www.efc.unc.edu

Understanding Financial

Documents

Financial Training and Grant Writing Workshop for Mayors

of Underserved Communities

Stacey Isaac Berahzer

October 11, 2012

Georgia College and University

Macon, GA

Outline

• Fund Accounting

• Financial Reporting

• Getting Information from Financial Reports

2

FUND ACCOUNTING

3

Government Accounting

• GAAP – Generally Accepted Accounting

Principles

– establishes the rules & conventions that guide

the form and content of general-purpose

financial statements

• GASB – Governmental Accounting

Standards Board

– the primary standard-setting authority for

gov’t, excluding the federal gov’t

4

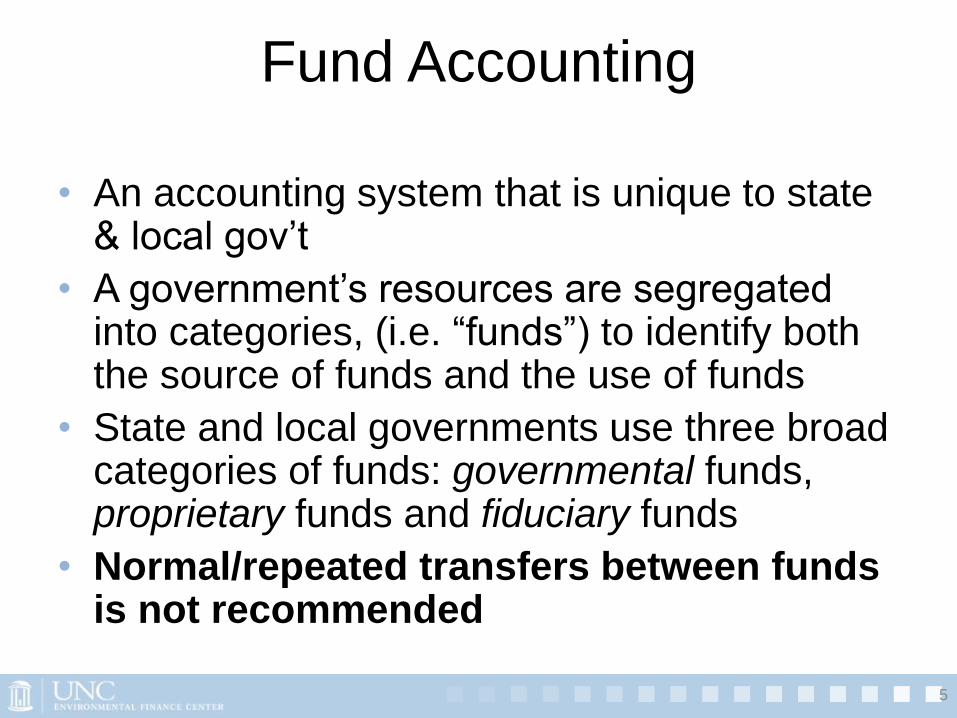

Fund Accounting

• An accounting system that is unique to state & local gov’t

• A government’s resources are segregated into categories, (i.e. “funds”) to identify both the source of funds and the use of funds

• State and local governments use three broad categories of funds: governmental funds, proprietary funds and fiduciary funds

• Normal/repeated transfers between funds is not recommended

5

Fund Accounting

FU

ND

S

Government

General

Special Revenue

Debt Service

Capital Projects

Permanent

Proprietary

Enterprise

Internal Service

Fiduciary …

6

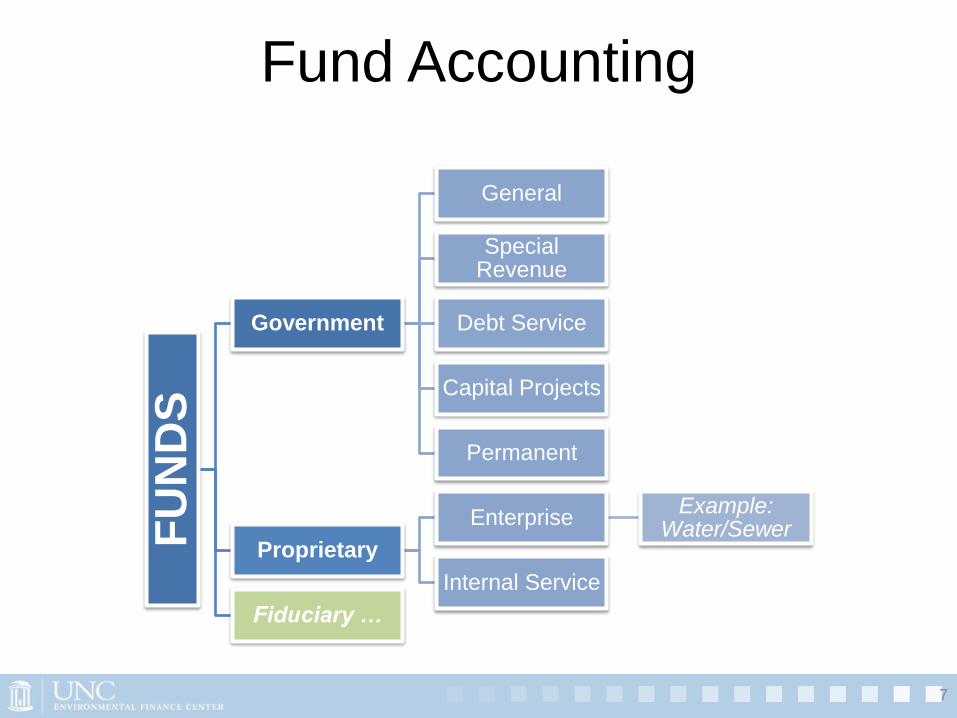

Fund Accounting

FU

ND

S

Government

General

Special Revenue

Debt Service

Capital Projects

Permanent

Proprietary

Enterprise Example:

Water/Sewer

Internal Service

Fiduciary …

7

Fund Accounting

• Examples of Government Funds:

– General Fund – each gov’t has one account for all resources that are not required to be accounted for in other funds. Includes most major gov’t functions such as police, fire, sanitation etc.

– special revenue – established to account for resources that are legally restricted for specific purposes, e.g. lottery money for education

– capital projects – used when buying/building major capital facilities

8

Exercise – “Fun with Funds”

Activity Fund(s)

Police

An electric utility system

Construction of a new wastewater

plant

Public Transit

Municipal motor vehicle pool

(maintenance)

9

Which fund(s) should be used to account for the

following activities:

FINANCIAL REPORTING

15

Depreciation - Revisited

• Loss of use & value; or

• “The systematic & rational allocation of the

cost of tangible noncurrent operating

assets over the period benefited by the

use of the asset”

Source: Government and Not-for-Profit Accounting: Concepts and

Practices, By Michael H. Granof, Saleha B. Khumawalas

16

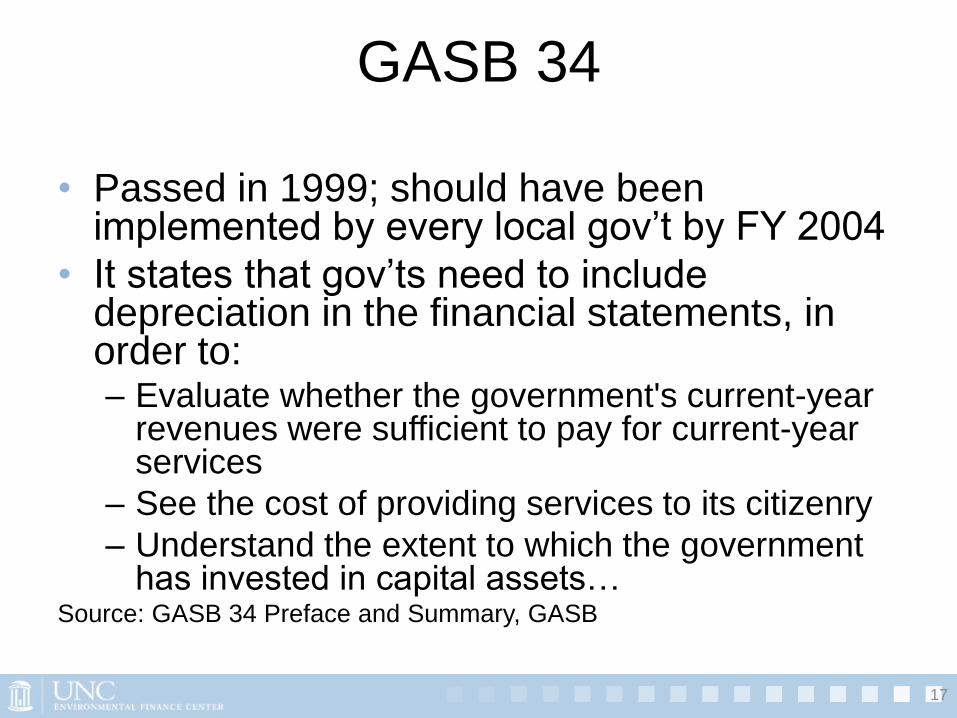

GASB 34

• Passed in 1999; should have been implemented by every local gov’t by FY 2004

• It states that gov’ts need to include depreciation in the financial statements, in order to: – Evaluate whether the government's current-year

revenues were sufficient to pay for current-year services

– See the cost of providing services to its citizenry

– Understand the extent to which the government has invested in capital assets…

Source: GASB 34 Preface and Summary, GASB

17

GASB 34

“Compliance with GASB 34 will be the single greatest element affecting daily lives for all Americans today.”

Source: web site advertisement for software provider

“GASB 34 is the "most significant

pronouncement in the history of financial reporting requirements for local governments in the United States." GASB 34 will have a major impact on the way that Municipalities manage all infrastructure assets.”

Source: web site for consulting services

“The inclusion of depreciation charges for which there is no actual cash expenditure-as a government expense distorts financial statements and reduces their values as a management tool.

Source: APWA Policy Statement adopted by APWA Board of Directors on 12/2/00

18

Software provider and Consulting Services say …

American Public Works Association says …

Capitalizable Asset

• Two years or more of useful life and has

materiality (e.g. cost $500 or more; or cost

$10,000 or more)

19

Financial Planning and Reporting Tools

• Annual reports

• Financial Statements

• Accounting reports

• CIPs

• Cash flow plans

• Annual budgets

• Performance measures

20

Planning Tools - Examples

• 10 Year Needs

• 5 Year Capital Improvement Plan

• 8 year Financial Plan

• 1 Year Budget

21

Budgeting

• Budget - An instrument to implement and

manage public policy by obtaining and

appropriating the necessary resources for

service delivery

• Budget Process – activities that

encompass the development,

implementation, and evaluation of the

budget for the provision of services

22

Budgeting Tools

• Inflationary Adjustment – converting

current dollars into constant (real) dollars

based on a selected index

• Consumer Price Index – an indicator that

measures the change in prices paid for a

fixed basket of goods and services with

constant quantity and quality as purchased

by average urban consumers

23

GFOA

• Government Finance Officers Association

• Offers awards in several categories for proper finance documents

• Mission – “to enhance and promote the professional management of governments for the public benefit by identifying and developing financial policies and best practices and promoting their use through education, training, facilitation of member networking, and leadership”

24

GETTING INFORMATION FROM

FINANCIAL REPORTS

25

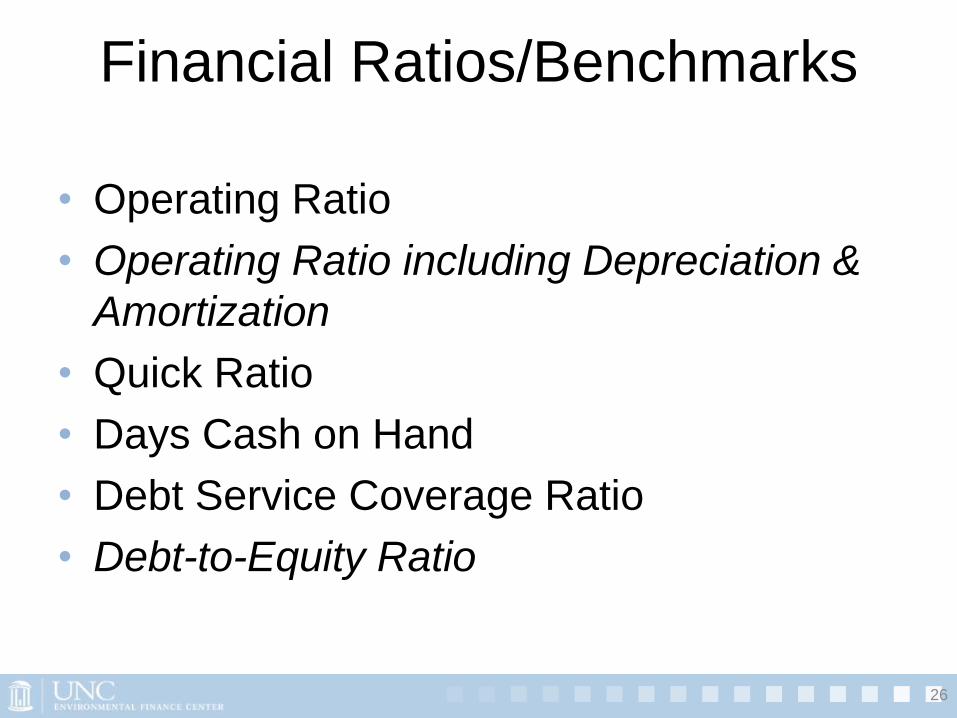

Financial Ratios/Benchmarks

• Operating Ratio

• Operating Ratio including Depreciation &

Amortization

• Quick Ratio

• Days Cash on Hand

• Debt Service Coverage Ratio

• Debt-to-Equity Ratio

26

Operating Ratio

A measure of self sufficiency.

The revenue you get from daily

operations, divided by

the expenditures or expenses you make to

keep operations running (see next slides)

Natural Benchmark: > 1.0

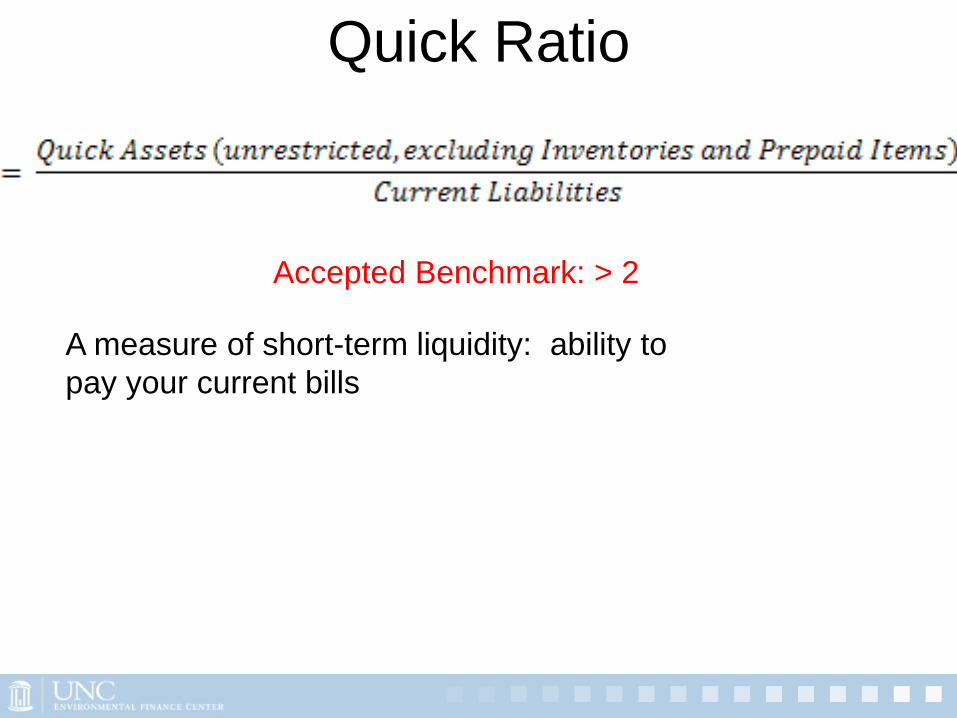

Quick Ratio

A measure of short-term liquidity: ability to

pay your current bills

Accepted Benchmark: > 2

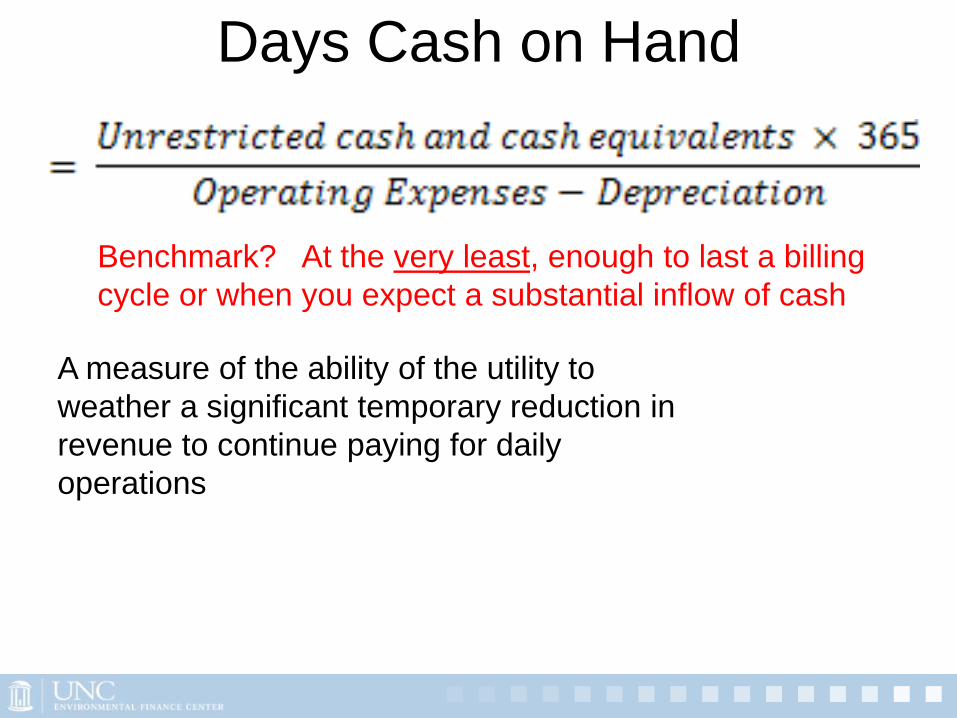

Days Cash on Hand

A measure of the ability of the utility to

weather a significant temporary reduction in

revenue to continue paying for daily

operations

Benchmark? At the very least, enough to last a billing

cycle or when you expect a substantial inflow of cash

Debt Service Coverage Ratio

A measure of the ability to pay debt service with operating

revenue:

Operating revenue left over after daily operation expenditures,

divided by

debt service

Natural Benchmark: > 1

Exercise – Reading Financial

Statements

• See Handout

31

Will post materials to:

http://efc.unc.edu/training.html

Stacey Isaac Berahzer

770-509-3887