Download - PREDICTIVE MODELS IN LIFE INSURANCE

6/5/2010

Munich Re

1

PREDICTIVE MODELS IN LIFE

INSURANCE

Philip L. Adams, ASA, MAAA

Date: 17 June 2010

Agenda

1. Predictive Models Defined

2. Predictive models past and present

3. Actuarial perspective

4. Application to Life Insurance: ILEC 02-04 and 05-07 data

6/5/2010

Munich Re

2

PREDICTIVE MODELS

WHAT THEY ARE (AND AREN’T)

05/06/2010Title of presentation and name of speaker3

What is predictive modeling?

“Predictive modeling is the use of modern statistical methods to identify and

measure past associations for the sake of inferring associations about the past, the

present and the future. Usually, this is expressed through probabilities, and it has a

very strong Bayesian flavor.”

-Your humble speaker

This sounds a lot like what actuaries have been doing for a century (except for the

“modern statistical methods” part).

6/5/2010

Munich Re

3

What it’s not

05/06/2010 5

Panacea Best thing since sliced

bread

The tool to end all tools

Nuts and Bolts of Predictive Modeling

Data mining: Use statistical methods to find patterns

“Correlation does not imply causation”

…but we often have to assert causation

Some associations cannot be measured using correlation

Correlation is measure of statistical collinearity

Correlation implies dependency, but not conversely

Example: If X is uniform on (-1,1), then X2 is uncorrelated with X

Take action with those patterns

Build a better product or service

Incorporate into risk management

05/06/2010 6

6/5/2010

Munich Re

4

PREDICTIVE MODELS

PAST AND PRESENT

05/06/20107Title of presentation and name of speaker

PREDICTIVE MODELS: The PastHoroscopes

6/5/2010

Munich Re

5

PREDICTIVE MODELS: In FictionThe Witch in Monty Python’s Holy Grail

05/06/2010Title of presentation and name of speaker 9

“Experience” taught

knight that witches

float, so compare

candidate to other

things that float

Peasants’ suggested

comparisons: wood,

very small rocks,

churches, water fowl

Analogous to a

decision tree

PREDICTIVE MODELS: Real Data, Bad AnalysisPirates and Global Warming

05/06/2010Title of presentation and name of speaker 10

Number of

pirates has

decreased since

1860

Globe has

consistently

warmed

Ergo, Somalia is

at the forefront

of the fight

against global

warming

6/5/2010

Munich Re

6

PREDICTIVE MODELS: Dubious conclusions

05/06/2010 11Title of presentation and name of speaker

More pirates!

PREDICTIVE MODELS: The Present

05/06/2010Title of presentation and name of speaker 12

Mortality tables

Lapse tables

Trends

Credit scoring

Underwriting manuals

UCS

Fraud detection

6/5/2010

Munich Re

7

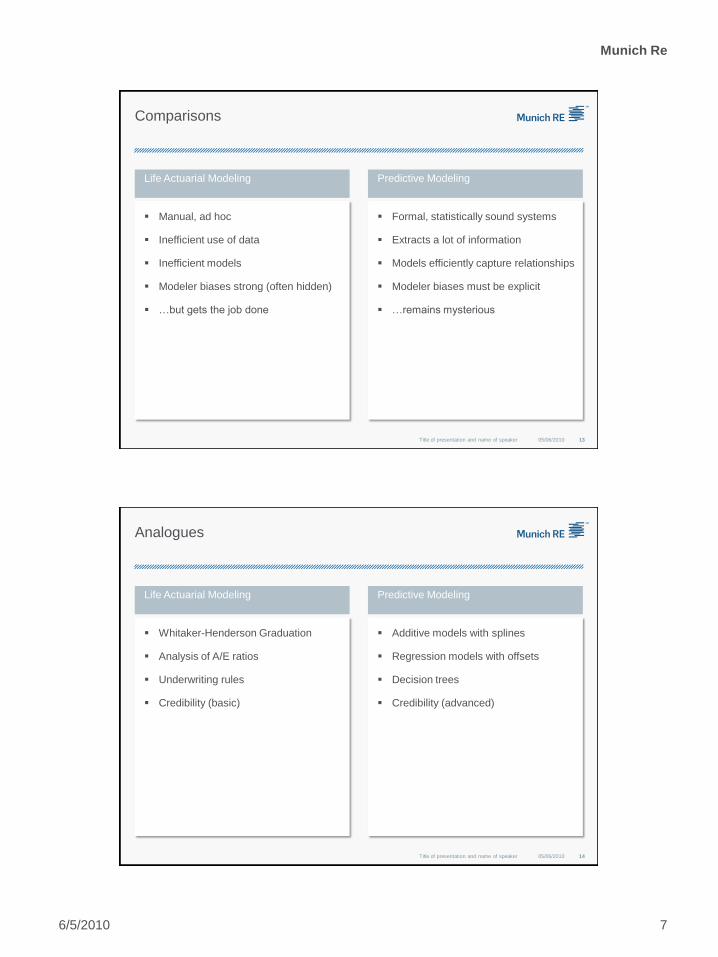

Manual, ad hoc

Inefficient use of data

Inefficient models

Modeler biases strong (often hidden)

…but gets the job done

Formal, statistically sound systems

Extracts a lot of information

Models efficiently capture relationships

Modeler biases must be explicit

…remains mysterious

05/06/2010Title of presentation and name of speaker 13

Comparisons

Life Actuarial Modeling Predictive Modeling

Whitaker-Henderson Graduation

Analysis of A/E ratios

Underwriting rules

Credibility (basic)

Additive models with splines

Regression models with offsets

Decision trees

Credibility (advanced)

05/06/2010Title of presentation and name of speaker 14

Analogues

Life Actuarial Modeling Predictive Modeling

6/5/2010

Munich Re

8

APPLICATIONS TO LIFE INSURANCE

05/06/2010Title of presentation and name of speaker15

Modeling the ILEC 02-04 Data

• Death claims and exposures on fully underwritten lives from 35 companies

collected between 2002 and 2004

• Nearly 700,000 claims overall

• Almost 500,000 in durations 21+

• For this presentation, we confine our attention to a particular subset

• Attained ages 20-84, durations 1-10

• Face amounts at least $10,000 and summarized into two bands

• Left with 37,087 death claims

• We anchor to PPR ultimate model from Edwalds, Craighead, Adams paper

6/5/2010

Munich Re

9

Modeling the ILEC 02-04 Data

Modeling the ILEC 02-04 Data

6/5/2010

Munich Re

10

Modeling the ILEC 02-04 Data

Modeling the ILEC 02-04 Data

6/5/2010

Munich Re

11

Modeling the ILEC 02-04 Data

Modeling with GAMs

05/06/2010 22Title of presentation and name of speaker

Linear Model

• Standard regression model using least squares minimization of some response against some collection of predictor variables

Generalized Linear Model

• Expand universe of response variables to probabilities, counts, etc.

Generalized Additive Model

• Expand universe of predictors to include smooth functions

xy 10

xyg 10

xfyg 0

6/5/2010

Munich Re

12

Modeling with GAMs

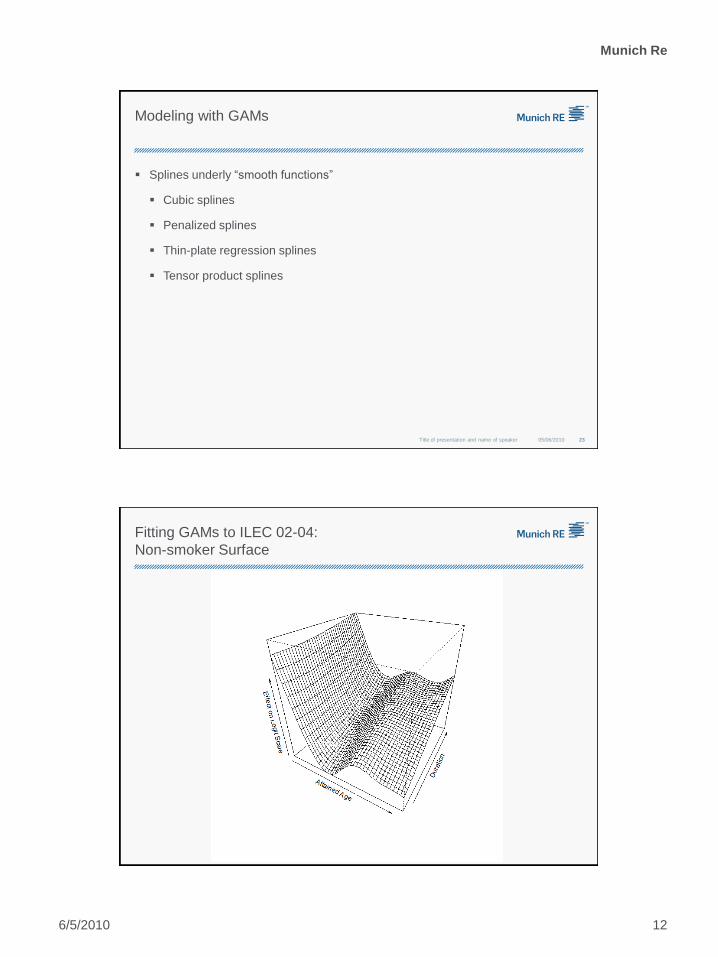

Splines underly “smooth functions”

Cubic splines

Penalized splines

Thin-plate regression splines

Tensor product splines

05/06/2010 23Title of presentation and name of speaker

Fitting GAMs to ILEC 02-04:

Non-smoker Surface

6/5/2010

Munich Re

13

Fitting GAMs to ILEC 02-04:

Smoker Surface

Fitting GAMs to ILEC 02-04:

Model Parameters

Parameters (offset from ultimate) Estimate Std. Error p-value e.d.f.

Fixed

Intercept -0.317 0.062 0.00% 1

Males -0.059 0.012 0.00% 1

Face Amounts $50,000+ -0.399 0.012 0.00% 1

Non-smokers -0.298 0.062 0.00% 1

Smokers 0.488 0.065 0.00% 1

Non-smokers in Duration 1 -0.823 0.078 0.00% 1

Non-smokers in Duration 2 -0.199 0.039 0.00% 1

Smokers in Duration 1 0.000 1

Smokers in Duration 2 -0.173 0.055 0.16% 1

SmoothNon-smokers 63 parameters 0.00% 18.06

Smokers 63 parameters 0.00% 9.81

6/5/2010

Munich Re

14

Fitting GAMs to ILEC 02-04:

Smoker Penalty

But can it predict?

Attach to ILEC 05-07 Dataset

Confined to data similar to fitting set

Data summarized, so judgment used for choice of age and duration

Table projected forward to 2008 using 1% per annum flat

Compare to 2008 VBT

Represents actuarial approach

05/06/2010 28Title of presentation and name of speaker

6/5/2010

Munich Re

15

2008 VBT and GAM ComparedGender and Smoker Status

A/E by Count A/E by Amount

Claims 08VBT Primary Predictive Model 08VBT Primary Predictive Model

Female 11,402 110.1% 112.8% 95.4% 105.9%

Non-Smoker 8,812 108.8% 110.1% 95.9% 105.3%

Smoker 2,590 115.1% 123.1% 92.4% 109.9%

Male 20,654 107.8% 106.6% 87.1% 88.2%

Non-Smoker 15,663 106.3% 105.0% 86.4% 86.9%

Smoker 4,991 113.1% 112.0% 92.1% 96.7%

Overall 32,056 108.7% 108.7% 89.2% 92.3%

05/06/2010 29Title of presentation and name of speaker

Bottom line results are comparable.

2008 VBT and GAM ComparedFace Amount Band

05/06/2010 30Title of presentation and name of speaker

A/E by Count A/E by Amount

Claims 08VBT Primary Predictive Model 08VBT Primary Predictive Model

10,000-24,999 4,062 150.7% 121.8% 149.7% 120.5%

25,000-49,999 4,212 135.5% 106.6% 134.9% 106.2%

50,000-99,999 5,531 121.4% 136.6% 120.7% 135.9%

100,000+ 18,251 95.3% 100.6% 87.0% 90.3%

Overall 32,056 108.7% 108.7% 89.2% 92.3%

GAM has better control for face amount variation.

6/5/2010

Munich Re

16

2008 VBT and GAM ComparedAttained Age Slope

05/06/2010 31Title of presentation and name of speaker

2008 VBT and GAM ComparedDuration Slope

05/06/2010 32Title of presentation and name of speaker

6/5/2010

Munich Re

17

References

Edwalds, T., Craighead, S., Adams, P. (2008) “Estimating Mortality Risk Using

Predictive Modeling.” Enterprise Risk Management Symposium.

Lowrie, Walter B. (1982) “An Extension of the Whittaker-Henderson Method of

Graduation,” Transactions of the Society of Actuaries, Vol. 34, pp. 329-372

R Development Core Team (2009). R: A Language and environment for

statistical computing. Vienna, Austria. R Foundation for Statistical Computing

Wood, S. (2006) Generalized Additive Models: An Introduction with R. Chapman

& Hall, London.

Image Credits

• Wikimedia Commons

• Monty Python

• Veganza.com

• Wenger

• CDC

05/06/2010 34Title of presentation and name of speaker