© 2013 Iron Mountain Incorporated. All rights reserved. Iron Mountain and the design of the mountain are registered trademarks of Iron Mountain Incorporated.

All other trademarks and registered trademarks are the property of their respective owners.

March 2015

Durable Fundamentals and Differentiated Business Model Deliver Enhanced Returns

2

Safe Harbor Language

Safe Harbor Statement Under the Private Securities Litigation Reform Act of 1995: This presentation contains certain forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 and other securities laws and is subject to the safe-harbor created by such Act. Forward-looking statements include our financial performance outlook and statements regarding our operations, economic performance, financial condition, goals, beliefs, future growth strategies, investment objectives, plans and current expectations, and the anticipated benefits of our conversion to a real estate investment trust for federal income tax purposes, including the opportunity to create value by acquiring leased space, our potential for a broadened investor base and enhanced valuations and the estimated range of our remaining special distribution and our ordinary dividends. These forward-looking statements are subject to various known and unknown risks, uncertainties and other factors. When we use words such as "believes," "expects," "anticipates," "estimates" or similar expressions, we are making forward-looking statements. You should not rely upon forward-looking statements except as statements of our present intentions and of our present expectations, which may or may not occur. Although we believe that our forward-looking statements are based on reasonable assumptions, our expected results may not be achieved, and actual results may differ materially from our expectations. Important factors that could cause actual results to differ from our other expectations include, among others: (i) our expected ordinary dividends may be materially different from our estimates; (ii) the cost to comply with current and future laws, regulations and customer demands relating to privacy issues; (iii) the impact of litigation or disputes that may arise in connection with incidents in which we fail to protect our customers' information; (iv) changes in the price for our storage and information management services relative to the cost of providing such storage and information management services; (v) changes in customer preferences and demand for our storage and information management services; (vi) the adoption of alternative technologies and shifts by our customers to storage of data through non-paper based technologies; (vii) the cost or potential liabilities associated with real estate necessary for our business; (viii) the performance of business partners upon whom we depend for technical assistance or management expertise outside the U.S.; (ix) changes in the political and economic environments in the countries in which our international subsidiaries operate; (x) claims that our technology violates the intellectual property rights of a third party; (xi) changes in the cost of our debt; (xii) the impact of alternative, more attractive investments on dividends; (xiii) our ability to qualify or remain qualified for taxation as a real estate investment trust (“REIT”); (xiv) our ability or inability to complete acquisitions on satisfactory terms and to integrate acquired companies efficiently; (xv) other trends in competitive or economic conditions affecting our financial condition or results of operations not presently contemplated; and (xvi) other risks described more fully in our filings with the Securities and Exchange Commission, including under the caption “Risk Factors” in our periodic reports, or incorporated therein. Except as required by law, we undertake no obligation to release publicly the result of any revision to these forward-looking statements that may be made to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

3

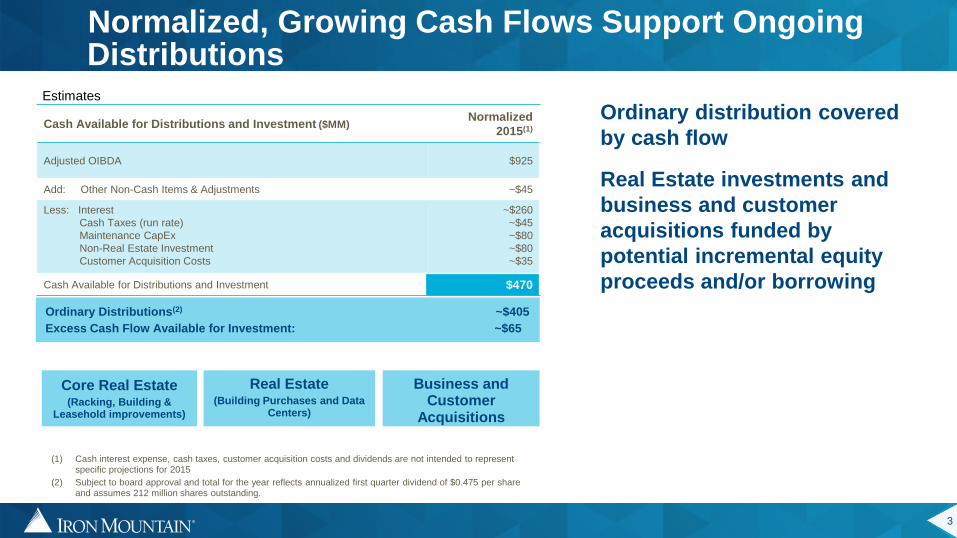

Ordinary distribution covered

by cash flow

Real Estate investments and

business and customer

acquisitions funded by

potential incremental equity

proceeds and/or borrowing

Cash Available for Distributions and Investment ($MM) Normalized

2015(1)

Adjusted OIBDA $925

Add: Other Non-Cash Items & Adjustments ~$45

Less: Interest

Cash Taxes (run rate)

Maintenance CapEx

Non-Real Estate Investment

Customer Acquisition Costs

~$260

~$45

~$80

~$80

~$35

Cash Available for Distributions and Investment $470

Normalized, Growing Cash Flows Support Ongoing Distributions

Ordinary Distributions(2) ~$405

Excess Cash Flow Available for Investment: ~$65

(1) Cash interest expense, cash taxes, customer acquisition costs and dividends are not intended to represent specific projections for 2015

(2) Subject to board approval and total for the year reflects annualized first quarter dividend of $0.475 per share and assumes 212 million shares outstanding.

Real Estate (Building Purchases and Data

Centers)

Business and Customer

Acquisitions

Core Real Estate (Racking, Building &

Leasehold improvements)

Estimates

4

We Store & Manage Information Assets

75% 17% 8%

Records Management Data Management Shredding

Based on FY2014 results

5

Diversified Global Business

$3B annual revenues

>155,000 customers

Serving 92% of Fortune 1000

68MM SF of real estate in ~1,100 facilities

Compelling Customer Value Proposition

Reduce costs and risks of storing and protecting information assets

Broadest range of footprint and services

Most trusted brand

Leading Global Presence

36 Countries

5 Continents

6

What You Will Hear Today

We are uniquely positioned to create value through our operating model and real estate strategy

Our market leadership position supports long-term value

Fundamentals support stable growth in storage rental

Leading storage rental-driven business, supported by market leadership and stable fundamentals, drives attractive shareholder returns

Attractive business characteristics underscore value creation

7

Global Real Estate Portfolio of More than 1,000 Facilities

68 million total square footage

Owned: 24 million sq. ft.

Leased: 44 million sq. ft.

Buyout option: ~3.5 million sq. ft.

Owned/Controlled: 40% of real estate by sq. ft.

Average size: 62k sq. ft.

Leased facilities

Weighted avg. remaining lease obligation: 5.6 yrs.

Weighted avg. remaining lease obligation with

exercise of all extension options: 12.4 yrs.

Records Management Utilization rates Building: 83%

Racking: 91%

Data Protection Utilization Rates

Building: 68%

Racking: 81%

8

Illustrative North America RM Storage

Annual Economics(1) (per square foot, except for ROIC)

Investment

Customer acquisition $ 42

Building and outfitting 54

Racking structures 54

Total investment $ 150

Storage Rental Income

Storage rental revenue $ 27

Direct operating costs (3)

Allocated field overhead (3)

Storage rental income $ 21

Pre-Tax Storage Rental ROIC(2) ~14%

Attractive, High-Return Storage Rental Businesses

(1) Reflects average portfolio pricing and assumes an owned facility (2) Includes maintenance CapEx, assumed at 2% of revenue

High storage rental revenue /SF

Occupancy costs incurred by the SF; revenue earned by the cubic foot

Storage rental value creation drivers

Racking investment supports ability to drive higher NOI

Low maintenance capex requirements

Network utilization

Portfolio management of multiple tenants

Related services

9

NA Leased (47%) Owned (36%) INTL Leased (17%)

Significant global real estate footprint – approximately 1,100 facilities in 68MM SF

Acquisition opportunity of $700MM to $1B over 10-year timeframe

Expanded real estate purchase program

Expected IRR of 9 – 12%

Supports REIT Asset Test

Enhances real estate residual value

Real Estate Acquisitions to Enhance Returns

Potential $2.5B - $3.0B Purchase Universe

10

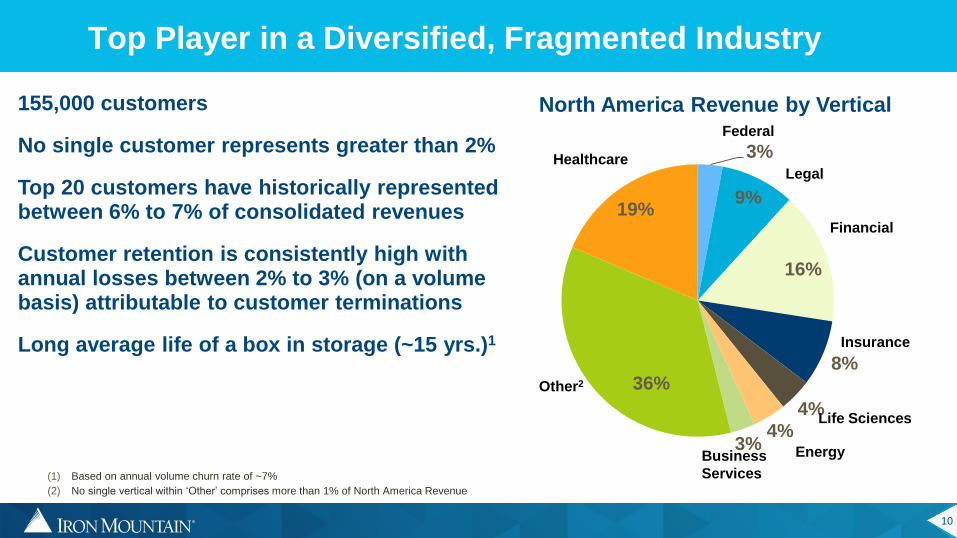

3%

9%

16%

8%

4%

4% 3%

36%

19%

North America Revenue by Vertical

Other2

Insurance

Financial

Healthcare

Federal

Legal

Energy Business

Services

Life Sciences

Top Player in a Diversified, Fragmented Industry

(1) Based on annual volume churn rate of ~7%

(2) No single vertical within ‘Other’ comprises more than 1% of North America Revenue

155,000 customers

No single customer represents greater than 2%

Top 20 customers have historically represented between 6% to 7% of consolidated revenues

Customer retention is consistently high with annual losses between 2% to 3% (on a volume basis) attributable to customer terminations

Long average life of a box in storage (~15 yrs.)1

11

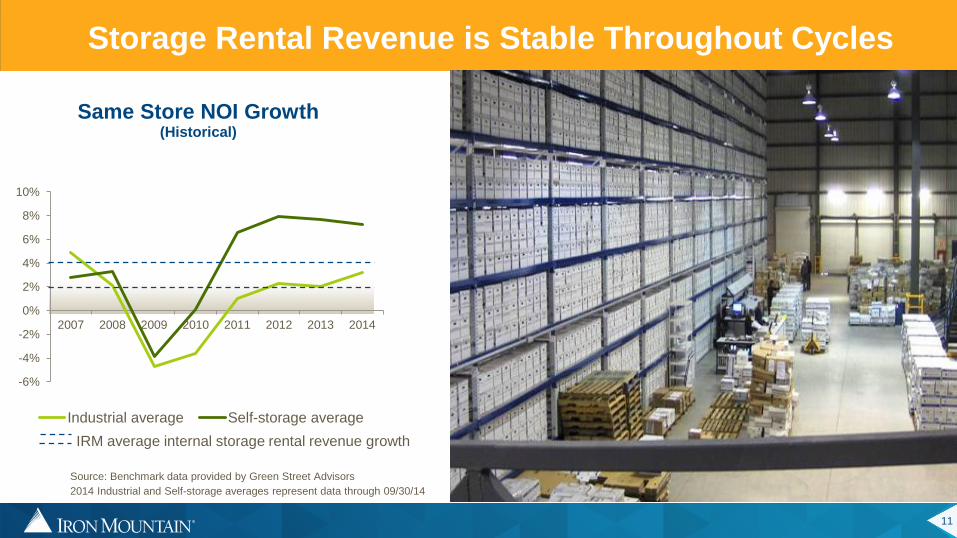

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

2007 2008 2009 2010 2011 2012 2013 2014

Same Store NOI Growth (Historical)

Industrial average Self-storage average

Storage Rental Revenue is Stable Throughout Cycles

Source: Benchmark data provided by Green Street Advisors

2014 Industrial and Self-storage averages represent data through 09/30/14

IRM average internal storage rental revenue growth

12

Large & growing

60% of revenues ($1.9B)

4% - 5% constant dollar growth

GDP correlated & inflation hedged

26 Consecutive Years of Storage Rental Growth

2014

$1,860

Storage Rental ($MM)

13

Consistent Incoming Storage Volume

6-7% new volume from existing customers globally

Cut sheet paper demand growth flat, but documents still being produced and stored

Records becoming more archival in nature

-4% -2% -3%

-6%

-3%

0%

3%

6%Q4-12 Q1-13 Q2-13 Q3-13 Q4-13 Q1-14 Q2-14 Q3-14 Q4-14

New Volume From Existing CustomersNA and WE Paper Demand

2% 1% 2%

-6%-3%0%3%6%9%

12%15%

Q4-12 Q1-13 Q2-13 Q3-13 Q4-13 Q1-14 Q2-14 Q3-14 Q4-14

New Volume From Existing Customers

Emerging Markets Paper Demand

Developed Markets Emerging Markets

Source for paper trends data: Resource Information Systems Inc. (RISI). 2014 demand figures are estimates

14

Strategy to Extend Durability of Business

Speed and Agility Simplification, Process Automation and Efficiency

Developed

Markets Drive Profitable Revenue

Growth; Grow Tape and

Cube Volume

Strategic Plan

Emerging Markets Expand and Leverage

Emerging

Businesses Identify, Incubate,

Scale or Scrap

(Data Center)

Organization and Culture Organizational Capabilities, Talent and Processes

CO

RE

PIL

LA

RS

E

NA

BL

ER

S

15

$2,694

$2,810-$2,870

$1,047 $1,100- $1,150

2013 Actual 2016 Targets

Revenue Adjusted OIBDA

Developed Market Targets ($MM)

Driving profitable growth

Enhanced cube volume growth

Sales force excellence

Acquisitions

Speed & Agility drives profitability

Getting More out of Global Developed Markets

Stable Base Supports Moderate Growth with Low Risk

(1) 2013 Adj. OIBDA excludes restructuring charges

(2) 2016 target excludes foreign exchange impact and is based on 2014 C$ budget rate

(1) (2)

16

Improved Retention and Acquisition Drive Net Volume Growth

6.6% 6.3% 6.3% 6.3% 6.2% 6.1% 6.1% 5.9%

1.9% 1.9% 2.0% 2.1% 2.1% 2.2% 2.1% 2.2%

1.5% 0.3%

2.1% 4.5% 5.2% 5.9%

3.7% 1.7%

-4.7% -4.6% -4.6% -4.6% -4.5% -4.7% -4.5% -4.4%

-2.7% -2.6% -2.6% -2.5% -2.3% -2.0% -1.9% -1.9%

2.6% 1.4% 3.2% 5.8% 6.7% 7.6% 5.5% 3.6%

Q1-13 Q2-13 Q3-13 Q4-13 Q1-14 Q2-14 Q3-14 Q4-14

New Volume from Existing Customers New Sales Acquisitions Destructions Outperm/Terms

Year-over-Year Global Net Volume Growth Rates (Records Management Only)

Net Volume Growth Rate

Represents year-over-year change in volume as of the end of each period presented. The quarterly percentages are calculated by dividing the trailing four quarters’ total activity by the ending balance of the same prior year period. Includes acquisitions of customers and businesses

17

Capturing Opportunity in Emerging Markets

Investing to drive leadership

Currently 13.9% of total revenue(3)

Goal: increase percentage of total revenue to 16%

~50% of emerging market growth driven by acquisitions

First wave of outsourcing

M&A Key Driver of Emerging Market Strategy

Emerging Market Targets

($MM)

100-120

Base

90-110

Acquisitions

(1) 2013 Adjusted OIBDA excludes restructuring charges

(2) 2016 target excludes foreign exchange impact and is based on 2014 C$ budget rate

(3) On a constant dollar basis

(1) (2)

$319

$510-$550

$65

$100- $150

2013 Actual 2016 Targets

Revenue Adjusted OIBDA

18

$160

$50

$145

$55

$85

$30

IMLA EMEA Asia

New Territories Current Territories

Acquisition opportunities in both emerging and developed markets

Developed markets – strategy to enhance storage growth while maintaining attractive returns 2014 Acquisitions of $64 MM

Emerging markets – investing to build strong leadership positions

Diversified portfolio of targets

Streamlined acquisition process

2014 Acquisitions of $125 MM

M&A Pipeline is Strong and Execution Well Underway

Revenue Pipeline Greater than 4x

Target for 2016

19

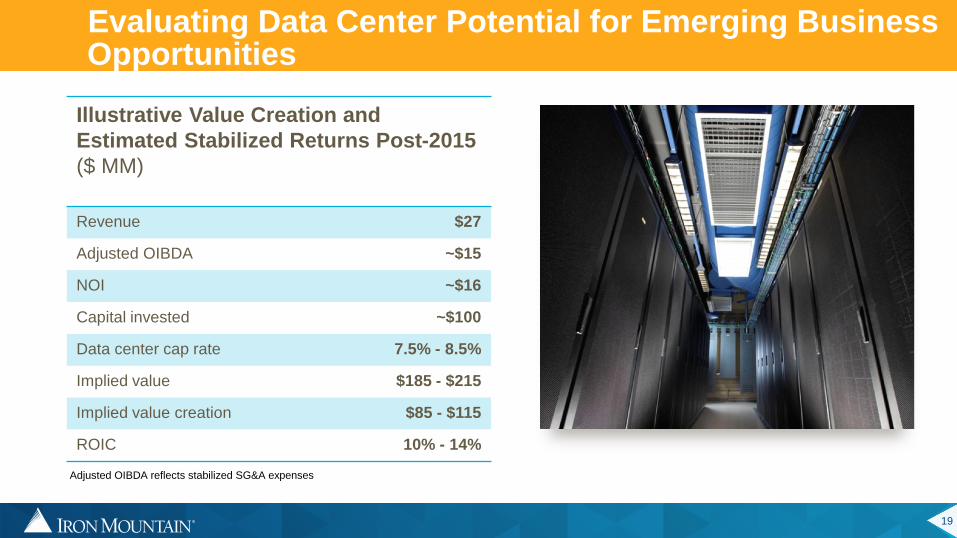

Evaluating Data Center Potential for Emerging Business Opportunities

Illustrative Value Creation and

Estimated Stabilized Returns Post-2015

($ MM)

Revenue $27

Adjusted OIBDA ~$15

NOI ~$16

Capital invested ~$100

Data center cap rate 7.5% - 8.5%

Implied value $185 - $215

Implied value creation $85 - $115

ROIC 10% - 14%

Adjusted OIBDA reflects stabilized SG&A expenses

20

$3,026

$3,360- $3,470

$2,200

$2,400

$2,600

$2,800

$3,000

$3,200

$3,400

$3,600

2013 Base Incremental M&A 2016 E

Strategic Plan Drives Solid Revenue Growth

($MM)

$200 - $265

$135 - $175 + Potential

Upside from EBOs

+ Potential Upside

from Additional

EBOs

Growth projection is on a constant dollar basis based on 2014 C$ budget rate

21

Low-volatility, Moderate Growth with Attractive Yield

$919

$35-$60

$20-$45 $20-$30 $995 - $1,055

Adj. OIBDA 2013 Base Incremental M&A Speed and Agility Adj. OIBDA 2016 E

*Assumes a 4% dividend yield

2013 excludes restructuring charges. Growth projection is on a constant dollar basis based on 2014 C$ budget rate

ROIC 9.7% 10% - 11%

Avg. Inv. Capital

~$5.5B ~$6.3B

($MM)

Driving Total Shareholder Returns - projected to be between 8% to 9%*

+ Potential Upside from

EBOs

+ Potential Upside

from Additional

EBOs

22

Drivers of Net Asset Value (NAV)

Corporate Governance

Balance Sheet Risk

Franchise Value

Premium / Discount to NAV

Overhead Structure

23

Significant Franchise Value Supports Enhanced Valuation

Solid track record of enhancing shareholder value

Share buybacks, pursuing REIT conversion, dividend enhancement

Most expansive global platform

Difficult and expensive to replicate

Strong international expansion opportunity

Attractive real estate characteristics

Low turnover costs

Low maintenance capex

High retention, low volatility

Formal corporate responsibility program and inclusion in SRI Indexes

24

Strong Corporate Governance Profile

Demonstrated responsiveness to investors

Non-staggered, independent Board with significant investment

No antitakeover provisions

Low potential conflicts of interest

25

Attractive Balance Sheet / Capital Structure Poised for Improvement as a REIT

Debt-to-total-market cap compares favorably

IRM debt-to-total market cap of 37%1

Minor amount of secured debt

Low percentage of floating rate debt

Low repayment/refinancing risk

Limited development/unfunded development

Intend to de-lever over time as a REIT

Refinancing in international markets to provide natural hedge and get

benefits of interest rate tax shield in taxable jurisdictions (1) Based on 02/20/2015 closing prices of $36.71 and 212 million shares outstanding

26

Overhead Structure Reflects Defensible Moat and Operating Business

High-return storage rental business

Average Adjusted OIBDA margins consistent with other

property types

Service business margins ~18% including overhead

Greater allocation to service due to nature of business

Lower capital intensity, so returns in line with storage business

Integrated business model drives new sales and retention,

but overhead will naturally be higher than traditional REITs

Limited additional operating leverage

Low downside risk, but limited upside potential

27

“Enterprise Storage” Compares Favorably

Iron Mountain Self-storage Industrial

North America annual rental revenue/SF $27.00 $13.80 $5.50

Tenant Improvements/SF N/A N/A $1.96

CapEx(1) ~3% 5.3% 12%

Average lease term Large customers: 3 Yrs.

Small customers: 1 Yr. Month-to-Month ~4-6 yrs.

Customer retention ~98% ~85% ~75%

Customer concentration Very low Very Low Low

Customer type Business Consumer Business

Non-Real Estate %(2) 30% 20% 10%

Stabilized Occupancy

(building & racking utilization)

Building: 80% to 85%

Racking: 90% to 95% 90% 93%

Operating Margin(3) Storage: 70% - 75% 68% 70%

(1) IRM CapEx represents maintenance CapEx as a percentage of Revenues. Comps represent recurring CapEx as a percentage of NOI. Excludes leasing commissions. (2) Non-Real Estate % for IRM is as a % of Total Adj. OIBDA. Comps are as a % of Assets. (3) Operating margin for IRM is storage gross margin.

Source: Company estimates and filings. Benchmark data provided by Green Street Advisors and J.P. Morgan

28

Potential for Broadened Investor Base and Enhanced Valuation

15.0

16.8

17.3

17.3

18.1

18.7

21.3

20.3

22.3

23.3

18.5 x

LPT

FR

PSB

EGP

DRE

DCT

PLD

CUBE

EXR

PSA

IRM

Price-to-2015 Pro Forma FFO

4.9%

1.9%

2.4%

3.6%

3.1%

3.1%

3.0%

2.6%

2.9%

2.8%

4.8%

LPT

FR

PSB

EGP

DRE

DCT

PLD

CUBE

EXR

PSA

IRM

Pro Forma Current Dividend Yield

*Based on a pro forma 2015 dividend of $1.90 per share, and 212 MM shares outstanding and a stock price of $39.37 as of 02/13/2015. REIT pricing as of 02/13/2015

Source: Company estimates and FactSet mean FFO and AFFO estimates.

19.5

22.6

23.8

22.0

22.0

26.2

26.4

21.2

22.8

24.4

16.7 x

LPT

FR

PSB

EGP

DRE

DCT

PLD

CUBE

EXR

PSA

IRM

Price-to-2015 Pro Forma AFFO

SE

LF

-ST

OR

AG

E

IND

US

TR

IAL

29

Key Messages

We are uniquely positioned to create value through our operating model and real estate strategy

Our market leadership position supports long-term value

Fundamentals support stable growth in storage rental

Leading storage rental-driven business, supported by market leadership and stable fundamentals, drives attractive shareholder returns

Attractive business characteristics underscore value creation

30

Questions?

© 2015 Iron Mountain Incorporated. All rights reserved. Iron Mountain and the design of the mountain are registered trademarks of Iron Mountain Incorporated.

All other trademarks and registered trademarks are the property of their respective owners.

Appendix

32

Updated Guidance

$MM 2015 Guidance C$ YOY Growth 2015 Guidance C$ YOY Growth

Operating Performance

Revenue $3,030 - $3,150 1% - 5% (1) $3,135 - $3,290 1% - 5% (1)

Adjusted OIBDA $905 - $945 1% - 5% (1) $945 - $985 2% - 5% (1)

Adjusted EPS – Fully Diluted $1.15 - $1.30 (2) $1.23 - $1.38

FFO (Normalized) $425 - $465 $440 - $480

FFO (Normalized) per share $2.00 - $2.20 (2) $2.12 - $2.28

AFFO (Old Definition) $550 - $590 $570 - $610

AFFO (New Definition) (3) $480 - $520 n/a

Capital Allocation

Total Capital and Investments (excluding Dividends) $550 - $650 $550 - $650

Real Estate Investment $230 - $270 $240 - $280

Maintenance CapEx $70 - $90 $80 - $100

Non-Real Estate Investment $70 - $90 $40 - $60

Business and Customer Acquisitions $150 - $250 $150 - $250

As of December 31, 2014 As of September 30, 2014

(1) YOY growth compared to 2014 constant dollar (C$) budget rates; includes 0% - 2% internal revenue growth

(2) Assumes 212 million shares outstanding

(3) AFFO (New Definition) is defined in the appendix (page 30) and further adjusts for Non-Real Estate Investment

33

Reconciliation of Net Income to Adjusted OIBDA

Q4 2013 Q4 2014 % Change FY 2013 FY 2014 % Change

Net Income (Loss) Attributable to Iron Mountain Incorporated $47,059 $12,749 (72.9)% $96,462 $326,119 n/a

Add:

Net Income (Loss) Attributable to Noncontrolling Interests 596 654 9.7% 3,530 2,627 (25.6)%

Loss (Income) from Discontinued Operations, Net of Tax 684 (729) n/a (831) 209 n/a

(Gain) Loss from Disposition of Real Estate, Net of Tax - (839) 0.0% (1,417) (8,307) n/a

Provision (Benefit) for Income Taxes (26,017) 876 (103.4)% 62,127 (97,275) n/a

FX (Gains) Losses (1) 13,660 32,726 n/a 36,203 58,318 61.1%

Other (Income) Expense (2) (2,425) 9,473 n/a 38,999 6,869 (82.4)%

Interest Expense, Net 63,518 72,984 14.9% 254,174 260,717 2.6%

Operating Income (Loss) $97,075 $127,894 31.7% $489,247 $549,277 12.3%

Depreciation and Amortization 83,249 88,575 6.4% 322,037 353,143 9.7%

(Gain) Loss on Disposal/Write-Down of PP&E (excluding Real Estate), Net 958 (164) (117.1)% 430 1,065 n/a

REIT Costs 13,638 3,728 (72.7)% 82,867 22,312 (73.1)%

Adjusted OIBDA $194,920 $220,033 12.9% $894,581 $925,797 3.5%

(1) Includes realized and unrealized FX (gains) losses (2) Excludes realized and unrealized FX (gains) losses; FY 2013 includes $44 million loss on extinguishment of debt and FY 2014 includes $16 million