Problem Set 3

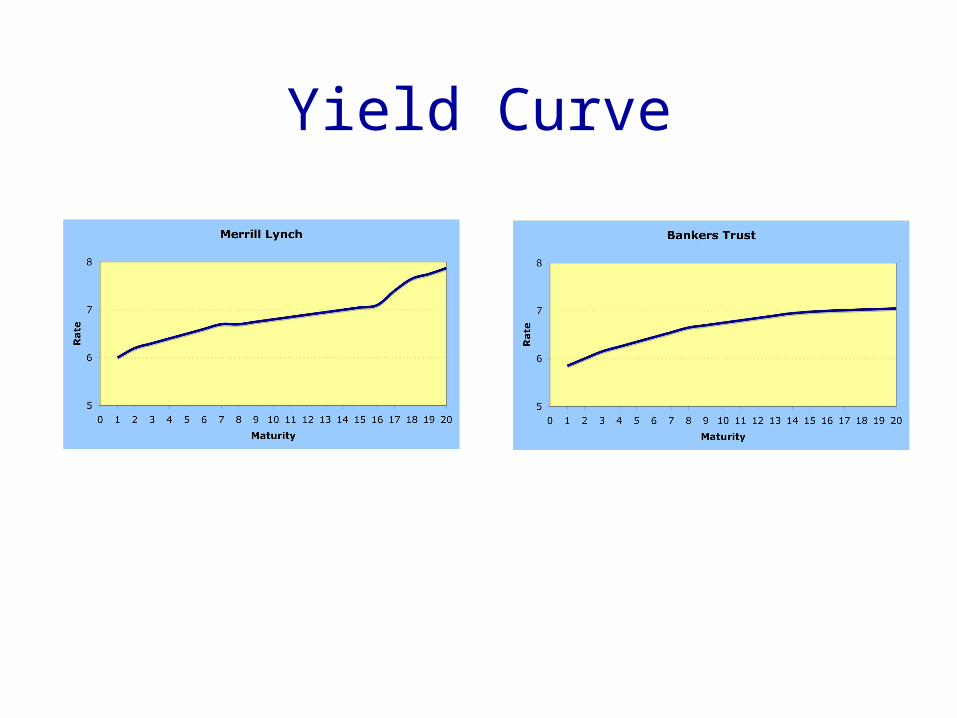

Understanding the Yield Curve

Disney Case

¥ Debt Support

2 2

€ Debt Support

¥ Debt Support

€ Debt Support

1 1

¥ Principal

€ Principal€ Principal

¥ Principal

Variation on a currency swap

Step 1 is notionalStep 2 is net

Borrow in Europe against income from Tokyo Disney

Dis

ney

IBJ Borrow in

Japan, invest in Europe

Fre

nch

Uti

lity

Currency Swap

German rate x €1,000,000

€ 1,000,000

2 2

U.S. rate x $1,500,000

German rate x €1,000,000

U.S. rate x $1,500,000

1 1

€ 1,000,000

$1,500,000$1,500,000

€ 1,000,000

3 3

$1,500,000

€ 1,000,000

$1,500,000

Illustration of a straight currency swap

Step 1 is notionalSteps 2 & 3 are net

Borrow in US, invest in Europe

Borrow in Europe, invest in US

Problem 40

Two-year bondR = 6.5%P/YR = 1N = 2Let’s say PV = $10,000Then FV = $11,342.25

Rollover StrategyStart with $10,0001st year add 6%

$10,600

2nd year add 7.5%$11,3952-year average return is 6.75%

Expected return is higher with rollover strategy

What risks are involved?

Problem 41

Two-year bondR = 7%P/YR = 1N = 2Let’s say PV = $10,000Then FV = $11,449.00

Rollover StrategyStart with $10,0001st year add 6%

$10,600

2nd year add 7.5%$11,3952-year average return is 6.75%

Expected return is higher with two-year bond

What pressures would result?Given the expectations, equilibrium 2-year rate would be

6.75% (Problem 42)

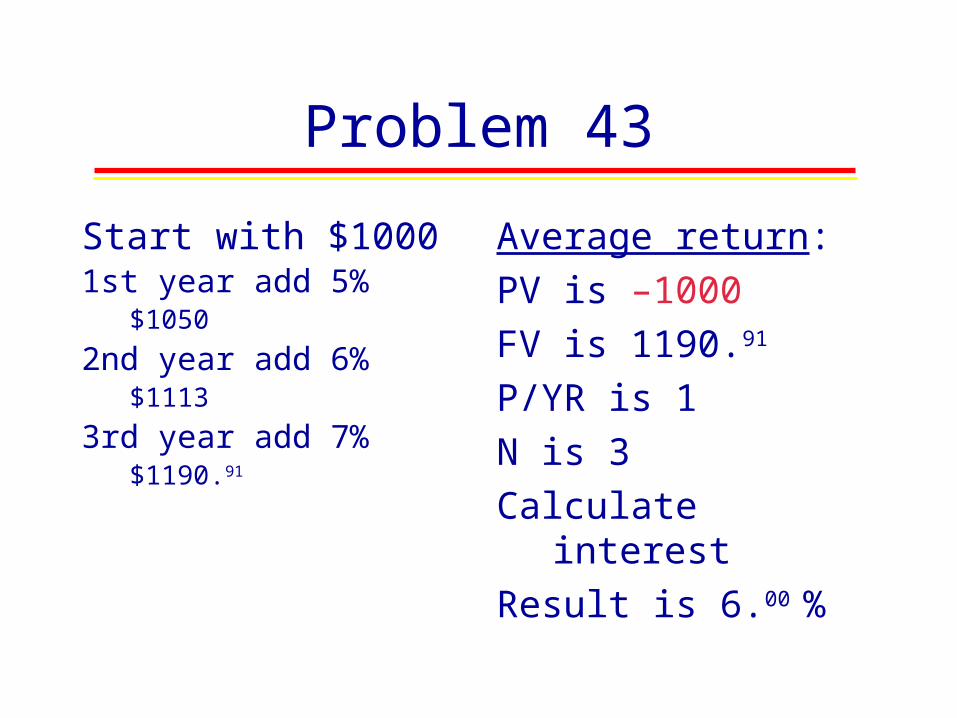

Problem 43

Start with $10001st year add 5%

$1050

2nd year add 6%$1113

3rd year add 7%$1190.91

Average return:

PV is –1000

FV is 1190.91

P/YR is 1

N is 3

Calculate interest

Result is 6.00 %

Problem 44

Start with $1,000,0001st year add 6%

$1,060,000

2nd year add 6.5%$1,128,900

3rd year add 7%$1,207,923

4th year add 8%$1,304,556.84

Average return:

PV is –1,000,000

FV is 1,304,556.84

P/YR is 1

N is 4

Calculate interest

Result is 6.8724 %

Expectations Theory

• We’ve just had some practice building up the yield curve according to the expectations theory

• Now, let’s do some arbitrage!

Problem 45

• Moving from 0% coupon to 6% couponAdds extra income of $6 per yearAdds $38.28 to price ($75.08 minus $36.80)

• Moving from 6% coupon to 8% couponAdds extra income of $2 per yearAdds $3.92 to price ($79 compared with $75.08)

Therefore an extra $6 per year should cost three times as much, $11.76

• The 0% bond is a bargain!

Problem 45

0 1 2 19 20

Sell $300.32 $12 $12 $412$12

Buy $12$237.00 $12 $312$12

NPV is clearly positive

Net $26.52 0 0 00

Buy 0$36.80 0 $1000

Problem 45

Yield

Risk (Convexity)

11.60%10.24%

10.00%

Coupon Stripping

• 6% coupon (2 pmts/yr)

• 10 years to maturity• Price: $76.71

• 8% coupon (2 pmts/yr)

• 10 years to maturity• Price: $89.72

Let’s combine these components into a zero-coupon bond

• Buy four of the 6%• Sell three of the 8%• Net: $100 in 10 years

• Pay $306.84

• Receive $269.16

• Net Payment: $37.68

Implied interest is 10% APR (2 P/YR)

Coupon Stripping

Buy

Sell

0 1 2

$306.84 $12

$12

$12 $412

$269.16 $12

19 20

$312

$12

$12

Implied interest is 10% APR (2 P/YR)

Net $37.68 0 0 $1000

Coupon Stripping

• Stripped zeroes of different maturities can be used to construct the yield curve

• Better than using duration

Problem 46

• Moving from 6% coupon to 8% couponAdds extra income of $2 per year

Adds $9 to price ($76 compared with $67)

• Moving from 8% coupon to 10% couponAlso adds extra income of $2 per year

But, adds $12 to price ($88 compared with $76)

• Therefore, the 10% bond is over-priced (compared with the 8% bond)

Problem 46

0 1 2 19 20

Buy $152.00 $8 $8 $208$8

Sell $3$67.00 $3 $103$3

NPV is clearly positive

Net $3.00 0 0 00

Sell $5$88.00 $5 $105$5

Problem 46

Yield

12.10%11.68%

12.22%

Risk (Convexity)

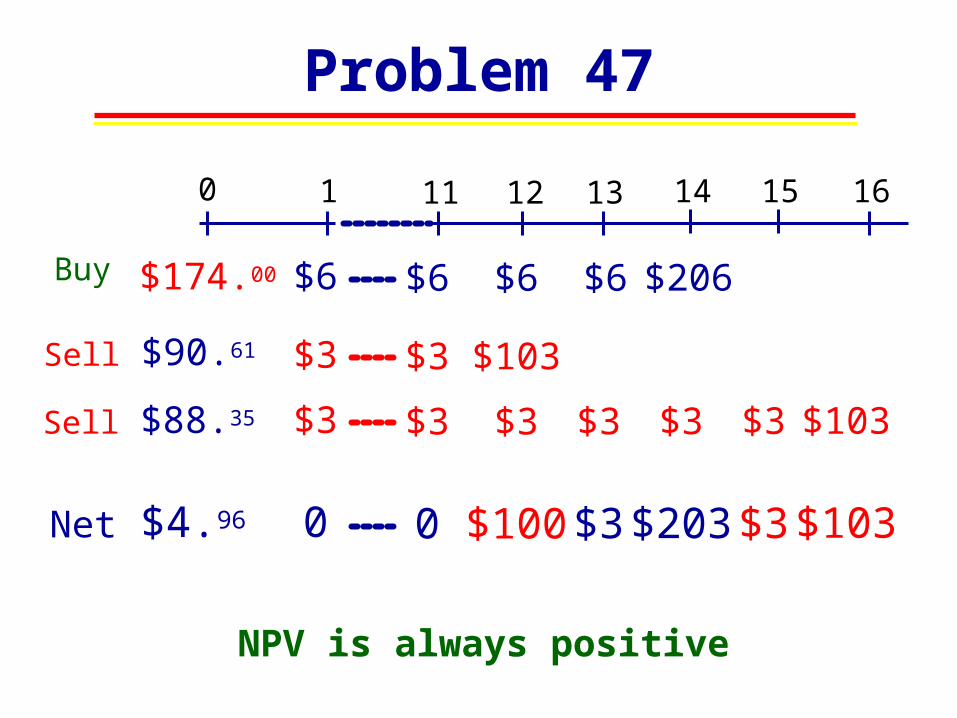

Problem 47

Yield

8%8%

8.5%

Risk (Convexity)

Problem 47

NPV is always positive

0 1 14 161211 13 15

Buy $174.00 $6 $6 $206$6 $6

Sell $90.61 $3 $3 $103

Sell $88.35 $3 $3 $3 $3 $3 $3 $103

Net $4.96 0 0 $100 $3 $203 $3 $103

Problem 48

Yield

8.50%8.38%

8.00%

Risk (Convexity)

Problem 48

NPV is always positive

0 1 14 161211 13 15

Sell $178.88 $6 $6 $206$6 $6

Buy $88.44 $3 $3 $103

Buy $86.35 $3 $3 $3 $3 $3 $3 $103

Net $4.09 0 0 $100 $3 $203 $3 $103

Problem 49

Yield

8% 8%

8.5%

Risk (Convexity)

Problem 49

NPV is always positive

0 1 14 161211 13 15

Sell $178.88 $6 $6 $206$6 $6

Buy $90.61 $3 $3 $103

Buy $85.70 $3 $3 $3 $3 $3 $3 $103

Net $2.57 0 0 $100 $3 $203 $3 $103

Problem 50

Yield

8% 7.75%

7%

Risk (Convexity)

Problem 50

NPV is always positive

0 1 14 161211 13 15

Buy $181.36 $6 $6 $206$6 $6

Sell $90.61 $3 $3 $103

Sell $93.95 $3 $3 $3 $3 $3 $3 $103

Net $3.20 0 0 $100 $3 $203 $3 $103

Problem 51

$170.96 £84.63

$200

Profit = £0.77

NYtoday

$1.00 = £ 0.495

$1.00 = £ 0.50

LONtoday

LONlater

$200 NYlater

What is not balanced?

Price £83.86Face £100

Price $85.48Future $100

£100

£83.86

Problem 52

€8,885 $12,439.00

€10,000

Profit = $899.20

FRAtoday

€1.00 = $1.40

€1.00 = $1.35

NYtoday

NYlater

€10,000 FRAlater

What is not balanced?

Price $85.48Face $100

Price €88.85Future €100

$13,500

$11,539.80

JunkCo Arbitrage

Fixed

If net is positive, underwriter pays party. If net is negative, party pays underwriter.

Illustration of a Floating/Fixed Swap

Party Underwriter CounterpartyVariable

Fixed

Variable

JunkCo Arbitrage

11% Fixed

Net for AAA Corp:•During 1st year, borrows at T-Note rate•During remaining time, net flow is zero•This is better than AAA could do by itself

JunkCo Underwriter AAA CorpT-Bill

11% Fixed

T-Bill

Lender

T + 3%

Lender

11% Fixed

T-Bill

SinkingFund

After 1st year

Net for JunkCo:•Net is 14% fixed•This is better than JunkCo could do by itself

Net for Underwriter:•Net flows are zero•Gains fees, future opportunities, & goodwill

JunkCo Arbitrage

How is this possible?Answer: Quality gap is inconsistent

Maturity

Rat

e

Yield Curves

AAA

JunkQuality Gap

Myron Labs Arbitrage

8% Fixed, £ Principal

1 1

BT, £ Principal

8% Fixed, $ Principal

BT, $ Principal 1st yr£ Principal after 1st yr

After 1st year£1,000,000

$2,000,000

Variation on a currency swap

Myr

on L

abs

Inte

rmed

iary

Ad

van

ced

Dev

ices

Lender

8% Fixed

BT-Bill

SinkingFund, £

After 1st year

Lender

BT + 2%

Dynamic Hedge

Volatility

$2,000,000

£1,000,000

End of last year

BF Goodrich Rabobank

11% Fixed

Net for Rabobank:•During initial time, borrows at LIBOR – x•During remaining time, net flow is x•This is better than Rabo could do by itself

BFG Morgan RabobankLIBOR – x

11% Fixed

LIBOR – x

Lender

LIBOR + .50%

Lender

11% Fixed

LIBOR

SinkingFund

At refinancing

Net for Goodrich:•Net is fixed 11.5% + x•This is better than BFG could do by itself

Net for Underwriter:•Net flows are zero•Gains fees, future opportunities, & goodwill

IRRM Products

• Listed Products– Futures– Options

• Custom Products– Swaps– Caps– Floors– Collars

Caps

PremiumClient UnderwriterToday

*Payments are made periodically (say, monthly or quarterly) over the life of the contract, with rates appropriately adjusted for the number of periods per year

Illustration of a 7% Interest Rate Cap on LIBOR

Max[(LIBOR – 7%), 0]

UnderwriterLater* Client

Floors

PremiumClient UnderwriterToday

*Payments are made periodically (say, monthly or quarterly) over the life of the contract, with rates appropriately adjusted for the number of periods per year

Illustration of a 3% Interest Rate Floor on LIBOR

Max[(3% – LIBOR), 0]

UnderwriterLater* Client

Collars

PremiumClient UnderwriterToday

*Payments are made periodically (say, monthly or quarterly) over the life of the contract, with rates appropriately adjusted for the number of periods per year

Illustration of a 3,7 Collar on LIBOR

Max[(LIBOR – 7%), 0]+ Max[(3% – LIBOR), 0]

UnderwriterLater* Client

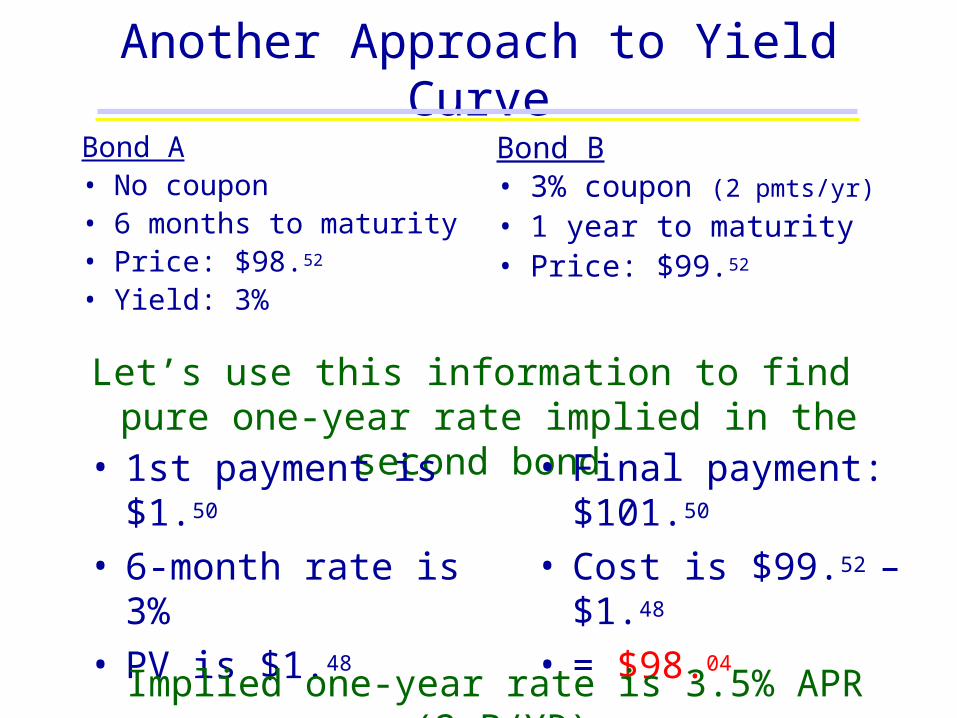

Another Approach to Yield Curve

Bond A• No coupon• 6 months to maturity• Price: $98.52

• Yield: 3%

Bond B• 3% coupon (2 pmts/yr)

• 1 year to maturity• Price: $99.52

Let’s use this information to find pure one-year rate implied in the second bond

• 1st payment is $1.50

• 6-month rate is 3%• PV is $1.48

• Final payment: $101.50

• Cost is $99.52 – $1.48 • = $98.04

Implied one-year rate is 3.5% APR (2 P/YR)

Finding the Yield Curve

Simplified:

0 1 2

Start: $99.52 $1.50 $101.50

Net: $98.04 0 101.50

Implied one-year rate is 3.5% APR (2 P/YR)

$1.48 $1.50

Another Approach to Yield Curve

Background data:• 6-month rate: 3%• 1-year rate: 3.5%

Bond C:• 3% coupon• 18 months to maturity• Price: $99.10

Let’s use this information to find pure 18-month rate implied in the second bond

• 1st pmt has PV $1.48

• 2nd pmt has PV $1.45

• Final payment: $101.50

• Cost is $99.10 – $1.48 – $1.45 = $96.17

Implied 18-month rate is 3.63% APR (2 P/YR)

Finding the Yield Curve

Simplified:

Implied 18-month rate is 3.63% APR (2 P/YR)

$1.48 $1.50

0 1 2 3

Start: $99.10 $1.50 $101.50$1.50

Net: $96.17 0 101.500

$1.45 $1.50

Another Approach to Yield Curve

Background data:• 6-month rate: 3%• 1-year rate: 3.5%• 18-month rate: 3.63%

Bond D:• 3% coupon• 2 years to maturity• Price: $98.67

Let’s use this information to find pure two-year rate implied in the second bond

• 1st pmt has PV $1.48

• 2nd pmt has PV $1.45

• 3rd pmt has PV $1.42

• Final payment: $101.50

• Cost is $98.67 – $1.48 – $1.45 – $1.42 = $94.32

Implied 2-year rate is 3.70% APR (2 P/YR)

Finding the Yield Curve

Simplified:

Implied 2-year rate is 3.70% APR (2 P/YR)

$1.48 $1.50

0 1 2 3

$1.45 $1.50

4

Start: $98.67 $1.50 $101.50$1.50 $1.50

Net: $94.32 0 101.500 0

$1.42 $1.50

Deriving Implied Forward Rates

Bond A• No coupon• 6 months to maturity• Price: $98.52

• Yield: 3%

Bond B• 3% coupon• 1 year to maturity• Price: $99.52 • Yield: 3.49%

Deriving Implied Forward Rates

NYtoday

$101.01

$101.50

$99.52

$1.50

Implied forward rate is 4% APR (2 P/YR)

3.00%NY

6 mos

4.00%

3.49%NY

1 year

Netreceipt$99.51

• Sell a one-year bond• Invest $99.52 for 6

months at 3%

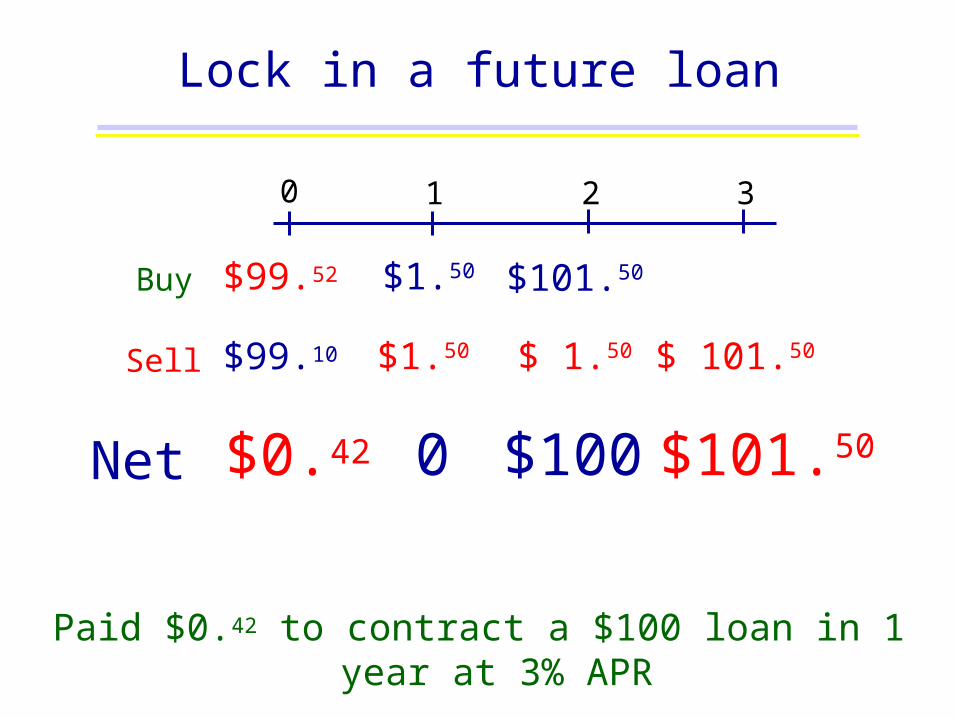

Lock in a future loan

Bond A:• 3% coupon• 1 year to maturity• Price: $99.52

Bond B:• 3% coupon• 18 months to maturity• Price: $99.10

Buy a one-year bond and sell an 18-month bond

Net payment $99.52 - $99.10 = $0.42

In 6 months:• Receive: $1.50

• Pay: $1.50

• Net zero

In 1 year:• Receive: $101.50

• Pay: $1.50 • Net $100

Paid $0.42 to contract a $100 loan in 1 year at 3% APR

In 18 months:• Pay: $101.50

Lock in a future loan

Buy $99.52 $1.50 $101.50

0 1 2 3

Net $0.42 0 $100 $101.50

Sell $1.50$99.10 $ 1.50 $ 101.50

Paid $0.42 to contract a $100 loan in 1 year at 3% APR

Nikkei Put Warrants

PENsS

CP

ER

S

BT

Cou

nte

rpar

ty

PE

FC

O

$5 mm

$5mm + Appreciation

1% Coupon Fixed Undisclosed Flow

AppreciationAppreciation

What happens to Tokyo Index?

Nikkei Put Warrants (Bringing innovation to retail)

Gol

dm

an S

ach

s

Opt

ion

Pre

miu

mA

t Beg

inni

ng

Cou

nte

rpar

ty

Flow

Dep

Dep

rici

atio

nA

t Mat

urityK

ingd

om o

f D

enm

ark

Pu

bli

c M

ark

et

Flow

Dep

Alternative PlanS

CP

ER

S

BT

PE

FC

O$5 mm

$5mm + App

1% Fixed

App

Flow

App

Gol

dm

an S

ach

s

PriceFlow

Dep DepKin

gdom

of

Den

mar

k

Pu

bli

c M

ark

et

Dynamic Hedge

Volatility

CitiCorp

MARKETING

Capital AdequacyCapital Adequacy

Will It Meet Competitive Requirements in a Virtual Space with Tomorrow’s Financial Services Dominators?

INNOVATION HUMANCAPITAL

Credit QualityCredit QualityLiquidityLiquidity

ENTERPRISERISK

MANAGEMENT

Bank of the FutureBank of the Future

Foundations & Structure

VISION(PLANNING

&STRATEGY)

COSTTRACKING& PRICING

Relationships & CapabilitiesRelationships & Capabilities

Cap

ital

Ad

equ

acy

Cap

ital

Ad

equ

acy

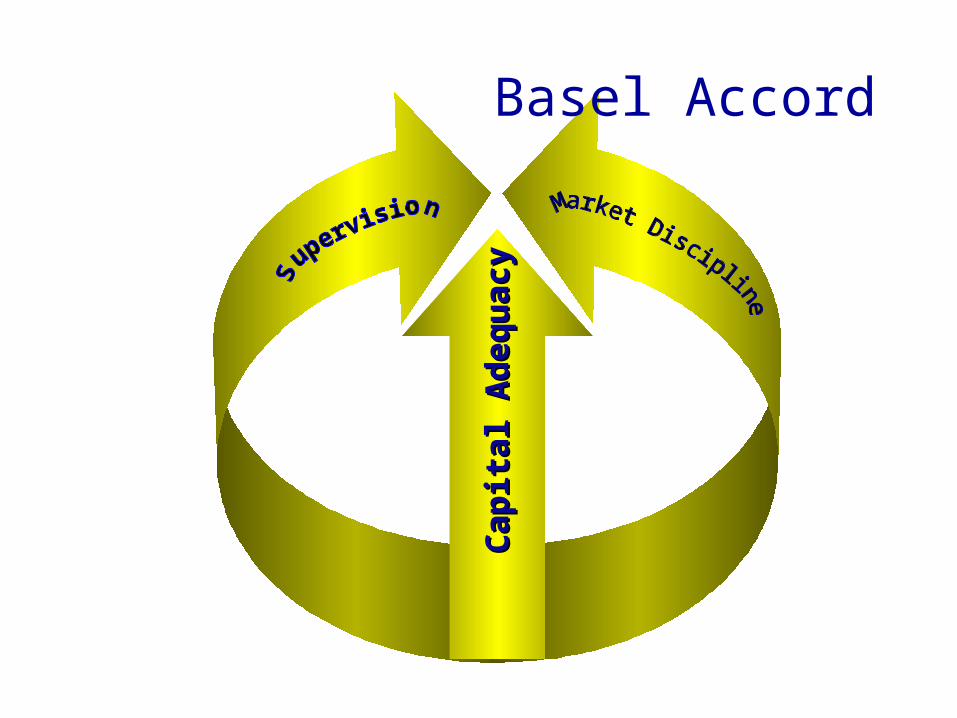

Basel Accord

Exhibit 9

Market Timing for Bonds

• The basic idea of market timing is to get into the market before it rises and get out before it falls– Translation:

• Long duration in advance of falling interest rates• Short duration in advance of rising interest rates

• Extreme market timing– Very long duration in advance of falling interest rates– Very long negative duration in advance of rising interest rates

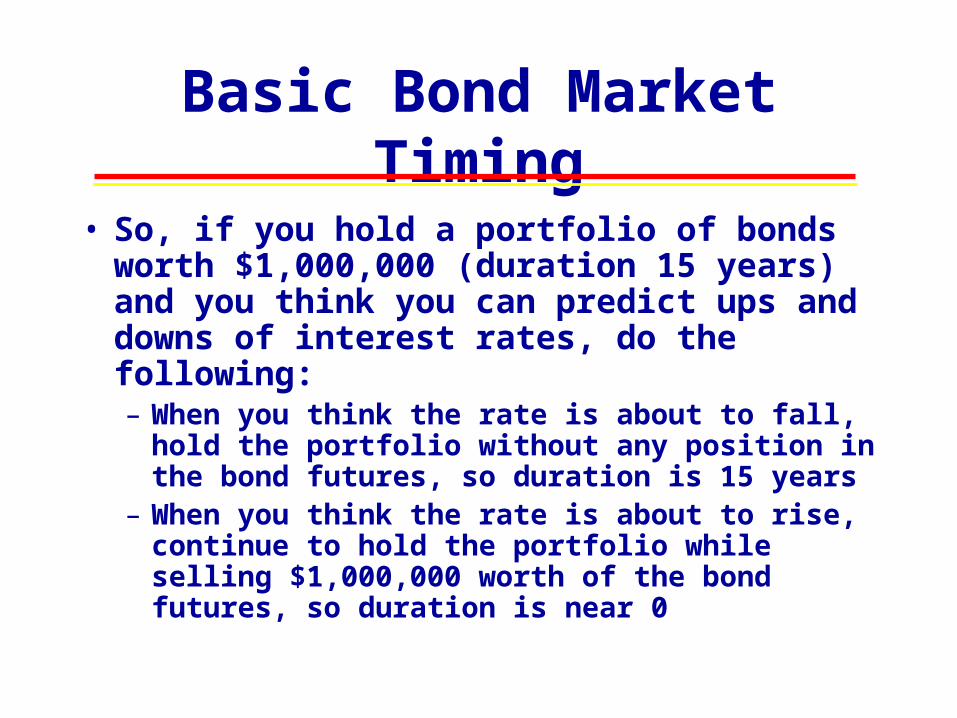

Basic Bond Market Timing

• So, if you hold a portfolio of bonds worth $1,000,000 (duration 15 years) and you think you can predict ups and downs of interest rates, do the following:– When you think the rate is about to fall, hold the

portfolio without any position in the bond futures, so duration is 15 years

– When you think the rate is about to rise, continue to hold the portfolio while selling $1,000,000 worth of the bond futures, so duration is near 0

Immunization

• Immunization might be appropriate for a bank with the following – Asset portfolio has average duration of 10 years– Liability portfolio has average duration of 1 year

• Immunization would use the same techniques as market timing strategies in order to– Shorten the duration of the asset portfolio– Adjust the duration of the liability portfolio so they

are both nearly the same

Connecticut Municipal Swap

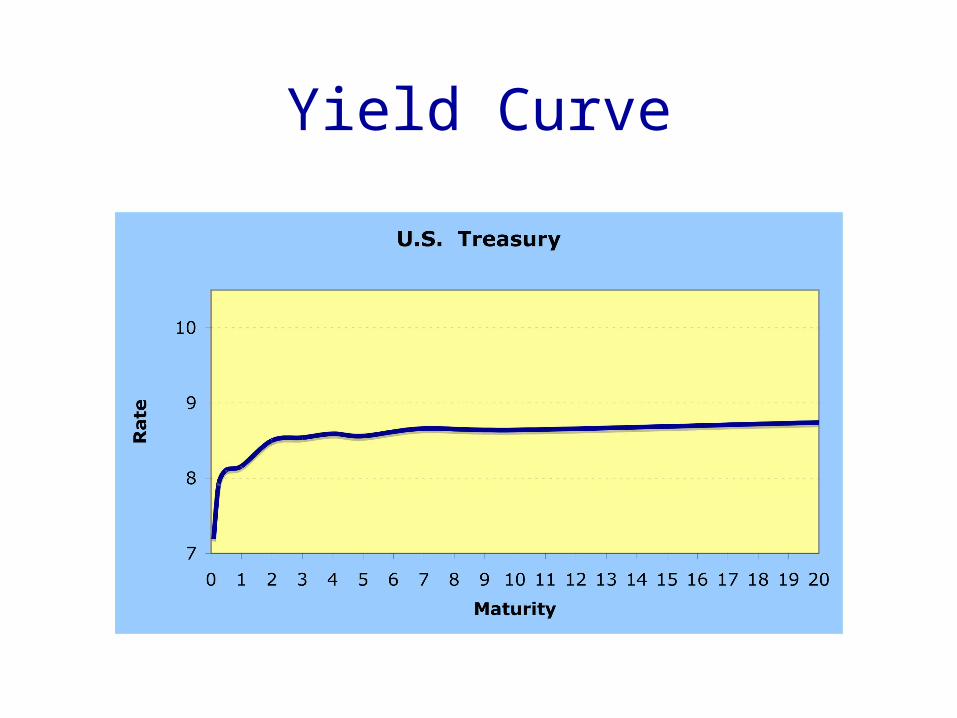

Yield Curve

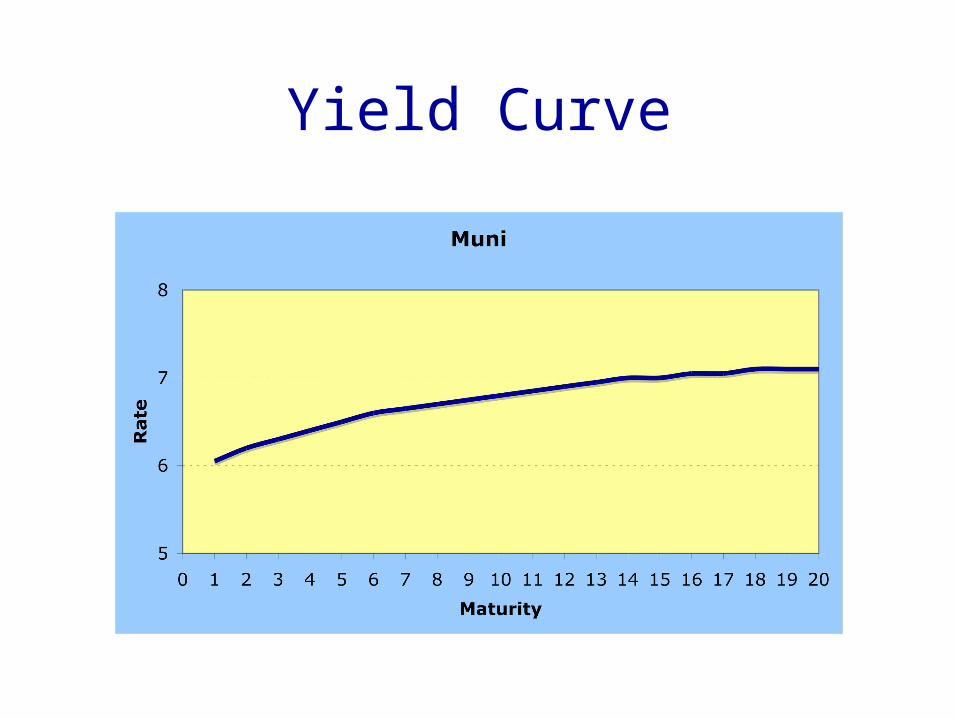

Yield Curve

Yield Curve

Advantage of Deductibility

Yield Curve

Exhibit 3

Exhibit 4

Exhibit 5

Exhibit 6