Download - Rakesh Presi Mcs.doc 2002

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 1/53

MCS University Paper 2002

Group No. 09

Deepika Punjabi 42Nandita Rai 43

Anish Rajput 44

Rakesh Ramwani 45Jeetu Sachdev 46

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 2/53

1. Impact of Management Style on

Management Control� Usually, subordinates attitude reflects that

what they perceive their superiors attitude

ultimately stem them from the CEO.

� Managers come in all shapes and sizes. Some

are charismatic and outgoing, others are less

ebullient. Some spend much time looking and

talking to people, others rely more heavily on

written reports.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 3/53

2. Free Cash Flow

� FCF represents the cash that a company is

able to generate after laying out money to

maintain or expand its asset base.

� A measure of companys financial

performance.

� Calculated as-

FCF= Net Income + Depreciation Net

changes in working Cap. Capital Exp.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 4/53

3. Management Control Process

� Such system consists of following activities:

� Strategic Planning

� Budget Preparation� Execution

� Evaluation of performance

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 5/53

4. Implication of Differentiated

Strategies on Controls

� Any organization, however well aligned its

structures is to the chosen strategy, can not

effectively implement its strategies without a

consistent management control system. While

organization structure defines the reporting

relationship and responsibilities and

authorities of different managers, it neededan appropriately designed control system to

the function effectively.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 6/53

Q 2.) Under which conditions

management is better advised not tocreate profit center. Explain the

advantage of creation of profit

center.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 7/53

� Three types of decisions are to be made:� Product decision

� Marketing decision

� Procurement or sourcing decision

In general, greater the degree of integration

within a company,more difficult it becomes toassign responsibility to a single profit centerfor all three activities.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 8/53

Advantages of Profit Centers

� Q uality of decision may improve.

� Speed of operating decision may increase as it

may not need to be referred to headquarters.� Headqarters,get free from day-today decision

making and hence,may concentrate on other

issues.

� Profit center provides top management the

information on profitability.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 9/53

Q.4 What is a responsibility center? List and

explain different types of Responsibility

Centres in organizations.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 10/53

What is a responsibility center?

� In simple words: an organizational unit for

which a manager is made responsible.

�

Examples: A specific store in a chain of grocerystores.

� A work-station in a production line

manufacturing automobile batteries.

� The payroll data processing center within a

firm.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 11/53

Types of Responsibility Centers

� Revenue Centers

� Cost Centers or Expense Centers

�Profit Centers and

� Investment Centers

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 12/53

Revenue Centers

� Responsibility Centers whose members

control revenues but,

�

Not the manufacturing or acquisition cost of the products or service they sell, or

� The level of investment in the responsibility

center.

� In other words, you cannot link the input to

the output.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 13/53

Revenue Centers (continued)

� Most revenue centers may not set selling prices

� They definitely have no control over the costs of inputacquired

� These centers are generally not allocated costs of thegoods that they market. Manager is responsible onlyfor costs directly incurred by his/her unit.

� They are evaluated on the basis of actual sales ororders booked against budgets or quotas and

� Example: a unit of a chain store in a mall.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 14/53

Expense/Cost Centers

� Responsibility centers whose employees control costs, but

� Do not control their revenues or investment level.

� Examples: Production department in a manufacturing unit, a

dry cleaning business� Two types of costs:

± Engineered: those costs that can be reasonably associated with a cost

center direct labor, direct materials, telephone/electricity consumed,

office supplies.

± Discretionary: where a direct relationship between a cost unit andexpenses cannot be reasonably made; Management allocates them

on a discretionary basis (e.g. depreciation expenses for machines

utilized).

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 15/53

Profit Centers

� Managers of profit centers control both the

revenues and costs of the product or service they

deliver.

� It is like an independent business except it is part

of a larger organization (e.g. departmental stores

of larger chains Wal Mart, restaurants,

corporate hotels such as Hilton, Holiday Inn).� The store manager would have responsibility for

pricing, product selection, and promotion.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 16/53

Profit Centers (continued)

� Cost for these units vary depending on ability tocontrol labor, waste, and hours.

� Revenues also will vary depending on the units servicelevel, location, etc.

� In other words, local discretion would affect revenuesand costs.

� Therefore, profits represent a broader index of bothcorporate and local decisions.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 17/53

Profit Centers (continued)

� If performance is poor, it may reflect poorconditions that no one in the organizationcould control local conditions.

� For this reason, organizations should notevaluate performance only based on costs andprofits, but

�

Perform detailed evaluations that includequality, material use, labor use, and servicemeasures that the local unit can control.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 18/53

Investment Centers

� Responsibility centers whose managers and

employees control revenues, costs, and the

level of investment.

� It is also like an independent business

(common when an organization acquires

another organization e.g. Sears financial

centers).

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 19/53

Q.3. (b) Explain the problems faced in pricing

corporate services furnished by corporate

services staff to business units in the

company. Assume profit centers

decentralization.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 20/53

Problems associated with charging

business units

� There are some of the problems associated withcharging business units for services furnished bycorporate staff units.

� Central accounting, public relations, administrationthese are the costs of central service staff units overwhich business units have no control

� if these costs are charged at all, they are allocated, andthe allocations do not include a profit component.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 21/53

Cont.

� There are two types of transfers:

�For central services that the receiving unitmust accept but can at least partially control

the amount used.

� For central services that the business unit can

decide whether or not to use.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 22/53

Control over amount of service

� Business units may be required to usecompany staffs for services such asinformation technology and research and

development.

In these situations, the business unit manager

cannot control the efficiency with which theseactivities are performed but can control theamount of the service received.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 23/53

Optional use of Services

� In some cases management may decide that business unitscan choose whether to use central service units.

� Business units may procure the service from outside,

develop their own capability, or choose not to use theservice at all.

� This type of arrangement is most often found for suchactivities as information technology, internal consulting

groups, and maintenance work.

� These service centers are independent.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 24/53

Q.3 (a) Describe the features of cost based

and market price based transfer pricing

methods?

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 25/53

25

Transfer pricing

Transfer Price is:the internal price charged by one segment of a firm for a

product or service supplied to another segment of the same

firmSuch as:

� Internal charge paid by final assembly division for

components produced by other divisions

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 26/53

26

Market-Based Transfer Prices

� Top management chooses to use the price of a

similar product or service that is publicly

available. Sources of prices include trade

associations, competitors, etc.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 27/53

27

Market-Based Transfer Prices

� Lead to optimal decision making when threeconditions are satisfied:

1. The market for the intermediate product is

perfectly competitive2. Interdependencies of subunits are minimal

3. There are no additional costs or benefits to thecompany as a whole from buying or selling in the

external market instead of transacting internally

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 28/53

28

Market-Based Transfer Prices

� A perfectly competitive market exists when there is a

homogeneous product with buying prices equal to selling

prices and no individual buyer or seller can affect those

prices by their own actions� Allows a firm to achieve goal congruence, motivating

management effort.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 29/53

29

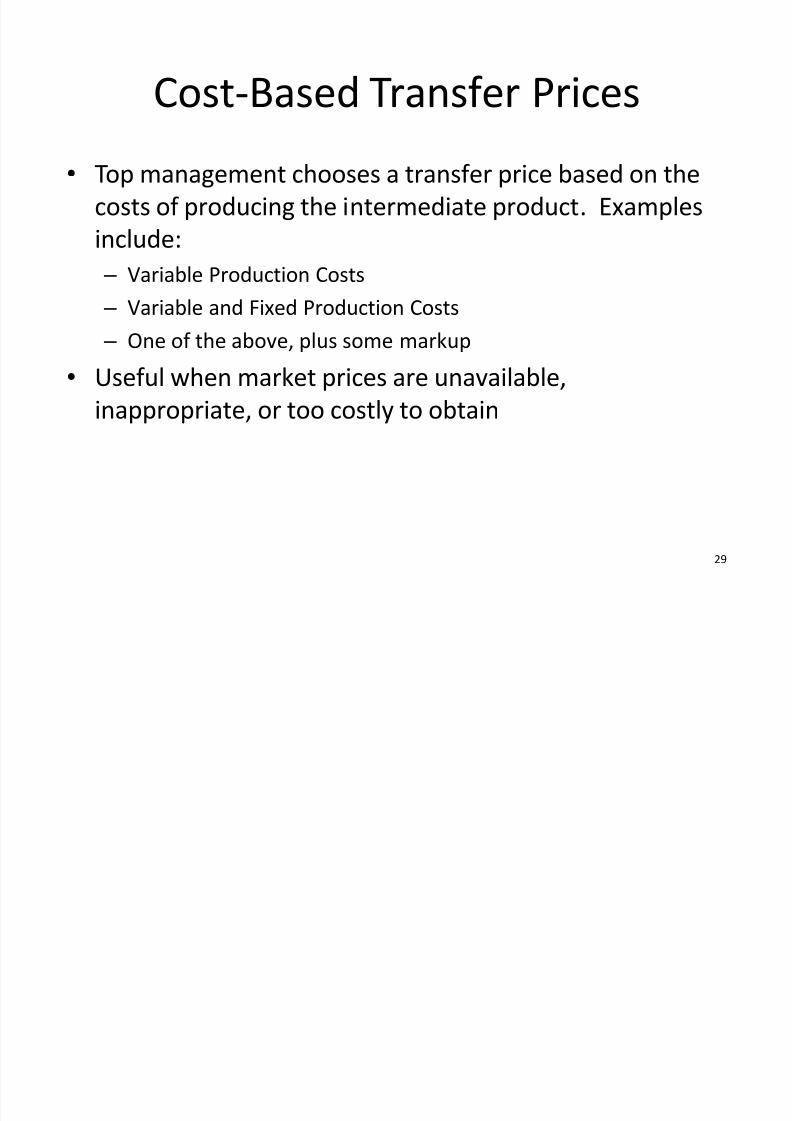

Cost-Based Transfer Prices

� Top management chooses a transfer price based on the

costs of producing the intermediate product. Examples

include:

±

Variable Production Costs ± Variable and Fixed Production Costs

± One of the above, plus some markup

� Useful when market prices are unavailable,

inappropriate, or too costly to obtain

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 30/53

30

Cost-Based Transfer Prices

� Top management chooses a transfer price based on the

costs of producing the intermediate product. Examples

include:

±

Variable Production Costs ± Variable and Fixed Production Costs

± One of the above, plus some markup

� Useful when market prices are unavailable,

inappropriate, or too costly to obtain

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 31/53

Q7 What is goal Congruence and factors influencing

it?

Senior management wants the organization toattain the organizations goals. But the individual

members of the organizations have their own

personal goals, and they are not necessarily

consistent with those of the organization. The central

purpose of a management control system is to

ensure a high level of what is called GOAL

CONGRUENCE

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 32/53

Factors influencing Goal Congruence:

� External Factors

�

Internal Factors ±Culture

±Management style

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 33/53

Q5) What are interactive controls?

� Interactive control is a subset of the management

control information that has a bearing on thestrategic uncertainties facing the businessbecomes the focal point.

� Industries subject to very rapid environmental

changes, management control information canalso provide the basis for thinking about newstrategies.

� Learning organization refers to the ability of organization employees to learn to cope with

environmental changes on an ongoing basis. � To facilitate the creation of a learning

organization.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 34/53

� Interactive control has the followingcharacteristics:

± A subset of the management control information thathas a bearing on the strategic uncertainties facing thebusiness becomes the focal point.

± Senior executives take such information seriously.

±

Managers at all levels of the organization focusattention on the information produced by the system.

± Superiors, subordinates and peers meet face-to-faceto interpret and discuss the implications of theinformation for future strategic

± The face-to-face meetings take the form of debate andchallenge of the underlying data, assumptions, andappropriate actions.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 35/53

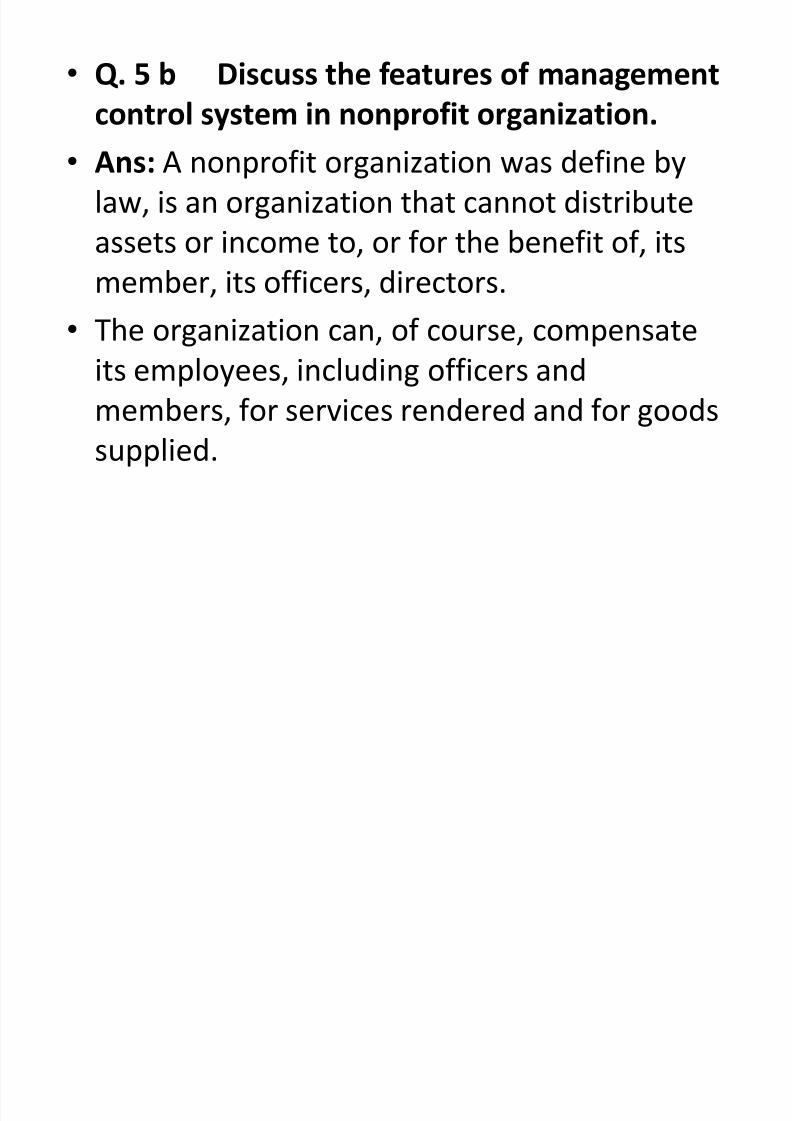

� Q. 5 b Discuss the features of management

control system in nonprofit organization.

� Ans: A nonprofit organization was define by

law, is an organization that cannot distribute

assets or income to, or for the benefit of, its

member, its officers, directors. � The organization can, of course, compensate

its employees, including officers and

members, for services rendered and for goodssupplied.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 36/53

� Characteristics of nonprofit organization

� Absence of the Profit Measure

�

Contributed capital� Fund Accounting

� Governance

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 37/53

� Management control System and its features

in nonprofit organization

± Product Pricing

± Strategic planning and budget Preparation

± Operation and Evaluation

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 38/53

� Q.6 (A) Explain the concept of ROI. What are

its advantages?� Return on investment (ROI) is the ratio of

profit before tax to the gross investment.

ROI is calculated with the help of the followingformula:

ROI = (Pre-Tax Profit/Sales) X (Sales/Net

Assets) or (Pre-Tax Profits/Net Assets)

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 39/53

� Advantages of ROI

1.ROI relates return to the level of investmentand not sales as the rate of return is more

realistic.

2.ROI can be decomposed into other variablesas shown. These variables have tremendous

analytical value.

3.ROI is an effective tool for inter-firm

comparison

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 40/53

Q9) Investment base used in performance

evaluation of investment centres consists of various elements. Explain general practices

used in organisation in treatment of each

element and the likely response induced by

the treatment of each of these elements in

managers.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 41/53

� PERFORMANCE MEASURES FOR INVESTMENT

CENTERS

� Rate of Return on Investment (ROI)

ROI = (Pre-Tax Profit/Sales) X (Sales/Net

Assets) or (Pre-Tax Profits/Net Assets)

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 42/53

� Advantages:

1) ROI allows management to assess both

profitability and efficiency in using assets.2) Divisions of unequal size can be com-pared.

3) Management is provided with information tomake decisions on where to invest

additional company funds. The company knowswhere it is getting "the most bangfor its buck."

Disadvantage:

If a manager is evaluated based on ROI, he or shewill not invest in any project that will lower thedivision's ROI, even if it would increase thecompany's profitability.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 43/53

� Residual Income

The amount of income that an individual has

after all personal debts, including the

mortgage, have been paid. This calculation is

usually made on a monthly basis, after the

monthly bills and debts are paid. Also, when amortgage has been paid off in its entirety, the

income that individual had been putting

toward the mortgage becomes residual

income.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 44/53

� Advantages:

1) It considers a company's minimum rate of

return.

2) Any project that increases residual income

will be pursued by division management.

� Disadvantage:

The relative size of the divisions is not

considered.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 45/53

� The balanced scorecard is a set of financial

and nonfinancial measures that reflect

multiple performance dimensions of a

business.

� EVA

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 46/53

� Transfer Pricing

It is the Price at which Divisions of a company

transact with each other. Transactions may

include the trade of supplies or labor between

departments. Transfer prices are used when

individual entities of a larger multi-entity firm are

treated and measured as separately run entities.

Also known as transfer cost

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 47/53

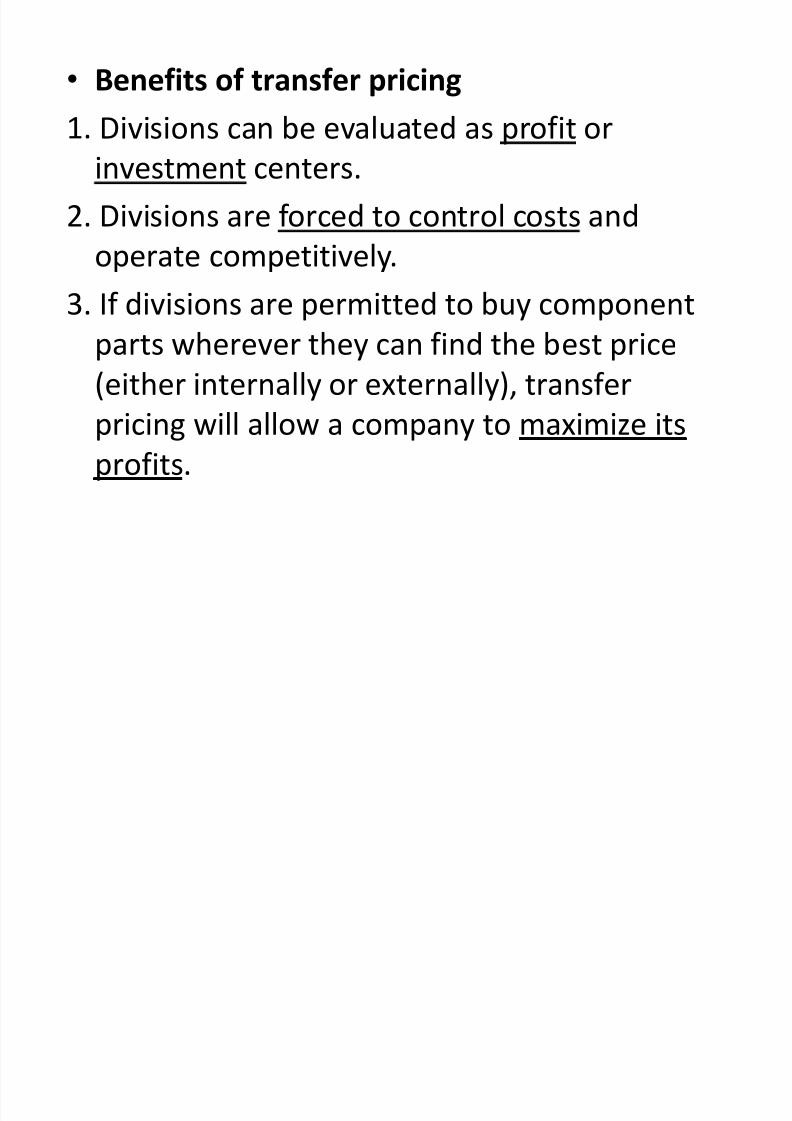

� Benefits of transfer pricing

1. Divisions can be evaluated as profit or

investment centers.

2. Divisions are forced to control costs and

operate competitively.

3. If divisions are permitted to buy component

parts wherever they can find the best price

(either internally or externally), transfer

pricing will allow a company to maximize itsprofits.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 48/53

� Few other Non - financial Performance

Measurement Tool

1.Measures of product quality

2.Customer complaints and warranty experience

3.Customer satisfaction and retention rates

4.Product availability and on-time performance

5.New product time to market and market share

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 49/53

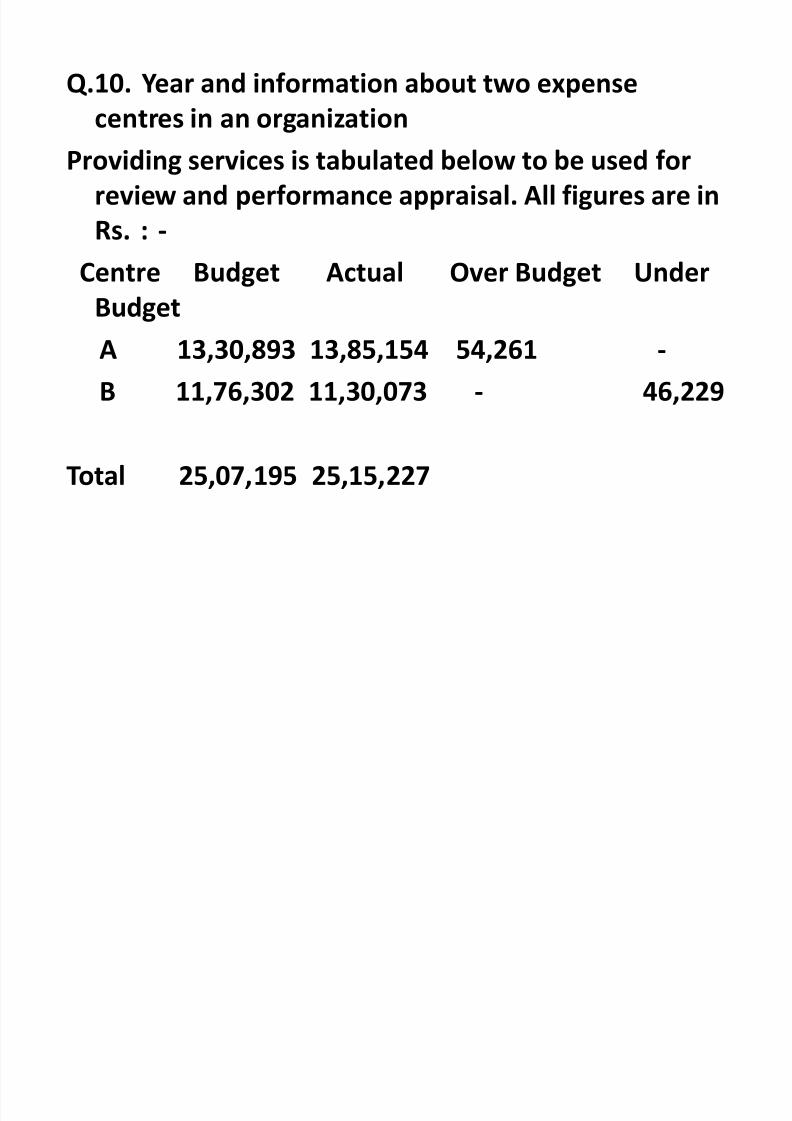

Q.10. Year and information about two expense

centres in an organization

Providing services is tabulated below to be used for

review and performance appraisal. All figures are in

Rs. : -

CentreB

udget ActualO

verB

udget UnderBudget

A 13,30,893 13,85,154 54,261 -

B 11,76,302 11,30,073 - 46,229

Total 25,07,195 25,15,227

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 50/53

� Number of personnel:

� A 46 46 - -� B 26 24 - 2

Manager to whom the heads of these two centers

report is not clear on how to use the availableinformation for evaluation. Assuming that any

further information requested would be

available ( on proper justification), assistant

Manager in his task of evaluation.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 51/53

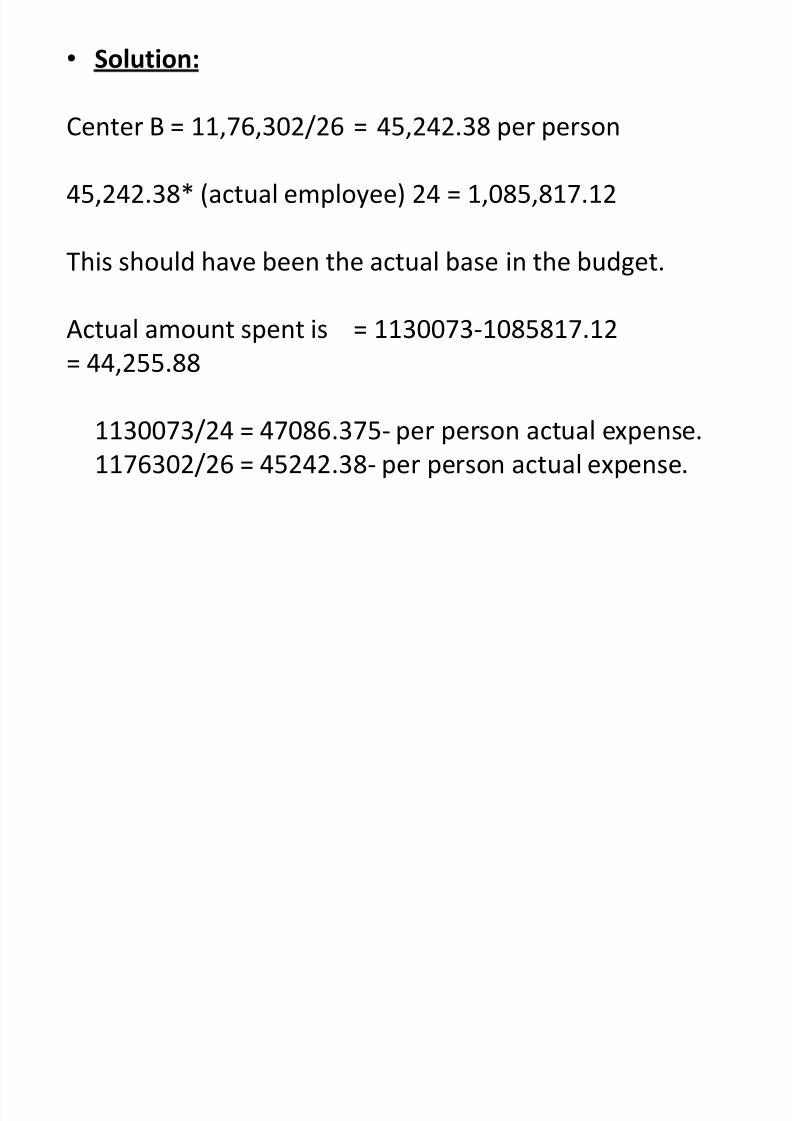

� Solution:

Center B = 11,76,302/26 = 45,242.38 per person

45,242.38* (actual employee) 24 = 1,085,817.12

This should have been the actual base in the budget.

Actual amount spent is = 1130073-1085817.12

= 44,255.88

1130073/24 = 47086.375- per person actual expense.1176302/26 = 45242.38- per person actual expense.

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 52/53

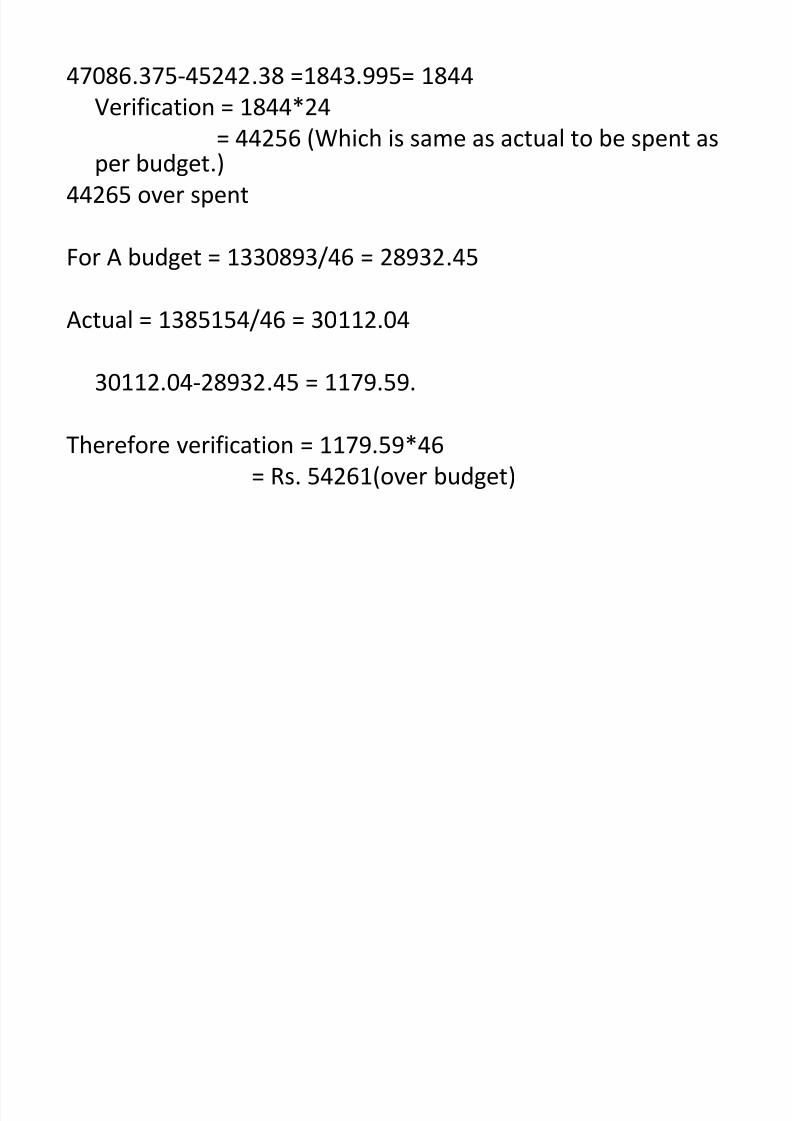

47086.375-45242.38 =1843.995= 1844

Verification = 1844*24

= 44256 (Which is same as actual to be spent asper budget.)

44265 over spent

For A budget = 1330893/46 = 28932.45

Actual = 1385154/46 = 30112.04

30112.04-28932.45 = 1179.59.

Therefore verification = 1179.59*46

= Rs. 54261(over budget)

8/7/2019 Rakesh Presi Mcs.doc 2002

http://slidepdf.com/reader/full/rakesh-presi-mcsdoc-2002 53/53

Thank You