POLICY POSITION PAPER ON THE PRUDENTIAL TREATMENT OF

CAPITALISED EXPENSES

RESULTS OF A SURVEY OF AUTHORISED DEPOSIT-TAKING INSTITIONS,

UNDERTAKEN BY THE AUSTRALIAN PRUDENTIAL REGULATION

AUTHORITY

June 2003

Lyndon Kingston

Hillary Maddox

Page 2

TABLE OF CONTENTS EXECUTIVE SUMMARY ......................................................................................................................................................3 INTRODUCTION......................................................................................................................................................................4

1. SURVEY RESULTS .......................................................................................................................................................7

2. ACCOUNTING STANDARDS ................................................................................................................................ 15

3. PRUDENTIAL STANDARDS .................................................................................................................................. 18

4. DISCUSSION AND RECOMMENDATIONS ..................................................................................................... 20

5. CONCLUSIONS ........................................................................................................................................................... 25

6. CONSULTATION AND APPLICATION............................................................................................................. 27

Page 3

Executive Summary

This report presents the results and analysis of a survey of Australian Authorised Deposit Taking

Institutions (ADIs)1 undertaken by the Australian Prudential Regulation Authority (APRA). The purpose

of the survey was to examine and quantify the accounting policy, nature and materiality of capitalised

expenses and intangible assets recognised by ADIs for financial and regulatory reporting purposes. From

this APRA assessed whether the prudential definition of intangible assets needed to be clarified, to achieve

better consistency in prudential reporting and application of the capital adequacy framework.

The review of the survey responses highlights the following:

1. General consistency across ADIs in the classification and treatment of intangible assets for financial

reporting, however some key exceptions exist. In addition there is a degree of inconsistency in the

accounting policy adopted by ADIs for the recognition and treatment of capitalised expenses for

financial reporting and regulatory reporting purposes. This introduces differences and inconsistencies

between ADIs in financial reporting and the application of the capital adequacy framework.

2. The amount of capitalised expenses recognised and deferred as assets by ADIs is relatively modest at

the industry level in proportion to total assets and regulatory capital, but it is evident that this rate of

contribution is growing. In addition there are a number of ADIs where the relevant items comprise up

to and exceed 10% of the ADI’s regulatory capital base. APRA does not consider it prudentially

appropriate for such material proportions of capital to be represented by capitalised expenses.

APRA proposes to clarify the definition of intangible assets for prudential reporting purposes to include

certain capitalised expenses, thereby deducting these from Tier 1 capital in accordance with Prudential

Standard APS 111‘Capital Adequacy: Measurement of Capital’, paragraph 9.

1 Comprising Australian owned banks, foreign bank subsidiaries, building societies and credit unions.

Page 4

Introduction

Capital is the cornerstone of an ADI’s strength and a strong capital position helps to ensure that an ADI

has the capability to absorb a reasonable level of unexpected losses from its activities. A measure of the

capital strength of an ADI is the capital adequacy ratio , the amount of an ADI’s regulatory capital

expressed as a percentage of its risk weighted exposures (i.e. on-balance sheet assets and off-balance sheet

exposures). According to Prudential Standard APS 110 ‘Capital Adequacy’, three main elements

determine an ADI’s capital adequacy:

Ø credit risk associated with exposures;

Ø market risk arising from trading activities; and

Ø the form and quality of capital held to support these exposures.

This capital adequacy framework serves to protect depositors and promote the stability and confidence in ,

the financial soundness of ADIs and the Australian financial system.

The prudential profile of the ADI industry as at 30 September 2002 is provided in Table 1.

Table 1 Prudential Profile of the ADI Industry

ADI

Total Assets

$M

% of Total Assets to

Total Industry

Assets

Regulatory Capital

$M

% of Regulatory

Capital to Total

Industry Capital

Total Risk Weighted

Exposures$M

% of Total Risk

Weighted Exposures

to Total Assets

% of Total

Capital Base to

Total Assets

% of Total Capital Base to

Total Risk Weighted

Exposures

Australian Owned Banks 1,145,997 90.5% 73,892 87.7% 737,883 64.4% 6.4% 10.01%

Foreign Subsidiary Banks 75,787 6.0% 6,831 8.1% 48,177 63.6% 9.0% 14.18%

Building Societies 13,171 1.0% 1,026 1.2% 7,249 55.0% 7.8% 14.15%

Credit Unions 26,694 2.1% 2,294 2.7% 15,898 59.6% 8.6% 14.43%

Other ADIs 4,589 0.4% 206 0.2% 752 16.4% 4.5% 27.40%

TOTAL 1,266,238 100% 84,249 100% 809,960

Note: Data is based on APRA statistical returns as at 30 September 2002 for the ADI consolidated group.

The measurement of the capital adequacy of an ADI is directly linked to the recognition and measurement

of its assets and capital. Accordingly, standards are a necessary prerequisite to ensure an accurate and

consistent interpretation of the capital adequacy framework is applied. Standards governing the

Page 5

recognition and measurement requirements of regulatory capital and regulatory assets incorporate the

recognition and measurement requirements of the accounting standards. Accounting standards are used in

the capital adequacy framework as they establish widely accepted rules for the recognition and

measurement of revenues, expenses, assets, liabilit ies and capital. Accordingly accounting standards

establish a framework that increases the understanding of and confidence in financial information, which

is essential for investors, depositors, regulators and others to be able to rely on credible and comparable

financial information.

The conceptual basis of accounting standards is predominantly structured on a going concern basis for the

operations of an entity, which is reflected in the accounting recognition and measurement requirements.

The prudential standards of the capital adequacy framework however, is biased more heavily towards a

liquidation basis, which seeks to ascribe a realisable recognition and measurement basis for assets and

capital supporting an ADI’s operations. This difference in conceptual basis is the most fundamental and

important difference between accounting standards and prudential standards in terms of the capital

adequacy framework. This important difference can result in divergent application of recognition and

measurement requirements of the accounting standards for certain asset and capital items for capital

adequacy purposes. Goodwill and identifiable intangible assets are an example of this. Values for these

items are recognised as assets and therefore capital under the accounting standards, but are not recognised

as regulatory assets and therefore regulatory capital under the capital adequacy framework.

Tension has emerged between accounting standards and prudential standards in terms of the accounting

policy adopted by ADIs for the recognition of certain expenses as assets and deferring the recognition of

these expenses over a number of years for both financial and prudential reporting. APRA has been

monitoring the growth in the recognition of capitalised expenses by ADIs over a number of financial years

and is increasingly concerned about the potential growth in value of these assets relative to regulatory

capital and the consistency of accounting treatment across ADIs. For prudential purposes, the main

concern is that, like goodwill and identifiable intangible assets, capitalised expenses may not be realisable

if need to protect policyholders.

To aid in quantifying the magnitude and consistency of this accounting practice across ADIs, and to

understand the practice in recognition and measurement of intangible assets and capitalised expenses,

APRA sent a survey to all Australian ADIs in September 2002 requesting details on their exposure to, and

accounting policy for, the recognition and measurement of capitalised expenses, up-front loan fees and

commissions received and intangible assets. In total, surveys were sent to 243 ADIs. The response rate

across all ADIs was 64% with responding ADIs accounting for 99% of total assets and 98% of total

prudential capital. The sector coverage (in terms of total assets) of responding ADIs is set out in Table 2.

It is considered that the ADIs that did not respond would not have a material influence on the survey

Page 6

results (materiality of ADI sectors is highlighted in table 1). APRA is grateful to all ADIs who participated

and provided the information necessary for this review.

Table 2 Response Rate

Response Rate of ADIs to Survey Australian

Owned BanksForeign Bank

Subsidiaries Building Societies Credit Unions

Total Industry

Number of ADIs responding 13 13 12 116 154

Percentage of Total Assets 100% 98% 72% 70% 99%

Percentage of Total Regulatory Capital 100% 96% 63% 70% 98%

The remainder of this report is structured into the following sections: 1. Survey Results

2. Accounting Standards

Overviews accounting principles used to recognise assets.

3. Prudential Standards

Overviews the capital adequacy requirements.

4. Recommendations

Outlines the proposed prudential accounting treatment.

5. Conclusions

Outlines the impact on regulatory capital of the proposed prudential accounting treatment.

This report does not encompass a policy discussion of capitalised expenses or intangible assets relating to

life and general insurance businesses which are controlled by ADI’s, but it does include such assets as part

of the discussion of the results of the survey. Assets in the nature of capitalised expenses and intangible

assets attributable to APRA regulated insurance businesses will be the subject of a future review specific

to the insurance industry. Assets of general insurers in the nature of capitalised expenses (i.e. Deferred

Acquisition Costs and Deferred Reinsurance Expenses), are permitted by AASB 1023 “Financial

Reporting of General Insurance Activities” to be capitalised as assets for financial reporting purposes,

however, they do not qualify for recognition as regulatory assets and must be fully expensed when

incurred under the revised prudential accounting framework of the Prudential Standards for APRA

regulated general insurers introduced from 1 July 2002.

Page 7

1. Survey Results

In September 2002, APRA sent a survey to all Australian owned banks, subsidiaries of foreign banks,

credit unions and building societies. This survey requested each ADI to list for the licensed ADI and

the consolidated ADI group, the value of assets recognised in the nature of capitalised expenses,

intangible assets and up front loan fees received recognised as revenue and as unearned income for its

last financial year. The survey information is summarised below into capitalised expenses and

intangible assets and is based on the values reported for the consolidated ADI group.

Capitalised Expenses

Table 3 summarise the survey results in terms of the proportion of capitalised expenses to total

regulatory capital of responding ADIs. Table 3 shows that the bulk of the value of capitalised expenses

recognised by ADIs is attributable to Australian owned banks, as 85% have exposure to capitalised

expenses of greater than 2.5% of regulatory capital, compared to 23% for responding foreign bank

subsidiaries, 33% for responding building societies and 5% for responding credit unions.

For the purposes of the analysis in Table 3 the value of capitalised expenses has been adjusted for

certain Australian owned banks. The adjustment removed capitalised expenses attributable to insurance

subsidiaries (i.e. deferred acquisition costs) that were included in the total value of capitalised expenses

reported in the surveys (refer to Table 4 for the total value). This was done because the analysis

conducted in Table 3 and 4 is based on the regulatory capital base of Australian owned banks, which

excludes retained earnings and reserves of these insurance subsidiaries. If the above adjustment was

not made this may have incorrectly increased the percentage of capitalised expenses to Total

Regulatory Capital.

Table 3 Capitalised Expenses as a Percentage of Total Regulatory Capital Base of Responding ADIs

Percentage of Total Regulatory Capital Base

% Band

Australian Owned Banks

(Number)

Foreign Bank Subsidiaries

(Number)

Building Societies

(Number)Credit Unions

(Number)0% - 5 4 83

0.01 - 2.5% 2 5 4 27 2.6 - 5.0% 6 1 1 3 5.1 - 7.5% 3 1 - 3

7.6 - 10.0% 1 - 2 - 10.1 - 12.5% - 1 - -

12.6 - 15.0% 1 - - - >15.0% - - 1 -

13 13 12 116

1 Total Regulatory Capital Base is based on the consolidated group reported in the APRA statistical data as at 30 September 2002 and only include ADIs that responded to the survey as highlighted in Table 1 'Response Rate'.

Page 8

Based on Table 4, capitalised expenses of the ADI industry make up about 4% of regulatory capital

after excluding deferred acquisition costs relating to insurance businesses of ADI group subsidiaries

and certain prepayments. Prepayments have been excluded as they differ in nature to other forms of

capitalised expenses. Capitalised expenses relating to loan and lease origination broker fees /

commissions are more material in terms of the percentage exposure to regulatory capital base for

foreign bank subsidiaries and building societies. This result is consistent with the survey conducted by

APRA on the use of brokers for loan origination in 2002 and is also reflective of the distribution profile

of these ADIs.

By far the most material capitalised expense relates to software development costs, with the combined

exposure to ‘software development costs – WIP’(1.3%) and ‘software development costs – In use’

(1.1%) to total regulatory capital represents 2.4% for the entire ADI industry and 2.7% for Australian

owned banks. For Australian owned banks the bulk of this total expenditure comprises costs associated

with staff salaries and consultants, which on average constitute roughly 80% of the total capitalised

software development costs (this ranges from 95% – 73%). Costs associated with software application

and hardware account for the residual. This type of information was only collected for Australian

owned banks as it was not seen to be material for other ADIs.

Table 4 Classification of Capitalised Expenses

Classification of Total Capitalised Expenses $M

% of Total Capital

Base $M

% of Total Capital

Base $M

% of Total Capital

Base $M

% of Total Capital

Base $M

% of Total Capital

Base

Total Capitalised Expenses 4,040 5.5% 230.9 3.5% 29.2 4.5% 19.2 1.2% 4,319 5.2%

Total capitalised expenses classified into:

Loan origination fees / commissions 655 0.9% 185.6 2.8% 22.0 3.4% 0.2 0.0% 863 1.0%Software development costs - WIP 1,074 1.5% - - - - - - 1,074 1.3%Software Development Costs - In use 874 1.2% 36.1 0.6% 0.7 0.1% 15.4 1.0% 926 1.1%Securitisation establishment costs 27 0.0% 5.5 0.1% 5.7 0.9% 0.2 0.0% 39 0.0%

Debt / capital raising costs 125 0.2% 0.4 0.0% 0.2 0.0% 0.9 0.1% 127 0.2%Deferred acquisition costs - insurance 733 1.0% - - - - - - 733 0.9%Prepayments 485 0.7% 0.2 0% - - - - 485 0.6%All Other Capitalised Expenses 67 0.1% 3.2 0.0% 0.5 0.1% 2.5 0.2% 73 0.1%

1

2

3 Survey information is based on the financial year of the consolidated group ending in 2002. The prudential data is based at 30 September 2002.

Total Capital Base' refers to Total Regulatory Capital Base as reported for the consolidated group in the APRA statistical data as at 30 September 2002 and only include the regulatory capital of ADIs that responded to the survey as highlighted in Table 1 'Response Rate'.

Australian Owned Banks

Foreign Bank Subsidiaries Building Societies Credit Unions Industry Total

Software development costs are classified into 'Work in Progress' (comprising feasibility and development stages) and 'In Use' (completed and operational stage). Only Australian owned banks reported the details of both classifications as they have the most material balances in the development stages. For the purpose of this analysis all other ADI's software costs were considered as 'In Use' unless specifically advised. This was due to immaterially.

Page 9

The following additional points are noted from the review of survey responses.

A. Accounting policy

Loan and lease origination fees / commissions

The following differences were noted in the accounting policy adopted by ADIs:

Ø While the majority of ADIs recognise and capitalise these as assets, others recognise these

fully as an expense when incurred.

Ø Disclosure of these assets in the statement of financial position was either reported or included

under the heading “Other Assets”, “Other Financial Assets”, or “Loans and Advances”.

Ø Those ADIs adopting an accounting policy of capitalising these expenses generally deferred

the expense recognition in line with matching the recognition of the income stream from the

underlying asset. From a financial accounting perspective this more appropriately reflects the

annual return on these assets over their life. This is a similar position for capitalising initial set

up transaction costs associated with the raising of debt / capital and securitisation vehicles.

Ø Instances have been highlighted where the amortisation policy for the expense recognition of

capitalised fees paid to loan originators and brokers does not appropriately accommodate the

impact of loan prepayments in terms of early pay out or refinancing of the underlying loans

originated.

Software development costs.

Ø There tends to be a more established and recognised principle for accounting policy on

capitalising software development costs. The accounting basis adopted by ADIs for

capitalising such costs as an asset is generally consistent and is based on the premise that the

costs are a necessary investment to enhance or upgrade the utilisation or functionality of the

asset, or the cost extends the useful life of the information systems of the ADI and therefore

the value in use to the ADI.

Ø Amortisation periods ranged from 3 years to 10 years.

Ø In terms of the classification of software development related costs for financial reporting

purposes, disclosure was commonly under the heading ‘Fixed Assets’, ‘Property, Plant &

Equipment’ or ‘Other Assets’ in the statement of financial position.

Page 10

Capitalisation of securitisation establishment costs; costs associated with debt / capital raisings and

all other similar transaction related costs

The majority of responding ADIs recognise and capitalise these as assets and defer expense

recognition over a period of time (e.g. maturity of debt raised), while others recognise these fully

as an expense when incurred.

B. Other general points noted.

Australian owned banks

Ø Banks were consistent in classifying the type of assets representing capitalised expenses.

Ø A relatively broad interpretation of what items of expenses are appropriate to capitalise and

defer as an asset has been adopted by a few banks.

Foreign subsidiary banks

Ø Foreign bank subsidia ries were consistent in terms of classifying the type of assets representing

capitalised expenses in the survey.

Ø The total value of capitalised expenses recorded for loan and lease origination and broker

commissions / fees is essentially concentrated in 3 foreign bank subsidiaries out of the 13

respondents.

Building societies

Ø Classification of items in the nature of capitalised expenses for the purpose of the survey was

generally consistent across responding building societies. However, an important point noted

was that capitalised software development costs were reported as a capitalised expense asset by

only 3 of the 12 responding building societies. This fact contributes to the relative low

percentage exposure recorded in Table 4 for building societie s. The 3 responding building

societies that did consider software development costs as a capitalised expense classified this

asset for financial reporting purposes as either ‘Property, Plant & Equipment’ or ‘Fixed

Assets’.

Ø Building societies have a signif icantly higher relative percentage exposure to capitalised

expenses associated with securitisation establishment costs than other ADIs. In both relative

and absolute terms they have a lower exposure to capitalised transaction costs associated with

Page 11

debt / capital raising than other ADIs. Given the differences in accounting treatment it is

difficult to draw definitive conclusions from this, but in relative terms this result is likely to be

attributable to securitisation being a preferred source of funding for building societies.

Credit unions

Ø As noted in the review of the survey results for intangible assets, there was inconsistency

among responding credit unions as to the classification of software and information technology

related expenses. They were either reported as an intangible asset or as a capitalised expense.

Ø The largest capitalised expense for credit unions relates to software development. Credit

unions have a higher relative exposure to software development costs in terms of percentage of

regulatory capital base than foreign bank subsidiaries and building societies. This result may in

part be due to the fact that the majority of responding building societies did not report software

development costs as capitalised expenses on the survey.

Intangible Assets

An analysis of the results of the survey responses are summarised in Table 5.

Table 5 Survey Summary for Intangible Assets

Composition of Intangible Assets $M

% of Total Capital

Base $M

% of Total Capital

Base $M

% of Total Capital

Base $M

% of Total Capital

Base $M

% of Total Capital

Base

Total Intangible Assets 20,872.1 22.9% 255.0 3.8% 4.6 0.7% 11.4 0.7% 21,143.2 21.1%Comprising:

Goodwill 9,568.1 10.5% 143.7 2.1% 1.5 0.2% 3.4 0.2% 9,716.7 9.7%

FITBs 374.0 0.4% 111.3 1.7% 0.0 0.0% 6.1 0.4% 491.4 0.5%Excess of net market value over net assets of life insurance controlled entities

10,927.0 12.0% - - - - - - 10,927.0 10.9%

Intellectual property 3.0 0.0% - - - - - - 3.0 0.0%Information Technology related costs - - - - - - 1.0 0.1% 1.0 0.0%Other capitalised expenses - - - - 3.2 0.5% 0.9 0.1% 4.1 0.0%

1. Total intangible assets based on survey results for the consolidated group.

3 Survey information is based on the last financial year of the consolidated group at the date of the survey.

Credit Unions Industry Total

2. Total Capital Base.Total Capital Base' represents total regulatory capital base of ADIs recorded in APRA's statistical data as at 30 September 2002 for responding ADIs only. 'Total Capital Base' is adjusted for the purposes of this analysis by adding back the reported value of goodwill and other intangible assets deducted from regulatory capital base for the purposes of determining the capital adequacy ratio as at 30 September 2002. Only the prudential value of goodwill and intangible assets are added back to total regulatory capital base.

Australian Owned Banks

Foreign Bank Subsidiaries Building Societies

Page 12

As highlighted in this table the bulk of intangible assets are attributable to the operations of the

Australian owned consolidated banking groups concentrated in the recognition of ‘goodwill’ and ‘excess

of net market value over net assets of life insurance controlled entities’. The value recognised for

goodwill predominantly relates to 4 Australian owned banks and the value recognised for ‘excess of net

market value over net assets of life insurance controlled entities’ predominantly relates to 2 Australian

owned banks. As expected the materiality of goodwill reduces significantly outside the banking sector.

In overall terms the bulk of intangible assets are concentrated with 2 Australian owned banks.

Table 5 also highlights some inconsistencies in the type of asset items that ADIs consider to be

intangible in nature for the purposes of the survey. Assets in the nature of information technology related

expenses and certain types of capitalised expenses are considered to be intangible by some responding

credit unions and building societies respectfully but not by any responding bank. Those capitalised

expenses considered intangible in nature by the minority of building societies relate to loan origination

broker fees and transaction costs associated with debt / capital raisings and securitisation establishment.

Disclosure of these capitalised expenses as intangible assets for financial reporting and prudential

reporting purposes (i.e. deduction from regulatory capital base) was inconsistent between the applicable

building societies.

The following are also highlighted from the review.

A. Accounting policy

Ø Accounting policy adopted by ADIs for the recognition, amortisation and disclosure of

goodwill and ‘excess of net market value over net assets of life insurance controlled entities’

for financial reporting purposes was consistent. Disclosure of goodwill in the statement of

financial position for financial reporting purposes was under the heading of “Goodwill” and

“Intangible Assets”.

Ø While being considered as intangible in nature, the value of ‘excess of market value of net

assets of life insurance business’ recognised in accordance with AASB 1038 ‘Life Insurance

Business’, was classified under “Other Assets” for financial reporting purposes. This

classification was consistently adopted by applicable Australian owned consolidated banking

groups. The Australian accounting disclosure requirements for this item do not seem consistent

or logical when comparing the materiality of this item against both the materiality and

disclosure requirements for goodwill, which is generally disclosed separately or under the

heading of intangible assets.

Page 13

B. Other general points.

Australian owned banks

Ø There was consistency in terms of the type of asset items each considered intangible in nature

for the purposes of the survey. The exception was future income tax benefits (FITBs) where a

minority of banks considered these assets intangible in nature.

Foreign bank subsidiaries

Ø There was consistency in terms of the type of assets each considered intangible in nature

except for FITBs where most did not consider these assets intangible in nature.

Ø There was general consistency between the types of assets classified as intangible for the

survey and those assets classified as intangible for capital adequacy purposes (i.e. goodwill).

Building societies

Ø FITBs were not considered by any responding building society to be an intangible asset.

Ø Classification of goodwill as intangible assets for financial reporting and prudential purposes

was consistent.

Ø Certain items of capitalised expenses were considered to be intangible in nature for both the

survey and for prudential reporting purposes, but other similar items of capitalised expenses

were not considered to constitute intangible assets by the same building societies. In addition,

other building societies did not consider the same type of capitalised expenses to be intangible

in nature for the purpose of the survey and financial reporting, but do for prudential reporting.

Credit unions

Ø The majority of responding credit unions considered FITBs to be intangible in nature.

Ø There was no consistency in the classification of information technology related expenses.

These were either reported in the survey as an intangible asset or as a capitalised expense.

Ø Credit unions classifying information technology related expenses as intangible in nature for

the purpose of the survey did not adopt the same classification for prudential reporting

purposes. Apart from this, there was consistency in the classification of intangible assets for

the purposes of the survey, financial reporting and prudential reporting (i.e. goodwill).

Page 14

The survey shows that there is general consistency in classification and treatment of intangible assets

for financial reporting and prudential reporting across ADIs. However some key inconsistencies are

highlighted, mainly in relation to the treatment and classification of certain capitalised expenses. This

introduces inconsistency between ADIs in the application of the capital adequacy framework.

The impact on regulatory capital of intangible assets deducted under the capital adequacy framework is

shown in Table 6. This information is based on APRA statistical data as at 30 September 2002 and is

not based on the survey information, but it is considered relevant to this topic .

Table 6 Impact of Intangible Assets on Regulatory Capital Adequacy

Intangible Assets

Australian Owned Banks

%

Foreign Bank Subsidiaries

%

Building Societies

%

Credit Unions

%

Percentage of Intangible Assets to Total Assets 1.82% 0.18% 0.06% 0.02%

Percentage of Intangible Assets to adjusted Total Regulatory Capital Base

22.86% 2.01% 0.75% 0.18%

Capital Adequacy Ratio 10.01% 14.18% 14.15% 14.43%

Adjusted Capital Adequacy Ratio (adjusted by adding back intangibles deducted from Capital Base).

12.09% 14.43% 14.25% 14.45%

1. The value of 'Intangible Assets' is based APRA statistical data as at 30 September 2002 and includes all ADIs.

2. The value of 'Total Assets' based on APRA statistical data as at 30 September 2002 and includes all ADIs.

3. Total Regulatory Capital Base.Total Regulatory Capital Base' represents total regulatory capital base as recorded in APRA statistical returns as at 30 September 2002 for all ADIs. 'Total Regulatory Capital Base' is adjusted for the purposes of this analysis by adding back the value of goodwill and other intangible assets that are deducted from regulatory capital base for purposes of calculating an ADI's capital adequacy as recorded in APRA statistical data as at 30 September 2002. The value of goodwill and intangible assets reported in the survey are not added back to total regulatory capital base.

The value of intangible assets as a percentage of adjusted total regulatory capital base for Australian

owned consolidated banking groups largely relates to goodwill (11.17%) and to ‘excess of net market

value over net assets of life insurance controlled entities’ (10.96%). The bulk of the intangible assets

deducted from regulatory capital (75%) are attributable to two Australian owned consolidated banking

groups. For foreign bank subsidiaries the intangible asset deduction is due to goodwill which is

attributable to two foreign bank subsidiaries. The value of intangible assets as a percentage of adjusted

total regulatory capital base for building societies relate to goodwill (0.19%) and to certain capitalised

expenses (0.56%): which is largely attributable to one building society. Apart from one other building

society capitalised expenses are not deducted as intangible assets from regulatory capital by any other

ADI. This highlights inconsistency in terms of the type of intangible assets that are deducted from

regulatory capital.

Page 15

2. Accounting Standards

APRA’s purpose in reviewing the accounting requirements is not to debate the interpretation and

application of accounting standards by ADIs, but is aimed at understanding the accounting basis or

policy adopted by ADIs in the recognition and measurement as assets, items constituting capitalised

expenses.

There are generally accepted accounting principles governing the requirements for recognising and

measuring assets. Whether expenditure is recognised as an asset or an expense may have a material

effect on an ADI’s reported financial performance and position. In terms of the ability of ADIs to

recognise and capitalise as assets items of expenditure and defer the recognition of the expense over a

period, there are non-mandatory generally accepted accounting principles that ADI’s are able to

reference, in particular Statement of Accounting Concepts 4 “Definition and Recognition of the

Elements of Financial Statements” (SAC 4). SAC 4 sets out non-mandatory principles for the three

essential characteristics that are to be satisfied as a prerequisite for an asset to be recognised:

1. It must represent future economic benefits to the entity;

2. The entity must have control over those future economic benefits so that it can enjoy the benefits

and regulate the access to others; and

3. The event giving rise to the entity’s control over the future economic benefit must have occurred.

A future economic benefit is the capacity to provide benefits to the ADI that uses the asset. An asset

should only be recognised when it is probable that the future economic benefits embodied in the asset

will eventuate, and the asset possesses a cost or other value that can be measured reliably.

Capitalisation is the recognition of the cost of creating or enhancing an asset as defined above.

Capitalisation occurs for new assets constructed; asset acquired and for asset enhancements when work

is complete. Expenditure on an asset is considered an enhancement or upgrade where the expenditure

results in an increase in the utilisation or functionality of the asset, or extends its useful life.

Capitalisation of such expenditure occurs under two conditions; capitalisation is at its actual cost, and

expenditure is written off over the estimated useful life of the asset.

Apart from this non-mandatory guidance on the recognition requirements for assets provided in SAC 4,

there are accounting standards and mandatory requirements applicable for ADIs, including the

following:

Page 16

Ø AASB 1021 ‘Depreciation’ requires that the amortised amount of an asset must be allocated on a

systemic basis over its useful life. The depreciation method applied to the asset must reflect the

pattern in which the future economic benefits are consumed by the entity. These costs should only

be deferred to future periods to the extent that benefits are expected to equal or exceed the costs.

The depreciable amount must be allocated from the time when the asset is first put into use.

The accounting policy of most ADIs is to amortise fees and commissions paid to loan and lease

brokers / originators over the expected life of the applicable underlying loan and lease portfolios,

with amortisation periods generally ranging from 3 to 5 years among ADIs. This indicates that

ADIs consider the useful life of the applicable underlying loan portfolio to be 3 to 5 years.

Instances have been highlighted where the amortisation period adopted was not appropriately

structured to accommodate the impact of loan prepayments in terms of payouts / refinancing prior

to contractual maturity of the underlying loans originated. For software development costs,

amortisation periods ranged from 3 to 10 years depending on the ADI’s assessment of the useful

life of the asset.

Ø AASB 1036 Borrowing Costs

This standard provides that when it is probable that the incurrence of borrowing costs will result in

future economic benefits and they can be reliably measured, they may be capitalised and included

in the carrying amount of an asset, subject to the asset meeting the definition of a qualifying asset

in AASB 1036. Te standard provides that financial assets are not qualifying assets. Borrowing costs

that are incurred for purposes other than to acquire the future economic benefits embodied in

qualifying assets are to be expensed as part of the periodic expenses of financing the entity's

operations. This would include borrowing costs relating to working capital and the holding of

equity securities. The standard provides that borrowing costs include:

(a) Interest on overdrafts and short-term and long-term borrowings; (b) Amortisation of discounts or premiums relating to borrowings;

(c) Amortisation of ancillary costs incurred in connection with the arrangement of

borrowings. Ancillary costs include non-refundable costs associated with originating or

acquiring a loan / finance. Such costs are typically accrued and amortised over the period

of a loan / financing;

(d) Finance charges in respect of finance leases recognised in accordance with Accounting

Standard AASB 1008 “Accounting for Leases”; and

(e) Exchange differences arising from foreign currency borrowings net of the effects of any

hedge of the borrowings.

Page 17

Additionally, while ADIs incorporated in Australia are required to adhere to Australian accounting

standards, international accounting standards may also provide guidance. In particular the Exposure

Draft of International accounting standards IAS 39 ‘Financial Instruments: Recognition and

Measurement’. This standard requires that transaction costs directly associated with a financial

instrument are required to be included in the initial recognition of the cost of the financial instrument.

Depending on the classification of the financial instrument and therefore the measurement basis (i.e.

fair value or amortised cost), transaction costs will be accounted for differently after initial recognition.

Under the fair value measurement framework transaction costs recognised initially in the cost of the

financial instrument will be expensed on initial restatement to fair value most likely in the form of a

revaluation loss, whereas under amortised cost measurement transaction costs will be recognised as an

expense over the life of the financial instrument.

There are accounting standards and mandatory requirements applicable for other industries that may be

viewed as providing some form of precedence or support from a financial reporting perspective for

ADI’s to capitalise expenses associated with the acquisition of assets or the sourcing of liabilities.

These accounting precedents relate to the following:

Ø AASB 1023 “Financial Reporting of General Insurance Activities” allows direct and indirect costs

associated with acquiring or writing insurance business to be capitalised as an asset and expensed

on a basis consistent with the recognition of income from the insurance policy acquired or written.

Costs can range from acquisition costs to salaries and other administrative costs, as long as they are

associated with future economic benefits of the policy.

Ø Urgent Issues Group abstract ruling 42, which is applicable for the telecommunications industry.

The ruling requires subscriber acquisition costs directly attributable to establishing specific

subscriber contracts, to be recognised as an asset where the asset definition and recognition criteria

are satisfied. Capitalised acquisition costs are required to be amortised over the period of expected

benefit (for example, up to the contract period, where specified).

Page 18

3. Prudential Standards

According to Prudential Standards APS 110 ‘Capital Adequacy’, the capital adequacy framework

requires ADIs on both a licensed entity basis, and a prudential consolidated ADI group basis, to

maintain a level of regulatory capital that is adequate and consistent with the risks to which they are

exposed from their activities. The minimum capital requirement is expressed as the capital adequacy

ratio, which is the amount of regulatory capital as a percentage of total risk weighted exposures

(comprising assets recognised on-balance and off-balance sheet exposures of the ADI). The reported

values of on-balance sheet assets and off-balance sheet exposures are risk weighted according to a

nominal risk profile, with higher risk weights (and therefore capital requirements) applied to assets and

exposures reflecting a deemed higher risk. The risk weights incorporate credit and market risk factors.

This measurement methodology for risk has been in place since 1988 and is currently being re-

examined by the Basel Committee on Banking Supervision and its proposed “Basel II” capital

framework.

The other crucial aspect in the measurement of an ADI’s capital adequacy ratio is the amount and type

of capital held by the ADI (i.e. the regulatory capital base). Two types of capital comprise the

regulatory capital base of an ADI; Tier One and Tier Two capital. Tier One capital of an ADI is capital

that is permanent and available to absorb losses and safeguards both the survival of the ADI and the

stability of the financial system. As a consequence Tier One includes (with certain exceptions) ordinary

share capital, reserves and retained earnings / losses. Tier Two capital on the other hand, includes other

forms of capital such as perpetual and term subordinated debt. Tier Two capital absorbs losses only in

the event of a wind-up, and provides a lower level of protection for depositors and other creditors.

All incorporated ADIs must maintain , at all times: Ø A ratio of total regulatory capital to total risk weighted exposures of at least 8% or such higher

level as determined by APRA;

Ø A ratio of tier one capital to total risk weighted assets of no less than four percent; and

Ø Tier two capital must not exceed one hundred percent of tier one capital.

The prudential capital adequacy framework adopts a conservative measure of capital due to its

objective and underlying conceptual basis. As a result adjustments are required to be made to

regulatory capital to derive the eligible regulatory capital base, which is then used for the purpose of

calculating the capital adequacy ratio. The values of the following assets that are recognised under

accounting standards are required to be deducted from Tier One capital to determine the eligible

regulatory capital base:

Page 19

Ø Goodwill;

Ø Other identifiable intangible assets;

Ø Future income tax benefits (other than those associated with general provisions for doubtful debts)

net of any provisions for deferred income tax liabilities; and

Ø Equity and other capital investments in associated lenders mortgage insurers.

These assets are also excluded from the value of assets when calculating the total risk weighted

exposures of the ADI for the purpose of calculating the capital adequacy ratio. Consequently the

calculation of eligible regulatory capital base will be less than the value of shareholders equity

calculated under the accounting standards. The impact on ADIs of the deduction of goodwill and other

identifiable intangible assets for regulatory capital purposes is highlighted in Table 6 in section 1

‘Survey Results’.

The non-recognition of these assets as regulatory assets (certainly the first three in the above list)

further highlights the difference in the conceptual basis between the going concern premise underlying

the recognition and measurement requirements of the accounting standards and the bias towards a

liquidation basis underlying the capital adequacy framework. While these assets are recognised in

accordance with the accounting standards, under the conceptual basis of the capital adequacy

framework they are not considered to meet the recognition requirements in terms of substance and

realisability, necessary for recognition as a regulatory asset and therefore regulatory capital.

There are no specific definitions for intangible assets (goodwill and other identifiable intangible assets)

in the prudential standards or the capital adequacy framework. Rather, the definition is based on the

terms defined by accounting concepts and standards. Capitalised expenses are not specifically covered

in the prudential standards or the capital adequacy framework and are generally risk weighted by ADIs

for the purposes of calculating capital adequacy. However as noted previously in this report some ADIs

deduct certain capitalised expenses from regulatory capital as a form of intangible asset.

Given the conceptual basis of the capital adequacy framework is biased towards excluding assets of

uncertain realisable value, it is arguable that a realisable measurement basis should be applied

consistently to all assets rather than selectively, such as happens with a fair value measurement

framework. The complexities and uncertainties associated with prescribing such a framework

consistently and accurately for all assets and liabilities is well documented and has to date prevented

both accounting standards makers and regulators from implementing this for financial reporting and

prudential reporting purposes. Importantly a fair value measurement framework may still not

necessarily align with the conceptual basis of the capital adequacy framework.

Page 20

4. Recommendations

APRA has been monitoring the growth in the recognition of capitalised expenses in the ADI industry

over the past few financial years and is concerned about the growth in value of these assets and the

degree of consistency of the accounting treatment across ADIs and the implications these represent for

the application of the capital adequacy framework. APRA’s concerns in this area are not allayed by the

impending adoption by Australia of international accounting standard IAS 39 ‘Financial Instrument:

Recognition and Measurement’. The accounting policy prescribed by this standard is that transaction

costs directly associated with the acquisition of financial assets and financial liabilities are to be

capitalised. This generates differences in the pattern and timing of expense recognition of these

capitalised transaction costs depending on which measurement basis is applied to the underlying

financial asset or liability.

Consistency was generally noted in the accounting policy and disclosure adopted by ADIs for the

recognition and classification of goodwill and identifiable intangible assets for both financial and

prudential reporting purposes. However, some key differences in classification were noted in relation

to capitalised expenses such as certain software development costs, securitisation establishment costs,

loan and lease origination broker fees, costs associated with debt / capital raisings and the nature of

other specific capitalised expenses. Most ADIs classified none of these capitalised expenses as

intangible assets for prudential reporting purposes, however some ADIs do. Accordingly APRA sees

this as further reason to clarify the definition of intangible assets for regulatory reporting purposes to

ensure the capital adequacy framework is consistently applied to all ADIs.

Within the accounting framework the capitalisation of expenses as assets and deferral of the expense

recognition over a period, which may span a number of financial years, may more appropriately

recognise or match the emergence of income and expense streams. However comparative to an

accounting policy that fully expenses these items when incurred the treatment improves the reported

financial performance and financial position of an ADI and as a result represents a favourable flow on

effect on stated capital adequacy. The main prudential concerns are:

Ø consistency in the application of the capital adequacy framework across ADIs; and

Ø like goodwill and identifiable intangible assets, certain types of capitalised expenses are not

considered to be available to protect depositors in an ADI failure scenario.

Page 21

APRA does not support, for capital adequacy purposes, an accounting policy allowing capitalisation of

certain types of expenses as assets. In light of this, APRA proposes that certain types of expenses that

are capitalised as assets, specifically those listed below (excluding those in the nature of prepayments)

are to be included in the definition of intangible assets for prudential purposes and deducted from Tier

1 capital in accordance with paragraph 9 of Prudential Standard APS 111‘Capital Adequacy:

Measurement of Capital’. APRA will implement changes to the appropriate prudential reporting

forms to separately capture the value of capitalised expenses and the composition of the value of

intangible assets deducted from Tier 1 capital.

This policy proposal for the treatment of capitalised expenses within the capital adequacy framework is

outlined individually below for each main type of capitalised expense concerned.

Loan and lease origination fees and commissions paid to mortgage originators and brokers

The accounting policy adopted by ADIs to capitalise the value of fees or commissions paid to loan

broker and originators in relation to loans and leases originated through those distribution channels , has

changed, or at least differentiated the pattern and timing of expense recognition between loans / leases

sourced through this distribution channel and loans / leases sourced through distribution channels such

as an ADI’s branch network. The expenses incurred with sourcing loans from mortgage originators are

being capitalised and the expense recognition deferred over a period of between 3 to 5 years on

average. Conversely the expense incurred in sourcing loans / leases through other channels such as the

ADI’s branch network is expensed fully when incurred as these predominantly comprise internal salary

and staff costs.

There are aspects of the accounting framework that require and justify this differential treatment. Also,

under a going concern basis of accounting, capitalising as an asset loan / lease origination fees and

deferring the expense recognition over a period more appropriately and accurately allows the matching

or emergence of the cost or return on the loan / lease portfolios to be reported. However, it is APRA’s

view that these capitalised expenses do not satisfy the recognition requirements for regulatory assets in

terms of substance and realisability under the objective and basis of the capital adequacy framework.

Accordingly APRA is proposing the following prudential treatment:

Permit loan / lease origination / broker fees and commissions that are capitalised as an

asset by an ADI to be set off against the balance of upfront loan / lease fees (this does not

extent to on-going account fees) associated with the lending portfolios that are deferred as

unearned income and recognised as a liability. The positive balance of net loan / lease

origination fees and commissions must be deducted from Tier 1 capital in accordance with

Page 22

Prudential Standard APS 111‘Capital Adequacy: Measurement of Capital’, paragraph 9. A

negative balance must not be added to Tier 1 capital.

This treatment will harmonise the application of the capital adequacy framework for all ADI

irrespective of the differing financial accounting policy adopted in relation to these type of expenses,

while also seeking to accommodate those ADIs that adopt the matching principle for the recognition

and deferral of both upfront loan / lease fee income and loan fee expense. This approach recognises the

potential inequity in requiring ADIs to deduct capitalised expenses whilst not recognising unearned

income associated with the lending portfolios.

Capitalisation of securitisation establishment costs; costs associated with debt / capital raisings and

other similar transaction related costs

For financial reporting purposes and for regulatory reporting purposes, some ADIs classify these items

as intangible assets where the majority do not. This results in differences in the treatment of these

assets in the calculation of regulatory capital.

It may be appropriate under a going concern basis of accounting for costs associated with establishing

securitisation schemes and debt / capital raisings to be recognised as an asset and the expense

recognition deferred and matched in line with the earning of economic benefit (e.g. for securitisation

schemes recoupment may be via management and servicing fees and / or spread accounts). However

under the capital adequacy framework APRA considers these costs do not satisfy the recognition

requirements for a regulatory asset and therefore regulatory capital and proposes the following

prudential treatment for these types of capitalised costs:

(i). The balance of securitisation establishment costs that are capitalised and deferred as an

asset by ADIs may be set off against the balance of unearned fee income relating to

securitisation schemes that is recognised and deferred as a liability by the ADI. Any

positive net balance of capitalised securitisation establishment costs is to be deducted

from Tier 1 capital in accordance with Prudential Standard APS 111‘Capital Adequacy:

Measurement of Capital’, paragraph 9. In accordance with AGN 120.3, any excess

unearned fee income over capitalised securitisation establishment costs must not be

added to Tier 1 capital.

(ii). Debt / capital raisings and all similar direct transaction related costs that are capitalised

as an asset by ADIs must be deducted from Tier 1 capital in accordance with Prudential

Standard APS 111‘Capital Adequacy: Measurement of Capital’, paragraph 9.

Page 23

The above recommended prudential treatment aims to harmonise the capital adequacy treatment for all

ADIs irrespective of the differing accounting policy adopted, or that prescribed by the accounting

standards.

Guidance note AGN 120.3 “Purchase and Supply of Assets (including Securities Issued by SPVs)”

precludes the recognition of the future revenue stream of fees from the regulatory capital base until

actually received (i.e. it prescribes a cash basis of accounting), however APRA considers that it is

reasonable that prospective fees which have been recognised for financial accounting purposes and

which are excluded from regulatory capital, should be offset against costs associated with the

establishment of securitisation schemes.

Specific item deduction

APRA has reservations from a financial and a prudential reporting perspective about specific costs that

have been capitalised and recognised as assets by ADIs and consider these items should be

appropriately classified as intangible assets for the purposes of determining the eligible prudential

capital base. Some of capitalised expenses concerned are the inclusion of training costs capitalised as

software development costs, cost of staff uniforms, transition and transformation costs and strategic

business development initiatives.

Software Development Costs

Software development costs can be justified for capitalisation and recognition as an asset for financial

accounting purposes as they are integral to the operation of the ADI as a going business concern, and

therefore a necessary component in future income production and investment. However under the

capital adequacy framework APRA considers it is questionable whether these costs satisfy the

recognition requirements for a regulatory asset and therefore regulatory capital.

In reviewing the appropriate treatment for software development costs for capital adequacy purposes

APRA considered the following alternatives:

1. Mandating deduction from regulatory capital of specific items of expenses capitalised as software

development costs (eg salary and staffing costs); or

2. No deduction from regulatory capital of specific items of expenses capitalised as software

development costs, but mandate a short amortisation period; or

Page 24

3. Full deduction of all software development costs from regulatory capital; or

4. Classification of capitalised software development costs into stages of completion (i.e.

‘Feasibility’, ‘Development’ and ‘In Use’). Deduction of ‘Feasibility’ and ‘Development’ stage of

software coupled with 100% asset risk weighting of ‘In Use’ stage; or

5. Costs associated with the ‘Feasibility’ stage and the ‘In Use’ stage are to be expensed when

incurred and only the costs associated with the ‘Development’ stage are to be capitalised. This is

the approach adopted by the Office of Comptroller of Currency (OCC) in the United States in

relation to costs associated with the development of software for internal bank use.

After considering the alternatives, the preferred approach is for the deduction of capitalised software

development costs that relate to the feasibility and application development stages from Tier 1 capital

in accordance with Prudential Standard APS 111 ‘Capital Adequacy: Measurement of Capital’

paragraph 9. Amortised costs associated with the operational or in use stage should be risk weighted at

100%. This approach is preferred amongst the alternatives as costs pertaining to the operational or in

use stage is more likely to have an identifiable realisable value and the contribution to future economic

benefits more likely to be measurable, compared to the other 2 stages where this is likely to be

inherently more blurred.

However the staged basis for deduction potentially introduces the following important prudential

implications:

Ø a regulatory bias into a commercial decision between ‘in-house’ software development compared to

outsourced software development (although this is not necessarily an undesirable outcome from a

prudential perspective due to the different risks inherent in the 2 alternatives); and

Ø a regulatory disincentive to develop and maintain robust information and risk management systems,

which is a key prudential focus for APRA and ADIs.

As a result of these important considerations, the stage based approach is not being proposed for

introduction at this stage and the existing prudential treatment of software development costs (i.e. 100%

risk weighting) will remain. Software development costs recognised by ADIs will be subject to further

monitoring and prudential consideration by APRA.

Page 25

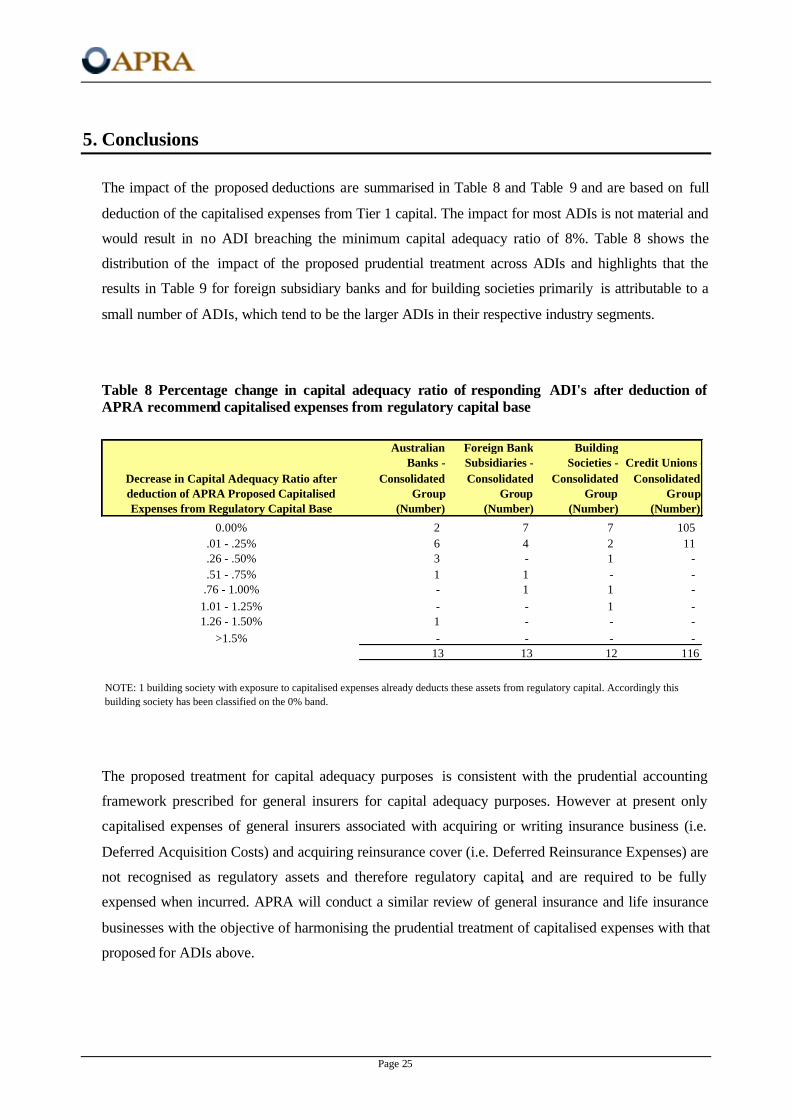

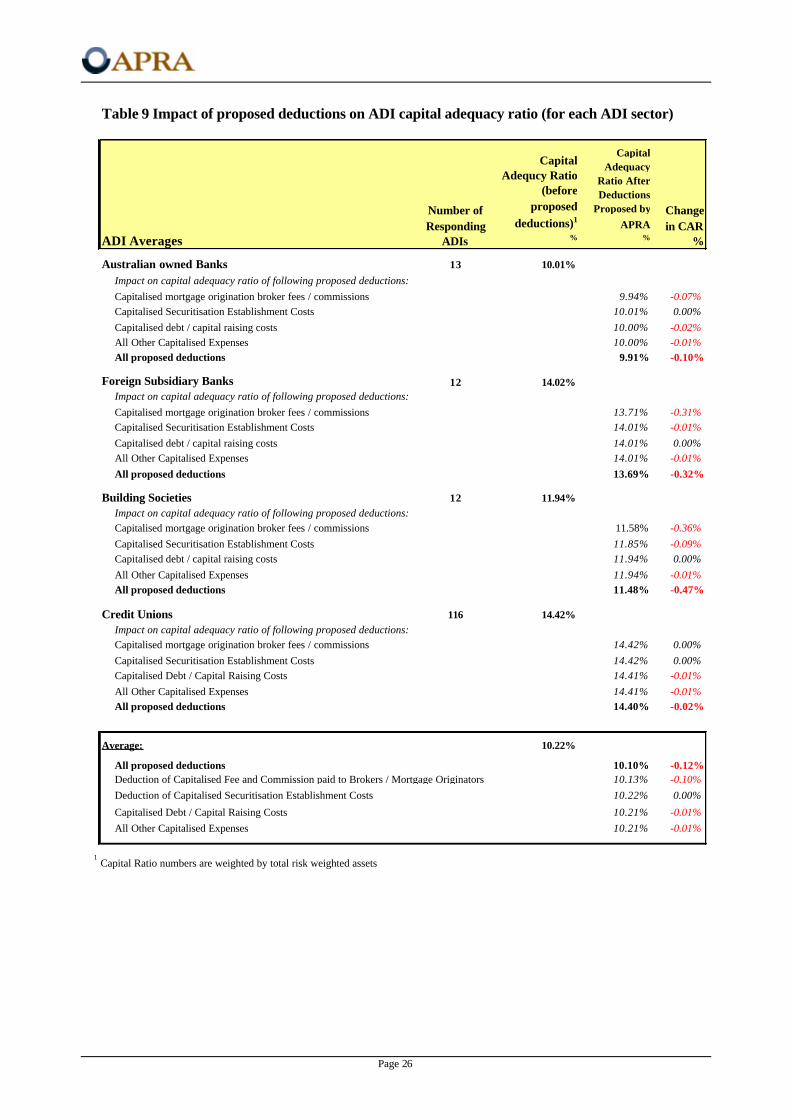

5. Conclusions

The impact of the proposed deductions are summarised in Table 8 and Table 9 and are based on full

deduction of the capitalised expenses from Tier 1 capital. The impact for most ADIs is not material and

would result in no ADI breaching the minimum capital adequacy ratio of 8%. Table 8 shows the

distribution of the impact of the proposed prudential treatment across ADIs and highlights that the

results in Table 9 for foreign subsidiary banks and for building societies primarily is attributable to a

small number of ADIs, which tend to be the larger ADIs in their respective industry segments.

Table 8 Percentage change in capital adequacy ratio of responding ADI's after deduction of APRA recommend capitalised expenses from regulatory capital base

Decrease in Capital Adequacy Ratio after deduction of APRA Proposed Capitalised Expenses from Regulatory Capital Base

Australian Banks -

Consolidated Group

(Number)

Foreign Bank Subsidiaries -Consolidated

Group(Number)

Building Societies -

Consolidated Group

(Number)

Credit Unions - Consolidated

Group(Number)

0.00% 2 7 7 105 .01 - .25% 6 4 2 11 .26 - .50% 3 - 1 - .51 - .75% 1 1 - -

.76 - 1.00% - 1 1 - 1.01 - 1.25% - - 1 - 1.26 - 1.50% 1 - - -

>1.5% - - - - 13 13 12 116

NOTE: 1 building society with exposure to capitalised expenses already deducts these assets from regulatory capital. Accordingly this building society has been classified on the 0% band.

The proposed treatment for capital adequacy purposes is consistent with the prudential accounting

framework prescribed for general insurers for capital adequacy purposes. However at present only

capitalised expenses of general insurers associated with acquiring or writing insurance business (i.e.

Deferred Acquisition Costs) and acquiring reinsurance cover (i.e. Deferred Reinsurance Expenses) are

not recognised as regulatory assets and therefore regulatory capital, and are required to be fully

expensed when incurred. APRA will conduct a similar review of general insurance and life insurance

businesses with the objective of harmonising the prudential treatment of capitalised expenses with that

proposed for ADIs above.

Page 26

Table 9 Impact of proposed deductions on ADI capital adequacy ratio (for each ADI sector)

ADI Averages

Number of Responding

ADIs

Capital Adequcy Ratio

(before proposed

deductions)1

%

Capital Adequacy

Ratio After Deductions

Proposed by APRA

%

Change in CAR

%

Australian owned Banks 13 10.01%Impact on capital adequacy ratio of following proposed deductions:Capitalised mortgage origination broker fees / commissions 9.94% -0.07%Capitalised Securitisation Establishment Costs 10.01% 0.00%Capitalised debt / capital raising costs 10.00% -0.02%All Other Capitalised Expenses 10.00% -0.01%All proposed deductions 9.91% -0.10%

Foreign Subsidiary Banks 12 14.02%Impact on capital adequacy ratio of following proposed deductions:Capitalised mortgage origination broker fees / commissions 13.71% -0.31%Capitalised Securitisation Establishment Costs 14.01% -0.01%Capitalised debt / capital raising costs 14.01% 0.00%All Other Capitalised Expenses 14.01% -0.01%All proposed deductions 13.69% -0.32%

Building Societies 12 11.94%Impact on capital adequacy ratio of following proposed deductions:Capitalised mortgage origination broker fees / commissions 11.58% -0.36%Capitalised Securitisation Establishment Costs 11.85% -0.09%Capitalised debt / capital raising costs 11.94% 0.00%All Other Capitalised Expenses 11.94% -0.01%All proposed deductions 11.48% -0.47%

Credit Unions 116 14.42%Impact on capital adequacy ratio of following proposed deductions:Capitalised mortgage origination broker fees / commissions 14.42% 0.00%Capitalised Securitisation Establishment Costs 14.42% 0.00%Capitalised Debt / Capital Raising Costs 14.41% -0.01%All Other Capitalised Expenses 14.41% -0.01%All proposed deductions 14.40% -0.02%

Average: 10.22%

All proposed deductions 10.10% -0.12%Deduction of Capitalised Fee and Commission paid to Brokers / Mortgage Originators 10.13% -0.10%Deduction of Capitalised Securitisation Establishment Costs 10.22% 0.00%

Capitalised Debt / Capital Raising Costs 10.21% -0.01%All Other Capitalised Expenses 10.21% -0.01%

1 Capital Ratio numbers are weighted by total risk weighted assets

Page 27

6. Consultation and application

APRA proposes that ADIs are required to convert to the new prudential treatment for quarterly

prudential reporting periods commencing form 1 July 2004.

APRA encourages ADIs and other interested parties to provide written submissions and feedback on

the proposals during the consultation period, which closes 30 September 2003. Submissions are to be

addressed to Lyndon Kingston GPO Box 9836, Sydney NSW 2001, or email