8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 1/29

1

FN312: ADVANCED FINANCIAL

MANAGEMENT TOPICS

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 2/29

2

LECTURE SERIES VI

7 Mergers, acquisitions and corporatereorganization

j Approaches to attain profitable growth (internal vs.external growth)

jDifferent types of Mergers/acquisitions

jMotives for mergers and acquisitions

jEvaluation of mergers

jCorporate reorganization

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 3/29

3

Approaches to attain profitable growth

A firm can achieve profitable growth throughexternal, internal or both.

Internal growth: growth attained within a firm by

Introducing/developing a new line of business (introducea new product).

Expanding the existing lines of business (expand themarket, increase the production capacity).

External growth: acquisition of existing businessentity. This is known as merger, acquisition,amalgamation, takeovers, absorption, consolidationetc.

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 4/29

4

Approaches to attain profitable growth

(cont.)

Advantages of Internal growth:

A firm is able to retain control

It offers flexibility: types of technology required

etc. Disadvantages:

The process may take a long time

It may be highly uncertain, particularly whenintroducing a new product/line of business

Inability to raise enough funds

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 5/29

5

Mergers/acquisitions

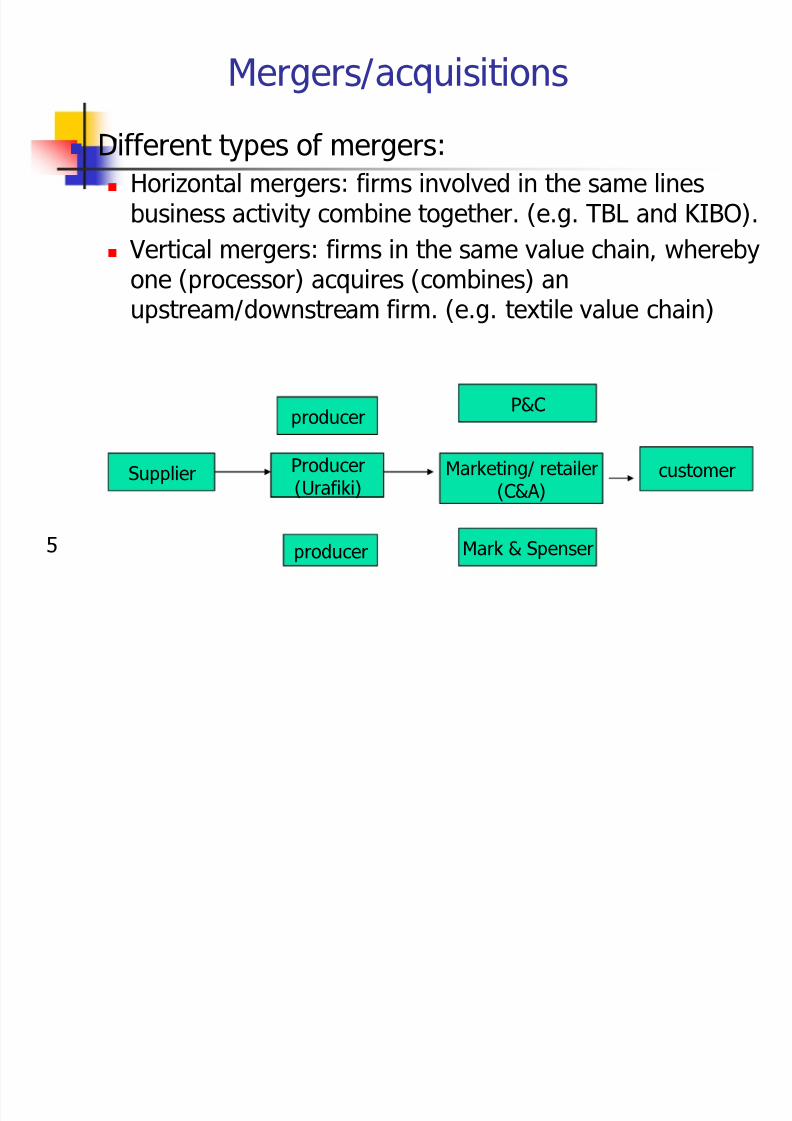

Different types of mergers: Horizontal mergers: firms involved in the same lines

business activity combine together. (e.g. TBL and KIBO).

Vertical mergers: firms in the same value chain, whereby

one (processor) acquires (combines) anupstream/downstream firm. (e.g. textile value chain)

Supplier Producer(Urafiki)

Marketing/ retailer(C&A)

customer

producer

producer Mark & Spenser

P&C

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 6/29

6

Mergers/acquisitions

Different types of mergers: Conglomerate merger: firms from different lines

of business (different industries/sectors)

combine together. E.g. One firm in textile industry and another in

pharmaceutical industry.

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 7/29

7

Motives for mergers/acquisitions

Defensive motives

Economies of scale

Increase utilisation of idle capacity in all aspects

(finance, production, management, staff, etc) Reduce transaction costs, distribution costs

Reduction of competition

Horizontal: increase mkt power and monopoly (TBL

and KIBO) Vertical: limit mkt entry as it results in the control of

outlets and suppliers (TBL and distributors; Largefishing coys in Mwanza)

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 8/29

8

Mot ves or mergers/acqu s t ons(cont.)

Defensive motives

Tax benefits

Fast growth

Synergy: combine strength and opportunitiesto overcome threats and weaknesses

A firm has favourable sources of funds but it has noinvestment opportunities, while another has

investment opportunity but it has no funds. Firms might have different strength in research and

development, management competencies, andproduction. Combining their activities may result in

an increase in their strength.

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 9/29

9

Motives for mergers/acquisitions(cont.)

Offensive motives (take-overs) Fast growth

Asset stripping: take advantage of undervalued shares,after buying then selling the assets at profit.

Financial opportunities: take advantage of inefficient (non-optimal) capital structure.

Diversification, particularly for conglomeratemergers

Reduce business risk Reduce fluctuation of an investors income. For this to be

achieved, incomes from merged investments need to beindependent, or inversely correlated.

the reduction should be higher that what the investor canachieve by diversifying his investment portfolio).

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 10/29

10

Evaluation of mergers

Analysis of mergers involves 3 steps Planning

Review a firms (acquiring) objectives of acquisition: itsstrength, corporate goals (planned expansion in terms of target markets, interested products, growth rate, etc).

This helps to identify the potential firm for target. Search and screening

Search: looking for suitable candidates for acquisition Screening: process of short-listing a few candidates from the

available ones. Then, gather detailed information for short-listed ones

Financial evaluation Central question: What is the benefit of merger to the

acquiring firm? A merger will make sense to the acquiring firm if its shareholders

benefit. Shareholders will benefit if merger leads to the maximisation of

their wealth.

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 11/29

11

Evaluation of mergers (cont)

Financial evaluation A merger will create an economic advantage

(EA) if the combined present value of themerged firms is greater than the sum of their

individual present values when treated asseparate firms. e.g.: Firm P has present value (value of a firm) = VP

Firm Q has present value (value of a firm) = VQ

When P and Q merge, the present value of themerger = VPQ

A merger will have EA if VPQ > VP + VQ

The economic advantage created, EA = V

PQ- (V

P+ V

Q)

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 12/29

12

Evaluation of mergers (cont)

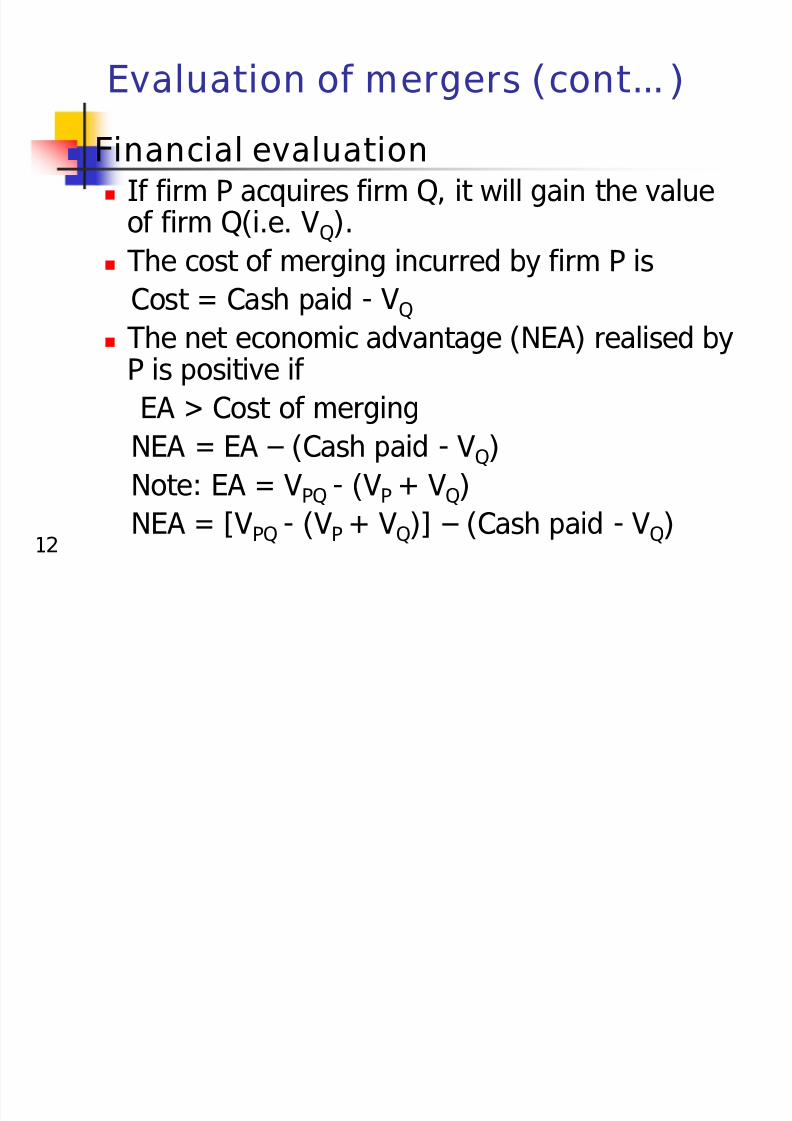

Financial evaluation If firm P acquires firm Q, it will gain the value

of firm Q(i.e. VQ).

The cost of merging incurred by firm P is

Cost = Cash paid - VQ

The net economic advantage (NEA) realised byP is positive if

EA > Cost of mergingNEA = EA (Cash paid - VQ)

Note: EA = VPQ - (VP + VQ)

NEA = [VPQ - (VP + VQ)] (Cash paid - VQ)

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 13/29

13

Evaluation of mergers (cont)

Financial evaluation

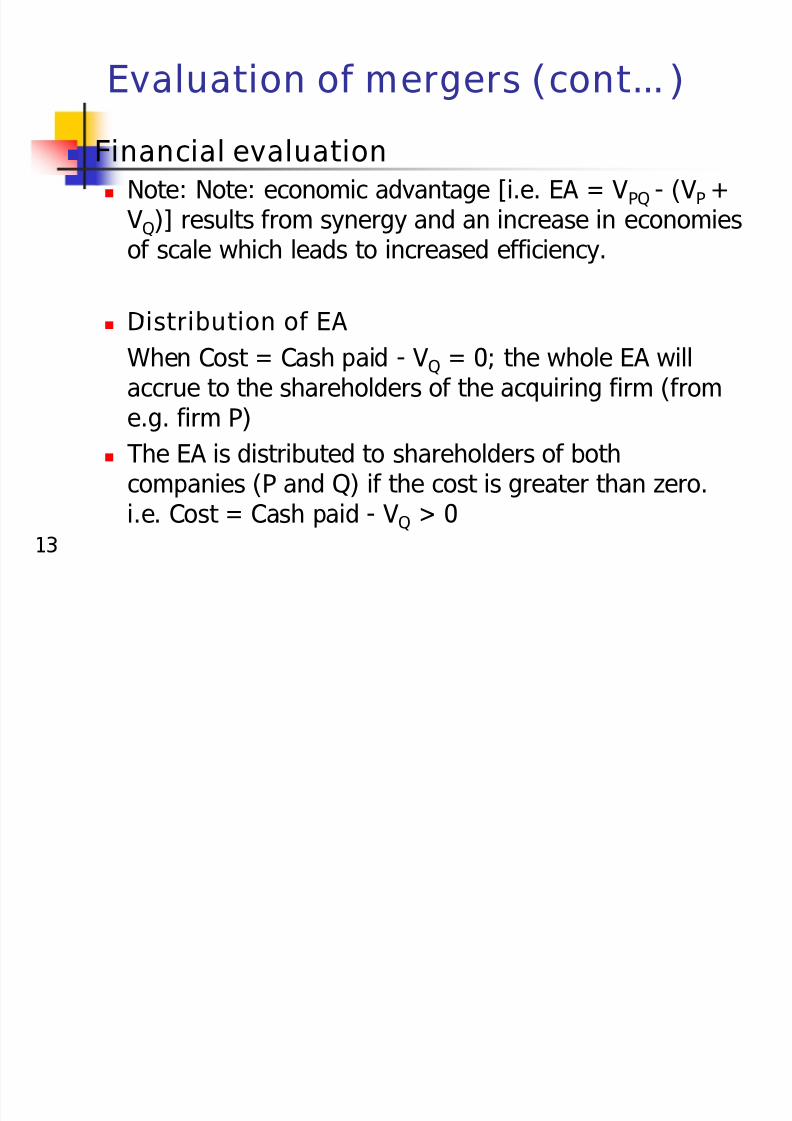

Note: Note: economic advantage [i.e. EA = VPQ - (VP + VQ)] results from synergy and an increase in economiesof scale which leads to increased efficiency.

Distribution of EA

When Cost = Cash paid - VQ = 0; the whole EA willaccrue to the shareholders of the acquiring firm (from

e.g. firm P) The EA is distributed to shareholders of both

companies (P and Q) if the cost is greater than zero.i.e. Cost = Cash paid - VQ > 0

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 14/29

14

Evaluation of mergers (cont) Financial evaluation

Example:

Firm P Firm Q

Market value Tshs. 18,000,000 3,000,000

Number of outstanding shares 120,000 50000

Market value per share Tshs. 150 60

Firm P considers acquiring firm Q. Value of P after merger = Tshs

25,000,000. Firm P requires to pay Tshs 4,500,000 to acquire firm Q.

What is the economic advantage of merger? Estimate the new market

value per share of acquiring company (i.e. P) after merger),

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 15/29

15

Evaluation of mergers (cont) Financial evaluation

Example: Estimation of EA and the new market value of shares of acquiring company (i.e. P) after merger

P after

merger Firm P Firm Q

Value of firm in Tshs. 25,000,000 18,000,000 3,000,000

EA [Value of Merger -(Value of

P + Value of Q) = Tshs. 4,000,000

Cash paid 4,500,000

Cost (cash - value of Firm Q) 1,500,000

NEA [EA - Cost] 2,500,000

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 16/29

16

Evaluation of mergers (cont)

Financial evaluation Example: Estimation of the market value per share of

acquiring company (i.e. P) after merger

P after

merger Firm P Firm QPresent Value of firms = Tshs 25,000,000 18,000,000 3,000,000

NEA [EA - Cost] (accrued to

shareholders of acquiring Firm) Tshs. 2,500,000

Total value of shares Tshs. 20,500,000

Total number of shares 120,000

Market value per share Tshs 170.83

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 17/29

17

Evaluation of mergers (cont)

Financial evaluation

Example: In case Firm P decides to issue shares to firm Q insteadof paying cash.

Thus, shares are exchanged in the ratio of cash to be paid tocombine value of the merged firm.

Value of P after

merger

Value accrued

to Firm P

Value accrued to

Firm Q

Value tshs 25,000,000 20,500,000 4,500,000

Distribution in %_ 100 82 18

Number of shares X 120,000

NOTE: If 82% is 120,000 shares, what is the number of share for 100%.

Number of shares 146,341.463 120,000 26,341

Market value per share

Tshs 170.83

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 18/29

18

Evaluation of mergers (cont)

Financial evaluation

In practice, the number of shares exchanged may bebased on the current market price of the acquiring firm.

EG. Market price per share of Firm P = Tshs. 150

Cash to be paid to Q = 4,500,000.Instead of cash, number of shares to be issued to Q is

Number of shares = 4,500,000 /150

= 30,000

Value of P after merger

Value tshs 25,000,000

Total number of shares 150,000

Market value per share Tshs 166.67

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 19/29

19

Evaluation of mergers (cont)

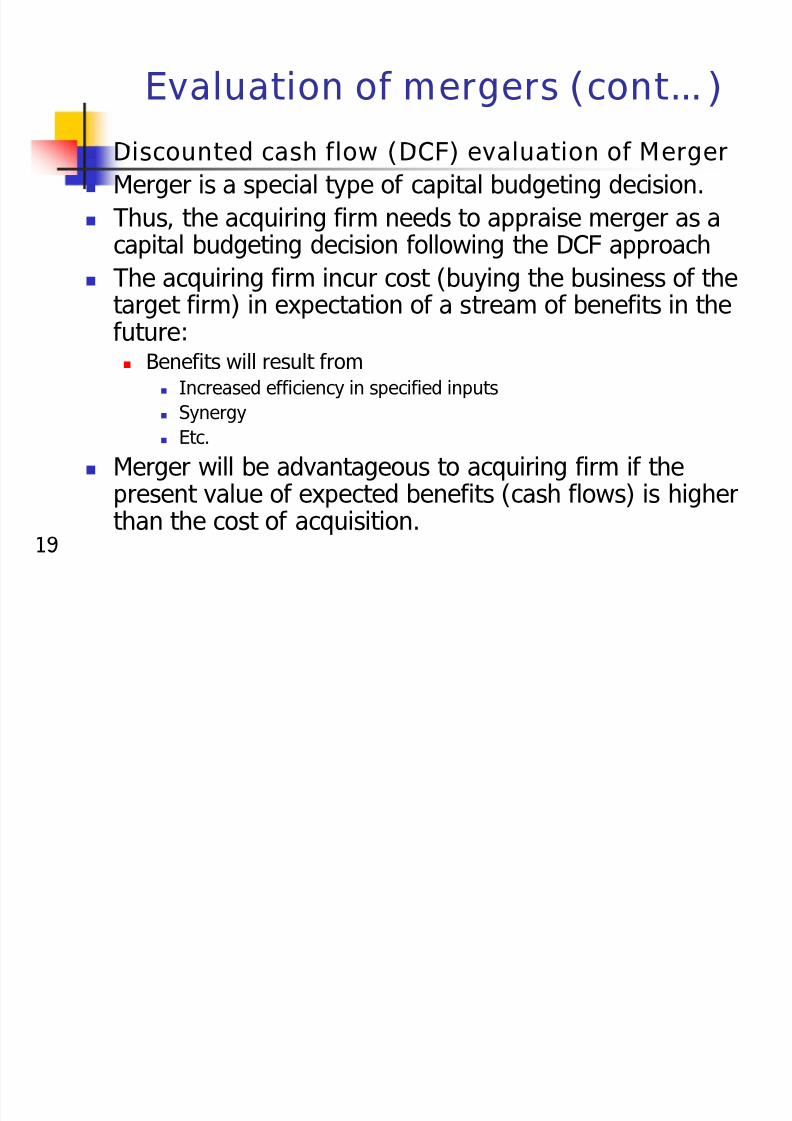

Discounted cash flow (DCF) evaluation of Merger

Merger is a special type of capital budgeting decision.

Thus, the acquiring firm needs to appraise merger as acapital budgeting decision following the DCF approach

The acquiring firm incur cost (buying the business of thetarget firm) in expectation of a stream of benefits in thefuture: Benefits will result from

Increased efficiency in specified inputs

Synergy Etc.

Merger will be advantageous to acquiring firm if thepresent value of expected benefits (cash flows) is higherthan the cost of acquisition.

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 20/29

20

Evaluation of mergers (cont)

Discounted cash flow (DCF) evaluation ofMerger

Information required:

Estimation of cash-flows (NCF)

NCF = EBIT (1-t) + Dep - NWK - CAPEX Dep = Depreciation

NWK = Change in Net working capital

CAPEX = Change in capital expenditure

Timing of cash flows

Discount rate: Mostly used one is the cost of capital of the target firm.

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 21/29

21

Evaluation of mergers (cont)

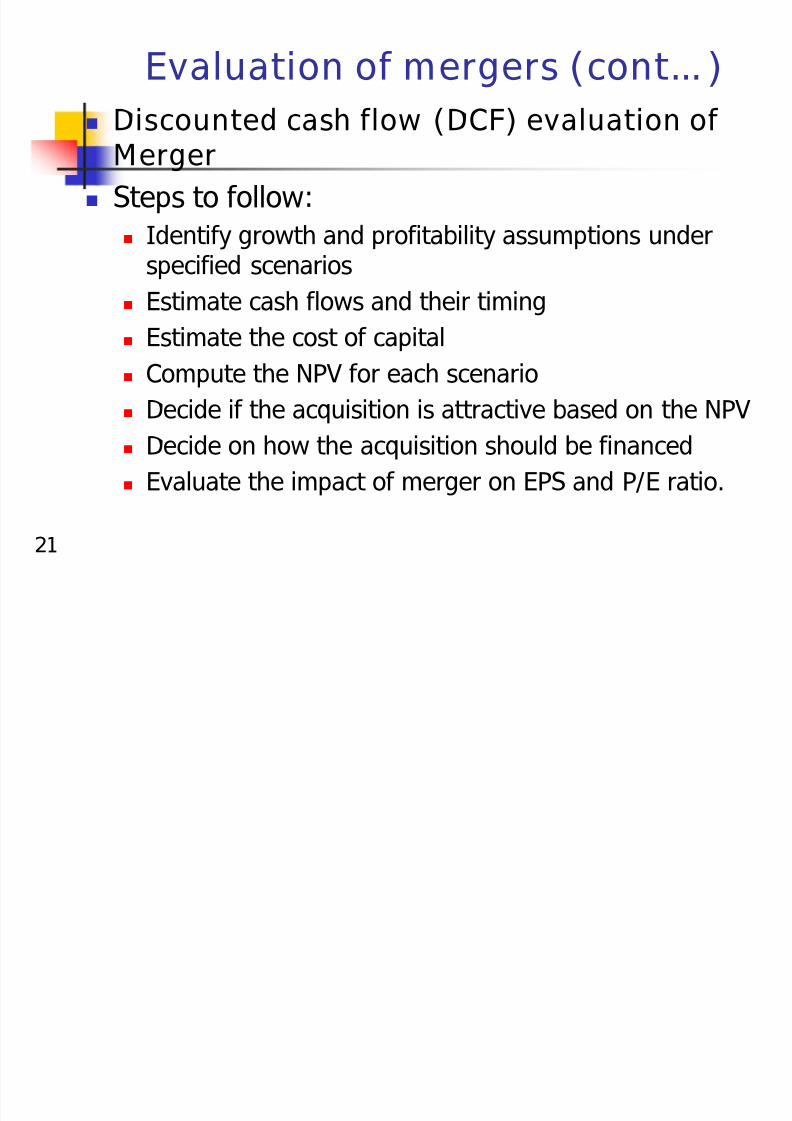

Discounted cash flow (DCF) evaluation ofMerger

Steps to follow:

Identify growth and profitability assumptions under

specified scenarios Estimate cash flows and their timing

Estimate the cost of capital

Compute the NPV for each scenario

Decide if the acquisition is attractive based on the NPV Decide on how the acquisition should be financed

Evaluate the impact of merger on EPS and P/E ratio.

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 22/29

22

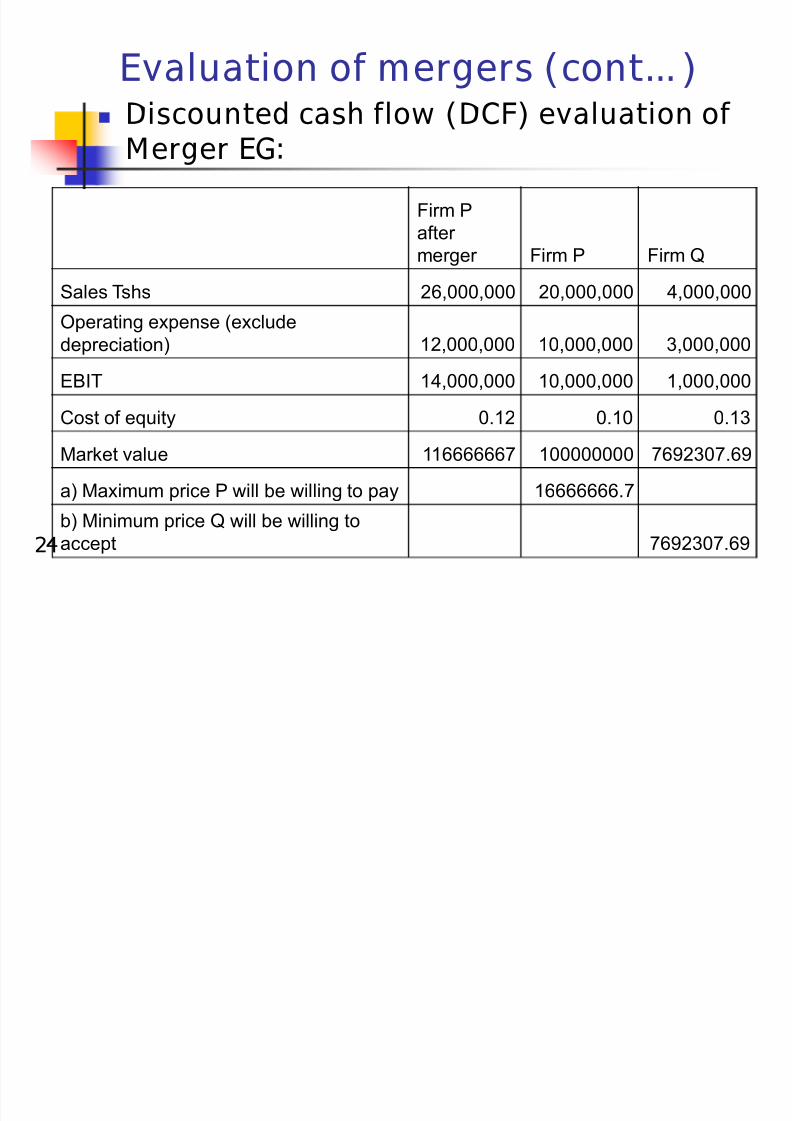

Evaluation of mergers (cont) Discounted cash flow (DCF) evaluation

of Merger EG:Firm P Firm Q

Sales Tshs 20,000,000 4,000,000

Operating expense (exclude depreciation) 10,000,000 3,000,000

EBIT 10,000,000 1,000,000Other info.

Outstanding shares 50,000 5,000

Cost of equity 0.10 0.13

Firms are financed by equity onlyEarnings will continue to be the same indefinitely (thus the cash flow are

perpetual)

Merger will results to an increase of sales (combined sales of P and Q) by Tshs 2

M, and a decrease of operating costs (combined) by Tshs 1 M.

If P's shareholders would require a return of 12% per annum if take-over of Q issuccessful answer the following questions

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 23/29

23

Evaluation of mergers (cont) Discounted cash flow (DCF) evaluation of

Merger EG:

a) What is the maximum price which P will be willing to pay

for Q?

b) what is the minimum price shareholders of Q would be

willing to accept?

c) if the agreed price is Tshs 10 M, estimate the % of total

number of shares which P will issue to Q.

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 24/29

24

Evaluation of mergers (cont) Discounted cash flow (DCF) evaluation of

Merger EG:

Firm P

after

merger Firm P Firm Q

Sales Tshs 26,000,000 20,000,000 4,000,000

Operating expense (exclude

depreciation) 12,000,000 10,000,000 3,000,000

EBIT 14,000,000 10,000,000 1,000,000

Cost of equity 0.12 0.10 0.13

Market value 116666667 100000000 7692307.69

a) Maximum price P will be willing to pay 16666666.7

b) Minimum price Q will be willing to

accept 7692307.69

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 25/29

25

Evaluation of mergers (cont)

EG. of financing options:

Cash

Exchange of shares Cash and shares

Shares and debt.

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 26/29

26

Evaluation of mergers (cont)

Cash as an option:

It does not cause any dilution of EPS andownership (which means control) of acquiringcompanys shareholders,

Not likely to cause wide a fluctuation of shareprice of a merger

Exchange of shares as an option:

It cause dilution of EPS and ownership (whichmeans control)

Likely to cause a wide fluctuation of share price

of a merger

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 27/29

27

Merger tactics

In the process of acquisition, the acquirer and target firm may agree on the on

the decision to merge,

the acquirer and management of the target firmmay sometimes disagree on the decision. In thisrespect, the acquirer may use the followingapproaches:

A proxy fight: The acquirer decides to seek the support of

the target firms shareholders at their annual meeting A tender offer: The acquirer makes an offer directly to the

target firms shareholders. The offer is made at valueshigher than the current market price per share.

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 28/29

28

Defensive tactics

How the management can defend their firmfrom being taken over,

Persuade the management that acquisition is not fortheir best interests,

increase dividend immediately,

Delay action deliberately

Seek a rival bid from a friendly company

Spread information about the negative performanceof the acquirer

8/6/2019 TOPIC 6 Acquisitions, Corporate Restructuring

http://slidepdf.com/reader/full/topic-6-acquisitions-corporate-restructuring 29/29

29

Corporate reorganization

Causes of financial distress Technical insolvency: The firm is unable to

meet its obligations as they fall due.

Bankruptcy: The market value of the firmsassets is less than its liabilities, and thusowners equity is negative.