Download - ©UFS Bankhall Advisor Forums Retirement Planning: Risks and Rewards MetLife Europe Limited

©UFS

Bankhall Advisor Forums

Retirement Planning: Risks and Rewards

MetLife Europe Limited

2

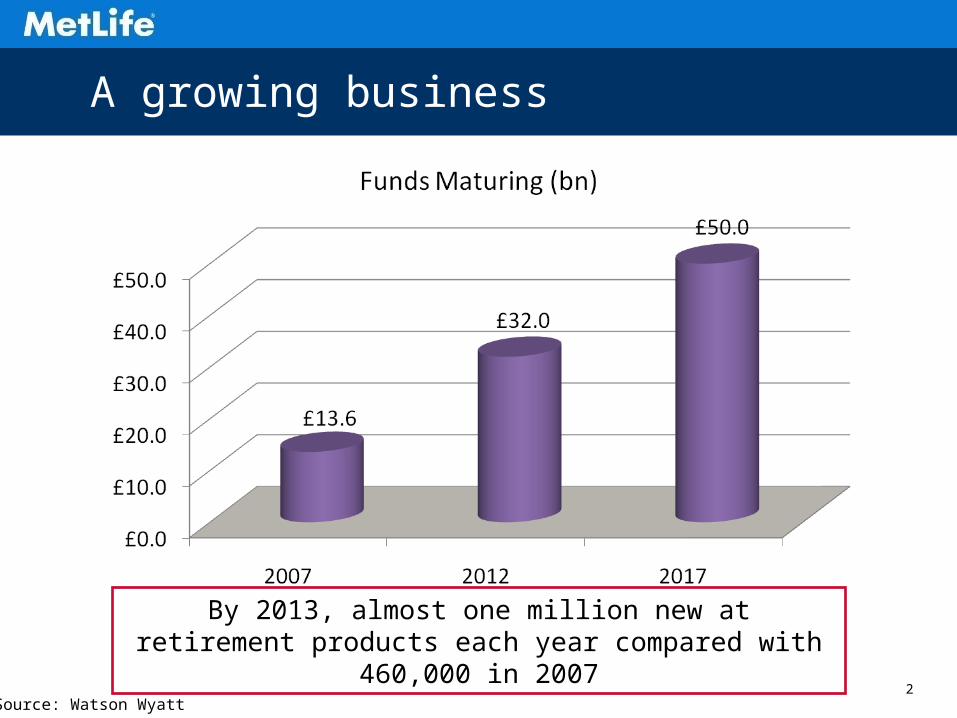

A growing business

Source: Watson Wyatt

By 2013, almost one million new at retirement products each year compared with 460,000 in 2007

3

Why you should invest your time

• Retirement income advice set to explode

• Move from state support to individual reliance

• Baby boomers

• DB to DC

• Personal pensions 1988

• UK solutions are complex and most require advice

4

Guarantees are a growing opportunity

2001 2011

Source: Standard Life Investment Briefing May 2007

PP Ann

SIPP DD

Funds

Age

PP Ann

SIPPDD

VA

Funds

Age

5

Retirement Risks

• Risks facing retirees– Longevity

– Inflation

– Investment» Performance

» Timing

– Interest rates

– Health

• Amongst a number of others…

6

Life Expectancy at age 65United Kingdom

Government Actuaries Department, central cohort projection for 2003 and 2006

7

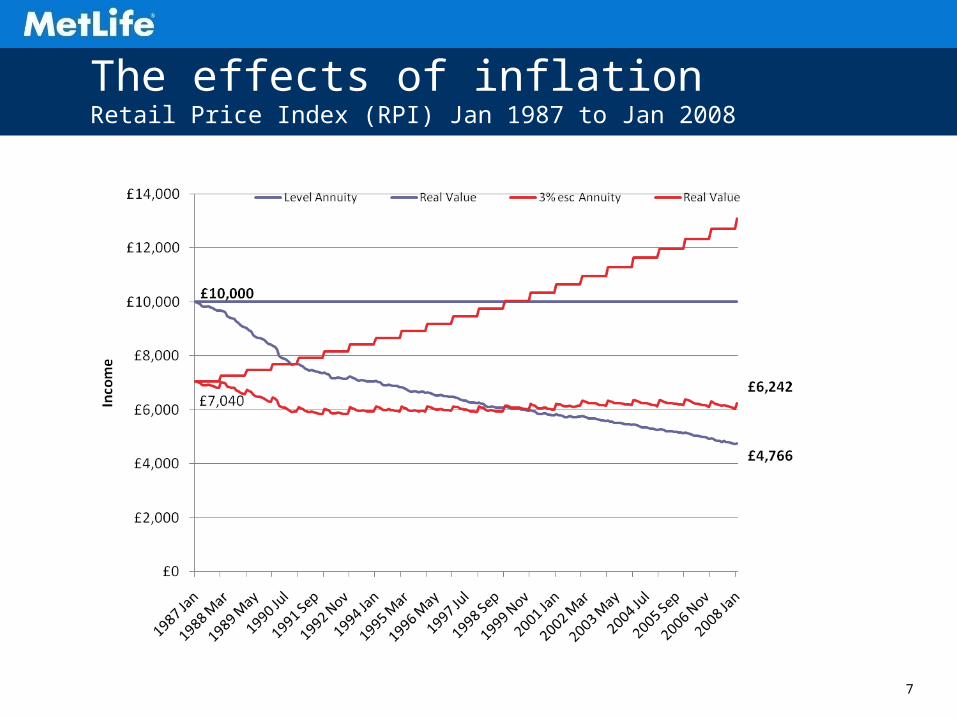

The effects of inflationRetail Price Index (RPI) Jan 1987 to Jan 2008

8

Running Out of Money6% investment growth per annum, £100,000 investment, income deducted annually in advance

9

FTSE All Share Index Total Return 1988-2007

11.53%

36.21%

-9.67%

20.80%

28.39%

-5.86%

23.92%

16.55%

23.56%

13.77%

24.20%

-5.92%

-13.22%

-22.68%

20.86%

12.80%

22.11%

16.80%

5.29%

20.43%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Source: Lipper 15th February 2008

The value of investments can fall as well as rise. Past performance is not a guide to future performance. You may get back less than you invested.

10

FTSE 100 Quarterly Trading Ranges

6,036 6,1335,987 5,987

6,444

6,732 6,717 6,7316,479

6,376

5,6375,6195,507 5,507

5,682

6,001

6,316

5,8596,071

5,4145,518

4,8194,600

5,000

5,400

5,800

6,200

6,600

7,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q32006 2007 2008

Source: Lipper Hindsight

11

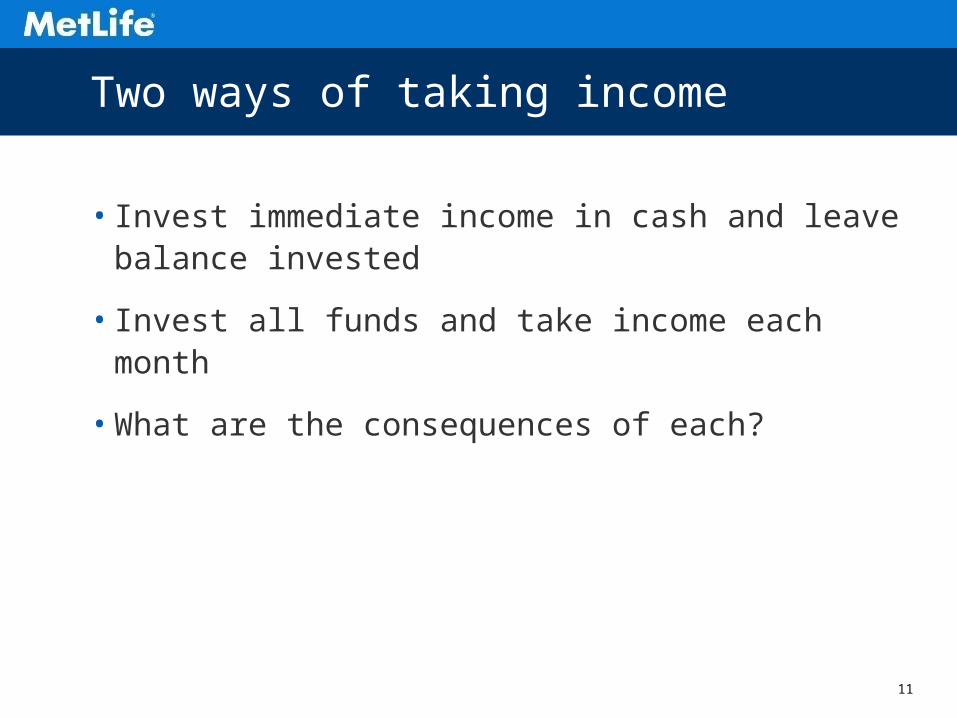

Two ways of taking income

• Invest immediate income in cash and leave balance invested

• Invest all funds and take income each month

• What are the consequences of each?

12

Invest all fundsHow much income really costs

Rising market

Falling market

£25,380

£36,274

Discounted cost over 5 years of £500 p.m. income at +7% p.a. and -7% p.a.

Gross cost of income £30,000

13

Set cash aside

DrawdownPension FundCritical Yield

8% per annum Equities75%

Cash25%

Critical Yield goes up

14

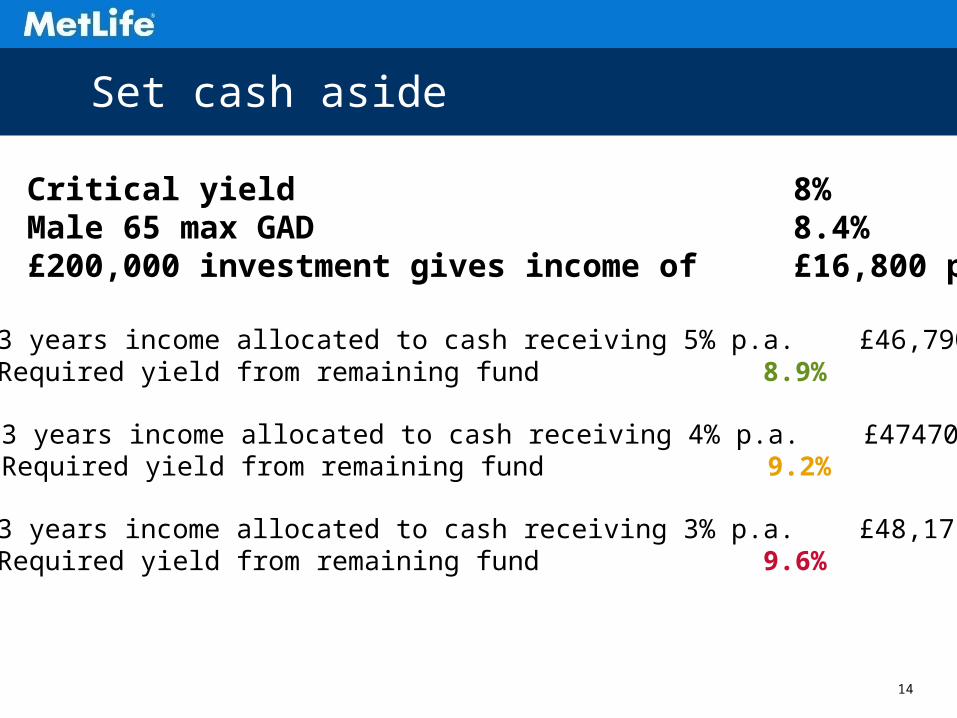

Set cash aside

Critical yield 8%Male 65 max GAD 8.4%£200,000 investment gives income of £16,800 p.a.

3 years income allocated to cash receiving 5% p.a. £46,790Required yield from remaining fund 8.9%

3 years income allocated to cash receiving 3% p.a. £48,171Required yield from remaining fund 9.6%

3 years income allocated to cash receiving 4% p.a. £47470Required yield from remaining fund 9.2%

15

Investment Timing£500,000 invested with £25,000 income taken annually and constant 6% per annum growth

The figures above show the return for the income taken at the growth rate shown. They do not represent any particular investment or portfolio of investments.These figures are for illustrative purposes only and cannot be guaranteed. They are not a recommendation or advice as to how markets will perform.

16

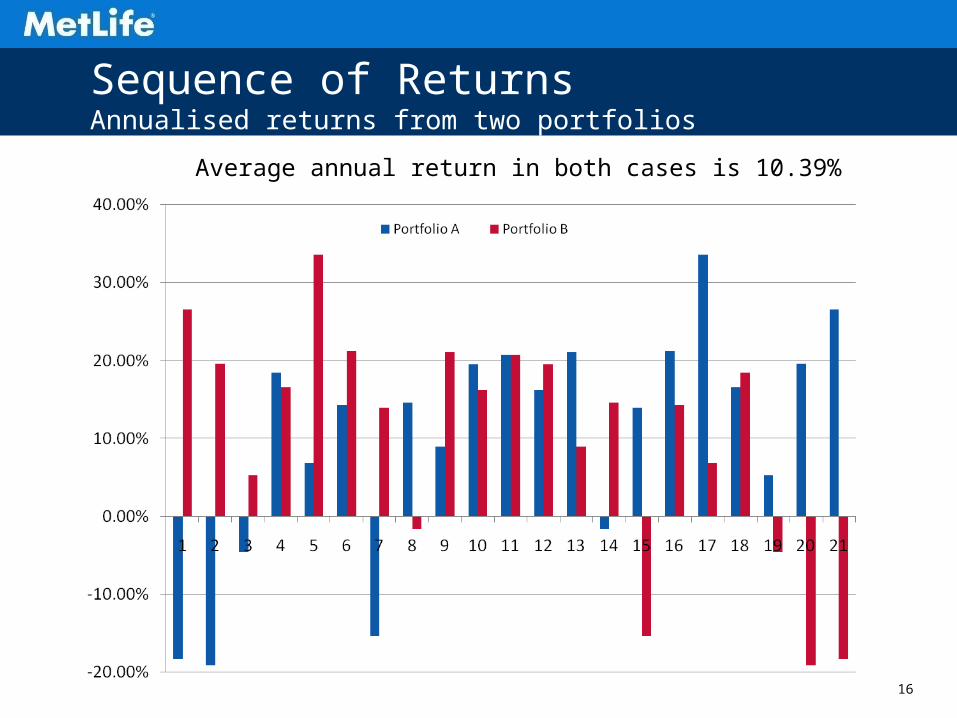

Sequence of ReturnsAnnualised returns from two portfolios

Average annual return in both cases is 10.39%

17

Sequence of ReturnsAnnualised returns from two portfolios

The two portfolios, £100,000 invested with £5,000 income increasing at 3.5% per annum taken annually in advance

18

You Tailor Their Pension, Not Us

Base Product

Product

Investment

Guarantees

Options

Index Funds

Index Portfolios

Goldman Sachs

Managed portfolios

SIPP

Capital Guarantee

Deferred Income

Guarantee

Immediate Income

Guarantee

Fund Switching

Auto Rebalancing

CustomerAgreedRemuneration

Trail Commission

Initial Commission

Fee

19

Applicable at every stage of retirement planning

Accumulation ConsolidationPre

RetirementRetirement

Deferred Income Guarantee

Dea

th

Capital Guarantee

Income Guarantee

20

Capital GuaranteeLock-ins every three years to ensure value at end of term

Secure ReviewFund Value Annual Growth

21

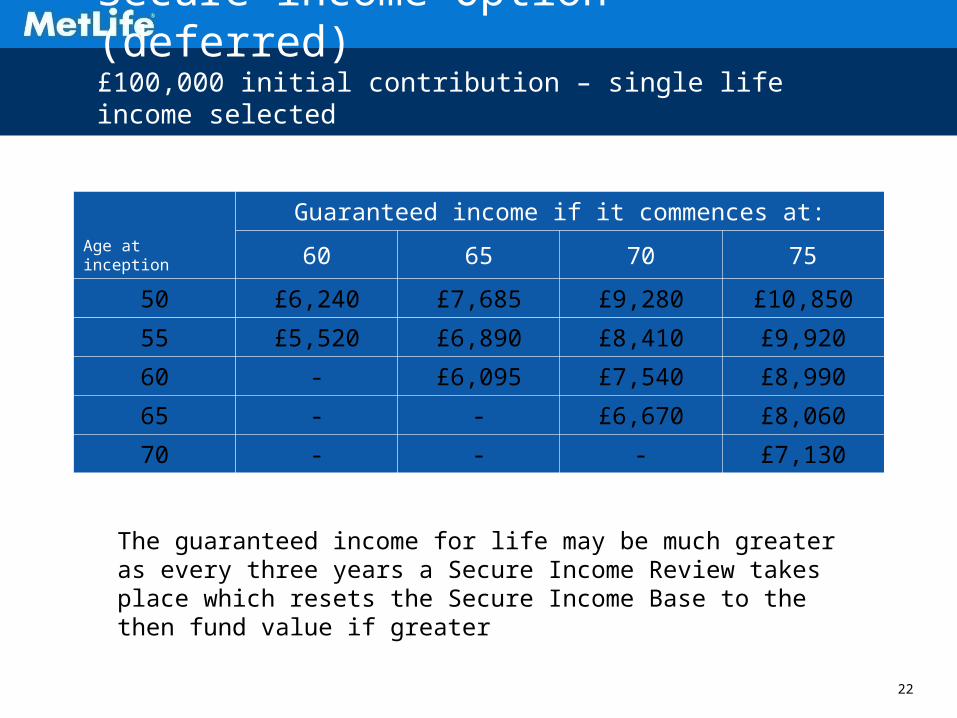

Secure Income Option (deferred)

• The Secure Income Option allows you to guarantee your income but defer the time when you start

• For each year of deferment you will increase the Secure Income Base by 3% of the initial contribution

• Every three years the Secure Income Base can increase further with the Secure Income Review

• This means that clients can have certainty about what income they will receive in the future

22

Secure income Option (deferred)£100,000 initial contribution – single life income selected

Age at inception

Guaranteed income if it commences at:

60 65 70 75

50 £6,240 £7,685 £9,280 £10,850

55 £5,520 £6,890 £8,410 £9,920

60 - £6,095 £7,540 £8,990

65 - - £6,670 £8,060

70 - - - £7,130

The guaranteed income for life may be much greater as every three years a Secure Income Review takes place which resets the Secure Income Base to the then fund value if greater

23

Deferred Income Guarantee3% increases guaranteed plus lock-ins where market falls at the end

Secure Income ReviewFund Value Annual Growth Secure Income Base

24

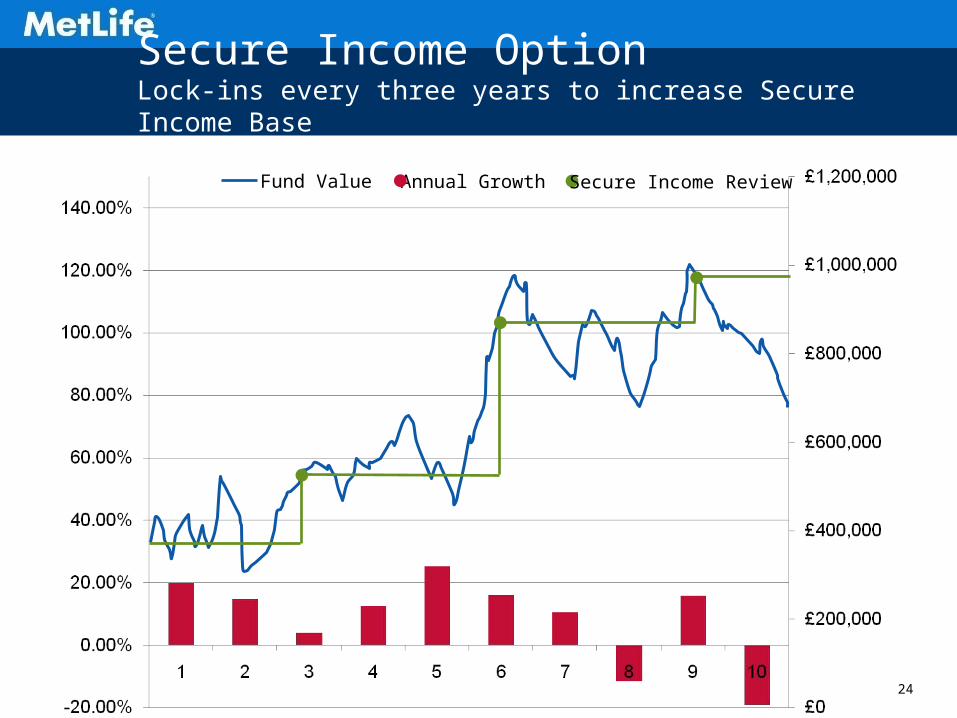

Secure Income OptionLock-ins every three years to increase Secure Income Base

Secure Income ReviewFund Value Annual Growth

25

Overcoming GAD Limits

• GAD limits the amount of income which can be taken from a drawdown fund

• Limits are:– 0% - 120% of Basis Amount before age 75

– 55% - 90% of Basis Amount for age 75 or over

• Could potentially cause income to be reduced when under guarantee

26

Fund level for GAD calculation

Difference between fund value and GAD

value made up by ‘notional units’

Overcoming GAD Limits

27

Summary

• Clients face many risks in retirement

• Individual advice is essential

28

MetLife Corporate Video - Rosy

This presentation has been provided to recipients for information only and has not been approved as a financial promotion. Notwithstanding the foregoing, this presentation is only being provided to professional financial advisers.

This presentation does not constitute an offer or inducement to purchase or subscribe for securities in a product or fund. The information in this presentation may not be complete and may be changed, modified or amended at any time and is not intended to, and does not, constitute any representations and warranties of MetLife Europe Limited. The information contained in this presentation is intended to provide general information only and does not take into account individual objectives,

financial situation or needs.

All reasonable care has been taken in relation to the preparation and collation of this presentation. Except for statutory liability which may not be excluded, no member of MetLife accepts responsibility for any loss or damage resulting from the use of or reliance on this presentation by any person. The information is taken from sources

which are believed to be accurate but no member of MetLife accepts any liability of any kind to any person who relies on the information contained in it.

The copyright of this presentation and any documents supplied with it and the information contained therein is vested in MetLife. They should not be copied, reproduced or redistributed without prior consent.

Issued by MetLife Europe Limited, authorised by the Irish Financial Services Regulatory Authority and regulated by the Financial Services Authority for the conduct of its UK insurance business. Registered office: First Floor, Fitzwilton House, Wilton Place, Dublin 2. Registration number: 415123. UK branch address: One Canada

Square, London E14 5AA. UK branch registered number: BR008866.

Important information

29