Semiconductor Industry Conference

October 15-17, 1984 Hotel Del Coronado San Diego, California

£:i: I Pui

1290 Ridder Park Drive San Jose, California 95131

(408) 971-9000 Telex: 171973

Sales/Service offices:

UNITED K INGDOM GERMANY DATAQUEST UK Limited DATAQUEST GmbH 144/146 New Bond Street In der Schneithohl 17

London WIY 9FD D-6242 Kronberg 2 United Kingdom West Germany

(01) 409-1427 (06173) 6921 Telex: 266195 Telex: 410939

FRANCE JAPAN DATAQUEST SARL DATAQUEST Japan, Ltd.

41, rue Ybry Azabu Heights, Suite 711 92522 Neuilly-sur-Seine Cedex 1-5-10, Roppongi, Minato-ku

France Tokyo 106, Japan (01) 758-1240 (03) 582-1441 Tfelex: 630842 Telex: J32768

The content of this report represents our interpretation and analysis of information generally available to the public or released by responsible individuals in the subject companies, but is not guaranteed as to accuracy or completeness. It does not contain material provided to us in confidence by our clients.

This information is not furnished in connection with a sale or offer to sell securities, or in connection with the solicitation of an offer to buy securities. This firm and its parent and/or their officers, stockholders, or members of their families may, from time to time, have a long or short position in the securities mentioned and may sell or buy such securities.

Printed in the United States of America. All rights reserved. No part of this publication may be reproduced, stored in retrieval systems, or transmitted, in any form or by any means—mechanical, electronic, photocoptying, duplicating, microfilming, videotape, or otherwise—without the prior written permission of the publisher.

© 1984 Dataquest Incorporated

P l o 2 o »—h

13 CD

3 o < CD

- > i a

r m o 0 u <

r

•

CX^^:^#a Dataquest 1984 SEMICONDUCTOR INDUSTRY CONFERENCE

October 14-17, 1984 Hotel Del Coronado

San Diego, California SUNDAY, October 14

3:00 p.m. to 7:00 p.m. Registration Registration Area 8:00 p.m. to 9:30 p.m. Cocktails Garden Patio

MONDAY, October 15

7:30 a.m. Buffet Breakfast Ballroom 7:30 a.m. Registration Continues Grand Hall Foyer 9:00 a.m. Welcome Regent Empress Room

Howard Z. Bogert Vice President Dataquest Incorporated

9:30 a.m. Semiconductor Outlook—Soft Landing or Hard Regent Empress Room Frederick L. Zieber Senior Vice President Dataquest incorporated

10:00 a.m. The Expanding Universe of Semiconductors Regent Empress Room Chuck Thompson Vice President Director, World Wide IVIarketing l^otorola Semiconductor Sector

10:30 a.m. Coffee Break Regent Empress Room 11:00 a.m. 1984: Before and Beyond Regent Empress Room

Jim Riley Senior Vice President Dataquest Incorporated

11:30 a.m. Bipolar Fights Back Regent Empress Room John C. East Vice President Bipolar Division Advanced l^icro Devices

12:15 p.m. Lunch Ballroom 1:45 p.m. Financial Analyst's Session Stuart Room

(Presentations by Pru-Bache Staff and Industry Executives) Mini-Conference Sessions (Presentations by Dataquest StafO

CAD/CAM and ASICs Regent Empress Room Memory Hanover Room Equipment and Technotogy Windsor Complex

3:00 p.m. Financial Analyst's Session Stuart Room (Presentations by Pru-Bache Staff and Industry Executives) Mini-Conference Sessions (Presentations by Dataquest Staff)

Geographic l i^nds Windsor Complex Microprocessors Oxford Room User Workshop Regent Empress Room

6:00 p.m. Cocktails Promenade Deck 7:00 p.m. Dinner Ballroom 8:30 p.m. Dinner Speaker Ballroom

Economic Outlook—What Will The Election's Impact Be? A. Gary Shilling President A. Gary Shilling and Co., Inc.

9:30 p.m. Informal Discussion and Hosted Refreshments Ballroom (over)

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company / 1290 Ridder Park Drive / San Jose, GA 95131 / (408) 971-9000 / Telex 171973

TUESDAY, October 16

7:45 a.m. Buffet Breakfast Ballroom 8:30 a.m. Pervasiveness—The Perspective Revisited Regent Empress Room

Charles H. Phipps Vice President, Semiconductor Group Manager, Market Development Texas Instruments Incorporated

9:00 a.m. Systems Design At The Chip Level Regent Empress Room Doug Ritchie Vice President Consumer Specific Products National Semiconductor Corporation

9:30 a.m. Distribution, A New Era Regent Empress Room John Abram Executive Vice President Arrow Electronics

10:00 a.m. Coffee Break Regent Empress Room 10:30 a.m. Servicing High-Performance Systems Designers Regent Empress Room

Roger Smullen President and Chief Executive Officer Applied Micro Circuits Corporation

11:00 a.m. Proliferation of Products and Systems in Japan Regent Empress Room Jerry Crowley President and Chief Executive Officer Oki Semiconductor

11:30 a.m. ASICs Come of Age Regent Empress Room Henri Jarrat President and Chief Operating Officer VLSI Technology

12:15 p.m. Lunch Baih lom 1:45 p.m. Applications, The Fuel of Pervasiveness Regent Empress Room

Ken McKenzie Associate Director, Semiconductor Group Dataquest Incorporated

2:15 p.m. Highly Integrated Systems Regent Empress Room Jon Cornell Senior Vice President and Sector Executive Harris Semiconductor

2:45 p.m. Fast CMOS: Key to VLSI Pervasiveness Regent Empress Room T. J. Rodgers President Cypress Semiconductor

3:15 p.m. Telecommunications Impact of Semiconductors .Regent Empress Room Marisa Bellisario Managing Director and Chief Executive Officer Italtel Group

4:00 p.m. Industry Athletic Challenge 10 km Course Once again Lane Mason of the SIS staff will host this industry's annual running event. Sign-ups at the registration desk.

6:00 p.m. Cocktails Garden Patio 7:00 p.m. Dinner—Western Barbeque Garden Patio 9:00 p.m. Informal Discussion and Hosted Refreshments Garden Patio

continued on next pag #

WEDNESDAY, October 17

7:45 a.m. Buffet Brealdast Ballroom 8:30 a.m. Ideas and the Proliferation of Technology Regent Empress Room

Professor Everett M. Rogers Institute for Communications Stanford University Judy Larsen, Ph.D. President Cognos Associates

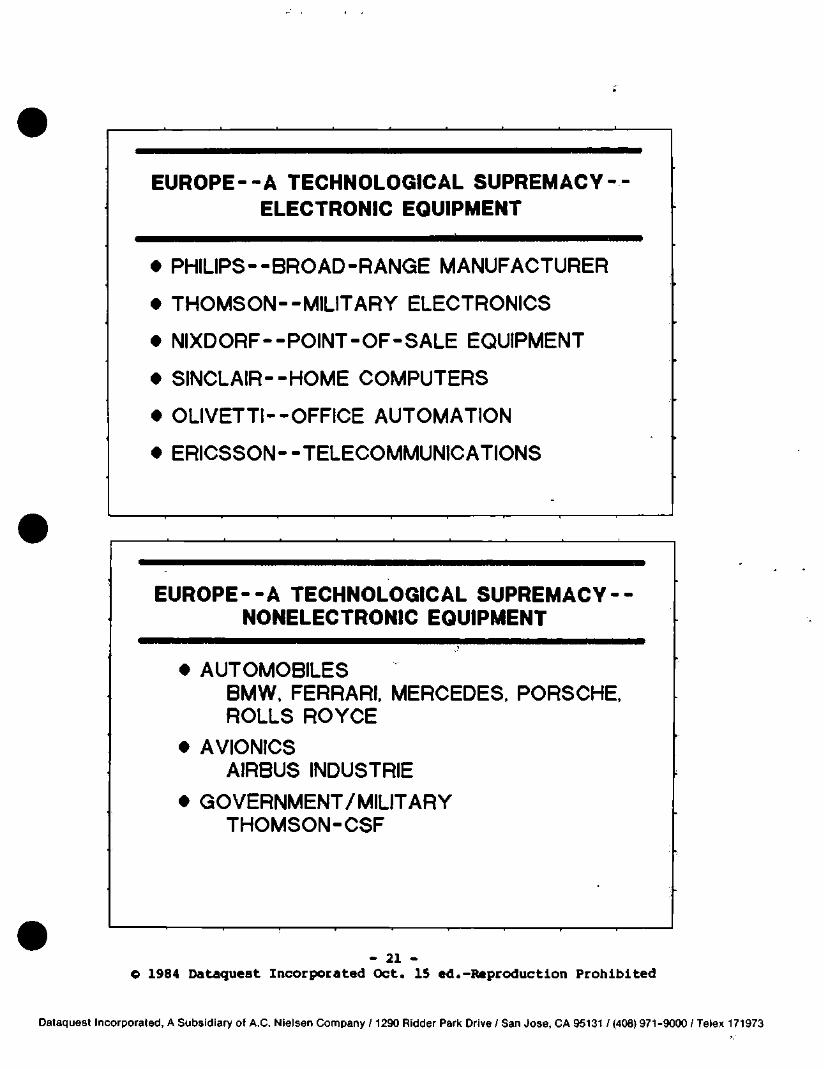

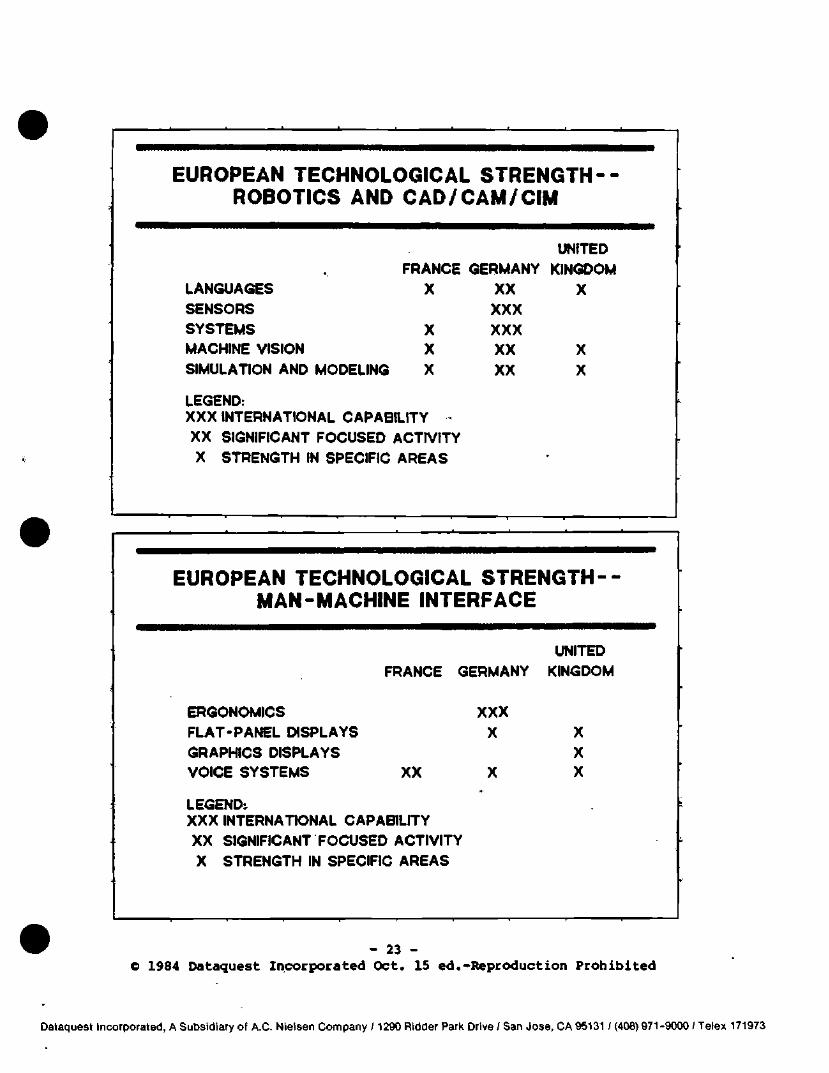

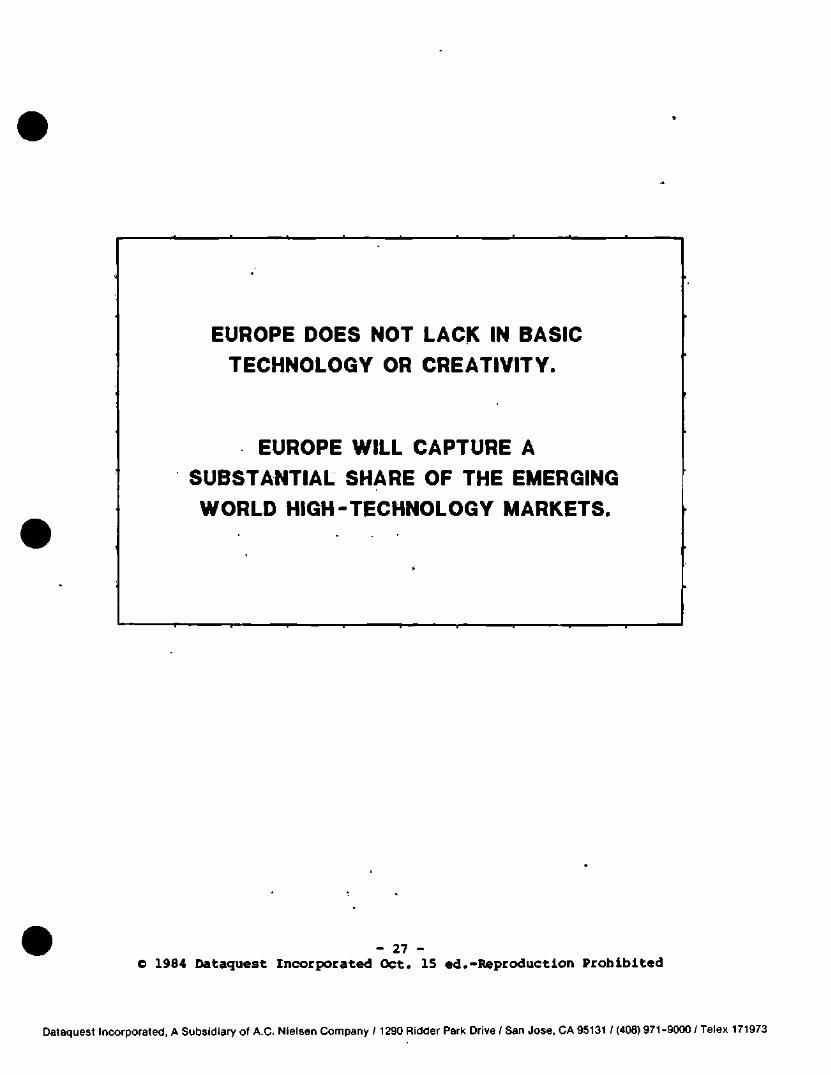

9:00 a.m. Europe—A Technological Backwater? Regent Empress Room Malcolm Penn Director Dataquest U.K. Ltd.

9:30 a.m. Semiconductor Equipment: Key to Pervasiveness Regent Empress Room Bill Bottoms President Semiconductor Equipment Division Varian Associates

10:00 a.m. Coffee Break Regent Empress Room 10:30 a.m. The Impact of Workstation Proliferation Regent Empress Room

Aryeh Finegold President Daisy Systems

11:00 a.m. Service, Software, and Silicon Regent Empress Room Wilfred J. Corrigan President and Chief Executive Officer LSI Logic

11:30 a.m. LSI Growth: 1985-1995 Regent Empress Room Jack Carsten Senior Vice President and General Manager Intel Corporation

12:00 noon Conference Conclusion Regent Empress Room 12:30 p.m. Buffet Luncheon Ballroom

Semiconductor Industry Service

Howard Z. Bogert Mr. Bogert is a Vice President of DATAOUEST and Director of its Semiconductor Industry Service. During his 23 years in electronics, he has held management positions in market research, product planning, long-range planning, research and development, and engineering. Most recently, he was a Divisional Vice President of Engineering for Rockwell International. Earlier, he was Director of MOS Development for Siliconix, and Manager of Design for AMI. Mr. Bogert holds a B.S. degree In Electrical Engineering from Stanford University, an M.S. degree from the University of Maryland, and an M.B.A. degree from the University of Santa Clara.

Kenneth V. McKenzie Mr. McKenzie is Associate Director of DATAQUEST's Semiconductor Industry Service. He is responsible for all research activities on semiconductors and related publications. His other duties include internal data processing coordination for the Semiconductor Industry Service and research into specific end-user markets. During Mr, McKenzie's 14 years in the electronics industry, he has held management positions in both design engineering and marketing. His most recent position was as Marketing Manager at ZIlog, Inc. Prior to that, Mr. McKenzie was Marketing Manager for 8-blt microprocessors at Intel Corporation.

James F. Riley Mr. Riley is a Senior Vice President of DATAQUEST. Previously, he was President of SIgnetics, a subsidiary of Corning Glass Works Incorporated, and of Intersil Incorporated. He has 20 years of experience In the semiconductor Industry, the last nine of which have been with DATAQUEST. Mr. Riley has considerable experience In corporate planning, marketing, and general management. Mr. Riley received a B;S. degree in Business Administration from Lehigh University, where he was elected to Phi Beta Kappa.

Frederick L. Zieber Mr. Zieber is a Senior Vice President of DATAQUEST, a member of Its Executive Committee, and the Director of Its Semiconductor Group. The Semiconductor Group Includes the Semiconductor Industry Service, the European Semiconductor Industry Service, the Japanese Semiconductor Industry Service, and the Semiconductor User Information Service Mr. Zieber has 12 years of experience in market research and consulting to the semiconductor industry, and previously worked in the semiconductor industry for nine years. He has experience in processing, designing, manufacturing, and testing integrated circuits and discrete devices. He holds two patents in semiconductor processing. Mr. Zieber has a B.S. degree In Electrical Engineering from Stanford University and an M.B.A. degree from the Graduate School of Business at Stanford University.

Lane iVIason Mr. Mason is a Senior Industry Analyst for DATAQUEST's Semiconductor Industry Service. He has been with DATAQUEST for five years, during which time he has gained Increased responsibility for coverage of MOS memory markets and company analyses, as well as general research support. Mr. Mason has worked for Hughes Aircraft and Raychem Corporation. He has a B.S. degree in Physics from the California Institute of Technology, and has done graduate work at U.C.L.A. in the Department of Economics.

(over)

Robert E. IVIcGeary Mr. McGeary is a Senior Industry Analyst for DATAQUEST's Semiconductor Industry Service. Prior to joining DATAQUEST, he was Product Marketing Manager at Applied Materials, Inc., where he managed the worldwide product marketing activities for the Dry Etch Division and managed product support for European dry etch business. Previously, he worked as Product Marketing Manager at GCA Corporation/IC Systems Group, as Accelerator Physicist at Lawrence Berkeley Laboratories, as a Nuclear Engineer at Mare Island Naval Shipyard, and as a Reactor Operator at the University of Washington. He received B.S. degrees in Physics and Mathematics from the University of Washington and an M.B.A. degree from St. Mary's College.

Andy Prophet Mr. Prophet is a Senior Industry Analyst for DATAQUEST's Semiconductor Industry Service. He is responsible for analyzing the application-specific market environment and future technology trends. Prior to joining DATAQUEST, he was Market Segment Manager for Synertek, Inc., and was responsible for major account marketing strategies for its customers. Previously, Mr. Prophet was CAD Director, Product Line Manager, and Circuit Design Manager at American Microsystems, Inc., and Teledyne. He has a B.S.E.E. degree from Illinois Institute of Technology, an M.S.E.E. degree from San Jose State University, and an M.B.A. degree from the University of Santa Clara.

IVIel Thomsen Mr. Thomsen is a Senior Industry Analyst for DATAQUEST's Semiconductor Industry Service. He is responsible for analyzing the market environment and future technology trends for microprocessors, microperipherals, and microcontrollers. Prior to joining DATAQUEST, he was Product Marketing Manager for Aehr Test Systems and was responsible for marketing dynamic burn-in systems used for reliability testing of digital integrated circuits. Mr. Thomsen has also held positions as a Product Marketing Manager and as Field Applications Engineer at Zilog, Inc., as Senior Design Engineer at Heathkit, and as Design Engineer at Magnavox, Inc., and at Sylvania Systems Division. He has a B.S.E.E. degree from the University of Michigan and an M.S.E.E. degree from Purdue University.

Gall Kelton-Fogg Ms. Kelton-Fogg is an Industry Analyst for DATAQUEST's Semiconductor Industry Service. Her area of responsibility is the end-use segmentation of semiconductor consumption, including application, geographical, and distribution analysis. Ms. Kelton-Fogg has worked in technology assessment, market research, and consulting for five years. Prior to joining DATAQUEST, she was with SRI International and the University of California, San Francisco. She has B.S. and M.S. degrees in Scientific Journalism from the University of Wisconsin-Madison.

Thomas E. Holland Mr. Holland is a Research Analyst for DATAQUEST's Semiconductor Industry Service. For the past three years, Mr. Holland has been active in research in the linear, discrete, and optoelectronic semiconductor markets. Prior to joining DATAQUEST, he was Director of Research at Technical Operations (West), where he directed company- and DOD-sponsored research and development. He also served as a consultant to the Director of Defense Research and Engineering on classified DOD programs. As a staff physicist at the Los Alamos Scientific Laboratory, he conducted basic research in detonation and shock phenomenology. He received B.S. and M.S. degrees in Mathematics and Physics from the University of Alabama.

Barbara Van Ms. Van is a Research Analyst for DATAQUEST's Semiconductor Industry Service. She is responsible for computer data bases in semiconductor consumption, market share analysis, and company financial analysis. Prior to joining DATAQUEST, she worked in a research capacity for a marketing research firm. Ms. Van has a B.A. degree in Commerce from the University of Santa Clara.

Arden DeVincenzi

Ms. DeVincenzi is a Research Analyst for DATAQUEST's Semiconductor Industry Service. Her responsibilities include research and analysis of the semiconductor industry with respect to equipment and materials. Prior to joining DATAQUEST, she worked in a computer systems marketing group where she maintained a nationwide distribution network, developed and coordinated marketing programs, and provided technical assistance on IBM, NCR, and Honeywell systems Ms. DeVincenzi received a B.S. degree in Marketing and Finance from California Polytechnic State University, San Luis Obispo

Katy Guill

Ms. Guill is a Research Associate with the Semiconductor Group. While at DATAQUEST, she has worked on projects including worldwide semiconductor forecasts, economic models, and development of computer data bases. Currently, she assists Mr. Mason in the memory market area and provides general research support, Ms. Guill received a B.S. degree in Business Administration from California Polytechnic State University, San Luis Obispo.

Janet M. Rey

Ms. Rey is a Research Associate for DATAQUEST's Semiconductor Industry Service. She assists in researching microprocessors, microperipherals, and microcontrollers. She has worked for Intel Corporation and Atari, Incorporated. Ms Rey received a B.S. degree in Business Administration from San Jose State University.

^wm

Anthea C. Stratigos

Ms. Stratigos is a Research Associate for DATAQUEST's Semiconductor Industry Service. Before joining DATAQUEST, she was an Information Developer for IBM Corporation, where she documented and supported software development and products for IBM's mainframe systems Ms Stratigo has a B.S. degree in Communication from Stanford University

1290 Ridder Park Drive / San Jose, CA 95131

(408) 971-9000 Telex: 171973

Dataquest

(:::a Dataquest

Dataquest

SEMICONDUCTOR INDUSTRY CONFERENCE EVALUATION QUESTIONNAIRE

San Diego, California October 15-17, 1984

Thank you for attending our Semiconductor Industry Conference. Would you please assist us in planning our next conference by completing and returning this questionnaire?

1. Please rate each presentation on a scale of 1 to 10 (where 10 is highest in terms of your approval):

CONTENT DELIVERY (1 to 10) (1 to 10)

COMMENTS (Use reverse side if necessary)

Zleber, Industry Outlook

Thompson, Expanding Universe

Riley, Before and Beyond

East, Bipolar

Ptiipps, Pervasiveness Perspective

Ritchie, Systems Chip Design

Abram, A New Era

Smullen, Servicing Systems

Crowley, Proliferation in Japan

Jarrat, ASICs Come of Age

McKenzie, Applications

Cornell, Integrated Systems

Rodgers, Fast CMOS

BellisarIo, Telecommunications

Rogers and Larsen, Ideas

Penn, European Backwater

Bottoms, Equipment Pervasiveness

Finegold, Workstation Impact

Corrigan, Service and Silicon

Carsten, LSI Growth

2. Mini-conference Evaluation. Please rate the meetings you attended on a scale of 1 to 10 (where 10 is highest in terms of your approval):

CONTENT DELIVERY (1 to 10) (1 to 10)

COMMENTS (Use reverse side if necessary)

CAD/CAM and ASIC

Equipment and Technology

Memory

Microprocessors

(over)

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company / 1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

2. Mini-conference Evaluation (Continued).

CONTENT DELIVERY COMMENTS Geographic Trends

User Worl<shop —

Financial

3. Would you like more mini-conferences at next year's SIS Conference? Yes No

4. At our next industry conference, would you prefer more or less of the following types of speakers?

MORE LESS

DATAOUEST Speakers

Speakers from Large Semiconductor Companies

Speakers from Small Semiconductor Companies

Speakers from Semiconductor Users

Speakers from Semiconductor Equipment and Materials Suppliers

Speakers from Distributors

Speakers from the Financial Community

5. Please suggest other types of speakers you might like to hear.

6. How would you rate the conference facilities (1 to 10)?

Location Guest Rooms Meals Meeting Rooms Recreational Facilities

7. Topics that would be of interest to you for the next Semiconductor conference:

8. Comments:

9. Your primary interest in the semiconductor industry is as a: Manufacturer

Service Vendor User Financial Analyst Other (Please Specify)

Name and Company (optional)

Dataquest

Taizo Abe

John Abram

Irv Abzug Harriet Abzug

Jet Advani

Edgar Anderson

Shelley Anderson

Giuseppe Anerdi

Alex Au

Erick Ayers

Willi Bacher

Bob Ball

Juan Bardina Patricia Bardina

lann Barron

John Baskett

Larry Baxter

Pete Bejarano

Terry Bell

Dr. Albert Belle Isle

Marisa Bellisario

Carol Bender

Giarmi Bertolini

SEMICONDUCTOR INDUSTRY CONFERENCE October 15 through 17, 1984

San Diego, California

List of Attendees

Shinko Electric Industries Company, Ltd.

Arrow Electronics

IBM Corporation

IBM Corporation

Messerschmitt-Boelkow-Blohm GmbH

Bank of the West

Fiat Semelco

Vitelic Corporation

Motorola Inc

Dimos AG

SAI-SEMI Specialists

Atcor Corporation

INMOS Corporation

Panatech Semiconductor

Dexter Corporation-Hysol Division

Trilogy Systems

Micro Component Technology

Custom Silicon, Inc.

Italtel Telematica

Dataquest Incorporated

Italtel Telematica

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company /1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Max Bertolino-Zan

Prakash Bhalerao

Jacques Biais

Robert Bickers

John Birkner

Anthony Blenk

Randy Block

Abe Bluestone

Betty Bluford

Howard Bogert Carol Bogert

Dmitry Bosky

G. William Bothwel1

Patricia Bothwel1

Timothy Bottoms

Wi 11 iam Bottoms

Thomas Bowman

Ken Brabitz

Del Brand Julie Brand

Kathy Braun

Holger Bree

Alan Brigish

George Bristol

Donald Brooks Teresa Brooks

Ing. C. Olivetti &C., S.p.A.

Digital Equipment Corporation

Rhone-Poulenc

Atcor Corporation

Monolithic Memories

Mutual of New York

Storm, Block & Associates

Teradyne, Inc.

Dataquest Incorporated

Dataquest Incorporated

Security Pacific Capital Corporation

Northern Telecom, Ltd

Northern Telecom, Ltd

Bank of America

Varian Associates

Applied Materials. Inc.

Digital Equipment Corporation

ITT Semiconductors

Western Digital Corporation

Messerschmi tt-Boelkow-Blohm GmbH

Videolog

Prudential-Bache Securities

Fairchild Camera & Instrument Corporation

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company /1290 Bidder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

C . "Kip" Brown

Neill Brownstein

Stan Bruederle

Joan Bui lock

Robert Bullock

Ron Butler

Josh Camba Miriam Camba

Franco Carnevali

Jack Carsten

Wade Chang

Dennis Chant

Sen Chen

Adam Chowaniec

Jack Christy

Lee Chu

Vic Chuidian Joanne Chuidian

E . Dennis Col bourne

Peyton Cole

Tom Col 1 ins Susan Col 1 ins

Perry Constantine

Tito Conti

Jon Cornel 1 Mary Cornel 1

MOS Electronics Corporation (MOSEL)

Bessemer Venture Partners

Dataquest Incorporated

Indium Corporation' of America

Indium Corporation of America

Teradyne, Inc.

Interlek, Inc.

Telettra S.p A.

Intel Corporation

ERSO/ITRI

Plessey Solid State

Air Products <Sc Chemicals, Inc.

Commodore International, Ltd.

Mitsubishi Electric Corporation

Mostek Corporation

Interlek, Inc.

Northern Telecom Electronics, Ltd,

Fairchild Camera & Instrument Corporat ion

Tandem Computers, Inc.

LSI Logic Corporation

Ing. C. Olivetti & C , S . p . A .

Harris Semiconductor

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company /1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Wilford Corrigan Sigrun Corrigan

Gary Cowles

Patricia Cox

Wi 11iam Creamer

Herbert Criscito

Jerry Crowley Nancie Crowley

Bill Cruizkshank Donna Cruizkshank

John Cummings

Joseph Curry

A. C. D'Augustine

Colman Daniel

Peter Danna Lorraine Danna

Edward Day

Ardan DeVincenzi

Michael Denick

Edward Desmond

Mark Desrosiers

Bea Destin

Daniel Devine

Tom Dexel

Stephen Dexter

Dr. Vir Dhaka

LSI Logic Corporation

Datapoint Corporation

Dataquest Incorporated

Bank of America

RCA Corporation

Oki Semiconductor

Shinko Electric America

Electric Power Research Institute

Semiconductor Microelectronics Internalional

INMOS Corporation

Hami1ton/Avnet

Philip A. Hunt Chemical Corporation

Motorola, Inc.

Dataquest Incorporated

IBM Corporal ion

IBM Corpora t ion

IBM Corporal ion

Dataquest Incorporated

Temescal

Dataquest Incorporated

Sears Investment Management Company

Micromos

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company / 1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Henry Dieselman

James Diller June Diller

John Dishman

Hubert Dohman Martha Dohman

Richard Douglas

William Douglass

Emi 1io Dragoni

Phi 11ip Drayer

Richard Dressier

Kevin Driscol 1

Roger Dunbar

John East

Robert Eckelmann

Ola Eckholm

Oliver Edwards

Jeffrey Ehr1ich

Mahmoud Elhamamsy

Mark ElIsberry

Richard Engli sh

Aldo Enrici

Wi11lam Everden

J im Favier

Beverly Feldman

Aryeh Finegold

Perkin-Elmer Corporation

Sierra Semiconductor Corporation

AT&T Bell Laboratories

Monsanto Electronic Material Company

Data General Corporaton

AMP, Inc.

Italtel Telematica

Enviro i imental Processing, Inc.

Mostek Corpo ra t ion

Digital Equipment Corporation

Arthur Young Sc Company

Advanced Micro Devices, Inc.

United States Department of Commerce

LM Ericsson Corporation

Motorola, Inc.

General Electric Company

AT&T Information Systems

Holt, Inc.

Hitachi America, Ltd.

AT&T Information Systems

Mullard. Ltd

Philip A Hunt Chemical Corporation

Digital Equipment Corporation

Daisy Systems Corporation

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company / 1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Doug Finke

Frank Florence

Karen Foley

Pete Fowler

Linda Fredericks

Werner Freiesleben

Harvey Frye

Brian FulImer

Orlando Gal legos

Penny Gal legos

Antonio Garcia Carolyn Garcia

David Garni tz

Tom Get linger

Jerry Gibbs

Kenneth Giles

Sara Giles

Marshall Gingold

Gene Goebel

J im Goldey Jeanne Goldey

Bob Gonzalez

Oliver Goold

Michael Graff

Milton Graimatt, III

Alan Grebene

Intel Corporation

Dataquest Incorporated

Dataquest Incorporated

INMOS Corporation

Harris Semiconductor

Wacker Siltronic Corporation

Eaton Corporation

Datapoint Corporation

Zytrex Corporation

Dataquest Incorporated

Interlek, Inc.

First National Bank of Boston

Prudential-Bache Securities

ZyMOS Corporation

Bipolar Integrated Technology, Inc

Bipolar Integrated Technology, Inc

AT&T Bell Laboratories

Shipley Company, Inc

AT&T Bell Laboratories

Motorola, Inc

GBL/Goold Electronics Corporation

Harris Corporation

Lex Service, Inc.

Microlinear Corporation

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company / 1290 RIdder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Rupert Grimm

Wendy Grossmen

Katy Guill

Paul Gupta

Dave Guzeman

Sardar Haddad

Bernard Hadley

Erick Hagmann

Iza HalIberg

Brendan Halpin

S. Ham

Donald Hamman

Fred Haney Barbara Haney

Mike Hankal

J. Harris

Basil Harrison

Paul Hart

Dan Hauer

John Hayn

John Height ley

Joseph Hei tz

Tom Hendrickson

Anna Henery

Carl Hildebrand Gail Hildebrand

BA Investment Management Corporation

Monsanto Electronic Material Company

Dataquest Incorporated

Inters!1, Inc.

ZyMOS Corporation

Mostek Corporation

Stack GnbH

Fairchild Camera & Instrument Corporation

Dataquest Incorporated

IDA Ireland

Tristar Semiconductor, Inc.

Teradyne, Inc.

Investors in Industry

Dataquest Incorporated

Acrian, Inc.

IBM Corporation

Hughes Aircraft Companv

S-MOS Systems, Inc.

McDonnell Douglas Microelectronics

INMOS Corporation

Telic-Alcatel

VHSIC Technology Corporation

Investors in Industry

Perkin-Elmer Corporation

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company / 1290 Bidder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Jay Hoag

John Hodgson

Bob Hoffman

Adrian Hohn

Michael Hollabaugh Debbie Hollabaugh

C h a r l e s Holt

Jennifer Hughes

Annmarie Ihle

Elizabeth Isaacs

John Jackson

Richard Jacobs

Richard Jacobs

Henri Jarrat

Frank Jelenko

Bob Jenkins Carolee Jenkins

Carl Johnson

Dwight Johnson

Dave Jones

Eric Jones

Hisao Kanamaru

Bert Kehren

Anthony Keig

James Kelley

Gail Kelton-Fogg

Citibank

VHSIC Technology Corporation

IBiA Corporation

LTX Corporation

International Microelectronic Products

Xerox Corporation

Ketchum Public Relations

IBM Corporal ion

Monsanto Electronic Material Company

Dataquest Incorporated

AT&T Bell Laboratories

Schweber Electronics, Inc.

VLSI Teclmology, I n c .

NEC Electronics USA, Inc.

Motorola, Inc.

.Zilog, Inc.

Eastman Kodak Company

Interlek, Inc

Bank of the West

Hitachi, Ltd.

Mostek Corporation

Union Carbide Corporation

NEC Electronics USA. Inc.

Dataquest Incorporated

Dafaquest Incorporated, A Subsidiary of A.C. Nielsen Company /1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

G. Mart Kernahan Elaine Kernahan

Jerry Kiachian

Gary Kibblewhite

Marshall Kidd

Charles Kimball

Marilyn Kissel

Richard Klein

Richard Konrad

Abe Kosakowsky

Andrew Koshar

C. V. Kovac

Fran Krch

Dan Krupka

Robert Kuhling

Hans Kurner

Burt Lancaster

Terry Lancaster

Dr. Judy Larsen

Richard Lawry Christine Lawry

George LeCrenn

Bob Lee Dorma Lee

Sang Lee Een Yearp Lee

Yong Lee

Exiiios Semiconductor Corporation

Intersi1, Inc.

LEX Corporation

General Electric Trust Investment

Morgan Guaranty Trust

Signetics Corporation

Prudentia1-Bache Securities

Synertek, Inc.

SAI-SEMI Specialists

Japan Electronics Bureau

Rockwell International Corporation

GTE Microcircuits

AT&T Bell Laboratories

Calma Company

ESEC USA Inc.

Air Products Sc Chemicals, Inc.

DuPont Pension Fund

Cognos Associates

Atcor Corporation

Hoya Corporation, Electronics Division

Aetna Life and Casualty

Tristar Semiconductor, Inc.

Hyxmdai Electronics America

Dataquest Incorporated, A Subsidiary of A.C Nielsen Company / 1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Mike Leibowitz

Robert Lenz

Kenneth Levy Gloria Levy

Edward Linde

Bob Lipp

C. Fred Little Betsy Little

Jay Litus, J r .

Herschel Loomis

Alan Louwerse

Ron Love 1 and

Paul Lovett Anne Lovett

Toby Mack

Azmat Maiik

Joe Marcello Betty Marcello

Dieter Marenbach

Bernard Marren

Harry Marshal 1

Randy Marshal 1

Jaime Martin

Jim Mart in Diane Martin

Lane Mason

Peter Masucci

Quality Automation, Inc.

RCA Corporation

KLA Instruments, Inc

IBM Corporation

California Devices, Inc.

Interconics

Toshiba America, Inc.

Naval Postgraduate School

ZyMOS Corporation

Department of Trade and Industry

Air Products & Chemicals, Inc.

National Electronic Distributors Association

Mitsubishi Electronics America, Inc

Interiek, Inc.

Western Digital Corporation

Western Microtechnology

J H. Whitney & Company

Raytheon Corporat ion

California Devices, Inc.

Capital Research Company

Dataquest Incorporated

Digital Equipment Corporation

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company / 1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

John Matlock

Gunter Matthai Paula Matthai

James McElwee

Robert McGeary

Ken McKenzie Debra McKenzie

Cameron McPhail

D. A. Mehta

Vern Meissner Dolores Meissner

Patricia Me laugh

John Mel gal vis

Arthur Midi 1i

Graham Mi 1ler

Norman Mi 1ler

Ralph Mi Her

Thomas Mino

Alicia Morehouse

Rick Morrison

Jack Murphy

Satoshi Nagata

Thomas Nelson

Ed Neubauer

Jean Paul Neuville

James Newcomb

S.E.H. .America

Robert Bosch CtaibH

Security Pacific Capital Corporation

Dataquest Incorporated

Dataquest Incorporated

Scottish Development Agency

AT&T Bell Laboratories

Wacker Siltronic Corporation

Bank of New York

IBM Corporation

Wells Electronics, Inc

LTX Corporation

Microlinear Corporation

TRW, Inc.

AT&T Technologies, Inc.

Dataquest Incorporated

AT&T Technologies, Inc

Philip A Hiuit Chemical Corporation

Mitsui High-Tek, Inc.

Union Carbide Corporat ion

NEC Electronics USA, Inc.

Sagem

Dataquest Incorporated

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company / 1290 Bidder Parl< Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Chr i s Newham

Jack Ni I s s o n

Gene Norreit

Mark Norwood

Bill O"Byrne

Dan 0'Nei11

Mary Olsson

Jack Ordway

Richard Orri11

Drew Osterman

Jean Page

Giovanni Pagliosa

Robert Palmer

Dennis Parker

Gerald Parker

Michael Pawlik

Malcolm Penn Gill Penn

Randall Peters

James Peterson

Richard Petritz Grace Petritz

Larry Phi 11ips

Charles Phipps

Fairchild Camera & Instrument Corporation

Hewlett-Packard Company

Dataquest Incorporated

Intel Corporation

Honeywe11, Inc.

Adler & Company

Dataquest Incorporated

Vitelic Corporation

IBM Corporation

International CMOS Technology

Dataquest Incorporated

Honeywell ISI, S.p.A.

Mostek Corporation

INMOS Corporation

IBM Corporation

Fairchild Camera & Instrument Corporation

Dataquest Incorporated

Texas Instruments, Inc.

Silicon Systems, Inc.

INMOS Corporation

Lehman Management Company

Texas Instruments, Inc.

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company / 1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Martin Plotkin

Kathryn Plumb

James Poitras

Tom Popek

Skip Powers

Nand Prasad

Walter Price

Andrew Procassini

Timothy Propeck

Andy Prophet

Christine Ragoucy

Gerald Ramsey

John Raszcewski

Paul Reagan

N. Damodar Reddy

Daniel Reeves

Janet Rey

Thomas Reynolds Maryanne Reynolds

Donald Richard

J im Riley

Douglas Ritchie

George Robertson

Peter Roche

T. J Rodgers Kathleen Rodgers

Fairchild Camera & Instrument Corporation

First Interstate Bank

General Electric Company

Zilog, Inc.

XTAR Electronics, Inc.

Interlek, Inc.

Rosenberg Capital Management

Hyundai Electronics America

Monolithic Memories

Dataquest Incorporated

Dieli

AT&T Technologies, Inc.

I ^ Corporation

GCA Corporation

Modular Semiconductor, Inc.

Eaton Corporation

Dataquest Incorporated

Sierra Semiconductor Corporation

Atari Corporation

Dataquest Incorporated

National Semiconductor Corporation

Interlek, Inc.

Data General C o r p o r a t o n

Cypress Semiconductor C o r p o r a t i o n

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company / 1290 Bidder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Everett Rogers

Enzo Rognoni

Geoff Rowett

Dave Royse

Robert Rusnack

Malcolm Russ

A. Graham Sadler

Frank Semnann Nancy Samnann

Bi 11 Sams

Judy Sanchez

Richard Santi11i

Robert Santos Midge Santos

Edwin Sauve'

Dick Schaeffer

Tom Schauf

John Scholes

John Schumacher

Susan Scibetta

E. Weston Seaman Betsy Seaman

Frank Seestrora Joaim Seestrom

Monte Seiters

Jerry Shames

John Shea Flor Shea

Stanford University

Ing. C. Olivetti & C , S.p.A.

LTX Corpo ra t ion

IBM Co rpo ra t ion

IBM Corporation

Wacker Siltronic Corporation

Northern Telecom Electronics, L t d .

Dataquest Incorporated

Assisted Technology

Bank of America

RCA Corporation

Hewlett-Packard Company

First Interstate Bank

The Wall Street Journal

Dynamit Nobel Silicon, Inc.

Thorn-EMI

J. C. Schumacher Company

Dataquest Incorporated

IBM Corporation

Pitney Bowes, Inc.

Northern Telecom, Ltd.

Burroughs Corporation

LSI Logic Corporation

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company / 1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Alan Shepherd Edith Shepherd

C . T. Shih

A. Gary Shilling

Sei Shohara

Art Sidorsky

Robert Silco Dorothy SiIco

Thoma s S i ngman

Brian Sjolseth

James Smith

Stratton Smith

Roger Smullen

Moo-Youl Sohn

Chaney Steinman

John Stewart

Anthea Stratigos

Rahul Sud

Michael Swaluk Lynn Swaluk

Frank Swiatowiec

Dave Sylvester

Kimio Takemori

Hiroo Taniguchi

Sheridan Tatsuno

Lloyd Taylor

Ferranti Electronics Limited

ERSO/ITRI

A. Gary Shilling and Company, Inc.

Xerox Corporation

standard Microsystems Corporation

VLSI Technology, Inc.

Union Carbide Corporation

IBM Corporation

Harris Corporation

Teradyne, Inc.

Applied Micro Circuits Corporation

Samsung Semiconductor & Telecommiuiicat ions Company, Ltd.

Ketchum Public Relations

GCA Corporation

Dataquest Incorporated

Lattice Semiconductor Corporation

Pitney Bowes, Inc

Trilogy Systems

San Jose Mercury News

Suwa Seiko Sha

Mitsubishi Electronics America. Inc

Dataquest Incorporated

Coiranodore I n t e r n a t i o n a l , L td .

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company / 1290 Bidder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Wallace Tchon

James Tempesta

Chuck Thompson Wanda Thompson

Mel Thornsen

M W. Thurlow

Lou Tieber

Jack TiIs

Jim Townsend

Mario Tripputi

Mentor Tseng

Lowel1 Turri ff

Barbara Van

Joe Van Poppelen

James Van Tassel

Robert Vosika

W Scott Walker Cassie Walker

Jan Waluk Dominique Waluk

Xicor, Inc.

Bank of America

Motorola Semiconductor, Inc.

Dataquest Incorporated

Smith Industries

Interlek, Inc

SAI-SEMI Specialists

Toshiba America, I n c .

Italtel Telematica

ERSO/ITRI

Cypress Semiconductor Corporation

Dataquest Incorporated

National Semiconductor Corporation

NCR Corporation

Micro Component Technology

Hughes Aircraft Company

Megatest Corporation

James Wei

Michael Weisberg

Jeff Wellington

Gunnar Wetlesen Mary Ellen Wetlesen

Rick Whittington

Col in Wiggins

Sharp Electronics Corporation

Prudentlal-Bache Securities

First National Bank of Boston

W & W Enterprises

Prudential-Bache Securities

Exxon Corporation

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company / 1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

William Wiley

Ray WiIfinger Mildred Wi Ifinger

Walter Willett

Jack Wi Ison

Otis Wolkins

N. Wood

J. Michael Worfolk

John Wunner

K. K. Yawata

Richard Yeung Paula Yeiuig

Phil Young Cynthia Young

Sam Yoxuig

Jonathan Yu

Tony Yu

Aldo Zana

Robert Zanotti

John Zeigler

Steve Zelencik Harriet Zelencik

Frederick Zieber Libbe Zieber

Bi11 Zubenko

John Zucker

First Interstate Bank

IBM Corporation

Union Carbide Corporation

Business Week

GTE M i c r o c i r c u its

Lex Service, Inc.

Lex Service, Inc.

Varian Corporation, Exitron Division

NEC E l e c t r o n i c s USA, Inc.

Capital Research Company

The Hibernia Bank

Exel Microelectronics, Inc.

Applied Microcircuits Corporation

United Microelectronics Corporation

Italtel Telematica

Aerospatlale

General Electric Company

Advanced Micro Devices, Inc.

Dataquest Incorporated

DuPont Pension Fund

Mitsubishi Electronics America, Inc.

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company / 1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

(:|K\ Dataquest

Dataquest

SEMICONDUCTOR INDUSTRY CONFERENCE October 15 through 17, 1984 San Diego, California

List of Attendees

A. Gary Shilling and Company, Inc. A. Gary Shilling, President

AMP, Inc William Douglass, New Business Development

AT&T Bell Laboratories John Dishman, Head, Technology Planning Department Marshall Gingold, Member of Technical staff Jim Goldey, Director Jeanne Goldey Richard Jacobs, Director, VLSI Design Laboratory

Dan Krupka, Department Head D. A. Mehta, Director, Silicon Processing

AT&T Information Systems Mahmoud Elhamamsy, District Manager Aldo Enrici, Assistant Manager

AT&T Technologies, Inc Thomas Mino, Manager, Engineering Rick Morrison, Business Systems Specialist

Gerald Ramsey, Material Management Manager

Acrian, Inc. J . Harris, President & Chief Executive Officer

Adler & Company Dau O'Neill, Associate

Advanced Micro Devices. Inc John East, Vice President, Bipolar Division Steve Zelencik, Senior Vice President Sales & Marketing

Harriet Zelencik

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company /1290 Ridder Parl< Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Aerospatiale Robert Zanotti

Aetna Life and Casualty Bob Lee, Investment Officer Donna Lee

Air Products & Chemicals, Inc. Sen Chen, Marketing Manager Burt Lancaster, Semiconductor Industry Manager Paul Lovett, Corporate Planner Anne Lovett

Applied Materials, Inc Thomas Bowman, Director, Strategic Marketing

Applied Micro Circuits Corporation Roger Smullen, President &c. Chief Executive Officer Jonathan Yu, Chief Operating Officer

Arrow Electronics John Abram, Executive Vice President

Arthur Yoxmg & Company Roger Dunbar, Partner

Assisted Technology Bill Sams, Vice President, Marketing & Sales

Atari Corporation Donald Richard, Vice President

Atcor Corporation Juan Bardina, Vice President Patricia Bardina Robert Bickers, President & Chief Operating Officer

Richard Lawry, Director Christine Lawry

BA Investment Management Corporation Rupert GriitHn, Vice President

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company /1290 Ridder Parl< Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Bank of America Timothy Bottoms, Group Vice President, High Technology

William Creamer, Vice President, High Technology Judy Sanchez, Vice President, C o r p o r a t e Banking James Tempesta, Assistant Vice President, High Technology

Bank of New York Patricia Melaugh, Investment Officer

Bank of the West Shelley Anderson, Vice President Eric Jones, Corporate Banking Officer

Bessemer Venture Partners Neill Brownstein, Partner

Bipolar Integrated Technology, Inc

Burroughs Corporation

Kenneth Giles, Vice President of Finance Sara Giles

Jerry Shames, General Manager, CEPO

Business Week Jack Wi Ison

California Devices, Inc, Bob Lipp, Chief Technical Officer Jaime Martin. Strategic Marketing Manager

Calma Company Robert Kuhling, Director Marketing & Market Development

Capital Research Company Jim Martin, Senior Vice President Diane Martin Richard Yeung, Vice President Paula Yeung

Citibank Jay Hoag, Senior Research Officer

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company / 1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Cognos Associates Dr. Judy Larsen, President

Commodore International, Ltd. Adam Chowaniec, Vice President, Technology Lloyd Taylor, Assistant Vice President of Technology

Custom Silicon, Inc. Dr. Albert Belle Isle, President

Cypress Semiconductor Corporation T. J. Rodgers, President Kathleen Rodgers Lowell Turriff, Vice President & Marketing

Sales

Daisy Systems Corporation Aryeh Finegold, President

Data General Corporation

Datapoint Corporation

Richard Douglas, Product Manager Peter Roche, Senior Marketing Specialist

Gary Cowles, Senior Manager, Electronic Corporate Contracts

Brian Fullmer, Director, Purchasing

Dataquest Incorporated Carol Bender, Marketing Support Representa t ive

Betty Bluford, Administrative Assistant

Howard Bogert, Vice President & . Director, Semiconductor Industry Service

Carol Bogert Stan Bruederle, Vice President Sc Director, Semiconductor User Industry Service

Patricia Cox, Research Analyst Ardan DeVincenzi, Research Analyst Bea Destin, Secretary Tom Dexel, Marketing Manager Frank Florence, Marketing Manager Karen Foley, Project Manager Penny Gal legos. Research Librarian

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company /1290 Bidder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Dataquest Inco rpo ra ted Katy Guill, Research Associate Iza Hallberg. Research Analyst Mike Hankal, A s s o c i a t e D i r e c t o r , Financial Services Program

John Jackson, Marketing Manager Gail Kel ton -Fogg, Industry Analyst Lane Mason, Senior Industry Analyst Rober t McGeary, S e n i o r Industry Analyst Ken McKenzie, Associate D i rec to r Debra McKenzie Alicia Morehouse, Client Care

Coordinator James Newcomb, Vice President & Director, CAD/CAM Industry Service

Gene N o r r e t t , Vice President & Director, Japanese Semiconductor Industry Service

Mary Olsson, Research Analyst Jean Page, Industry Analyst Malcolm Penn, Vice President & Director European Semiconductory Industry Service

Gill Penn Andy Prophet, Senior Industy Analyst Janet Rey, Research Associate Jim Riley, Senior Vice President, Seminconductor Industry Service

Frank Sammann, Senior Vice President, Sales

Nancy Sammann Susan Scibetta, Consultant Anthea Stratigos, Research Associate Sheridan Tatsuno, Research Analyst Mel Thomsen, Senior Industry Analyst Barbara Van, Research Analyst Frederick Zieber, Senior Vice President, Semiconductor Group Libbe Zieber

Department of Trade and Industry Dr Ron Love 1 and

Dexter Corporation—Hysol Division Larry Baxter, Manager

International Marketing

Diel i Christine Ragoucy

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company / 1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Digital Equipment Corporation Prakash Bhalerao, Custom Engineering Group Manager

Ken Brabitz, Planning Manager, LSI Group

Kevin Driscoll, Controller, Finance Manager Beverly Feldman, Product Manager P e t e r Masucci, Marketing Manager

Dimos AG Willi Bacher, President

DuPont Pension Fund Terry Lancaster, Vice President Bill Zubenko, Security Analyst

Dynami t Nobel Silicon, Inc Tom Schauf, Marketing Manager

ERSO/ITRI Wade Chang, Marketing Manager C. T. Shih, Design Manager Mentor Tseng, Marketing Planner

ESEC USA, Inc Hans Kurner. Vice President

Eastman Kodak Company Dwight Johnson, Program Manager, Electronic Design

Eaton Corporation Harvey Frye, Director, Sales Administration & National Accounts

Daniel Reeves, District Sales Manager, Southern California

Electric Power Research Institute John Cunanings, Director, Renewable Resource Systems Department

Environmental Processing, Inc Phillip Drayer, President & Chief Operating Officer

Exel Microelectronics, Inc. Sam Young, Director of Marketing

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company /1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Exmos Semiconductor Co rpo r a t ion G. Mart Kernahan, Chairman of the Board

Elaine Kernahan

Exxon Corporation Colin Wiggins, Portfolio Manager

Fairchild Camera & Instrument Corporation

Donald B r o o k s , Executive Vice President Teresa Brooks Peyton Cole, Strategic Communications Manager, NAS Erick Hagmann, Strategic Marketing Manager Chris Newham, Strategic Plarming Manager, NAS

Michael Pawlik, Marketing Manager Martin Plotkin, Marketing Director

Ferranti Electronics Limited Alan Shepherd, Managing Director Edith Shepherd

Fiat Semelco Giuseppe Anerdi, Purchasing Manager

First Interstate Bank Kathryn Plumb, Assistant Vice President Edwin Sauve', Vice President Wi11iam Wiley, Vice President and Manager

First National Bank of Boston David Garnitz, Loan Officer Jeff Wellington, Loan Officer

GBL/Goold Electronics Corporation Oliver Goold, President

GCA Corporation Paul Reagan, Senior Vice President John Stewart, Vice President, Integrated Circuits Systems Group

GTE Microcircui ts Fran Krch, Manager , Strategic Planning Otis Wolkins, President

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company / 1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

General Electric Company Jeffrey Ehrlich, Manager, Product Application Technology James Poitras, Manager, Business Development John Zeigler, Contracting Agent

G e n e r a l Electric Trust Investment Marshall Kidd, Manager, Technical Analysis

Hami1ton/Avnet

Harris Corporation

Colman Daniel, Vice President

Jon Cornell, Senior Vice President & Sector Executive

Mary Cornel 1 Linda Fredericks, D i r e c t o r of Marketing Communicat ions

Michael Graff, Vice President, Marketing, Semiconductor Division James Smith, Vice President

Hewlett-Packard Company Jack Nilsson, Marketing Engineer Robert Santos, Product Marketing Manager

Midge Santos

Hitachi America, Ltd. Richard English, S e n i o r Area Manager

Hi tachi, Ltd H i s a o Kanamaru, Department Manager, Marketing Sc Planning Department

Holt, Inc Mark Ellsberry, Director of Marketing

Honeywell ISI, S p a . Giovanni Pagliosa

Honejnurel 1 , Inc . Bill O'Byrne, Commodity Manager

Hoya Corporation, Electronics Division

George LeCreim, Marketing Manager

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company /1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Hughes Aircraft Company Paul Hart, Manager, Custom LSI Procurement

W. Scott Walker, Group Vice President & Manager, Solid State- Products Division

Cassie Walker

Hyundai Electronics America Yong Lee, Vice President, General Manager, Semiconductor Operations Andrew Procassini, Vice President, Market ing

IBM Corporation Irv Abzug, Vice President & Director, Corporate Component Procurement

Harriet Abzug Jet Advani, Advisory Engineer Michael Denick, Manager, New Products Office

Edward Desmond, Manager, Industrial Engineering Services

Mark Desrosiers, Staff Programmer Basil Harrison, Advisory Engineer Bob Hoffman, Senior Buyer Annmarie Ihle, Buyer Edward Linde, Senior Engineer John Melgalvis, Industrial Engineer Richard Orrill, Senior Engineer Gerald Parker, Program Manager, Process

Technology John Raszcewski, Advisory Engineer Dave Royse, Analyst Robert Rusnack, Advisory Enginee'-E. Weston Seaman, Manager, New Products Cost Engineering

Betsey Seaman Brian Sjolseth, Advisor Plaimer Ray Wilfinger, Prograun Manager Mildred Wilfinger

IDA Ireland Brendan Halpin, Regional Director

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company / 1290 RIdder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

INMOS Corporation larui Barron, Chief Strategic O f f i c e r A. C. D'Augustine, Vice President, Marketing Pete Fowler, Marke t ing Manager John Heightley, Chief Operating Officer Dennis Parker, Group Controller Richard Petritz, Chairman Grace Petritz

ITT Semiconductors Del Brand, Director of Marketing & Sales Julie Brand

Indium Corporation of America Robert Bullock, Senior Vice Presiden' Joan Bui lock

Ing. C. 01ivetti & C., S.p.A.

Intel Corporation

Max Be r t o1i no-Zan Tito Conti, Director of Quality, Corporate Staff

Enzo Rognoni

Jack Carsten, Senior Vice President & General Manager

Doug Finke, Product Marketing Engineer Mark Norwood, Components, Strategic staff Manager

Interconics C. Fred Little, Market Development Manager Betsy Little

Interlek, Inc . Josh Camba, Senior Vice President, Finance

Miriam Ceunba Vic Chuidian. President & Chief Executive Officer Joanne Chuidian Antonio Garcia, Chairman of the Board Carolyn Garcia Dave Jones, Vice President, Test International Division

Joe Marcello, Special Assistant to Chairman for Corporate Development

Betty Marcello Nand Prasad, Executive Vice President George Robertson, Vice President, Sales Lou Tieber, Vice President, Sales

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company / 1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

International CMOS Technology Drew Osterman, President

Internat ional Microelectronic Products

Michael Ho l l abaugh , Marketing Manager Debbie Hollabaugh

Intersi1, Inc. Paul Gupta, Vice President, O p e r a t i o n s Jerry Kiachian, Vice President, Applicat ions

Investors in Industry Fred Haney, Principal Barbara Haney Anna Henery, Principal

Italtel Telematica Marisa Bellisario, President Gianni Bertolini, Director of Corporate Procurement

Emilio Dragoni, Manager Mario Tripputi, Manager Aldo Zana, Director of External Relations

J C. Schumacher Company John Schumacher, President

J. H. Whitney & Company Harry Marshall, Partner

Japan Electronics Bureau Andrew Koshar

KLA Instruments, Inc. Kenneth Levy, President Gloria Levy

Ketchum Public Relations Jennifer Hughes Chaney Steinman, Vice President &

D i r e c t o r of Research

LM Ericsson Corporation Ola Eckholm, Chief Component Engineer

Dataquest Incorporated, A Subsidiary of AC. Nielsen Company / 1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

LSI Logic Corporation Perry Constantine, Vice President, North America Marketing

Wilford Corrigan, President Sigriui Corrigan John Shea, Director, Military Technology

Flor Shea

LTX Corporation Adrian Hohn, Vice President Graham Mi 1ler, President Geoff Rowett, Vice President, European Operat ions

Lattice Semiconductor Corporation Rahul Sud, President & Chief Executive Officer

Lehman Management Company Larry Phillips, .Analyst

Lex Service, Inc. Milton Grannatt, III, Vice President Planning-Supplier Development

Gary Kibblewhite, Planning Manager N. Wood J. Michael Worfolk, Vice President, Business Development

MOS Electronics Corporation (MOSEL) C. "Kip" Broym, Director, Custom Circui ts

McDonnell Douglas Microelectronics John Hayn, Manager of Applications Engineering

Megatest Corporation Jan Waluk, Sales Manager, Major Accounts Dominique Waluk

Messerschmitt-Boelkow-Blohm GmbH Edgar Anderson, Manager, Marketing Sc Sales, Electronics Products

Holger Bree

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company /1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Micro Component Technology Terry Bell, General Manager, Test Systems Division

Robert Vosika, Vice President

Microlinear Corporation Alan Grebene, President Norman Miller, Executive Vice President

Micromos Dr. Vir Dhaka, Chairman & Chief Executive Officer

Mitsubishi Electric C o r p o r a t i o n Jack Christy, Regional Sales Manager

Mitsubishi Electronics America, Inc Azmat Malik, Product Marketing Manager Hiroo Taniguchi, Executive Vice President Sc General Manager John Zucker, National Sales Director

Mitsui High-Tek, Inc

Modular Semiconductor, Inc

Satoshi Nagata, Director & Executive Planner

N. Damodar Reddy, President

Monolithic Memories John Birkner, Manager of PALs, Product Planning Department Timothy Propeck, Vice President, Market ing

Monsanto Electronic Material Company Hubert Dohman, Vict President, Quality Assurance

Martha Dohman Wendy Grossmen, Technical Analyst Elizabeth Isaacs, Manager, Product Educat ion

Morgan Guaranty Trust Charles Kimball, Vice President Investment Research Department

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company / 1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Mostek Corporation Lee Chu, Director, Industry Marketing Sadar Haddad, Strategy Analyst Bert Kehren, Director, Strategic Planning

Robert Palmer, Executive Vice President, Semiconductor Operations

Motorola Semiconductor, Inc Chuck Thompson, Vice President & Director, Worldwide Marketing

Wanda Thompson

Motorola, Inc, Erick Ayers, Assistant Strategic Manager Edward Day, Strategic Planning Manager Oliver Edwards, Manager, Marketing Planning

Bob Gonzalez, Japanese Analyst Bob Jenkins, Vice President Carolee Jenkins

Mullard, Ltd.

Mutual of New York

William Everden, Divisional Director, Industrial Division

Anthony Blenk, Technology Analyst

NCR Corporation James Van Tassel, Vice President Microelectronics Division

NEC Electronics USA. Inc Frank Jelenko, Vice President, Marketing James Kelley, Vice President, Technology Center

Ed Neubauer, Vice President, Marketing & Sales K. K. Yawata, President

National Electronic Distributors Associat ion

Toby Mack, Executive Vice President

National Semiconductor Corporation Douglas Ritchie, Vice President, Consumer Specific Products Joe Van Poppelen, Vice President Market ing

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company /1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Naval Postgraduate School Herschel Loomis, Electrical Engineer

Northern Telecom Electronics, Ltd. E. Dennis Colbourne, Assistant Vice President, Semiconductor Operations

A. Graham Sadler, Vice President, Semiconductor Operations

Northern Telecom, Ltd. G. Wi1liam Bothwel1, Director, Materials and Purchasing Patricia Bothwel1 Monte Seifers, Director, Semiconductor Sales

Oki Semiconductor Jerry Crowley, President &c Chief Executive Officer

Nancie Crowley

Panatech Semiconductor John Baskett, President

Perkin-Elmer Corporation Henry Dieselman, Manager, Plarming Carl Hildebrand, Vice President, Sales Service, Semiconductor Equipment Group

Gail Hildebrand

Philip A. Hunt Chemical Corporation Peter Danna, Vice President, New Business Lorraine Danna Jim Favier, Vice President, Microelectronics Jack Murphy, Director of Sales

Pitney Bowes, Inc. Frank Seestrom, Director, Programs Joann Seestrom Michael Swaluk, Manager, Electronic Support

Lynn Swaluk

Plessey Solid State Dennis Chant, President

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company /1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Prudential-Bache Securities George Bristol, Managing Director Tom Gettinger, Research Analyst Richard Klein, Vice President Michael Weisberg, Director of Technology Research

Rick Whittington, Vice President

Quality Au tomat ion , Inc. Mike Leibowitz, President

RCA Corporation Herbert Criscito, Vice President, Marketing Robert Lenz, Administrator, Sales Analysis

Richard Santilli, Vice President. Market Development

Raytheon Corporation Randy Marshall, Director, International Marketing

Rhone-Poulenc Jacques Biais, Manager, Electronic Materials Group

Robert Bosch GmbH Gunter Matthai, Manager, Technology Plarming Paula Matthai

Rockwell International Corporation C. V -Kovac, Vice President, Key Accoiuits

Rosenberg Capital Management Walter Price, Partner

S-MOS Systems, Inc. Dan Hauer, President

S.E.H. America John Ma t lock, Vice President, Technology

SAI-SEMI Specialists Bob Ball, Vice President, Marketing Abe Kosakowsky, Marketing Manager Jack Tils, Semiconductor Marketing Manager

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company /1290 Bidder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Sag em Jean Paul Neuville

Samsung Semiconductor & Telecommiuii cat ions Company, Ltd.

Moo-Youl Sohn, Planning Manager

San Jose Mercury News Dave Sylvester, Business Writer

Schweber Electronics, Inc Richard Jacobs, Director of Strategic Plaiuiing

Scottish Development Agency Cameron McPhai1, Development

Sears Investment Management Company Stephen Dexter, Investment Analyst

Security Pacific Capital Corporation Dmitry Bosky, Investment Officier James McElwee, Vice President

Semiconductor Microelectronics Internallonal

Joseph Curry, Consultant

Sharp Electronics Corporation James Wei, National Marketing Manager

Shinko Electric America Bill Cruizkshank, Executive Vice President

Donna Cruizkshank

Shinko Electric Industries Company, Ltd.

Taizo Abe, Director, Engineering Department

Shipley Company, Inc Gene Goebel, Director of Sales Mic roe lec t ron i c Products

Sierra Semiconductor Corporation James Diller, President June Diller Thomas Reynolds, Vice President, Marketing Sc Sales

Maryanne Reynolds

Dataquest incorporated, A Subsidiary of A.C. Nielsen Company /1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Signetics Corporation Marilyn Kissel, Senior Financial Analyst

Silicon Systems, Inc. James Peterson, Director of Marketing

Smith Industries M. W. Thurlow

stack GmbH Bernard Hadley, Managing Director

standard Microsystems C o r p o r a t i o n Art Sidorsky, Executive Vice President

Stanford University Everett Rogers, Professor-Institute for Coranuni cat i ons

storm. Block <Sc Associates Randy Block, General Partner

Suwa Seiko Sha Kimio Takemori

Synertek, Inc R i c h a r d Konrad, Vice President, Marketing & Sales

Telic-Alcatel Joseph Heitz, Engineer, Purchasing Department

TRW. Inc Ralph Miller, Vice President & General Manager

Tandem Computers, Inc Tom Collins, Development Engineering Manager Susan Col 1 ins

Telettra S.p.A Franco Carnevali

Teme seal Daniel Devine, Director of Marketing

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company / 1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Teradyne, Inc. Abe Bluestone, Product Manager Ron Butler, Purchasing Manager Donald Hamman, Controller Stratton Smith, Director of Purchasing

Texas Instruments, Inc. Randall Peters, Manager Strategic Planning

Charles Phipps, Vice President, Semiconductor Group

The Hihernia Bank Phil Yoimg, Senior Vice President Cynthia Young

The Wall Street Journal Dick Schaeffer, Technology Editor

Thorn-EMl John Scholes, Corporate Planning Execut ive

Toshiba America, Inc Jay Litus, Jr., Director of Marketing Jim Townsend, Strategic Marketing Manager

Trilogy Systems Pete Bejarano, Director Frank Swiatowiec, Director

Tristar Semiconductor, Inc S. Ham, Vice President, Chief of Staff Sang Lee, President Een Yearp Lee

Union Carbide Corporation Anthony Keig, Business Research Manager Thomas Nelson, Manager, Electronics AppIicat ions

Thomas Singman, Manager, Marketing P1ann i ng

Walter Willett, Manager, On Site Sales

United Microelectronics Corporation Tony Yu, Manager, U.S. Operations

United States Department of Commerce Robert Eckelmann, Industry Analyst

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company /1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

United Technologies Corporation Richard Dressier, Deputy Director, Financial Planning & Analysis

VHSIC Technology Corporation Tom Hendrickson, President John Hodgson, Vice President

VLSI Technology, Inc Henri Jarrat, President & Chief Executive Officer

Robert Silco, Director, Corporate Market ing Dorothy SiIco

Varian Associates William Bottoms, President

Varian Corporation, Exitron Division

John Wunner, Marketing Manager

Videolog

Vitelic Corporation

Alan Brigish, President

Alex Au, President & Chief Executive Off icer Jack Ordway, Vice President, Marketing & Sales

W & W Enterprises Gunnar Wetlesen, President Mary Ellen Wetlesen

Wacker Siltronic Corporation Werner Freiesleben, President Vern Meissner, Director of Marketing Dolores Meissner Malcolm Russ, Executive Vice President

Wells Electronics, Inc Arthur Midili, President

Western Digital Corporation Kathy Braun, Director, Storage Management Marketing Dieter Marenbach, Strategic Planner

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company / 1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Western Microtechnology Bernard Marren, President & Director

XTAR E l e c t r o n i c s, Inc Skip Powe r s , Chief Executive Officer

Xerox Corporation Charles Holt, Vice President Sei Shohara, Manager, Technical Staff

Xicor, Inc Wallace Tchon, Vice President strategic Planning

Zilog, Inc. Carl Johnson, Manager, Technical Marketing Tom Popek, Senior Vice President & General Manager, Components Division

ZyMOS Corporation

Zytrex Corporation

Jerry Gibbs, Marketing Director Dave Guzeman, Vice President, Marketing & Sales . Alan Louwerse, Executive Vice President

Orlando Gal legos. Senior Director of Market ing

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company /1290 RIdder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

:^T^Datac|iiest

CT^v^ '"*' E>ataquest CLIENT

SEMICONDUCTOR INDUSTRY SERVICE

ADC Corporation AMI-Austria AT&T AT&T Bell Laboratories AT&T Conununications AT&T Consumer Products AT&T Resource Management AT&T Technologies, Inc. Accutest Adler & Co. Advanced Micro Devices, Inc. Aerospatiale Air Products and Chemicals, Inc. American Microsystems, Inc. Analog Devices BV Ando Electric Co., Ltd. Applied Intelligent Systems, Inc. Applied Materials, inc. Applied Micro Circuits Corporation Arrow Electronics, Inc. Arthur Andersen & Company Arthur Young & Company Asahi Chemical Industry Co., Ltd. Assisted Technology, Inc. Atari, Incorporated BMC Industries, Inc. BSR International BULL Transac Bank of America Banlc of California Bank of the West Banque Nationale de Paris Borg Warner Chemicals British Technology Group Burroughs Corporation CIN Industrial Finance Ltd. CIT-Alcatel CMOS Technology, Inc. California Devices, Inc.

California First Bank Calma Company Canon, Inc. Chase Manhattan Bank Churchill international Cii Honeywell Bull Con^uter Sciences Corporation Crocker Bank (The) Custom Microelectronics Assembly, Inc. D.G.S.I. D.I.E.L.I. DWS Deutschen Gesellschaft fur Wertpapiersparen Daleco Research & Development, Inc. Data General Corporation Datapoint Corporation Department of industry UK Dexter Corporation/Hysol Division Digital Equipment Corporation DOW Chemical Dynamit Nobel Silicon, Inc. E.I. DuPont de Nemours & Co., Inc. BRSO Eastunan Kodak Company Eaton Corporation Electric Power Research institute (EPRI) Electronics Industry Association of Japan Emerson Electric Co. Environmental Processing Ericsson Information Systems AB Eurotechnique Exel Microelectronics, inc. Pairchild Camera & Instrument Co. Fairchild Semiconducteur Europe S.A. Fairchild Memory Test Systems Fairchild Research Fairchild Semiconductor Fairchild Test Systems Group Fairchild/Schlumberger Ferranti Computer Systems, Ltd.

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company /1290 Bidder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Ferranti Electronics, Ltd. Finalco

Firs t In te r s ta te Bank of California F i r s t In te r s ta te Bank of Oregon Firs t In t e r s t a t e Capital Inc. F i rs t National Bank of Boston Four-Phase Systems, Inc. Fujitsu Microelectronics, Inc. Fujitsu Limited GCA Corporation GTE Microcircuits GTE-Network Systems, Inc. GenRad, Inc. General Electric Company General Electric Company, Ltd. General Instrument Corporation General Instruments International, Ltd. General Motors Corporation Gold Star Semiconductor, Ltd. Gould/Biomation Inc. Harris Corporation Hewlett-Packard Company Hitachi America, Ltd. Hitachi Electronic Components Europe GmbH Hitachi, Ltd. Holt, Inc. Honeywell, Inc. Hoya Corporation, Electronics Division Hughes Aircraft Company IBM Compec IBM Corporation IBM France IBM Japan, Ltd. IBM Oesterreich IBM UK, Ltd. ICG Electronics Enterprises IDA Ireland ITT Advanced Technology Center ITT Europe ITT Intermetall GmbH ITT Semiconductors Idemitsu Petrochemical Co., Ltd. Imperial Chemical Industry (ICI) Indium Corporation of America Ing. C. Olivetti & C , S.p.A. Inmos Corporation Inmos, Ltd. Institutional Venture Partners Integrated Device Technology Intel Corporation Intel International Corp. S.A. InterWest Partners Interlek. Inc. International Microelectronic Products, Inc. Intersil, Inc.

investors in industry Investors in industry Group PLC Itau Technologia S.A. J. H. Whitney & Co. Japan Electronics Bureau Jardine Flemings, Ltd. Kaiser Electronics Kanematsu-Gosho (USA) LSI Logic Corporation LTX Corporation La Telephonie Industrtelle et Commerciale (Telic)

Landmarks Group (The) Lattice Semiconductors Lex Service, inc. Linear Technology Corp. LOS Alamos National Laboratories MBB GmbH Marconi Electronic Devices, Ltd. Matra Harris Semiconducteurs Matrix Partners, L.P. Mayfield Fund McDonnell Douglas Microelectronics Megatest Corporation Merrill, Pickard, Anderson & Eyre Micro Component Technology, Inc. Micro Power Systems, Inc. Microelectronic Marin Microelectronics Technology Company Micromos, inc. Ministerio de Industria Y Energia Mitsubishi Corporation Mitsubishi Electric Corporation Mitsubishi Electronics America, Inc. Miyazaki Oki Electric Industry Co., Ltd. Modern Electrosystems, Inc. Modular Semiconductor, Inc. Monolithic Memories, Inc. Monsanto Electric Materials Company Mosley Management Corporation Mostek Corporation Mostek Japan K.K. Motorola Semiconductor Europe Motorola, Inc. Mullard, Ltd. Murray Electronics PLC NCR Corporation NEC Corporation NEC Electronics USA, Inc. Narumi China Corporation National Bureau of Standards National Economic Development Office (NEIXD) National Semiconductor Corporation Nissan Motor Co., Ltd. Northern Telecom, Ltd.

Oak Management Corporation Oki Electric industry Co., Ltd. Oki Semiconductor, Inc. Oxcal Venture Corp. Oxford Venture Corp. Perkin-Elmer Corporation Philip A. Hunt Chemical Corporation Philips International BV Pioneer-Standard Electronics, inc. Pitney Bowes, Inc. Plessey Semiconductors Ltd. Plessey Solid.State Prime Capital Management Co., Inc. QCAD Quality Automation Quasel, Inc. Qume Corporation RCA Corporation RTC la Radiotechnique-Compdec Raytheon Data Systems Rhone Poulenc,Siltec Ricoh Systems, inc. Robert Bosch GmbH Rockwell International Corporation S.A.M.E.S., Ltd. S.E.H. America, Inc. S A Matra SAI-SEMI Specialists SEEQ Technology, Inc. SGS Semiconductor Corporation SGS-ATES STACK GmbH STC Semiconductors Ltd. Sagem Scottish Development Agency Security Pacific Capital Corp. Sharp Electronics Corporation Shin-Etsu Handotai Co., Ltd. Shinko Electric Industries Co., Ltd. Siemens AG Siemens Corporation Sierra Semiconductor Corp. Signetics Corporation Solid State Scientific, Inc. Sony Corporation Standard Microsystems Corporation Stet Societa Finanziaria Telefonica S.p.A. Supertex, Inc. Suwa Seikosha Co., Ltd. Synertek, Inc. TRW Active Components Tachibana Co., Ltd. Takeda Riken, Ltd. Takeda Systems, Inc. Tandem Computers, Inc.

Targetronix Tegal Corporation Tektronix, inc. Telefunkeh Electronic GmbH Temescal Teradyne, Inc. Texas Instruments, Inc. The Ericsson Corporation Thomson CSP Thomson EFCIS Thorn-EMI Toshiba America, Inc. Toshiba Corporation Toshiba Europe (I.E.) GmbH Toshiba Semiconductor (USA), Inc. Tristar Semiconductor, inc. U.S. Departiment of Commerce UTI Instruments Company Union Bank Union Carbide Corporation Union Trust Company of Maryland Union Venture Corporation United Micro^electronics Corp. United Technologies Corporation Unitrode Corporation VLSI Technology, Inc. Varian Associates Vitelic Corporation Wacker Chemitronic GmbH Wacker Siltronic Corporation Weitek Western Digital Corporation Wyle Laboratories XTAR Electronics, Inc. Xerox Corporation Xicor, Incorporated Yamada Seisakusho Co., Ltd. Zilog, Inc. ZyMOS Corporation Zytrex Corporation

06/28/84

Dataquest

Dataquest

SEMICONDUCTOR INDUSTRY CONFERENCE SPEAKERS

Frederick L. Zieber Senior Vice President Dataquest Incorporated

Chuck Thompson Vice President Director, World Wide Mktg. Motorola Semi Sector

Jim Riley Senior Vice President Dataquest Incorporated

John C. East Vice President Bipolar Division Advanced Micro Devices

Charles H. Phipps Vice President, Semiconductor Group Manager, Market Development Texas Instruments Incorporated

Doug Ritchie Vice President Consumer Specific Products National Semiconductor Corp.

Roger Smullen President and CEO Applied Micro Circuits Corp.

Henri Jarrat President Chief Operating Officer VLSI Technology

Jon Cornell Senior Vice President and Sector Executive Harris Semiconductor

A. Gary Shilling President A. Gary Schilling & Co.

John Abram Executive Vice President Arrow Electronics

Jerry Crowley President and CEO Oki Seiconductor

Ken McKenzie Associate Director Semiconductor Group Dataquest Incorporated

T. J. Rodgers President Cypress Semiconductor

Professor Everett M. Rogers Institute for Communications Stanford University

Judy Larsen, Ph. D. President Cognos Associated

Bill Bottoms President Semiconductor Equipment Division Varian Associates

Wilfred J. Corrigan President and CEO LSI Logic

Marisa Bellisario Managing Director, and Chief Executive Officer Italtel Group

Malcolm Penn Director Dataquest U. K. Ltd.

Aryeh Finegold President Daisy Systems

Jack Carsten Senior Vice President and General Manager Intel Corporation

Dataquest incorporated, A Subsidiary of A.C. Nielsen Company /1290 Ridder Park Drive /San Jose, CA 95131 / (408) 971-9000 / Telex 171973

Dataquest

SEMICONDUCTOR OUTLOOK—SOFT LANDING OR HARD

Frederick L. Zieber Senior Vice President and

Director of the Semiconductor Group Dataquest Incorporated

Mr. Zieber is a Senior Vice President of DATAQUEST Incorporated, a member of its Executive Committee, and the Director of its Semiconductor Group. He has 13 years of experience in market research and consulting to the semiconductor industry, and previously had 9 years of experience working in the semiconductor industry. He has experience in integrated circuit and discrete device processing, design, manufacture, and testing. He holds two patents in semiconductor processing. Mr. Zieber has a B.S. degree in Electrical Engineering from Stanford University, and an M.B.A. degree from the Graduate School of Business at Stanford university.

Dataquest Incorporated SEMICONDUCTOR INDUSTRY CONFERENCE

October 15, 16, and 17, 1984 San Diego, California

Dataquest Incorporated, A Subsidiary of A.C. Nielsen Company /1290 Ridder Park Drive / San Jose, CA 95131 / (408) 971-9000 / Telex 171973

SEMICONDUCTOR OUTLOOK SOFT LANDING OR HARD

The last nine years it has fallen upon me to present the DATAQUEST forecast of semiconductor demand. Our forecasting has not always been perfect, (those who live by the crystal ball learn to eat ground glass sooner or later), but our record has generally been excellent. I believe this year is the most difficult situation I have faced. There has been some dark clouds on the horizon that have moved perceptively closer.

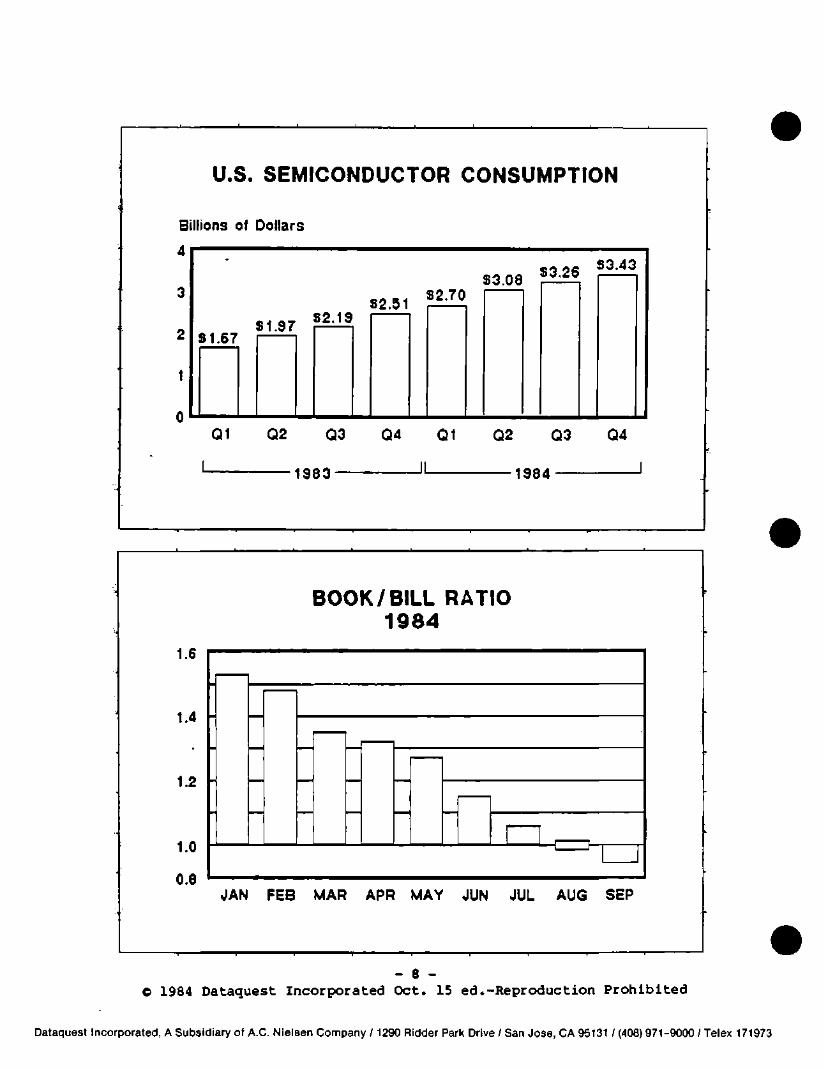

Lets look at what's been happening recently. For the last two years semiconductor output has increased tremendously. This chart gives semiconductor shipments into the United States, by quarter, for 1983 and 1984. Two years ago at this conference we forecast that demand would pick up strongly by April 1983. That is exactly what happened. Since then shipments have grown at a tremendous rate. Currently shipments are nearly double the rate of the first quarter of 1983. This unprecedented rate of growth over the last year and a half was spurred by the economy and Other market factors. Demand was extremely strong.

More recently, order rates have been declining. With shipments increasing, the book-to-bill ratio has been falling steadily and inexorably all year long. Although this chart was made several weeks ago, we expected the book-to-bill ratio for September to be less than one. This is what's happened. For the last three months, shipments have exceeded orders. Any of us who have been in the industry long enough have seen this pattern before, usually as the prelude to a full-fledged, extremely painful, industry recession. What is the outlook of the rest Of 1984 in 1985?

Let's look at what is happening at the semiconductor users. Very recently, over the past two or three months, there has been a rapid inventory build up. This is nowhere near the magnitude of 1980 or 1974, but excess inventory is excess inventory. Users of semiconductors have seen a slower rate of increase in their own orders. The euphoric expectations of earlier in the year have come face to face with a less buoyant economy and reality. Most systems companies are facing the future with lower expectations than they had several months earlier. This affects their order rates for semiconductors. Semiconductor usage rates are not as expected, the future usage rates are lower, and increasing inventories mandate adjustment of order rates. Additionally, there has been several disasters among systems companies. There has been a tremendous increase in new companies in many market areas each with high expectations of major market share. It is inevitable that the

- 1 -