implementation Update

Ø Resource Adequacy Concerns

Ø Maritime Market Issues

Ø International Power Line

Ø August 14 Operation

Presentation Summary

Ø NB Power restructuring legislationØ Separate corporations (Transco,Disco,Genco,Nucco)

Ø New ISO

Ø Wholesale & Large Industry Market opening

Ø Legislation passed but not proclaimed

Ø Original target April 1, 2003 but now set at ??????

Ø ProForma equivalent tariff Ø Sept 30, 2003

Market Implementation Update

Ø Maritime area will be deficient in capacity

Ø Projected by 2007

Ø Load growth continues Ø Natural gas penetration less than expected

Ø Actual growth masked by past years weather

Ø Reality was revealed last winter

Resource Adequacy Concerns

Winter Peak - 8:00 AM, Feb 17, 2003

Area Load 5365 MWExports 165 MWImports 30 MWNet load 5500 MWResources 6300 MW

3030

130

NM

NMNew

BrunswickPEI

NovaScotia

Maine

Québec

NewHampshire

165

45

10

Ø Coleson Cove and Pt Lepreau projectsØ Quality energy but no new capacity

Ø Natural gas outlook is poorØ Both availability and price

Ø Area needs new resources - From where?Ø Generation?Ø Imports?Ø Transmission?Ø Market interaction?

Resource Adequacy Concerns

Maritimes Market Issues

NM

NMNew

BrunswickPEI

NovaScotia

Maine

Québec

NewHampshire

Limited Transmission Access

No open access

LMP

PancakedMEPCO Tariff

Tariff Issues

No Spot Market

Ø Improved HQ tariffØ Detailed cost allocation study in Oct 2003Ø New application expected this year ???

Ø Improved ISO-NE tariffØ New application expected in Oct 2003Ø Improved scheduling ??Ø Remove pancaking of MEPCO & Phase II ??Ø Resolve marginal loss issue ??

External Regulatory Solutions

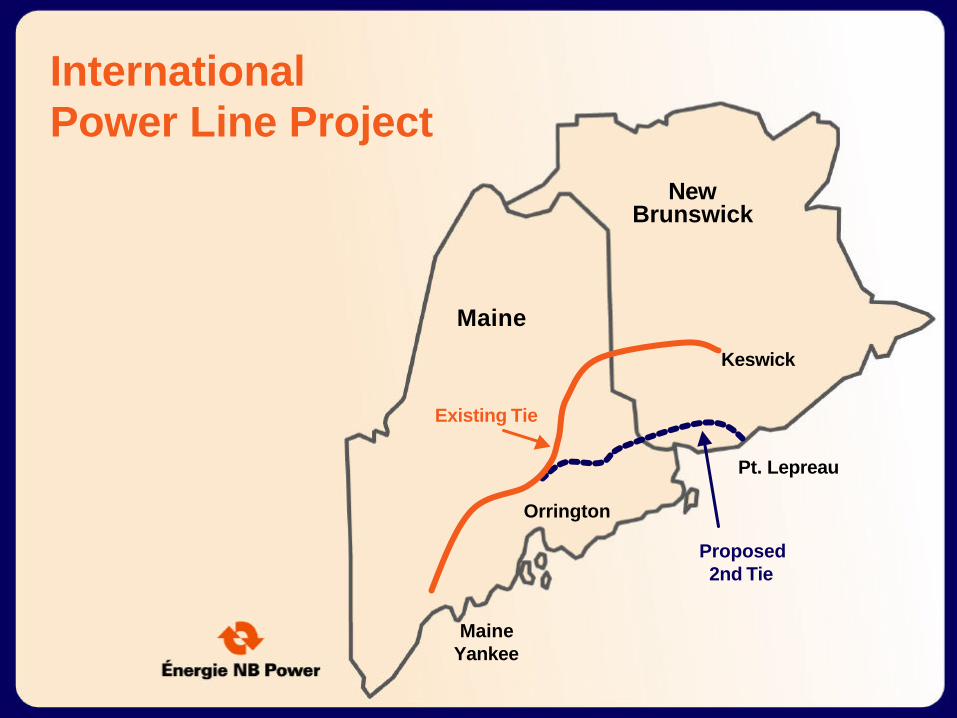

International Power Line Project

NewBrunswick

Maine

Keswick

Pt. Lepreau

Orrington

Existing Tie

Maine Yankee

Proposed 2nd Tie

Ø Improved market access to / from New EnglandØ 300MW export and 400MW import

Ø Improved reliability for Maritimes and MaineØ Parallel interconnectionØ Capacity benefits

Ø Increased efficiency in New Brunswick / MaineØ Loss savingsØ Improved LMP pricing

IPL Project Benefits

Ø NEB approval in CanadaØ Start construction by Dec 2006Ø Conditional on US project

Ø Continuing toward US approvals– Cooperation from Bangor Hydro (Emera)

Ø Finalizing the business case– Acceptable tariff required– Meetings with various stakeholders

IPL Project Status

Ø NE and Maritimes areas survived - How?Ø Good luck? Or Good management?

Ø Or Protection systems that worked

Ø Prior operation in MaritimesØ 3000 MW load (1600MW in NB)

Ø 500 MW export to NE

Ø 300MW export to Quebec

Aug 14, 2003 - Avoiding the Blackout

Ø The disturbanceØ 1500MW generation surge from NY to NE/Maritimes

– about 7-8% of total load

Ø Major frequency increase

Ø NE-NB tie reversed - 300MW import to Maritimes

– 800MW swing on 3000MW load - 25% of load

Ø NE/Maritimes separated from NY

Ø What happened in Maritimes?

Aug 14, 2003 - Avoiding the Blackout

Ø Maritime protection systems operated wellØ Automatic generation rejection - 400MW

Ø Increased HVDC export to Quebec - 100MW

Ø Governors responded - 200MW

– Pt Lepreau contributed 140MW

Ø Maritime Imbalance contribution Ø About 45% of the need (700 out of 1500MW)

Ø From 15% of the system (3000 out of 20,000MW)

Aug 14, 2003 - Avoiding the Blackout

Ø Maritime Area perspectiveØ Single 345kV line to Eastern Interconnection

Ø Experience “islanding” once every two years

Ø Maritime Area approach Ø Need protection systems in place and operational

ØRegular modeling and design preparation

ØRegular governor and relay systems testing

Aug 14, 2003 - Avoiding the Blackout

Questions?