Institutional EYE IiAS Comment | 18 February 2016

1 iias.in February 2016

Subscribe to IiAS Research Related Research Royalty flows in Suzuki’s

blood

Paying the price Multinationals Royalty Payments and Minority Shareholders

Royalty runs in MNCs bloodstream

Royalty payments and Minority Shareholders

Write to us [email protected]

Focus

First Reaction

Governance Spotlight

Regulatory Overview

Thematic Research Event Based Research

General

Royalty continues to outpace profits; shareholders must demand a greater say IiAS’ study of the 32 MNCs in the BSE500 shows that in FY15 they paid royalty aggregating Rs. 63 bn or ~21% of their pre-royalty pre-tax profits, to their global parent. While royalty is a legitimate payout, IiAS believes these must be linked to performance: yet, royalty and related payments for these companies increased at twice the rate of the growth in their pre-royalty pre-tax profits over the past five years. IiAS believes that regulations must compel all royalty, like other related party payments be approved by shareholders, pushing companies to explain their basis of charging royalty.

Royalty has been a contentious issue for MNCs set up in India. In FY15, 32 MNCs1 paid out an aggregate Rs. 63 bn, which was almost 21% of their pre-royalty pre-tax profits – a growth of 10% over FY14 levels. MNCs based in India pay royalty because they use brands/technology know-how that have been developed outside India by their global parents and are a result of extensive product research and knowledge. Therefore, royalty is a legitimate payout – but, how much is the right amount? Chart 1: Growth in royalty payments has outpaced sales and profits growth for the 32 MNCs

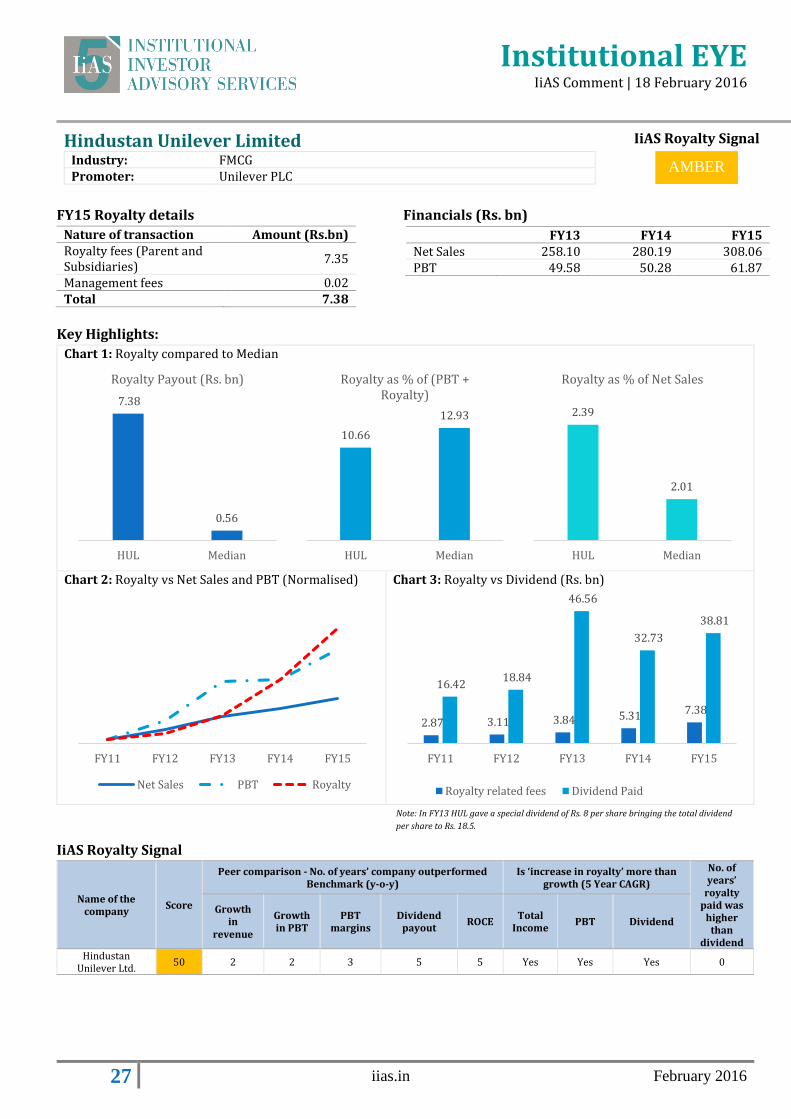

Our study of the 32 MNCs in the BSE 500 shows that over the past five years, aggregate royalty and related payments for these MNCs increased at a five-year CAGR of ~20% compared to a mere ~7% growth in their pre-royalty pre-tax profits. The steady increase in royalty payouts can be largely attributed to a change in regulations in December 2009 (Refer Annexure A), which liberalized the payment of foreign technology collaborations and royalty fees under the automatic route (including lump sum payments for transfer of technology, payments for the use of trademark and brand name). Maruti, HUL, ABB2, Nestlé2 and Bosch2 have paid out the maximum amount as royalty in the past three years: aggregate royalty payouts of these five companies was Rs. 47.8 bn or ~24% of aggregated pre-royalty pre-tax profits (up from Rs. 43.6 bn in the previous corresponding year). In fact, Maruti’s and ABB’s royalty payouts aggregated over 30% of their pre-royalty pre-tax profits in FY15.

1 See methodology on page 39 for the selection process of these 32 MNCs 2 December year end – refers to data for financial year ended 31 December 2014

FY11 FY12 FY13 FY14 FY15

Sales PBT+Royalty Royalty

Institutional EYE IiAS Comment | 18 February 2016

2 iias.in February 2016

IiAS Royalty Signal 1 B A S F India Ltd.

2 Schneider Electric Infrastructure Ltd.

3 3M India Ltd.

4 Alstom T & D India Ltd.

5 Heidelberg Cement India Ltd.

6 Hitachi Home & Life Solutions (India) Ltd.

7 S K F India Ltd.

8 United Spirits Ltd.

9 A B B India Ltd.

10 Whirlpool of India Ltd.

11 A C C Ltd.

12 Akzo Nobel India Ltd.

13 Alstom India Ltd.

14 Ingersoll-Rand (India) Ltd.

15 Maruti Suzuki India Ltd.

16 Ambuja Cements Ltd.

17 Bosch Ltd.

18 Colgate-Palmolive (India) Ltd.

19 F A G Bearings India Ltd.

20 Gillette India Ltd.

21 Grindwell Norton Ltd.

22 Hindustan Unilever Ltd.

23 Nestlé India Ltd.

24 Cummins India Ltd.

25 Wabco India Ltd.

26 Bata India Ltd.

27 Novartis India Ltd.

28 Castrol India Ltd.

29 Kansai Nerolac Paints Ltd.

30 Timken India Ltd.

31 Glaxosmithkline Consumer Healthcare Ltd.

32 Procter & Gamble Hygiene & Health Care Ltd.

Performance alone should be the benchmark for royalty payments Royalty payments could have been justified had the 32 MNCs in our research outperformed BSE 200 companies with respect to sales growth or earned higher margins. However, this is not the case. The BSE 200 companies have reported better growth and margins (please refer Table 1 and Table 2) than these 32 MNCs in FY15. This begs the question, what are companies paying for if their local competitors are growing faster and earning better margins?

Table 1: BSE 200 vs. 32 MNCs

5 year CAGR (2011-2015) Revenue growth PBT growth

BSE 200 13.5% 8.4%

32 MNC's 12.1% 5.6%

Table 2: BSE 200 vs. 32 MNCs (margins comparison)

PBT Margins (median) 2011 2015

BSE 200 15.3% 12.7%

32 MNC's 13.9% 11.5%

IiAS believes good governance practices require royalty payouts to be considered, and perhaps tempered in case of weak performance. Novartis is the only of the 32 MNCs that reduced royalty by 21%, after its FY15 profits were lower by 20% over the previous year. What will Nestlé Limited (Nestlé India) do? Nestlé terms of royalty include a steady step-up of royalty percentages by 0.2% of sales annually beginning 1 January 2014. The Maggi noodle controversy led to a negative impact of ~Rs.5.0 bn on Nestlé India’s profitability in CY15. Shareholders will know only after the company publishes its 2015 annual report. Royalty Signal To assess the appropriateness of royalty payouts, IiAS has developed the “IiAS Royalty Signal”. The model assesses the appropriateness of royalty payout levels and includes measuring royalty payouts in context of revenues, margins and dividend. Based on the overall score, companies are categorised into three buckets: green, amber and red (please refer to Annexure B for scoring; Annexure C for methodology). Based on the analysis, IiAS finds some similarities in companies categorized within a bucket:

1. Red: These companies have (i) performed weaker than peers in the BSE 200, (ii) have royalty payouts higher than dividends and (iii) royalty has grown faster than revenues and profits.

2. Amber: For most of these companies, (i) dividend payouts have been higher than royalty payouts over the past five years and (ii) royalty continues to outpace the increase in sales and/or profits.

3. Green: All the companies in this category have (i) paid dividends higher than royalty over the past five years, (ii) royalty increasing at a slower pace than sales and profits and (iii) performed better than peers in BSE 200.

We first looked at royalty payments in December 2012 and introduced the royalty signal in 2013 (based on FY13 financial statements). Our updated analysis (based on FY15 financials), shows:

Institutional EYE IiAS Comment | 18 February 2016

3 iias.in February 2016

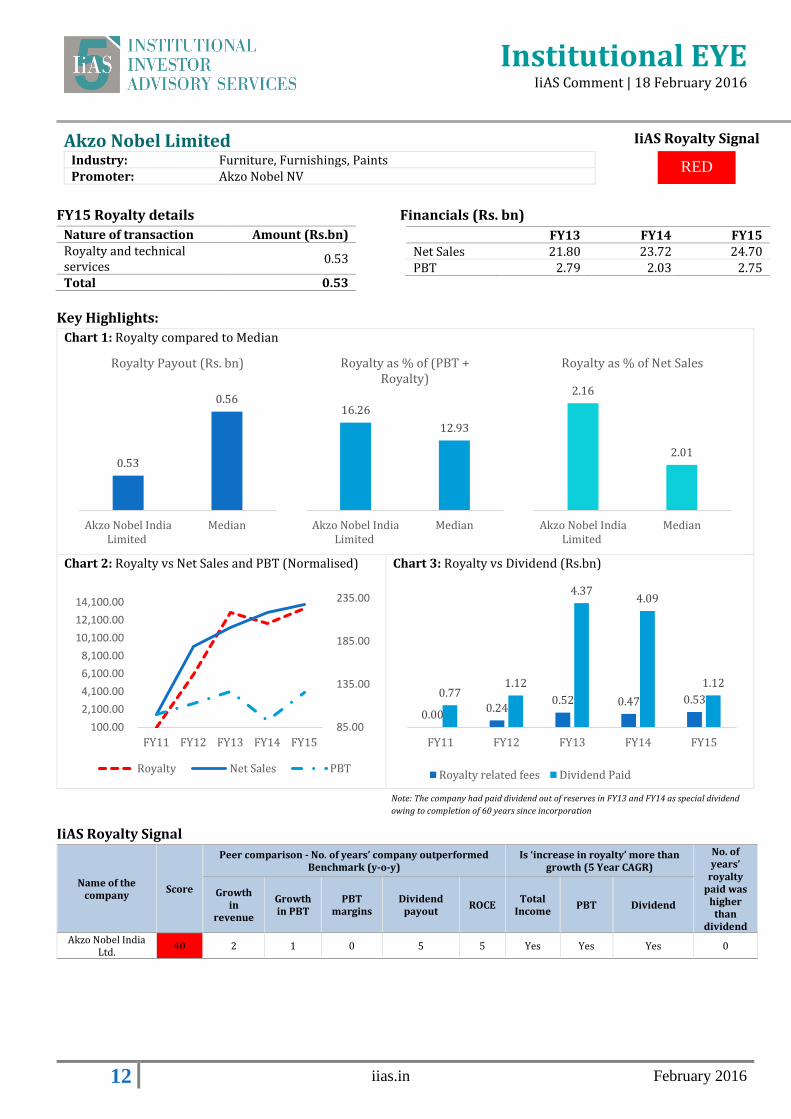

a. Disproportionate increase in royalty (5 year CAGR) compared to revenues/profits/dividends has led Akzo Nobel, Alstom India and SKF India moving to red bucket (amber last year) and Cummins India to amber (green last year).

b. FAG Bearings and Bosch have improved on their position to amber (red last year) owing higher growth in sales viz-a-viz royalty.

c. Timken India has moved to green (amber last year) as performance outpaced the growth in royalties in FY15.

Detailed company profiles are given in Annexure D. Poor disclosure levels continue to keep a veil on royalty and related payments Companies do not explain the basis of charging royalty. If the terms of royalty are changed, the revised royalty percentages are announced. But how are these arrived at since the actual benefits of future R&D on company’s products cannot be quantified at the time of the agreement? How did the companies establish that these are being paid at arm’s length? Maruti, for example, has flip flopped on royalty payouts a number of times in the past few years in order to accommodate Suzuki’s demands. For instance, they increased royalty payouts to account for the Rupee-Yen exchange rate fluctuations: but why did Maruti’s board cave into absorbing all the exchange losses? Usually royalty expenses are disclosed in the annual report, and not necessarily when the amount is increased. Therefore, shareholders become aware of the actual quantum of payout only after the expense has been incurred. For example, to know if Nestlé India has paid royalty at a higher rate3, shareholders will have to wait till the company publishes its 2015 annual report. Although royalty to the global parent is a related party transaction, under current regulations, such transactions do not need shareholder approval. In order to push companies to explain the basis of their charging royalty and be more considered in their royalty payouts, IiAS believes these payments must be brought under the ambit of shareholder approval. Until then, investors must engage with MNCs in India and actively push them to rationalize royalty payouts. Box 1: Royalty payments do not usually require shareholder approval

d.

3 Nestlé’s terms of royalty include a steady step-up of royalty percentages by 0.2% of sales annually beginning 1 January 2014

Investors must engage with companies to understand the terms and conditions based on which royalty is being paid. Royalty payments, although these are with related parties, are not presented to shareholder for a vote because:

Companies classify these as transactions in the ordinary course of business, and claim that these are being paid at arm’s length pricing: under Companies Act 2013, such transactions do not need shareholder approval.

Since the transaction value is rarely over 10% of revenues or networth, shareholder approval under SEBI’s Listing Obligations and Disclosure Requirements (LODR) Regulations, 2015 is also not required.

Institutional EYE IiAS Comment | 18 February 2016

4 iias.in February 2016

Exhibit 1*: 5 Year CAGR (Royalty vs. Royalty + PBT)

*excludes United Spirits Ltd (5 year CAGR Royalty: 58%; PBT + Royalty: -228%

Maruti

HUL

ABB

Nestlé Bosch

Colgate

GSK Consumer Healthcare

ACC

P&G

Ambuja

3M

Castrol

Alstom T&D

SKF

Cummins

Akzo Nobel

Alstom India

Schneider Electric

Whirlpool

Hitachi

BASF

FAG Bata

Timken

Heidelberg

Wabco

Nerolac

Gillette

Grindwell Norton

Ingersoll Rand

Novartis

-10.0%

10.0%

30.0%

50.0%

70.0%

90.0%

110.0%

-30.0% -20.0% -10.0% 0.0% 10.0% 20.0% 30.0%

Ro

yalt

y

PBT+Royalty

Institutional EYE IiAS Comment | 18 February 2016

5 iias.in February 2016

Annexure A: Regulations In the December of 2009, the government of India, through press note 8, liberalized the payment of foreign

technology collaborations and royalty fees under the automatic route (including lump sum payments for transfer

of technology, payments for the use of trademark and brand name).

The liberalization of the Foreign Technology Agreement Policy was aimed at facilitating inflow of foreign direct

investment and technology transfers into the country. Foreign partners would now no longer have to go through

administrative hoops. Importantly this meant that ‘foreign sponsors’ who earlier required government approval

for charging royalty under the various heads were now free to charge any amount as royalty to their Indian

subsidiaries (refer table 3 below).

Table 3: Restrictions pre and post liberalising royalty payments:

Type of payment

Condition Pre-Press Note 8 (2009 series)

Post-Press Note 8 (2009 series)

Lump sum payments

Under technical collaboration

< US$ 2 million No limit

Royalty payable

Under technical collaboration

8 % on export and 5% on domestic sales

No restrictions - subject to FEMA (Current Account Transactions) Rules, 2000

Royalty payable

For use of trademark and brand name of the foreign collaborator

2% of exports and 1% of domestic sales

No restrictions - subject to FEMA (Current Account Transactions) Rules, 2000

The unintended consequences of waiving restrictions on royalty payments is reflected in the steady increase in

technical know-how, royalty, consultancy fees etc. by foreign partners since 2009, without a commensurate

increase in either sales or margins.

Institutional EYE IiAS Comment | 18 February 2016

6 iias.in February 2016

Annexure B: IiAS Royalty Signal: Snapshot of financial data

Name of the company Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’ royalty paid was higher

than dividend Growth in revenue

Growth in profits

before tax

PBT margins

Dividend payout

ROCE Total

Income Profits

before tax Dividend

B A S F India Ltd. 0 2 1 0 1 1 Yes Yes Yes 4

Schneider Electric Infrastructure Ltd. 0 0 1 0 1 1 Yes Yes Yes 4

3M India Ltd. 10 0 1 0 0 3 Yes Yes Yes 5

Alstom T & D India Ltd. 10 1 1 0 5 0 Yes Yes Yes 5

Heidelberg Cement India Ltd. 10 2 0 0 0 0 No Yes Yes 5

Hitachi Home & Life Solutions (India) Ltd. 20 3 2 0 3 2 Yes Yes Yes 5

S K F India Ltd. 20 1 2 1 3 5 Yes Yes Yes 3

United Spirits Ltd. 20 1 0 0 0 0 Yes Yes Yes 2

A B B India Ltd. 30 0 3 0 5 0 Yes Yes No 5

Whirlpool of India Ltd. 30 2 1 0 0 5 No No Yes 5

A C C Ltd. 40 1 0 1 5 5 Yes Yes Yes 0

Akzo Nobel India Ltd. 40 2 1 0 5 5 Yes Yes Yes 0

Alstom India Ltd. 40 2 1 2 5 5 Yes Yes Yes 0

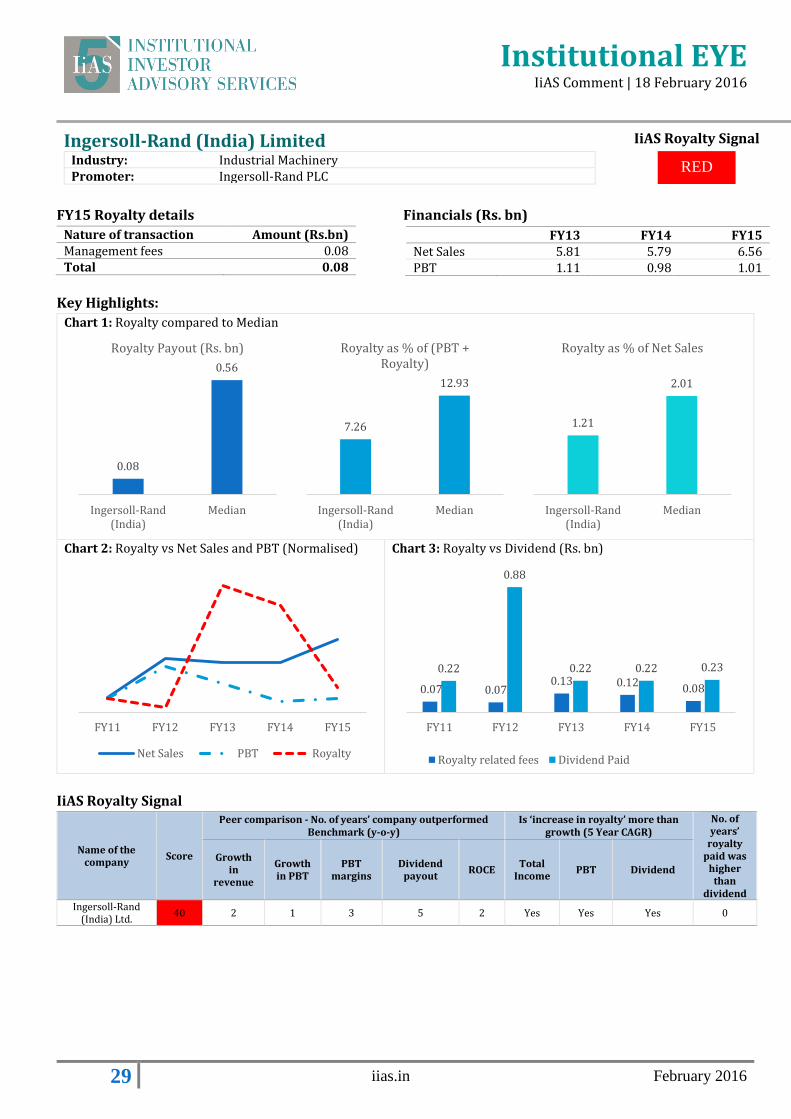

Ingersoll-Rand (India) Ltd. 40 2 1 3 5 2 Yes Yes Yes 0

Maruti Suzuki India Ltd. 40 3 3 0 0 5 Yes Yes No 5

Ambuja Cements Ltd. 50 0 1 3 5 5 Yes Yes Yes 0

Bosch Ltd. 50 2 3 2 1 5 No No No 5

Colgate-Palmolive (India) Ltd. 50 2 0 4 5 5 Yes Yes Yes 0

F A G Bearings India Ltd. 50 3 3 2 0 5 No No Yes 5

Gillette India Ltd. 50 4 2 1 5 4 Yes Yes Yes 0

Grindwell Norton Ltd. 50 1 1 2 5 5 No Yes Yes 0

Hindustan Unilever Ltd. 50 2 2 3 5 5 Yes Yes Yes 0

Nestlé India Ltd. 50 1 1 3 5 5 Yes Yes Yes 0

Cummins India Ltd. 60 2 3 3 5 5 Yes Yes Yes 0

Wabco India Ltd. 60 3 1 3 0 5 No No No 3

Bata India Ltd. 70 3 4 2 1 5 No No Yes 0

Novartis India Ltd. 70 0 1 5 4 4 No Yes No 0

Castrol India Ltd. 80 0 2 4 5 5 No No No 0

Kansai Nerolac Paints Ltd. 80 3 2 0 4 5 No No No 0

Timken India Ltd. 80 3 3 1 4 5 No No Yes 1

Glaxosmithkline Consumer Healthcare Ltd. 90 2 3 3 5 5 No No No 0

Procter & Gamble Hygiene & Health Care Ltd. 90 4 4 3 5 5 No No Yes 0 Source: CMIE, IiAS Research, Company Data

Institutional EYE IiAS Comment | 18 February 2016

7 iias.in February 2016

Annexure C: Methodology

In preparing this report IiAS has relied on data provided by CMIE. FY15 Standalone company data has been used for our analysis. For the purpose of analysis, companies with year ending Dec’14, June’15, and Mar’15 have been represented as FY15 Numbers

Figures are annualized wherever necessary to establish comparability.

Identification of MNCs Filtering Royalty Signal

Companies forming part of BSE 500 were evaluated for foreign parent holding.

For the purpose of this analysis, IiAS defines MNCs as those companies having a foreign parent holding more than 25% of its equity.

Some companies (like Motherson Sumi) who have foreign promoter holding more than 25% but the Indian parent exercises significant control over the company have been excluded.

Any government related organisation/Financial institutions have not been considered for the same.

Companies (like Page

Industries) that pay royalty on

account of franchisee

agreements have also not been

considered.

Companies with a royalty

payment of less than Rs. 60 mn

have been excluded.

Companies that have just begun

to pay royalty have been

excluded because these do not

have sufficient track record of

performance after paying out

royalty. Therefore, only those

companies that have paid

royalty in atleast three of the

last five years have been

considered

All metrics under ‘Peer Comparison’ are assigned a weightage of 10 points. This includes (a) Growth in revenue (b) Growth in profits and (c) ROCE, (d) Dividend Payout and (e) Net Margins. If the company outperformed the benchmark index in three years or more in any of the above metrics, it is assigned 10 points for that metric.

Each parameter under ‘increase in royalty’ is assigned a weightage of 10 points. If the company’s 5 year CAGR in total income, PBT and dividends was higher than the increase in royalty, it is assigned 10 points.

If the company’s dividend was higher than royalty payments in three years or more, it is assigned 20 points. Based on the above, companies scoring 80 points and above are green, 40-70 points amber and 40 and below, red.

<40 50-80

>80

Institutional EYE IiAS Comment | 18 February 2016

8 iias.in February 2016

Annexure D: Company Profiles

Note:

For the Company profiles the median used as a benchmark is the median data of the 32 MNCs covered in our

analysis.

Institutional EYE IiAS Comment | 18 February 2016

9 iias.in February 2016

3M India Limited IiAS Royalty Signal

Industry: Diversified Promoter: 3M Company

FY15 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

3M India Ltd. 10 0 1 0 0 3 Yes Yes Yes 5

0.79

0.56

3M Median

Royalty Payout (Rs. bn)

32.40

12.93

3M Median

Royalty as % of (PBT + Royalty)

4.30

2.01

3M Median

Royalty as % of Net Sales

FY11 FY12 FY13 FY14 FY15

Net Sales PBT Royalty

0.43

0.57 0.64

0.72 0.79

FY11 FY12 FY13 FY14 FY15

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Support services/ Corporate management fee

0.59

Royalty fee 0.20 Total 0.79

FY13 FY14 FY15 Net Sales 15.74 17.42 18.40 PBT 0.75 0.69 1.64

RED

Note: The company incurred high depreciation and finance costs as the company

invested in research and production facilities. High costs along with weak

macroeconomic environment in the country led to a decrease in bottom line in the

past three years.

Institutional EYE IiAS Comment | 18 February 2016

10 iias.in February 2016

ABB India Ltd IiAS Royalty Signal

Industry: Heavy Electrical Equipment Promoter: ABB Limited

CY14 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

A B B India Ltd. 30 0 3 0 5 0 Yes Yes No 5

4.97

0.56

ABB India Limited Median

Royalty Payout (Rs. bn)

58.3

12.93

ABB India Limited Median

Royalty as % of (PBT + Royalty)

6.43

2.01

ABB India Limited Median

Royalty as % of Net Sales

CY10 CY11 CY12 CY13 CY14

Net Sales PBT Royalty

3.10

3.76

4.43 4.67 4.97

0.49 0.74 0.74 0.74 0.94

CY10 CY11 CY12 CY13 CY14

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Royalty, technology and trademark fees

2.66

Expenditure on information technology, management and other services

2.16

Amortised technological know-how fees

0.15

Total 4.97

CY12 CY13 CY14 Net Sales 75.65 77.22 77.33 PBT 2.06 2.72 3.55

RED

Institutional EYE IiAS Comment | 18 February 2016

11 iias.in February 2016

ACC Limited IiAS Royalty Signal

Industry: Cement & Cement Products Promoter: Holcim Limited

CY14 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

A C C Ltd. 40 1 0 1 5 5 Yes Yes Yes 0

1.13

0.56

ACC Limited Median

Royalty Payout (Rs. bn)

9.05

12.93

ACC Limited Median

Royalty as % of (PBT + Royalty)

0.96

2.01

ACC Limited Median

Royalty as % of Net Sales

CY10 CY11 CY12 CY13 CY14

Net Sales PBT Royalty

0.48 0.71 1.00 1.08 1.13

6.686.11

6.55 6.62

7.58

CY10 CY11 CY12 CY13 CY14

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Technology and Know-how fees

1.13

Total 1.13

CY12 CY13 CY14 Net Sales 113.58 111.69 117.38 PBT 14.51 12.27 11.35

RED

Institutional EYE IiAS Comment | 18 February 2016

12 iias.in February 2016

Akzo Nobel Limited IiAS Royalty Signal

Industry: Furniture, Furnishings, Paints Promoter: Akzo Nobel NV

FY15 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs.bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

Akzo Nobel India Ltd.

40 2 1 0 5 5 Yes Yes Yes 0

0.53

0.56

Akzo Nobel IndiaLimited

Median

Royalty Payout (Rs. bn)

16.26

12.93

Akzo Nobel IndiaLimited

Median

Royalty as % of (PBT + Royalty)

2.16

2.01

Akzo Nobel IndiaLimited

Median

Royalty as % of Net Sales

85.00

135.00

185.00

235.00

100.00

2,100.00

4,100.00

6,100.00

8,100.00

10,100.00

12,100.00

14,100.00

FY11 FY12 FY13 FY14 FY15

Royalty Net Sales PBT

0.00 0.24

0.52 0.47 0.530.77

1.12

4.374.09

1.12

FY11 FY12 FY13 FY14 FY15

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Royalty and technical services

0.53

Total 0.53

FY13 FY14 FY15 Net Sales 21.80 23.72 24.70 PBT 2.79 2.03 2.75

RED

Note: The company had paid dividend out of reserves in FY13 and FY14 as special dividend

owing to completion of 60 years since incorporation

Institutional EYE IiAS Comment | 18 February 2016

13 iias.in February 2016

Alstom India Limited IiAS Royalty Signal

Industry: Heavy Electrical Equipment Promoter: ALSTOM S.A.

FY15 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

Alstom India Ltd. 40 2 1 2 5 5 Yes Yes Yes 0

0.49

0.56

ALSTOM India Ltd Median

Royalty Payout (Rs. bn)

15.61

12.93

ALSTOM India Ltd Median

Royalty as % of (PBT + Royalty)

2.32

2.01

ALSTOM India Ltd Median

Royalty as % of Net Sales

FY11 FY12 FY13 FY14 FY15

Net Sales PBT Royalty

0.25

0.41 0.52

0.44 0.49

0.78 0.78 0.78

1.11

0.81

FY11 FY12 FY13 FY14 FY15

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Royalty, Technology Know-how Fees

0.49

Total 0.49

FY13 FY14 FY15 Net Sales 27.86 26.05 21.24 PBT 2.82 3.20 2.66

RED

Institutional EYE IiAS Comment | 18 February 2016

14 iias.in February 2016

Alstom T&D India Limited IiAS Royalty Signal

Industry: Electric Utilities Promoter: ALSTOM S.A.

FY15 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

* Figures have been annualised

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

Alstom T & D India Ltd.

10 1 1 0 5 0 Yes Yes Yes 5

0.70

0.56

Alstom T&D Median

Royalty Payout (Rs. bn)

29.20

12.93

Alstom T&D Median

Royalty as % of (PBT + Royalty)

1.89

2.01

Alstom T&D Median

Royalty as % of Net Sales

FY11 FY12* FY13 FY14 FY15

Net Sales PBT Royalty

0.60

0.45

0.60

0.74 0.70

0.50

0.40

0.50 0.54 0.55

FY11 FY12* FY13 FY14 FY15

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Technology Licence Fee and Others

0.39

Trade Mark Fees 0.31 Total 0.70

FY13 FY14 FY15 Net Sales 31.52 35.24 37.11 PBT 1.22 1.77 1.70

RED

Institutional EYE IiAS Comment | 18 February 2016

15 iias.in February 2016

Ambuja Cements Limited IiAS Royalty Signal

Industry: Cement and Cement Products Promoter: Holcim Limited

CY14 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

Ambuja Cements Ltd.

50 0 1 3 5 5 Yes Yes Yes 0

0.97

0.56

Ambuja CementsLimited

Median

Royalty Payout (Rs. bn)

5.16

12.93

Ambuja CementsLimited

Median

Royalty as % of (PBT + Royalty)

0.97

2.01

Ambuja CementsLimited

Median

Royalty as % of Net Sales

CY10 CY11 CY12 CY13 CY14

Net Sales PBT Royalty

0.48 0.59 0.65 0.90 0.97

4.63

5.706.45 6.47

9.21

CY10 CY11 CY12 CY13 CY14

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Technology & Know How fees

0.97

Total 0.97

CY12 CY13 CY14 Net Sales 97.30 91.60 99.80 PBT 19.02 15.14 17.83

AMBER

Institutional EYE IiAS Comment | 18 February 2016

16 iias.in February 2016

BASF India Limited IiAS Royalty Signal

Industry: Speciality Chemicals Promoter: BASF SE

FY15 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

B A S F India Ltd. 0 2 1 0 1 1 Yes Yes Yes 4

0.41

0.56

BASF Median

Royalty Payout (Rs. bn)

-160.80

12.93

BASF Median

Royalty as % of (PBT + Royalty)

0.91

2.01

BASF Median

Royalty as % of Net Sales

FY11 FY12 FY13 FY14 FY15

Net Sales PBT Royalty

0.24

0.30 0.33

0.35

0.41 0.40

0.20 0.20 0.20 0.21

FY11 FY12 FY13 FY14 FY15

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs. bn) Royalty and technical Fees 0.41 Total 0.41

FY13 FY14 FY15 Net Sales 37.54 42.35 44.70 PBT 1.69 1.94 (0.66)

RED

Note: The commencement of operations at the company’s Dahej plant led to

higher depreciation, interest and start up related costs. This resulted in losses in

FY15.

Institutional EYE IiAS Comment | 18 February 2016

17 iias.in February 2016

Bata India Limited IiAS Royalty Signal

Industry: Footwear Promoter: Bata (BN) BV

FY15* Royalty details Financials (Rs. bn)

* Figures have been annualised

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

* Figures have been annualised

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

Bata India Ltd. 70 3 4 2 1 5 No No Yes 0

0.22

0.56

Bata India Limited Median

Royalty Payout (Rs. bn)

7.79

12.93

Bata IndiaLimited

Median

Royalty as % of (PBT + Royalty)

1.03

2.01

Bata IndiaLimited

Median

Royalty as % of Net Sales

CY10 CY11 CY12 CY13 FY15*

Net Sales PBT Royalty

0.14 0.14 0.160.19

0.22

0.30

0.45 0.450.49

0.39

CY10 CY11 CY12 CY13 FY15*

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Technical Collaboration Fee (Global Footwear Services Pte Ltd)

0.21

Royalty (Bata Brands S.a.r.l., Bata Brands SA)

0.11

Total 0.22

CY12 CY13 FY15* Net Sales 18.42 20.65 21.55 PBT 2.53 2.83 2.63

AMBER

Institutional EYE IiAS Comment | 18 February 2016

18 iias.in February 2016

Bosch Limited IiAS Royalty Signal

Industry: Auto Parts & Equipment Promoter: Robert Bosch GmbH

FY15* Royalty details Financials (Rs. bn)

* Figures have been annualised

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

* Figures have been annualised

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

Bosch Ltd. 50 2 3 2 1 5 No No No 5

3.63

0.56

Bosch Median

Royalty Payout (Rs. bn)

18.80

12.93

Bosch Median

Royalty as % of (PBT + Royalty)

3.87

2.01

Bosch Median

Royalty as % of Net Sales

CY10 CY11 CY12 CY13 FY15*

Net Sales PBT Royalty

2.67 3.14

3.51 4.10

3.63

1.46

4.93

2.19 2.04 2.57

CY10 CY11 CY12 CY13 FY15*

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Royalty and technical service fee

1.49

Professional, consultancy and other charges

2.14

Total 3.63

CY12 CY13 FY15* Net Sales 84.17 85.41 93.93 PBT 13.46 12.57 15.65

AMBER

Institutional EYE IiAS Comment | 18 February 2016

19 iias.in February 2016

Castrol India Limited IiAS Royalty Signal

Industry: Oil Marketing & Distribution Promoter: BP PLC

CY14 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

Castrol India Ltd. 80 0 2 4 5 5 No No No 0

0.73

0.56

Castrol IndiaLimited

Median

Royalty Payout (Rs. bn)

9.15

12.93

Castrol IndiaLimited

Median

Royalty as % of (PBT + Royalty)

2.16

2.01

Castrol IndiaLimited

Median

Royalty as % of Net Sales

CY10 CY11 CY12 CY13 CY14

Net Sales PBT Royalty

0.78 0.73 0.66 0.77 0.73

4.33 4.314.02 4.06

4.40

CY10 CY11 CY12 CY13 CY14

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Royalty 0.73 Total 0.73

CY12 CY13 CY14 Net Sales 31.21 31.80 33.92 PBT 6.66 7.62 7.26

GREEN

Institutional EYE IiAS Comment | 18 February 2016

20 iias.in February 2016

Colgate Palmolive (India) Limited IiAS Royalty Signal

Industry: Personal Products Promoter: Colgate-Palmolive Company

FY15 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

Colgate-Palmolive (India) Ltd.

50 2 0 4 5 5 Yes Yes Yes 0

1.88

0.56

Colgate Palmolive Median

Royalty Payout (Rs. bn)

19.40

12.93

Colgate Palmolive Median

Royalty as % of (PBT + Royalty) 4.72

2.01

Colgate Palmolive Median

Royalty as % of Net Sales

FY11 FY12 FY13 FY14 FY15

Net Sales PBT Royalty

0.97 1.21

1.44 1.66

1.88

3.49 3.95

4.43 4.30 3.88

FY11 FY12 FY13 FY14 FY15

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Royalty 1.88 Total 1.88

FY13 FY14 FY15 Net Sales 31.64 35.79 39.82 PBT 6.63 7.28 7.80

AMBER

Institutional EYE IiAS Comment | 18 February 2016

21 iias.in February 2016

Cummins India Limited IiAS Royalty Signal

Industry: Industrial Machinery Promoter: Cummins Inc

FY15 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

Cummins India Ltd.

60 2 3 3 5 5 Yes Yes Yes 0

0.63

0.56

Cummins IndiaLimited

Median

Royalty Payout (Rs. bn)

6.28

12.93

Cummins IndiaLimited

Median

Royalty as % of (PBT + Royalty)

1.43

2.01

Cummins IndiaLimited

Median

Royalty as % of Net Sales

FY11 FY12 FY13 FY14 FY15

Net Sales PBT Royalty

0.62 0.65 0.65 0.61 0.63

3.46 3.54

4.21 4.224.62

FY11 FY12 FY13 FY14 FY15

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Transfer of Technology, Royalty

0.63

Total 0.63

FY13 FY14 FY15 Net Sales 45.89 39.77 44.06 PBT 10.51 8.18 9.37

AMBER

Institutional EYE IiAS Comment | 18 February 2016

22 iias.in February 2016

FAG Bearings India Limited IiAS Royalty Signal

Industry: Industrial Machinery Promoter: FAG Kugelfischer GmbH

CY14 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs.bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

F A G Bearings India Ltd.

50 3 3 2 0 5 No No Yes 5

0.32

0.56

FAG Bearing Median

Royalty Payout (Rs. bn)

12.23

12.93

FAG Bearing Median

Royalty as % of (PBT + Royalty)

2.00

2.01

FAG Bearing Median

Royalty as % of Net Sales

CY10 CY11 CY12 CY13 CY14

Net Sales PBT Royalty

0.20

0.26 0.27 0.28

0.32

0.10

0.19

0.10 0.12

0.15

CY10 CY11 CY12 CY13 CY14

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Fees for use of technology/trademark and capitalised technical services

0.26

Charges for SAP/R3 and connectivity

0.07

Total 0.32

CY12 CY13 CY14 Net Sales 14.36 14.20 16.18 PBT 2.33 1.85 2.32

AMBER

Institutional EYE IiAS Comment | 18 February 2016

23 iias.in February 2016

Gillette Limited IiAS Royalty Signal

Industry: Personal Products Promoter: The Procter & Gamble Company

FY15 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs.bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

Gillette India Ltd. 50 4 2 1 5 4 Yes Yes Yes 0

0.10

0.56

Gillette IndiaLimited

Median

Royalty Payout (Rs. bn)

3.98

12.93

Gillette IndiaLimited

Median

Royalty as % of (PBT + Royalty)

0.54

2.01

Gillette IndiaLimited

Median

Royalty as % of Net Sales

FY11 FY12 FY13 FY14 FY15

Net Sales PBT Royalty

0.08 0.11 0.13 0.17

0.10

0.57 0.57 0.57 0.57 0.59

FY11 FY12 FY13 FY14 FY15

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Royalty 0.10 Total 0.10

FY13 FY14 FY15 Net Sales 14.38 17.46 18.72 PBT 1.38 0.81 2.46

AMBER

Institutional EYE IiAS Comment | 18 February 2016

24 iias.in February 2016

GlaxoSmithKline Consumer Healthcare Limited IiAS Royalty Signal

Industry: Packaged Foods Promoter: GlaxoSmithKline PLC

FY15 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

* Figures have been annualised

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

Glaxosmithkline Consumer

Healthcare Ltd. 90 2 3 3 5 5 No No No 0

1.44

0.56

GSK ConsumerHealthcare Limited

Median

Royalty Payout (Rs. bn)

13.9

12.93

GSK ConsumerHealthcare Limited

Median

Royalty as % of (PBT + Royalty) 3.33

2.01

GSK ConsumerHealthcare Limited

Median

Royalty as % of Net Sales

CY10 CY11 CY12 FY14* FY15

Net Sales PBT Royalty

0.84 0.96 1.09

1.30 1.44

2.45

1.71

2.20

1.77

2.78

CY10 CY11 CY12 FY14* FY15

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Royalty 1.44 Total 1.44

CY12 FY14* FY15 Net Sales 31.88 38.95 43.08 PBT 6.49 8.13 8.89

GREEN

Institutional EYE IiAS Comment | 18 February 2016

25 iias.in February 2016

Grindwell Norton Limited IiAS Royalty Signal

Industry: Other Industrial Products Promoter: Saint-Gobain

FY15 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

Grindwell Norton Ltd.

50 1 1 2 5 5 No Yes Yes 0

0.09

0.56

Grindwell NortonLimited

Median

Royalty Payout (Rs. bn)

5.90

12.93

Grindwell NortonLimited

Median

Royalty as % of (PBT + Royalty)

0.84

2.01

Grindwell NortonLimited

Median

Royalty as % of Net Sales

FY11 FY12 FY13 FY14 FY15

Net Sales PBT Royalty

0.06 0.08 0.07 0.07 0.09

0.390.42 0.42 0.42 0.43

FY11 FY12 FY13 FY14 FY15

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Royalty, Trademark Amortisation

0.09

Total 0.09

FY13 FY14 FY15 Net Sales 9.45 9.42 11.10 PBT 1.36 1.20 1.49

AMBER

Institutional EYE IiAS Comment | 18 February 2016

26 iias.in February 2016

Heidelberg Cement Limited IiAS Royalty Signal

Industry: Cement and Cement Products Promoter: Heidelberg Cement AG

FY15* Royalty details Financials (Rs. bn)

* Figures have been annualised

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

* Figures have been annualised

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

Heidelberg Cement India Ltd.

10 2 0 0 0 0 No Yes Yes 5

0.17

0.56

Heidelberg Cement Median

Royalty Payout (Rs. bn)

15.07

12.93

Heidelberg Cement Median

Royalty as % of (PBT + Royalty)

1.04

2.01

Heidelberg Cement Median

Royalty as % of Net Sales

CY10 CY11 CY12 CY13 FY15*

Net Sales PBT Royalty

0.14 0.16

0.17 0.17 0.17

0.01

CY10 CY11 CY12 CY13 FY15*

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Technical Knowhow Fees 0.17 Total 0.17

CY12 CY13 FY15* Net Sales 11.04 12.09 16.35 PBT 0.46 (0.85) 0.96

RED

Note: Weak macro-economic environment and high capital expenditures lead to a

drop in the profitability of the company in CY13.

Institutional EYE IiAS Comment | 18 February 2016

27 iias.in February 2016

Hindustan Unilever Limited IiAS Royalty Signal

Industry: FMCG Promoter: Unilever PLC

FY15 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

Hindustan Unilever Ltd.

50 2 2 3 5 5 Yes Yes Yes 0

7.38

0.56

HUL Median

Royalty Payout (Rs. bn)

10.66

12.93

HUL Median

Royalty as % of (PBT + Royalty)

2.39

2.01

HUL Median

Royalty as % of Net Sales

FY11 FY12 FY13 FY14 FY15

Net Sales PBT Royalty

2.87 3.11 3.84 5.31 7.38

16.42 18.84

46.56

32.73

38.81

FY11 FY12 FY13 FY14 FY15

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Royalty fees (Parent and Subsidiaries)

7.35

Management fees 0.02 Total 7.38

FY13 FY14 FY15 Net Sales 258.10 280.19 308.06 PBT 49.58 50.28 61.87

AMBER

Note: In FY13 HUL gave a special dividend of Rs. 8 per share bringing the total dividend

per share to Rs. 18.5.

Institutional EYE IiAS Comment | 18 February 2016

28 iias.in February 2016

Hitachi Home & Life Solutions (India) Ltd IiAS Royalty Signal

Industry: Consumer Electronics Promoter: Hitachi Appliances Inc.

FY15 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

Hitachi Home & Life Solutions

(India) Ltd. 20 3 2 0 3 2 Yes Yes Yes 5

0.42

0.56

Hitachi Median

Royalty Payout (Rs. bn)

29.43

12.93

Hitachi Median

Royalty as % of (PBT + Royalty)

2.68

2.01

Hitachi Median

Royalty as % of Net Sales

FY11 FY12 FY13 FY14 FY15

Net Sales PBT Royalty

0.23 0.25 0.30 0.31

0.42

0.04 0.04 0.05 0.05 0.05

FY11 FY12 FY13 FY14 FY15

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Royalty 0.34 Technical Know-how fees amortised

0.08

Total 0.42

FY13 FY14 FY15 Net Sales 9.30 11.00 15.73 PBT 0.21 0.11 1.01

RED

Institutional EYE IiAS Comment | 18 February 2016

29 iias.in February 2016

Ingersoll-Rand (India) Limited IiAS Royalty Signal

Industry: Industrial Machinery Promoter: Ingersoll-Rand PLC

FY15 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

Ingersoll-Rand (India) Ltd.

40 2 1 3 5 2 Yes Yes Yes 0

0.08

0.56

Ingersoll-Rand(India)

Median

Royalty Payout (Rs. bn)

7.26

12.93

Ingersoll-Rand(India)

Median

Royalty as % of (PBT + Royalty)

1.21

2.01

Ingersoll-Rand(India)

Median

Royalty as % of Net Sales

FY11 FY12 FY13 FY14 FY15

Net Sales PBT Royalty

0.07 0.070.13 0.12

0.08

0.22

0.88

0.22 0.22 0.23

FY11 FY12 FY13 FY14 FY15

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Management fees 0.08 Total 0.08

FY13 FY14 FY15 Net Sales 5.81 5.79 6.56 PBT 1.11 0.98 1.01

RED

Institutional EYE IiAS Comment | 18 February 2016

30 iias.in February 2016

Kansai Nerolac Paints Limited IiAS Royalty Signal

Industry: Furniture, Furnishing, Paints Promoter: Kansai Paint Company Limited

FY15 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

Kansai Nerolac Paints Ltd.

80 3 2 0 4 5 No No No 0

0.13

0.56

Kansai NerolacPaints Limited

Median

Royalty Payout (Rs. bn)

3.11

12.93

Kansai NerolacPaints Limited

Median

Royalty as % of (PBT + Royalty)

0.36

2.01

Kansai NerolacPaints Limited

Median

Royalty as % of Net Sales

FY11 FY12 FY13 FY14 FY15

Net Sales PBT Royalty

0.12 0.12 0.15 0.15 0.13

0.630.69 0.69 0.69

0.91

FY11 FY12 FY13 FY14 FY15

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Royalty and technical fees 0.13 Total 0.13

FY13 FY14 FY15 Net Sales 28.39 31.36 35.32 PBT 4.20 3.07 3.99

GREEN

Institutional EYE IiAS Comment | 18 February 2016

31 iias.in February 2016

Maruti Suzuki Limited IiAS Royalty Signal

Industry: Cars & Utility Vehicles Promoter: Suzuki Motor Corporation

FY15 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

Maruti Suzuki India Ltd.

40 3 3 0 0 5 Yes Yes No 5

27.68

0.56

Maruti Median

Royalty Payout (Rs. bn)

36.20

12.93

Maruti Median

Royalty as % of (PBT + Royalty) 5.69

2.01

Maruti Median

Royalty as % of Net Sales

FY11 FY12 FY13 FY14 FY15

Net Sales PBT Royalty

19.08 18.40

25.44 25.86 27.68

2.52 2.52 2.83 4.24

9.09

FY11 FY12 FY13 FY14 FY15

Total Royalty Dividend Paid

Nature of transaction Amount (Rs.bn) Running Royalty 26.58 Lump sum Royalty Amortised for the year 1.10 Total 27.68

FY13 FY14 FY15 Net Sales 426.13 426.45 486.06 PBT 29.91 36.59 48.68

RED

Institutional EYE IiAS Comment | 18 February 2016

32 iias.in February 2016

Nestlé India Limited IiAS Royalty Signal

Industry: Packaged Foods Promoter: Nestlé S.A

CY14 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

Nestlé India Ltd. 50 1 1 3 5 5 Yes Yes Yes 0

4.16

0.56

Nestlé Median

Royalty Payout (Rs. bn)

19.00

12.93

Nestlé Median

Royalty as % of (PBT + Royalty)

4.24

2.01

Nestlé Median

Royalty as % of Net Sales

CY10 CY11 CY12 CY13 CY14

Net Sales PBT Royalty

2.60 3.17 3.49 3.69

4.16

5.45 5.43 5.43 5.47

7.17

CY10 CY11 CY12 CY13 CY14

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) General license fees 3.51 Information technology and management information systems fees

0.65

Total 4.16

CY12 CY13 CY14 Net Sales 83.02 90.62 98.06 PBT 15.53 16.78 17.74

AMBER

Institutional EYE IiAS Comment | 18 February 2016

33 iias.in February 2016

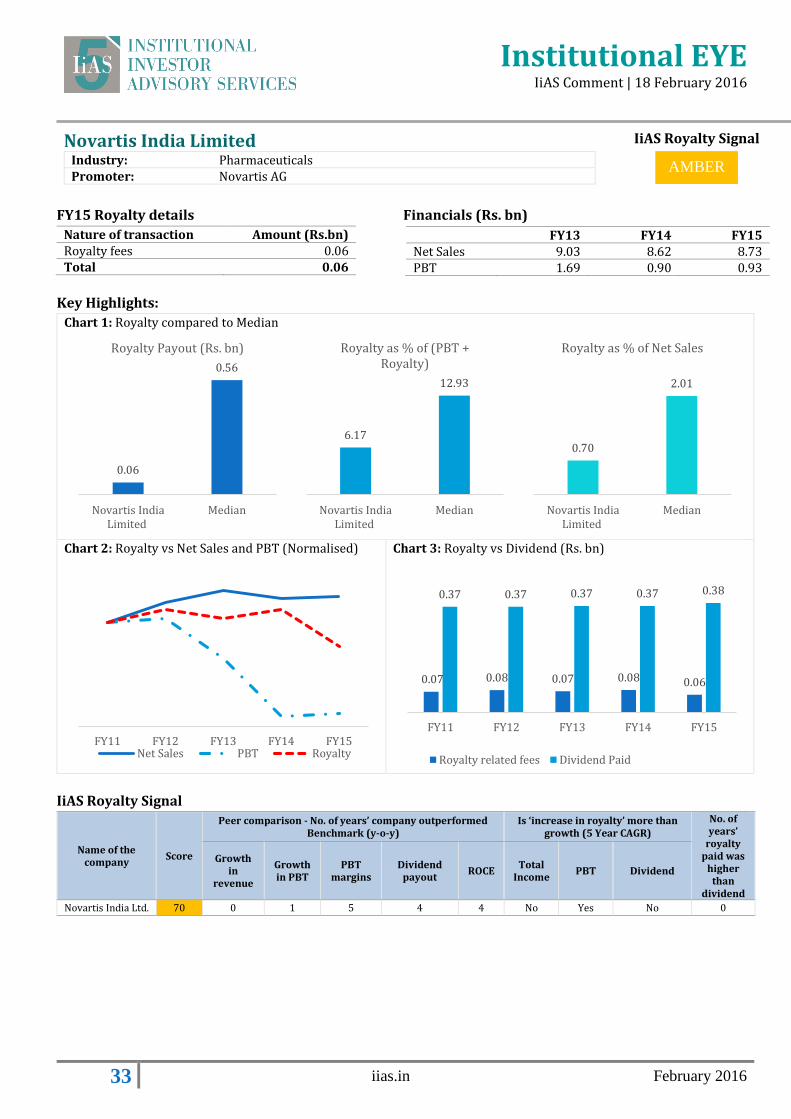

Novartis India Limited IiAS Royalty Signal

Industry: Pharmaceuticals Promoter: Novartis AG

FY15 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

Novartis India Ltd. 70 0 1 5 4 4 No Yes No 0

0.06

0.56

Novartis IndiaLimited

Median

Royalty Payout (Rs. bn)

6.17

12.93

Novartis IndiaLimited

Median

Royalty as % of (PBT + Royalty)

0.70

2.01

Novartis IndiaLimited

Median

Royalty as % of Net Sales

FY11 FY12 FY13 FY14 FY15Net Sales PBT Royalty

0.07 0.08 0.07 0.08 0.06

0.37 0.37 0.37 0.37 0.38

FY11 FY12 FY13 FY14 FY15

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Royalty fees 0.06 Total 0.06

FY13 FY14 FY15 Net Sales 9.03 8.62 8.73 PBT 1.69 0.90 0.93

AMBER

Institutional EYE IiAS Comment | 18 February 2016

34 iias.in February 2016

Procter & Gamble Limited IiAS Royalty Signal

Industry: Personal Products Promoter: The Procter & Gamble Company

FY15 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs.bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

Procter & Gamble Hygiene & Health

Care Ltd. 90 4 4 3 5 5 No No Yes 0

1.00

0.56

P&G Median

Royalty Payout (Rs. bn)

16.70

12.93

P&G Median

Royalty as % of (PBT + Royalty)

4.30

2.01

P&G Median

Royalty as % of Net Sales

FY11 FY12 FY13 FY14 FY15

Net Sales PBT Royalty

0.52 0.57 0.71

0.85

1.00

0.85 0.85 0.95

1.04 1.18

FY11 FY12 FY13 FY14 FY15

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Royalty 1.00 Total 1.00

FY13 FY14 FY15 Net Sales 16.87 20.51 23.32 PBT 2.86 4.60 5.01

GREEN

Institutional EYE IiAS Comment | 18 February 2016

35 iias.in February 2016

SKF Limited IiAS Royalty Signal

Industry: Other Industrial Goods Promoter: AB SKF

CY14 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

S K F India Ltd. 20 1 2 1 3 5 Yes Yes Yes 3

0.66

0.56

SKF India Limited Median

Royalty Payout (Rs. bn)

17.63

12.93

SKF India Limited Median

Royalty as % of (PBT + Royalty) 2.79

2.01

SKF India Limited Median

Royalty as % of Net Sales

CY10 CY11 CY12 CY13 CY14

Net Sales PBT Royalty

0.11 0.14

0.46

0.620.66

0.43 0.46 0.46 0.46

0.55

CY10 CY11 CY12 CY13 CY14

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Royalty 0.39 Trade Mark Fees 0.26 Total 0.66

CY12 CY13 CY14 Net Sales 21.85 22.26 23.52 PBT 2.83 2.53 3.06

RED

Note: The company launched a new product in CY12 (SKF BeyondZero) with

technical support from the parent translating into a significant spike in royalty

payouts.

Institutional EYE IiAS Comment | 18 February 2016

36 iias.in February 2016

Schneider Electric Infrastructure Limited IiAS Royalty Signal

Industry: Heavy Electrical Equipment Promoter: Schneider Electric Singapore Pte. Limited

FY15 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

IiAS Royalty Signal

Name of the company Score

Peer comparison - No. of years’ company

outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more

than growth (5 Year CAGR) No. of years’

royalty paid

was higher

than dividend

Growth

in

revenue

Growth

in PBT

PBT

margins

Dividend

payout ROCE

Total

Income PBT Dividend

Schneider Electric Infrastructure Ltd. 0 0 1 0 1 1 Yes Yes Yes 4

0.49

0.56

SchneiderElectric

Median

Royalty Payout (Rs. bn)

154.53

12.93

Schneider Electric Median

Royalty as % of (PBT + Royalty) 3.71

2.01

Schneider Electric Median

Royalty as % of Net Sales

FY12 FY13 FY14 FY15

Net Sales PBT Royalty

0.06

0.250.21

0.49

0.11

FY12 FY13 FY14 FY15

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs. bn) Trademark Fee 0.24 Management Support Fee 0.25 Total 0.49

FY13 FY14 FY15 Net Sales 13.10 12.16 13.10 PBT (0.28) (1.25) (0.17)

RED

Note: The company has been witnessing increasing inventory levels owing to the

weak economic environment. Poor infrastructure offtake impacted the financial

performance of the company.

Institutional EYE IiAS Comment | 18 February 2016

37 iias.in February 2016

Timken India Limited IiAS Royalty Signal

Industry: Industrial Machinery Promoter: The Timken Company

FY15 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs. bn)

* Figures have been annualised.

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

Timken India Ltd. 80 3 3 1 4 5 No No Yes 1

0.19

0.56

Timken IndiaLimited

Median

Royalty Payout (Rs. bn)

13.34

12.93

Timken IndiaLimited

Median

Royalty as % of (PBT + Royalty)

2.03

2.01

Timken IndiaLimited

Median

Royalty as % of Net Sales

CY10 FY12* FY13 FY14 FY15

Net Sales PBT Royalty

0.09 0.16 0.16 0.17 0.19

1.18

0.16

0.52

0.25

CY10 FY12* FY13 FY14 FY15

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Royalty 0.19 Total 0.19

FY13 FY14 FY15 Net Sales 6.89 7.20 9.29 PBT 0.64 0.66 1.22

GREEN

Note: In FY12 the company paid out a higher interim dividend of Rs. 20 per share on

account of successful operations.

Institutional EYE IiAS Comment | 18 February 2016

38 iias.in February 2016

United Spirits Limited IiAS Royalty Signal

Industry: Breweries & Distilleries Promoter: Diageo PLC

FY15 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (in Rs. bn)

Chart 3: Royalty vs Dividend (Rs. bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

United Spirits Ltd. 20 1 0 0 0 0 Yes Yes Yes 2

0.58

0.56

United SpiritsLimited

Median

Royalty Payout (Rs. bn)

-3.08

12.93

United SpiritsLimited

Median

Royalty as % of (PBT + Royalty)

0.72

2.01

United SpiritsLimited

Median

Royalty as % of Net Sales

84.26 79.52

0.43 0.58

(50.60)

(18.99)

FY14 FY15

Net sales (Rs. bn) Royalty related fees PBT

0.01 - -

0.43

0.58

0.38 0.38 0.38

0.04

FY11 FY12 FY13 FY14 FY15

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Trade-mark license fees 0.58 Total 0.58

FY13 FY14 FY15 Net Sales 83.18 84.26 79.52 PBT 3.21 (50.60) (18.99)

RED

Institutional EYE IiAS Comment | 18 February 2016

39 iias.in February 2016

Wabco India Limited IiAS Royalty Signal

Industry: Auto Parts & Equipment Promoter: WABCO Holdings Inc

FY15 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT

Chart 3: Royalty vs Dividend (Rs. bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

Wabco India Ltd. 60 3 1 3 0 5 No No No 3

0.14

0.56

Wabco IndiaLimited

Median

Royalty Payout (Rs. bn)

7.47

12.93

Wabco IndiaLimited

Median

Royalty as % of (PBT + Royalty)

1.06

2.01

Wabco IndiaLimited

Median

Royalty as % of Net Sales

FY12 FY13 FY14 FY15

Net Sales PBT Royalty

0.07

0.120.14 0.14

0.11 0.11 0.11 0.11 0.11

FY11 FY12 FY13 FY14 FY15

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Royalty fees 0.08 Fees for technical services 0.06 Total 0.14

FY13 FY14 FY15 Net Sales 9.66 11.11 13.48 PBT 1.85 1.61 1.77

AMBER

Institutional EYE IiAS Comment | 18 February 2016

40 iias.in February 2016

Whirlpool of India Limited IiAS Royalty Signal

Industry: Consumer Electronics Promoter: Whirlpool Corporation

FY15 Royalty details Financials (Rs. bn)

Key Highlights:

Chart 1: Royalty compared to Median

Chart 2: Royalty vs Net Sales and PBT (Normalised)

Chart 3: Royalty vs Dividend (Rs.bn)

IiAS Royalty Signal

Name of the company

Score

Peer comparison - No. of years’ company outperformed Benchmark (y-o-y)

Is ‘increase in royalty’ more than growth (5 Year CAGR)

No. of years’

royalty paid was

higher than

dividend

Growth in

revenue

Growth in PBT

PBT margins

Dividend payout

ROCE Total

Income PBT Dividend

Whirlpool of India Ltd.

30 2 1 0 0 5 No No Yes 5

0.43

0.56

Whirlpool Median

Royalty Payout (Rs. bn)

12.53

12.93

Whirlpool Median

Royalty as % of (PBT + Royalty)

1.31

2.01

Whirlpool Median

Royalty as % of Net Sales

FY11 FY12 FY13 FY14 FY15

Net Sales PBT Royalty

0.37 0.36 0.36 0.35

0.43

FY11 FY12 FY13 FY14 FY15

Royalty related fees Dividend Paid

Nature of transaction Amount (Rs.bn) Royalty Fee 0.29 Technical know-how fee 0.14 Total 0.43

FY13 FY14 FY15 Net Sales 27.73 28.35 32.94 PBT 1.79 1.74 3.01

RED

Institutional EYE IiAS Comment | 18 February 2016

41 iias.in February 2016

Disclaimer This document has been prepared by Institutional Investor Advisory Services India Limited (IiAS). The information contained herein is solely from publicly available data, but we do not represent that it is accurate or complete and it should not be relied on as such. IiAS shall not be in any way responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. This document is provided for assistance only and is not intended to be and must not be taken as the basis for any voting or investment decision. The user assumes the entire risk of any use made of this information. Each recipient of this document should make such investigation as it deems necessary to arrive at an independent evaluation of the individual resolutions referred to in this document (including the merits and risks involved). The discussions or views expressed may not be suitable for all investors. The information given in this document is as of the date of this report and there can be no assurance that future results or events will be consistent with this information. This information is subject to change without any prior notice. IiAS reserves the right to make modifications and alterations to this statement as may be required from time to time. However, IiAS is under no obligation to update or keep the information current. Nevertheless, IiAS is committed to providing independent and transparent recommendation to its client and would be happy to provide any information in response to specific client queries. Neither IiAS nor any of its affiliates, group companies, directors, employees, agents or representatives shall be liable for any damages whether direct, indirect, special or consequential including lost revenue or lost profits that may arise from or in connection with the use of the information. The disclosures of interest statements incorporated in this document are provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report.

Confidentiality This information is strictly confidential and is being furnished to you solely for your information. This information should not be reproduced or redistributed or passed on directly or indirectly in any form to any other person or published, copied, in whole or in part, for any purpose. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject IiAS to any registration or licensing requirements within such jurisdiction. The distribution of this document in certain jurisdictions may be restricted by law, and persons in whose possession this document comes, should inform themselves about and observe, any such restrictions. The information provided in these reports remains, unless otherwise stated, the copyright of IiAS. All layout, design, original artwork, concepts and other Intellectual Properties, remains the property and copyright of IiAS and may not be used in any form or for any purpose whatsoever by any party without the express written permission of the copyright holders.

IiAS Voting Policy IiAS' voting recommendations are based on a set of guiding principles, which incorporate the basic tenets of the legal framework along with the best practices followed by some of the better governed companies. These policies clearly list out the rationale and evaluation parameters which are taken into consideration while finalizing the recommendations. The detailed IiAS Voting Guidelines are available at www.iias.in/IiAS-voting-guidelines.aspx. The draft report prepared by the analyst is referred to an internal Review and Oversight Committee (ROC), which is responsible for ensuring consistency in voting recommendations, alignment of recommendations to the IiAS’ voting criteria and setting and maintaining quality standards of IiAS’ proxy reports. Details regarding the functioning and composition of the ROC committee are available at www.iias.in. In undertaking its activities, IiAS relies on information available in the public domain i.e. information that is available to public shareholders. However, in order to provide a more meaningful analysis, IiAS, generally seeks clarifications from the subject company. IiAS reserves the right to share the information provided by the subject company in its reports. Further details on IiAS policy on communication with subject companies are available at www.iias.in.

Analyst Certification The research analyst(s) for this report certify/ies that no part of his/her/their compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this report. IiAS’ internal policies and control procedures governing the dealing and trading in securities by employees are available at www.iias.in.

Conflict Management IiAS and its research analysts may hold a nominal number of shares in companies IiAS covers (including the subject company), as on the date of this report. A list of IiAS’ shareholding in companies is available at www.iias.in.

However, IiAS, the research analyst(s) responsible for this report, and their associates or relatives, do not have actual/beneficial ownership of one per cent or more securities of the subject company, at the end of the month immediately preceding the date of publication of this report. A list of shareholders of IiAS as of the date of this report is available at www.iias.in. However, the preparation of this report is monitored by an internal Review and Oversight Committee (ROC) of IiAS and is not subject to the control of any company to which such report may relate and which may be a shareholder of IiAS.

Institutional EYE IiAS Comment | 18 February 2016

42 iias.in February 2016

Other Disclosures IiAS further confirms that, save as otherwise set out above or disclosed on IiAS’ website (www.iias.in):

IiAS, the research analyst(s) responsible for this report, and their associates or relatives, do not have any financial interest in the subject company.

IiAS, the research analyst(s) responsible for this report, and their associates or relatives, do not have any other material conflict of interest at the time of publication of this report.

As a proxy advisory firm, IiAS provides subscription, databased and other related services to various Indian and international customers (which could include the subject company). IiAS generally receives between INR 10,000 and INR 25,00,000 for such services from its customers. Other than compensation that it may have received for providing such services to the subject company in the ordinary course, none of IiAS, the research analyst(s) responsible for this report, and their associates or relatives, has received any compensation from the subject company or any third party for this report.

None of IiAS, the research analyst(s) responsible for this report, and their associates or relatives, has received any compensation from the subject company or any third party in the past 12 months in connection with the provision of services of products (including investment banking or merchant banking or brokerage services or any other products and services), or managed or co-managed public offering of securities of the subject company.

The research analyst(s) responsible for this report has not served as an officer, director or employee of the subject company. None of IiAS or the research analyst(s) responsible for this report has been engaged in market making activity for the subject company.

Institutional Investor Advisory Services India Limited (IiAS) is an advisory firm, dedicated to providing participants in the Indian market with independent opinion, research and data on corporate governance issues. IiAS also provides voting recommendations on shareholder resolutions for over 650 companies. To know more about IiAS visit www.iias.in Subscriptions help IiAS stay fiercely independent. To subscribe to IiAS research write to us at [email protected]

Office Institutional Investor Advisory Services 15th Floor, West Wing, P J Tower, Dalal Street, Fort, Mumbai - 400 001 India Contact [email protected] T: +91 22 2272 1570-3 F: +91 22 2272 1574

markets ∩ governance