@ SCG 2013

SCG Chemicals outlook hosted by SCBS

Mr. Cholanat Yanaranop

President

SCG Chemicals

Mr. Chaovalit Ekabut

VP-Finance and Investment & CFO, SCG

Mar 18th, 2014

1

- 2 -

Agenda

Where are we in the cycle?

New competing olefins supplies

Our strategies

2

The petrochemical cycle: 7-10 years

200

300

400

500

600

700

800

900

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

USD/ton

Asian crisis

Hamburger crisis

Eurozone crisis

HDPE – Naphtha gap history 1990-2014

3 Note: Prices refer to SEA regional prices

Trough Trough

Trough

200

600

1,000

1,400

1,800

2,200

HDPE

Naphtha

USD

/to

n

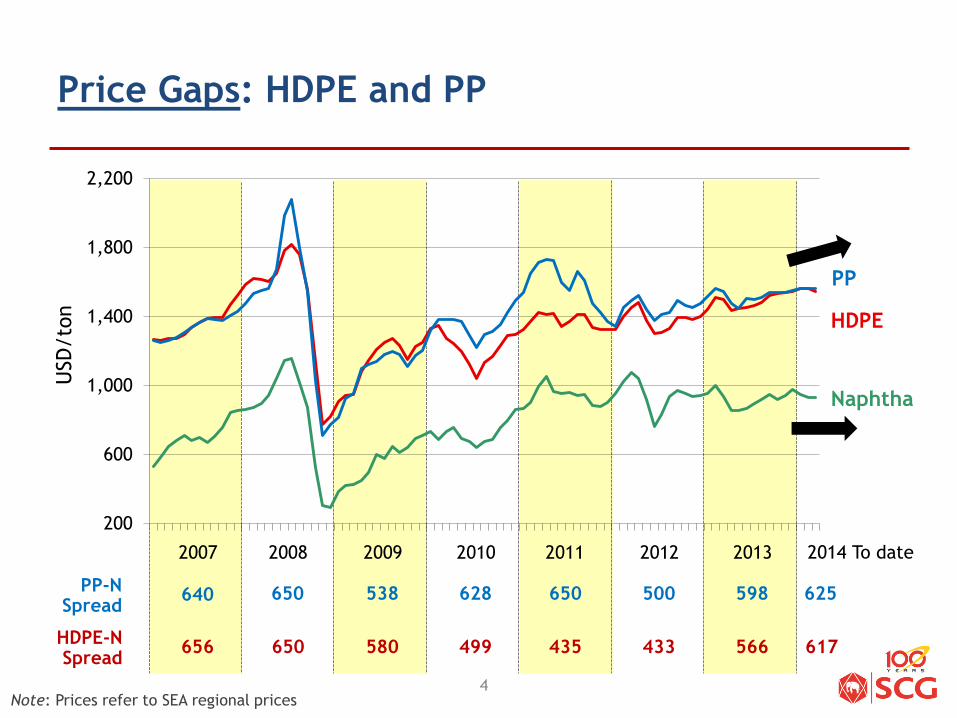

Price Gaps: HDPE and PP

Note: Prices refer to SEA regional prices

PP

PP-N Spread

HDPE-N Spread

625

617

4

2014 To date 2013 2012 2011 2010 2009 2008 2007

598 500

566 433 435 499 580

650 628 538 650

650 656

640

4

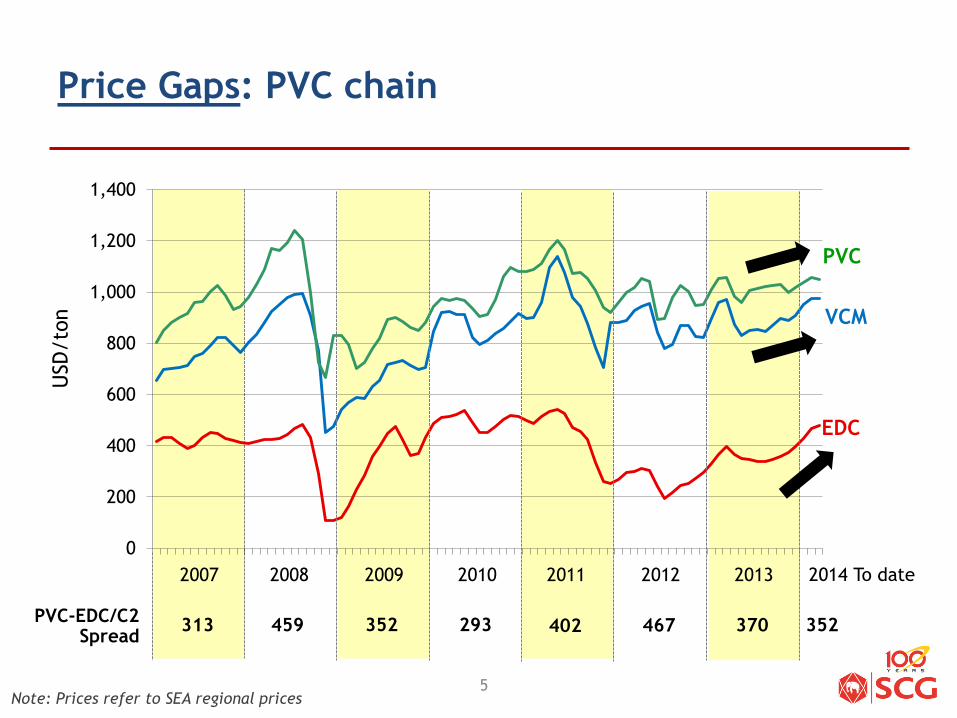

PVC

EDC

VCM

Note: Prices refer to SEA regional prices

Price Gaps: PVC chain U

SD

/to

n

PVC-EDC/C2 Spread

313 459 293

5

0

200

400

600

800

1,000

1,200

1,400

2014 To date 2013 2012 2011 2010 2009 2008 2007

352 402 467 370 352

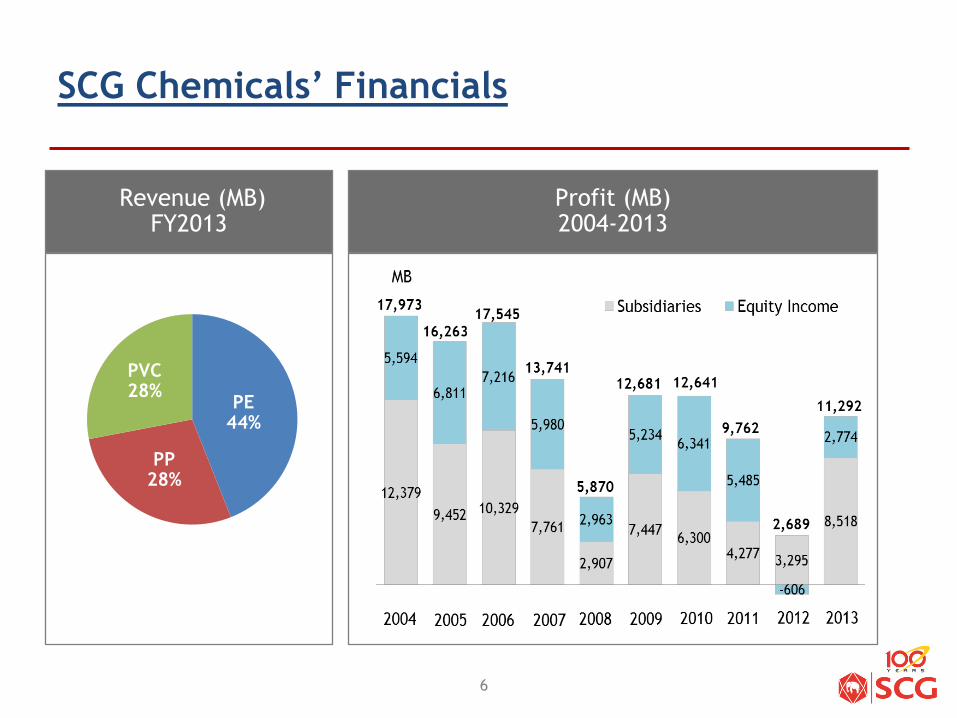

SCG Chemicals’ Financials

Revenue (MB) FY2013

PVC 28%

PE 44%

PP 28%

Profit (MB) 2004-2013

6

- 7 -

Agenda

Where are we in the cycle?

New competing olefins supplies

Our strategies

7

8

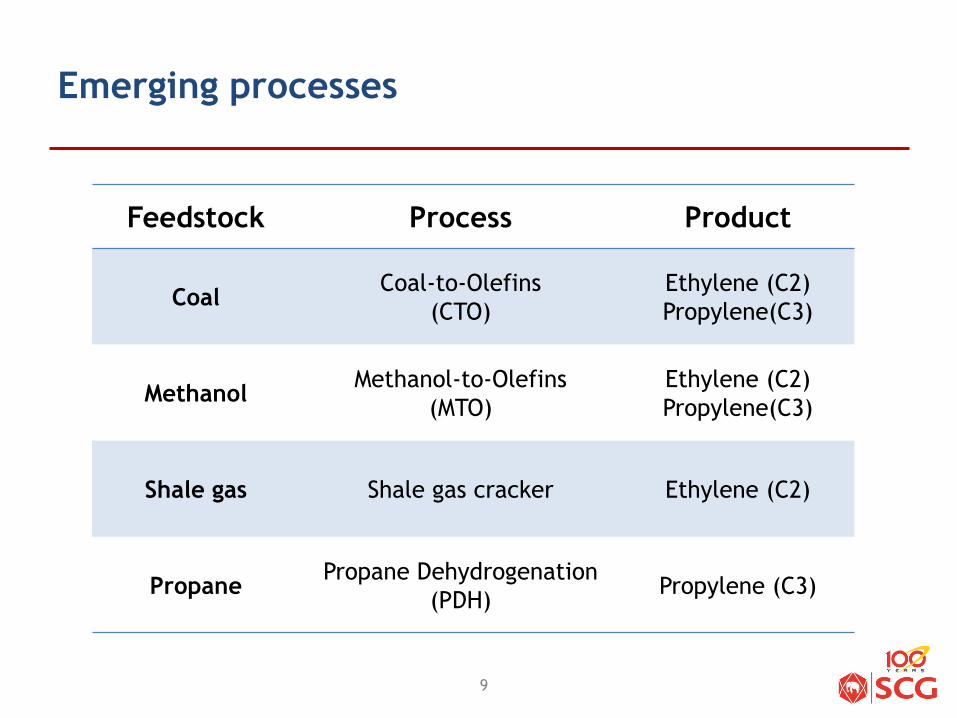

Chemicals feedstock

Pros

(+) Relatively cheaper feedstock

Pros

(+) Good yield of

ethylene (C2) and

propylene (C3)

(+) Lower price in

summer

Pros

(+) Wide product

variety, 50-60%

yield as by-

product

(non-ethylene, non-

propylene)

(+) Easy to transport

Ethane LPG Naphtha

Cons

(-) No product variety, only for ethylene (C2) production

(-) Subject to local availability, due to uneconomical bulk transportation

Cons

(-) High price and

limited supply in winter

Cons

(-) Relatively more

expensive

- 8 -

Coal

Cons

(-) High investment

(-) Environmental

concern; require

large supply of

water and high

CO2 emission

Pros

(+) Relatively

cheaper

feedstock

(+) Abundant of raw

material

- 9 -

Feedstock Process Product

Coal Coal-to-Olefins

(CTO)

Ethylene (C2)

Propylene(C3)

Methanol Methanol-to-Olefins

(MTO)

Ethylene (C2)

Propylene(C3)

Shale gas Shale gas cracker Ethylene (C2)

Propane Propane Dehydrogenation

(PDH) Propylene (C3)

Emerging processes

9

Global ethylene capacity (2018): naphtha and conventional gas accounts for 91% of the capacity

Ethylene global capacity in 2018 by feedstock

Naphtha 48% Conventional

Gas 43%

Shale gas 4%

Coal & Methanol &Others 5%

Incremental Ethylene capacity

2014 – 2018 by region

16% 25%

32%

27%

Note: Operating rate of coastal capacity in China is

subject to seasonal feedstock availability

North America

Middle East

North East

Asia*

South East Asia

Europe & CIS

7%

31% 15%

14%

32%

10

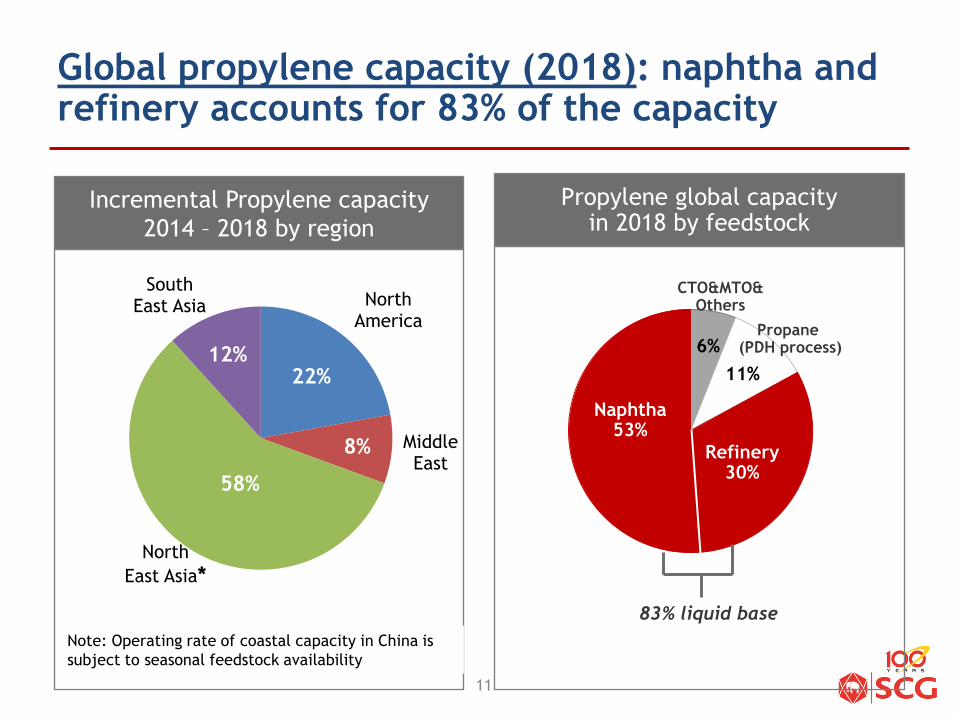

Propylene global capacity in 2018 by feedstock

Naphtha 53%

CTO&MTO& Others

83% liquid base

Refinery 30%

Propane (PDH process)

Global propylene capacity (2018): naphtha and refinery accounts for 83% of the capacity

11

11%

6%

Incremental Propylene capacity

2014 – 2018 by region

16%

30%

7% 47%

Note: Operating rate of coastal capacity in China is

subject to seasonal feedstock availability

North America

Middle East

North

East Asia*

South East Asia

22%

8%

58%

12%

3%

4% 4% 4% 4%

3%

8%

5%

1%

3% 3% 3%

2%

6%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

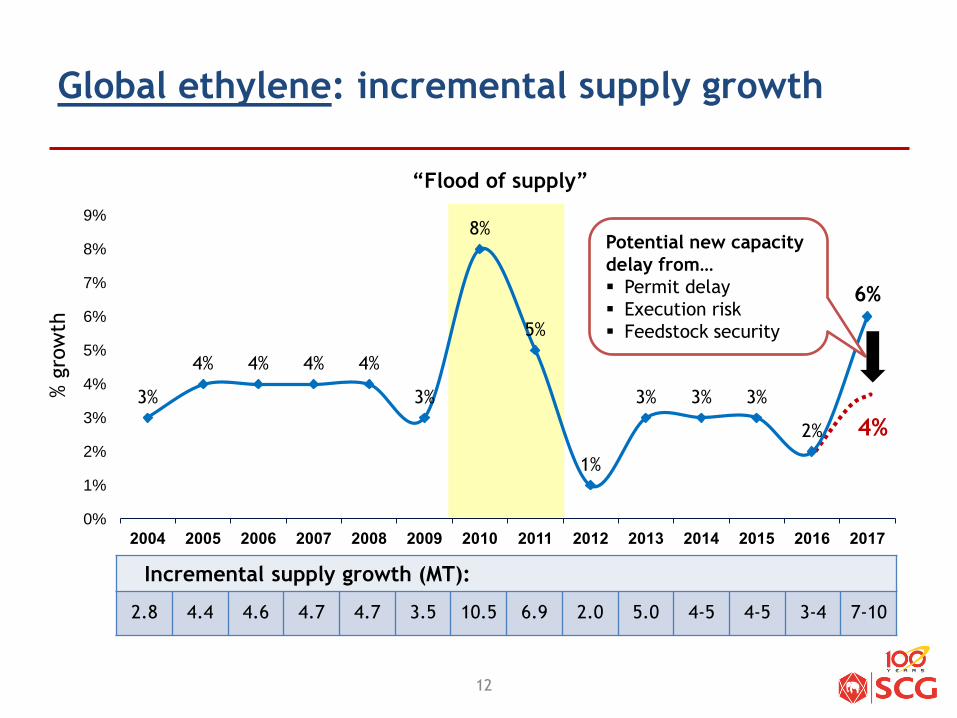

“Flood of supply”

Global ethylene: incremental supply growth

Potential new capacity

delay from…

Permit delay

Execution risk

Feedstock security

4%

% g

row

th

Incremental supply growth (MT):

2.8 4.4 4.6 4.7 4.7 3.5 10.5 6.9 2.0 5.0 4-5 4-5 3-4 7-10

12

- 13 -

Agenda

Where are we in the cycle?

New competing olefins supplies

Our strategies

13

Competitiveness and reduced commodities

effects through HVA (high value added products) and innovation

HVA = High value added products and services

5-10% higher margin

An element of services bundled

- 14 - 14

34% 38%

45% 50%

2010 2011 2012 2013 2010 2011 2012 2013

Note: HVA Sales from Subsidiaries + Associates (100% portion)

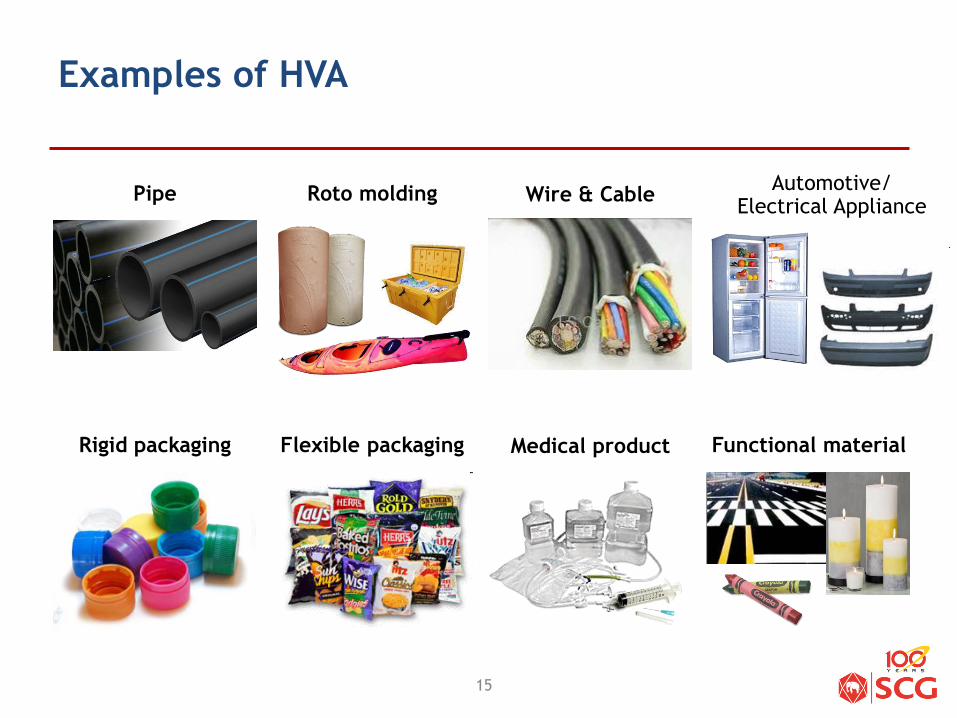

Examples of HVA

- 15 - 15

Pipe Roto molding Wire & Cable Automotive/

Electrical Appliance

Rigid packaging Flexible packaging Medical product Functional material

Co-creation with customers to jointly develop new value added solutions

SCG Chemicals have played

vital part in delivering

success to our customers

- 16 - COCO JELLY 16

+55% of PE/PP are exported to +110 countries

SCG Chemicals

Integrated and competitive operations.

Thailand

Integrated and competitive regional operations

Vietnam

Crackers

ROC (1999)

1.2 MT C2&C3

MOC (2010)

1.7MT C2&C3

Downstream

Subsidiaries Associates

PE

PP

PVC Others

Dow

Mitsui

Chemicals

Mitsubishi

Rayon

JSR

Indonesia

Cracker

CAP (1995)

0.9 MT C2&C3

CAP-Debot (Late-2015)

1.3 MT C2&C3

Cracker

Long Son

Petrochemical (LSP)

1.4 MT C2&C3

Status update • Signed long-term

feedstock agreement

• Signed land lease

advance agreement

• Appointed financial

advisor

• During bidding for

EPC and securing

necessary financing

Downstream

Subsidiaries Associates

PE

PP

SM BD

Michelin (Start up 2017)

17

THANK YOU

18

![VIII Seminário “Desenvolvimento ... - ibracon.org.br1].pdf · C1 C2 C3 C1 C2 C3 C1 C2 C3 C1 C2 C3 C1 C2 C3 C1 C2 C3 R EVEVC R EVEVC 91dias 300dias Volume Total Intrudido de Hg](https://cdn.vdocuments.net/doc/165x107/5c0a1db209d3f2411a8b59c1/viii-seminario-desenvolvimento-1pdf-c1-c2-c3-c1-c2-c3-c1-c2-c3-c1.jpg)