RSA Research Network Seminar, Outsourcing and Offshoring Business Services

1

Global trends in business service movements: the role of East Central Europe with special

emphasis on related methodological problems

Magdolna SassInstitute of Economics of the Hungarian

Academy of Sciences and ICEG EC

RSA Research Network Seminar, Outsourcing and Offshoring Business Services

2

Outline of the presentation

1. BPO, East Central Europe/Hungary: new hosts

2. Methodological problems

3. Location advantages

4. Impact on the local economy

5. Relocation

6. ConclusionResearch on BPO in ECE is based on company interviews

Work in progress

Presentation based on the project „"Foreign Direct Investment in Central and Eastern Europe: What Kind of Competitiveness for the Visegrad Four?" and OTKA no. 68435 (Hungarian research fund).

RSA Research Network Seminar, Outsourcing and Offshoring Business Services

3

East Central Europe and Hungary as a new location for BPO

• Movements of jobs/related FDI mainly between developed countries and India (started out from English-speaking countries, continental Europe only followed)

• in East Central Europe, especially the Czech Republic, Hungary and Poland are the main hosts to BPO projects, though their share is much lower than expected on the basis of media reports, Romania and Bulgaria catching up after 2007 (EU-membership)

• Estimation on the basis of the number of projects: 1400-1500 in Europe, 150-180 in the three countries in CEE (India, other Western European locations dominate), distributed approx. equally (biggest project go to India or are in W.Europe)

• Combined market share of CEE’s globally: less than 1 per cent (McKinsey (2006)) – still very limited

RSA Research Network Seminar, Outsourcing and Offshoring Business Services

4

Hungary as a host to BPOService centres receiving financial incentives in Hungary

CompanyHome country Location in Hungary Number of jobs (actual or planned)

ExxonMobil USA Budapest 1200

IBM ISSC USA Budapest 1300

Diageo United Kingdom Budapest 600

Getronics Netherlands Budapest 510

Jabil USA Szombathely 719

SAP Germany Budapest 600

Tata India Budapest 450

Convergys USA Budapest 282

EDS USA Budapest, Szeged 1150

InBev Belgium Budapest 380

Budapest Bank USA Békéscsaba 530

Morgan Stanley United Kingdom Budapest 450

Citigroup USA Budapest 302

Vodafone United Kingdom Budapest 746

British Telecom United Kingdom Budapest, Debrecen 700

T-Systems Germany Budapest, Debrecen 1750

Source: ITDH

RSA Research Network Seminar, Outsourcing and Offshoring Business Services

5

Hungary as a host to BPO

• Approx. 50 centres• Approx. 20-22 thousand people, 99 % white collar, between 80 and

90 % with university diploma and multiple language knowledge• Going to the countryside now (university towns close to the border

are the new locations)• Dynamic growth in output, exports (high share in EU27 comparison,

turnover centred on the EU, share of other services /other business services grew in services exports, specialisation indices show a relative specialisation on other business services – though methodological problems)

• Various activities (often more activities in one project)

RSA Research Network Seminar, Outsourcing and Offshoring Business Services

6

Research questions and method

• Methodological problems of measurement• Location advantages determining the choice of the new location

(inside CEE)• Impact on the host economy• Relocations in business servicesMethods• Methodological problems: literature review and own calculations

(illustrations)• Location advantages and impact: questionnaire based company

interviews (5 in Hungary: 2 captive, 3 non-captive) and as a basis for comparison: 3-3 interviews in the Czech Republic, Poland and Slovakia;

• Case by case analysis for relocations for the period between July 2003 and September 2005, based on the database of Hunya, Sass (2005)

RSA Research Network Seminar, Outsourcing and Offshoring Business Services

7

Methodological problems 11. Services – definition: missing, unclear (Knight, 1999; Bryson, 2001), Nachum

(1999): larger differences in between service industries than between services and manufacturing + lack of definition of business services (various definitions used)

2. FDI data – problems + usually small/diverse amounts invested (case studies: FDI in the range of 1 million to 1 billion USD in Hungary)

3. Number of projects can be misleading as well– differing sizes; number of jobs/employment can be the best proxy, but 1. data relatively old + usually less jobs are created in relocated and/or newly opened plants in CEECs (Hunya, Sass, 2005)

4. Captive and non-captive; manufacturing and services (captiveÍ) may be mixed up in one project

5. Categories: data are presented at a too high level of aggregation (e.g. in NACE); classification problems (Thakor, Kumar, 2000)

6. Data on services foreign trade would be good for showing the extent of BPO/relocation: many problems (transfer pricing, etc.) – see later

7. Inside BOP: services export lines are used for profit repatriation as well (evidence from Hungary)

8. Recording problems present in both manufacturing and services9. Relocation: only on a case by case basis, but even this can be misleading

(relocated and new activities ,mixed in one project)

RSA Research Network Seminar, Outsourcing and Offshoring Business Services

8

Methodological problems 2• Specific problem: large differences between reported and mirror

statistics, which indicates that data are unreliable• Reasons:

– different thresholds and different correction methods in EU-member countries,

– simplified reporting, – coverage different, – exchange rates used , – double or triple reporting due to „intermediary” trade (important in the

EU), – no reporting, – VAT-fraud,– Time lag in reporting

• Relatively big in goods trade, and is expected to be even larger for services trade due to even more problematic tracing (no actual cross border transport of goods is involved)

RSA Research Network Seminar, Outsourcing and Offshoring Business Services

9

Methodological problems 3

• Correction: problematic (both sides (reported and mirror statistics) are „moving targets”)

• Extent: in 2006: export overreported by almost 10 %, import underreported by almost 4 %

RSA Research Network Seminar, Outsourcing and Offshoring Business Services

10

Problems with services trade data% difference between reported and mirror services trade statistics, 2006

-60,0

-40,0

-20,0

0,0

20,0

40,0

60,0

80,0

Belgiu

m

Bulga

ria

Czech

Rep

ublic

Denm

ark

Ger

man

y (in

cludin

g ex-

GDR from

199

1)

Eston

ia

Irelan

d

Gre

eceSpa

in

Franc

eIta

ly

Cypru

s

Latv

ia

Lith

uani

a

Luxe

mbo

urg

(Gra

nd-Duc

hé)

Hunga

ryM

alta

Nethe

rland

s

Austri

a

Polan

d

Portu

gal

Roman

ia

Slove

nia

Slova

kia

Finlan

d

Sweden

Unite

d Kin

gdom

%

export

import

RSA Research Network Seminar, Outsourcing and Offshoring Business Services

11

Problems with „other services” trade statistics (related to BPO)

% differences between reported and mirror statistics, foreign trade in other services, 2006

-150,0

-100,0

-50,0

0,0

50,0

100,0

%

export

import

RSA Research Network Seminar, Outsourcing and Offshoring Business Services

12

Trade statistics: goods and services

difference between reporter and mirror statistics, goods and services export and import, 2006, without Cyprus

-60,0

-40,0

-20,0

0,0

20,0

40,0

60,0

80,0

%

services export

services import

goods export

goods import

RSA Research Network Seminar, Outsourcing and Offshoring Business Services

13

Location advantages 1

• determine which countries are chosen as hosts to new or relocated service centres (based on Dunning (1983) OLI-paradigm)

• similar to those of efficiency seeking investments (costs and availability of appropriately trained or trainable skilled work in the required quantity) + specific: infrastructure (mainly telecom)

• Additional: availability of certain services (financial etc.), good regulatory and business environment, protection of IP, office space, geographical proximity/same/similar time zone in some cases (nearshoring), different time zone in others, language knowledge (specific: other than English European languages, „small” European languages (including Turkish in Hungary))

RSA Research Network Seminar, Outsourcing and Offshoring Business Services

14

Location advantages 2 – inside the region

Specific advantage: knowledge of „smaller” languages, good geographical position

Inside CEE:Poland stands out with its size (bigger

projects), location (NE, Baltics)Czech Republic: central location, best

flight connections, specialisation on IT

Hungary: minor languages (minorities in neighbouring countries), good location (CEE, towards SEE)

Choosing among the three countries is based on:

• Earlier presence of the company;• Previous good (or bad) experience

with the country;• Choice is influenced by the relative

dynamism, success of local affiliates;• Special language requirements;• Active lobbying of the local affiliate;• Quality of life, culture, English

schooling etc. in the target city, especially in cases when expatriates are involved

• Very limited role of incentives (mainly for bigger projects)

RSA Research Network Seminar, Outsourcing and Offshoring Business Services

15

Impact on the host economy 1

• Companies with foreign participation have the potential to impact upon positively on the business environment, on local companies in the host country, though this impact is not automatic

• Analysed in the literature almost exclusively in manufacturing, though it is relevant for services sector FDI as well

• While the share of the three analysed countries in BPO is not high, from the host economy point of view, these are big projects and have a potentially big impact on the local economy

• Various fields of impact on the local economy is analysed on the basis of company interviews:

1. Job creation2. Linkages and other local contacts3. Impact on the business environment and infrastructure4. Spillovers through trained employees5. Market acces, FT, BOP

RSA Research Network Seminar, Outsourcing and Offshoring Business Services

16

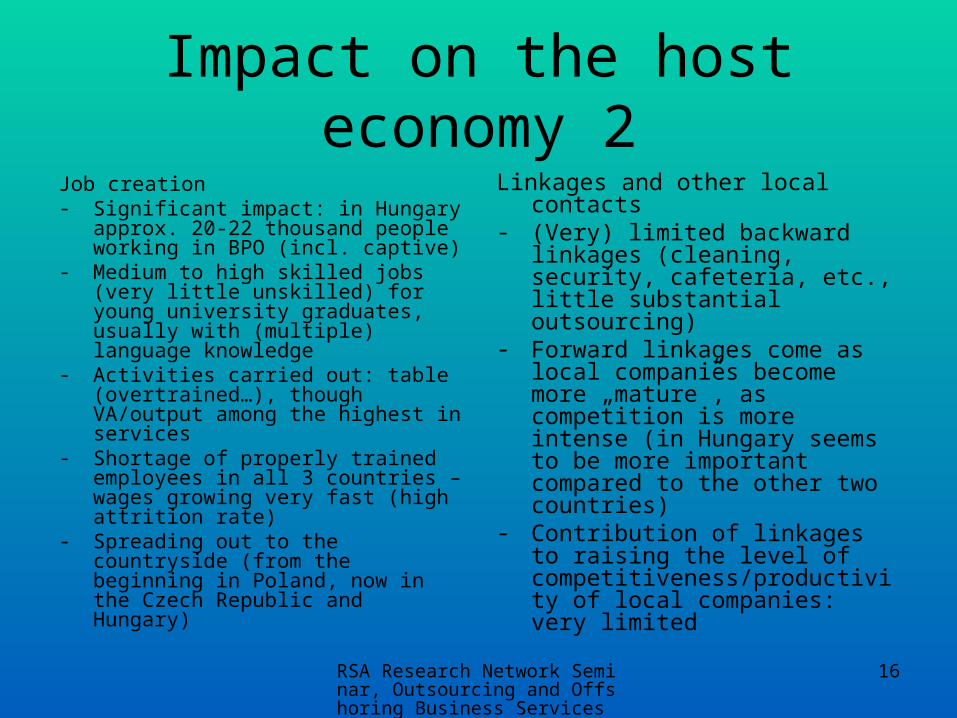

Impact on the host economy 2Job creation- Significant impact: in Hungary approx.

20-22 thousand people working in BPO (incl. captive)

- Medium to high skilled jobs (very little unskilled) for young university graduates, usually with (multiple) language knowledge

- Activities carried out: table (overtrained…), though VA/output among the highest in services

- Shortage of properly trained employees in all 3 countries – wages growing very fast (high attrition rate)

- Spreading out to the countryside (from the beginning in Poland, now in the Czech Republic and Hungary)

Linkages and other local contacts- (Very) limited backward linkages

(cleaning, security, cafeteria, etc., little substantial outsourcing)

- Forward linkages come as local companies become more „mature”, as competition is more intense (in Hungary seems to be more important compared to the other two countries)

- Contribution of linkages to raising the level of competitiveness/productivity of local companies: very limited

RSA Research Network Seminar, Outsourcing and Offshoring Business Services

17

Table 16 Activities carried out in the companies interviewed in Hungary

Back officeCustomer contact Common

corporate functions

Knowledge services and decision analysis

Research and development

Transaction processing

Document management

Data entryData

processing

Call centres HRAccountingAdministrativeFinancial

servicesIT call centres

and other IT services

Quality management

Program and project management

Financial program management

Integration engineering

Supply chain management

Analytical accounting services

Business performance analysis

Cost analysis

Software development

Source: own compilation based on company interviews

RSA Research Network Seminar, Outsourcing and Offshoring Business Services

18

Impact on the host economy 3

Impact on the business environment, infrastructure

- Competition for appropriately trained employees is intense: companies are more active locally, than „ordinary” FIEs (participation in local business associations, links with universities)

- Intense use of local infrastructure: in some cases results in better services

Spillovers through trained employees

- This seems to be one of the most important local impacts

- Trained employees in certain cases set up their own enterprises or go to work to domestic companies

- Not only skills, but business culture, business ethics are transferred through (former) workers

RSA Research Network Seminar, Outsourcing and Offshoring Business Services

19

Impact on the host economy 4Market acces, BOP, FDI, FT, other• Methodological and data

problems• Export-intensive projects

(lower export/sales rate is above 60 %)

• Relatively high share in FDI stock (10 %) in Hungary

• Increase in services trade, especially in other services and other business services

• Balance of trade: turned positive (graph)

• Specialisation indices and RCA show change in business services towards relative specialisation and RCA

Graph 1 Balance of trade in computer services and Other business services, 1995-2006, million euros

-700

-600

-500

-400

-300

-200

-100

0

100

200

300

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

mill

ion

euro

s

Computer services Other business services

RSA Research Network Seminar, Outsourcing and Offshoring Business Services

20

Relocation• Relocation: a process, in which either there is a transfer of production

capacities from another country, or there is a capacity extension in one affiliate parallel with a capacity reduction in another, or there is a capacity extension in one affiliate, while other affiliates‘ capacities do not change.

• Even more methodological problems• Case by case analysis is needed• In Hunya, Sass (2005): company cases of relocations in the period between

July 2003- September 2005• 9 of 61 cases affected business services (declared relocations)• Affected locations (from which the activity was transferred): mainly Western

Europe (Germany, the Netherlands, Austria, UK, Ireland, non-specified Western Europe) and the US

• Owners of companies: mainly US and UK• Activities: various, more than one per project, but not all activities of a firm

are relocations (company interviews)• Location in Hungary: mainly Budapest

RSA Research Network Seminar, Outsourcing and Offshoring Business Services

21

Declared relocations in business services, July 2002-September 2005

CompanyActivity Foreign location

affectedMunkahely-teremtés vagy -veszteség

GE Capital (USA) Regional call centre Other Western European locations

+400-500

Renault Nissan(French-Japanese)

Regional logistics centre Austria +60-80

Electronic Data Systems (USA)

Regional centre Western Europe and the US

+350-400

Avis (UK) Financial administrative centre, regional call centre, financial-informatics services

Germany, (Belgium) +400

Diageo (UK) Extension of capacities of service centre, new activities (accounting)

UK +60

Electronic Data Systems (USA)

Capacity extension for new activities, call centre

Western Europe, USA

+400

Avis Europe Plc. (UK) Extension of financial services centre Western Europe +135

Maxtor Group (USA) African, European and Middle-Eastern service centre relocation (leaving call centre and financial planning there)

Ireland + Approx. 20

Marsh (USA) European accounting and administrative activities (except for UK, Ireland and the Netherlands)

UK +12

RSA Research Network Seminar, Outsourcing and Offshoring Business Services

22

Conclusion

CEEs/Visegrad countries increasingly involved in BPOMany methodological problems hinders the analysis (esp. the extent of

relocation)From a competitiveness point of view BPO projects in CEE- Contribute to the formation of a better domestic business environment, in

some cases availability of high quality services for domestic companies (forward linkages)

- Local contacts- backward linkages (suppliers): minimal, though, esp. forward linkages increasing over time

- Job creation for medium to high skilled, (though overtrained, partly due to the language knowledge requirement) spillovers through employees (skills, culture, ethics, own SMEs)

- Significant impact on the BOP, though due to methodological problems, it is difficult to quantify separately for these projects (FDI, FT-balance, profit repatriation etc.)

(Inside EU movements) Importance from the point of view of raising the competitiveness of overall EU-27

RSA Research Network Seminar, Outsourcing and Offshoring Business Services

23

Thank you for your attention!