Download - Transforming Health Care Delivery

René Lerer, M.D. President, GuideWell

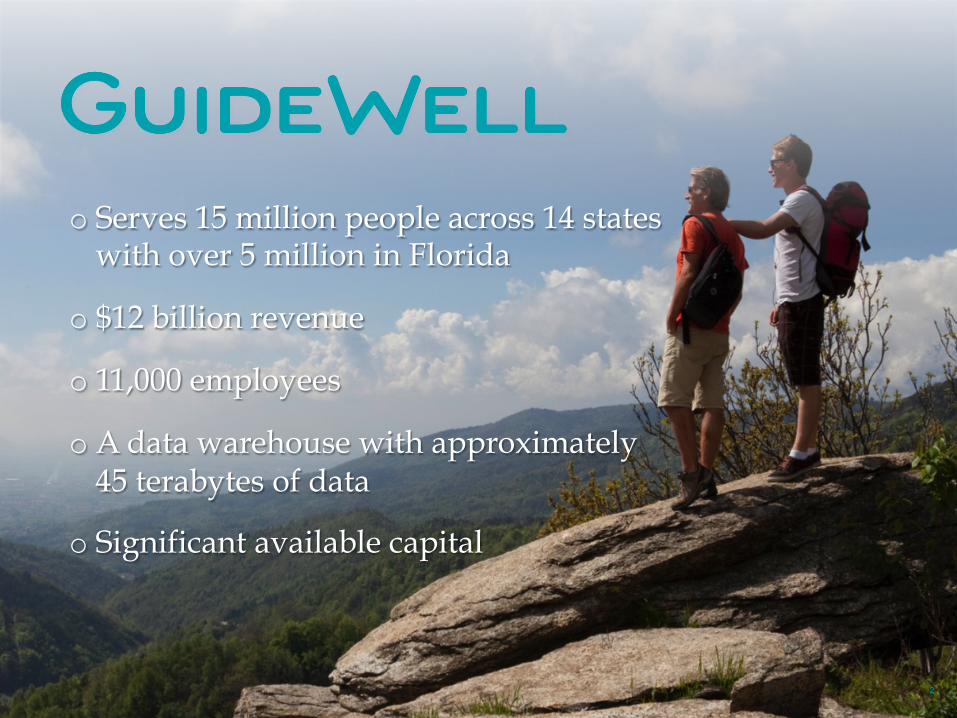

o Serves 15 million people across 14 states with over 5 million in Florida

o $12 billion revenue

o 11,000 employees

o A data warehouse with approximately 45 terabytes of data

o Significant available capital

2

Health Insurance Business

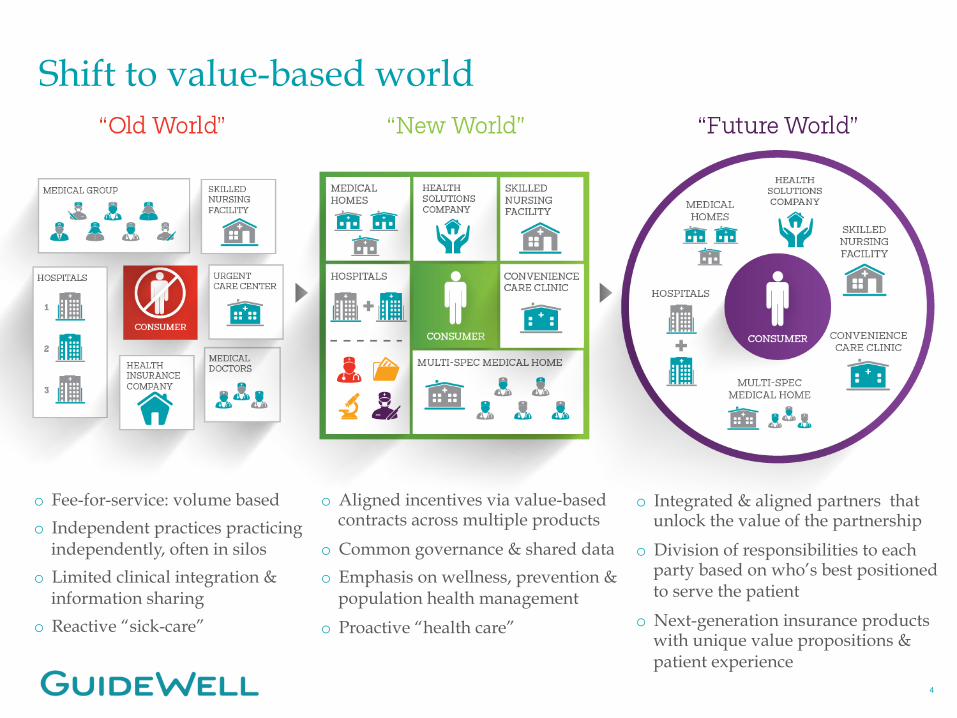

Shift to value-based world

4

o Fee-for-service: volume based

o Independent practices practicing independently, often in silos

o Limited clinical integration & information sharing

o Reactive “sick-care”

o Aligned incentives via value-based contracts across multiple products

o Common governance & shared data

o Emphasis on wellness, prevention & population health management

o Proactive “health care”

o Integrated & aligned partners that unlock the value of the partnership

o Division of responsibilities to each party based on who’s best positioned to serve the patient

o Next-generation insurance products with unique value propositions & patient experience

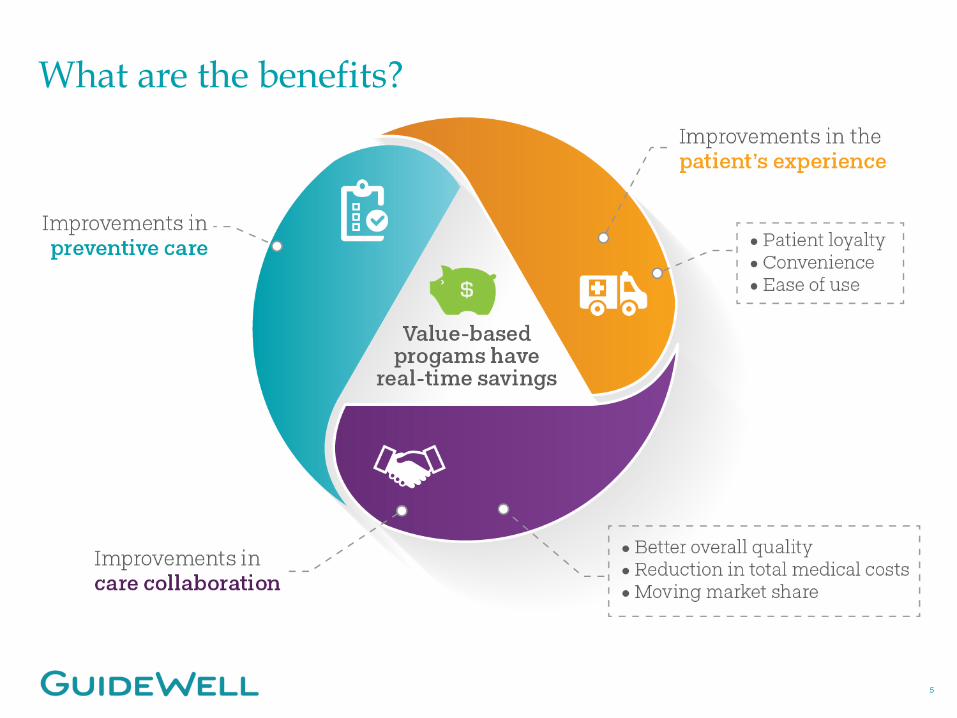

What are the benefits?

5

o Create value from clinical integration and physician acquisitions

o Better access to longitudinal data & real time information on patient populations

o Less “mother-may-I” care management

o Better financial alignment with payors and less zero-sum gain negotiations

What hospitals expect

6

o Reduced bad debt from patient liability

o Solutions that reduce the number of Floridians without insurance coverage

o Ambulatory care services (rad, lab, surg) in-migration vs. out-migration

o Support to transition from volume to value

o Serve as patient’s health care quarterback in a model that makes it financially viable to do so

o Improved cost and quality data to make more informed referral decisions for patients

o Reduced bad debt from patient liability

What physicians expect

7

o Less “mother-may-I” care management

o Technology and back-office solutions that allow the option for practices to remain independent in an industry that is rapidly consolidating

o More patient time and less administrative hassle

o Support with coding and documentation for accurate risk adjustment and STARs performance

o Leverage provider partners with feet on the street, multidisciplinary care management models for high-risk patients

o Engaged primary care partners and select specialists to serve as the patient’s medical home

o Mitigation of unit cost pressure

What payors expect

8

o Less provider consolidation for the wrong reasons / price arbitrage

o Delivery partners able to turn their data into patient-specific action for STARs scores

o Launch next-generation insurance products/solutions that leverage the value of accountable care

9

Physician-Centered Value-Based Care

Accountable Care Organizations (ACOs) with Major Health System

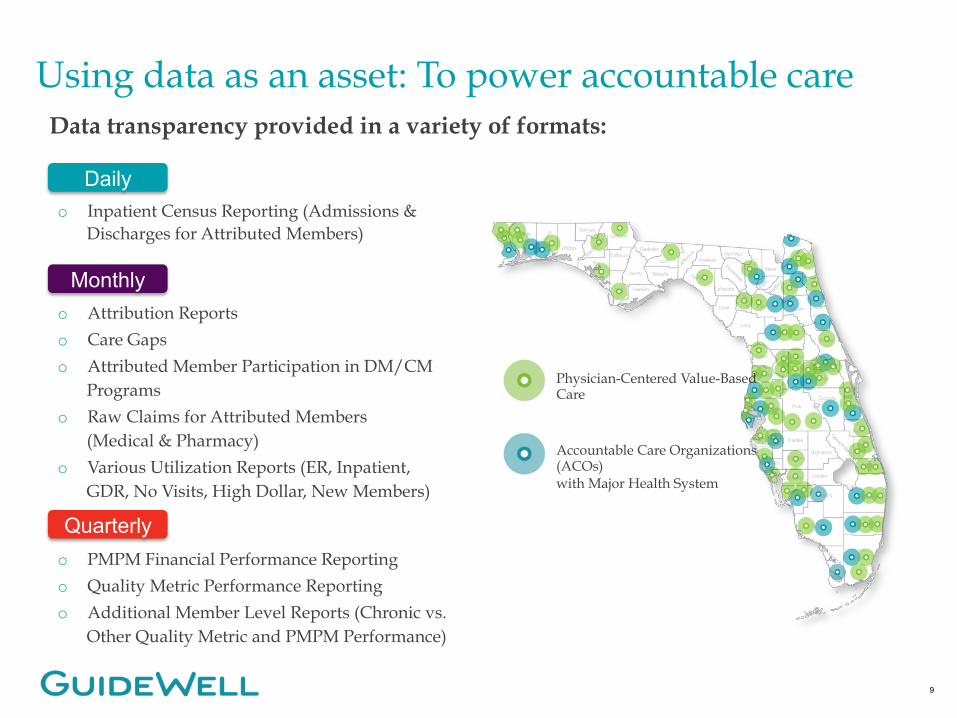

Using data as an asset: To power accountable care Data transparency provided in a variety of formats:

Daily o Inpatient Census Reporting (Admissions &

Discharges for Attributed Members)

Monthly o Attribution Reports o Care Gaps o Attributed Member Participation in DM/CM

Programs o Raw Claims for Attributed Members

(Medical & Pharmacy) o Various Utilization Reports (ER, Inpatient,

GDR, No Visits, High Dollar, New Members)

Quarterly o PMPM Financial Performance Reporting o Quality Metric Performance Reporting o Additional Member Level Reports (Chronic vs.

Other Quality Metric and PMPM Performance)

What we are looking for in a partner

10

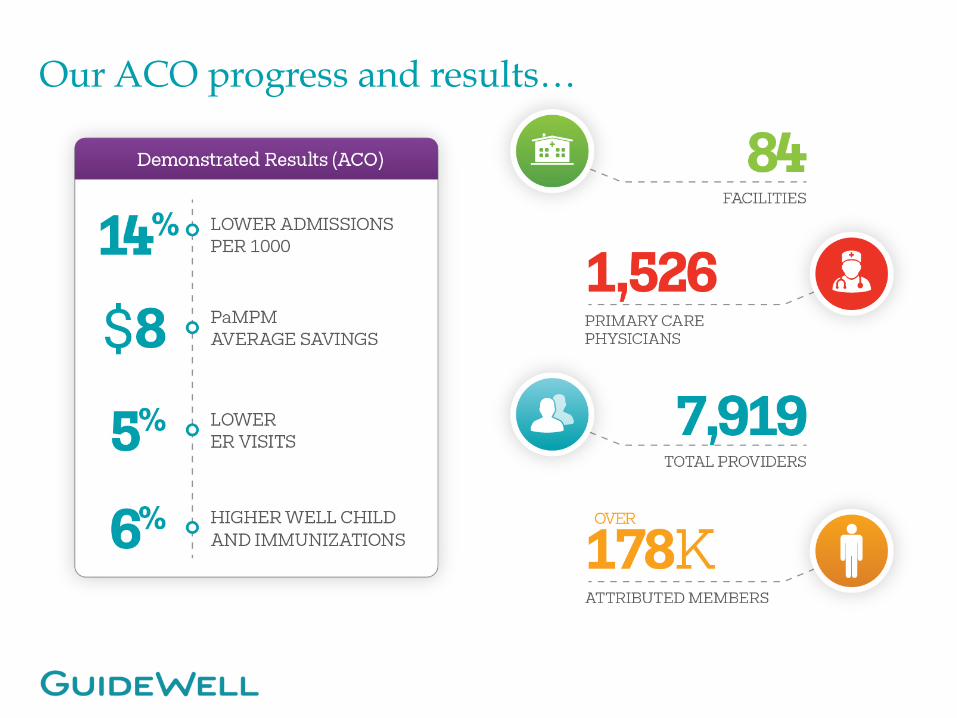

Our ACO progress and results…

o Industry consolidation: Hospitals, Physicians and Payors – What is the impact to the consumer?

o A rapidly growing B2C world where consumers’ expectations are very different than employers’

– How do we meet their needs ?

o The role of: – Telehealth and remote monitoring – Retail health: CVS, Walgreens, Walmart, Target, etc. – Digital engagement, navigation and decision support

o Where does disruptive innovation come from and can the establishment disrupt itself?

o ACO structures – Hospital vs. non-hospital led ACOs

Open issues for the Industry

12