Review of the Code of Banking Practice, Final Report, December 2008

1

Review of

The Code of Banking Practice

Final Report

December 2008

Jan McClelland and Associates Pty Limited

Review of the Code of Banking Practice, Final Report, December 2008

2

TABLE OF CONTENTS

TABLE OF CONTENTS ......................................................................................................... 2

ABBREVIATIONS AND DEFINITIONS .............................................................................. 10

SUMMARY OF RECOMMENDATIONS ............................................................................. 12

RESPONSIBLE LENDING ............................................................................................... 12

General Principle of Responsible Lending - Clause 2 .......................................................... 12

Provision of Credit – Clause 25.1 ....................................................................................... 12

FINANCIAL HARDSHIP – Clause 25.2 ............................................................................ 13

DEBT COLLECTION - Clause 29 ..................................................................................... 14

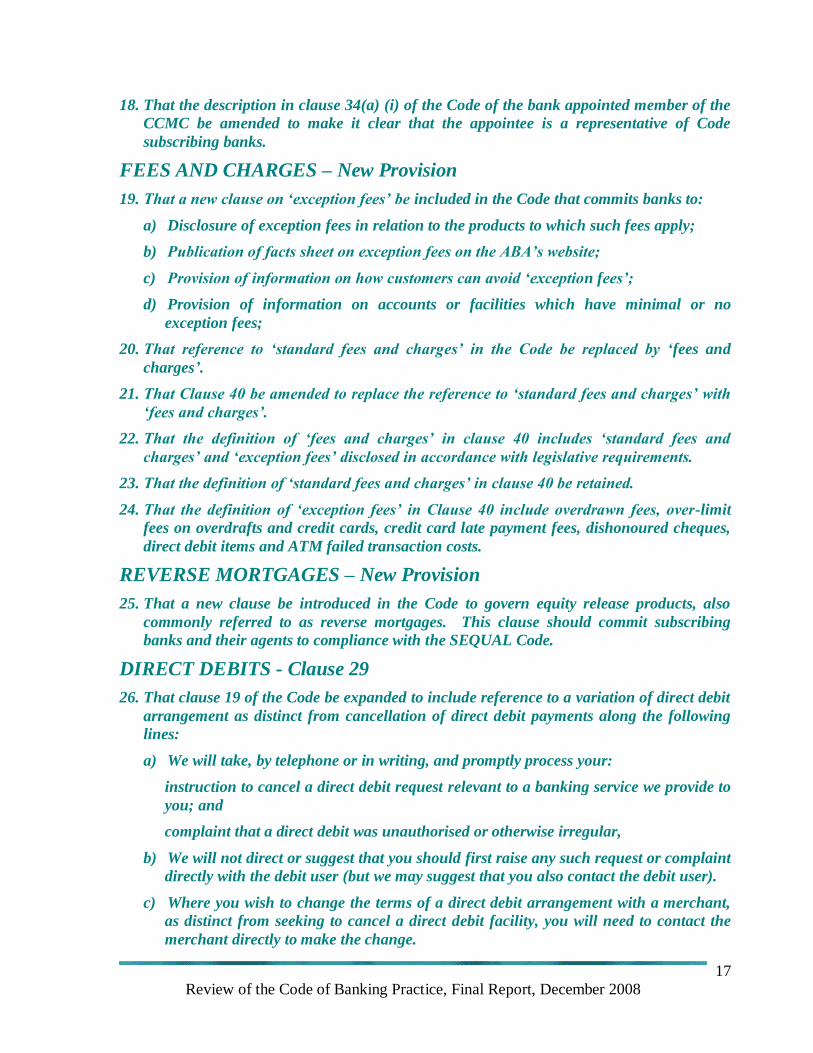

GUARANTEES - Clause 28 ............................................................................................... 15

JOINT DEBTORS - Clause 26 ........................................................................................... 15

CODE COMPLIANCE MONITORING COMMITTEE AND THE FINANCIAL

OMBUDSMAN SERVICE - Clause 34 .............................................................................. 15

FEES AND CHARGES – New Provision ........................................................................... 17

REVERSE MORTGAGES – New Provision ...................................................................... 17

DIRECT DEBITS - Clause 29 ............................................................................................ 17

ACCOUNT SWITCHING – New Provision ....................................................................... 18

ELECTRONIC BANKING - Clause 33 .............................................................................. 18

COMMUNICATION – New Provision............................................................................... 19

ACCOUNT SUITABILITY - Clause 14 ............................................................................. 19

DISCLOSURES - TERMS AND CONDITIONS - Clauses 10 and 13 ................................ 20

COMPLIANCE WITH LAWS - Clause 3........................................................................... 21

KEY COMMITMENTS – Clause 2 .................................................................................... 21

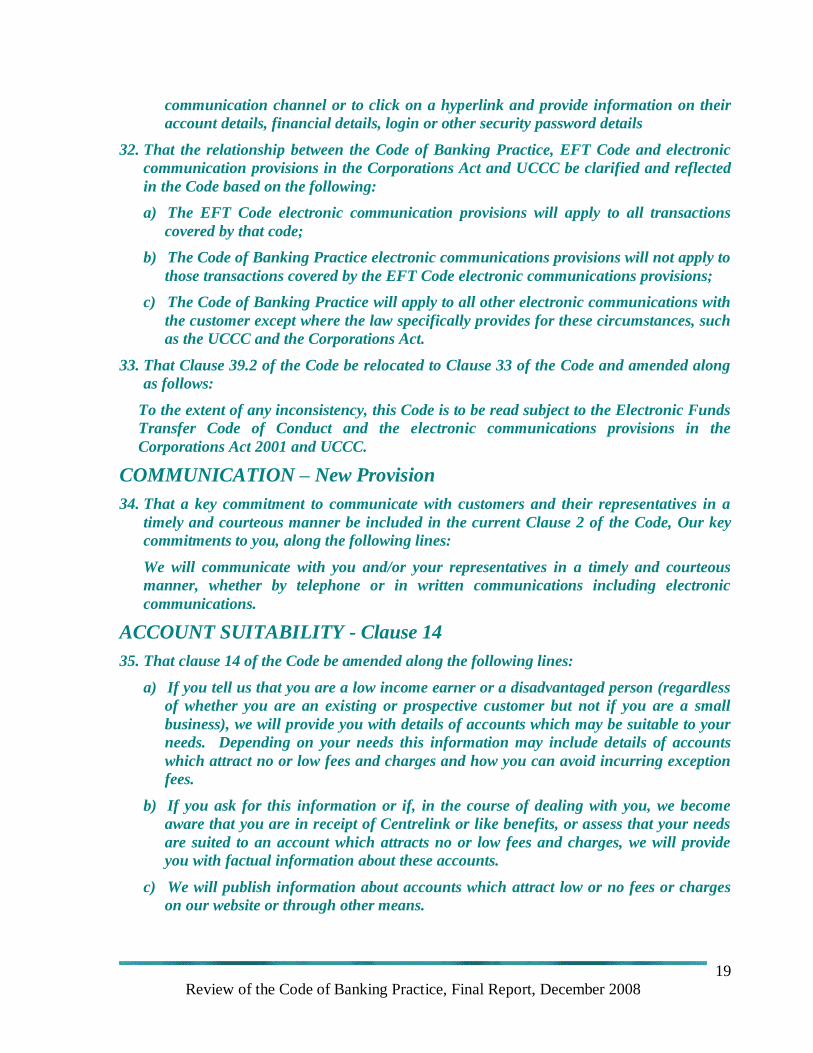

COPIES OF DOCUMENTS - Clause 11 ............................................................................ 21

OPENING OF ACCOUNTS - Clause 16 ............................................................................ 21

CHANGES TO TERMS AND CONDITIONS - Clause 18 ................................................. 21

CHARGEBACKS - Clause 20 and Clause 10 ..................................................................... 22

PRIVACY AND CONFIDENTIALITY - Clause 22 ........................................................... 22

STATEMENT OF ACCOUNTS - Clause 24 ...................................................................... 22

ADVERTISING - Clause 30 ............................................................................................... 22

INTERNAL AND EXTERNAL DISPUTE RESOLUTION - Clauses 35, 36 and 37 .......... 22

Review of the Code of Banking Practice, Final Report, December 2008

3

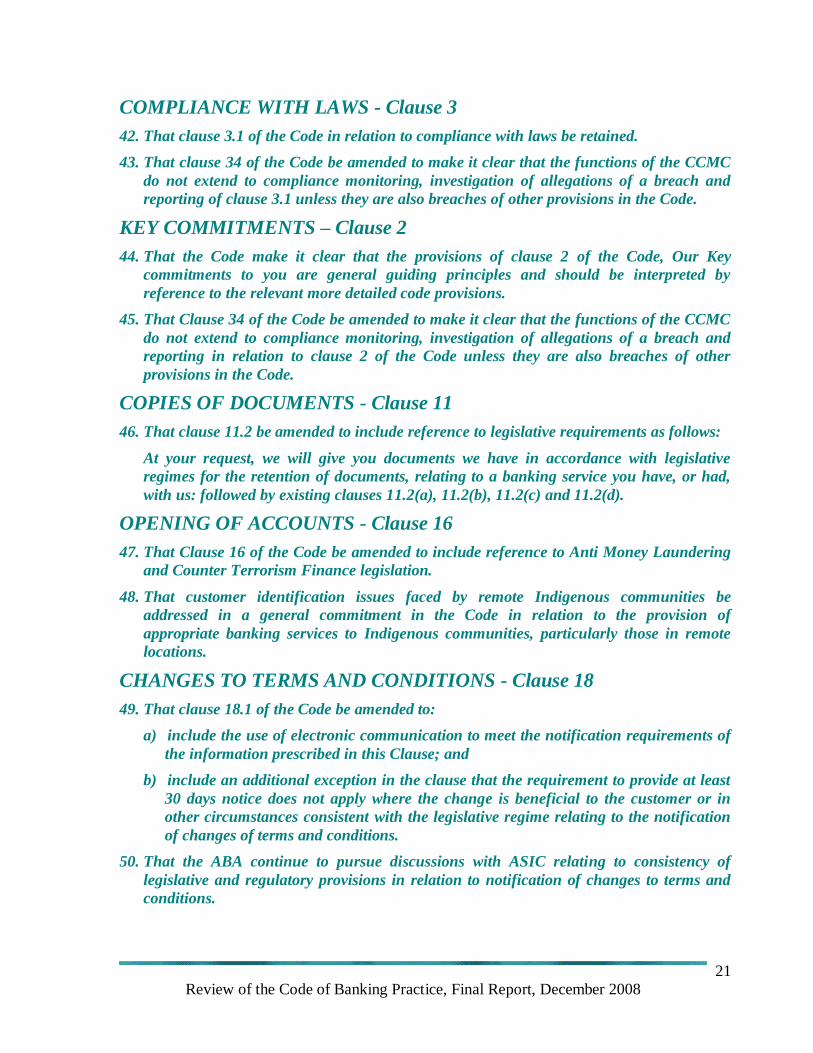

APPLICATION AND TRANSITIONAL PROVISIONS - Clause 39 ................................. 23

CUSTOMERS IN REMOTE INDIGENOUS COMMUNITIES – New Provision .............. 23

LANGUAGE AND STRUCTURE OF THE CODE ........................................................... 24

STAFF TRAINING AND COMPETENCY - Clause 7 ....................................................... 24

UNFAIR CONTRACT TERMS ......................................................................................... 24

ACCOUNT COMBINATION- Clause 17........................................................................... 24

USE OF FINANCE AND MORTGAGE BROKERS ......................................................... 24

PROMOTION OF THE CODE – Clause 9 ......................................................................... 25

CHAPTER 1 - INTRODUCTION .......................................................................................... 26

1.1 Appointment of the Review .............................................................................................. 26

1.2 The Code of Banking Practice .......................................................................................... 26

1.3 Terms of Reference .......................................................................................................... 26

1.4 Approach .......................................................................................................................... 26

1.4.1 Preparation for the Review ......................................................................................... 26

1.4.2 Announcement of the Review .................................................................................... 27

1.4.3 Consultations ............................................................................................................. 27

1.4.4 Initial Submissions ..................................................................................................... 27

1.4.4 Review of Documentation .......................................................................................... 27

1.4.5 Attendance at Forums ................................................................................................ 28

1.4.6 Issues Paper ............................................................................................................... 28

1.4.7 Final Report ............................................................................................................... 28

1.5 Structure of the Report ...................................................................................................... 28

1.6 Acknowledgements .......................................................................................................... 29

CHAPTER 2 - CONTEXT ..................................................................................................... 30

2.1 Economic and Regulatory Changes ................................................................................... 30

2.2 Status and Standing of the Code........................................................................................ 31

CHAPTER 3 - RESPONSIBLE LENDING ............................................................................ 33

3.1 Credit Assessment - Clause 25.1 ....................................................................................... 33

3.1.1 Issues Paper ............................................................................................................... 33

3.1.2 Responses to the Issues Paper .................................................................................... 34

3.2 Unsolicited Offers of Credit Card Limit Increases – Clause 25.1....................................... 36

3.3 Developments since the Last Code Review ....................................................................... 37

Review of the Code of Banking Practice, Final Report, December 2008

4

3.3.1 Subscribing Banks‟ Policies on Responsible Lending................................................. 37

3.3.2 National Regulation of Consumer Credit .................................................................... 37

3.3.3 Ministerial Council on Consumer Affairs Regulatory Impact Statement on Responsible

Lending Practices in relation to Consumer Credit Cards ..................................................... 38

3.3.4 Australian Law Reform Commission Review of Privacy Legislation ......................... 38

3.3.5 Financial Ombudsman Service ................................................................................... 38

3.4 The Way Forward ............................................................................................................. 39

3.4.1 Credit Assessment...................................................................................................... 39

3.4.2 Unsolicited Offers of Credit Limit Increases .............................................................. 40

Recommendations .............................................................................................................. 41

General Principle of Responsible Lending ...................................................................... 41

Provision of Credit ......................................................................................................... 41

CHAPTER 4 - FINANCIAL HARDSHIP .............................................................................. 43

4.1 Financial Hardship - Clause 25.2 ...................................................................................... 43

4.1.1 Issues Paper ............................................................................................................... 43

4.1.2 Response to the Issues Paper ...................................................................................... 43

4.1.3 The Way Forward ...................................................................................................... 45

Recommendations .............................................................................................................. 46

CHAPTER 5 - DEBT COLLECTION .................................................................................... 48

5.1 Debt Collection - Clause 29 .............................................................................................. 48

5.1.1 Issues Paper ............................................................................................................... 48

5.1.2 Responses to the Issues Paper .................................................................................... 48

5.1 3 The Way Forward ...................................................................................................... 49

Recommendations .............................................................................................................. 49

CHAPTER 6 - GUARANTEES.............................................................................................. 51

6.1 Guarantees - Clause 28 ..................................................................................................... 51

6.1.1 Issues Paper ............................................................................................................... 51

6.1.1 1 Commercial Asset Financing Guarantors ............................................................. 51

6.1 1 2 Cooling off Period ............................................................................................... 51

6.1.1.3 Undisclosed Principle and Agent Arrangements .................................................. 51

6.1.1.4 Compliance with Privacy Principles .................................................................... 52

6.1.2 Responses to the Issues Paper .................................................................................... 52

6.1.2.1 General Comments on the Guarantee Provisions of the Code .............................. 52

Review of the Code of Banking Practice, Final Report, December 2008

5

6.2.1.2 Commercial Asset Financing Guarantors ............................................................. 53

6.2.1.3 Cooling Off Period .............................................................................................. 54

6.2.1.4 Principal and Agent Arrangements ...................................................................... 54

6.2.1.5 Privacy Principles ............................................................................................... 55

6.2.1.6 Enforcement ........................................................................................................ 55

6.1.3 The Way Forward ...................................................................................................... 55

6.1.3.1 Commercial Asset Financing Guarantees ............................................................ 55

6.1.3.2 Cooling Off Period .............................................................................................. 56

6.1.3.3 Principal and Agent Arrangements ...................................................................... 56

6.1.3.4 Privacy Principles ............................................................................................... 57

6.1.3.5 Enforcement ........................................................................................................ 57

Recommendations .............................................................................................................. 58

CHAPTER 7 - JOINT DEBTORS .......................................................................................... 59

7.1 Joint Debtors - Clause 26 .................................................................................................. 59

7.1.1 The Issues Paper ........................................................................................................ 59

7.1.2 Responses to the Issues Paper .................................................................................... 59

7.1.3 The Way Forward ...................................................................................................... 60

Recommendations .............................................................................................................. 60

CHAPTER 8 - CODE COMPLIANCE MONITORING COMMITTEE AND THE

FINANCIAL OMBUDSMAN SERVICE ............................................................................... 61

8.1 Code Compliance Monitoring Committee - Clause 34 ...................................................... 61

8.1.1 Issues Paper ............................................................................................................... 61

8.1.2 Responses to the Issues Paper .................................................................................... 61

8.1.3 The Way Forward ...................................................................................................... 65

Recommendations .............................................................................................................. 67

CHAPTER 9 - FEES AND CHARGES .................................................................................. 69

9.1 Exception Fees – New Provision ....................................................................................... 69

9.1.1 Issues Paper ............................................................................................................... 69

9.1.2 Responses to the Issues Paper .................................................................................... 70

Recommendations .............................................................................................................. 72

CHAPTER 10 – OTHER ISSUES .......................................................................................... 74

10.1 REVERSE MORTGAGES – New Provision .................................................................. 74

10.1 1 Issues Paper ............................................................................................................. 74

Review of the Code of Banking Practice, Final Report, December 2008

6

10.1.2 Responses to the Issues Paper .................................................................................. 74

Recommendations .............................................................................................................. 74

10.2 DIRECT DEBITS - Clause 29 ........................................................................................ 74

10.2.1 Issues Paper ............................................................................................................. 74

10.2.2 Responses to the Issues Paper .................................................................................. 75

Recommendations .............................................................................................................. 75

10.3 ACCOUNT SWITCHING – New Provision ................................................................... 76

10.3.1 Issues Paper ............................................................................................................. 76

10.3.2 Responses to the Issues Paper .................................................................................. 76

Recommendations .............................................................................................................. 77

10.4 ELECTRONIC BANKING - Clause 33 .......................................................................... 77

10.4.1 Issues Paper ............................................................................................................. 77

10.4.2 Responses to the Issues Paper .................................................................................. 77

Recommendations .............................................................................................................. 78

10.5 COMMUNICATION – New Provision ........................................................................... 79

10.5.1 Issues Paper ............................................................................................................. 79

10.5.2 Responses to the Issues Paper .................................................................................. 79

Recommendation ................................................................................................................ 79

10.6 ACCOUNT SUITABILITY - Clause 14 ......................................................................... 80

10.6.1 Issues Paper ............................................................................................................. 80

10.6.2 Responses to the Issues Paper .................................................................................. 80

Recommendations .............................................................................................................. 81

10.7 DISCLOSURES - TERMS AND CONDITIONS - Clauses 10 and 13 ............................ 81

10.7.1 Issues Paper ............................................................................................................. 81

10.7.2 Responses to the Issues Paper .................................................................................. 81

Recommendations .............................................................................................................. 82

10.8 COMPLIANCE WITH LAWS - Clause 3 ....................................................................... 82

10.8.1 Issues Paper ............................................................................................................. 82

10.8.2 Responses to the Issues Paper .................................................................................. 83

Recommendations .............................................................................................................. 83

10.9 KEY COMMITMENTS ................................................................................................. 83

10.9.1 Issues Paper ............................................................................................................. 83

Review of the Code of Banking Practice, Final Report, December 2008

7

10.9.2 Responses to the Issues Paper .................................................................................. 83

10.9.3 The Way Forward .................................................................................................... 83

Recommendations .............................................................................................................. 84

10.10 COPIES OF DOCUMENTS - Clause 11 ....................................................................... 84

10.10.1 Issues Paper ........................................................................................................... 84

10.10.2 Responses to the Issues Paper ................................................................................ 84

Recommendations .............................................................................................................. 84

10.11 OPENING OF ACCOUNTS - Clause 16 ...................................................................... 85

10.11.1 Issues Paper ........................................................................................................... 85

10.11.2 Responses to the Issues Paper ................................................................................ 85

Recommendations .............................................................................................................. 85

10.12 CHANGES TO TERMS AND CONDITIONS - Clause 18 ........................................... 85

10.12.1 Issues Paper ........................................................................................................... 85

10.12.2 Responses to the Issues Paper ................................................................................ 85

Recommendations .............................................................................................................. 85

10.13 CHARGEBACKS - Clause 20 and Clause 10 ............................................................... 86

10.13.1 The Issues Paper .................................................................................................... 86

10.13.2 Responses to the Issues Paper ................................................................................ 86

Recommendations .............................................................................................................. 86

10.14 PRIVACY AND CONFIDENTIALITY - Clause 22 ..................................................... 87

10.14.1 Issues Paper ........................................................................................................... 87

10.14.2 Responses to the Issues Paper ................................................................................ 87

Recommendations .............................................................................................................. 88

10.15 STATEMENT OF ACCOUNTS - Clause 24 ................................................................ 88

10.15.1 Issues Paper ........................................................................................................... 88

10.15.2 Responses to the Issues Paper ................................................................................ 88

Recommendations .............................................................................................................. 88

10.16 ADVERTISING - Clause 30 ......................................................................................... 88

10.16.1 Issues Paper ........................................................................................................... 88

10.16.2 Responses to the Issues Paper ................................................................................ 88

Recommendations .............................................................................................................. 89

10.17 INTERNAL AND EXTERNAL DISPUTE RESOLUTION - Clauses 35, 36 and 37 .... 89

Review of the Code of Banking Practice, Final Report, December 2008

8

10.17.1 Issues Paper ........................................................................................................... 89

10.17 2 Responses to the Issues Paper ................................................................................ 89

Recommendations .............................................................................................................. 90

10.18 APPLICATION AND TRANSITIONAL PROVISIONS - Clause 39 ........................... 91

10.18 1 Issues Paper ........................................................................................................... 91

10.18.2 Responses to the Issues Paper ................................................................................ 91

Recommendations .............................................................................................................. 91

10.19 CUSTOMERS IN REMOTE INDIGENOUS COMMUNITIES – New Provision ......... 91

10.19.2 Issues Paper ........................................................................................................... 91

10.19.2 Responses to the Issues Paper ................................................................................ 92

Recommendations .............................................................................................................. 92

10.20 LANGUAGE AND STRUCTURE OF THE CODE ..................................................... 93

10.20.1 Issues Paper ........................................................................................................... 93

10.20.2 Responses to the Issues Paper ................................................................................ 93

Recommendations .............................................................................................................. 93

CHAPTER 11 – OTHER MATTERS RAISED IN SUBMISSIONS TO THE ISSUES PAPER

............................................................................................................................................... 94

11.1 STAFF TRAINING AND COMPETENCY - Clause 7 ................................................... 94

11.1.1 Issues Paper ............................................................................................................. 94

11.2 Response to the Issues Paper ....................................................................................... 94

Recommendations .............................................................................................................. 94

11.2 UNFAIR CONTRACT TERMS ..................................................................................... 94

11.2.1 Issues Paper ............................................................................................................. 94

11.2.2 Response to the Issues Paper .................................................................................... 94

Recommendation ................................................................................................................ 95

11.3 ACCOUNT COMBINATION- Clause 17 ....................................................................... 95

11.3.1 Issues Paper ............................................................................................................. 95

11.3.2 Responses to the Issues Paper .................................................................................. 95

Recommendations .............................................................................................................. 96

11.4 USE OF FINANCE AND MORTGAGE BROKERS...................................................... 96

11.4.1 Issues Paper ............................................................................................................. 96

11.4.2 Responses to the Issues Paper .................................................................................. 96

Recommendation ................................................................................................................ 97

Review of the Code of Banking Practice, Final Report, December 2008

9

11.5 PROMOTION OF THE CODE – Clause 9 ..................................................................... 97

11.5.1 Issues Paper ............................................................................................................. 97

11.5.2 Responses to the Issues Paper .................................................................................. 97

Recommendation ................................................................................................................ 97

CONTRIBUTIONS TO THE REVIEW BY SUBMISSIONS, CONSULTATIONS AND

CORRESPONDENCE ........................................................................................................... 98

Review of the Code of Banking Practice, Final Report, December 2008

10

ABBREVIATIONS AND DEFINITIONS

ABA Australian Bankers‟ Association

Abacus Association of Building Societies and Credit Unions

ACCC Australian Competition and Consumer Commission

AML/CTF legislation Anti Money Laundering and Counter Terrorism Financing Act

ASIC Australian Securities and Investments Commission

ALRC Australian Law Reform Commission

BFSO Banking and Financial Services Ombudsman

CCMC Code Compliance Monitoring Committee

Consultative Forum ABA‟s Community and Consumer Consultative Forum

Consumer Advocates Joint Consumer Submission contributors

COSBOA Council of Small Business Organisations of Australia

COSL Credit Ombudsman Service Limited

COTA Over 50’s Ltd Council on the Ageing

EFT Code Electronic Funds Transfer Code of Conduct

EDR External Dispute Resolution

FOS Financial Ombudsman Service

FSR Financial Services Reform Act 2001

IDR Internal Dispute Resolution

IP Review of Code of Banking Practice Issues Paper May 2008

JCS Joint Consumer Submission

Australian Financial Counselling and Credit Reform

Association

Care Financial Counselling Service and Consumer Law

Centre ACT

CHOICE

Consumer Action Law Centre

Consumer Credit Legal Centre NSW

Consumer Credit Legal Service WA

Consumers‟ Federation of Australia

Financial Counsellors Association of Queensland

MCCA Ministerial Council on Consumer Affairs

Review of the Code of Banking Practice, Final Report, December 2008

11

MFAA Mortgage and Finance Association of Australia

NSW OFT New South Wales Office of Fair Trading

SEQUAL Senior Australian Equity Release Association of Lenders

The Code Code of Banking Practice

The reviewer Jan McClelland & Associates Pty Limited

UCCC Uniform Consumer Credit Code

USA United States of Australia

UK United Kingdom

Review of the Code of Banking Practice, Final Report, December 2008

12

SUMMARY OF RECOMMENDATIONS

RESPONSIBLE LENDING

General Principle of Responsible Lending - Clause 2

1. That a key commitment to responsible lending be included in the current Clause 2 of the

Code, Our key commitments to you, along the following lines:

We will be responsible lenders in approving credit, offering credit limit increases,

supporting customers facing financial difficulty; and promoting responsible use of credit.

Provision of Credit – Clause 25.1

2. That a separate clause on provision of credit be included in the Code, building on Clause

25.1 but expanded to include two parts, one relating to approval of an application for a

credit facility and another relating to unsolicited or other offers of credit card limit

increases, which covers the following:

A. Approval of an Application for a Credit Facility

1) Before we approve your application for a credit facility or for an increase in your

existing credit facility, we will exercise the care and skill of a diligent and prudent

banker in selecting and applying appropriate assessment methods to your

circumstances and financial position and in forming our opinion about your ability

to repay the credit facility.

2) Our credit assessment methods will vary depending on a range of factors including

the credit facility product, whether you are a new customer or have an existing

banking relationship with us, the information you have provided to us and the

information available to us from other sources. Our credit assessment methodologies

will include, as appropriate to your circumstances, consideration of at least two of the

following factors:

a) Information you have provided on your income and financial commitments;

b) How you have handled your finances in the past;

c) Our internal credit scoring techniques;

d) Information from credit reference agencies.

Review of the Code of Banking Practice, Final Report, December 2008

13

B. Unsolicited or Other Credit Limit Increase Offers

1) If we decide to make you an offer of an increase in the credit limit of your credit

facility, we will take into account the following criteria:

a) Your recent credit facility repayments history, including whether you have been

able to meet repayments or whether you have a history of missed or late payment;

b) Your income, if in the course of our dealing personally with you, we become

aware that you are in receipt of a welfare payment that is your sole source of

income;

c) Your recent credit facility history, including whether you have a history of

consistently reaching or exceeding the credit limit while making only the

minimum monthly repayments, and/or whether we are aware of other information

that suggests you may be likely to be experiencing financial stress;

d) Your banking relationship with us, including whether you are a new customer

and/or whether you have acquired any other products from us; and

e) Your request not to receive unsolicited offers of credit limit increases, if you have

made such a request.

2) If we decide to make you an offer to increase your credit limit on an existing credit

facility, we will provide information on:

a) The new minimum monthly payment and repayment period if you accept the offer

and the credit facility is fully drawn on;

b) How to request a lower credit facility limit than the one we have offered;

c) How and when to reject the offer, for example, if you are having difficulties

meeting your current repayments, or if your financial circumstances have

changed or are likely to change such that you cannot afford to meet increased

repayments; and

d) Easy and efficient ways to reduce your credit facility limit and how long it will

take to process your request for a reduction in your credit facility limit.

FINANCIAL HARDSHIP – Clause 25.2

3. That a separate clause on financial hardship be included in the Code, building on Clause

25.2 but expanded to cover the following:

1) With your agreement, we will try to help you overcome your financial difficulties with

any credit facility you have with us. We will deal with you or, at your request, with

your financial counsellor or representative.

2) If, in the course of our personal dealings with you, we identify that you might be

experiencing difficulties in meeting your repayments we may contact you and invite

you to discuss your situation with us and the options available to assist you in

meeting your obligations in these circumstances.

3) If at any time you feel you are experiencing difficulties in meeting your repayments,

you should make contact with us as soon as possible to discuss your situation with us

Review of the Code of Banking Practice, Final Report, December 2008

14

and the options available to assist you in meeting your obligations in these

circumstances.

4) If, at the time, the hardship variation provisions of the Uniform Consumer Credit

Code could apply to your circumstances, we will inform you about them.

5) We will provide you with information about our processes for dealing with customers

in financial difficulty, including relevant contact numbers, at your request and when

we send you a default notice.

6) We will respond promptly and courteously to any requests for assistance from you.

7) We will take into account the information available to us, including the information

you provide to us, about your financial situation and determine whether or not we are

able to provide assistance and the nature and extent of such assistance.

8) We will inform you in writing of our decision whether or not to provide you with

assistance and the reasons for our decision. If we agree to provide you with

assistance we will confirm in writing the agreed arrangements.

9) While we are considering your application for assistance where you are experiencing

financial difficulty in relation to a credit facility with us, we will not commence any

enforcement action in relation to the debt or assign the debt. If we reject your

application for assistance, we will allow you a reasonable period of time to obtain

advice, before we commence enforcement action in relation to the debt or assign the

debt. If we have commenced enforcement action before you made the request, we will

not proceed to judgement whilst we are considering your situation.

10) We will not require you to access your Superannuation Fund to repay your credit

facility with us.

11) We will have information about our processes for dealing with customers in financial

difficulty available on our website.

12) We will ensure that relevant staff are trained in the financial hardship provisions of

the Code, and applicable consumer credit legislation.

DEBT COLLECTION - Clause 29

4. That Clause 29 of the Code is amended to include reference to ACCC and ASIC debt

collection guidelines as amended or replaced from time to time.

5. That the debt collection clause follow the proposed revised clause on Financial Hardship

and include the following:

a) We will comply with the Australian Competition and Consumer Commission and

Australian Securities and Investments Commission guideline “Debt Collection

Guideline for Collectors and Creditors, October 2005,” as amended or replaced from

time to time, when collecting amounts due to us. We will ensure that our debt

collection agents do likewise.

b) If we sell a debt to a third party we will choose firms that agree to observe the ACCC

and ASIC debt collection guidelines referred to in (1) and that are members of an

ASIC approved external dispute resolution scheme.

Review of the Code of Banking Practice, Final Report, December 2008

15

GUARANTEES - Clause 28

6. That the definition of commercial asset financing guarantor in Clause 40 of the Code be

amended to broaden the class of guarantors to include directors, owners or managers of

the business that is managed by or under the direction of the director, owner or manager.

7. That Clause 28.14 of the Code be expanded to provide that enforcement of a judgement

against the guarantor or any security provided by the guarantor will only be taken after

attempts have been made to enforce the judgement against the debtor and/or enforce any

security against the debtor.

JOINT DEBTORS - Clause 26

8. That Clause 26.1 of the Code be amended to provide:

We will not accept you as a co-debtor under a credit facility where it is clear, on the facts

known to us, that you will not receive a benefit under the facility.

CODE COMPLIANCE MONITORING COMMITTEE AND THE

FINANCIAL OMBUDSMAN SERVICE - Clause 34

9. That the CCMC be established as a separate independent unit within the FOS reporting

directly to and accountable to the FOS Board for the performance of its prescribed

functions under the Code.

10. That separate terms of reference of the CCMC be developed by the CCMC in

consultation with the ABA, the FOS ASIC and consumer interests. The terms of

reference for the CCMC should be consistent with the compliance monitoring,

investigation and reporting functions of the CCMC under the Code and be published on

the CCMC, FOS and ABA websites.

11. That the terms of reference of the CCMC make it clear that the CCMC and the FOS

have different functions of Code compliance monitoring and dispute resolution

respectively and guarantee the independence of one from the other in the performance of

those functions respectively as well as independence from banks.

12. That the charter, constitution, terms of reference and operating protocols of the FOS

Board and of the CCMC and the Code make it clear that individuals and organisations

have the right to make complaints about Code breaches directly to the CCMC.

13. That the Code make it clear that the CCMC retains its powers under the Code to conduct

investigations in response to complaints of Code breaches from any person or

organisation, and also to initiate investigations and reviews on its own initiative, and to

make determinations in relation to those investigations.

14. That the Code also spell out functions of the CCMC as including to:

a) conduct its own enquiries into banks‟ compliance with the Code;

b) prepare an annual report on compliance with the Code;

c) contribute to joint publications between the CCMC and FOS on Code interpretation

and compliance issues; and

Review of the Code of Banking Practice, Final Report, December 2008

16

d) promote awareness of the Code with banks through the provision of feedback on

Code issues.

15. That the charter, constitution, terms of reference and operating protocols of the FOS and

of the CCMC make it clear that the following arrangements apply in matters that are

referred to the FOS or the CCMC.

a) Where the FOS, in performance of its prescribed function of dispute resolution,

identifies a Code issue and finds that there has been a Code breach, that

determination is a final determination as to whether a Code breach has been

established. FOS must report its determination to the CCMC for further monitoring

as appropriate and provide access to its case file on the matter if required by the

CCMC.

b) Where the FOS, in performance of its prescribed function of dispute resolution,

identifies a Code issues and finds that there has been no Code breach, the

determination of FOS is final and the CCMC cannot investigate the matter. FOS

must inform the CCMC of its decision and provide access to its case file if required by

the CCMC.

c) Where the FOS, in performance of its prescribed function of dispute resolution,

identifies a Code issue, but does not make a determination on this aspect of the

dispute, the FOS must refer the issue to the CCMC and provide access to its case file

if required by the CCMC.

d) Except where the FOS, in performance of its prescribed function of dispute

resolution, identifies a Code issue and determines whether there has been a Code

breach, in all other cases the CCMC shall have sole responsibility to make a

determination whether a breach of the Code has occurred.

e) If a customer seeks to refer a dispute to the FOS alleging a breach of the Code but

there is no financial loss, the FOS must advise the customer of the right to take the

matter to the CCMC.

f) Where the CCMC, in accordance with its prescribed function of Code compliance

monitoring, determines whether a breach of the Code has occurred, that

determination is a final determination as between the CCMC and the FOS as to

whether a Code breach has been established.

g) There will be free flow of information between the FOS and the CCMC to enable the

FOS and the CCMC to perform and discharge their respective functions properly.

16. That the FOS and the CCMC ensure that the community is aware of the CCMC‟s

existence, role and separate function in relation to compliance monitoring and establish

a Memorandum of Understanding that sets out their respective roles, agreed protocols

for handling Code matters, and protocols for the sharing of information.

17. That staff at FOS and the CCMC be jointly trained on the distinction between the dispute

resolution function of the FOS and the compliance monitoring function of the CCMC

and the protocols for handling matters including the referral of matters from the FOS to

the CCMC and the sharing of information in accordance with the MOU between the

FOS and CCMC.

Review of the Code of Banking Practice, Final Report, December 2008

17

18. That the description in clause 34(a) (i) of the Code of the bank appointed member of the

CCMC be amended to make it clear that the appointee is a representative of Code

subscribing banks.

FEES AND CHARGES – New Provision

19. That a new clause on „exception fees‟ be included in the Code that commits banks to:

a) Disclosure of exception fees in relation to the products to which such fees apply;

b) Publication of facts sheet on exception fees on the ABA‟s website;

c) Provision of information on how customers can avoid „exception fees‟;

d) Provision of information on accounts or facilities which have minimal or no

exception fees;

20. That reference to „standard fees and charges‟ in the Code be replaced by „fees and

charges‟.

21. That Clause 40 be amended to replace the reference to „standard fees and charges‟ with

„fees and charges‟.

22. That the definition of „fees and charges‟ in clause 40 includes „standard fees and

charges‟ and „exception fees‟ disclosed in accordance with legislative requirements.

23. That the definition of „standard fees and charges‟ in clause 40 be retained.

24. That the definition of „exception fees‟ in Clause 40 include overdrawn fees, over-limit

fees on overdrafts and credit cards, credit card late payment fees, dishonoured cheques,

direct debit items and ATM failed transaction costs.

REVERSE MORTGAGES – New Provision

25. That a new clause be introduced in the Code to govern equity release products, also

commonly referred to as reverse mortgages. This clause should commit subscribing

banks and their agents to compliance with the SEQUAL Code.

DIRECT DEBITS - Clause 29

26. That clause 19 of the Code be expanded to include reference to a variation of direct debit

arrangement as distinct from cancellation of direct debit payments along the following

lines:

a) We will take, by telephone or in writing, and promptly process your:

instruction to cancel a direct debit request relevant to a banking service we provide to

you; and

complaint that a direct debit was unauthorised or otherwise irregular,

b) We will not direct or suggest that you should first raise any such request or complaint

directly with the debit user (but we may suggest that you also contact the debit user).

c) Where you wish to change the terms of a direct debit arrangement with a merchant,

as distinct from seeking to cancel a direct debit facility, you will need to contact the

merchant directly to make the change.

Review of the Code of Banking Practice, Final Report, December 2008

18

27. That staff are trained in the provisions of Clause 19 including:

a) the distinction between cancellation of direct debits and changes to the terms of direct

debit arrangements; and

b) the need to process cancellation requests and complaints promptly in order to avoid

the possibility of the customer‟s banking facility becoming overdrawn and incurring

exception fees due to the continuing payment of the direct debit facility.

ACCOUNT SWITCHING – New Provision

28. That the Code include a new provision on switching accounts for personal customers.

29. That the new Code provision on switching accounts reflect the four key principles

announced by the ABA on 9 February 2008 and available on the ABA website with a

focus on:

a) Obligations of the old financial institution to provide a list of the customer‟s direct

debit and credit arrangements over the past 13 months to the customer in order to

facilitate the establishment of the arrangements for the new account;

b) Obligations of the new financial institution to provide the customer with information

and support to help the customer make the switch. If requested by the consumer, the

new financial institution will assist in notifying the Direct Entry users of the new

direct debit and direct credit arrangements and assist with closing the customer‟s old

bank account;

c) Obligations in regards to timeliness, the provision of information to customers on

how to avoid exception fees, and dealing fairly with customers throughout the

account switching process;

d) Provision of quarterly progress reports to the Government.

30. That the Code include a provision that banks will publish their account switching

arrangements on the ABA website and on their individual websites.

ELECTRONIC BANKING - Clause 33

31. That Clause 33 be simplified, taking into account the proposed revisions to the Electronic

Funds Transfer Code by ASIC, with a focus on:

a) Providing customers with the option of receiving material electronically if it is

available;

b) Notifying customers by electronic communication when and how information can be

retrieved electronically;

c) Incorporating electronic communication as a product feature and including this in

any product disclosures

d) Providing information electronically in a form that allows the customer to retain it;

and

e) Protecting customers from ‟phishing‟ by including a commitment that customers will

not be sent an email or SMS message requesting them to reply via the same electronic

Review of the Code of Banking Practice, Final Report, December 2008

19

communication channel or to click on a hyperlink and provide information on their

account details, financial details, login or other security password details

32. That the relationship between the Code of Banking Practice, EFT Code and electronic

communication provisions in the Corporations Act and UCCC be clarified and reflected

in the Code based on the following:

a) The EFT Code electronic communication provisions will apply to all transactions

covered by that code;

b) The Code of Banking Practice electronic communications provisions will not apply to

those transactions covered by the EFT Code electronic communications provisions;

c) The Code of Banking Practice will apply to all other electronic communications with

the customer except where the law specifically provides for these circumstances, such

as the UCCC and the Corporations Act.

33. That Clause 39.2 of the Code be relocated to Clause 33 of the Code and amended along

as follows:

To the extent of any inconsistency, this Code is to be read subject to the Electronic Funds

Transfer Code of Conduct and the electronic communications provisions in the

Corporations Act 2001 and UCCC.

COMMUNICATION – New Provision

34. That a key commitment to communicate with customers and their representatives in a

timely and courteous manner be included in the current Clause 2 of the Code, Our key

commitments to you, along the following lines:

We will communicate with you and/or your representatives in a timely and courteous

manner, whether by telephone or in written communications including electronic

communications.

ACCOUNT SUITABILITY - Clause 14

35. That clause 14 of the Code be amended along the following lines:

a) If you tell us that you are a low income earner or a disadvantaged person (regardless

of whether you are an existing or prospective customer but not if you are a small

business), we will provide you with details of accounts which may be suitable to your

needs. Depending on your needs this information may include details of accounts

which attract no or low fees and charges and how you can avoid incurring exception

fees.

b) If you ask for this information or if, in the course of dealing with you, we become

aware that you are in receipt of Centrelink or like benefits, or assess that your needs

are suited to an account which attracts no or low fees and charges, we will provide

you with factual information about these accounts.

c) We will publish information about accounts which attract low or no fees or charges

on our website or through other means.

Review of the Code of Banking Practice, Final Report, December 2008

20

36. That a definition of „low income earner‟ be included in the definitions in clause 40 of the

Code to include persons receiving Centrelink or like benefits and persons meeting the

Australian Bureau of Statistics definition of „low income earner‟.

37. That account suitability provisions for Indigenous customers be included in a general

commitment in the Code in relation to the provision of appropriate banking services to

Indigenous communities, particularly those in remote locations.

DISCLOSURES - TERMS AND CONDITIONS - Clauses 10 and 13

38. That clause 10 be simplified to clarify and eliminate any overlap or duplication with

other Code provisions.

39. That the review of Clause 10 be informed by the work of the Australian Government

Financial Services Working Group looking at the length, complexity and readability of

disclosure documentation in financial services.

40. That clause 10.2(e) of the Code be amended to incorporate all of the provisions of clause

13 of the Code, thus removing overlap and duplication as follows:

(e) inform you that, at your request, we will provide you with general descriptive

information about our banking services, including where appropriate:

- our account opening procedures;

- our obligations regarding the confidentiality of your information;

- complaint handling procedures;

- bank cheques;

- informing us promptly when you are in financial difficulty;

- your taking care to read the terms and conditions of your banking service(s); and

- cheques, if your account provides cheque access, including:

- cheque clearance times;

- the effect of crossing a cheque; explaining what “not negotiable” and “account payee

only” mean and the effect of deleting “or bearer” on a cheque where these words

appear on a cheque;

- stopping payment on cheques;

- reducing the risk of unauthorised alteration of a cheque you write;

- cheque dishonour;

- post dated cheques; and

- stale cheques.

41. That clause 13 of the Code be deleted.

Review of the Code of Banking Practice, Final Report, December 2008

21

COMPLIANCE WITH LAWS - Clause 3

42. That clause 3.1 of the Code in relation to compliance with laws be retained.

43. That clause 34 of the Code be amended to make it clear that the functions of the CCMC

do not extend to compliance monitoring, investigation of allegations of a breach and

reporting of clause 3.1 unless they are also breaches of other provisions in the Code.

KEY COMMITMENTS – Clause 2

44. That the Code make it clear that the provisions of clause 2 of the Code, Our Key

commitments to you are general guiding principles and should be interpreted by

reference to the relevant more detailed code provisions.

45. That Clause 34 of the Code be amended to make it clear that the functions of the CCMC

do not extend to compliance monitoring, investigation of allegations of a breach and

reporting in relation to clause 2 of the Code unless they are also breaches of other

provisions in the Code.

COPIES OF DOCUMENTS - Clause 11

46. That clause 11.2 be amended to include reference to legislative requirements as follows:

At your request, we will give you documents we have in accordance with legislative

regimes for the retention of documents, relating to a banking service you have, or had,

with us: followed by existing clauses 11.2(a), 11.2(b), 11.2(c) and 11.2(d).

OPENING OF ACCOUNTS - Clause 16

47. That Clause 16 of the Code be amended to include reference to Anti Money Laundering

and Counter Terrorism Finance legislation.

48. That customer identification issues faced by remote Indigenous communities be

addressed in a general commitment in the Code in relation to the provision of

appropriate banking services to Indigenous communities, particularly those in remote

locations.

CHANGES TO TERMS AND CONDITIONS - Clause 18

49. That clause 18.1 of the Code be amended to:

a) include the use of electronic communication to meet the notification requirements of

the information prescribed in this Clause; and

b) include an additional exception in the clause that the requirement to provide at least

30 days notice does not apply where the change is beneficial to the customer or in

other circumstances consistent with the legislative regime relating to the notification

of changes of terms and conditions.

50. That the ABA continue to pursue discussions with ASIC relating to consistency of

legislative and regulatory provisions in relation to notification of changes to terms and

conditions.

Review of the Code of Banking Practice, Final Report, December 2008

22

CHARGEBACKS - Clause 20 and Clause 10

51. That Clause 20(d) is amended to include additional means of providing the annual

information on chargebacks, such as by Internet, websites or other electronic means as

follows:

(d) include general information about chargebacks with credit card statements at least

once every 12 months including by access to our website or other electronic

communications in accordance with the electronic communication provisions of this

Code.

52. That clause 10.5(b) of the Code be amended to include reference to timeframes set by

credit card providers as follows:

(b) a prominent statement of the time frames within which you should report a disputed

transaction (so that we may reasonably ask for a chargeback where such a right exists

and within the timeframes set by the relevant credit card provider) and a note to the effect

that, where the Electronic Funds Transfer code of conduct applies, there may be no such

time frames in certain circumstances; and

PRIVACY AND CONFIDENTIALITY - Clause 22

53. That any changes to Clause 22 be considered in the context of the report by the

Australian Law Reform Commission into privacy legislation.

54. That the proposed principles on privacy suggested by consumer advocates be taken into

account in reviewing clause 22 in the context of the report by the Australian Law Reform

Commission into privacy legislation.

STATEMENT OF ACCOUNTS - Clause 24

55. That Clause 24 of the Code be aligned with the relevant EFT Code provisions when they

are finalised.

56. In the interim clause 24.1 of the Code be amended to include a new paragraph (e)

(e) where the transaction information has already been provided to you by other means.

ADVERTISING - Clause 30

57. That clause 30 on Advertising be retained in the Code.

58. That clause 30.1 be amended to include reference to legislative requirements in relation

to advertising by banks as follows:

We will ensure that our advertising and promotional literature drawing attention to a

banking service is not deceptive or misleading in accordance with legislative

requirements.

INTERNAL AND EXTERNAL DISPUTE RESOLUTION - Clauses 35,

36 and 37

59. That clause 35.1 (b) in relation to internal dispute resolution standards be amended to

read as follows:

Review of the Code of Banking Practice, Final Report, December 2008

23

(b) meet the standards set out in any internal complaints handling standard or guideline

that ASIC declares is to apply to this Code;

60. That clause 36 (b) in relation to external dispute resolution policy statements or

guidelines be amended to read as follows:

(b) consistent with any external dispute resolution standard or guide that ASIC declares

is to apply to this Code.

61. That clause 35.1 (a) be amended as follows:

a) be free and accessible.

62. That any additional legal or other costs which may be incurred and/or imposed on

customers by banks should be reasonable having particular regard to the impact on

customers experiencing financial difficulties.

APPLICATION AND TRANSITIONAL PROVISIONS - Clause 39

63. That clause 39 be amended to reflect the changes in the Code following this review,

making it clear that subscription to the Code means subscription to the entire Code.

64. That the application and transitional provisions clarify that the requirement for third

party debt collectors and finance and mortgage brokers to be members of an ASIC

approved EDR scheme, as recommended by the review:

a) apply to any new contracts entered into after the commencement date of the new

Code; but

b) do not apply retrospectively to contracts which have been signed prior to the

commencement of the new Code and the terms of which extend beyond the

commencement date of the new Code.

CUSTOMERS IN REMOTE INDIGENOUS COMMUNITIES – New

Provision

65. That the Code include a new clause on Customers in Remote Indigenous Communities.

66. That the new clause on Customers in Indigenous Communities records the support of

subscribing banks to the Indigenous Commitment Statement and incorporates principles

in relation to the provision of appropriate banking services to customers in remote

Indigenous communities where such services are currently provided, taking into account

the following issues:

a) Provision of information and communication with customers in indigenous

communities;

b) Account suitability for customers in remote indigenous communities;

c) Identification issues relating to the opening of accounts for customers in remote

Indigenous communities;

d) Indigenous cultural and community awareness training for staff operating in

indigenous communities;

Review of the Code of Banking Practice, Final Report, December 2008

24

e) The implications of government programs such as income management programs on

the provision of banking services and products in remote indigenous communities.

LANGUAGE AND STRUCTURE OF THE CODE

67. That the language of the revised Code be simplified and less formal.

68. That the structure of the Code be amended to link related topics more closely together in

the Code.

69. That the Code be drafted in a way that will keep pace with rapid developments in the

consumer and financial regulatory environments.

STAFF TRAINING AND COMPETENCY - Clause 7

70. That clause 7 (a) of the Code be amended to make explicit reference to compliance with

the Code as follows:

can competently and efficiently discharge their functions and provide the banking

services they are authorised to provide in compliance with the Code; and

71. That clause 7 (b) of the Code be amended to include reference to the practical

application of the Code to banking transactions and services as follows:

have an adequate knowledge of the provisions of this Code and its application to banking

transactions and banking services.

UNFAIR CONTRACT TERMS

72. That the issue of the inclusion of unfair contract terms in the Code be considered in the

context of the proposed national regulation of consumer credit.

ACCOUNT COMBINATION- Clause 17

73. That clause 17 of the Code be amended to make it clear that banks will not exercise their

right to combine accounts:

a) While the bank is considering an application for financial hardship assistance in

accordance with the financial hardship provisions of the Code, subject to the

customer‟s agreement that funds in another account (s) can be held by the bank until

a decision is made to approve or decline the application for assistance; or

b) While the customer is complying with an agreed repayment arrangement under the

financial hardship provisions of the Code.

USE OF FINANCE AND MORTGAGE BROKERS

74. That the requirement that banks only use Finance and Mortgage Brokers who are

members of an ASIC approved EDR scheme be considered in the context of the

development of national legislation on finance broking.

Review of the Code of Banking Practice, Final Report, December 2008

25

PROMOTION OF THE CODE – Clause 9

75. That clauses 9 (a) and (c) of the Code be amended to include a commitment by

subscribing banks to prominently display a copy of the Code at their branches and on

their websites.

Review of the Code of Banking Practice, Final Report, December 2008

26

CHAPTER 1 - INTRODUCTION

1.1 Appointment of the Review

I was appointed by the Australian Bankers‟ Association (ABA) on 29 November 2007 to

conduct a review of the Code of Banking Practice (Code). The commencement of the review

was publicised in a press release issued by the ABA on 21 December 2007 and by letters sent

by me on 3 January 2008 to consumer representatives, Chief Executives of State Government

Departments of Fair Trading, Commonwealth regulatory agencies and industry associations

and other organisations that might have an interest in the review.

1.2 The Code of Banking Practice

The Code of Banking Practice is a voluntary code of conduct which sets standards of good

banking practice for banks to follow when dealing with individual and small business

customers and their guarantors. The Code was first published in November 1993, and with the

agreement of the Federal Treasurer, became fully operative from 1 November 1996.

Clause 5 of the Code prescribes that the ABA is to commission an independent and transparent

review of the Code at least every 3 years in consultation with: banks which adopt the Code;

consumer organisations; other interested industry associations; relevant regulatory bodies; and

other interested stakeholders.

The first review of the Code was undertaken in 2000 and 2001. The current version of the

Code, which was published in May 2004, reflects the outcomes of the extensive consultation

undertaken during the first review of the Code.

1.3 Terms of Reference

The terms of reference for the review are set out in full at Appendix A of the Issues Paper,

which I published on 28 May 2008.

1.4 Approach

1.4.1 Preparation for the Review

On 16 May 2007 the ABA advised consumers, regulators and stakeholders of the forthcoming

review of the Code and sought their views on the scope of the review and the issues to be

considered by the review. Ten organisations responded identifying issues and providing

comments and suggestions on proposed amendments to the Code. Copies of this

correspondence were provided to me at the time of my appointment to provide a context to the

review and to assist me in shaping the review methodology.

Review of the Code of Banking Practice, Final Report, December 2008

27

At the time of my engagement, the ABA arranged for me to meet with members of the ABA‟s

Community and Consumer Consultative Forum1 (Consultative Forum) and with representatives

of Code subscribing banks to seek their views on relevant issues and to consult with them on

the proposed methodology and timeframe for the review.

Because of the strong foundation established by the previous review of the Code, consumer

advocates, regulators and banks were generally of the view that the current Code does not need

to be changed significantly. Nonetheless, they acknowledged that the current review provides

an opportunity to review the provisions of the Code in the context of legislative, economic,

social and technological changes which have occurred since the previous review.

1.4.2 Announcement of the Review

The commencement of the review was publicised in a press release issued by the ABA on 21

December 2007.

On 3 January 2008 I wrote to consumer representatives, Chief Executives of State Government

Departments of Fair Trading, Commonwealth regulatory agencies, industry associations and

other persons and organisations who might have an interest in the review advising them of the

commencement of the review and inviting submissions and consultations with them on issues,

comments and suggestions.

A Code Review website was established in April 2008. The website included a copy of the

current Code, the terms of reference of the review, copies of press releases and updates on the

review process. Major submissions received during the review process were also published on

the website.

1.4.3 Consultations

Between January and May 2008 I held meetings and discussions with consumer advocates,

financial counselling organisations, government departments, industry associations, interested

organisations and individuals. I also met with representatives of Code subscribing banks and

attended presentations and discussions on aspects of banking practice organised by individual

subscribing banks.

1.4.4 Initial Submissions

A number of organisations indicated that they would not be making written submissions to the

Review until after the release of the Issues Paper. Others chose to make submissions outlining

issues identified during consultations with me. Sixteen submissions were received (ten from

organisations and six from individuals). Seven submissions from organisations were published

on the website with the permission of those organisations.

1.4.4 Review of Documentation

In addition to extensive consultation with organisations and individuals, I undertook a review

of documentation on banking and related practices overseas and in other sectors, legislative and

1 Established under Clause 5.3 of the Code

Review of the Code of Banking Practice, Final Report, December 2008

28

regulatory changes and decisions of courts, regulators and dispute resolution bodies which

might impact on the Code.

1.4.5 Attendance at Forums

During the course of the review, I attended forums organised by the Australian Securities and

Investment Commission (ASIC), the Australian Competition and Consumer Commission

(ACCC) and the ABA on issues relevant to the Code review. These included an ASIC Remote

Lending Forum on 13 March 2008, a forum on financial hardship organised by the ABA on 2

May 2008, an ACCC/ASIC Debt Collection Forum on 5 September 2008 and a number of

meetings of the Consultative Forum.

1.4.6 Issues Paper

On 28 May 2008 I published an Issues Paper that identified key issues raised by consumer

advocates, financial counsellors, regulators, banks and individuals in submissions and

consultations. The Issues Paper made a number of interim recommendations in relation to

these issues. Responses to the Issues Paper were invited by 9 July 2008. At the request of

stakeholders, this date was extended to 31 July 2008.

Twenty five submissions were received in response to the Issues Paper. Twenty four

submissions received in response to the Issues Paper were published on the Code review

website in early August 2008.

1.4.7 Final Report

Following receipt of submissions in response to the Issues Paper, I undertook an analysis of the

respective positions of consumer advocates, regulators, banks and industry representatives on

key issues and others identified by them in their submissions and continued to hold

consultations with interested parties.

Having carefully considered the various views and submissions put to me, I developed a set of

recommendations which I proposed to include in my final report. These were provided to the

ABA, consumer advocates, ASIC, the New South Wales Office of Fair Trading (NSW OFT),

the Financial Ombudsman Service (FOS) and the Code Compliance Monitoring Committee

(CCMC) on 20 November 2008 for comment and discussion prior to the finalization of my

report. Their comments and discussions on the proposed recommendations have been helpful

to me in finalising my recommendations in the Final Report.

1.5 Structure of the Report

This report is intended to be read in conjunction with the Issues Paper. For ease of reference,

the Final Report follows a similar format to the Issues Paper.

The key and most contentious issues identified by consumer advocates, regulators and

banks are discussed at the beginning of the report.

The report then discusses a range of other issues identified in submissions and consultations

that require attention to reflect changes in the regulatory environment or banking practice.

The report also includes discussion on a number of additional issues that were not included

in the Issues Paper but were raised in the JCS in response to the Issues Paper.

Review of the Code of Banking Practice, Final Report, December 2008

29

For each issue, the report provides a brief outline of what the Issues Paper recommended, the

responses to the Issues Paper, my assessment of the various perspectives on the issue and

recommendations. The report identifies the relevant clause(s) of the Code in discussing each

issue. The report also identifies where there is currently no Code provision in relation to a

particular issue.

A consolidated set of recommendations is included at the commencement of the report.

1.6 Acknowledgements

I would like to thank the many organisations and individuals who have contributed to the

review2. They have been most generous in giving their time and in sharing information,

insights and suggestions on the Code and related banking standards and services. They have

approached the consultations in a spirit of cooperation and with a genuine desire to achieve a

Code that works effectively for banks and consumers and contributes to the economic and

social wellbeing of Australia.

I also wish to acknowledge the outstanding work of the previous Code reviewer, Mr Richard

Viney, in establishing a strong base and platform for the current review. His support and

assistance to me during the review process have been greatly appreciated.

2More than one hundred and fifty individuals and over sixty organisations have contributed to the review by

submissions, consultation and correspondence.

Review of the Code of Banking Practice, Final Report, December 2008

30

CHAPTER 2 - CONTEXT

2.1 Economic and Regulatory Changes

The review has been undertaken at an unprecedented time in Australia‟s financial and

economic history. The global economic downturn has created uncertainty for banks in respect

to the availability of finance and the cost of borrowing and has had a significant impact on the

financial situation of individual consumers. At the same time there has been a strong focus on

national regulation of the financial services sector.

The Issues Paper discussed changes in the global economic and national financial regulatory

environments and their impact on the Code of Banking Practice3. Developments in the

financial services regulatory environment in Australia since the previous review of the Code

include;

Anti-Money Laundering and Counter-Terrorism Financing Act 2006;

The Australian Government Productivity Commission‟s Inquiry into Australia‟s

Consumer Policy Framework 2007-2008 and the proposed national regulation of

consumer credit;

The Australian Law Reform Commission Review of Privacy Legislation;

Projects sponsored by the Ministerial Council of Consumer Affairs on matters such as

responsible lending; proposed legislative amendments in relation to fringe lending;

reverse mortgages; and unfair contract provisions;

The Senate Economic Committee‟s review of the Australian Securities and Investment

Commission (Fair Bank & Credit Card Fees) Amendment Bill 2007;

ASIC‟s review of online financial services disclosures;

The development of a new ASIC dispute resolution standard;

The merger of Financial Ombudsman Services;

Account switching;

The establishment of a Financial Services Working Group to look at the current key

issues associated with financial services advice and disclosure.

Reviews of other Codes of Practice and the development of new codes of Practice in the