H

H

H

J

The 2014-2019 Global Edugame Market, Ambient Insight, LLC

3

Table of Contents

Table of Figures .................................................................................... 4

Executive Overview .............................................................................. 5

Definitions: Game-based Learning and Simulation-based Learning are Different

Product Types ............................................................................................. 7

Definition of Game-based Learning ................................................................................... 8

Definition of Simulation-based Learning ............................................................................. 8

Gamification Versus Game-based Learning ......................................................................... 9

Sources of Data on the US and Worldwide Edugame Market .............................. 9

2014-2019 Global Edugame Revenue Forecasts ..................................... 10

Where are the Buyers? Global Edugame Market by Region .............................. 10

Who are the Buyers? Global Edugame Revenues by Buyer Segment ................ 11

What Are They Buying? Global Edugame Revenues by Product Type ................ 13

2014-2019 US Edugame Revenue Forecast ............................................ 14

US Edugame Revenues by Buying Segment .................................................. 14

2014-2019 US Consumer Spending on Mobile Edugames by Six Categories ...... 17

Ambient Insight's Six Mobile Edugame Categories .................................................. 18

Brain Trainers and Brain Fitness Games ............................................................................18

Knowledge-based Games ................................................................................................19

Skill-based Games .........................................................................................................19

Language Learning Games ..............................................................................................20

Location-based Learning Games ......................................................................................20

Mobile Augmented Reality Games ....................................................................................21

Leading Indicators: Edugame Private Investment Patterns ....................... 22

Sources of Information on Learning Technology Investments .......................... 24

The 2014-2019 Global Edugame Market, Ambient Insight, LLC

4

Table of Figures

Figure 1 - 2014-2019 Global Forecasts for Game-based Learning and Simulation-based Learning ...... 5

Figure 2 - Ambient Insight’s Learning Technology Research Taxonomy ........................................... 6

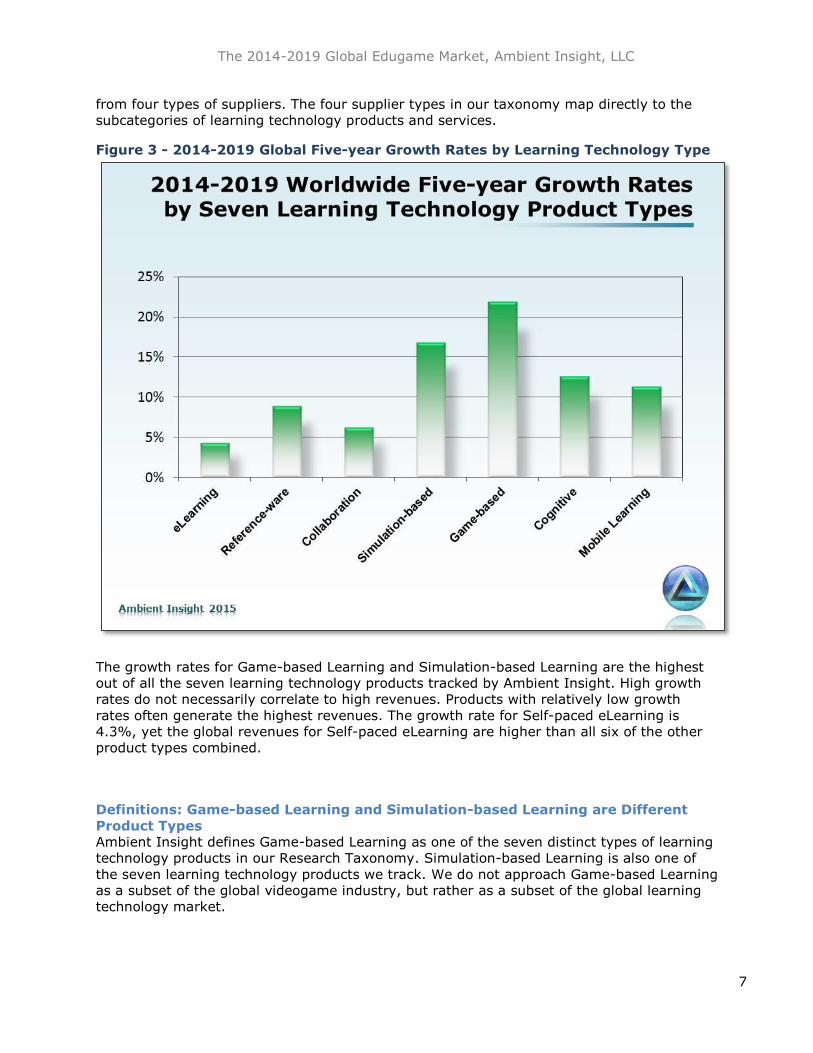

Figure 3 - 2014-2019 Global Five-year Growth Rates by Learning Technology Type .......................... 7

Figure 4 - 2014-2019 Worldwide Game-based Learning Revenues by Seven Regions .......................11

Figure 5 - 2014-2019 Worldwide Game-based Learning Market by Buyer Segment..........................12

Figure 6 - 2014-2019 Global Edugame Revenues by Product Type (in US$ Millions).........................13

Figure 7 - 2014-2019 US Game-based Learning Market by Buyer Segment (in US$ Millions) ............15

Figure 8 - 2014-2019 US Game-based Learning Revenues by Delivery Platform ..............................16

Figure 9 - 2014-2019 US Edugame Revenues by Game Category (in US$ Millions) ..........................17

Figure 10 - Proximity Triggers Location-based Learning ...............................................................21

Figure 11 - 2010-H1/2015 Global Investment in Game-based Learning Companies (US$ Millions) .....23

About Us

Ambient Insight is an ethics-based market research firm that identifies revenue opportunities

for learning technology suppliers. We track the learning technology markets in 119 countries.

Ambient Insight publishes quantitative syndicated reports that break out revenues by customer

segment (demand-side) and by product category (supply-side) based on our taxonomy and

our proprietary Evidence-based Research Methodology (ERM). We specialize exclusively in

learning technology; we have the most complete view of the international learning technology

market in the industry.

www.ambientinsight.com

The 2014-2019 Global Edugame Market, Ambient Insight, LLC

5

Executive Overview Worldwide revenues for Game-based Learning products and services reached $1.8 billion in

2014. The global five-year compound annual growth rate (CAGR) is 21.9% and revenues

will more than double to $4.9 billion by 2019. The terms Game-based Learning and

edugame are used interchangeably in this whitepaper.

Figure 1 - 2014-2019 Global Forecasts for Game-based Learning and Simulation-

based Learning

In our Research Taxonomy, Ambient Insight defines Game-based Learning and Simulation-

based Learning as two different types of learning technology products. The global revenues

for Simulation-based Learning are provided here to provide context. The worldwide

Simulation-based Learning market has a 16.8% growth rate and revenues will climb to $8.3

billion by 2019. Combined, the two products will generate $13.2 billion for suppliers by

2019.

This whitepaper includes an analysis of the global edugame market by seven regions: North

America, Latin America, Western Europe, Eastern Europe, Africa, Asia, and the Middle East.

It also breaks down the global revenues by eight buying segments: consumer, preschool,

primary education, secondary education, tertiary education, corporations & businesses,

federal government agencies, and state/provincial/local government agencies.

The 2014-2019 Global Edugame Market, Ambient Insight, LLC

6

Since edugames are heavily concentrated in the early academic grades, Ambient Insight

breaks out the PreK-12 segment by three sub-categories: preschool, primary, and

secondary. The tertiary segment includes vocational, professional, and higher education

institutions.

Figure 2 - Ambient Insight’s Learning Technology Research Taxonomy

This whitepaper also includes a "deep dive" into the edugame market in the US. The US

section of this whitepaper breaks out revenues by the same eight buying segments. It also

provides a detailed analysis of the consumer buying behavior for six types of mobile

edugames:

Knowledge-based games

Skills-based games

Brain trainers

Language learning games

Location-based learning games (emerged in 2009)

Mobile augmented reality games (emerged in 2010)

The purpose of our taxonomy is to provide clarity to suppliers competing in a complex

global market. We track buying behavior in over 119 countries across seven international

regions. We track six buyer segments that buy seven types of learning technology products

The 2014-2019 Global Edugame Market, Ambient Insight, LLC

7

from four types of suppliers. The four supplier types in our taxonomy map directly to the

subcategories of learning technology products and services.

Figure 3 - 2014-2019 Global Five-year Growth Rates by Learning Technology Type

The growth rates for Game-based Learning and Simulation-based Learning are the highest

out of all the seven learning technology products tracked by Ambient Insight. High growth

rates do not necessarily correlate to high revenues. Products with relatively low growth

rates often generate the highest revenues. The growth rate for Self-paced eLearning is

4.3%, yet the global revenues for Self-paced eLearning are higher than all six of the other

product types combined.

Definitions: Game-based Learning and Simulation-based Learning are Different

Product Types

Ambient Insight defines Game-based Learning as one of the seven distinct types of learning

technology products in our Research Taxonomy. Simulation-based Learning is also one of

the seven learning technology products we track. We do not approach Game-based Learning

as a subset of the global videogame industry, but rather as a subset of the global learning

technology market.

The 2014-2019 Global Edugame Market, Ambient Insight, LLC

8

In the context of the global learning technology market, isolating Game-based Learning

products is relatively straightforward. Isolating the Game-based Learning market in the

context of the global videogame industry is a daunting task and rarely attempted in the

industry.

Definition of Game-based Learning

In Ambient Insight's Research Taxonomy, Game-based Learning is defined as a knowledge

transfer method that utilizes "game play," which includes some form of competition (against

oneself or others) and a reward/penalty system that essentially functions as an assessment

method. Game-based Learning products (edugames) have explicit pedagogical goals. A user

"wins" an edugame when they achieve the learning objectives of the gameplay.

All educational games are designed for behavior modification (learning), pedagogical

intervention, or cognitive remediation. The first two are well known but the third is relatively

new.

There are remediation-based edugames designed to alter behavior attributed to

developmental or cognitive challenges (such as dyslexia.) There are also remediation

edugames used to strengthen appropriate (and mitigate inappropriate) behavior in areas of

health and wellness, diversity, conflict management, team building, and leadership.

Virtual worlds designed for children often embed edugaming in semi-immersive

environments. Whyville, JumpStart, and Mingoville are good examples of virtual worlds that

include edugames designed for children. Most virtual worlds for children under ten include

edugames.

Virtual worlds that embed edugames illustrate the difference between Simulation-based

Learning and Game-based Learning. The "environment" is indeed simulated but the

knowledge transfer method is game-based. In Simulation-based Learning, the simulation

itself is the knowledge transfer method.

Definition of Simulation-based Learning

There are distinct pedagogical differences between Simulation-based Learning and Game-

based Learning. There is confusion in the marketplace with practitioners and suppliers using

the terms interchangeably.

The definitions of Simulation-based Learning and Game-based Learning in our taxonomy are

based on the research done by Alessi and Trollip. In their seminal work entitled, "Computer

Based Instruction: Methods and Development," they identified five types of computer-aided

instruction (CAI): drills, tutorials, simulations, instructional games, and tests. Alessi and

Trollip define four types of Simulation-based Learning:

Physical Object and Environmental

Process

Procedural

Situational

The researchers compressed these four into two instructional strategies: learning about

something (physical and process), and learning to do something (procedural and

situational). These can be restated in instructional terms as knowledge-based and

performance-based simulations.

The 2014-2019 Global Edugame Market, Ambient Insight, LLC

9

Ambient Insight does not include high-end military, aviation, and heavy equipment

simulator revenues in our forecasts. The barriers-to-entry are quite high to develop and

market these machines and only a handful of suppliers can compete in the simulator

market.

Gamification Versus Game-based Learning

There is a continuing debate (if not confusion) about the difference between gamification

and Game-based Learning and the two terms are often conflated. They are different things.

Edugame provider SpongeLab describes the difference this way:

"Gamification is the application of videogame rules, mechanics and conventions to a non-

gaming situation. Put simply, if a student is playing a videogame and learning from it, we

aren’t witnessing gamification - the student is experiencing game-based learning. An

educational game hasn’t been ‘gamified’ - because it’s a game already!"

Brian Burke, author of the 2014 book called Gamify: How Gamification Motivates People to

Do Extraordinary Things, writes that "Gamification is often loosely defined, leading to

market confusion, inflated expectations and implementation failures." The confusion in the

education and training industry is due in some part to the "bolting" on of game elements to

legacy education and training products.

For example, Badgeville sells gamification add-ons for corporate training. Course Hero has

online courses that use Bunchball’s game mechanics. Oxford University Press and Scholastic

use SecretBuilder’s game platform to "gamify books".

According to Bunchball, "Gamification is the process of taking something that already exists

– a website, an enterprise application, an online community – and integrating game

mechanics into it to motivate participation, engagement, and loyalty. Gamification takes the

data-driven techniques that game designers use to engage players, and applies them to

non-game experiences to motivate actions that add value to your business."

Sources of Data on the US and Worldwide Edugame Market The financial reports from the domestic and international online education companies

provide invaluable insight into the rapidly evolving market conditions and revenue

opportunities in any given country. The financial reports of publicly-traded online education

suppliers are particularly useful in providing insight into buying behavior in specific regions

and countries.

Most of these learning technology companies focus on particular products, buying segments,

and specific types of content so their financial reports provide details on specific buying

behavior patterns in each of the buying segments analyzed in this whitepaper.

The major international educational publishers are active in most countries of the world.

Pearson, McGraw-Hill, Santillana, Cambridge University Press, Houghton Mifflin Harcourt,

Oxford University Press, and Macmillan all have significant market presence across the

globe and their financial reports provide detailed data on the academic segments.

There are several analytics firms that track the top selling mobile apps in the major app

stores in countries across the planet. All of them have an education category. App Annie

and Distimo (now owned by App Annie) are the best-known global app analytics firms; they

The 2014-2019 Global Edugame Market, Ambient Insight, LLC

10

provide extensive data on the top selling and top downloaded Mobile Learning apps in all of

the countries analyzed in this report. Their top 100 rankings provide insight on the demand

for specific types of content.

A comprehensive source of data on trends in the Game-based Learning industry is the Gamesandlearning.org site. They describe themselves this way: "Gamesandlearning.org is a

news and information service aimed at increasing the amount of information available for

those interested in developing and funding new educational games for children and young

adults. The site is operated by the Joan Ganz Cooney Center at Sesame Workshop and is a

project of the Games and Learning Publishing Council. The Council and the Site are made

possible by a grant from the Bill & Melinda Gates Foundation."

2014-2019 Global Edugame Revenue Forecasts Worldwide revenues for edugames (mobile and non-mobile combined) reached $1.8 million

in 2014. The five-year compound annual growth rate (CAGR) is a robust 21.9% and

revenues will surge to $4.9 billion by 2019. The global Game-based Learning revenues are

heavily concentrated in Asia, followed by North America.

Where are the Buyers? Global Edugame Market by Region Asia accounts for the vast majority of mobile edugame revenues throughout the forecast

period. China is the top edugame buying country in Asia (and indeed, the world).

Consumers in China spent $621.7 million on mobile education apps and edugames in 2014;

this is higher than the entire amount spent in North America in 2014.

Early childhood learning apps dominate the top selling app rankings in China, followed by

language learning apps. Eighteen of the twenty top-selling educational apps in Apple's store

in China in June 2015 were early learning childhood apps. Essentially all early learning

childhood apps contain game play.

Magikid, BabyBus, 2Kids, Coco Play,TribePlay, and SmarTots are the largest early childhood

learning app developers in China in terms of revenue. Apps from all of them consistently

rank in the top selling educational apps in China.

In terms of growth, the Middle East has the highest growth rate for Game-based Learning at

48.5%, followed by Africa, Eastern Europe, and Latin America at 46.7%, 41.5%, and

36.7%, respectively. High growth rates usually (but not always) are the result of low

baseline revenues and revenues for edugames were quite low in all of these regions in

2014. That said, the revenues will spike to relatively high amounts by 2019 in all of the high

growth regions.

The growth rate for edugames in Western Europe is a robust 26.9% and revenues will more

than triple to $46.2 million by 2019. The United Kingdom is the top edugame buying

country in Western Europe, followed by Spain and France. Like almost all countries in the

world, the edugame market in the UK is being driven by consumer demand for mobile

edugames.

Nine of the top twenty bestselling educational apps in the Apple store in the UK in June

2015 were early childhood learning apps. There were three brain trainers in the top twenty:

Lumosity (ranked in third place), Peak, and Fit Brains.

The 2014-2019 Global Edugame Market, Ambient Insight, LLC

11

Figure 4 - 2014-2019 Worldwide Game-based Learning Revenues by Seven

Regions

NOTE: These forecasts are for mobile and non-mobile (PC/web/console) edugames combined, although the vast amount of expenditures are for mobile edugames.

The growth rate for edugames in North America (Canada and the US combined) is 14.6%.

Revenues will nearly double to $920.2 million by 2019. The North America edugame market

is dominated by US consumer demand for mobile edugames and revenues for mobile

edugames far outpaced the revenues for non-mobile (PC/web/console) edugames. A

detailed analysis of US consumer buying behavior is provided in this whitepaper.

Who are the Buyers? Global Edugame Revenues by Buyer Segment This section breaks out global revenues by eight buying segments: consumer, preschool,

primary education, secondary education, tertiary education, corporations & businesses,

federal government agencies, and state/provincial/local government agencies.

Prior to 2015, Ambient Insight combined all PreK-12 buying behavior into a single segment.

For the edugame market, we now breakout the PreK-12 by three sub-segments: preschools,

primary, and secondary. We do this because the academic revenues for edugames are

The 2014-2019 Global Edugame Market, Ambient Insight, LLC

12

highly concentrated in the lower grades; this more granular breakout provides visibility into

the specific revenue opportunities in PreK-12.

Figure 5 - 2014-2019 Worldwide Game-based Learning Market by Buyer Segment

Consumer spending on mobile edugames across the planet accounted for 74% of all global

spending in 2014. By 2019, consumers will still account for 66% of all Game-based Learning

expenditures.

The highest growth rates are in the tertiary education, preschool, and corporate segments

at 40.1%, 33.6%, and 29.3%, respectively. Except for the primary education sub-segment,

revenues are still relatively low in the other academic segments.

The uptake in the tertiary and corporate segments is the first clear evidence of traction in

both of those slow-adopter segments. Corporations across the planet outspend the primary

schools on edugames. This is clear evidence that the stigma (play is inappropriate at work)

of Game-based Learning in the workplace is fading fast and directly related to the younger

demographic in the workplace; both managers and employees grew up playing video games

and digital edugames.

The 2014-2019 Global Edugame Market, Ambient Insight, LLC

13

What Are They Buying? Global Edugame Revenues by Product Type It should be no surprise that packaged retail content accounts for the vast amount of

expenditures on digital edugames throughout the forecast period. Sales of packaged mobile

edugames reached $1.5 billion in 2014. The growth rate is a healthy 21.7% and revenues

will reach $4.2 billion by 2019.

Figure 6 - 2014-2019 Global Edugame Revenues by Product Type (in US$ Millions)

In terms of content types, early childhood learning apps, language learning apps, and brain

trainers consistently rank in the top twenty bestselling Mobile Learning apps in almost every

country of the world. By far, early childhood learning apps dominate the global market.

The growth rate for custom content development services is the highest of all three

edugame product types at 25.7%. The demand is heavily concentrated in the corporate and

government segments.

There is still no significant demand for specialized edugame tools or platforms. The growth

rate is negative at -2.6% and revenues will drop slightly to $32.2 million by 2019. General-

purpose Self-paced Learning and Mobile Learning tools and platforms are experiencing brisk

sales (particularly in Asia) and often used to author edugames. Adobe's Flash tool is still a

popular edugame authoring tool and the general-purpose game engine Unity is used by

many edugame developers as well. This is dampening the demand for specialized edugame

tools.

The 2014-2019 Global Edugame Market, Ambient Insight, LLC

14

An interesting edugame platform is eSyncTraining's EduGame Cloud, which is a plug-in for

Adobe's Connect conferencing tool. EduGame Cloud is integrated with the Connect

interfaces for Blackboard, Canvas, and Moodle. There are educational versions of MineCraft

and SimCity called MinecraftEDU and SimCityEDU, respectively.

The high growth rates for digital edugames in the global corporate segment would indicate a

need for specialized Game-based Learning tools, but corporations (and government

agencies) tend to buy services from third-party developers; the buyer of the tools is not the

corporation but rather the service provider.

The one "sweet spot" for specialized edugame tools are Location-based Learning tools used

to develop mobile games for galleries, tourist attractions, zoos, aquariums, parks, and

exhibitions. These developers use their tools to create custom edugames for clients and also

license the platforms for organizations that want to build the edugames in house.

2014-2019 US Edugame Revenue Forecast The revenues for Game-based Learning products and services reached $436.8 million in the

US in 2014. This is for edugames on all delivery platforms combined including mobile, PC,

web, and console. The growth rate is 12.7% and revenues will climb to $792.8 million by

2019. The revenues are concentrated in the consumer segment and the PreK-12 segment

(broken out by three sub-segments in this section). Corporations and government agencies

are strong buyers of custom Game-based Learning development services.

US Edugame Revenues by Buying Segment This section breaks out expenditures by eight buying segments: consumer, preschool,

primary education, secondary education, tertiary education, corporations & businesses,

federal government agencies, and state/provincial/local government agencies.

The highest growth rates in the US are in the academic segments. The tertiary segment has

the highest growth rate of 38.8%, virtually on par with the global growth rate for that

segment. Revenues were quite low in this segment in 2014, but will grow over five times to

$21.8 million by 2019.

The growth rate in the secondary academic segment in the US is 32.6%; revenues will spike

from a modest $8.2 million in 2014 to $33.5 million by 2019. Unlike the early grades, the

edugames in highest demand are primarily STEM-related. Math edugames are the top

bestselling edugames in this segment.

The growth rates in the preschool and primary PreK-12 sub-segments are 28.3% and

21.3%, respectively. The games used in those sub-segments all center on early childhood

learning topics including literacy, numeracy, and basic cognitive skills. In the US, Game-

based Learning is ubiquitous in the early grades but starts to taper out in upper middle

school.

The app store providers have made it easier for schools to provision mobile devices. Google,

Apple, and Amazon now offer volume discounts and volume provision platforms for the

The 2014-2019 Global Edugame Market, Ambient Insight, LLC

15

schools. A major catalyst for Mobile Learning in the US academic segments is the rapid

adoption of tablets in the schools. When schools buy both laptops and tablets, they tend to

provide the younger children with the tablets.

In terms of demand, the academic segments tend to purchase packaged retail content and

organizational buyers buy both retail packaged content and custom development services.

Language learning apps are the top bestselling retail apps in the government and corporate

segments.

The growth rates in the federal and state/local agencies are 11.5% and 16.1%,

respectively. Government agencies pay developers to create mobile edugames mostly for

young children on a range of topics including literacy, health, and language learning. The US

State Department paid The SuperGroup in Atlanta to develop the Trace Effects edugame

used to teach people English. "Gamers interact and solve puzzles in a virtual world filled

with diverse English-speaking characters."

Figure 7 - 2014-2019 US Game-based Learning Market by Buyer Segment (in US$

Millions)

NOTE: This forecast includes revenues for mobile and non-mobile (PC/web/console) edugames. A detailed analysis of the consumer expenditures on mobile edugames is provided in another section of this whitepaper.

Consumers account for the majority of expenditures in the US and those expenditures are

heavily concentrated in mobile edugames. Consumers still buy a significant amount of non-

The 2014-2019 Global Edugame Market, Ambient Insight, LLC

16

mobile edugames (PC, web-based, and some console edugames) but the US consumer

edugame market is dominated by mobile edugames.

The growth rate for non-mobile edugames (across all buying segments combined) is quite

negative at -12.5%; the revenues are being cannibalized by mobile edugames and the

decline of non-mobile edugames in the supply chain. There are very few console-based

edugames left on the market. Learning is by definition personal and mobile devices have

proved ideal as a knowledge transfer method.

Game companies that focus on the console games rarely develop edugames. Relative to the

massive revenues generated by other types of games, there is little incentive for them to

develop edugames. Nintendo and Microsoft still have edugames on the market for their

consoles.

Figure 8 - 2014-2019 US Game-based Learning Revenues by Delivery Platform

The growth rate for mobile Game-based Learning products in the US (across all buying

segments) is a robust 20.3% and revenues will spike to $714.0 million by 2019. The spike

in revenues for mobile edugames is due in large part to the strong demand in the consumer

segment.

The 2014-2019 Global Edugame Market, Ambient Insight, LLC

17

2014-2019 US Consumer Spending on Mobile Edugames by Six Categories Consumers in the US spent $328.4 million on Game-based Learning products (both mobile

and non-mobile combined) in 2014 and $276.1 million of these expenditures were for

mobile edugames. The growth rate for mobile edugames in the consumer segment is a

healthy 11.7% and revenues will reach $479.3 million by 2019.

In the 2014 market, roughly 87% of all consumer spending on Game-based Learning was

for mobile edugames. By 2019, mobile edugames will account for 92% of all consumer

spending on digital game-based education products.

Language learning edugames generated the highest revenues for Mobile Learning suppliers

in the 2014 market. The resurgence (if not the reinvention) in the demand for brain trainers

is due to the migration to smartphone formats. By 2019, brain trainer revenues will reach

$123.1 million, the highest of all mobile edugame categories.

Figure 9 - 2014-2019 US Edugame Revenues by Game Category (in US$ Millions)

The number one bestselling educational app in the Apple app store in the US as of July 2015

was the early childhood learning app ABCmouse. There were nine early childhood learning

apps in the top twenty bestselling educational apps. There were three brain trainers in the

top twenty including Lumosity (ranked at second place), Elevate, and Fit Brains.

The 2014-2019 Global Edugame Market, Ambient Insight, LLC

18

In the Google's Play Store in the US in July 2015, Lumosity was the number one

bestselling app. There were two other brain trainers in the top twenty: Elevate and

NeuroNation.

In the Windows store in July 2015, eight of the top twenty were early childhood

learning apps.

In the Amazon store in July 2015, eleven of the top twenty bestselling educational

apps were early childhood learning apps including a MY LITTLE PONY app at number

one. Lumosity's brain trainer came in at number two.

Perhaps the most innovative mobile edugames coming on the market are based on location-

based technology and augmented reality platforms. New location-based Mobile Learning

(also known as locative-learning) products are shifting from merely navigating the user to a

place, to engaging the user in learning experiences at a location in both time and space. For

learning, this translates to, "I’m here, what is or has been here?"

Ambient Insight's Six Mobile Edugame Categories

Ambient Insight defines six categories of mobile edugames to help suppliers identify specific

revenue opportunities:

Knowledge-based games

Skills-based games

Brain trainers

Language learning games

Location-based learning games (emerged in 2009)

Mobile augmented reality games (emerged in 2010)

The growth rates for augmented and location based edugames in the US consumer segment

are very high at 61.7% and 36.98%, respectively. The growth rates are almost certainly

due to the low baselines in the 2014 market; although analysts are trained not to equate

correlation with causation. The major catalysts for both these mobile edugame types are

also due to the rapid evolution of both location-based technology and augmentation

products.

Brain Trainers and Brain Fitness Games

Brain trainer and brain fitness games are based on cognitive science, neuropsychology, and

brain-based learning theories emerging from educational psychology and educational

neuroscience. It is an instructional method that targets the neuro-physiological processes

involved in learning and has little in common with traditional instructional design principles.

The "fitness" metaphor derives from physical exercise concepts. Researchers and suppliers

have a growing body of empirical evidence to show that people who use the products can

condition and train the brain to improve memory, attention, visual and spatial awareness,

auditory processing, linguistic skills, planning skills, and problem solving.

Ambient Insight does not categorize products designed for cognitive rehabilitation or for

clinical diagnosis as brain training games even though many of these products integrate

gaming elements in their products.

The 2014-2019 Global Edugame Market, Ambient Insight, LLC

19

Brain trainers emerged in 2005; they were pioneered by Nintendo and had a near-instant

success all over the world. They continue to be popular with consumers across the globe.

Nintendo single-handedly created the international market for the brain trainers. Nintendo

has defined this new category of games as "mental training." Brain Age was released in

2005 and was the first commercial brain trainer success; as of March 2015, over 20 million

copies of Brain Age had been sold across the planet – 4.1 million in Japan alone.

Brain Age 2 was even more popular and 5.3 million copies have been sold in Japan. Mobile

brain trainers for smartphones now consistently rank in the top twenty bestselling

educational apps in most countries in Asia; brain trainers developed for mainstream mobile

devices have essentially created a second wave of demand for the products.

In December 2012, Vancouver-based Vivity Labs (now owned by Rosetta Stone) launched

their brain trainer mobile app in the Apple store and sold one million copies in the first 60

days. Until quite recently, mobile brain trainers were primarily designed for Nintendo

devices. The brain training suppliers migrated their products to mobile phone formats in the

last three years and there are now dozens of brain trainers on the market that are

experiencing brisk sales.

Consumers in the US spent $64.1 million on mobile brain trainers in 2014. Nintendo, Lumos

Labs, and Vivity Labs (now owned by Rosetta Stone) are the top mobile brain trainer

suppliers in the US. Nintendo still dominates the US market due to the continued popularity

of their Brain Age series of games. The latest version was released in the US in February

2013. New brain trainer suppliers entered the market in 2013 and 2014 including Peak,

Memorado, NeuroNation, and Elevate.

Knowledge-based Games

Handheld and mobile knowledge-based edugames are designed to help users learn and

memorize concepts, principles, facts, patterns, and rules (such as verb conjugation.) These

edugames are usually designed as quizzes, flashcards, or trivia games. They are relatively

easy to design and there are commercial development tools on the market. Players compete

for high scores and often the incentive is a race against the clock.

In the current market, the majority of knowledge-based mobile games are designed for the

PreK-3 market. They focus predominantly on the "3 R’s" to help children learn to recognize

shapes, colors, letters, words, and numbers. Test prep edugames for standardized exams

are also prevalent. In the US consumer segment, mobile knowledge-based edugames have

a modest growth rate of 9.5%.

This type of mobile edugame is the most mature and suppliers tend to compete on price,

more so than the other categories. That said, this type of edugame will generate the third-

highest revenues throughout the forecast period; revenues in the US consumer segment will

reach $84.2 million by 2019.

Skill-based Games

A skill is the ability to apply knowledge in the context of a performance. Skill-based games

are designed to improve hand-eye coordination, improve performance on physical tasks,

and hone psychomotor skills of players. For example, a math game is considered a skill-

based game. Memorizing the rules of math is knowledge-based. Applying that knowledge in

calculations is a skill. Memorizing facts for a driver's license written test is knowledge-based,

while applying those rules in the car is a skill.

The 2014-2019 Global Edugame Market, Ambient Insight, LLC

20

An excellent example of Skill-based edugames are cooking apps. They provide step-by-step

instructions on how to cook specific food items. The recipe is knowledge-based, but the

performance of following the recipe is skill-based. Gameloft (Pocket Chef) and Nintendo

(Cooking Mama) have some of the most popular cooking edugames.

Mobile flight simulators are now accurate enough to teach people the basics of operating a

plane. RealFlight sells mobile flight simulators for both the iOS and Android platforms.

"RealFlight Mobile makes it easy to learn basic flight skills in a hurry." A company called X-

Plane also sells mobile flight simulators that they claim are "85% as accurate as the

simulator currently being used by companies like Boeing, Lockheed Martin, and NASA." The

game elements in these apps comes from "challenges" that need to be overcome.

The growth rate for this type of mobile edugame in the US segment is a healthy 10.3% and

revenues will surge to $71.5 million by 2019. A major catalyst for this type of mobile

edugame is the advances in tablet and smartphone technology.

Language Learning Games

Memorizing foreign words is knowledge-based, while using those words in speech and

writing is a skill. Ambient Insight breaks out mobile language learning edugames for

suppliers because they are part of the greater language learning market. There is a growing

demand for language learning edugames on mobile devices and the revenue opportunities

are significant.

This type of mobile edugame has been a staple in the Japanese market and now games like

this are being adopted across the planet. The language "coaching" games for the Nintendo

devices are good examples of this genre. Speech recognition and real time translation are

used in the more sophisticated language learning games.

In the US consumer segment, the growth rate for this type of mobile edugame is 7.4%, the

lowest of all six types of mobile edugames. Yet, this edugame type generated the highest

revenues in 2014 at $93.1 million and will be the second bestselling mobile edugame type

by 2019 with revenues of $114.0 million. Language learning edugames for young children

are the bestselling products. These products are designed to teach children their native

language and also to learn a second language.

Location-based Learning Games

Location-based Learning games, one of the "native" types of Mobile Learning defined by

Ambient Insight, emerged in 2009. Essentially, developers are designing educational game

play around physical locations and in time.

Location-based Learning suppliers have been leveraging innovations that have been driving

location-based services (LBS) and have taken advantage of proximity marketing—the

localized wireless distribution of content to shoppers as they trigger special offers.

RFID chips, GPS chips, barcodes, SMS short codes, and image recognition are often used in

Location-based Learning games, particularly in clinical healthcare environments, first

responder situations, consumer and patient education, museums, tourist attractions,

navigation applications, and in the travel industry.

The 2014-2019 Global Edugame Market, Ambient Insight, LLC

21

Tour guides and exhibition navigation guides are among the fastest growing type of

Location-based Learning edugame. Suppliers create their own apps to sell directly to

consumers and offer a range of custom content services for museum tours, gallery tours,

ghost tours, mystery tours, history tours, nature tours, city tours, and walking tours.

Figure 10 - Proximity Triggers Location-based Learning

In the US consumer segment, the growth rate for mobile Location-based Learning games is

a robust 35.8% and revenues will climb to $52.9 million by 2019. The primary sellers (more

accurately resellers) are tourism and exhibition operators. Visitors often have access to free

apps, but are just as often charged for the apps, particularly if a device is supplied as well.

Mobile Augmented Reality Games

Mobile Augmented Reality utilizes images, schematics, audio, multimedia, historical context,

location data, and other forms of content overlaid on real-world objects via the device’s

camera and manipulated by users holding the device.

The augmented elements are "triggered" by specific objects, radio chips, print-based

markers, barcodes, and location coordinates (collectively these are known as triggers).

Mobile augmented reality games emerged in 2010 and had a rocky start. The demand

diminished in 2012-2013, but came roaring back in 2014 and the first half of 2015; this is

due to the proliferation of augmentation hardware and software being developed and

The 2014-2019 Global Edugame Market, Ambient Insight, LLC

22

marketed by large companies like Microsoft, Sony, Facebook, Google, Apple, and

Qualcomm.

The growth rate for this type of mobile edugame in the US consumer segment is a

staggering 61.7% and revenues will spike to $33.3 million by 2019. It is quite likely that

this forecast will have to be revised upward once the various new augmented reality

platforms gain traction.

In June 2015, NASA and Microsoft announced a partnership in which two HoloLens headsets

would be sent to the International Space Station "The units will be used for a new 'Sidekick'

pilot program that's designed to help crews work on the ISS. The program provides

augmented-reality overlays to educate astronauts about how to perform certain procedures

on the station, which could eventually reduce the need for extensive crew training."

In July 2015, Microsoft launched an RFP for higher education research facilities to submit

project ideas for their new HoloLens augmented realty headset. Microsoft is "interested in

seeing its technology used for things like data visualization, new forms of collaboration,

interactive art and new teaching tools." Case Western has already developed a medical

education app for the headset. Microsoft will provide $100 thousand in seed funding for the

new projects for at least five institutions.

Leading Indicators: Edugame Private Investment Patterns Ambient Insight views private investment activity as a leading indicator. The presence of

concentrated investment activity in specific learning technology types or in products that

target particular buying segments indicates that investors are banking on a significant

return on their investment.

Investor interest in Game-based Learning companies has been rising steadily over the last

five years. In 2011, $32.5 million in funding went to Game-based Learning companies, more

than double the $12.6 million invested in edugame companies in 2010.

Game-based Learning suppliers across the globe garnered $106.3 million in funding in

2014, the highest total in the history of the digital edugame industry. An astonishing $83.6

million was invested in edugame supplies in just the first half of 2015 alone.

Investors are investing heavily in suppliers that make edugames for children. Brazil-based

Movile's mobile education division called PlayKids obtained $15 million in June 2015.

PlayKids consistently rank in the top bestselling educational apps in app stores across the

planet. A Beijing-based company called Satech develops edugames for children with special

needs and obtained $10 million in January 2015. A math edugame company in South Korea

called LocoMotive Labs garnered $4 million in February 2015. Investors are also interested

in companies that sell brain training products:

Lumos Labs (Lumosity) has garnered $67.4 million in private equity since 2008

Berlin-based NeuroNation obtained $2 million in late 2013

Berlin-based Memorado raised $3.3 million in March 2015, on top of the $1.3 million

they obtained in 2014

London-based Peak obtained $7 million in April 2015

The 2014-2019 Global Edugame Market, Ambient Insight, LLC

23

Mobile brain trainers consistently ranked in the top twenty bestselling educational apps in

the app stores in 97 of the 119 countries tracked by Ambient Insight. (Source: The Worldwide

2014-2019 Mobile Learning Market, Ambient Insight, LLC)

Figure 11 - 2010-H1/2015 Global Investment in Game-based Learning Companies

(US$ Millions)

The recent entry of the major learning technology suppliers is a strong indication of a

healthy market. Rosetta Stone acquired Vivity Labs (the developer of the Fit Brains brain

trainer) in late 2013. Rosetta Stone released their Arcade Academy in October 2013, which

they called "the first gamified language-learning app for adults".

Houghton Mifflin Harcourt acquired the virtual world called Curiosityville in May 2014.

Curiosityville’s edugames "teach math and literacy skills to children ages three to eight. As a

child plays in Curiosityville, our data collection and analytical engine provides real-time

information about what and how a child learns. Personalized recommendations to educators

and families extend the learning online and with hands on activities."

The increase in edugame startups also indicate a growing market. There were 560 edugame

startups listed on the Angel List site as of May 2015 (up from 392 in July 2014). This list is a

good way for new suppliers to see which edugame suppliers are getting initial funding.

The 2014-2019 Global Edugame Market, Ambient Insight, LLC

24

Sources of Information on Learning Technology Investments Ambient Insight tracks private investments made to learning technology suppliers via press

releases, financial reports, investment firm sites, targeted searches, and public-domain

investment tracking sites including CrunchBase, Ventures Africa, peHUB, Xconomy,

DealStreetAsia, VCCircle India, VatorNews, EducationInverstor (UK), China Money Network,

SinoBeat, VC4Africa, FinanceAsia, VentureVillage (Germany), the Latin American Private

Equity & Venture Capital Association (LAVCA), SeedTable, the Asian Venture Capital Journal,

DealCurry (India), and VentureBeat.

We also track public domain investment sources that focus on particular countries. For

example, the top information source for the commercial education technology market in

China is a learning technology news website called Jiemo Media (JMDEdu).

www.ambientinsight.com