Download - Time to leave foreign stock markets?

International stockmarkets have sig-nificantly outper-

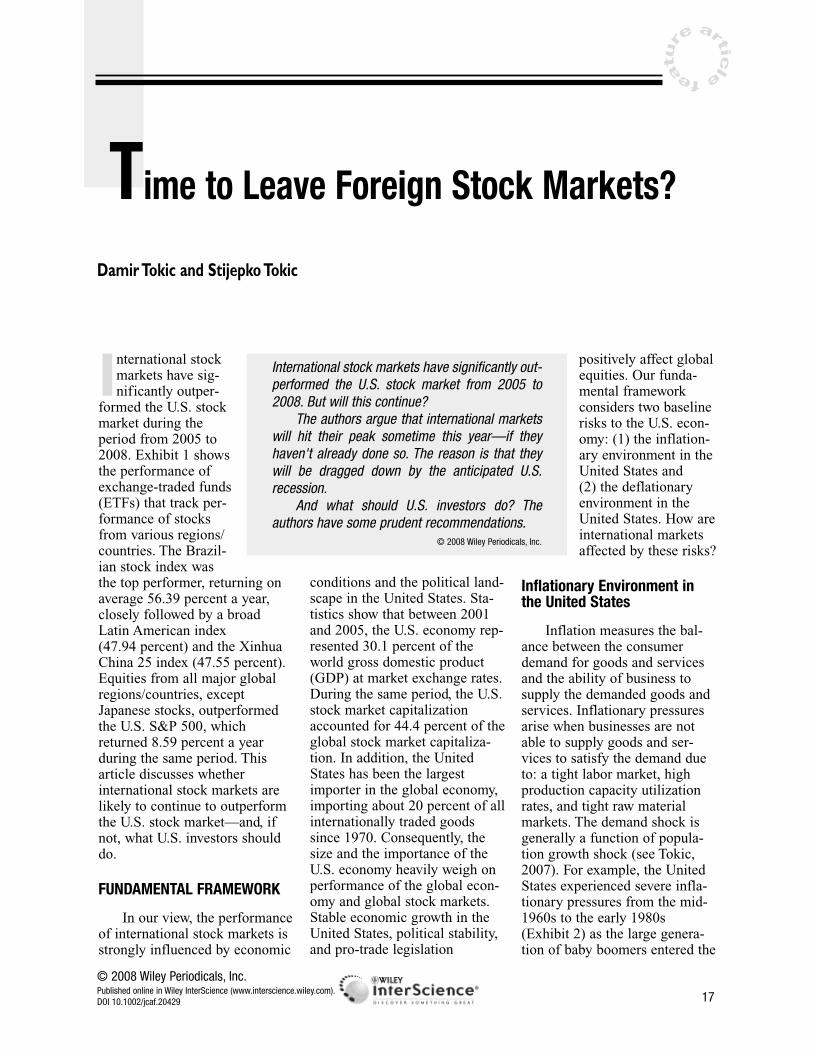

formed the U.S. stockmarket during theperiod from 2005 to2008. Exhibit 1 showsthe performance ofexchange-traded funds(ETFs) that track per-formance of stocksfrom various regions/countries. The Brazil-ian stock index wasthe top performer, returning onaverage 56.39 percent a year,closely followed by a broadLatin American index (47.94 percent) and the XinhuaChina 25 index (47.55 percent).Equities from all major globalregions/countries, exceptJapanese stocks, outperformedthe U.S. S&P 500, whichreturned 8.59 percent a yearduring the same period. Thisarticle discusses whetherinternational stock markets arelikely to continue to outperformthe U.S. stock market—and, ifnot, what U.S. investors shoulddo.

FUNDAMENTAL FRAMEWORK

In our view, the performanceof international stock markets isstrongly influenced by economic

conditions and the political land-scape in the United States. Sta-tistics show that between 2001and 2005, the U.S. economy rep-resented 30.1 percent of theworld gross domestic product(GDP) at market exchange rates.During the same period, the U.S.stock market capitalizationaccounted for 44.4 percent of theglobal stock market capitaliza-tion. In addition, the UnitedStates has been the largestimporter in the global economy,importing about 20 percent of allinternationally traded goodssince 1970. Consequently, thesize and the importance of theU.S. economy heavily weigh onperformance of the global econ-omy and global stock markets.Stable economic growth in theUnited States, political stability,and pro-trade legislation

positively affect globalequities. Our funda-mental frameworkconsiders two baselinerisks to the U.S. econ-omy: (1) the inflation-ary environment in theUnited States and (2) the deflationaryenvironment in theUnited States. How areinternational marketsaffected by these risks?

Inflationary Environment inthe United States

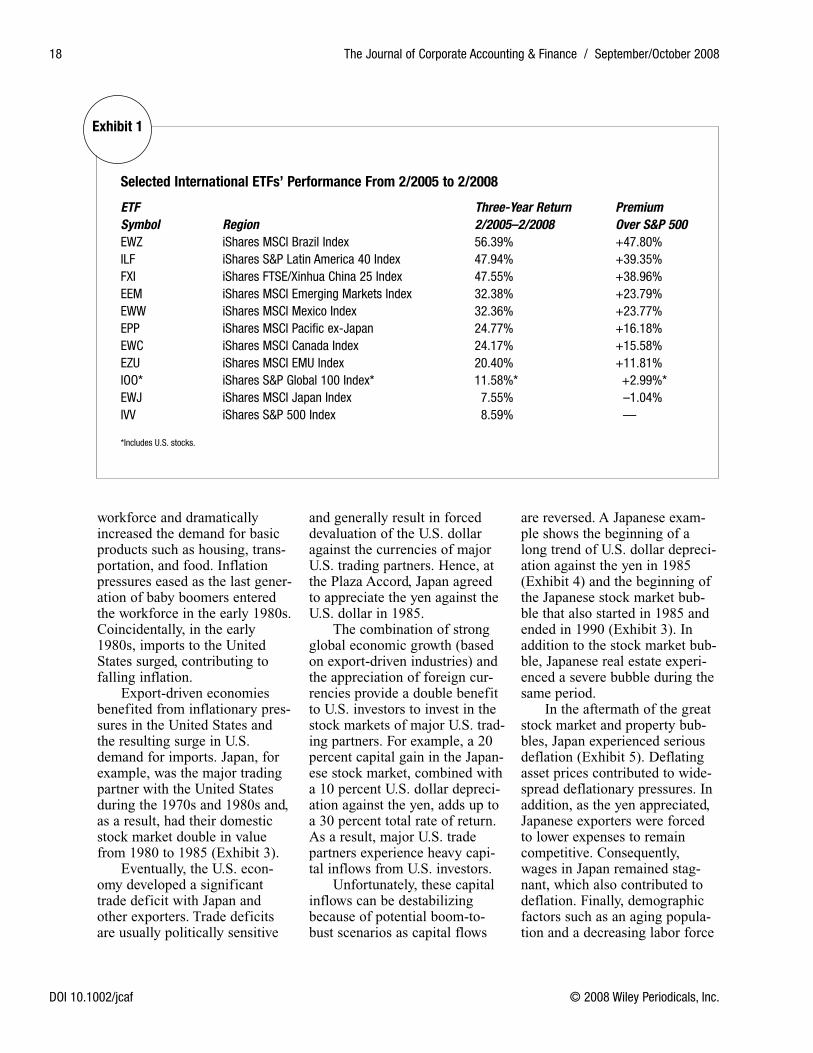

Inflation measures the bal-ance between the consumerdemand for goods and servicesand the ability of business tosupply the demanded goods andservices. Inflationary pressuresarise when businesses are notable to supply goods and ser-vices to satisfy the demand dueto: a tight labor market, highproduction capacity utilizationrates, and tight raw materialmarkets. The demand shock isgenerally a function of popula-tion growth shock (see Tokic,2007). For example, the UnitedStates experienced severe infla-tionary pressures from the mid-1960s to the early 1980s(Exhibit 2) as the large genera-tion of baby boomers entered the

International stock markets have significantly out-performed the U.S. stock market from 2005 to2008. But will this continue?

The authors argue that international marketswill hit their peak sometime this year—if theyhaven't already done so. The reason is that theywill be dragged down by the anticipated U.S.recession.

And what should U.S. investors do? Theauthors have some prudent recommendations.

© 2008 Wiley Periodicals, Inc.

featur

e artic

le

17

© 2008 Wiley Periodicals, Inc.Published online in Wiley InterScience (www.interscience.wiley.com).DOI 10.1002/jcaf.20429

Time to Leave Foreign Stock Markets?

Damir Tokic and Stijepko Tokic

JCAF19-6_20429.qxp 8/19/08 5:07 PM Page 17

workforce and dramaticallyincreased the demand for basicproducts such as housing, trans-portation, and food. Inflationpressures eased as the last gener-ation of baby boomers enteredthe workforce in the early 1980s.Coincidentally, in the early1980s, imports to the UnitedStates surged, contributing tofalling inflation.

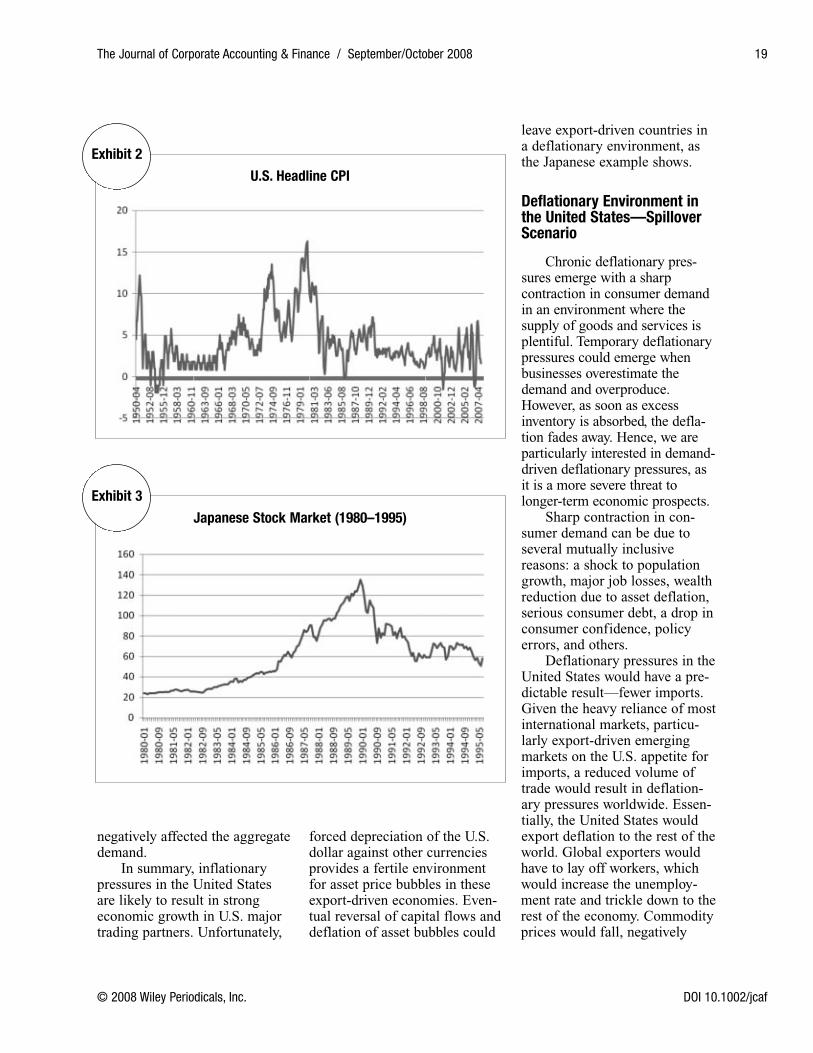

Export-driven economiesbenefited from inflationary pres-sures in the United States andthe resulting surge in U.S.demand for imports. Japan, forexample, was the major tradingpartner with the United Statesduring the 1970s and 1980s and,as a result, had their domesticstock market double in valuefrom 1980 to 1985 (Exhibit 3).

Eventually, the U.S. econ-omy developed a significanttrade deficit with Japan andother exporters. Trade deficitsare usually politically sensitive

and generally result in forceddevaluation of the U.S. dollaragainst the currencies of majorU.S. trading partners. Hence, atthe Plaza Accord, Japan agreedto appreciate the yen against theU.S. dollar in 1985.

The combination of strongglobal economic growth (basedon export-driven industries) andthe appreciation of foreign cur-rencies provide a double benefitto U.S. investors to invest in thestock markets of major U.S. trad-ing partners. For example, a 20percent capital gain in the Japan-ese stock market, combined witha 10 percent U.S. dollar depreci-ation against the yen, adds up toa 30 percent total rate of return.As a result, major U.S. tradepartners experience heavy capi-tal inflows from U.S. investors.

Unfortunately, these capitalinflows can be destabilizingbecause of potential boom-to-bust scenarios as capital flows

are reversed. A Japanese exam-ple shows the beginning of along trend of U.S. dollar depreci-ation against the yen in 1985(Exhibit 4) and the beginning ofthe Japanese stock market bub-ble that also started in 1985 andended in 1990 (Exhibit 3). Inaddition to the stock market bub-ble, Japanese real estate experi-enced a severe bubble during thesame period.

In the aftermath of the greatstock market and property bub-bles, Japan experienced seriousdeflation (Exhibit 5). Deflatingasset prices contributed to wide-spread deflationary pressures. Inaddition, as the yen appreciated,Japanese exporters were forcedto lower expenses to remaincompetitive. Consequently,wages in Japan remained stag-nant, which also contributed todeflation. Finally, demographicfactors such as an aging popula-tion and a decreasing labor force

18 The Journal of Corporate Accounting & Finance / September/October 2008

DOI 10.1002/jcaf © 2008 Wiley Periodicals, Inc.

Selected International ETFs’ Performance From 2/2005 to 2/2008

ETF Three-Year Return Premium

Symbol Region 2/2005–2/2008 Over S&P 500

EWZ iShares MSCI Brazil Index 56.39% +47.80%ILF iShares S&P Latin America 40 Index 47.94% +39.35%FXI iShares FTSE/Xinhua China 25 Index 47.55% +38.96%EEM iShares MSCI Emerging Markets Index 32.38% +23.79%EWW iShares MSCI Mexico Index 32.36% +23.77%EPP iShares MSCI Pacific ex-Japan 24.77% +16.18%EWC iShares MSCI Canada Index 24.17% +15.58%EZU iShares MSCI EMU Index 20.40% +11.81%IOO* iShares S&P Global 100 Index* 11.58%* +2.99%*EWJ iShares MSCI Japan Index 7.55% –1.04%IVV iShares S&P 500 Index 8.59% —

*Includes U.S. stocks.

Exhibit 1

JCAF19-6_20429.qxp 8/19/08 5:07 PM Page 18

negatively affected the aggregatedemand.

In summary, inflationarypressures in the United Statesare likely to result in strongeconomic growth in U.S. majortrading partners. Unfortunately,

forced depreciation of the U.S.dollar against other currenciesprovides a fertile environmentfor asset price bubbles in theseexport-driven economies. Even-tual reversal of capital flows anddeflation of asset bubbles could

leave export-driven countries ina deflationary environment, asthe Japanese example shows.

Deflationary Environment inthe United States—SpilloverScenario

Chronic deflationary pres-sures emerge with a sharpcontraction in consumer demandin an environment where thesupply of goods and services isplentiful. Temporary deflationarypressures could emerge whenbusinesses overestimate thedemand and overproduce.However, as soon as excessinventory is absorbed, the defla-tion fades away. Hence, we areparticularly interested in demand-driven deflationary pressures, asit is a more severe threat tolonger-term economic prospects.

Sharp contraction in con-sumer demand can be due toseveral mutually inclusivereasons: a shock to populationgrowth, major job losses, wealthreduction due to asset deflation,serious consumer debt, a drop inconsumer confidence, policyerrors, and others.

Deflationary pressures in theUnited States would have a pre-dictable result—fewer imports.Given the heavy reliance of mostinternational markets, particu-larly export-driven emergingmarkets on the U.S. appetite forimports, a reduced volume oftrade would result in deflation-ary pressures worldwide. Essen-tially, the United States wouldexport deflation to the rest of theworld. Global exporters wouldhave to lay off workers, whichwould increase the unemploy-ment rate and trickle down to therest of the economy. Commodityprices would fall, negatively

The Journal of Corporate Accounting & Finance / September/October 2008 19

© 2008 Wiley Periodicals, Inc. DOI 10.1002/jcaf

Exhibit 2

U.S. Headline CPI

Exhibit 3

Japanese Stock Market (1980–1995)

JCAF19-6_20429.qxp 8/19/08 5:07 PM Page 19

affecting commodity-producereconomies. The global economicand political environment wouldresemble the environment of theGreat Depression of the 1930s.Implications from the axiom“when the U.S. sneezes, the restof the world catches a cold”would suggest a stronger U.S.dollar, as capital flows are

reversed back into U.S. Treasuries.

Deflationary Environment inthe United States—Decoupling Scenario

The spillover scenarioclearly carries unwanted globalpolitical and economic conse-

quences. Hence, global policy-makers would have to orches-trate a bailout of the U.S. econ-omy. A decoupling scenarioenvisions strong global eco-nomic growth as the U.S. econ-omy goes through a period ofsluggish growth due to demand-driven deflationary pressures.

Specifically, the global con-sumer would have to replace theU.S. consumer as a growthengine. Therefore, globalexporters would have to shifttheir efforts to sell products todomestic consumers and globalconsumers, excluding the U.S.consumer. In addition, U.S. com-panies would export their goodsand services to growing globaleconomies, reducing the severityof the U.S. economic slowdown.

However, a full cooperationof global policymakers would berequired to implement globalconsumption-enhancing policies.Depreciation of the U.S. dollarwould be necessary to increaseU.S. exports, which would addpoints to U.S. GDP growth.Unfortunately, appreciating for-eign currencies and strongglobal economic growth wouldencourage heavy capital inflowsfrom U.S. investors into interna-tional markets, which wouldlikely cause a boom-to-bust sce-nario in commodities, realestate, and international equities.

EXPLANATION OF RECENTPERFORMANCE OFINTERNATIONAL EQUITIES

Within our fundamentalframework, we identify the caseof a mild deflationary environ-ment in the United States with aspillover effect on internationalmarkets in 2001 as the U.S.economy experienced a defla-tionary scare following theburst of the technology stockmarket bubble. The newspaper

20 The Journal of Corporate Accounting & Finance / September/October 2008

DOI 10.1002/jcaf © 2008 Wiley Periodicals, Inc.

Exhibit 4

Price of the U.S. Dollar in Japanese Yen (1980–1995)

Exhibit 5

Headline CPI in Japan (1980–1995)

JCAF19-6_20429.qxp 8/19/08 5:07 PM Page 20

headlines about the ConsumerPrice Index (CPI) turned nega-tive for the first time since theearly 1950s (Exhibit 2). Thevolume of international tradecontracted as U.S. imports andU.S. exports decreased. Conse-quently, international marketsexperienced a deflationaryslowdown as well.

The deflationary scare didnot appear to be persistent, andexpectations were that the realeconomy would not be seriouslyaffected by the bursting of thetech bubble. However, expecta-tions changed following the Sep-tember 11, 2001, terrorist attack.Concerned about the deeperdeflationary pressures, the Fed

allegedly engineered a housingbubble to re-inflate the economyand a V-shape recovery in thestock market. Low short-terminterest rates encouraged specu-lation in real estate withadjustable rate mortgages, inter-est-only mortgages, and otherexotic products. In addition, thelack of regulatory oversightencouraged predatory lending.As a result, the real estate mar-ket boomed. However, the econ-omy appeared to be gainingground only after the consumerdiscovered the possibility ofextracting the home equity viahome equity line of credit(HELOC) loans and used thefunds to consume. Internationalmarkets initially participated assuppliers of goods for U.S. con-sumption as U.S. imports surged.

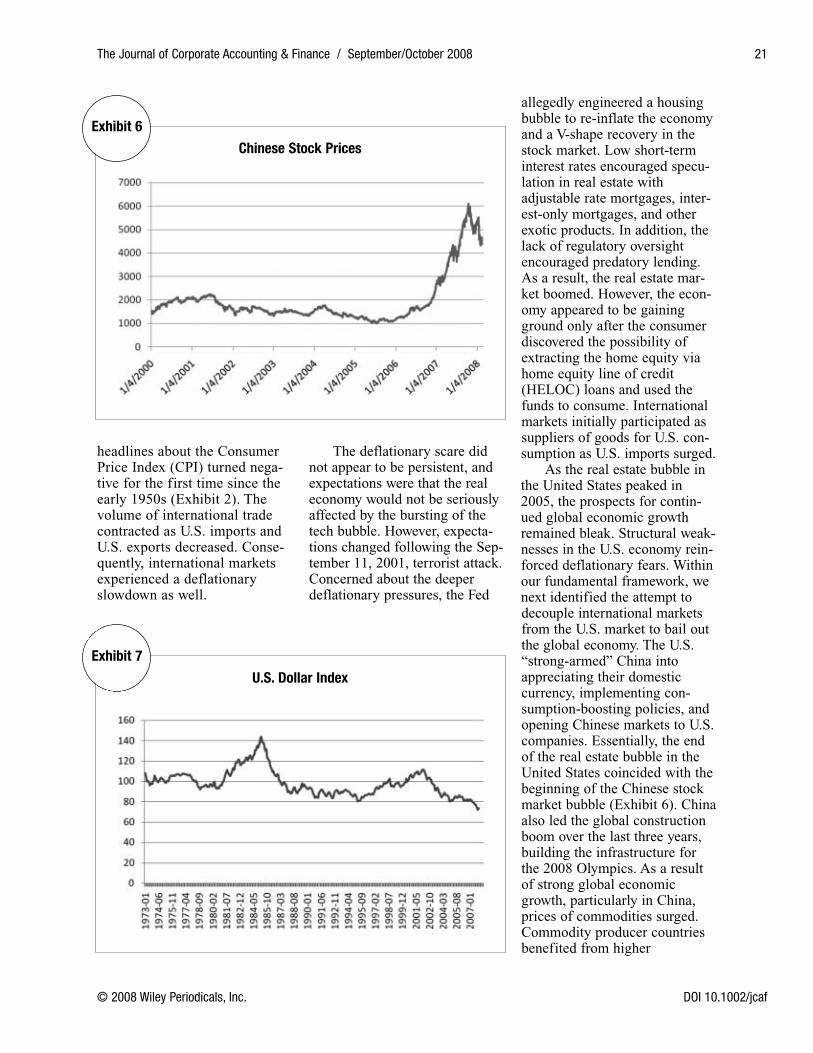

As the real estate bubble inthe United States peaked in2005, the prospects for contin-ued global economic growthremained bleak. Structural weak-nesses in the U.S. economy rein-forced deflationary fears. Withinour fundamental framework, wenext identified the attempt todecouple international marketsfrom the U.S. market to bail outthe global economy. The U.S.“strong-armed” China intoappreciating their domesticcurrency, implementing con-sumption-boosting policies, andopening Chinese markets to U.S.companies. Essentially, the endof the real estate bubble in theUnited States coincided with thebeginning of the Chinese stockmarket bubble (Exhibit 6). Chinaalso led the global constructionboom over the last three years,building the infrastructure forthe 2008 Olympics. As a resultof strong global economicgrowth, particularly in China,prices of commodities surged.Commodity producer countriesbenefited from higher

The Journal of Corporate Accounting & Finance / September/October 2008 21

© 2008 Wiley Periodicals, Inc. DOI 10.1002/jcaf

Exhibit 6

Chinese Stock Prices

Exhibit 7

U.S. Dollar Index

JCAF19-6_20429.qxp 8/19/08 5:07 PM Page 21

22 The Journal of Corporate Accounting & Finance / September/October 2008

DOI 10.1002/jcaf © 2008 Wiley Periodicals, Inc.

commodity prices and their mar-kets surged, along with the valueof their currencies against theU.S. dollar. In fact, the U.S. dol-lar index depreciated against allindustrial countries’ currencies,similar to the period post-PlazaAccord in the 1980s (Exhibit 7).

As the U.S. economy slowedin 2007, with the first signs ofdamage due to the subprime fall-out in the aftermath of the burst-ing of the housing bubble, theglobal economy remained rela-tively stable. Actually, U.S.exports surged, easing the reces-sion fears in the United States.

Many economists praised decou-pling of international marketsfrom the U.S. market. However,in January 2008, internationalmarkets fell as sharply as theU.S. market. The questionremains: Have international mar-kets really decoupled from theU.S. market and, thereby, willinternational stocks continue tooutperform?

WILL INTERNATIONAL STOCKCONTINUE TO OUTPERFORM?

We are in the camp thatbelieves that the U.S. economy

will face disinflationary pres-sures, negative-to-sluggish eco-nomic growth, and low rates ofreturn in the foreseeable future.Whether international marketswill be able to outperform theU.S. market depends on whethertheir policymakers are able todecouple their markets from theU.S. market. We see three poten-tial scenarios (Exhibit 8).

Scenario 1—InternationalMarkets Have Already Busted:Peaked in 2007

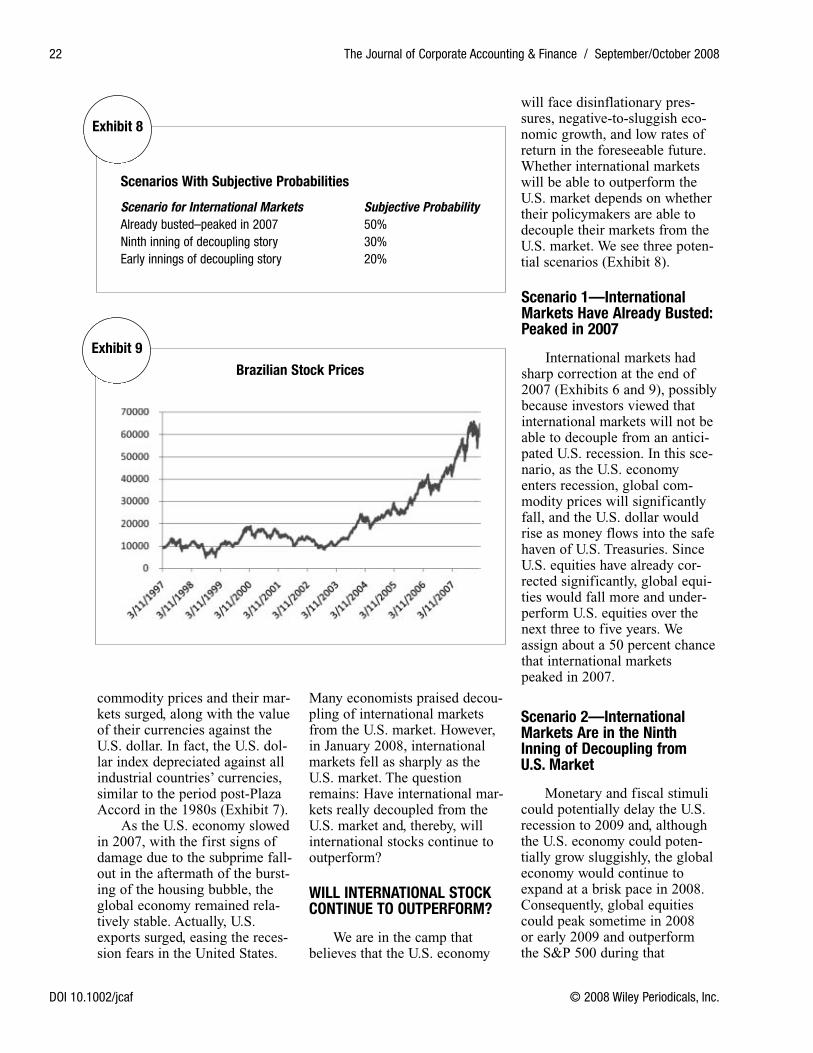

International markets hadsharp correction at the end of2007 (Exhibits 6 and 9), possiblybecause investors viewed thatinternational markets will not beable to decouple from an antici-pated U.S. recession. In this sce-nario, as the U.S. economyenters recession, global com-modity prices will significantlyfall, and the U.S. dollar wouldrise as money flows into the safehaven of U.S. Treasuries. SinceU.S. equities have already cor-rected significantly, global equi-ties would fall more and under-perform U.S. equities over thenext three to five years. Weassign about a 50 percent chancethat international marketspeaked in 2007.

Scenario 2—InternationalMarkets Are in the NinthInning of Decoupling from U.S. Market

Monetary and fiscal stimulicould potentially delay the U.S.recession to 2009 and, althoughthe U.S. economy could poten-tially grow sluggishly, the globaleconomy would continue toexpand at a brisk pace in 2008.Consequently, global equitiescould peak sometime in 2008 or early 2009 and outperform the S&P 500 during that

Scenarios With Subjective Probabilities

Scenario for International Markets Subjective Probability

Already busted–peaked in 2007 50%Ninth inning of decoupling story 30%Early innings of decoupling story 20%

Exhibit 8

Exhibit 9

Brazilian Stock Prices

JCAF19-6_20429.qxp 8/19/08 5:07 PM Page 22

period—and then crash moresignificantly and underperformU.S. stock further on. We assignabout a 30 percent chance to thisscenario, mostly because 2008 isthe year of the ChineseOlympics and the U.S. elections.

Scenario 3—InternationalMarkets Are in the EarlyInnings of Decoupling fromthe U.S. Market

Decoupling of global finan-cial markets from the U.S.market would require globallycoordinated efforts to addressrisk associated with the troublingstate of the U.S. economy, notonly due to the housing fallout,but also due to longer-termstructural changes and demo-graphics. Assuming that globalpolicymakers are able to coordi-nate a bailout of the globaleconomy, it would still not be asmooth ride. Inflation wouldsignificantly increase due to therising price of oil, food, andother commodities. Strongereconomic growth and risinginflation abroad would causesignificant depreciation of theU.S. dollar, which would onlyadd to pressures of risingcommodities and inflation.Appreciation of foreign curren-

cies would cause speculativemoney inflow into foreignassets. Consequently, commodi-ties, foreign equities, andforeign currencies would inflateto irrational levels, causing thebubble.

Eventually, the enormousbubble in emerging markets, for-eign currencies, and commodi-ties would burst. Unfortunately,the result would be similar to theJapanese example from the late1980s, except that this time theglobal economy as a wholewould sink into deflation andprolonged recession. We seeabout a 20 percent chance forthis scenario.

IMPLICATIONS

Decoupling of internationalmarkets from the U.S. marketwould be a temporary bailout ofthe global economy with signifi-cant negative longer-term impli-cations. Specifically, as theglobal economy continues briskexpansion, while the U.S. entersrecession, a new bubble wouldemerge in foreign stocks, foreigncurrencies, and commodities.Eventual reversal of moneyflows would have long-termdeflationary effects on the globaleconomy.

Long-term returns for interna-tional equities will continue to beheavily correlated with return onU.S. equities; however, the stan-dard deviation (or risk) willcontinue to be higher. Therefore,economic prosperity and stabilityin the United States will continueto be the most important eco-nomic indicator of global eco-nomic prosperity and stability.Hence, U.S. policymakers mustaddress structural weaknesses inthe U.S. economy for the long-termbenefit of the global economy.

We estimate about an 80percent chance that internationalequities peaked in 2007 or willpeak in 2008. Consequently, U.S.investors should graduallyreduce their international hold-ings and increase allocations toU.S. Treasuries, investment-grade U.S. corporate bonds, orlow-risk U.S. equities. We feelthat speculators anticipating thebubble in commodities and for-eign equities and the further sig-nificant fall of the U.S. dollarhave about a 20 percent chanceof being right.

REFERENCE

Tokic, D. (2007). Baby boomers and finan-cial markets: A relationship in the making. Journal of Investing, 16(2), 77–84.

The Journal of Corporate Accounting & Finance / September/October 2008 23

© 2008 Wiley Periodicals, Inc. DOI 10.1002/jcaf

Damir Tokic, PhD, is an associate professor of finance at the University of Houston–Downtown.Stijepko Tokic, JD, LLM, is an assistant professor of business law at Northeastern Illinois University.

JCAF19-6_20429.qxp 8/19/08 5:07 PM Page 23