The Peak in World Oil Supply

Dr. Peter R. A. Wells

September 2008

AcknowledgementsAcknowledgements• Data Sources

– IHS – crude oil field data (except USA)– International Oil Scouts Association (USA)– Our own database and analyses for oil fields (Iran, Iraq,

Saudi Arabia)– IEA, EIA, BP, UK DTI, NPD, government agencies in

Australia, Canada, USA (MMS, states of California, Oklahoma, Texas, Ohio, Louisiana etc)

– Permission to publish analysis derived from the IHS database

© Peter R.A. Wells

North America

South & Central America

Europe and Eurasia

Middle East

AfricaAsia Pacific

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030

000

b/d

EIA 2007 Reference CaseCERA 2006 Asian PhoenixIEA 2006 Alternative Policy ScenarioIEA 2006 Deferred Investment CaseIEA 2007 Reference Case

Is growth in oil consumption sustainable?Is growth in oil consumption sustainable?

Data from BP Statistical Review of World Energy, EIA, IEA and CERA

© Peter R.A. Wells

0

5

10

15

20

25

30

0 200 400 600 800 1,000 1,200 1,400 1,600Population, millions

Per C

apita

Oil

Con

sum

tion,

b/y

Are Asian aspirations realisable?Are Asian aspirations realisable?

USA

W EurJapanS Korea

FSU

Sub Saharan Africa

India China

?

Data from BP Statistical Review of World Energy and UN

© Peter R.A. Wells

What do we mean by What do we mean by ““OilOil”” or or ““liquidsliquids””??• Crude oil including condensate produced with crude oil at the

separator

• Natural gas liquids (NGLs): natural gas plant liquids (NGPLs) produced from associated and non-associated gas fields and condensate produced from non-associated gas fields

• Tar sands: Syncrude/bitumen extracted from tar sands

• GTL and CTL: Liquids produced in gas-to-liquids and coal-to-liquids plants

• Liquid biofuels: ethanol, biodiesel etc.

• Shale oil: oil extracted from oil shale

• Other hydrocarbon liquids: orimulsion, MTBE etc.

• Refinery Gains: Net liquid gains in refining crude oil due mainly to hydrogenation

© Peter R.A. Wells

Components of supplyComponents of supply

Crude Oil

NGLs

Biofuels

Canadian Tar sands

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

80,000,000

90,000,000

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

b/d

Historical production data from our own database derived from EIA, IEA, BP Statistical Review of World Energy and national publicly available databases

1.0%1.6%

11.4%

86.0%

© Peter R.A. Wells

USA

Rest of Non-OPEC

FSU

OPEC

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

80,000,000

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

b/d

Components of crude oilComponents of crude oil

42.8%

16.2%

33.9%

7.1%

Historical production data from our own database derived from EIA, IEA, BP Statistical Review of World Energy and national publicly available databases

© Peter R.A. Wells

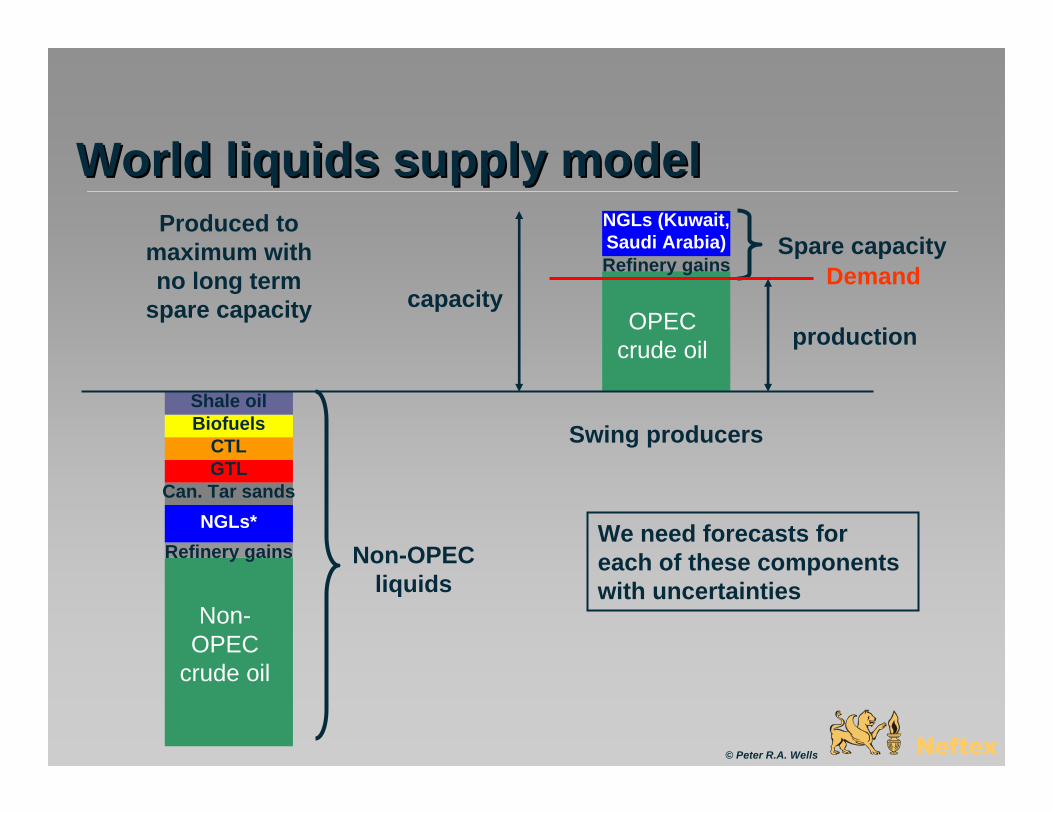

World liquids supply modelWorld liquids supply model

Non-OPEC

crude oil

Refinery gainsNGLs*

Can. Tar sands

Shale oilBiofuels

GTLCTL

OPEC crude oil

NGLs (Kuwait, Saudi Arabia)Refinery gains

Produced to maximum with no long term

spare capacity

Non-OPEC liquids

Spare capacity

Swing producers

Demandcapacity

production

© Peter R.A. Wells

We need forecasts for each of these components with uncertainties

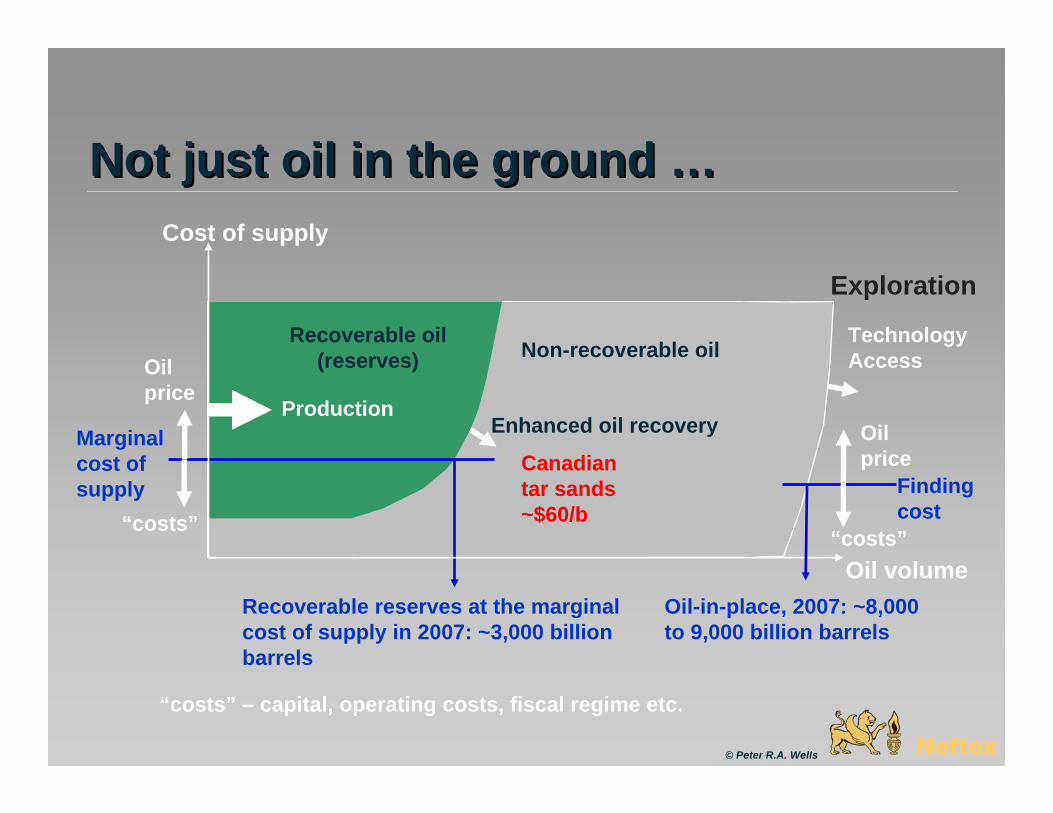

Not just oil in the ground Not just oil in the ground ……

Recoverable oil (reserves) Non-recoverable oil

Exploration

Oil price

Enhanced oil recoveryMarginal cost of supply

Recoverable reserves at the marginal cost of supply in 2007: ~3,000 billion barrels

Oil-in-place, 2007: ~8,000 to 9,000 billion barrels

Cost of supply

Oil volume

Production

Finding cost

Oil price

Technology Access

Canadian tar sands ~$60/b“costs”

“costs”

© Peter R.A. Wells

“costs” – capital, operating costs, fiscal regime etc.

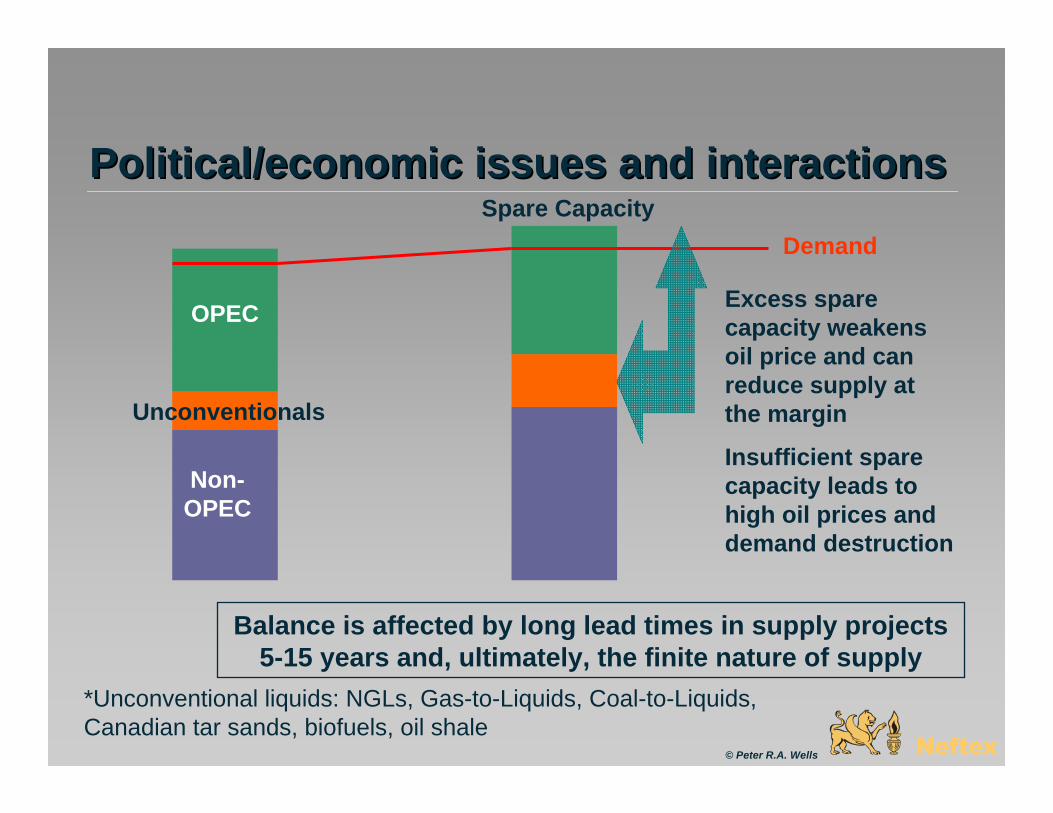

Political/economic issues and interactionsPolitical/economic issues and interactions

Non-OPEC

OPEC

Unconventionals

*Unconventional liquids: NGLs, Gas-to-Liquids, Coal-to-Liquids, Canadian tar sands, biofuels, oil shale

Spare CapacityDemand

Excess spare capacity weakens oil price and can reduce supply at the margin

Insufficient spare capacity leads to high oil prices and demand destruction

© Peter R.A. Wells

Balance is affected by long lead times in supply projects 5-15 years and, ultimately, the finite nature of supply

Spare capacity and oil priceSpare capacity and oil price

0

10

20

30

40

50

60

70

80

90

100

1970 1975 1980 1985 1990 1995 2000 2005

Rea

l oil

pric

e (2

007)

, $/b

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

spar

e ca

paci

ty, b

/d

Price floor set by the needs of the Saudi Arabian budget

Oil price Spare Capacity

Spare capacity from IMF, PIW, OPEC

Oil price from BP

© Peter R.A. Wells

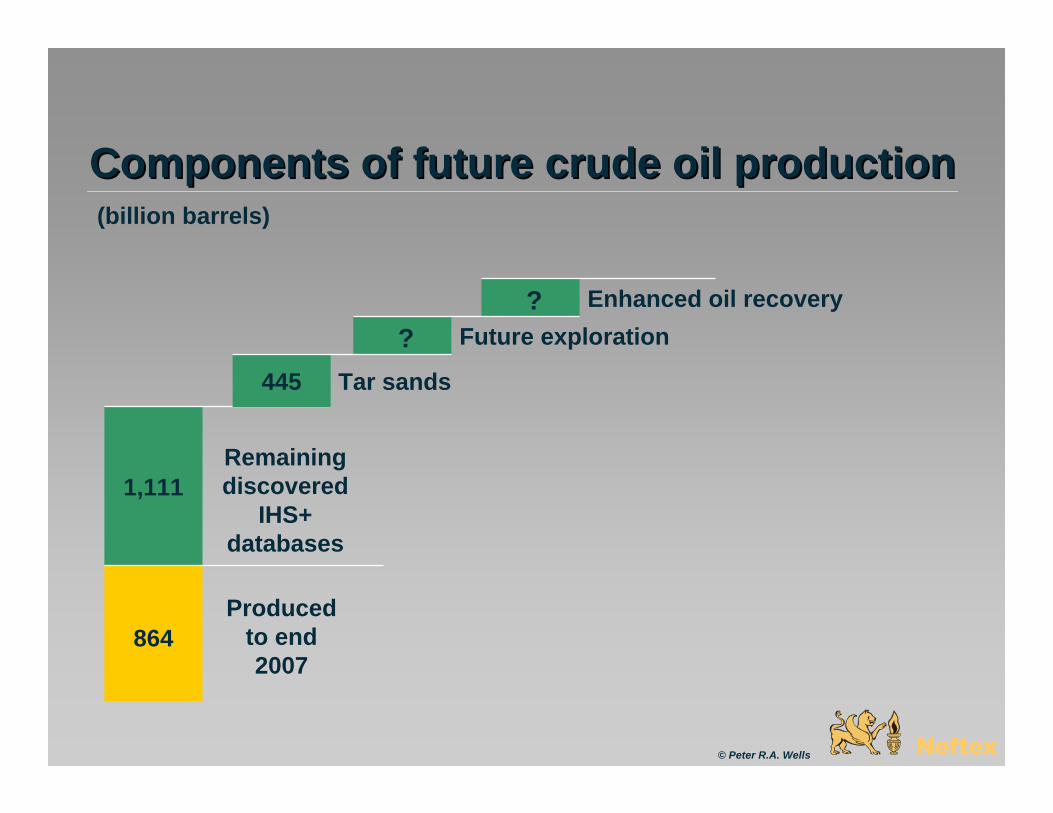

Components of future crude oil productionComponents of future crude oil production

© Peter R.A. Wells

??

864

1,111

(billion barrels)

Produced to end 2007

Remaining discovered

IHS+ databases

Future explorationEnhanced oil recovery

Tar sands445

Future Exploration SuccessFuture Exploration Success

© Peter R.A. Wells

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

USGS CERA Neftex

billi

on b

arre

ls

mean

mean

P5

P95

P95

P5

USGS/CERA 3 x Saudi Arabia?? 45% of past discoveries?? 150 years to 2,000 bln b, but only 30 years to 900 billion b?? Requires discovery rate of 36 blnb/year – Only achieved 12 blnb/year between 1995 and 2007

Neftex1 x Saudi Arabia 15% of past discoveries Requires discovery rate of 13 blnb/year (2008 to 2020) declining to 5 bln b/year in 2030

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

1850 1870 1890 1910 1930 1950 1970 1990 2010 2030 2050

mill

ion

barr

els

OPECFSURest of non-OPEC less FSUUSA

Future exploration success Future exploration success -- based on based on USGS/CERA viewUSGS/CERA view

Raw field reserves data and exploration success history for OPEC, FSU and rest of non-OPEC from IHS and for USA from the International Oil Scouts Association

Forecast exploration success from our Monte Carlo simulator

USGS 2000

© Peter R.A. Wells

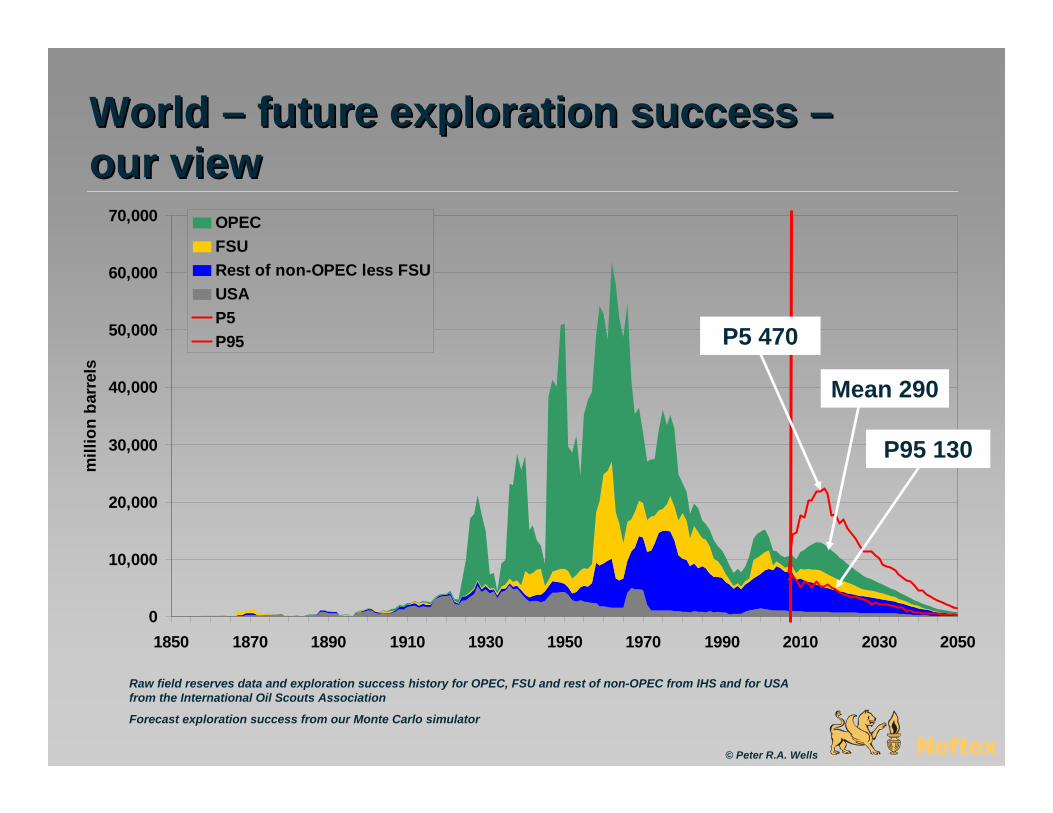

World World –– future exploration success future exploration success ––our viewour view

Raw field reserves data and exploration success history for OPEC, FSU and rest of non-OPEC from IHS and for USA from the International Oil Scouts Association

Forecast exploration success from our Monte Carlo simulator

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

1850 1870 1890 1910 1930 1950 1970 1990 2010 2030 2050

mill

ion

barr

els

OPECFSURest of non-OPEC less FSUUSAP5P95

© Peter R.A. Wells

P5 470

Mean 290

P95 130

Improved Oil Recovery (IOR)Improved Oil Recovery (IOR)

© Peter R.A. Wells

production

time

production

time

Oil pulled forward from the tail – “accelerated” no

reserves added

Additional reserves extracted

Enhanced Oil Recovery

“Field Upgrades”

Technologies:

Miscible non hydrocarbon gas (CO2, N2) floods, thermal, chemical

Technologies:

Horizontal wells, multilateral wells, MRC wells, smart wells, smart fields, gas lift, pumps, fracturing

AIM is to recover more of the oil profitably - MAY increase reserves

AIM is to raise and extend production BY increasing reserves

Major New Technologies take timeMajor New Technologies take time

• Horizontal wells were first drilled in 1929

• Early 1980s, USSR developed drilling technologies for long radius wells making them widely applicable

• In 2000, 24,000 horizontal wells were drilled

• Technology took ~15-20 years to become widespread

• If it is not under development today, it will not have much impact until after 2025

© Peter R.A. Wells

USA experience with Enhanced Oil USA experience with Enhanced Oil Recovery (EOR)Recovery (EOR)

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006

b/d

Thermal (steam injection)

Miscible non-hydrocarbon gas injection

(CO2, N2 injection)

Chemical floods

© Peter R.A. Wells

USA experience of EOR USA experience of EOR –– specific to field, specific to field, reservoir, oil type, locationreservoir, oil type, location

• Thermal/Steam: Heavy oils in good reservoirs above 900 metres depth – thermal methods such as steam injection can increase reserves considerably (add up to 40% of OIIP to recovery) (California, Oman, some Persian Gulf fields, Venezuela (not tar sands))

• CO2: Light to medium oils in poor reservoirs (few fractures) –miscible non-hydrocarbon gas injection (CO2, N2) can add 8-17% of OIIP to recovery to reserves (Permian Basin USA, some Persian Gulf oil fields)

• No Gains: Light-medium oils in good quality reservoirs achieve high recovery rates (>65%) from water or hydrocarbon gas injection – EOR cannot add much to recovery and reserves (North Sea, West African and Gulf of Mexico fields)

© Peter R.A. Wells

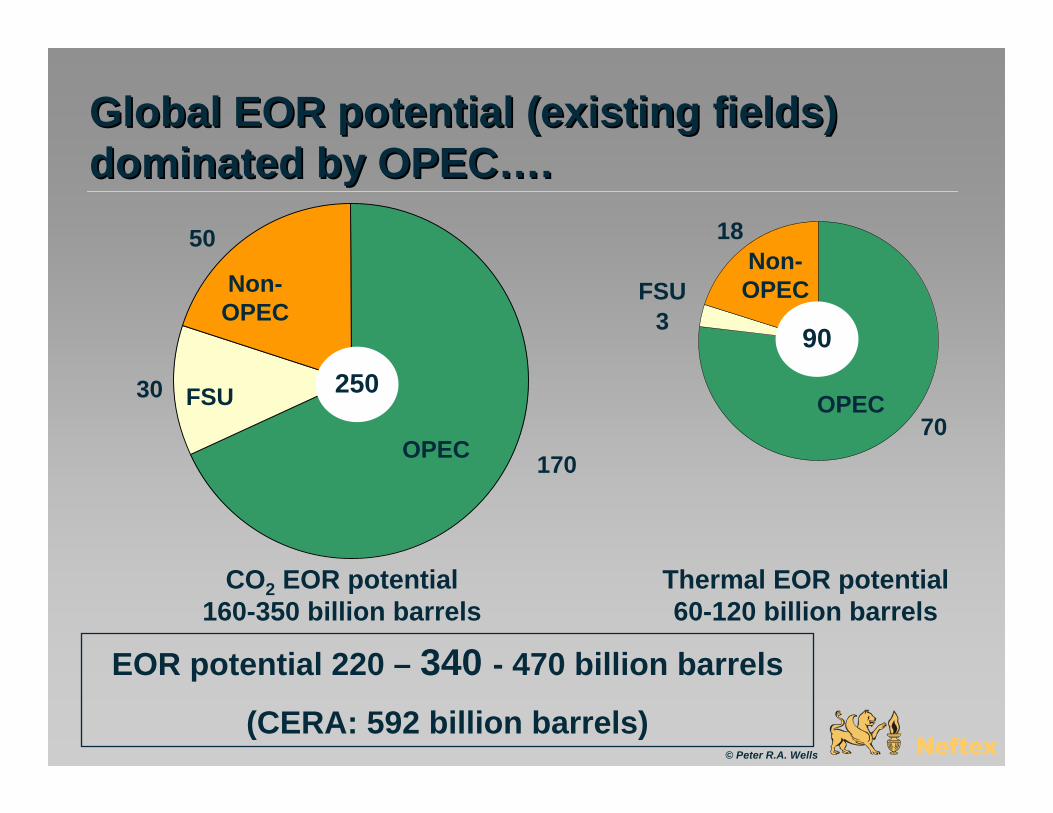

Global EOR potential (existing fields) Global EOR potential (existing fields) dominated by OPECdominated by OPEC……..

70

18

3

OPEC

Non-OPEC

FSU OPEC

Non-OPECFSU

CO2 EOR potential 160-350 billion barrels

Thermal EOR potential 60-120 billion barrels

170

30

50

EOR potential 220 – 340 - 470 billion barrels

(CERA: 592 billion barrels)

25090

© Peter R.A. Wells

World (potential) crude oil volumesWorld (potential) crude oil volumes……. .

© Peter R.A. Wells

290340

864

1,111

(billion barrels)

Produced to end 2007

Remaining discovered

IHS+ databases

Future explorationEnhanced oil recovery

Tar sands445

130-470220-470

3,050TOTAL conventional

crude oil, 2,600

Simulation Model approach to crude oil Simulation Model approach to crude oil forecasting forecasting

• If a field has not been discovered it cannot be produced or enhanced – model starts with the discovery history (proven + probable (2P) reserves and date of discovery)

• Model is built up using individual fields –– Real discovered fields in the IHS or other databases

discovered to the end of 2007 (10s of thousands)– Modelled yet-to-be-discovered fields based on

forecast exploration success after 2007 (10s of thousands)

• Preserves the granularity of individual oil fields throughout the forecast and continuity of methodology

© Peter R.A. Wells

Simulation Model approach to crude Simulation Model approach to crude oil forecasting oil forecasting

© Peter R.A. Wells

Past discoveries Future

discoveries

Country Field Date discovery 2P reserves A 1 1890 500 B 2 1910 45 …… ….. …… ……

Country Field Date discovery 2P reserves A 1 2008 900 B 2 2009 320 …… ….. …… ……

Field size

time

Probability distributions for

time between discovery and

production

time

Probability distributions for

shape of production

profile

Field size

+ + + +

+ …..10s of thousands of fields0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

45,000,000

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

b/d

Simulation Model approach to crude oil Simulation Model approach to crude oil forecasting forecasting

• A simulation model provides a direct link between exploration success/Enhanced Oil Recovery (EOR) and production on the scale of individual oil fields

• Uncertainties in input are properly carried through and expressed as uncertainties in the forecast

• If a calibrated simulation model can replicate historical production closely then we can have confidence in its forecasts (history match)

• To test the model, we have history matched:– USA– Non OPEC less USA, less FSU (ROW)– FSU

© Peter R.A. Wells

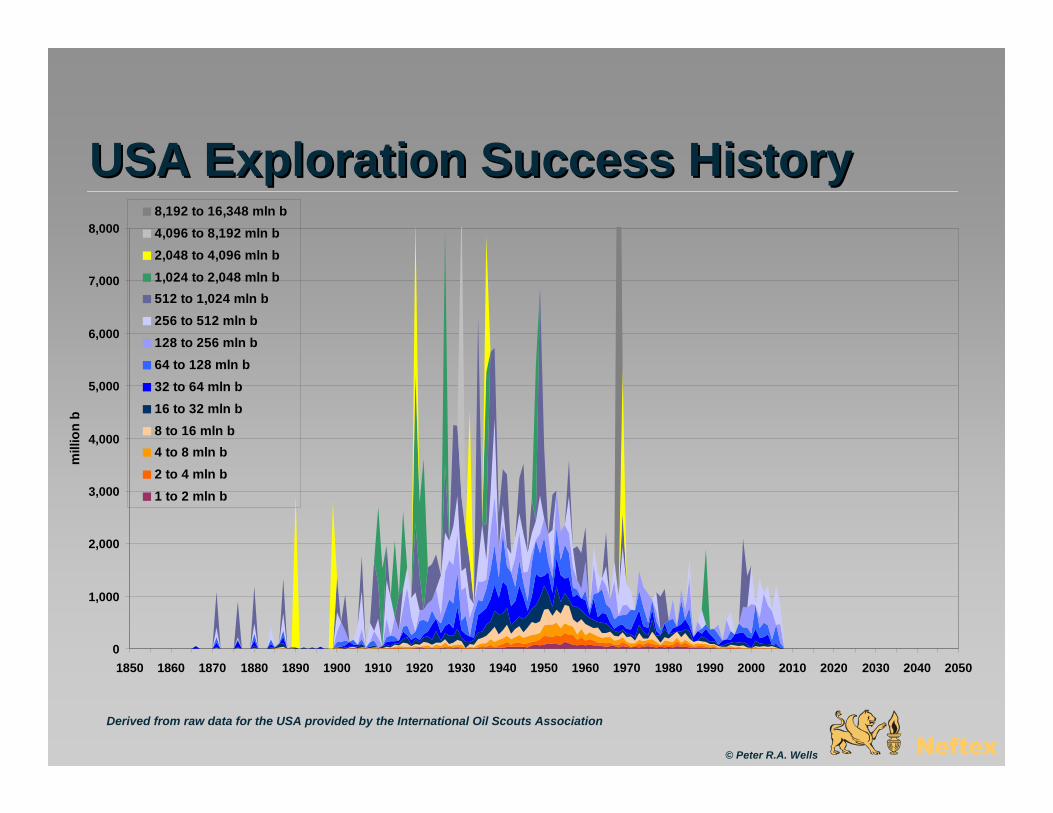

USA Exploration Success HistoryUSA Exploration Success History

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1850 1860 1870 1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

mill

ion

b

8,192 to 16,348 mln b4,096 to 8,192 mln b2,048 to 4,096 mln b1,024 to 2,048 mln b512 to 1,024 mln b256 to 512 mln b128 to 256 mln b64 to 128 mln b32 to 64 mln b16 to 32 mln b8 to 16 mln b4 to 8 mln b2 to 4 mln b1 to 2 mln b

Derived from raw data for the USA provided by the International Oil Scouts Association

© Peter R.A. Wells

History matching History matching -- USAUSA

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

10,000,000

1850 1860 1870 1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

b/d

1 to 2 mln b2 to 4 mln b4 to 8 mln b8 to 16 mln b16 to 32 mln b32 to 64 mln b64 to 128 mln b128 to 256 mln b256 to 512 mln b512 to 1,024 mln b1,024 to 2,048 mln b2,048 to 4,096 mln b4,096 to 8,192 mln b8,192 to 16,348 mln bUSA crude oil production

Derived from raw data for the USA provided by the International Oil Scouts Association

Actual production profile from our own database

© Peter R.A. Wells

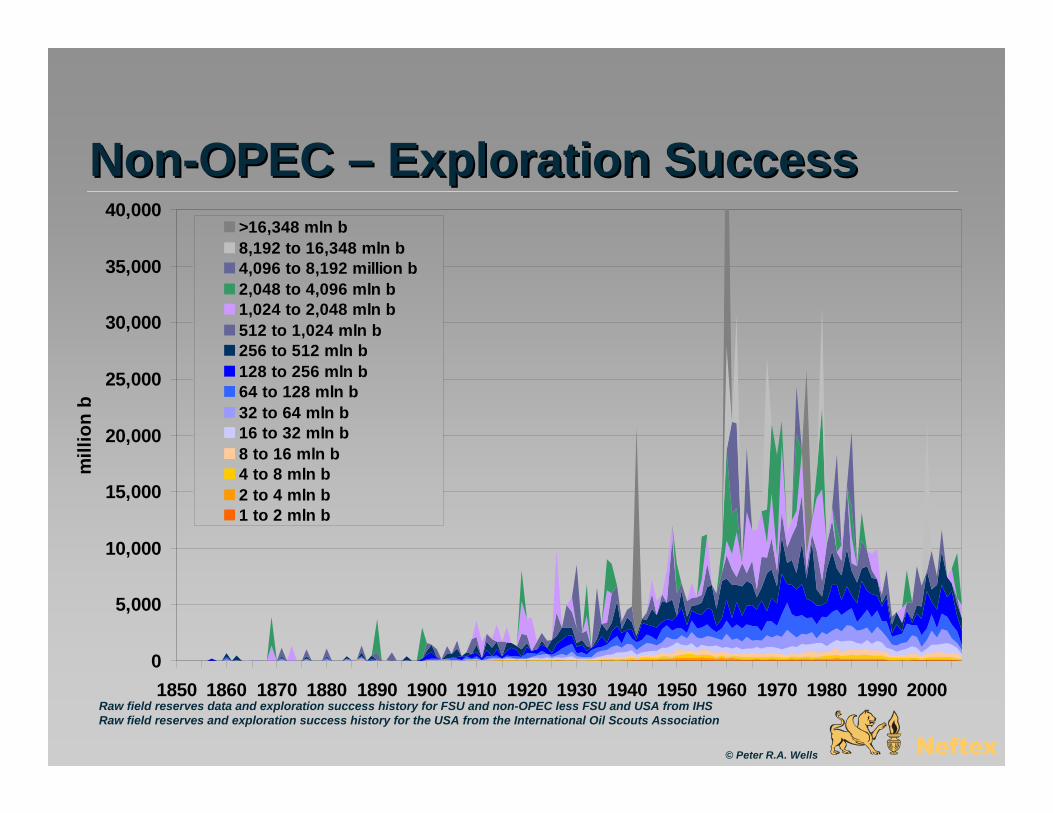

NonNon--OPEC OPEC –– Exploration SuccessExploration Success

Raw field reserves data and exploration success history for FSU and non-OPEC less FSU and USA from IHSRaw field reserves and exploration success history for the USA from the International Oil Scouts Association

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1850 1860 1870 1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000

mill

ion

b

>16,348 mln b8,192 to 16,348 mln b4,096 to 8,192 million b2,048 to 4,096 mln b1,024 to 2,048 mln b512 to 1,024 mln b256 to 512 mln b128 to 256 mln b64 to 128 mln b32 to 64 mln b16 to 32 mln b8 to 16 mln b4 to 8 mln b2 to 4 mln b1 to 2 mln b

© Peter R.A. Wells

History Matching History Matching –– NonNon--OPECOPEC

Raw field reserves data and exploration success history from IHS and International Oil Scouts Association

Actual production profile from our own database

Forecast model profile from the Monte Carlo Simulation

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

45,000,000

1850 1860 1870 1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

b/d

© Peter R.A. Wells

History Matching History Matching –– NonNon--OPECOPEC

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

45,000,000

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

b/d

Raw field reserves data and exploration success history from IHS and International Oil Scouts Association

Actual production profile from our own database

Forecast model profile from the Monte Carlo Simulation © Peter R.A. Wells

Most nonMost non--OPEC, non FSU oil fields are OPEC, non FSU oil fields are offshore offshore –– rapid declinesrapid declines……EOR??EOR??

0

5,000

10,000

15,000

20,000

25,000

1850 1860 1870 1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000

mill

ion

b

0

10

20

30

40

50

60

70

80

90

100

Perc

ent o

ffsho

re

Offshore discoveries

Onshore discoveries

Smoothed Percent Offshorediscoveries

Derived from raw data provided by IHS

© Peter R.A. Wells

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1850 1860 1870 1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

mill

ion

b

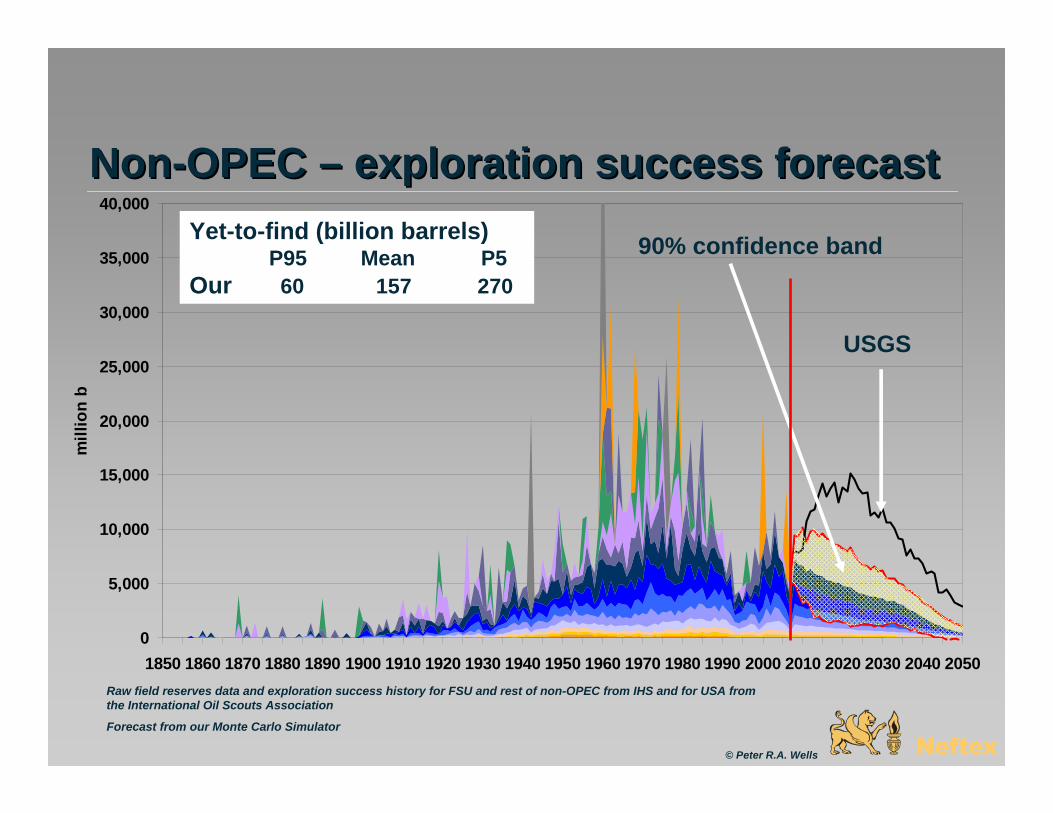

NonNon--OPEC OPEC –– exploration success forecastexploration success forecast

Raw field reserves data and exploration success history for FSU and rest of non-OPEC from IHS and for USA from the International Oil Scouts Association

Forecast from our Monte Carlo Simulator

Yet-to-find (billion barrels)P95 P95 Mean P5 Our 60 157 270

USGS

90% confidence band

© Peter R.A. Wells

NonNon--OPEC OPEC –– at peak! at peak! –– after 2008, demand growth after 2008, demand growth must be met by increased capacity in OPEC or must be met by increased capacity in OPEC or unconventional liquidsunconventional liquids

Raw field reserves data and exploration success history for FSU and rest of non-OPEC from IHS and for USA from the International Oil Scouts Association

Forecast from Monte Carlo simulator

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

45,000,000

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030

b/d

Produced to end 2007

625 billion barrels

Future production 530 billion barrels

© Peter R.A. Wells

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

45,000,000

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030

b/d

90% confidence band

Actual crude oilproductionMean forecastproduction

NonNon--OPEC OPEC –– uncertaintiesuncertainties

Raw field reserves data and exploration success history for FSU and rest of non-OPEC from IHS and for USA from the International Oil Scouts Association

Forecast from Monte Carlo simulator© Peter R.A. Wells

OPECOPEC’’s Dilemma s Dilemma ……. . How much new capacity and by when?How much new capacity and by when?

© Peter R.A. Wells

?

?

Non-OPEC (55.3)

10.2

41.9

31.0

Crude oil

NGLsCan. Tar sands (1.6)

Biofuels (1.3)

Crude oil OPEC (32.0)

Demand (~87)Spare capacity

(1.5)

CTL, GTL, ref. gain etc (1.6)

ref. gain (0.9)

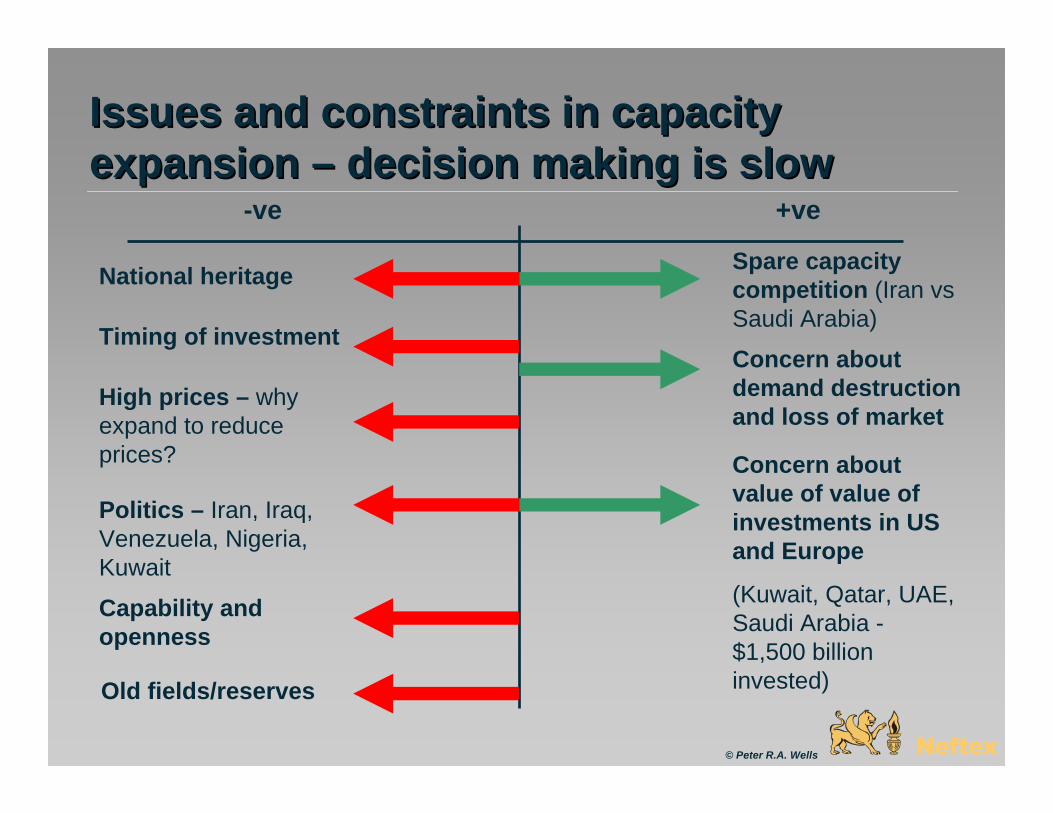

Issues and constraints in capacity Issues and constraints in capacity expansion expansion –– decision making is slowdecision making is slow

© Peter R.A. Wells

-ve +ve

Spare capacity competition (Iran vsSaudi Arabia)

Concern about demand destruction and loss of market

Concern about value of value of investments in US and Europe

(Kuwait, Qatar, UAE, Saudi Arabia -$1,500 billion invested)

National heritage

High prices – why expand to reduce prices?

Politics – Iran, Iraq, Venezuela, Nigeria, Kuwait

Timing of investment

Capability and openness

Old fields/reserves

OPEC OPEC –– our forecast of exploration successour forecast of exploration success

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

1880 1890 1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

mill

ion

b

(billion barrels) P95 mean P5 86 96 120

(2008 to 2050)

Raw historical data from IHS Forecasts by Neftex

© Peter R.A. Wells

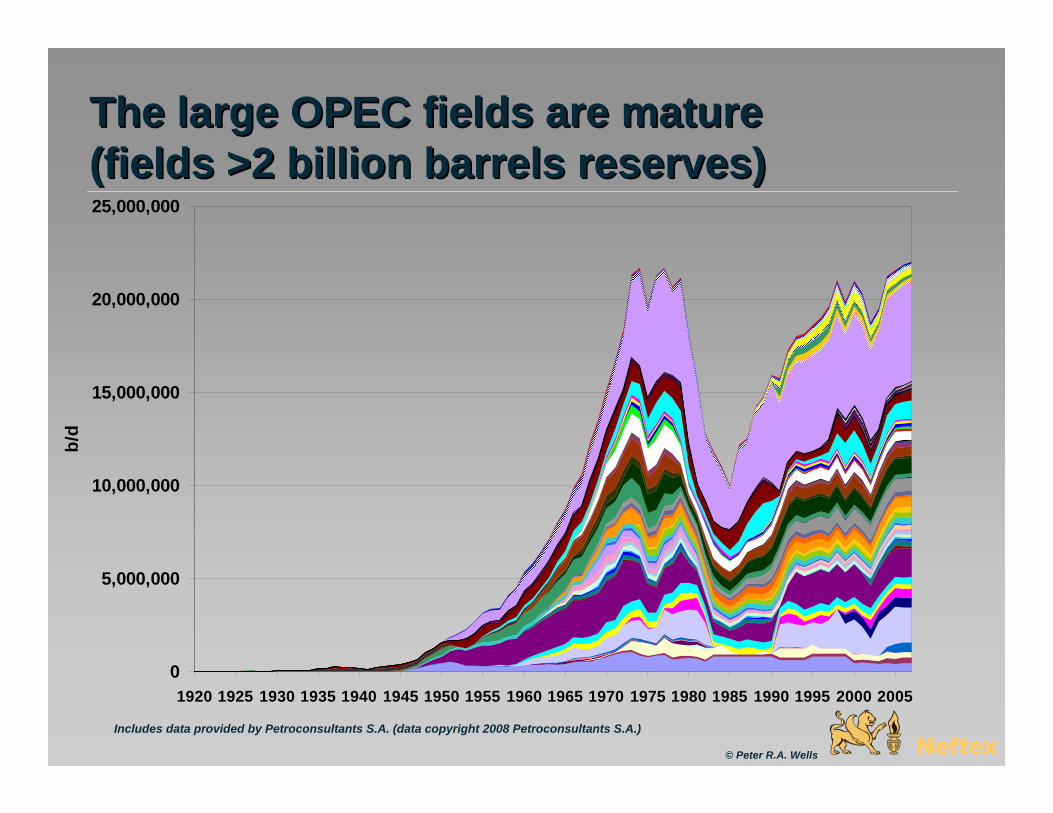

The large OPEC fields are mature The large OPEC fields are mature (fields >2 billion barrels reserves)(fields >2 billion barrels reserves)

© Peter R.A. Wells

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

1920 1925 1930 1935 1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

b/d

Includes data provided by Petroconsultants S.A. (data copyright 2008 Petroconsultants S.A.)

OPEC OPEC –– issue is not reserves but maximum issue is not reserves but maximum sustainable rate and pace of getting theresustainable rate and pace of getting there

Existing producing oil fields

Enhanced/improved oil recovery

Discovered undeveloped fields

Future exploration success

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

b/d

Maximum production capacity determined by maximum production from primary and secondary recovery from existing producing fields

EOR, development of discovered fields and exploration extend plateau

(EXCEPTIONS:- Nigeria, Libya, Algeria)

Existing producing

fields

© Peter R.A. Wells

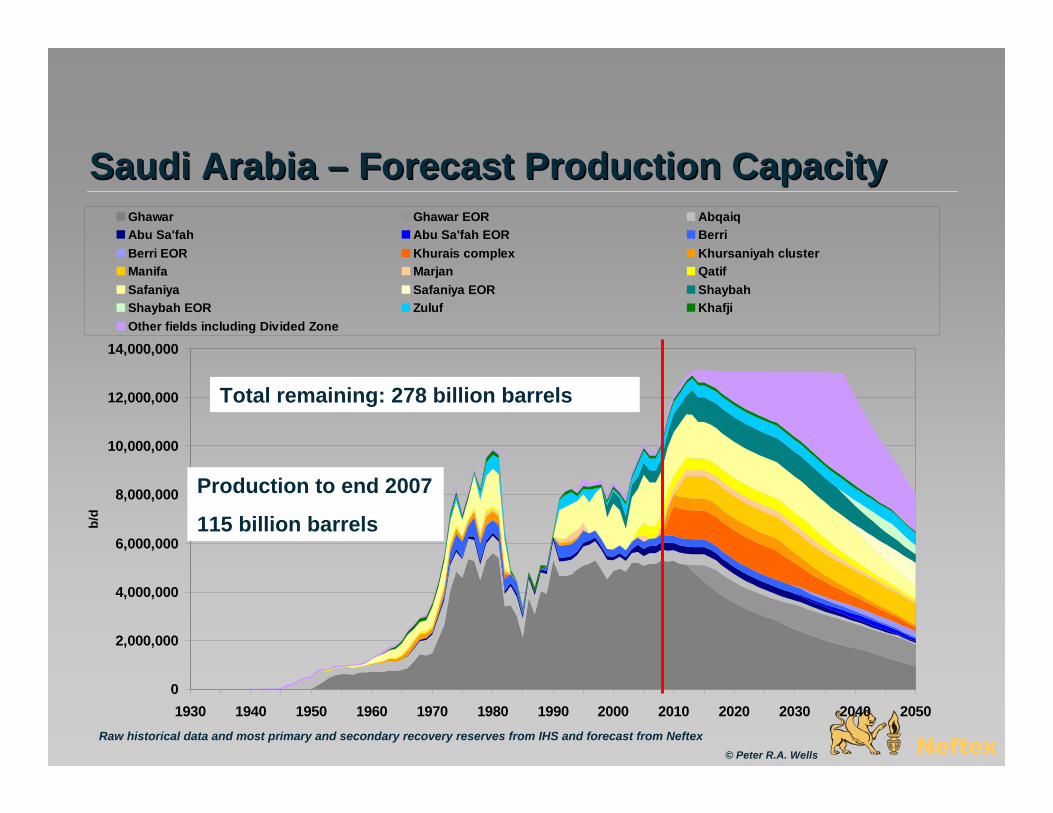

Saudi Arabia Saudi Arabia –– Forecast Production CapacityForecast Production Capacity

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

1930 1940 1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

b/d

Ghawar Ghawar EOR AbqaiqAbu Sa'fah Abu Sa'fah EOR BerriBerri EOR Khurais complex Khursaniyah clusterManifa Marjan QatifSafaniya Safaniya EOR ShaybahShaybah EOR Zuluf KhafjiOther fields including Divided Zone

Raw historical data and most primary and secondary recovery reserves from IHS and forecast from Neftex

Total remaining: 278 billion barrels

Production to end 2007

115 billion barrels

© Peter R.A. Wells

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

b/d

Iran Iran –– forecast production capacityforecast production capacity

Raw historical data and most primary and secondary recovery reserves for conventional crude from Khazar AssociatesForecasts by Neftex

Total remaining: 90 billion barrels

Production to end 2007

61 billion barrels

© Peter R.A. Wells

Ahwaz

MarunGachsaranAgha Jari

Azadegan Undeveloped discoveries

Iraq Iraq –– Forecast Production CapacityForecast Production Capacity

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

b/d

Rumaila (North & South) Kirkuk East Baghdad West QurnaMajnoon Zubair Nahr Umr HalfayaJambur Buzurgan Bai Hassan SubbaKhabbaz Tuba Balad RatawiLuhais Abu Ghraib Ajil TikritQaiyarah Naft Khaneh Amara SufayaAin Zalah Jabal Fauqi Butmah TawkheTaq Taq Nasiriya Gharraf RafidainAhdab Noor Kifl HamrinDiscovered, undeveloped fields Yet-to-Find fields

Raw historical data and most primary and secondary recovery reserves from and forecast from Neftex

Total remaining: 177 billion barrels

Production to end 2007

31 billion barrels

© Peter R.A. Wells

0.0

1,000,000.0

2,000,000.0

3,000,000.0

4,000,000.0

5,000,000.0

6,000,000.0

7,000,000.0

1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

b/d

Orinoco tar sands

Discovered and yet-to-find fields

Other existing fields

Lagunillas, Tia Juana, Bachaquero,Cabimas

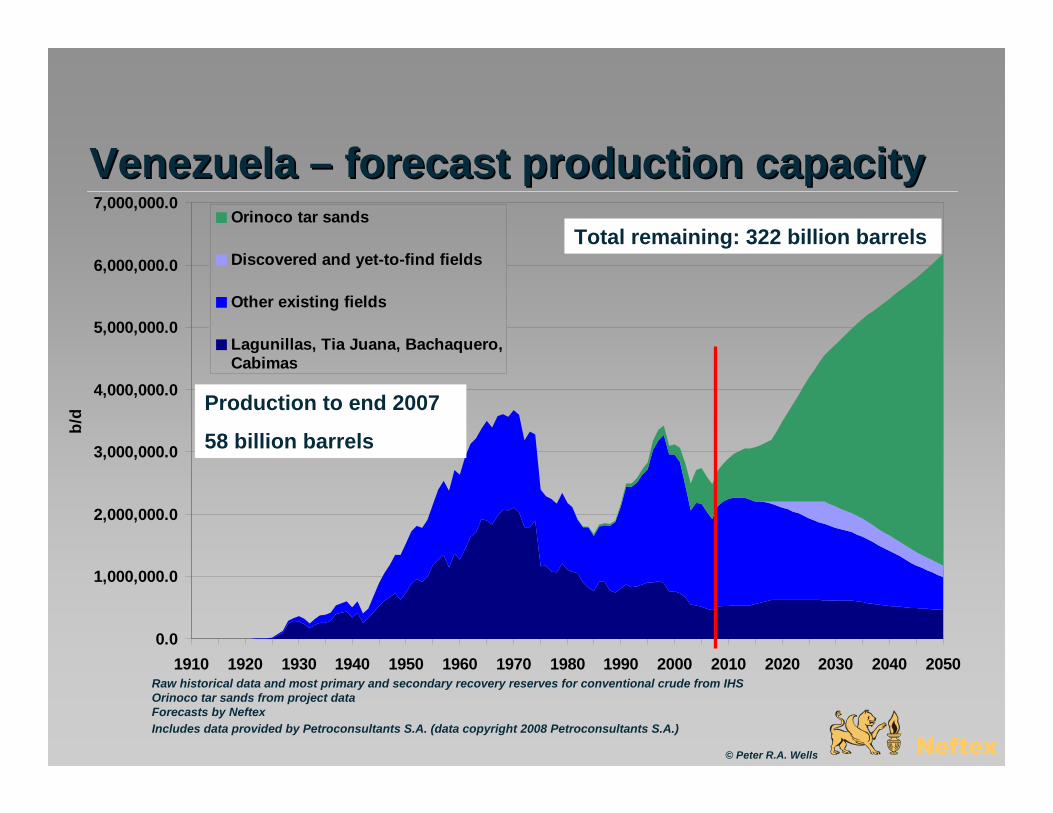

Venezuela Venezuela –– forecast production capacityforecast production capacity

Raw historical data and most primary and secondary recovery reserves for conventional crude from IHS Orinoco tar sands from project dataForecasts by Neftex

Total remaining: 322 billion barrels

Production to end 2007

58 billion barrels

© Peter R.A. Wells

Includes data provided by Petroconsultants S.A. (data copyright 2008 Petroconsultants S.A.)

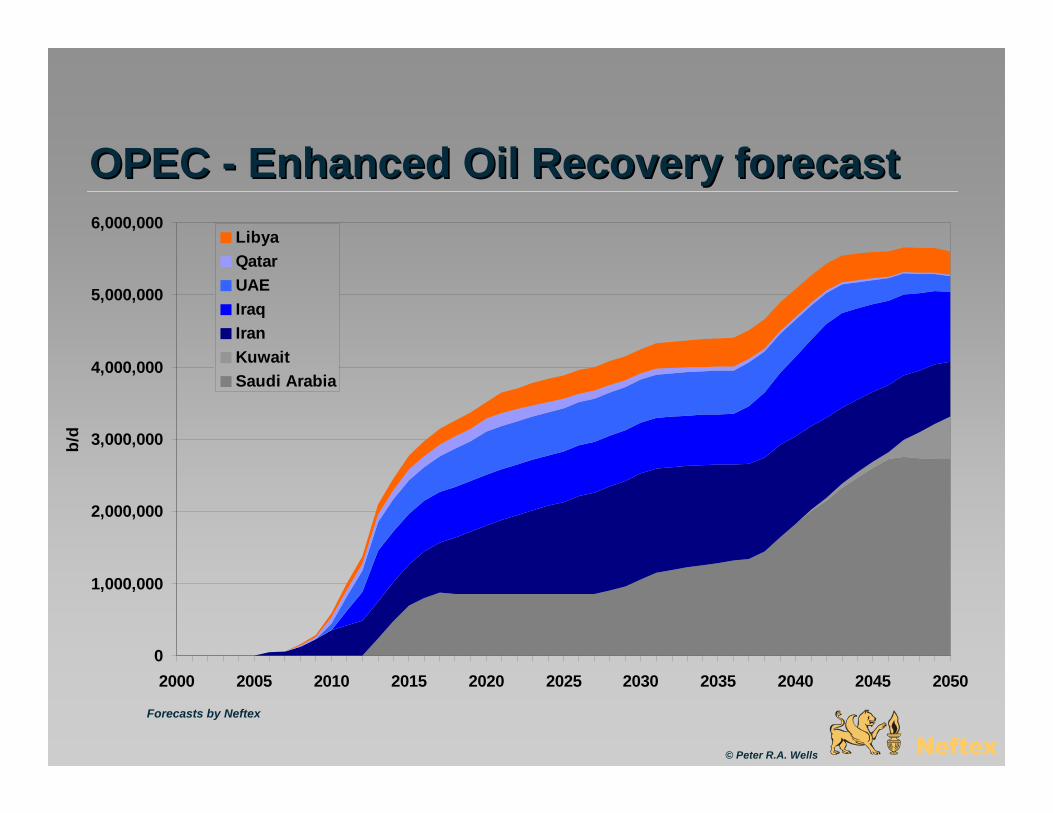

OPEC OPEC -- Enhanced Oil Recovery forecastEnhanced Oil Recovery forecast

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

b/d

LibyaQatarUAEIraqIranKuwaitSaudi Arabia

Forecasts by Neftex

© Peter R.A. Wells

Saudi Arabia

Kuwait

Iraq

Iran

UAEQatar

AlgeriaNigeria

LibyaVenezuela

Indonesia

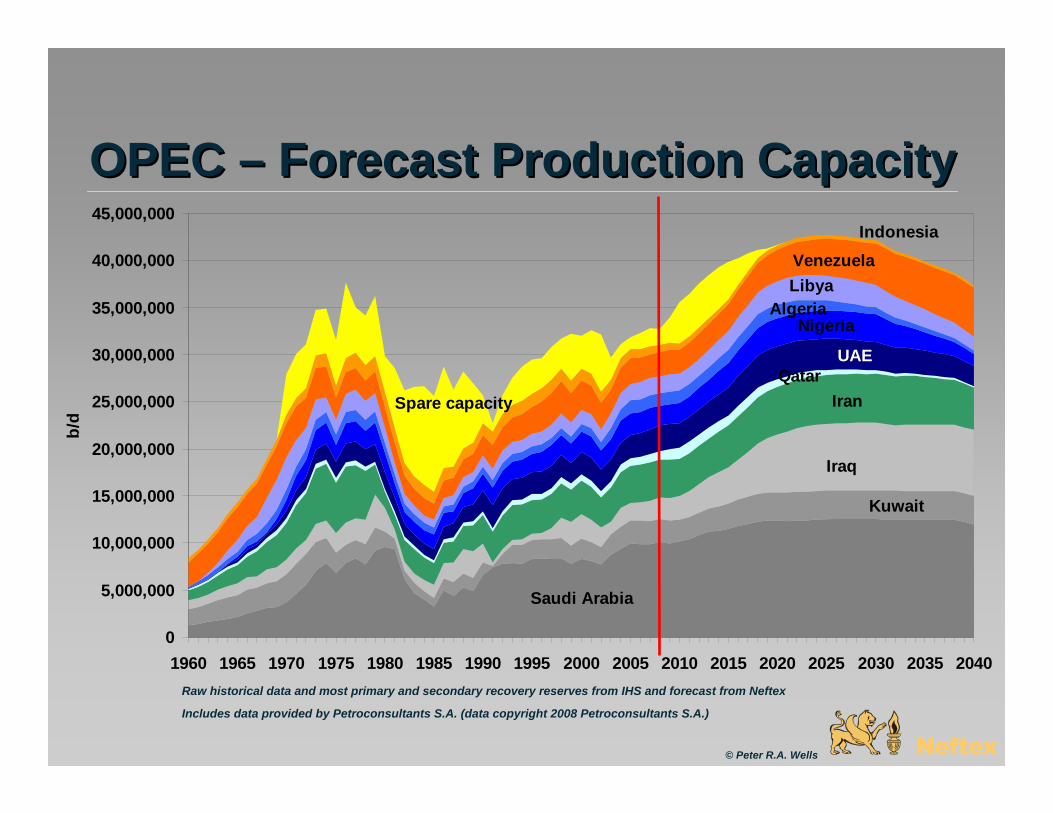

Spare capacity

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

45,000,000

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040

b/d

OPEC OPEC –– Forecast Production CapacityForecast Production Capacity

Raw historical data and most primary and secondary recovery reserves from IHS and forecast from Neftex

© Peter R.A. Wells

Includes data provided by Petroconsultants S.A. (data copyright 2008 Petroconsultants S.A.)

Challenges for OPECChallenges for OPEC• Balance creation of capacity to “guesstimate” of future call on

OPEC

• Call on OPEC is the difference between two large unknowns –non-OPEC liquids (from crude oil to biofuels) and demand

• Extensive investment of capital and expertise will be required just to maintain current production capacity

• Additional capital to create new capacity is available but decision making is necessarily cautious

• Major potential for new capacity is in four countries: – Saudi Arabia (potential 2-3 million b/d) – underway but technical

risks– Iran (1-2 million b/d) - stymied by politics – Iraq (4-5 million b/d) - major political/security risks– Venezuela tar sands (>2 million b/d) – resource nationalism

© Peter R.A. Wells

High Impact potential new production High Impact potential new production capacity is also high riskcapacity is also high risk

© Peter R.A. Wells

0.1

1

10

Impact on capacity,

million b/d

low high

Qatar

Kuwait

Iran

Iraq

Saudi Arabia

UAE Libya

Algeria

Nigeria

Venezuela

AngolaEcuador

Political risks and constraints

Nigeria – IOCs active

Above or below ground risks?Above or below ground risks?

© Peter R.A. Wells

low

High

Geological constraints

“Below ground”

low high

Qatar

Kuwait

Iran

Iraq

Saudi Arabia

UAELibya

Algeria

Nigeria

Venezuela

Angola

Political constraints

“Above ground”

USAROW

FSU

Natural Gas Liquids (Natural Gas Liquids (NGLsNGLs))

USA

Canada

Saudi Arabia

Qatar

Iran

Algeria Exploration success

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050

b/d

Historical data from our own database based on EIA, IEA, BP Statistical Review of World Energy and national databases

© Peter R.A. Wells

““NonNon--crude oilcrude oil”” liquids liquids

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040 2050 2060 2070

b/d

Oil shaleOther liquidsBiofuelsCoal-to-LiquidsGas-to-LiquidsCanadian tar sandsNGLs

© Peter R.A. Wells

Peak liquids production: 98Peak liquids production: 98--105 million b/d 105 million b/d Between: 2017 and 2023 Between: 2017 and 2023

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

1980 1990 2000 2010 2020 2030 2040

b/d

CERA Asian Phoenix (2006) 121 million b/d

IEA Ref. Case (2007) 116 million b/d

Non-OPEC crude oil

OPEC crude oil

NGLs

BiofuelsCTLGTLShale oil

Spare capacity

Canadian tar sands

© Peter R.A. Wells

World liquids supply base case World liquids supply base case ––121121--116 million b/d in 2030???116 million b/d in 2030???

40,000,000

50,000,000

60,000,000

70,000,000

80,000,000

90,000,000

100,000,000

110,000,000

120,000,000

1980 1990 2000 2010 2020 2030 2040

b/d

CERA Asian Phoenix (2006) 121 million b/d

IEA Ref. Case (2007) 116 million b/d

© Peter R.A. Wells

Hard to make up for 40 years of declining Hard to make up for 40 years of declining exploration successexploration success

Raw field reserves data and exploration success history for OPEC, FSU and rest of non-OPEC from IHS and for USA from the International Oil Scouts Association

Forecast exploration success from our Monte Carlo simulator

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

1850 1870 1890 1910 1930 1950 1970 1990 2010 2030 2050

mill

ion

barr

els

OPECFSURest of non-OPEC less FSUUSAP5P95

© Peter R.A. Wells

OPEC OPEC -- Crude Oil Crude Oil

© Peter R.A. Wells

-3,000,000

-2,000,000

-1,000,000

0

1,000,000

2,000,000

3,000,000

4,000,000

1990 1995 2000 2005 2010 2015 2020 2025

year

-on-

year

cha

nge,

b/d

0

20

40

60

80

100

120

140

Rea

l oil

pric

e, d

ated

Bre

nt, $

/b

Non OPEC Saudi Arabia Iraq Rest of OPEC Oil price

World crude oil peaks

Change in production Change in capacity

Liquids balanceLiquids balance

© Peter R.A. Wells

-2,000,000

-1,000,000

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

1990 1995 2000 2005 2010 2015 2020 2025

year

-on-

year

cha

nge,

b/d

0

20

40

60

80

100

120

140

Rea

l oil

pric

e, d

ated

Bre

nt, $

/b

World crude oil NGLs Canadian tar sands

Biofuels Other unconventionals Oil price

World liquids peaks

Change in production Change in capacity

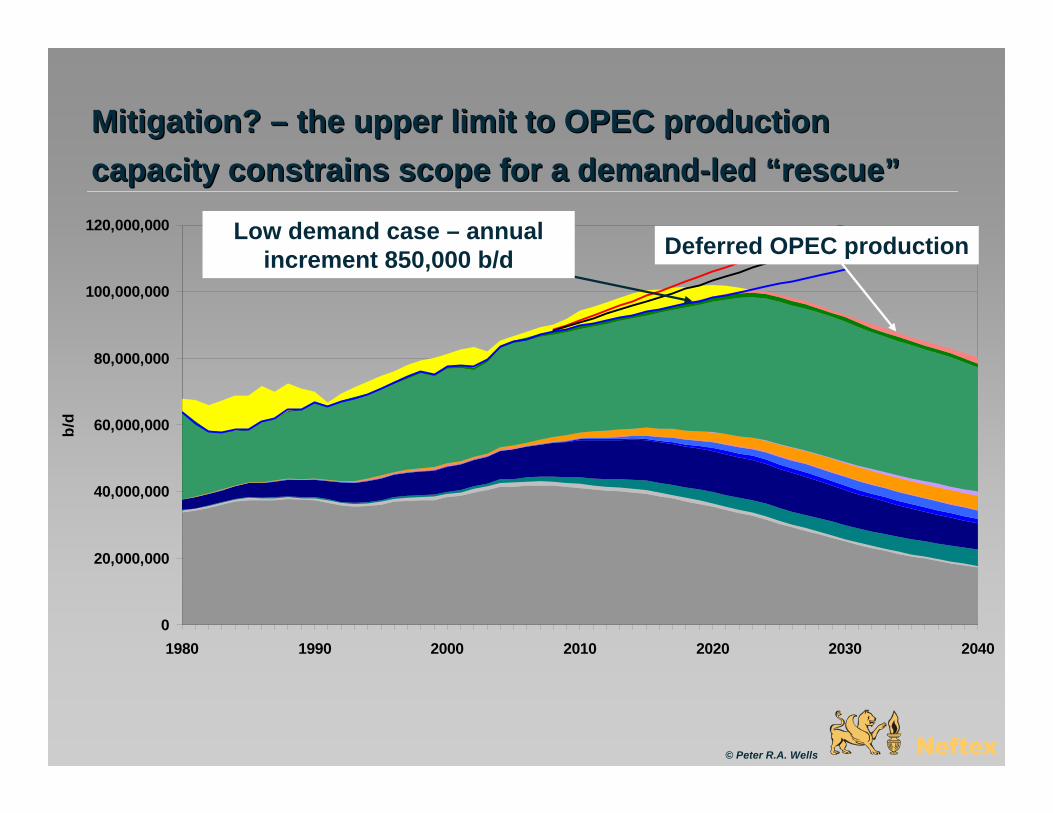

Mitigation? Mitigation? –– the upper limit to OPEC production the upper limit to OPEC production capacity constrains scope for a demandcapacity constrains scope for a demand--led led ““rescuerescue””

© Peter R.A. Wells

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

1980 1990 2000 2010 2020 2030 2040

b/d

Deferred OPEC productionLow demand case – annual increment 850,000 b/d

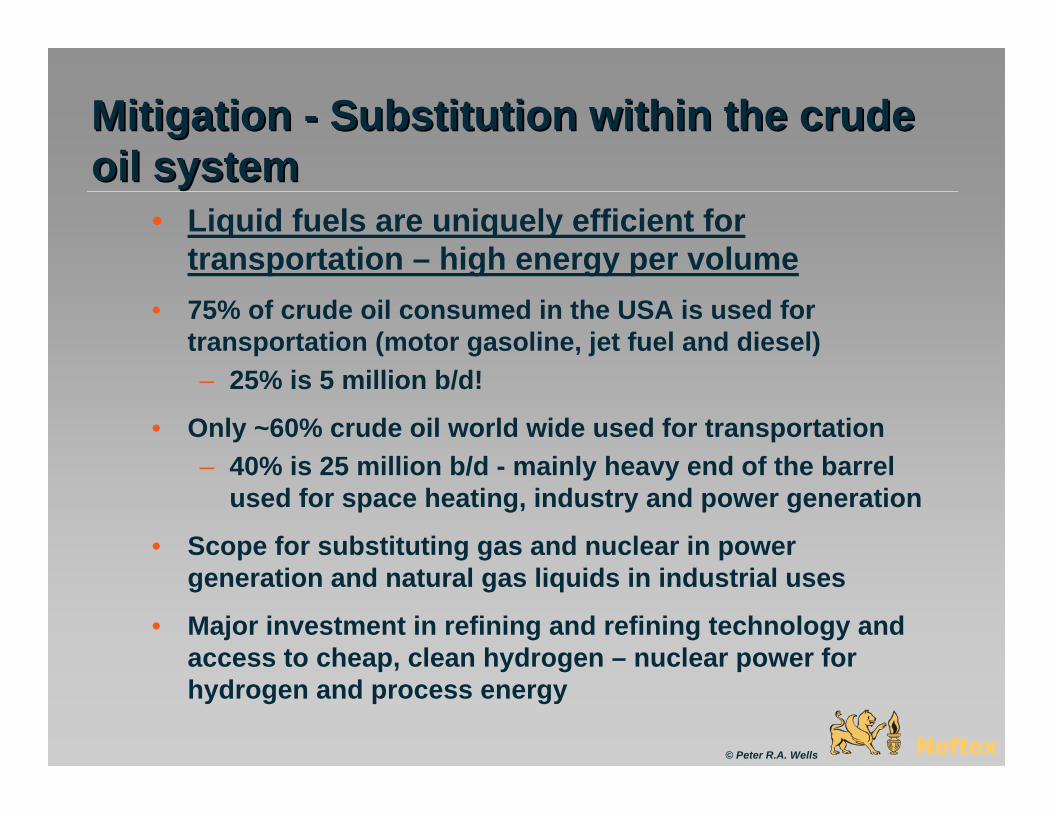

Mitigation Mitigation -- Substitution within the crude Substitution within the crude oil systemoil system

© Peter R.A. Wells

• Liquid fuels are uniquely efficient for transportation – high energy per volume

• 75% of crude oil consumed in the USA is used for transportation (motor gasoline, jet fuel and diesel)– 25% is 5 million b/d!

• Only ~60% crude oil world wide used for transportation– 40% is 25 million b/d - mainly heavy end of the barrel

used for space heating, industry and power generation

• Scope for substituting gas and nuclear in power generation and natural gas liquids in industrial uses

• Major investment in refining and refining technology and access to cheap, clean hydrogen – nuclear power for hydrogen and process energy

Mitigation Mitigation -- substitutionssubstitutions…… electricity replaces electricity replaces gasoline (plug ins, hydrogen fuel cells) gasoline (plug ins, hydrogen fuel cells) –– nuclear!nuclear!

Global Warming

Security of Supply

Coal-to-liquids

Corn ethanol

Sugar cane ethanol

Gas-to-liquids

EU biodiesel

hybridsplug-ins

nuclearbehaviour

Canadian tar sands

Shale oil

Gas from Russia

Clean coal power

Solar-wind-tidalhydrogen

© Peter R.A. Wells

diesel

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

1980 1990 2000 2010 2020 2030 2040

b/d

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

1980 1990 2000 2010 2020 2030 2040

b/d

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

Mitigation Mitigation -- Natural gas will outlast liquids Natural gas will outlast liquids ……Compressed natural gas (CNG)Compressed natural gas (CNG)

© Peter R.A. Wells

Natural gas

Back up slidesBack up slides

© Peter R.A. Wells

BiofuelsBiofuels

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

1970 1980 1990 2000 2010 2020 2030 2040 2050

b/d

Rest of Latin AmericaAfricaMiddle EastRest of developing AsiaIndonesiaPacific CanadaEUChinaIndiaBrazilUSAP5 of our estimateHigh case, IEA 2006P95 of our estimate

© Peter R.A. Wells

Shale OilShale Oil

0

500

1,000

1,500

2,000

2,500

3,000

2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

000

b/d

0

500

1,000

1,500

2,000

2,500

3,000

Forecast range RandUS DOE/DOD Time-Shifted Canadian Tar SandsEIA Base Case Forecast

Environment (GHG, land) Infrastructure Capital cost Gas, water resources Unproven technology

© Peter R.A. Wells

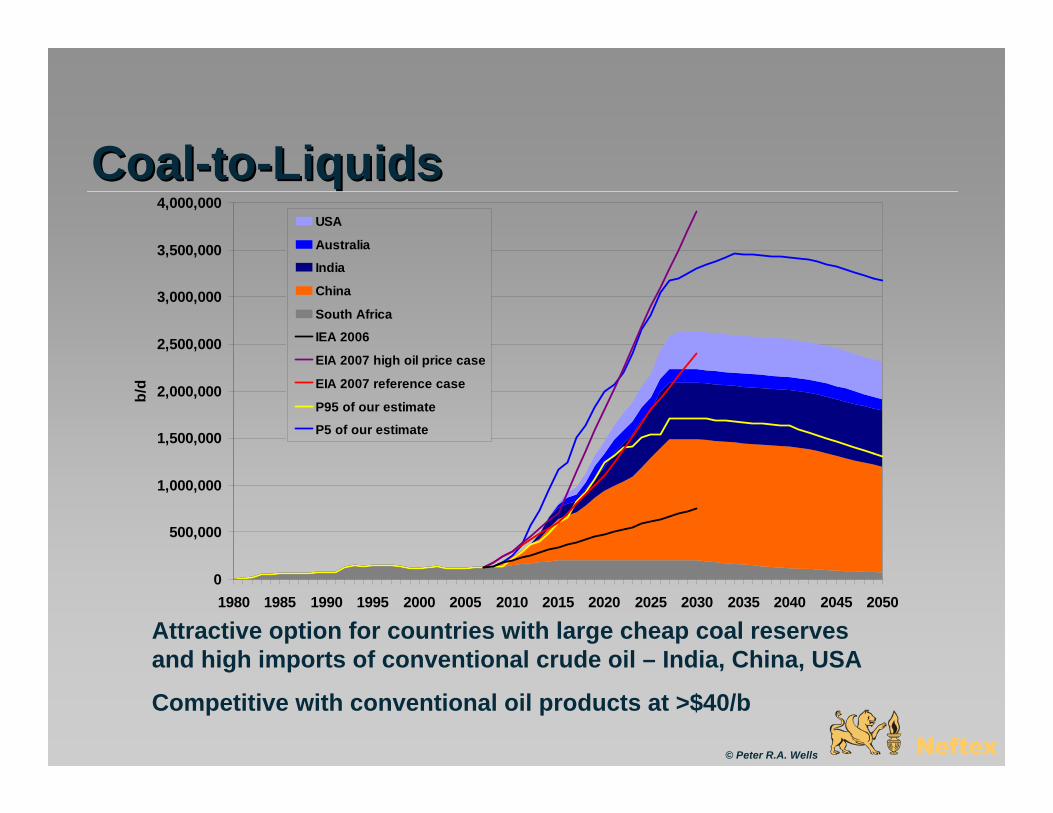

CoalCoal--toto--LiquidsLiquids

Attractive option for countries with large cheap coal reserves and high imports of conventional crude oil – India, China, USA

Competitive with conventional oil products at >$40/b

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

b/d

USA

Australia

India

China

South Africa

IEA 2006

EIA 2007 high oil price case

EIA 2007 reference case

P95 of our estimate

P5 of our estimate

© Peter R.A. Wells

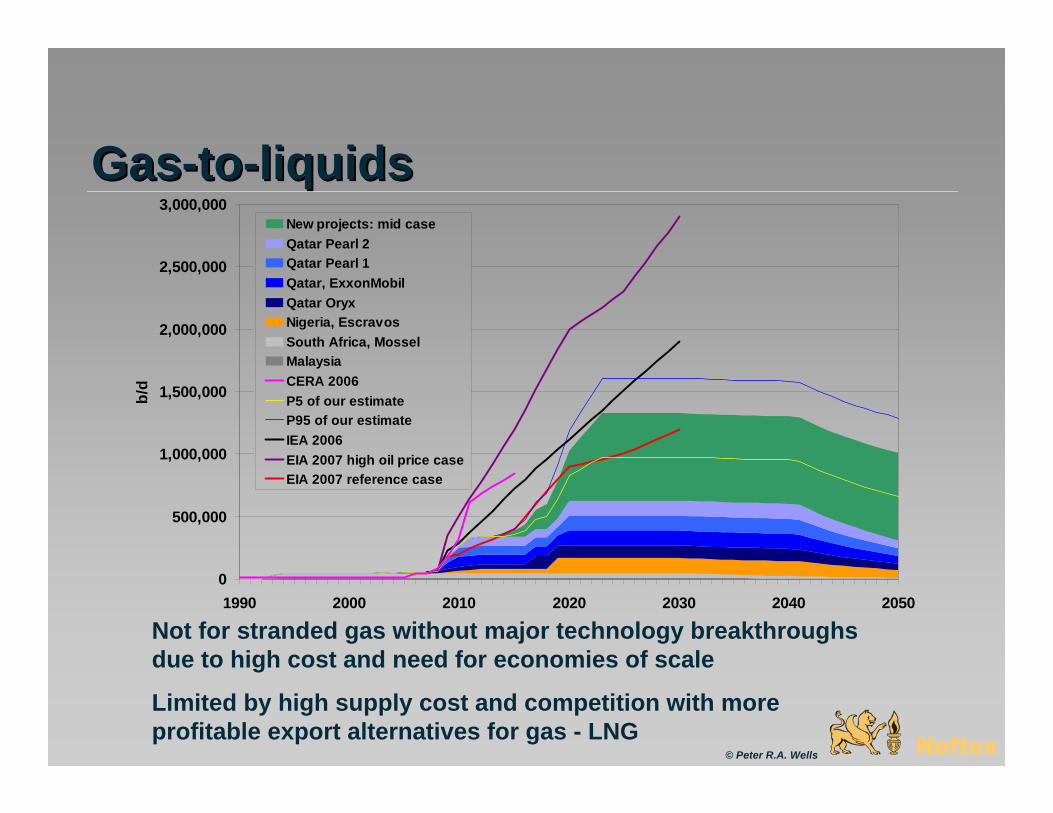

GasGas--toto--liquidsliquids

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

1990 2000 2010 2020 2030 2040 2050

b/d

New projects: mid caseQatar Pearl 2Qatar Pearl 1Qatar, ExxonMobilQatar OryxNigeria, EscravosSouth Africa, MosselMalaysiaCERA 2006P5 of our estimateP95 of our estimateIEA 2006EIA 2007 high oil price caseEIA 2007 reference case

Not for stranded gas without major technology breakthroughs due to high cost and need for economies of scale

Limited by high supply cost and competition with more profitable export alternatives for gas - LNG

© Peter R.A. Wells

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030

b/d

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000Production90 % confidence bandForecast Mean caseIEA 2005CERA 2005ExxonMobil 2005NEB Fortress Islands case 2007NEB Triple E case 2007NEB reference case 2007CAPP unconstrained 2007CAPP moderate growth 2007EIA

Canadian Tar SandsCanadian Tar SandsEnvironment (GHG, land) Infrastructure Capital cost Gas, water resources

© Peter R.A. Wells