Edition Forty Seven — February 2016

Prepare for $10-$15/bbl oil as Iran, US return to the market

UK government must save North Sea oil and gas sector

Why do oil prices keep going down?

OIL & GAS MANAGEMENT, LAW AND ACCOUNTING courses designed to take your career to the next level –

Full time, Part time and online.

Apply now for January and September 2016!

ABERDEEN BUSINESS SCHOOLwww.RGU.ac.uk/TOPDOG

#RGUTOPDOG

At blue asterisk, we specialise in providing on-demand cartography and graphic design services at highly competitive rates.

We work within your deadlines to provide accurate, high quality end products, from maps and montages to presentations and reports.

Find out how we can make your business stand out from the rest...

Cartographic Drafting & Design Services

We’ve got it covered…

blueasterisk.co.uk | [email protected] | +44 (0)1883 340341

Serving the E&P industry for over 25 years

Contact us for more detailsor visit our website

1 OilVoice Magazine – February 2016

The Biggest Conspiracy of the Century by Saudi Arabia and OPEC to Eliminate Its Competition

Written by Chris Vermeulen from The Gold and Oil Guy

Saudi Arabia and OPEC Manipulate Oil Prices

About eighteen months ago the international price of WTI Crude Oil, at the close of

June 2014, was $105.93 per barrel. Flash-forward to today; the price of WTI Crude

Oil was just holding above $38.00 per barrel, a drastic fall of more than 65% since

June 2014. I will point out several reasons behind this sharp, sudden, and what now

seems to be prolonged slump.

The Big Push

Despite a combination of factors triggering the fall in prices, the biggest push came

from the U.S. Shale producers. From 2010 to 2014, oil production in the U.S.

increased from 5,482,000 bpd to 8,663,000 (a 58% increase), making the U.S.

2 OilVoice Magazine – February 2016

the third largest oil-producing country in the world.

The next big push came from Iraq whose production increased from 2,358,000 bpd

in 2010 to 3,111,000 bpd in 2014 (a 32% increase), mostly resulting from the revival

of its post-war oil industry.

The country-wide financial crunch, and the need for the government to increasingly

export more to pay foreign companies for their production contracts and continue the

fight against militants in the country took production levels to the full of its current

capacity.

In addition; global demand remained flat, growing at just 1.1% and even declining for

some regions during 2014. Demand for oil in the U.S. grew just 0.6% against

production growth of 16% during 2014.

Europe registered extremely slow growth in demand, and Asia was plagued by a

slowdown in China which registered the lowest growth in its demand for oil in the last

five years. Consequently, a global surplus was created courtesy of excess supply

and lack of demand, with the U.S. and Iraq contributing to it the most.

The Response

In response to the falling prices, OPEC members met in the November of 2014, in

Vienna, to discuss the strategy forward. Advocated by Saudi Arabia, the most

influential member of the cartel, along with support from other GCC countries in the

OPEC, the cartel reluctantly agreed to maintain its current production levels.

This sent WTI Crude Oil and Brent Oil prices below $70, much to the annoyance of

Russia (non-OPEC), Nigeria and Venezuela, who desperately needed oil close

to $90 to meet their then economic goals.

For Saudi Arabia, the strategy was to leverage their low-cost of production

advantage in the market and send prices falling beyond such levels so that high-cost

competitors (U.S. Shale producers are the highest cost producers in the market) are

driven out and the market defines a higher equilibrium price from the resulting

correction. The GCC region, with a combined $2.5 trillion in exchange reserves,

braced itself for lower prices, even to the levels of $20 per barrel.

The Knockout Punch

By the end of September 2014, according to data from Baker Hughes, U.S. Shale

rigs registered their highest number in as many years at 1,931. However, they also

registered their very first decline to 1,917 at the end of November 2014, following

OPEC's first meeting after price falls and its decision to maintain production levels.

3 OilVoice Magazine – February 2016

By June 2015, in time for the next OPEC meeting, U.S. Shale rigs had already

declined to just 875 by the end of May; a 54% decline.

The Saudi Arabia strategy was spot on; a classic real-life example of predatory price

tactics being used by a market leader, showing its dominant power in the form of

deep foreign-exchange pockets and the low costs of production. Furthermore, on the

week ending on the date of the most recent OPEC meeting held on December 4th,

2015, the U.S. rig count was down even more to only 737; a 62% decline. Despite

increased pressure from the likes of Venezuela, the GCC lobby was able to ensure

that production levels were maintained for the foreseeable future.

Now What?

Moving forward; the U.S. production will decline by 600,000 bpd, according to a

forecast by the International Energy Agency. Furthermore, news from Iraq is that its

production will also decline in 2016 as the battle with militants gets more expensive

and foreign companies like British Petroleum have already cut operational budgets

for next year, hinting production slowdowns. A few companies in the Kurdish region

have even shut down all production, owing to outstanding dues on their contracts

with the government.

Hence, for the coming year, global oil supply is very much likely to be curtailed.

However, Iran's recent disclosure of ambitions to double its output once sanctions

are lifted next year, and call for $30 billion in investment in its oil and gas industry, is

very much likely to spoil any case for a significant price rebound.

4 OilVoice Magazine – February 2016

The same also led Saudi Arabia and its GCC partners to turn down any requests

from other less-economically strong members of OPEC to cut production, in their

December 2015, meeting. Under the current scenarios members like Venezuela,

Algeria and Nigeria, given their dependence on oil revenues to run their economies,

cannot afford to cut their own production but, as members of the cartel, can plea to

cut its production share to make room for price improvements, which they can

benefit from i.e. forego its market share.

It's Not Over Until I've Won?

With news coming from Iran, and the successful delivery of a knockout punch to a

six-year shale boom in the U.S., Saudi Arabia feared it would lose share to Iran if it

cut its own production. Oil prices will be influenced increasingly by the political

scuffles between Saudi Arabia and its allies and Iran. The deadlock and increased

uncertainty over Saudi Arabia and Iran's ties have sent prices plunging further. The

Global Hedge Fund industry is increasing its short position for the short-term, which

stood at 154 million barrels on November 17th, 2015, when prices hit $40 per barrel;

all of this indicating a prolonged bear market for oil.

One important factor that needs to be discussed is the $1+ trillions of junk bonds

holding up the shale and other marginal producers. As you know, that has been

teetering and looked like a crash not long ago. The pressure is still there. As the

shale becomes more impaired, the probability of a high-yield market crash looks very

high. If that market crashes, what happens to oil? Wouldn't there be feedback effects

between the oil and the crashing junk market, with a final sudden shutdown of

marginal production? Could this be the catalyst for a quick reversal of oil price?

The strategic interests, primarily of the U.S. and Saudi Arabia; the Saudis have

strategically decided to go all in to maintain their market share by maximizing oil

production, even though the effect on prices is to drive them down even further. In

the near term, they have substantial reserves to cover any budget shortfalls due to

low prices. More importantly, in the intermediate term, they want to force marginal

producers out of business and damage Iran's hopes of reaping a windfall due to the

lifting of sanctions. This is something they have in common with the strategic

interests of the U.S. which also include damaging the capabilities of Russia and ISIS.

It's certainly complicated sorting out the projected knock-on effects, but no doubt

they are there and very important.

I'll Show You How Great I Am

Moreover, despite a more than 50% decline in its oil revenues, the International

Monetary Fund has maintained Saudi Arabia's economy to grow at 3.5% for 2015,

buoyed by increasing government spending and oil production. According to data by

Deutsche Bank and IMF; in order to balance its fiscal books, Saudi Arabia needs an

5 OilVoice Magazine – February 2016

oil price of $105. But the petroleum sector only accounts for 45% of its GDP, and as

of June 2015, according to the Saudi Arabian Monetary Agency, the country had

combined foreign reserves of $650 billion. The only challenge for Saudi Arabia is to

introduce slight taxes to balance its fiscal books. As for the balance of payments

deficit; the country has asserted its will to depend on its reserves for the foreseeable

future.

Conclusion

The above are some of the advantages which only Saudi Arabia and a couple of

other GCC members in the OPEC enjoy, which will help them sustain their strategy

even beyond 2016 if required. But I believe it won't take that long. International

pressure from other OPEC members, and even the global oil corporations' lobby will

push leaders on both sides to negotiate a deal to streamline prices.

With the U.S. players more or less out by the end of 2016, the OPEC will be in more

control of price fluctuations and, therefore, in light of any deal between Iran and

Saudi Arabia (both OPEC members) and even Russia (non-OPEC), will alter global

supply for prices to rebound, thus controlling prices again.

What we see now in oil price manipulation is just the mid-way point. Lots of

opportunity in oil and oil related companies will slowly start to present themselves

over the next year which I will share my trades and long term investment pays with

subscribers of my newsletter at TheGoldAndOilGuy.com

View more quality content from

The Gold and Oil Guy

PICK A WINNERFOR THESE CHALLENGINGTIMES

Stay ahead of the game, and don’t wait for partners to show you the value in your assets! Find out more at

ikonscience.com/jifi

With the industry’s current focus on cost control, it is remarkable that more and more forward-thinking oil & gas companies are stepping up to invest in Ikon Science’s revolutionary RokDoc Ji-Fi®, a new tool to build reliable seismically-driven geological models. Ji-Fi breaks the mold of traditional workflows and opens up a whole new realm of possibilities. The cost/benefit of Ji-Fi is so compelling it redefines how customers leverage data and knowledge to drive success in their exploration, development and production activities.

The Present And Future Of GeoPrediction

ikonscience.com

C

M

Y

CM

MY

CY

CMY

K

Ji-Fi A4.pdf 1 20/05/2015 08:05:25

6 OilVoice Magazine – February 2016

Why oil under $30 per barrel is a major problem

Written by Gail Tverberg from Our Finite World

A person often reads that low oil prices-for example, $30 per barrel oil prices-will

stimulate the economy, and the economy will soon bounce back. What is wrong with

this story? A lot of things, as I see it:

1. Oil producers can't really produce oil for $30 per barrel

A few countries can get oil out of the ground for $30 per barrel. Figure 1 gives an

approximation to technical extraction costs for various countries. Even on this basis,

there aren't many countries extracting oil for under $30 per barrel-only Saudi Arabia,

Iran, and Iraq. We wouldn't have much crude oil if only these countries produced oil.

Figure 1. Global breakeven prices (considering only technical extraction costs) versus production.

Source: Alliance Bernstein, October 2014

2. Oil producers really need prices that are higher than the technical extraction

costs shown in Figure 1, making the situation even worse.

Oil can only be extracted within a broader system. Companies need to pay taxes.

These can be very high. Including these costs has historically brought total costs for

many OPEC countries to over $100 per barrel.

Independent oil companies in non-OPEC countries also have costs other than

7 OilVoice Magazine – February 2016

technical extraction costs, including taxes and dividends to stockholders. Also, if

companies are to avoid borrowing a huge amount of money, they need to have

higher prices than simply the technical extraction costs. If they need to borrow,

interest costs need to be considered as well.

3. When oil prices drop very low, producers generally don't stop producing.

There are built-in delays in the oil production system. It takes several years to put a

new oil extraction project in place. If companies have been working on a project, they

generally won't stop just because prices happen to be low. One reason for continuing

on a project is the existence of debt that must be repaid with interest, whether or not

the project continues.

Also, once an oil well is drilled, it can continue to produce for several years. Ongoing

costs after the initial drilling are generally very low. These previously drilled wells will

generally be kept operating, regardless of the current selling price for oil. In theory,

these wells can be stopped and restarted, but the costs involved tend to deter this

action.

Oil exporters will continue to drill new wells because their governments badly need

tax revenue from oil sales to fund government programs. These countries tend to

have low extraction costs; nearly the entire difference between the market price of oil

and the price required to operate the oil company ends up being paid in taxes. Thus,

there is an incentive to raise production to help generate additional tax revenue, if

prices drop. This is the issue for Saudi Arabia and many other OPEC nations.

Very often, oil companies will purchase derivative contracts that protect themselves

from the impact of a drop in market prices for a specified time period (typically a year

or two). These companies will tend to ignore price drops for as long as these

contracts are in place.

There is also the issue of employee retention. In a sense, a company's greatest

assets are its employees. Once these employees are lost, it will be hard to hire and

retrain new employees. So employees are kept on as long as possible.

The US keeps raising its biofuel mandate, regardless of the price of oil. No one stops

to realize that in the current over-supplied situation, the mandate adds to low price

pressures.

One brake on the system should be the financial pain induced by low oil prices, but

this braking effect doesn't necessarily happen quickly. Oil exporters often

have sovereign wealth funds that they can tap to offset low tax revenue. Because of

the availability of these funds, some exporters can continue to finance governmental

services for two or more years, even with very low oil prices.

8 OilVoice Magazine – February 2016

Defaults on loans to oil companies should also act as a brake on the system. We

know that during the Great Recession, regulators allowed commercial real estate

loans to be extended, even when property valuations fell, thus keeping the problem

hidden. There is a temptation for regulators to allow similar leniency regarding oil

company loans. If this happens, the 'braking effect' on the system is reduced,

allowing the default problem to grow until it becomes very large and can no longer be

hidden.

4. Oil demand doesn't increase very rapidly after prices drop from a high level.

People often think that going from a low price to a high price is the opposite of going

from a high price to a low price, in terms of the effect on the economy. This is not

really the case.

4a. When oil prices rise from a low price to a high price, this generally means

that production has been inadequate with only the production that could be obtained

at the prior lower price. The price must rise to a higher level in order to encourage

additional production.

The reason that the cost of oil production tends to rise is because the cheapest-to-

extract oil is removed first. Oil producers must thus keep adding production that is

ever-more expensive for one reason or another: harder to reach location, more

advanced technology, or needing additional steps that require additional human

labor and more physical resources. Growing efficiencies can somewhat offset this

trend, but the overall trend in the cost of oil production has been sharply

upward since about 1999.

The rising price of oil has an adverse impact on affordability. The usual pattern is

that after a rise in the price of oil, economies of oil importing nations go into

recession. This happens because workers' wages do not rise at the same time as oil

prices. As a result, workers find that they cannot buy as many discretionary items

and must cut back. These cutbacks in purchases create problems for businesses,

because businesses generally have high fixed costs including mortgages and other

debt payments. If these businesses are to continue to operate, they are forced to cut

costs in one way or another. Cost reduction occurs in many ways, including reducing

wages for workers, layoffs, automation, and outsourcing of manufacturing to cheaper

locations.

For both employers and employees, the impact of these rapid changes often feels

like a rug has been pulled out from under foot. It is very unpleasant and

disconcerting.

4b. When prices fall, the situation that occurs is not the opposite of 4a. Employers

9 OilVoice Magazine – February 2016

find that thanks to lower oil prices, their costs are a little lower. Very often, they will

try to keep some of these savings as higher profits. Governments may choose to

raise tax rates on oil products when oil prices fall, because consumers will be less

sensitive to such a change than otherwise would be the case. Businesses have no

motivation to give up cost-saving techniques they have adopted, such as automation

or outsourcing to a cheaper location.

Few businesses will construct new factories with the expectation that low oil prices

will be available for a long time, because they realize that low prices are only

temporary. They know that if oil prices don't go back up in a fairly short period of time

(months or a few years), the quantity oil available is likely to drop precipitously. If

sufficient oil is to be available in the future, oil prices will need to be high enough to

cover the true cost of production. Thus, current low prices are at most a temporary

benefit-something like the eye of a hurricane.

Since the impact of low prices is only temporary, businesses will want to adopt only

changes that can take place quickly and can be easily reversed. A restaurant or bar

might add more waiters and waitresses. A car sales business might add a few more

salesmen because car sales might be better. A factory making cars might schedule

more shifts of workers, so as to keep the number of cars produced very high. Airlines

might add more flights, if they can do so without purchasing additional planes.

Because of these issues, the jobs that are added to the economy are likely to be

mostly in the service sector. The shift toward outsourcing to lower-cost countries and

automation can be expected to continue. Citizens will get some benefit from the

lower oil prices, but not as much as if governments and businesses weren't first in

line to get their share of the savings. The benefit to citizens will be much less than if

all of the people who were laid off in the last recession got their jobs back.

5. The sharp drop in oil prices in the last 18 months has little to do with the

cost of production.

Instead, recent oil prices represent an attempt by the market to find a balance

between supply and demand. Since supply doesn't come down quickly in response

to lower prices, and demand doesn't rise quickly in response to lower prices, prices

can drop very low-far below the cost of production.

As noted in Section 4, high oil prices tend to be recessionary. The primary way of

offsetting recessionary forces is by directly or indirectly adding debt at low interest

rates. With this increased debt, more homes and factories can be built, and more

cars can be purchased. The economy can be forced to act in a more 'normal'

manner because the low interest rates and the additional debt in some sense

counteract the adverse impact of high oil prices.

10 OilVoice Magazine – February 2016

Figure 2. World oil supply and prices based on EIA data.

Oil prices dropped very low in 2008, as a result of the recessionary influences that

take place when oil prices are high. It was only with the benefit of considerable debt-

based stimulation that oil prices were gradually pumped back up to the $100+ per

barrel level. This stimulation included US deficit spending, Quantitative Easing (QE)

starting in December 2008, and a considerable increase in debt by the Chinese.

Commodity prices tend to be very volatile because we use such large quantities of

them and because storage is quite limited. Supply and demand have to balance

almost exactly, or prices spike higher or lower. We are now back to an 'out of

balance' situation, similar to where we were in late 2008. Our options for fixing the

situation are more limited this time. Interest rates are already very low, and

governments generally feel that they have as much debt as they can safely handle.

6. One contributing factor to today's low oil prices is a drop-off in the stimulus

efforts of 2008.

As noted in Section 4, high oil prices tend to be recessionary. As noted in Section 5,

this recessionary impact can, at least to some extent, be offset stimulus in the form

of increased debt and lower interest rates. Unfortunately, this stimulus has tended to

have adverse consequences. It encouraged overbuilding of both homes and

factories in China. It encouraged a speculative rise in asset prices. It encouraged

11 OilVoice Magazine – February 2016

investments in enterprises of questionable profitability, including many investments

in oil from US shale formations.

In response to these problems, the amount of stimulus is being reduced. The US

discontinued its QE program and cut back its deficit spending. It even began raising

interest rates in December 2015. China is also cutting back on the quantity of new

debt it is adding.

Unfortunately, without the high level of past stimulus, it is difficult for the world

economy to grow rapidly enough to keep the prices of all commodities, including oil,

high. This is a major contributing factor to current low prices.

7. The danger with very low oil prices is that we will lose the energy products

upon which our economy depends.

There are a number of different ways that oil production can be lost if low oil prices

continue for an extended period.

In oil exporting countries, there can be revolutions and political unrest leading to a

loss of oil production.

In almost any country, there can be a sharp reduction in production because oil

companies cannot obtain debt financing to pay for more services. In some cases,

companies may go bankrupt, and the new owners may choose not to extract oil at

low prices.

There can also be systemwide financial problems that indirectly lead to much lower

oil production. For example, if banks cannot be depended upon for payroll services,

or to guarantee payment for international shipments, such problems would affect all

oil companies, not just ones in financial difficulty.

Oil is not unique in its problems. Coal and natural gas are also experiencing low

prices. They could experience disruptions indirectly because of continued low prices.

8. The economy cannot get along without an adequate supply of oil and other

fossil fuel products.

We often read articles in the press that seem to suggest that the economy could get

along without fossil fuels. For example, the impression is given that renewables are

'just around the corner,' and their existence will eliminate the need for fossil fuels.

Unfortunately, at this point in time, we are nowhere being able to get along without

fossil fuels.

Food is grown and transported using oil products. Roads are made and maintained

using oil and other energy products. Oil is our single largest energy product.

12 OilVoice Magazine – February 2016

Experience over a very long period shows a close tie between energy use and GDP

growth (Figure 3). Nearly all technology is made using fossil fuel products, so even

energy growth ascribed to technology improvements could be considered to be

available to a significant extent because of fossil fuels.

Figure 3. World GDP growth compared to world energy consumption growth for selected time periods since

1820. World real GDP trends from 1975 to present are based on USDA real GDP data in 2010$ for 1975 and

subsequent. (Estimated by the author for 2015.) GDP estimates for prior to 1975 are based on Maddison project

updates as of 2013. Growth in the use of energy products is based on a combination of data from Appendix A

data from Vaclav Smil's Energy Transitions: History, Requirements and Prospects together with BP Statistical

Review of World Energy 2015 for 1965 and subsequent.

While renewables are being added, they still represent only a tiny share of the

world's energy consumption.

13 OilVoice Magazine – February 2016

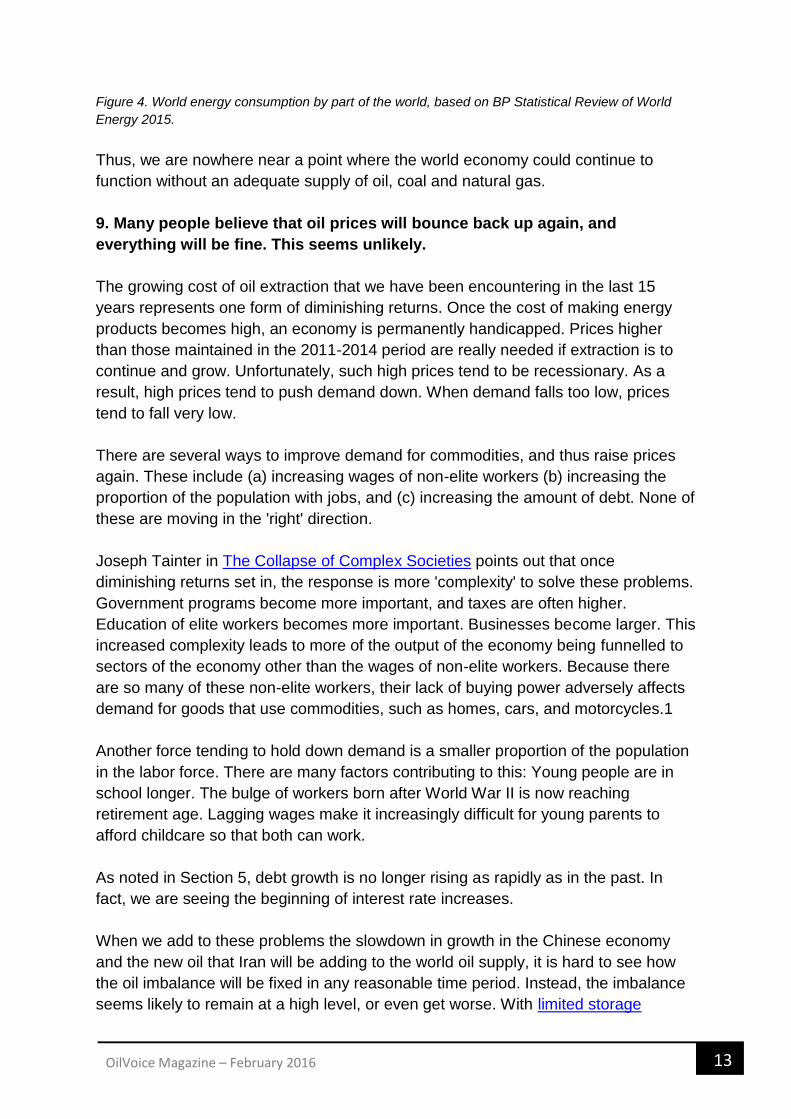

Figure 4. World energy consumption by part of the world, based on BP Statistical Review of World

Energy 2015.

Thus, we are nowhere near a point where the world economy could continue to

function without an adequate supply of oil, coal and natural gas.

9. Many people believe that oil prices will bounce back up again, and

everything will be fine. This seems unlikely.

The growing cost of oil extraction that we have been encountering in the last 15

years represents one form of diminishing returns. Once the cost of making energy

products becomes high, an economy is permanently handicapped. Prices higher

than those maintained in the 2011-2014 period are really needed if extraction is to

continue and grow. Unfortunately, such high prices tend to be recessionary. As a

result, high prices tend to push demand down. When demand falls too low, prices

tend to fall very low.

There are several ways to improve demand for commodities, and thus raise prices

again. These include (a) increasing wages of non-elite workers (b) increasing the

proportion of the population with jobs, and (c) increasing the amount of debt. None of

these are moving in the 'right' direction.

Joseph Tainter in The Collapse of Complex Societies points out that once

diminishing returns set in, the response is more 'complexity' to solve these problems.

Government programs become more important, and taxes are often higher.

Education of elite workers becomes more important. Businesses become larger. This

increased complexity leads to more of the output of the economy being funnelled to

sectors of the economy other than the wages of non-elite workers. Because there

are so many of these non-elite workers, their lack of buying power adversely affects

demand for goods that use commodities, such as homes, cars, and motorcycles.1

Another force tending to hold down demand is a smaller proportion of the population

in the labor force. There are many factors contributing to this: Young people are in

school longer. The bulge of workers born after World War II is now reaching

retirement age. Lagging wages make it increasingly difficult for young parents to

afford childcare so that both can work.

As noted in Section 5, debt growth is no longer rising as rapidly as in the past. In

fact, we are seeing the beginning of interest rate increases.

When we add to these problems the slowdown in growth in the Chinese economy

and the new oil that Iran will be adding to the world oil supply, it is hard to see how

the oil imbalance will be fixed in any reasonable time period. Instead, the imbalance

seems likely to remain at a high level, or even get worse. With limited storage

14 OilVoice Magazine – February 2016

available, prices will tend to continue to fall.

10. The rapid run up in US oil production after 2008 has been a significant

contributor to the mismatch between oil supply and demand that has taken

place since mid-2014.

Without US production, world oil production (broadly defined, including biofuels and

natural gas liquids) is close to flat.

Figure 5. Total liquids oil production for the world as a whole and for the world excluding the US,

based on EIA International Petroleum Monthly data.

Viewed separately, US oil production has risen very rapidly. Total production rose by

about six million barrels per day between 2008 and 2015.

15 OilVoice Magazine – February 2016

Figure 6. US Liquids production, based on EIA data (International Petroleum Monthly, through June

2015; supplemented by December Monthly Energy Review for most recent data).

US oil supply was able to rise very rapidly partly because QE led to the availability of

debt at very low interest rates. In addition, investors found yields on debt so low that

they purchased almost any equity investment that appeared to have a chance of

long-term value. The combination of these factors, plus the belief that oil prices

would always increase because extraction costs tend to rise over time, funneled

large amounts of investment funds into the liquid fuels sector.

As a result, US oil production (broadly defined), increased rapidly, increasing nearly

1.0 million barrels per day in 2012, 1.2 million barrels per day in 2013, 1.7 million

barrels per day in 2014. The final numbers are not in, but it looks like US oil

production will still increase by another 700,000 barrels a day in 2015. The 700,000

extra barrels of oil added by the US in 2015 is likely greater than the amount added

by either Saudi Arabia or Iraq.

World oil consumption does not increase rapidly when oil prices are high. World oil

consumption increased by 871,000 barrels a day in 2012, 1,397,000 barrels a day in

2013, and 843,000 barrels a day in 2014, according to BP. Thus, in 2014, the US by

itself added approximately twice as much oil production as the increase in world oil

demand. This mismatch likely contributed to collapsing oil prices in 2014.

Given the apparent role of the US in creating the mismatch between oil supply and

demand, it shouldn't be too surprising that Saudi Arabia is unwilling to try to fix the

problem.

Conclusion

Things aren't working out the way we had hoped. We can't seem to get oil supply

and demand in balance. If prices are high, oil companies can extract a lot of oil, but

consumers can't afford the products that use it, such as homes and cars; if oil prices

are low, oil companies try to continue to extract oil, but soon develop financial

problems.

Complicating the problem is the economy's continued need for stimulus in order to

keep the prices of oil and other commodities high enough to encourage production.

Stimulus seems to takes the form of ever-rising debt at ever-lower interest rates.

Such a program isn't sustainable, partly because it leads to mal-investment and

partly because it leads to a debt bubble that is subject to collapse.

Stimulus seems to be needed because of today's high extraction cost for oil. If the

cost of extraction were still very low, this stimulus wouldn't be needed because

products made using oil would be more affordable.

16 OilVoice Magazine – February 2016

Decision makers thought that peak oil could be fixed simply by producing more oil

and more oil substitutes. It is becoming increasingly clear that the problem is more

complicated than this. We need to find a way to make the whole system operate

correctly. We need to produce exactly the correct amount of oil that buyers can

afford. Prices need to be high enough for oil producers, but not too high for

purchasers of goods using oil. The amount of debt should not spiral out of control.

There doesn't seem to be a way to produce the desired outcome, now that oil

extraction costs are high.

Rigidities built into the oil price-supply system (as described in Sections 3 and 4)

tend to hide problems, letting them grow bigger and bigger. This is why we could

suddenly find ourselves with a major financial problem that few have anticipated.

Unfortunately, what we are facing now is a predicament, rather than a problem.

There is quite likely no good solution. This is a worry.

Note:

[1] For example, more dividend and interest payments are paid, tending to benefit

the financial industry and the elite classes. More of the output of the economy goes

to workers in supervisory positions or having advanced education. Other workers-

those with more 'ordinary' responsibilities-find their wages falling behind the general

rise in the cost of living. As a result, they find it increasingly difficult to buy cars,

homes, motorcycles, and other goods that use commodities.

View more quality content from

Our Finite World

A PERFECT FIT

neosgeo.com

Seismic + Non-Seismic

NEOS Adds Seismic Imaging to Its Multi-Physics Toolkit

Following our recent acquisition, some of the best and brightest minds in seismic imaging have joined the NEOS

team. Continuing to do what they do best, the NEOS Seismic Imaging Group will deliver stand-alone processing

and imaging services, including advanced onshore depth imaging in some of the most challenging regions in the

world. But it doesn’t stop there. Our strengths in multi-physics imaging align perfectly and we will be teaming up

to change the way the industry explores. Incorporating seismic attributes into our proprietary predictive analytics

methods and undertaking multi-physics inversions is just the beginning. Together we offer a truly complete

portfolio of subsurface imaging solutions to our clients.

Seismic + Non-Seismic. A powerful combination.

17 OilVoice Magazine – February 2016

Prepare for $10-$15/bbl oil as Iran, US return to the market

Written by Paul Hodges from ICIS

Oil markets finally entered their 'give-up phase' last week. Amazingly, it is now nearly

18 months since the start of the Great Unwinding of policymaker stimulus in August

2014, when Brent was still $105/bbl. On Friday night, Brent closed at $29/bbl. As

ICIS Chemical Business (ICB) notes in its latest editorial:

'International eChem's Paul Hodges has been predicting $20-30/ bbl since August

2014 and he has now been joined by the likes of Goldman Sachs and Morgan

Stanley in expecting the rout to continue and low prices to persist for years'.

Until last week, virtually all the analysts were still insisting that oil prices would return

to at least $50/bbl, or even $100/bbl. In their view, it was just a matter of 'when', not

'if'. But now, they finally begin to face reality, as I discussed with ICB:

'It's a market share game, as the Saudis realised when they gave up trying to hold

the price 18 months ago. You either sell today, or risk ending up leaving the oil in the

ground.'

The chart of the Great Unwinding above shows how far we have travelled before this

simple truth was finally recognised:

Brent oil prices are now down 71%, and fell 13% last week

18 OilVoice Magazine – February 2016

The US$ is up 21%, having broken out of its 30-year downtrend

And more recently, of course, the other elements of the Great Unwinding have

begun to impact - European and Japanese equity markets are down 10% since the

start of the year, and US markets are down 9%. As US financial magazine

Barron's notes:

'The juice that the Federal Reserve had provided is being withdrawn, and the

symptoms of going off the stuff are becoming apparent. The U.S. stock market is off

to its worst start of any year on record.'

OIL MARKETS ARE NOW IN THE GIVE-UP PHASE

What happens next is obviously the key question. I have never known a major price

movement, of the kind we've seen with oil over the past 18 months, end without an

overshoot. It therefore seems very unlikely that it could suddenly stabilise at $25/bbl,

although I do expect this to return to being the long-term level

Supply/demand factors suggest there is still a major imbalance in the market

o The IEA says there are a record 3bn barrels of storage

o The US has record storage, and European storage is virtually full

o China has become a net exporter of oil products as its economy slows

o The mild Western winter has reduced demand for heating purposes

2 major exporters are now re-joining the market:

o Iran is expected to add up to 500kb/d in January now nuclear

sanctions have ended, and has said its production costs are $1.70/bbl.

It wants to regain lost market share as quickly as possible

o The US has just begun shipments. Given its high storage levels, it

would make sense to monetise these quickly via sales, especially as

they are costing money to store

The short-term outlook is weak, given that Chinese/Asian demand is now

slowing ahead of Lunar New Year on February 8, and March will see the

traditional maintenance season for Western refineries after the winter

US production costs are falling fast, with Daniel Yergin suggesting that a

dollar spent in December was '65% more efficient that a dollar spent in 2014'

The outbreak of tension between Saudi Arabia and Iran makes it most unlikely

that OPEC could agree to any major cuts in production, even if Saudi wanted

to change course

Companies and investors therefore need to prepare for further chaos ahead. I fear

that oil producers and oil consumers will now start to go bankrupt - producers

because they cannot pay their interest bills, and consumers because they have high

and expensive stock levels. Many consumers put their trust in the so-called 'experts',

and rushed to fill tanks and warehouses in November/December, assuming that

19 OilVoice Magazine – February 2016

prices would rise in January. Today, however, buyers all down the chain are in a

state of simple panic, and worry that making any purchase is like trying to 'catch a

falling knife'.

As I have long feared, we face a very difficult 2016.

WEEKLY MARKET ROUND-UP

My weekly round-up of Benchmark prices since the Great Unwinding began is below,

with ICIS pricing comments:

Brent crude oil, down 71%

Naphtha Europe, down 66%. 'Fundamentals weaken on US gasoline build'

Benzene Europe, down 59%. 'Tumbling crude oil and benzene numbers are

weighing down on the European styrene spot market this week, with talk of

strong derivative demand doing little to stem the downward movement.'

PTA China, down 46%. 'Downstream polyester producers have confirmed

turnaround plans and adjusted contractual volumes for the Lunar New Year

holidays, sources in the country said. They also have sufficient inventories to

last them until after the long holiday'

HDPE US export, down 41%. 'Prices have to come down because there is too

much North American supply already and more capacity coming on line

throughout 2016'

¥:$, down 15%

S&P 500 stock market index, down 4%

Paul Hodges is Chairman of International eChem, trusted commercial advisers to the

global chemical industry.

View more quality content from

ICIS

20 OilVoice Magazine – February 2016

The great condensate con: Is the oil glut just about oil?

Written by Kurt Cobb from Resource Insights

My favorite Texas oilman Jeffrey Brown is at it again. In a recent email he's pointing

out to everyone who will listen that the supposed oversupply of crude oil isn't quite

what it seems. Yes, there is a large overhang of excess oil in the market. But how

much of that oversupply is honest-to-god oil and how much is so-called lease

condensate which gets carelessly lumped in with crude oil? And, why is this

important to understanding the true state of world oil supplies?

In order to answer these questions we need to get some preliminaries out of the

way.

Lease condensate consists of very light hydrocarbons which condense from gaseous

into liquid form when they leave the high pressure of oil reservoirs and exit through

the top of an oil well. This condensate is less dense than oil and can interfere with

optimal refining if too much is mixed with actual crude oil. The oil industry's own

engineers classify oil as hydrocarbons having an API gravity of less than 45--the

higher the number, the lower the density and the 'lighter' the substance. Lease

condensate is defined as hydrocarbons having an API gravity between 45 and

70. (For a good discussion about condensates and their place in the marketplace,

read 'Neither Fish nor Fowl - Condensates Muscle in on NGL and Crude Markets.')

Refiners are already complaining that so-called 'blended crudes' contain too much

lease condensate, and they are seeking out better crudes straight from the

wellhead. Brown has dubbed all of this the great condensate con.

Brown points out that U.S. net crude oil imports for December 2015 grew from the

previous December, according to the U.S. Energy Information Administration (EIA),

the statistical arm of the U.S. Department of Energy. U.S. statistics for crude oil

imports include condensate, but don't break out condensate separately. Brown

believes that with America already awash in condensate, almost all of those imports

must have been crude oil proper.

Brown asks, 'Why would refiners continue to import large--and increasing--volumes

of actual crude oil, if they didn't have to--even as we saw a huge build in [U.S.] C+C

[crude oil plus condensate] inventories?'

21 OilVoice Magazine – February 2016

Part of the answer is that U.S. production of crude oil has been declining since mid-

2015. But another part of the answer is that what the EIA calls crude oil is actually

crude plus lease condensate. With huge new amounts of lease condensate coming

from America's condensate-rich tight oil fields--the ones tapped by hydraulic

fracturing or fracking--the United States isn't producing quite as much actual crude

oil as the raw numbers would lead us to believe. This EIA chart breaking down the

API gravity of U.S. crude production supports this view.

Exactly how much of America's and the world's presumed crude oil production is

actually condensate remains a mystery. The data just aren't sufficient to separate

condensate production from crude oil in most instances.

Brown explains: 'My premise is that U.S. (and probably global) refiners hit in late

2014 the upper limit of the volume of condensate that they could process' and still

maintain the product mix they want to produce. That would imply that condensate

inventories have been building faster than crude inventories and that the condensate

is looking for an outlet.

That outlet has been in blended crudes, that is heavier crude oil that is blended with

condensates to make it lighter and therefore something that fits the definition of light

crude. Light crude is generally easier to refine and thus more valuable.

Trouble is, the blends lack the characteristics of nonblended crudes of comparable

density (that is, the same API gravity), and refiners are discovering to their chagrin

that the mix of products they can get out of blended crudes isn't what they expect.

So, now we can try to answer our questions. Brown believes that worldwide

production of condensate 'accounts for virtually all of the post-2005 increase in C+C

[crude plus condensate] production.' What this implies is that almost all of the 4

million-barrel-per-day increase in world 'oil' production from 2005 through 2014 may

actually be lease condensate. And that would mean crude oil production proper has

been nearly flat during this period--a conjecture supported by record and near record

average daily prices for crude oil from 2011 through 2014. Only when demand

softened in late 2014 did prices begin to drop.

Here it is worth mentioning that when oil companies talk about the price of oil, they

are referring to the price quoted on popular futures exchanges--prices which reflect

only the price of crude oil itself. The exchanges do not allow other products such as

condensates to be mixed with the oil that is delivered to holders of exchange

contracts. But when oil companies (and governments) talk about oil supply, they

include all sorts of things that cannot be sold as oil on the world market including

biofuels, refinery gains and natural gas plant liquids as well as lease

condensate. Which leads to a simple rule coined by Brown: If what you're selling

cannot be sold on the world market as crude oil, then it's not crude oil.

22 OilVoice Magazine – February 2016

The glut that developed in 2015 may ultimately be tied to some increases in actual,

honest-to-god crude oil production. The accepted story from 2005 through 2014 has

been that crude oil production has been growing, albeit at a significantly slower rate

than the previous nine-year period--15.7 percent from 1996 through 2005 versus 5.4

percent from 2005 through 2014 according to the EIA. If Brown is right, we have all

been victims of the great condensate con which has lulled the world into a sense of

complacency with regard to actual oil supplies--supplies he believes have been

barely growing or stagnant since 2005.

'Oil traders are acting on fundamentally flawed data,' Brown told me by phone. Often

a contrarian, Brown added: 'The time to invest is when there's blood in the streets.

And, there's blood in the streets.'

He explained: 'Who of us in January of 2014 believed that prices would be below $30

in January of 2016? If the conventional wisdom was wrong in 2014, maybe it's

similarly wrong in 2016' that prices will remain low for a long time.

Brown points out that it took trillions of dollars of investment from 2005 through today

just to maintain what he believes is almost flat production in oil. With oil companies

slashing exploration budgets in the face of low oil prices and production declining at

an estimated 4.5 and 6.7 percent per year for existing wells worldwide, a recovery in

oil demand might push oil prices much higher very quickly.

That possibility is being obscured by the supposed rise in crude oil production in

recent years that may just turn out to be an artifact of the great condensate con.

View more quality content from

Resource Insights

Early bird deadline extended! View full event details and register now for optimal savings at barcelona2016.iceevent.org.

• Technical Program featuring 300 oral and poster presentation sessions addressing the theme “Collaboration in a Changing World”

• State-of-the-art Exhibition displaying the latest in products, technologies, and services

• Student and Young Professional special events

• Short courses including:

• Carbonate Essentials: Pores to Prospect, presented by Christopher Liner

• Marine Broadband Technologies: Theory and Practice, presented by David H. Carlson

• Advanced Sequence Stratigraphic Applications for Exploration (SEPM course), presented by Vitor Abreu

• Field Trips including: • Fractured carbonate reservoirs outcrops: observing faults, fractures, and karsts permeability networks in different carbonate depositional settings

• Carbonate reservoir analogues: play concepts and controls on porosity

• Reservoir analogues from modern and ancient turbidite systems – Tabernas Basin, Spain

• Thrust belt structure and foreland basin evolution in the southern Pyrenees – Aragon, Spain

• Face-to-face networking opportunities designed to build connections, drive new business, and enhance career opportunities

• Women in Geosciences Forum

• Access to leaders on the forefront of advancing the geosciences industry

Register now for ICE Barcelona, Europe’s premier geosciences event!Benefit from:

IC E Barcelona

Centre de Convencions Internacional de Barcelona

3-6 April • Barcelona, Spainbarcelona2016.iceevent.org

®

MEDIA PARTNERS:

GOLD SPONSOR: SILVER SPONSOR:

22 OilVoice Magazine – February 2016

The glut that developed in 2015 may ultimately be tied to some increases in actual,

honest-to-god crude oil production. The accepted story from 2005 through 2014 has

been that crude oil production has been growing, albeit at a significantly slower rate

than the previous nine-year period--15.7 percent from 1996 through 2005 versus 5.4

percent from 2005 through 2014 according to the EIA. If Brown is right, we have all

been victims of the great condensate con which has lulled the world into a sense of

complacency with regard to actual oil supplies--supplies he believes have been

barely growing or stagnant since 2005.

'Oil traders are acting on fundamentally flawed data,' Brown told me by phone. Often

a contrarian, Brown added: 'The time to invest is when there's blood in the streets.

And, there's blood in the streets.'

He explained: 'Who of us in January of 2014 believed that prices would be below $30

in January of 2016? If the conventional wisdom was wrong in 2014, maybe it's

similarly wrong in 2016' that prices will remain low for a long time.

Brown points out that it took trillions of dollars of investment from 2005 through today

just to maintain what he believes is almost flat production in oil. With oil companies

slashing exploration budgets in the face of low oil prices and production declining at

an estimated 4.5 and 6.7 percent per year for existing wells worldwide, a recovery in

oil demand might push oil prices much higher very quickly.

That possibility is being obscured by the supposed rise in crude oil production in

recent years that may just turn out to be an artifact of the great condensate con.

View more quality content from

Resource Insights

23 OilVoice Magazine – February 2016

Oil Price Crash: How low will the oil price go?

Written by Euan Mearns from Energy Matters

I have been following the oil price crash since it began in late 2014, providing annual

forecast scenarios and monthly vital statistics updates. There has recently been an

acceleration in activity and news, and as the oil price has continued its fall to below

$30, investors and speculators wrestle with the main question: 'how low will the oil

price go?'

In August 2015 I gave a crude answer to that question based on history in a post

called The Oil Price: how low is low? where I observed:

To get straight to the point. Brent will need to fall below $30 to match the lows seen

in 1986 and to below $20 to match the lows seen in 1998.

This observation was based on deflated annual average price from BP ($2014). The

notion of $20 oil has since caught on and some commentators are now speculating

that $10 is possible. It is time to have a closer look at what history tells us.

This article was originally published on the Energy Matters blog.

First a look at recent oil price action.

24 OilVoice Magazine – February 2016

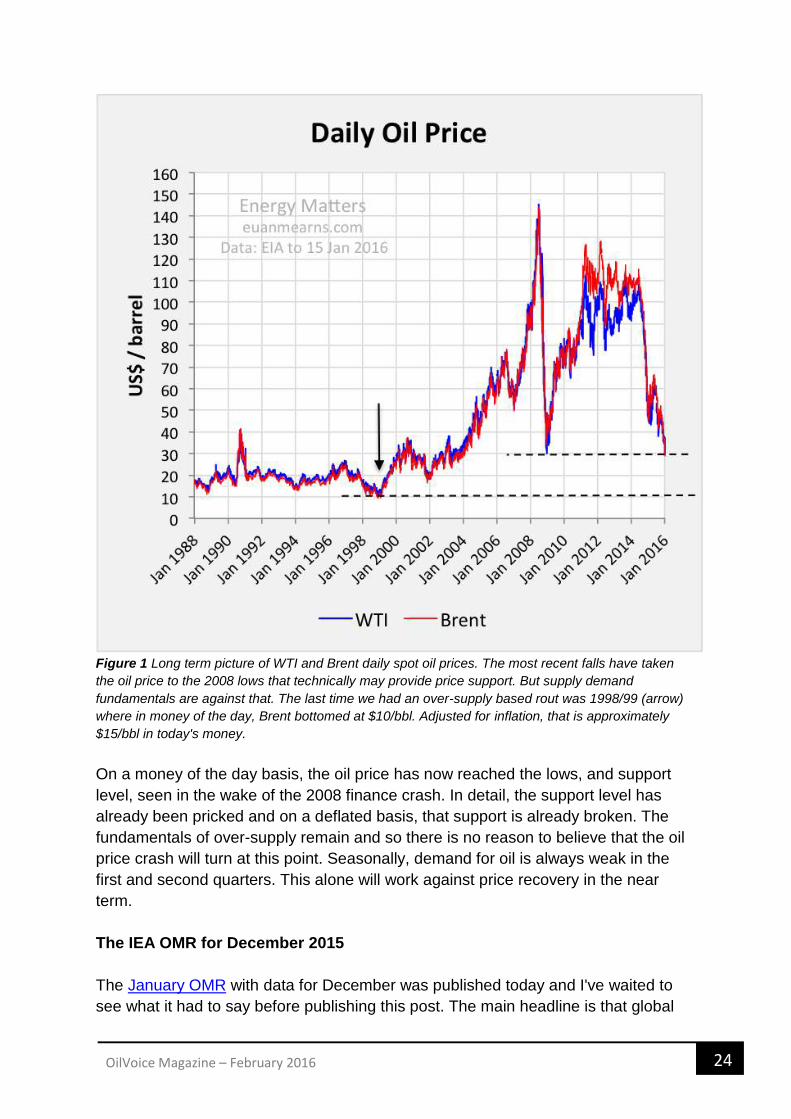

Figure 1 Long term picture of WTI and Brent daily spot oil prices. The most recent falls have taken

the oil price to the 2008 lows that technically may provide price support. But supply demand

fundamentals are against that. The last time we had an over-supply based rout was 1998/99 (arrow)

where in money of the day, Brent bottomed at $10/bbl. Adjusted for inflation, that is approximately

$15/bbl in today's money.

On a money of the day basis, the oil price has now reached the lows, and support

level, seen in the wake of the 2008 finance crash. In detail, the support level has

already been pricked and on a deflated basis, that support is already broken. The

fundamentals of over-supply remain and so there is no reason to believe that the oil

price crash will turn at this point. Seasonally, demand for oil is always weak in the

first and second quarters. This alone will work against price recovery in the near

term.

The IEA OMR for December 2015

The January OMR with data for December was published today and I've waited to

see what it had to say before publishing this post. The main headline is that global

25 OilVoice Magazine – February 2016

total liquids supply was 96.88 Mbpd in December, down 90,000 bpd on November.

This is effectively unchanged. The IEA observes:

a procession of investment banks has warned that oil prices 'could' fall to $25/bbl,

$20/bbl or, in one case, $10/bbl.

and asks the question

Can It Go Any Lower?

and concludes

So the answer to our question is an emphatic yes. It could go lower.

Recent News

Sanctions against Iran, as expected by all, have been lifted clearing the decks

for full oil exports to resume. Recent estimates suggest an additional 500,000

bpd exports. In my Oil Price Scenarios for 2016 post I assumed 800,000 bpd

additional oil from Iran. Regardless of whichever comes to pass, Iran returning

to full exports makes the over-supply situation worse.

Saudi Arabia has floated the idea of selling a 10% stake in Aramco, the Saudi

State oil company. This confirms the precarious state of Saudi finances but

also Saudi commitment to staying the strategic course. They would rather sell

the family silver than back down from their course towards national ruin.

Personally I don't believe this transaction will ever take place since investors

will be buying into production and not reserves, in a Nation that lies at the

centre of turmoil in the Middle East.

The Chinese stock market has crashed again and looks like it could now head

much lower leaving major questions about the general state of the Chinese

economy. The engine behind the commodities super cycle looks like it may

take some time out for repairs.

BHP Billiton, with Australian roots, listed in London but with global operations

is one of the World's largest diversified energy companies with stakes in oil &

gas, coal and uranium mining. They just announced a $7 billion write down on

their US shale assets. With a market capitalisation of £36 billion, BHP can

withstand balance sheet losses such as this more easily than the smaller

shale players.

UK North Sea oil production is rising for the first time since 1999.

US oil and gas drilling rig count continues to fall steadily but not so steeply as

during the early stage of the oil price crash. Below I take a closer look at the

oil price crash of 1998 / 99. The chart shows that back then US operational

rigs fell from 1000 to 500 before making a sharp recovery. Today, the oil+gas

rig count stands at 650, not yet so low as 1998/99 but proportionally much

26 OilVoice Magazine – February 2016

lower since the drilling fleet size is now 2000. At least it was 2000 leading into

the crash.

Figure 2 Stacked chart of US oil and gas directed drilling. The total rig count stood at 650 on 15

January, 515 oil and 135 gas. The combined rig count is still falling steeply and this must inevitably

bring about more significant declines in US oil and gas production at some future date once the

backlog of drilled but uncompleted wells works through the system.

The oil price crash of 1998/99

The oil price is already in irrational over-sold territory where virtually all producers

are making substantial losses, be they fiscal losses in OPEC countries or economic

losses in the market economies of the OECD. Longer term, the oil price must rise

above the level where everyone makes money, but short term, economics is not

helpful in trying to constrain where the market bottom might be. In the absence of

any rational economic pointers, all one can fall back upon is what happened before

27 OilVoice Magazine – February 2016

during similar circumstances. The oil price crash of 2008 is not a good analogy,

driven by financial crisis, that crash was ended with OPEC reining in production by 5

Mbpd. We have to go back to 1998 / 99 to see what happened during an oil market

driven price crash.

In money of the day, Brent fell below $10 / bbl for brief spells during December 1998

and February 1999. Back then, WTI traded at a premium to Brent of roughly $1.50 /

bbl. Today the WTI-Brent spread is effectively zero. Adjusting price for inflation using

the BP deflator points to price lows of about $14 for Brent in 2014 dollars.

Figure 3 WTI and Brent daily spot prices as reported by the EIA in money of the day (MOTD).

28 OilVoice Magazine – February 2016

Figure 4 Same as Figure 3 with prices adjusted for inflation using the BP deflator where $2014 =

$1998*1.45. Note that the price defines a distinct double bottom.

It is important to note that the nature of the 1998/99 price crash was different to

today's since this marked the culmination of an oil bear market that began in 1981.

Today's crash is caused by an inelastic market constrained by production volume

where relative swings in supply and demand of ±2 Mbpd is causing price swings of

±$40 per barrel. The market is currently caught in the over-supply + weak demand

vortex.

Once in a decade buying opportunity?

It is important at this stage to note that I am not a qualified investment advisor. All I

am doing here is laying out a framework of data and information to help others reach

their own decisions.

29 OilVoice Magazine – February 2016

There is no near-term bullish news for oil in the 'Recent News' I recount above. With

over-supply remaining, I therefore expect price to carry on down during the first two

quarters. It is worth noting that $20 is still 33% below $30 - that is a long way down!

But in the interim, distressed investors may be forced to sell on margin calls which

provides fuel to the downward spiral.

My central scenario for Brent in December 2016 was $37. Other commentators see

the price higher than that by year end. Should Brent go sub-$20 by mid-year this

would clearly present a good investment opportunity if prices do indeed rise

thereafter as expected. Of course, if one waits for sub-$20 and the price never gets

there, that would result in an opportunity lost.

My gut feel is that market bottom will be in the vicinity of $15. There are two reasons

for saying this. The first is that professional investment houses will to large extent be

looking at the same data I am and if they reach the same conclusions, they will

define the behaviour of the herd. The second is that current price trajectory heads

towards $15 by the end of the second quarter. Beyond that, supply and demand

should converge towards balance, heralding recovery.

In my 2016 scenarios, one scenario was called 'Event' and the probability of an

Event taking place, like disruptive terrorist attacks in Saudi Arabia, will increase as

the price falls. For example, Saudi ability to pay for state security is impaired while

the levels of social unrest linked to mounting poverty rises. If there is an Event that

sends the oil price sky high then lucky investors will be those who got on board

beforehand.

View more quality content from

Energy Matters

30 OilVoice Magazine – February 2016

The Trends That Will Be Driving the Oil Price in 2016 (and Beyond…)

Written by Andreas de Vries from Andreas de Vries

The past 18 months have been especially tough for those in the business of

forecasting the crude oil price.

At the end 2013, when Brent closed at $112 per barrel and WTI at $100, the

investment banks expected crude to continue to price around $100 per barrel during

2014. In actuality, of course, the price dropped to below $60 per barrel that year, as

the market became oversupplied and OPEC refused to cut its production to

rebalance supply and demand.

For 2015 essentially everyone got it wrong again. At the start of that year the general

expectation was that at around $60 per barrel, the price was (close to) bottoming out,

since a substantial amount of the North-America unconventional production (US

shale and Canadian tarsands) had become uneconomical and would thus be

removed from the market shortly. But, as US shale production did not go down

nearly as much as expected, the price decline that started in 2014 did not bottom out

but kept on going. During December 2015 Brent eventually reached an 11-year low

of $34 per barrel.

How could the forecasts have gotten it so wrong?

A major factor was the human tendency to assume that the trends we presently

experience, the trends that drive our world today, will continue into the future. In

other words, that fundamentally everything will stay the same.

For example the 2015 crude oil price forecast foresaw a reduction in US shale

production because it assumed these barrels would continue to cost between $70

and $90 to produce, as they did when OPEC's 'War on Shale' began in 2014. What

really happened, however, was that the shale producers aggressively drove

improvements and efficiencies in all elements of their value chain. New reservoir

analysis techniques and well completion improvements have enabled the producers

to increase average initial production of newly drilled wells (as compared to wells

drilled earlier in the Shale Revolution), while refracking has proven to be a (partial)

solution for the shale wells' notorious decline rate. Furthermore, the introduction

31 OilVoice Magazine – February 2016

of pad drilling has reduced the overall time needed for drilling while extending the

reach of horizontal wells, thus lowering development costs. This has enabled the US

shale industry to drastically lower production costs by as much as 65% according to

some estimates, maintain 2014 production levels throughout most of 2015, and even

prepare for a possible future uptick in prices through maintaining DUCs (drilled but

uncompleted wells) capable of adding some 500.000 barrels per day to production.

This lesson in this little bit of recent crude oil price forecasting history is that

forecasting requires more than extrapolation of the current trends in the industry

today. It requires identification of coming trends that will drive the industry tomorrow.

In this regard, crude oil price forecasters should take note of the research done

by Ray Kurzweil into the nature of technological innovation. Kurzweil is one of

America's leading inventors and futurists and currently Google's Director for

Engineering. For his book 'Singularity is Near' he researched different sciences and

technologies - computers, memory, DNA sequencing, communication, internet - to

find that innovation does not proceed in a constant manner. Rather, it tends

to accelerate. The more we learn, the easier it becomes to learn even more, and the

faster we will learn even more.

If Kurzweil's Law of accelerating innovation were to hold in the oil & gas industry as

well, what new trends would this lead to in the future?

Firstly, it would mean that shale technology goes global, substantially increasing

both shale production and proved (technologically and economically recoverable)

reserves. Continued innovation in shale technology will namely address the key pain

points of shale oil and gas production, i.e. its cost and environmental impact,

opening the way for development of the contingent resources located in places such

as China, Russia, Argentina, Europe and the United Arab Emirates. A lot of these

improvements are already underway, in fact. For example, centralized rather than

well-by-well wastewater management is being studied to lower shale's operational

costs and environmental footprint and waterless fracking is being researched to

eliminate the issue completely.

Secondly, it would mean shale technology becomes a quaternary recovery

technique, increasing crude oil production and expected ultimate recovery rates for

mature oilfields around the world. Tests on a number of mature oilfields in North

America have already shown that the techniques behind shale, horizontal drilling and

hydraulic fracturing, can indeed achieve this, not only through developing tight zones

in these fields that were left behind during original development, but also through re-

stimulation. The cutting edge of these technologies is currently being tested on the

giant mature conventional oilfields of the Middle East.

These two new trends will, in turn, lead in a third new trend: decoupling of the crude

32 OilVoice Magazine – February 2016

oil price from political events. If, namely, shale technology goes global and becomes

a quaternary recovery technique for mature conventional fields, global crude oil

production capacity will not only be increased but also diversified, reducing the

influence of individual countries over production and transportation. The current

global crude oil market is characterized by concentrated production with just 10

countries being responsible for two thirds of global crude oil production, five of whom

are located in the greater Middle East. At the same time the top 10 consumers of

crude oil also make up close to 60% of global consumption. This leads

to transportation chokepoints and a relatively small number of countries having

substantial leverage over the global crude oil supply and demand balance.

Diversification of production will reduce the importance of these countries for the

global crude oil supply and demand balance, thus making the crude oil price less

susceptible to political events in these countries. This trend can be witnessed

already as well, for example in the relatively muted response of the crude oil price to

events such as the Syrian Revolution, the rise of ISIL in Iraq, and most recently the

tensions between Saudi-Arabia and Iran.

Andreas de Vries works as a Strategy Consultant in the Oil & Gas industry, helping

companies to not only develop strategies but also execute them.

View more quality content from

Andreas de Vries

33 OilVoice Magazine – February 2016

What is the long run average oil price?

Written by Steve Brown from The Steam Oil Production Company Ltd

I read lots of commentary claiming that only now (when Brent is less than $35/bbl)

are we getting back to the long run average oil price, which of course is where some

economists think it should be. Of course nothing has changed since 1861 so the

price back then is just as relevant as last year's price... or perhaps the geology has

got a little tougher, and safety standards improved a tad. But the kind of economists

who believe in long run average prices probably also believe that technology is

making things in the oil patch cheaper and cheaper.

They couldn't be more wrong - electronic and computer technology is an aberration,

Moore's Law just doesn't apply much outside that domain. Indeed in some sectors

like medical the costs spiral upwards as technology advances.

Of course we can now do things with seismic technology and horizontal wells that we

couldn't in the past, but in reality we use the technology to access more elusive

reserves and stringent safety and environmental standards have layered cost on the

industry.

That rant is all to justify an assertion that in calculating the average oil price in the

past we need to take account of how recent the oil prices we are averaging are. It is

patent nonsense to average oil prices from 1861 to 2015 and say that $34.11 is the

average oil price and therefore today's oil price is somehow the 'right' price.

So I've come up with a methodology and done a calculation or too. I weighted last

year's price at 100% and knocked off 5% per annum all the way back to 1861. That

means the price in 2001 is half as relevant as last year's price, that 1987 matters a

quarter as much, 1968 a tenth as much and 1861 hardly at all. On that basis the

average oil price is $58.23, so if we are reverting to a mean, I think the mean we are

reverting to is closer to $60/bbl than $34/bbl.

34 OilVoice Magazine – February 2016

Data from 1861-2015 BP statistical review of world energy, 2015 EIA

Of course we might not be reverting to a mean... we might actually be working our

way through all the cheap and easy to develop reserves, we might be adding costs

by adhering to higher and better safety and environmental standards and we might

be on a pathway to a long run average price of about $80/bbl, but if I say that no-one

will believe me.

View more quality content from

The Steam Oil Production Company Ltd

35 OilVoice Magazine – February 2016

UK government must save North Sea oil and gas sector

Written by Alex Russel and Peter Strachan from Robert Gordon

University

The UK government is abandoning the North Sea oil and gas sector to its fate,

despite the fact that there is still enough oil and gas in place in the region to generate

the same amount of revenue that has been reaped up to now, argue Alex Russell

and Peter Strachan of Robert Gordon University. They advocate that full control of

energy and oil within the Scottish section should go to the Scottish government, so

that at least this part can be saved.

The (oil) well-funded Oil and Gas Authority (OGA) was established on 1 April 2015

as a consequence of the publication on 24 February 2014 of Sir Ian Wood's Review

on maximising economic recovery from the remnants of the UK's North Sea oil fields.

The OGA is an executive agency of the Department of Energy and Climate Change

(DECC) and states on its website that 'we work with government and industry to

make sure that the UK gets the maximum economic benefit from its oil and gas

reserves'.

With respect to offshore oil production the OGA can point to an unexpected increase

over the past year in barrels of oil equivalent output. Alas, at the same time there has

been around as many as 80,000 North Sea oil-related job losses over the past 15

months. From a UK perspective does this outcome represent a maximisation of

economic benefit? It may be akin to maximisation of production but in economic

terms it resembles a car crash.

Strange bedfellows

Those oil companies which have slashed their workforce and increased production

will indeed be getting some return on their huge recent past investments. However, it

appears that due to the low oil price accounting losses are being incurred and rather

than contributing cash to the UK Exchequer oil companies are having past tax

payments repaid to them by Chancellor George Osborne.

The reason for this situation is that US-inspired political machinations involving Saudi

Arabia have driven down the price of a barrel of Brent crude to a mere $30 and have

brought the UK oil sector to the brink of oblivion. OPEC, the cartel of oil producers

36 OilVoice Magazine – February 2016

led by the oil rich Kingdom of Saudi Arabia has been labelled the villain of the piece

for its failure to increase oil prices by reducing oil output in the face of a global glut of

oil stocks.

Well, there may be a smidgeon of truth in these claims, but over most of the past

forty-five years OPEC has been pilloried by the West for taking actions that

increased oil prices. They really can't win. And in any event it is all a red herring. If

there is a genuine cartel that can control the price of oil it consists not of OPEC but

of the US and Saudi Arabia alliance. US production and stockpiling of oil has never

been higher. By all accounts Saudi Arabia is on the point of selling shares in its

national oil company Saudi Aramco and that can only be to strengthen even further

its political and economic ties with the US.

Has world history seen stranger bedfellows? Would the US have any interest in

having a relationship with the Saudis if that Kingdom had no oil? No answers

required please, as this really is the world's dumbest rhetorical question. Self-interest

is at the heart of the relationship and when a definitive history of the fallout from it is

written it will not be on the list of Barack Obama's favourite bedtime reads.

Strident demands

Arguably, the US/Saudi Arabia cartel has forced down the oil price to put economic

pressure on their common adversary Russia. Clearly there are other external factors

that have impacted on oil price such as the downturn in the economies of China and

Europe but primarily US and Saudi over-production relative to demand is the root

cause of the oil crisis.

It is perhaps an example of economic and political genius on the part of the US.

When oil prices were high they milked rewards from their fast depleting fracking

plays and now that oil is scraping the bottom of the price barrel they have persuaded

other countries to sell their oil at give-away prices. The US economy is booming as a

consequence.

Unfortunately the high cost North Sea oil industry has been a casualty of this

situation. The OGA's strident demands for North Sea Operators to be more efficient

in their operations and to share what in the past would be commercially sensitive

information with them, has resulted in a cataclysmic loss of possibly 80,000 North

Sea-related jobs.

It is hard to believe that substantial real efficiencies have been brought about by

forcing oil companies to share information and resources as claimed by the OGA.

The reality is that rates of pay for contractors have been slashed and investment in

exploring for new reserves has stopped. The resultant job losses are a disaster

especially for the North East of Scotland and for the future of the industry.

37 OilVoice Magazine – February 2016

Huge profits

A way should be found to persuade oil companies to focus on finding new reserves

of oil and gas that can be exploited when oil prices rise rather than to produce oil

currently at a loss. The UK government and the oil companies need to invest in the

future and repay back the huge profits they have taken out of the North Sea. It is

good news if real efficiencies have and can continue to be made across the industry

and everyone would support the OGA in their efforts to achieve this outcome. But

even then there would need to be questions asked why over the past forty years

these inefficiencies were tolerated. Exactly how much revenue to the UK has been

lost through the prevalence of inefficient operational practices by oil companies? Will

anyone be held accountable?

The UK Government led by Chancellor George Osborne has shown all the sparkling