Strategy Seminar

Personal Financial Services

Australia and New Zealand Banking Group Limited

24 August 2001

Page 2

Agenda

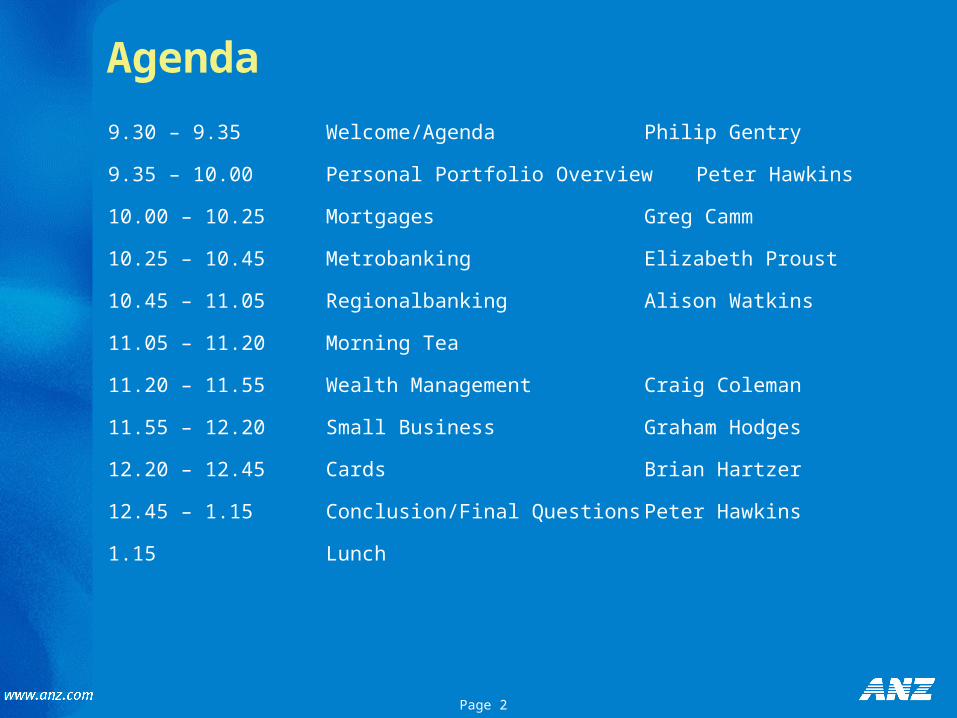

9.30 – 9.35 Welcome/Agenda Philip Gentry

9.35 – 10.00 Personal Portfolio Overview Peter Hawkins

10.00 – 10.25 Mortgages Greg Camm

10.25 – 10.45 Metrobanking Elizabeth Proust

10.45 – 11.05 Regionalbanking Alison Watkins

11.05 – 11.20 Morning Tea

11.20 – 11.55 Wealth Management Craig Coleman

11.55 – 12.20 Small Business Graham Hodges

12.20 – 12.45 Cards Brian Hartzer

12.45 – 1.15 Conclusion/Final Questions Peter Hawkins

1.15 Lunch

Personal Financial Services

Realising a unique growth opportunity

Peter HawkinsGroup Managing Director

Australia and New Zealand Banking Group Limited24 August 2001

Page 4

• Joined ANZ April 1989

• Commenced current position February 1998

Greg Camm - Mortgages

Page 5

• Joined ANZ January 1998

• Commenced current position March 2001

Elizabeth Proust - Metrobanking

Page 6

• Joined ANZ February 1999

• Commenced current position March 2001

Alison Watkins - Regionalbanking

Page 7

• Joined ANZ in 1994

• Commenced current position October 2000

Craig Coleman – Wealth Management

Page 8

• Joined ANZ in 1991

• Commenced current position September 2000

Graham Hodges – Small to Medium Business

Page 9

• Joined ANZ September 1999

• Commenced current position September 1999

Brian Hartzer – Cards & ePayments

Page 10

Personal Financial Services

Greg CammMortgages

Elizabeth ProustMetrobanking

Alison Watkins Regionalbanking

Craig ColemanWealth Management

Graham Hodges Small to Medium Business

Brian HartzerCards & ePayments

Page 11

The Personal Portfolio – today’s themes

A Portfolio of specialist Customer and Product

Businesses with important interdependencies

• Specialisation works

• Now applying specialisation to the rest of the

Personal portfolio

• Significant customer and bottom line benefits

Realising a unique growth opportunityRealising a unique growth opportunity

Page 12

Considerable momentum developing

302

840

547

712

251

266

1997 Mar 2001*

Personal

Corporate

Int & Subs

NPAT

3.1

3.2

3.3

3.4

3.5

3.6

3.7

3.8

3.9

4.0

4.1

Mar-98

Sep-98

Mar-99

Sep-99

Mar-00

Sep-00

Customer Numbers

27%

50%

23%

46%

39%

15%

m

*Mar 2001 annualised

Page 13

Specialisation has driven the success of our product businesses

%

Source: Economics @ ANZ

10

11

12

13

14

15

J an-95 Apr-96 J ul-97 Oct-98 J an-00 Apr-01

Market Share (Mortgages)

Break in series

23

24

25

26

27

28

J un-98 May-99 Apr-00 Mar-01

% Market Share (Card Spend)*

* 3 month moving average

Page 14

Drivers of value creation – not just a cost story

Specialisation

• Award winning products

• Sales capability - driving

revenue gains

• Dramatic productivity

gains

Specialisation

• Award winning products

• Sales capability - driving

revenue gains

• Dramatic productivity

gains

800

900

1,000

1,100

1,200

1,300

1,400

1,500

1,600

Mar-99 Sep-99 Mar-00 Sep-00 Mar-01

50%

55%

60%

65%

70%

Mar-99 Sep-99 Mar-00 Sep-00 Mar-01

Substantial value creation

Revenue

Cost Income

$m

CAGR 6.5%

Page 15

233

322333

380

420

150

200

250

300

350

400

450

Mar-99

Sep-99

Mar-00

Sep-00

Mar-01

Our strategy is delivering strong results

Small Business

Wealth Mgmt

Regionalbanking

Metrobanking

Cards

Mortgages

26% NPAT Increase

CAGR - 34%

$m

58

11234

55102

10273

72

24

23

41

53

1H 2000 1H 2001

Personal Portfolio - NPAT

Page 16

12.0

24.7

0

5

10

15

20

25

30

ANZ Peer Average

6.5

9.7

0

2

4

6

8

10

12

ANZ Peer Average

10.2

14.2

02468

10121416

ANZ Peer Average

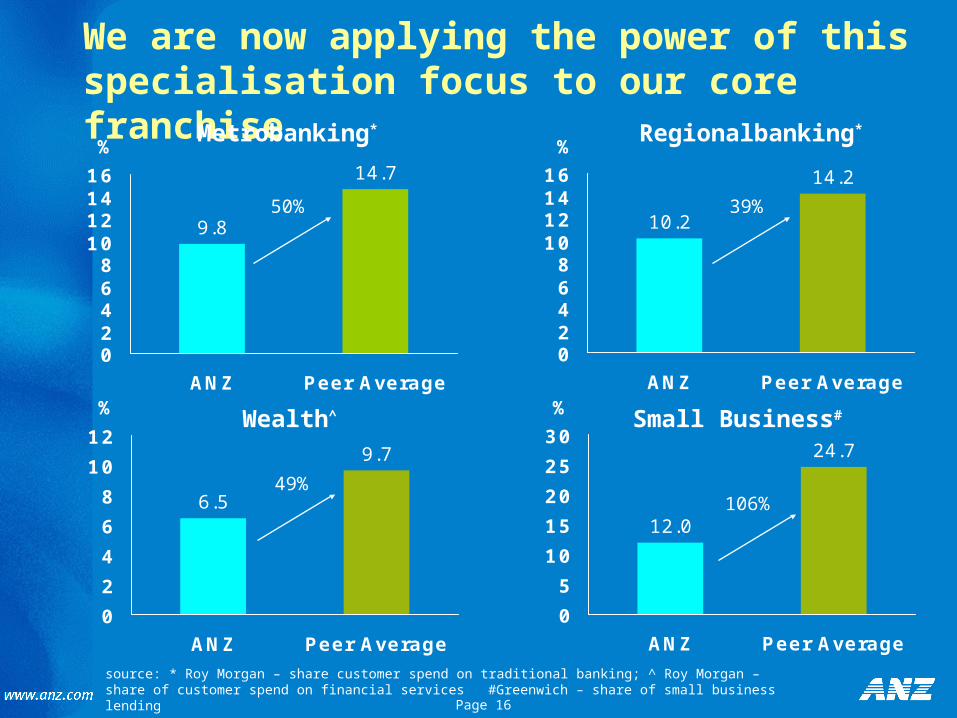

We are now applying the power of this specialisation focus to our core franchise

9.8

14.7

02468

10121416

ANZ Peer Average

Metrobanking* Regionalbanking*

Wealth^ Small Business#

source: * Roy Morgan – share customer spend on traditional banking; ^ Roy Morgan – share of customer spend on financial services #Greenwich – share of small business lending

50% 39%

49%106%

%

%

%

%

Page 17

Existing revenue $2.6b

The growth opportunities in Personal are substantial

10

0

Customer #’s (m)

~40% ~50%**

Peer Average

Share of Customer Wallet

** Average share of wallet for CBA, NAB, WBC - source: Roy Morgan Research

4

5

Total potential revenue growth - $1.5b*

Increased wallet on higher share

$160m7.3

Increase Market Share•1m new customers•Potential revenue - $650m

Increase Wallet Share•Meet peer average•Potential revenue - $650m

* Australia only

Page 18

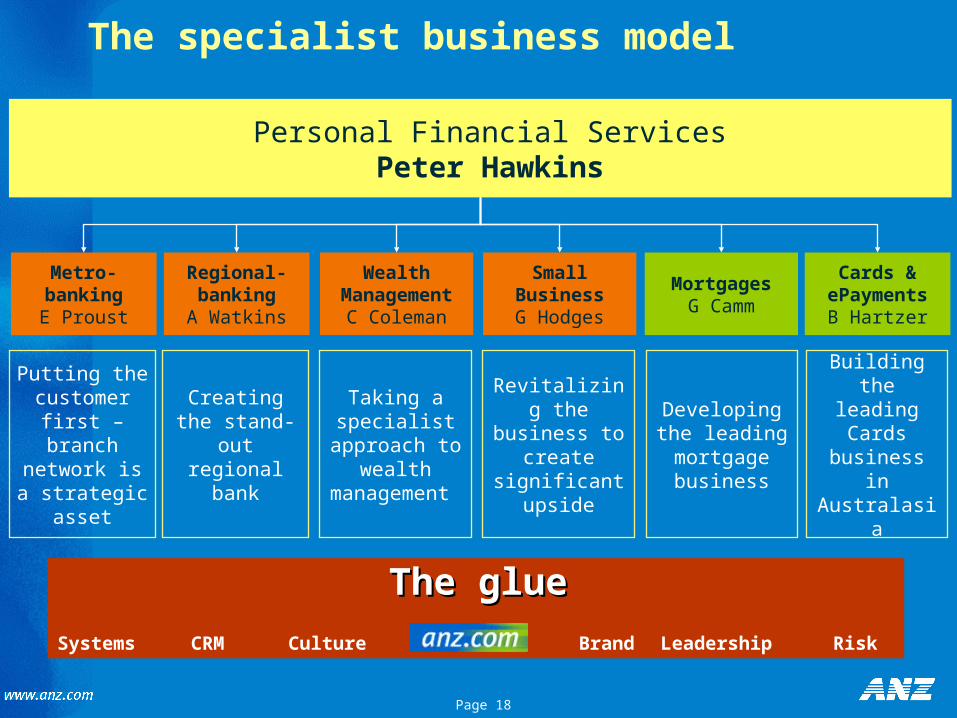

Personal Financial ServicesPeter Hawkins

Regional- bankingA Watkins

Wealth Management

C Coleman

Small BusinessG Hodges

MortgagesG Camm

Cards & ePayments

B Hartzer

Creating the stand-out regional

bank

Taking a specialist

approach to wealth

management

Revitalizing the business

to create significant

upside

Developing the leading mortgage business

Building the leading Cards

business in Australasia

Systems CRM Culture Brand Leadership Risk

Metro-bankingE Proust

The specialist business model

Putting the customer

first – branch network is a

strategic asset

The glueThe glue

Page 19

“Putting customers first” is critical to the next phase of our specialisation strategy

• Four customer businesses created

• More accurate and appropriate segmentation of customer base

• The branch network as a strategic asset

• All customer facing processes being redesigned and automated

• Earning the trust of the community

• Cultural change program

• Technology being implemented:

– Integrated front-end across all channels and products

– Straight through processing

– CRM and behaviour scoring

100

165

191 192

Control Cards Access a/c Mortgages

CRM Marketing(Recent Case Study

demonstrating effectiveness of predictive models)

Page 20

Our targets

• Increase NPAT by 15%+ CAGR to 2005

• Continue above market growth momentum of product businesses

• Develop above market growth momentum in customer businesses

• Continue to drive productivity to fund growth investments

• Grow customers faster than our peers

– 1 million new customers by 2005

• Double customer and staff advocacy by 2004

– Publicly report results

Page 21

Summary

• Personal is performing well – specialisation works – above market growth

• We have substantial growth opportunities

• Now applying specialist focus to our customer businesses

• We are differentiating ourselves through our specialist strategy

Realising a unique growth

opportunity