6225 Lusk Boulevard | San Diego, CA 92121 | Phone 800.317.4747 | Fax 858.546.3741 | www.chandlerasset.com

CHANDLER ASSET MANAGEMENT

September 12, 2013

The Changing Investment Landscape

CAJPA Fall Conference

Martin Cassell, CFA CEO & Chief Investment Officer

Table of Contents

Introduction Major Economic Indicators – Evolution Since Financial Crisis

Section 1 Federal Reserve Balance Sheet

Section 2 Demographic Trends and Their Impact on Fixed Income

Section 3 GSE Reform

Section 4 Portfolio Considerations in the New Investment Landscape

2

December 2006: Prior to the Onset of the Financial Crisis

December-06 Broad Economic Statistics GDP - most recent QoQ 3.2 Unemployment Rate 4.4 Underemployment Rate (U6) 7.9 CPI - YoY 2.5 CPI Core - YoY 2.6

Interest Rates Fed Funds Rate 5.25 Two Year Treasury Yield 4.81 Five Year Treasury Yield 4.69 Ten Year Treasury Yield 4.70

Equity Markets DJIA 12,463.15 S&P 500 1,418.30 NASDAQ 2,415.29

Currencies Dollar Index 83.65 Euro 1.3197 Yuan - China 7.8045 Yen 119.06

3

• GDP growth at trend, unemployment rate low at 4.4%

• Treasury yields comfortably outpaced inflation • Fed Funds rate higher than benchmark Treasury

rates as the interest rate “conundrum” leads to an inverted Treasury curve – recycling of dollars

• Equity market performance strong in 2006 • DJIA 16.29% • S&P 500 13.62% • NASDAQ 9.52%

• Dollar index declined 8.25% during the year

Source: Bloomberg

December 2007: The Financial Crisis Begins

4

December-06 December-07 Broad Economic Statistics GDP - most recent QoQ 3.2 1.5 Unemployment Rate 4.4 5.0 Underemployment Rate (U6) 7.9 8.8 CPI - YoY 2.5 4.1 CPI Core - YoY 2.6 2.4

Interest Rates Fed Funds Rate 5.25 4.25 Two Year Treasury Yield 4.81 3.05 Five Year Treasury Yield 4.69 3.44 Ten Year Treasury Yield 4.70 4.03

Equity Markets DJIA 12,463.15 13,264.82 S&P 500 1,418.30 1,468.36 NASDAQ 2,415.29 2,652.28

Currencies Dollar Index 83.65 76.66 Euro 1.3197 1.4589 Yuan - China 7.8045 7.3037 Yen 119.06 111.75

• GDP growth decelerates below trend and the unemployment rate ticks up

• Headline inflation moves higher but core inflation remains contained

• FOMC begins to ease monetary policy and Treasury yields remain below Fed Funds Rate – conundrum continues

• Equity markets post positive year over year returns

• DJIA 6.43% • S&P 500 3.53% • NASDAQ 9.81%

• Dollar continues to decline in the face of easing monetary policy and better growth prospects in alternative global regions

Source: Bloomberg

December 2008: Risk Markets Collapse

5

December-07 December-08 Broad Economic Statistics GDP - most recent QoQ 1.5 (8.3) Unemployment Rate 5.0 7.3 Underemployment Rate (U6) 8.8 13.5 CPI - YoY 4.1 0.1 CPI Core - YoY 2.4 1.8

Interest Rates Fed Funds Rate 4.25 0.25 Two Year Treasury Yield 3.05 0.76 Five Year Treasury Yield 3.44 1.56 Ten Year Treasury Yield 4.03 2.22

Equity Markets DJIA 13,264.82 8,776.39 S&P 500 1,468.36 903.25 NASDAQ 2,652.28 1,577.03

Currencies Dollar Index 76.66 81.31 Euro 1.4589 1.3971 Yuan - China 7.3037 6.8277 Yen 111.75 90.64

• GDP growth severely negative • Unemployment rate moves

materially higher • Inflation rolls over with the

slowdown in the economy • Fed Funds rate lowered to 0.25%

as the FOMC takes actions to stem deflation risk

• Treasury yields are lower and no longer inverted but one has to invest out to ten year to earn a yield above core inflation

• Equity market crushed • DJIA -33.84% • S&P 500 -38.49% • NASDAQ -40.54%

• Dollar firms in flight to quality Source: Bloomberg

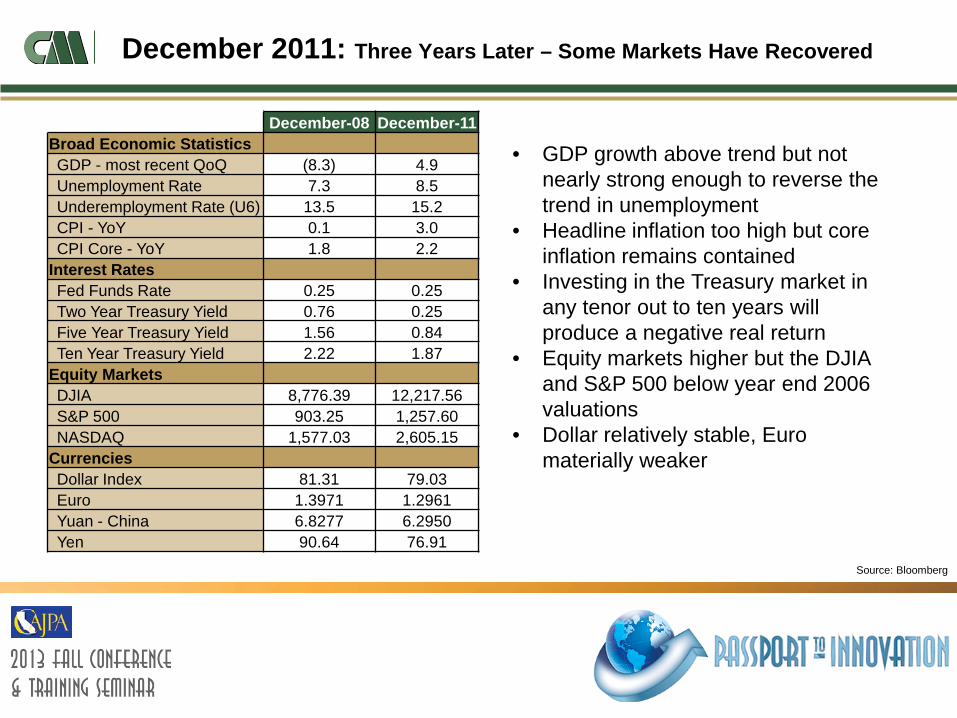

December 2011: Three Years Later – Some Markets Have Recovered

6

December-08 December-11 Broad Economic Statistics GDP - most recent QoQ (8.3) 4.9 Unemployment Rate 7.3 8.5 Underemployment Rate (U6) 13.5 15.2 CPI - YoY 0.1 3.0 CPI Core - YoY 1.8 2.2

Interest Rates Fed Funds Rate 0.25 0.25 Two Year Treasury Yield 0.76 0.25 Five Year Treasury Yield 1.56 0.84 Ten Year Treasury Yield 2.22 1.87

Equity Markets DJIA 8,776.39 12,217.56 S&P 500 903.25 1,257.60 NASDAQ 1,577.03 2,605.15

Currencies Dollar Index 81.31 79.03 Euro 1.3971 1.2961 Yuan - China 6.8277 6.2950 Yen 90.64 76.91

• GDP growth above trend but not nearly strong enough to reverse the trend in unemployment

• Headline inflation too high but core inflation remains contained

• Investing in the Treasury market in any tenor out to ten years will produce a negative real return

• Equity markets higher but the DJIA and S&P 500 below year end 2006 valuations

• Dollar relatively stable, Euro materially weaker

Source: Bloomberg

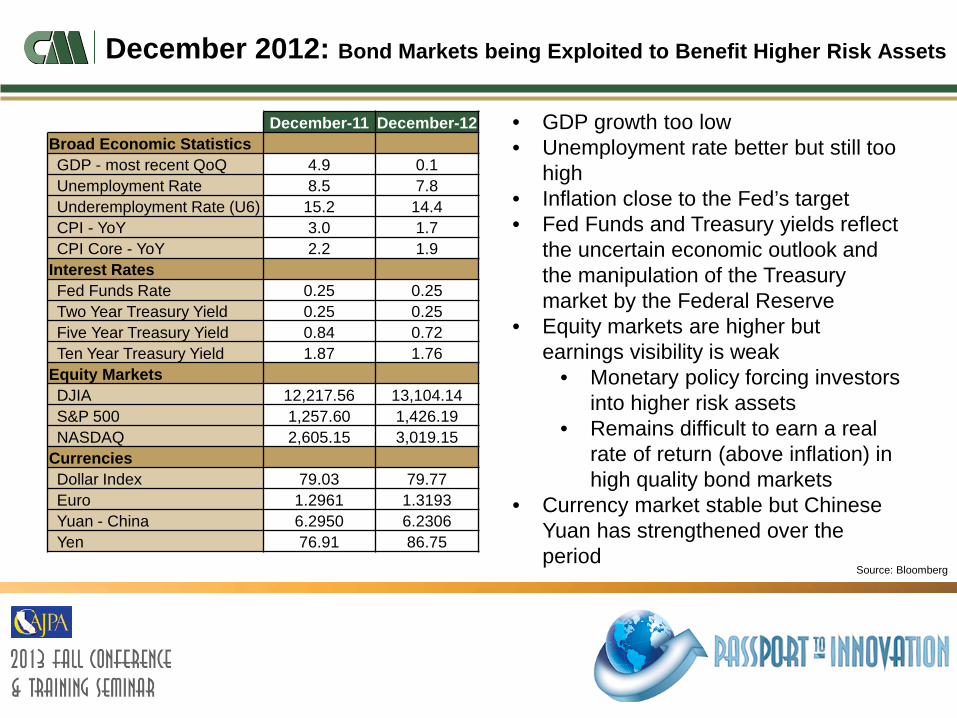

December 2012: Bond Markets being Exploited to Benefit Higher Risk Assets

7

• GDP growth too low • Unemployment rate better but still too

high • Inflation close to the Fed’s target • Fed Funds and Treasury yields reflect

the uncertain economic outlook and the manipulation of the Treasury market by the Federal Reserve

• Equity markets are higher but earnings visibility is weak

• Monetary policy forcing investors into higher risk assets

• Remains difficult to earn a real rate of return (above inflation) in high quality bond markets

• Currency market stable but Chinese Yuan has strengthened over the period

Source: Bloomberg

December-11 December-12 Broad Economic Statistics GDP - most recent QoQ 4.9 0.1 Unemployment Rate 8.5 7.8 Underemployment Rate (U6) 15.2 14.4 CPI - YoY 3.0 1.7 CPI Core - YoY 2.2 1.9

Interest Rates Fed Funds Rate 0.25 0.25 Two Year Treasury Yield 0.25 0.25 Five Year Treasury Yield 0.84 0.72 Ten Year Treasury Yield 1.87 1.76

Equity Markets DJIA 12,217.56 13,104.14 S&P 500 1,257.60 1,426.19 NASDAQ 2,605.15 3,019.15

Currencies Dollar Index 79.03 79.77 Euro 1.2961 1.3193 Yuan - China 6.2950 6.2306 Yen 76.91 86.75

December 2006 – December 2012: Summarizing the High Level Data

8

Source: Bloomberg

December-06 December-07 December-08 December-11 December-12 Broad Economic Statistics GDP - most recent QoQ 3.2 1.5 (8.3) 4.9 0.1 Unemployment Rate 4.4 5.0 7.3 8.5 7.8 Underemployment Rate (U6) 7.9 8.8 13.5 15.2 14.4 CPI - YoY 2.5 4.1 0.1 3.0 1.7 CPI Core - YoY 2.6 2.4 1.8 2.2 1.9

Interest Rates Fed Funds Rate 5.25 4.25 0.25 0.25 0.25 Two Year Treasury Yield 4.81 3.05 0.76 0.25 0.25 Five Year Treasury Yield 4.69 3.44 1.56 0.84 0.72 Ten Year Treasury Yield 4.70 4.03 2.22 1.87 1.76

Equity Markets DJIA 12,463.15 13,264.82 8,776.39 12,217.56 13,104.14 S&P 500 1,418.30 1,468.36 903.25 1,257.60 1,426.19 NASDAQ 2,415.29 2,652.28 1,577.03 2,605.15 3,019.15

Currencies Dollar Index 83.65 76.66 81.31 79.03 79.77 Euro 1.3197 1.4589 1.3971 1.2961 1.3193 Yuan - China 7.8045 7.3037 6.8277 6.2950 6.2306 Yen 119.06 111.75 90.64 76.91 86.75

Inflation Adjusted Fixed Income Returns

Possibility of Positive Real Returns in 2013-2015?

9

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

2004 2005 2006 2007 2008 2009 2010 2011 2012

High Quality Fixed Income versus Core CPI

US Treasury / Agency 1-5 Year Benchmark Core CPI, year over yearSource: Bloomberg & Bank of America Merrill Lynch Indices

SECTION 1

Federal Reserve Balance Sheet

10

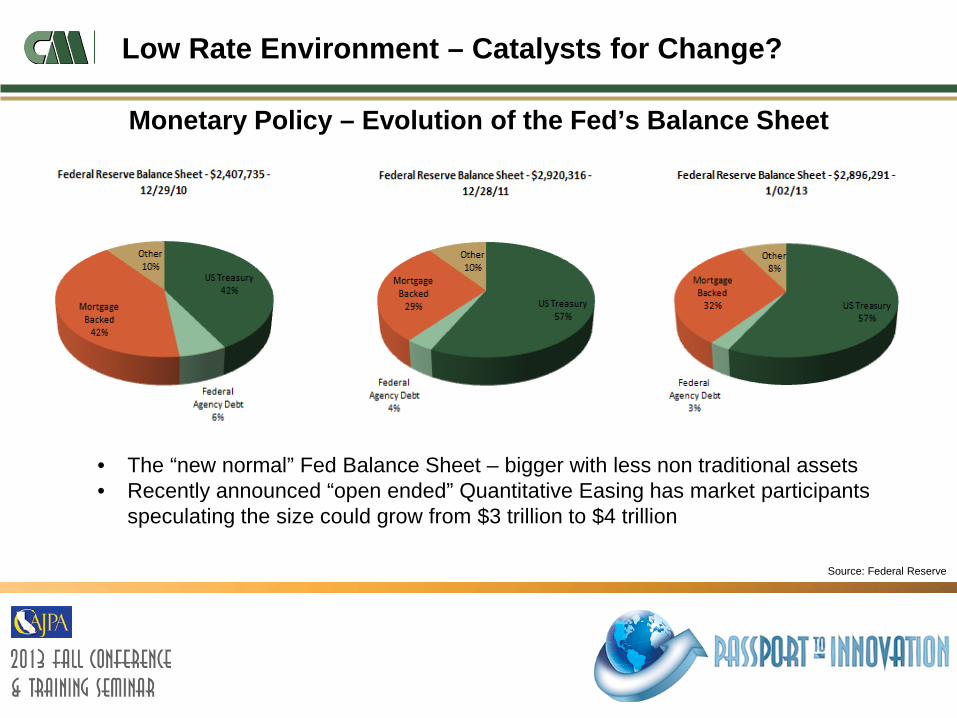

Low Rate Environment – Catalysts for Change?

Monetary Policy – Evolution of the Fed’s Balance Sheet

11

• Prior to the depths of the financial crisis the Fed’s Balance sheet was pristine • Dominated by Treasury assets • Total asset between $850-900 billion

Source: Federal Reserve

Low Rate Environment – Catalysts for Change?

Monetary Policy – Evolution of the Fed’s Balance Sheet

12

• Fed’s balance sheet grows dramatically – 2.5x - to support the economy during the financial crisis

• Treasury assets are no longer the dominant holding • “Other” assets in 2008 include all the initial measures implemented by the Federal Reserve to

inject liquidity into the system • Quantitative easing expands in 2009 to include Mortgage Backed Securities

Source: Federal Reserve

Low Rate Environment – Catalysts for Change?

Monetary Policy – Evolution of the Fed’s Balance Sheet

13

• The “new normal” Fed Balance Sheet – bigger with less non traditional assets • Recently announced “open ended” Quantitative Easing has market participants

speculating the size could grow from $3 trillion to $4 trillion

Source: Federal Reserve

Low Rate Environment – Catalysts for Change?

Will the Fed begin to taper in 2013?

14

Source: Federal Reserve

$0.00

$500,000.00

$1,000,000.00

$1,500,000.00

$2,000,000.00

$2,500,000.00

$3,000,000.00

$3,500,000.00

7/24/2008 7/24/2009 7/24/2010 7/24/2011 7/24/2012 7/24/2013

Asse

ts In

Milli

ons $

Fed's Balance Sheet

Other Assets Emergency Programs Discount Window Borrowing GSE Debt Agency Mortgage Back Security Treasury Bonds

Bear Stearns

Lehman Brothers Fed attempting to

bring stability to the Banking system & the Housing Market

QE1 QE2

QE3

• March 2008 – Bear Stearns melts down and is purchased by JP Morgan • September 2008 – Lehman Brothers goes bankrupt – The Fed begins “Quantitative Easing” • November 2010 – The Fed begins QE-2, purchasing $600 trillion in Treasuries over the next 6 months • In September 2012: The Fed announced open ended purchases of MBSs at the rate of $40 billion per month. • In December 2012: The Fed announced purchases of treasury securities at the rate of $45 billion per month until unemployment remains above

6.5% or inflation rises above 2%.

FOMC Forecasts

Fed Forecast calling for a slow decline in the unemployment rate

15

Source: Federal Reserve

FOMC Forecasts

Dispersion – End of Calendar Year Forecasts

16

Source: Federal Reserve

SECTION 2

Demographic Trends and Their Impact on Fixed Income

17

Demographics

Baby Boom Generation Entering Retirement

18

Source: U.S. Census Bureau, decennial census of population, 1900 to 2000; 2012 Census Summary File 1

Demographics

Demand for Bond Funds Remains Strong

19

Source: Investment Company Institute

$- $0.20 $0.40 $0.60 $0.80 $1.00 $1.20 $1.40 $1.60 $1.80 $2.00

Jun-

03

Dec

-03

Jun-

04

Dec

-04

Jun-

05

Dec

-05

Jun-

06

Dec

-06

Jun-

07

Dec

-07

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

Dec

-10

Jun-

11

Dec

-11

Jun-

12

Bill

ions

Fund Flows

Bond Funds Equity Funds

Demographics

Despite the Low Yield Environment Demand is Not Dropping

20

Demographics

Population Age 65 or Older as a Percentage of those 20-64 Years Old

21

SECTION 3

GSE Reform

22

GSE Reform

■ Fannie Mae and Freddie Mac remain under conservatorship

■ US Treasury recently mandated the retained portfolio accelerate the pace of contraction to 15% per year (previously 10%)

■ No longer required to pay 10% dividend on preferred shares bolstering the capital of each of the entities

■ But…. All profits now flow directly to the US Treasury

■ Agency asset class is likely to provide less yield to investors versus US Treasury securities

Government Sponsored Enterprises

23

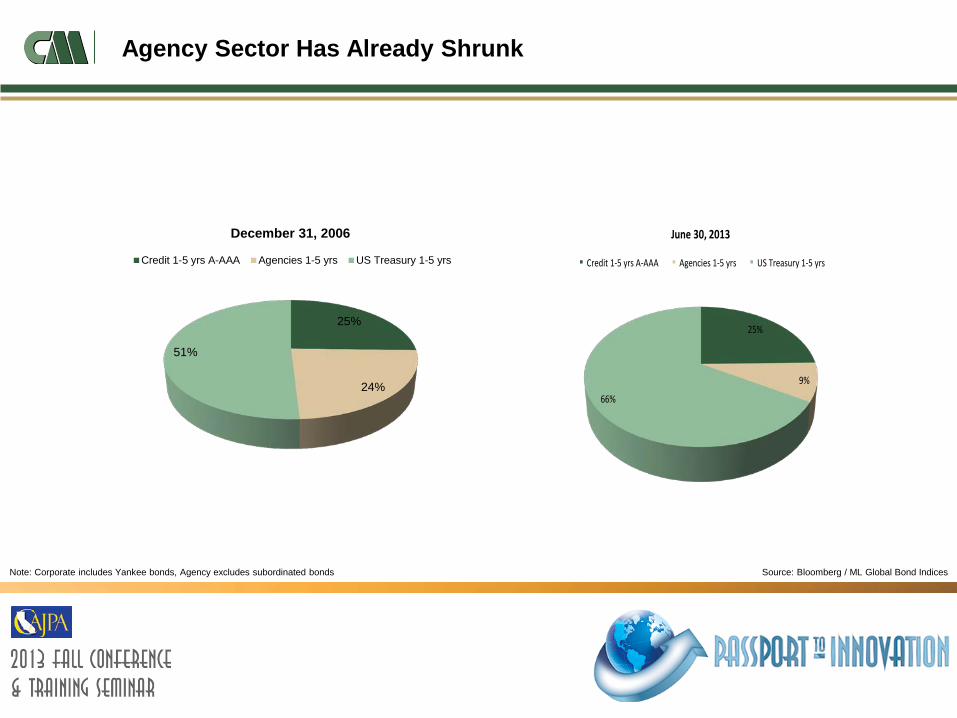

Agency Sector Has Already Shrunk

24

Source: Bloomberg / ML Global Bond Indices Note: Corporate includes Yankee bonds, Agency excludes subordinated bonds

25%

24%

51%

December 31, 2006

Credit 1-5 yrs A-AAA Agencies 1-5 yrs US Treasury 1-5 yrs

25%

9%

66%

June 30, 2013

Credit 1-5 yrs A-AAA Agencies 1-5 yrs US Treasury 1-5 yrs

Yields and Spreads Have Collapsed

25

Source: Bloomberg / ML Global Bond Indices Note: Corporate includes Yankee bonds, Agency excludes subordinated bonds

0.000

1.000

2.000

3.000

4.000

5.000

6.000

12/31/06 12/31/07 12/31/08 12/31/09 12/31/10 12/31/11 12/31/12 06/30/13Credit 1-5 yrs A-AAA 5.259 4.757 5.784 2.757 2.071 2.174 1.048 1.476

Agencies 1-5 yrs 5.087 3.785 1.544 1.533 0.975 0.629 0.419 0.815

US Treasury 1-5 yrs 4.803 3.158 0.814 1.531 0.929 0.413 0.361 0.658

Historical Yields of Sector Components

Credit Quality Evolution

26

8%

40%52%

BofA Merrill Lynch 1-5 Year AAA-A US Corporate Index March 31, 2007

AAA AA A

1%

22%

77%

BofA Merrill Lynch 1-5 Year AAA-A US Corporate Index March 31, 2013

AAA AA A

Source: Bank of America Merrill Lynch Indices

Credit Quality Spread Differentiation

27

0

10

20

30

40

50

60

70

80

90

AAA AA A3/31/2007 44 53 62

3/31/2013 29 52 84

BofA Merrill Lynch 1-5 Year AAA-A US Corporate Index OAS

Source: Bank of America Merrill Lynch Indices

Agency Spreads: Past 3 Years

Agency Universe – Shrinking Supply and Conservatorship

28

Source: Barclays Live

0.000

0.050

0.100

0.150

0.200

0.250

0.300

0.350

0.400

0.45012

/31/

09

02/2

8/10

04/3

0/10

06/3

0/10

08/3

1/10

10/3

1/10

12/3

1/10

02/2

8/11

04/3

0/11

06/3

0/11

08/3

1/11

10/3

1/11

12/3

1/11

02/2

9/12

04/3

0/12

06/3

0/12

08/3

1/12

10/3

1/12

12/3

1/12

02/2

8/13

04/3

0/13

06/3

0/13

Agency Sector OAS (Option Adjusted Spread)

SECTION 4

Portfolio Considerations in the New Investment

Landscape

29

Establishing Investment Objectives

Safety

Maintain appropriate level of exposure to risk

Liquidity

Sufficient short-term investments

Marketable securities

Targeted maturities

Extra layer

Yield (Return, Growth)

Income

Long-term growth

30

Sector Allocation

■ Safety

■ Liquidity

■ Diversification

■ Value

Goals of Sector Allocation

31

US Treas

Hsng Ag

Other Ag

Corp. MTN

Money Market

Preparing for Investment Without Agencies

Housing Agency Issuance is Shrinking

32

■ Safety

■ Liquidity

■ Diversification

■ Value

US Treas

Hsng Ag

Other Ag

Corp. MTN

Alternative Asset Classes

■ Investors are seeking alternatives to traditional public funds asset classes – Treasury and Agency debt

■ Investing in Corporate Notes, Negotiable CDs, Yankee CDs, MBS and ABS can improve income from investments

BUT… as with all investments, the potential for increased return goes hand-in-hand with the assumption of more risk

33

Portfolio Management is Risk Management

The greater an investor’s exposure to properly diversified risk, the higher the expected return over time

The greater an investor’s exposure to risk, the higher the volatility of return from period to period

The objective of “safety” requires establishing risk constraints

Risk is something to be managed not avoided

34

Different Types of Risks

■ Market Risk

■ Credit Risk

■ Liquidity Risk

■ Reinvestment Risk

■ Event Risk

35

Market Risk

■ Also called interest rate risk

■ The risk that the value of a security or a portfolio will change as interest rates change

■ Value can go up or down, inversely to interest rate changes

■ All securities are subject to market risk, even US government guaranteed

■ The longer the duration of the portfolio, the greater the change in value

■ We can’t predict interest rates, but, using duration, we can calculate approximately how much the portfolio market value will change with a given, instantaneous change in interest rates

36

Credit Risk

■ Credit risk is the risk that the issuer of a bond may not be able to make timely payments of principal and/or interest

■ Investors receive higher yields when they purchase riskier securities

■ Agencies vs. Treasuries

■ Corporates vs. Agencies

■ “A” vs. “AAA” Corporates

■ Credit ratings change over time

■ Yield spreads vary over time

37

Liquidity Risk

■ Liquidity risk ■ The risk that the portfolio won’t provide adequate cash flow for

the agency ■ The risk that a security can’t be sold, if necessary, at a good

price ■ Measured by such factors as the difference between bid and

ask ■ Number of market makers for the issue ■ Usually, the larger the issue size, the greater the liquidity

■ Liquidity risk can be minimized by maintaining appropriate balances of short-term securities in the portfolio

38

Reinvestment Risk

■ Reinvestment risk: cash flows from a bond must be reinvested at the market rate at the time the cash flow occurs

■ Interest payments

■ Principal paid at maturity

■ Paydowns from mortgage securities

■ Principal from called bonds

39

Event Risk

■ An unexpected event causes a sudden deterioration in an issuer's credit quality, and a concomitant instant decline in price

■ NRSRO ratings do not (cannot) reflect event risk

40

Macroeconomic Analysis

■ Analysis of economic trends

■ Employment

■ Housing

■ Inflation

■ Federal Open Market Committee announcements and actions

41

Industry Analysis

■ Industry trends

■ Earnings

■ Sales

■ Regulatory issues and changes

■ Demographic and social changes

■ Industry business cycle analysis

42

Issuer Specific Analysis

■ Financial health

■ Profitability

■ Balance Sheet

■ Cash Flow

■ Management and corporate governance

■ Bond covenants

■ Capital structure

43

How to Leverage Changing Market Landscape

■ Conservative Approach: Objective should be consistent, steady returns versus the risk benchmark

■ Transparency: Holdings need to meet the requirements of the statues of the governing body

■ Diversification: A broad mix of securities across eligible sectors and term structure

■ Technology: Access to real time information is imperative to ensure best in class idea generation and trade execution

■ Depth of Team Managing Assets: Portfolio Managers with experience and expertise navigating varied market cycles

■ Manage Risk: Generate risk adjusted out-performance over an intermediate time horizon

High Level Characteristics of a Successful Short Duration Mandate

44

Wrap Up

■ Keep it safe - Don’t overstretch for yield

■ Provide for liquidity

■ Having non-governmental issuers in the portfolio offers greater expected earnings

■ AND involves greater risk

■ Effective implementation of a program of non-governmental investing requires

■ Expertise and the time to perform research and analysis

■ Sufficient resources, including external subscription services

■ Continuous monitoring of issues in the portfolio and under consideration

■ A high level of diversification by sector and by issuer

45

46

Conclusion

■ Do your own credit research, don’t rely strictly on ratings agencies

■ Be aware of the risks in your portfolio

■ Make sure you can pass the “sleep test”

Important Disclosures

47

Past performance is not indicative of future results. The information herein is provided for informational purposes only and should not be construed as a recommendation of any security, strategy or investment product, nor an offer or solicitation for the purchase or sale of any financial instrument. References to investment indices are for informational purposes and do not imply that managing portfolios to those styles will achieve comparable returns. Indices do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment management fee, the incurrence of which would have the effect of decreasing historical performance results. Indices are unmanaged, and one cannot invest directly in an index.

Any forecasts, forward-looking statements and assumptions are inherently limited and should not be relied upon as an indicator of future results. Any opinions and views constitute judgments made by the author at the date of this presentation and may become outdated or superseded at any time without notice. Any statements concerning financial market trends are based on current market conditions, which will fluctuate.

Economic factors, market conditions and investment strategies will affect the performance of any portfolio and there are no assurances that it will match or outperform any particular benchmark. The data contained in this presentation is the property of those providers, which were obtained from sources believed to be reliable, but are subject to change at any time at the provider’s discretion. Unless otherwise noted, Chandler is the source of illustrations, performance data, and characteristics contained in this presentation.

Biography

48

Martin Cassell, CFA CEO, Chief Investment Officer Martin Cassell is the chief executive and investment officer at Chandler Asset Management and is a principal of the firm. Mr. Cassell is responsible for defining, planning, and directing company programs. He heads implementation of the firm’s investment strategies and portfolio risk management. He designed the proprietary quantitative models that drive our investment process, establishing duration, structure, and asset allocation throughout client portfolios. Mr. Cassell joined Chandler Asset Management in 1991 from the City of San Diego where he managed a $1 billion fixed income portfolio. He began his investment career in 1987 managing portfolios at World Savings and Loan. Mr. Cassell received his B.S. in finance from California State University, Hayward. He is a member of the CFA Society of San Diego and holds the designation of Chartered Financial Analyst. He is also a member of the California Association of Joint Power Authorities (CAJPA) finance committee.