The Financial Impact on Student Success

1

Using Data to Create Strategies in a Disruptive Marketplace

Sarah BauderThe Alecxih Group

Agenda01

National Landscape: Impacts on Financing Education

02The Angst of the Middle Class

03Financial Aid Behavioral Loan Default Study

04Student Success Initiatives and Best Practices

NATIONAL LANDSCAPE

3

Future of

Higher

Education?

ChangingEconomics

ChangingTechnology

Changing Demography

Changing Perceptions and Expectations

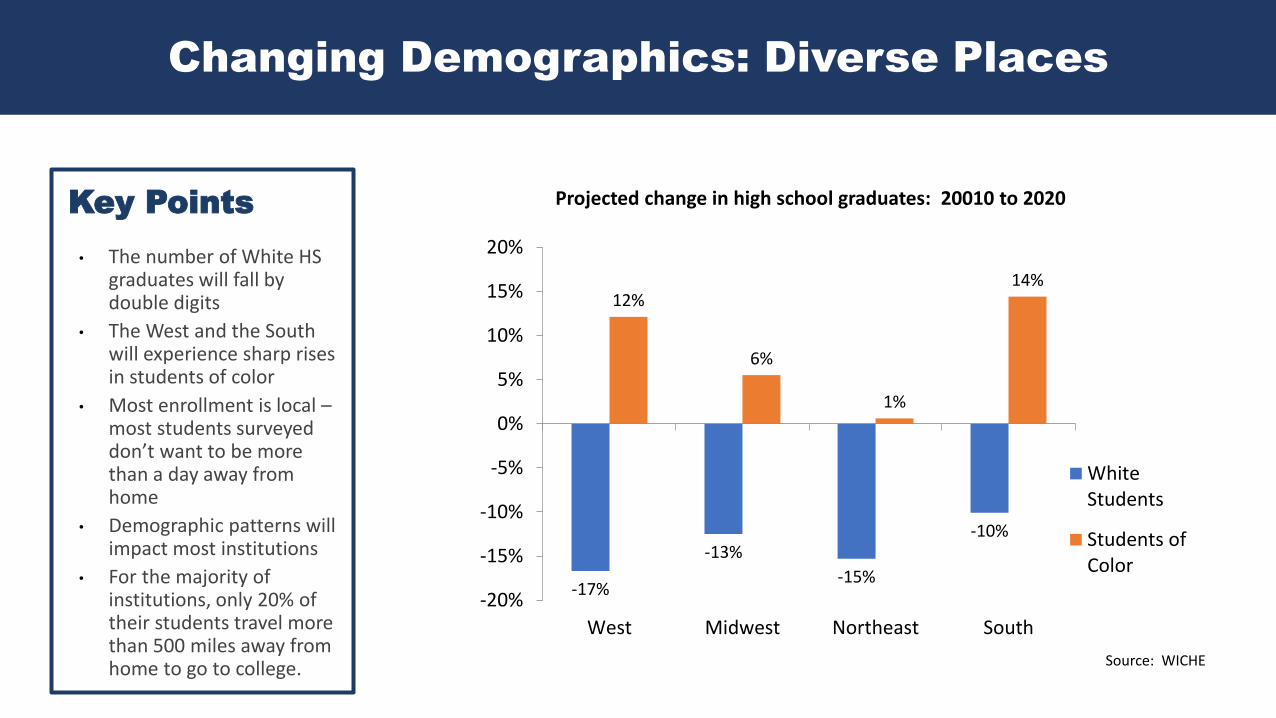

-17%

-13%

-15%

-10%

12%

6%

1%

14%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

West Midwest Northeast South

Projected change in high school graduates: 20010 to 2020

WhiteStudents

Students ofColor

Source: WICHE

Key Points

• The number of White HS graduates will fall by double digits

• The West and the South will experience sharp rises in students of color

• Most enrollment is local –most students surveyed don’t want to be more than a day away from home

• Demographic patterns will impact most institutions

• For the majority of institutions, only 20% of their students travel more than 500 miles away from home to go to college.

Changing Demographics: Diverse Places

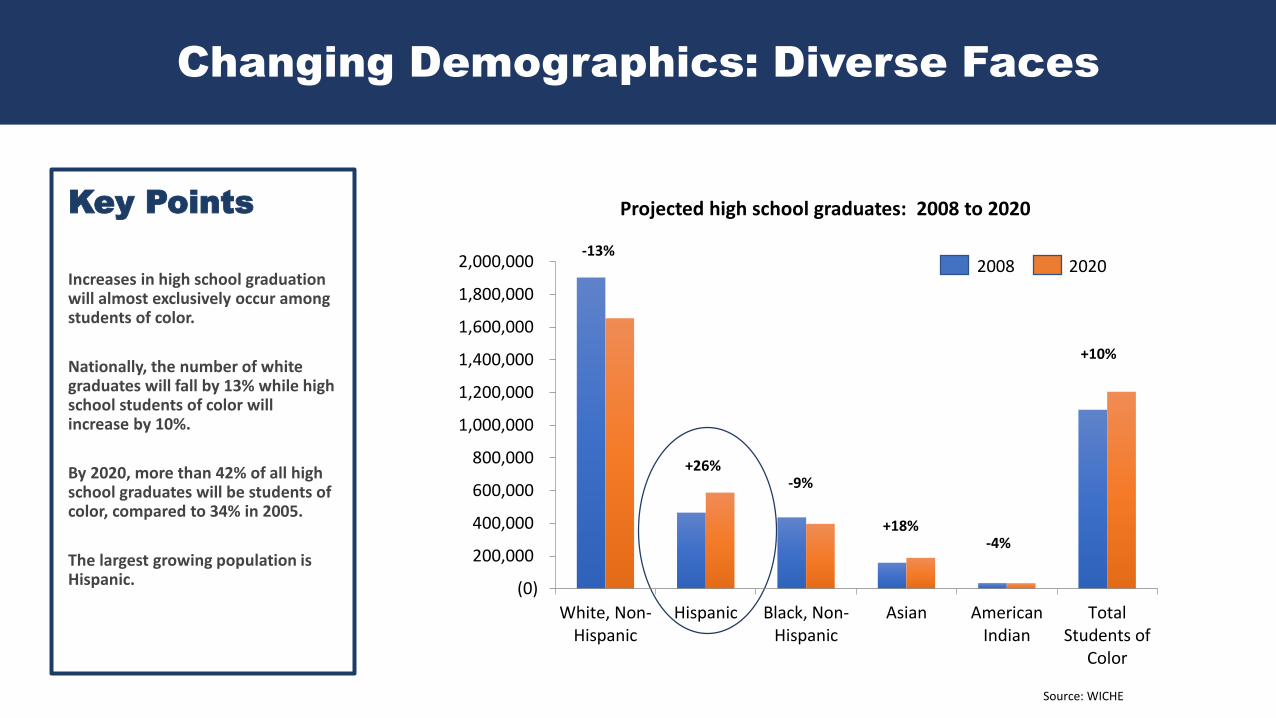

(0)

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

White, Non-Hispanic

Hispanic Black, Non-Hispanic

Asian AmericanIndian

TotalStudents of

Color

Projected high school graduates: 2008 to 2020

-13%

+26%-9%

+18%-4%

+10%

2008 2020

Source: WICHE

Changing Demographics: Diverse Faces

Key Points

Increases in high school graduation will almost exclusively occur among students of color.

Nationally, the number of white graduates will fall by 13% while high school students of color will increase by 10%.

By 2020, more than 42% of all high school graduates will be students of color, compared to 34% in 2005.

The largest growing population is Hispanic.

Source: WICHE

Bienvenido al Futuro de los Estados Unidos

Key Points

There are 50 million people of Hispanic descent in the US today; nearly equal to the sum total of the nation’s black and Asian populations which totals 53 million.

The number of Hispanics in the US alone rose by 43 percent between 2000 and 2010.

Only 8 states experienced growth of less than 40 percent in their Hispanic population between 2000-2010 and 12 states experiences 90 percent or more.

63% were born in the US.

67% attend non-selective colleges with low graduation rates.

Sources: Breakpoint; Georgetown Center on Education and the Workforce

Latino completion rates for bachelor’s and associate’s degrees lag behind Whites, but Latino’s have higher certificate completion rates.

Source: WICHE

Latino first-time enrollees at two and four year colleges increased while white enrollment decreased.

Key Points

• The rapid advancement of technology is

linked to and mirrors human knowledge

growth, creating a society in which

transformational new technology is

introduced frequently- expect change

• Ubiquitous hardware, artificial

intelligence, digitization of data, advanced

robotics, deep learning, and the internet

of things are fundamentally transforming

how Americans live, learn, and work and

majors on campuses

• In previous eras, moderate to highly

skilled workers would have to learn new

technology two or three times over the

course of their lifetime. Today,

transformational new technologies are

appearing at an increasing pace,

outdating former technology as quickly as

three to five years.

Changing Technology

7

14501400 1500 1550 1600 1650 1700 1750 1800 1850 1900 1950 2000 2050

Printing Press Telescope Steam Engine

Telegraph

Lightbulb

Telephone

Car

Man on the moon

Microprocessor

WWW

iPhone

Internet of Things

Advanced Robotics

3D Organ Printing

Self-Aware AI

Ac

ce

lera

tin

g G

row

th i

n T

ech

no

log

y

Source: INED + Entangled analysis

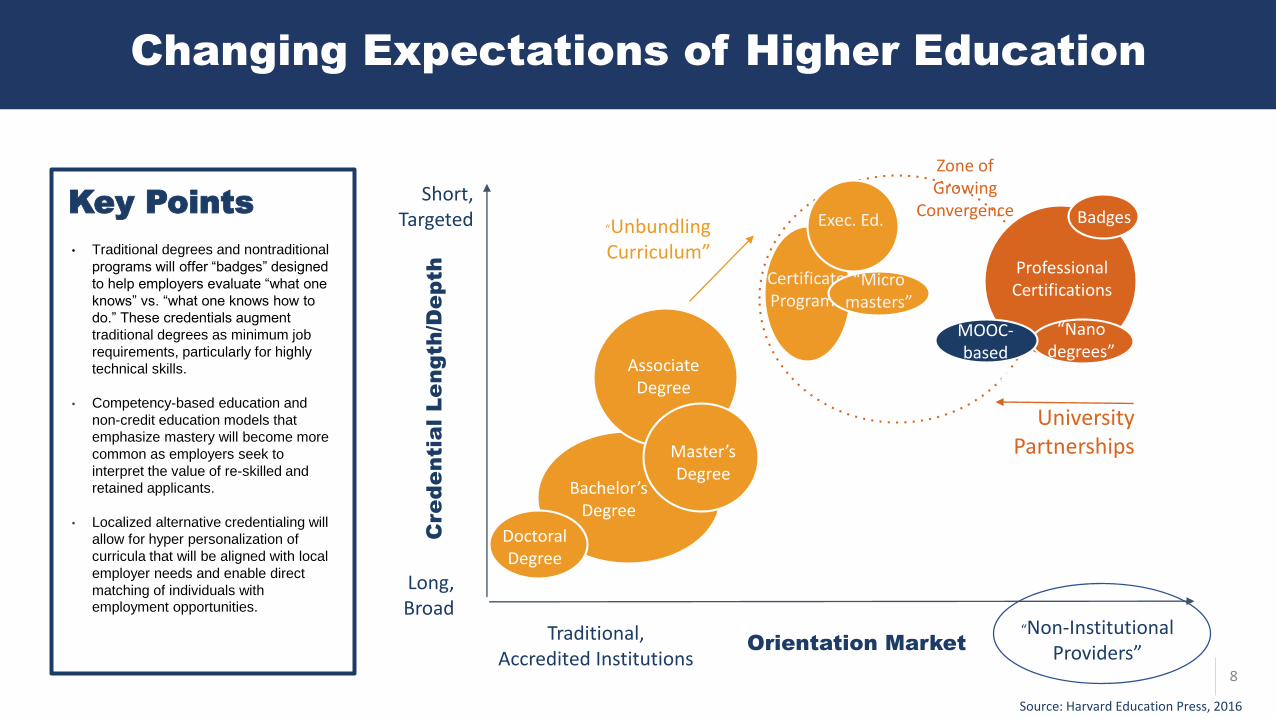

Changing Expectations of Higher Education

8

Key Points

• Traditional degrees and nontraditional

programs will offer “badges” designed

to help employers evaluate “what one

knows” vs. “what one knows how to

do.” These credentials augment

traditional degrees as minimum job

requirements, particularly for highly

technical skills.

• Competency-based education and

non-credit education models that

emphasize mastery will become more

common as employers seek to

interpret the value of re-skilled and

retained applicants.

• Localized alternative credentialing will

allow for hyper personalization of

curricula that will be aligned with local

employer needs and enable direct

matching of individuals with employment opportunities.

Source: Harvard Education Press, 2016

Cre

de

nti

al

Le

ng

th/D

ep

th

Short, Targeted

Long, Broad

Orientation Market“Non-Institutional

Providers”Traditional,

Accredited Institutions

Zone of Growing

Convergence

University Partnerships

“Unbundling Curriculum”

Certificate Programs

Exec. Ed.

Professional Certifications

Badges

“Nanodegrees”

MOOC-based

certificates

“Micromasters”

Associate Degree

Master’s Degree

Bachelor’sDegree

DoctoralDegree

U.S. Companies Spent $9.7 Billion in 2017 for Training or Upskilling Employees!

Source: Training Magazine

Skills most needed for the future: • Critical Thinking• Complex Problem Solving• Leadership• Emotional Intelligence• Teamwork/Collaboration

Source: World Economic Forum

Globalization has increased workforce diversity. Economic pressures have resulted in workers remaining in the labor force longer than previous generations.

Source: World Economic Forum

Changing Partnerships and Collaboration

By 2024, 25 percent of the workforce is projected to be age 55 or older. Older workers are expected to be disproportionately affected by the effects of automation, needing more training.

Source: Entangled Solutions

Millennials will soon represent more than half the workforce, drastically shifting workplace culture and expectations.

Source: Gallup

The Angst of the Middle Class

Changing Economics

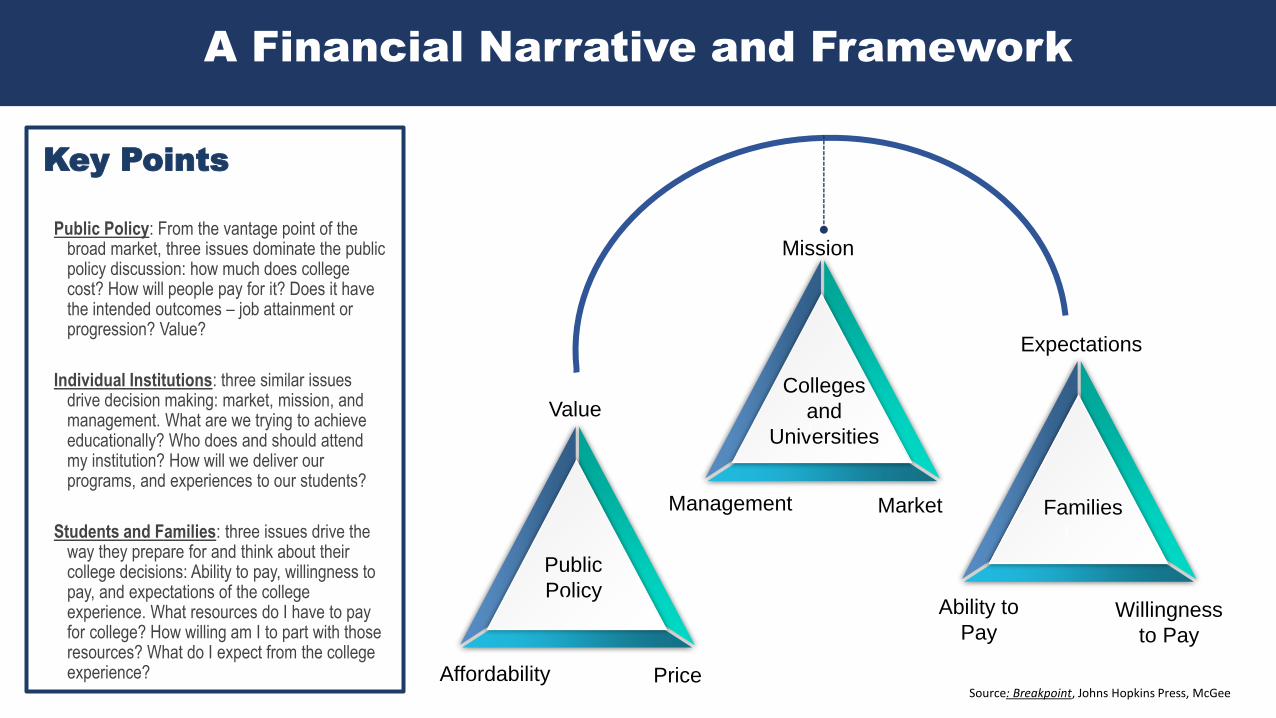

Key Points

Public Policy: From the vantage point of the broad market, three issues dominate the public policy discussion: how much does college cost? How will people pay for it? Does it have the intended outcomes – job attainment or progression? Value?

Individual Institutions: three similar issues drive decision making: market, mission, and management. What are we trying to achieve educationally? Who does and should attend my institution? How will we deliver our programs, and experiences to our students?

Students and Families: three issues drive the way they prepare for and think about their college decisions: Ability to pay, willingness to pay, and expectations of the college experience. What resources do I have to pay for college? How willing am I to part with those resources? What do I expect from the college experience?

Source: Breakpoint, Johns Hopkins Press, McGee

A Financial Narrative and Framework

Public

Policy

Affordability Price

ValueColleges

and

Universities

Management Market

Mission

Families

Ability to

PayWillingness

to Pay

Expectations

77%

35%

7%

11%

38%

48%

0%

20%

40%

60%

80%

100%

Struggling a Lot Struggling a Little Not Struggling

How worried are you that you will havetrouble paying for your children’s college education?

Not Worried At All

Not Too Worried

Somewhat Worried

Very Worried

Source: Public Agenda, 2011

Anxiety Heavy

Key Points

4 in 10 Americans identified themselves as “struggling a lot”

42% said they were “struggling a little”. Only 17% said they weren’t struggling at all

4 in 10 Americans said they were very worried or somewhat worried about losing their job in the next year

In total, nearly 80% of all parents said they were worried that they would have trouble paying for their children’s college education

Pew Report shows that 75% of

Americans believe college is

unaffordable

$-

$20,000

$40,000

$60,000

$80,000

$100,000

White, Non-Hispanic

Black Asian Hispanic

Median Family Income, 2017

All Families with School-Age Children

Married Couple Families with School-Age Children

37%

88%

46%

63%

0% 20% 40% 60% 80% 100%

Hispanic

Asian

Black

White, Non-Hispanic

% 19 Year Olds Enrolled in College

Source: US Census Bureau

Changing Economics

Key Points

There are enormous differences in family incomes by race and ethnicity, differences that influence opportunity.

The financial aid challenges are immediately apparent.

Family structure matters: for each group, married couple families with children have substantially higher incomes than the incomes for all families with school age children.

Higher Education will face enormous enrollment challenges in this new era of changing demography and economics.

Source: https://nces.ed.gov/pubs2017/2017051.pdf

0%

20%

40%

60%

80%

100%

120%

140%

Lowest 20% SecondQuintile

ThirdQuintile

FourthQuintile

Top 20% Top 5%

2012-2013 Tuition, Fees, Room, and Board as % of mean family income by quintile

Private Four-Year Colleges

Public Four-Year Colleges

Source: US Census Bureau, College Board. Percentages displayed reflect average price as a percent of the mean of each income quintile..

Who Needs Financial Aid, Anyway?

Key Points

• According to Pew Research, only 53% of families with children have saved anything for their kids college

• 46% say they haven’t saved enough.

• We have an efficacy problem with needs analysis and college costs as income rises into and through the middle class

Source: https://trends.collegeboard.org/sites/default/files/2017-trends-in-college-pricing_0.pdf

Average Net Price by Family Income

Key Points

• Students who are financial aid recipients with family incomes below $48,001 received enough grant aid on average to cover tuition and fees with funds left over for expenses.

• Middle income families between $48,001 and $110,000 had to pay on average $5,800 to cover just tuition and fees.

• On average tuition and fees comprises 39% of an institutional cost of attendance.

16

● 39% of Black borrowers drop out of college,

compared to 29% of white borrowers.

● 38% of low-income borrowers drop out

compared to less than a quarter of their higher-

income peers.

● 30% of all students who began their

postsecondary education in 2011-2012, left

without a credential within 3 years. 40% of

African Americans, 32% of Hispanic students and

38% of low-income students had left.

● 50% of students who drop out come from

families that earn less than $35,000.

● Between 10% and 35% of students who drop out

owe $1500 or less and are in good academic

standing.

Finances Impacts Student Success and Diversity Initiatives

Source: BPS 04/09 Beginning Postsecondary Longitudinal Landscape 2011-12 National Postsecondary Student Aid Study (NPSAS: 12)

Less than $1500More than $1500

% of stopouts with $1,500 or more of unmet financial need.

% of 1st time student stopouts who reported a financial reason for doing so.

https://nces.ed.gov/pubs2017/2017051.pdf

Completion is the New Normal for Student Success

Key Points

Increases in salary were evident in all races as education attainment increases.

Black and Hispanics earn less than Asian or White counterparts, with Asian having the most earning power.

Financial Aid Longitudinal Study

1999-2011

University of Maryland

Method and Purpose

• All Undergraduate degree seeking students who borrowed any federal loan in the years 1999-2009

• Matched that data to institutional campus data by department – bursar, registrar, development, athletics

• Matched that report to NSLDS to all students who defaulted on a federal loan from 1999-2013

• Determine indices related to default

• Define the academic, demographic, and financial characteristics of students who default

• Identify which characteristics are highly associated with defaults

• Examine graduation with characteristics of default

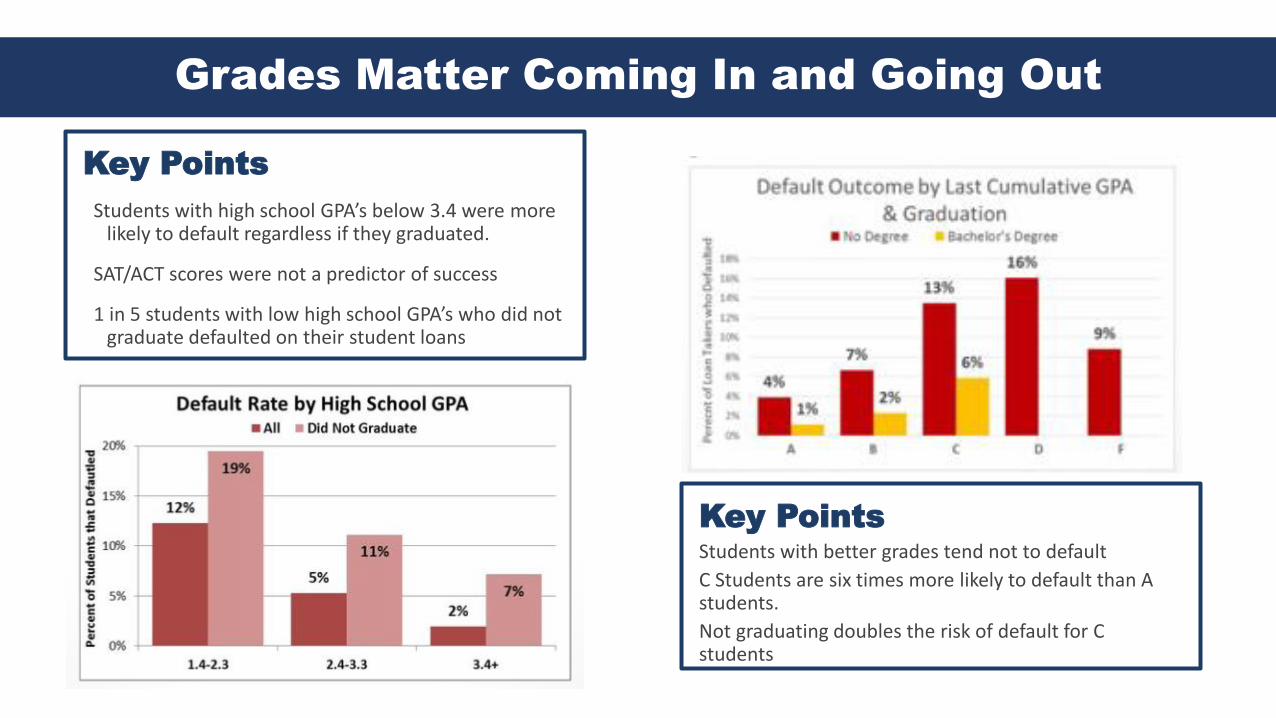

Key PointsStudents with better grades tend not to default

C Students are six times more likely to default than A students.

Not graduating doubles the risk of default for C students

Key Points

Students with high school GPA’s below 3.4 were more likely to default regardless if they graduated.

SAT/ACT scores were not a predictor of success

1 in 5 students with low high school GPA’s who did not graduate defaulted on their student loans

Grades Matter Coming In and Going Out

Key Points

Students enrolled in 13+ terms were more likely to default regardless of their graduation outcome.

Those that did not graduate were almost three times more likely to default than those that did graduate.

Key PointsIn general, students with high loan amounts, have a higher risk of default.

For students who graduated, the risk of default did not increase until the student’s total loan amount exceeded $20,000.

Students who do not graduate and have over $20K in loans have a 3.6x greater risk of default

Time to Degree Matters

Key Points

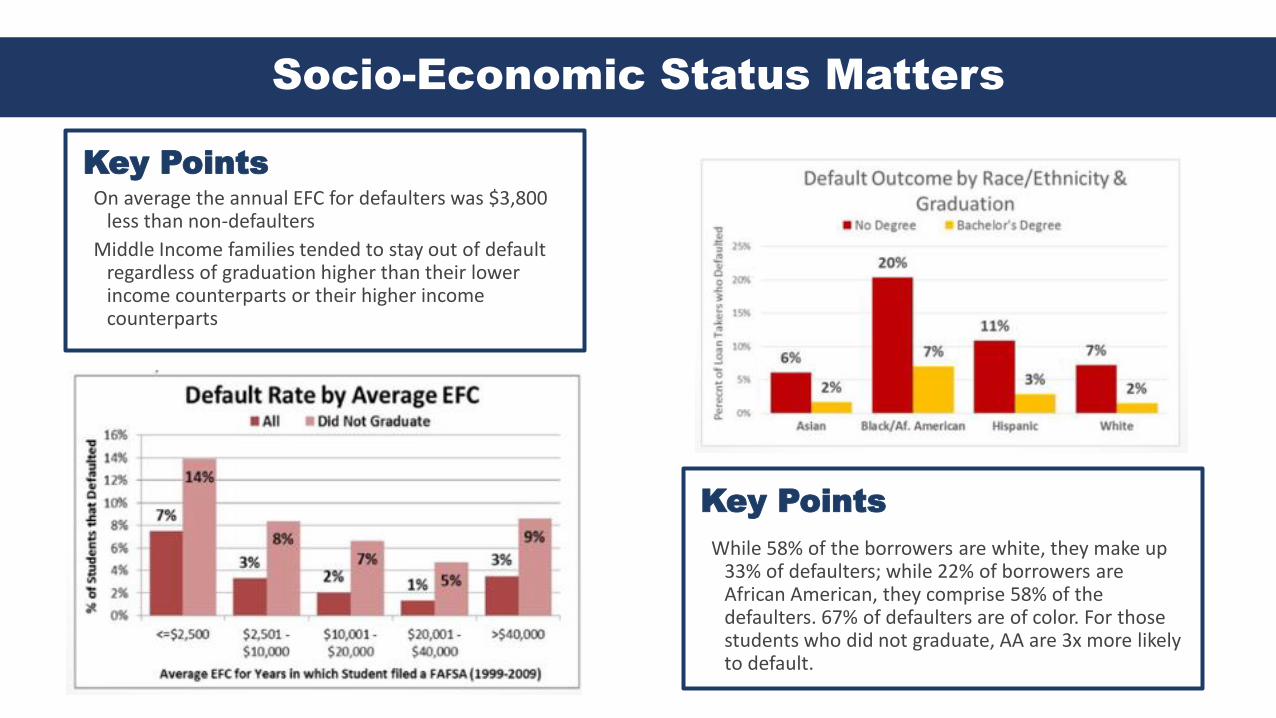

While 58% of the borrowers are white, they make up 33% of defaulters; while 22% of borrowers are African American, they comprise 58% of the defaulters. 67% of defaulters are of color. For those students who did not graduate, AA are 3x more likely to default.

Key PointsOn average the annual EFC for defaulters was $3,800

less than non-defaulters

Middle Income families tended to stay out of default regardless of graduation higher than their lower income counterparts or their higher income counterparts

Socio-Economic Status Matters

Key Points

Students in undeclared majors had a higher percentage of defaults regardless of graduation

Students who declared a major after the three semester defaulted at a rate 5 times their peers

Students in Science, Math, Computer Science, Engineering, Business, Journalism and Architecture had negligible default rates if the student graduated. And similar default rates if they didn’t graduate

Side note: This information is important for institutions interested in Income Share Agreement Programs

Major Matters

Take Aways

• Among student who default, 57% do so within the first five years.

• Student who do not graduate have default rates 4 times higher than those that do graduate

• Males have a slightly higher risk of default

• Failure to graduate increases risk of default among males but not females

• 15% of loan borrowers were independent students; these students had 2.3 times higher default rates than

dependent students

• Transfer students had default rate doubled that of first time enrollees regardless if they graduated

• Instate and out of state students had very similar default rates unless they did not graduate. Then out of

state student’s default rate was four percentage points higher.

STUDENT AFFAIRS

.

. REGISTRAR

FINANCIAL AIDINFORMATION TECHNOLOGY

DEANS AND COLLEGESBURSAR

Data Collection and Student Behaviors

Incomplete gradesLate fines

Parking feesQualitative Survey Data

Assignments

Stopped outCan’t enroll next semester

Owes Money after drop/add

Small Sample of Information Gathered

Date Registered for Classes

Repeated Classes

Changed majors (how many times)

Study Abroad

Dates of applications

What We Learned

Did Not Graduate

• Declared major after third semester• More than six procrastination indicators in any one

semester

• HS GPA below 3.2 unweighted (SAT has no significance)• Single parent household• Part Time• Transfer• More than 13 semesters• African American male• Worked off campus• Off campus housing first two years• No Study Abroad• Repeated Introductory Math and/or English• Owed $; Academically qualified

Graduated

• Declared major at orientation or before third semester

• Less than 3 procrastination indicators in any one semester

• Full time over 15 credits continuously• Graduated before 12th semester• Studied Abroad in sophomore and/or junior year• Worked on campus or only over breaks • On campus housing first two years• Asked for help: tutoring; mentor; • Appealed for additional funding – emergency aid

BLACK MALE INITIATIVE

8% RULE LOAN REPORT

SENIOR DEBT CAP PROGRAM

FEDERAL WORK STUDY PROGRAM

ADJUSTED PACKAGING STRATEGIES AND AWARD LETTERS

Student Success Initiatives

TEAMED WITH BURSAR ON DELINQUENT REPORTS

STUDY ABROAD FOR LOW-INCOME STUDENTS

29

KEY POINTS

• High ROI; small dollars

• Improves Collaboration Across Divisions

• Promotes Donor Support – Real-time Impact on Funds

• Teaches Data Mining and Predictive Analytic Skills

• Creates an Environment for Innovation

• Paves the Path for more Impactful Programs

Emergency Aid Team

Shared Data

Shared Policies

Shared Technology

Shared Resources

Aid / Crisis

Coordinator

Coordination

Technology

Emergency Aid