1UPSCALE TECH-SAVVY MILLENNIALS Copyright © 2014 The Nielsen Company

U P S C A L E T E C H-S AV V Y M I L L E N N I A L S:SAVING AND INVESTMENT STRATEGIES AROUND THE WORLD

2 UPSCALE TECH-SAVVY MILLENNIALS

UPSCALE TECH-SAVV Y MILLENNIALS:SAVING AND INVESTMENT STRATEGIES AROUND THE WORLD

In Q3 2013, the Nielsen Global Survey of Saving and Investment

Strategies polled more than 30,000 Internet respondents in 60 countries

to evaluate how consumers around the world were preparing for current

and future financial expenses. Nielsen evaluated 16 different saving

and investment strategies used to fund 14 financial goals ranging from

unforeseen life events and shorter-term goals, such as unexpected

household emergencies and buying a house, to longer-term objectives,

such as saving for retirement and for their children’s future.

A majority of global respondents (almost 7 out of 10) believe they will

achieve their financial goals, yet only two of these seven think current

planning efforts are sufficient. In a nutshell, there is a growing global

consumer need to help guide and plan for the financial future.

Yet, savings is only half the story and must be examined in the context

of spending, especially in light of high inflation and rising food costs.

Despite higher income, North Americans report the lowest percentage

(9%) with the ability to spend freely, with 51 percent indicating they only

have enough money to cover shelter, food and the basics. In contrast,

Asians report the highest percentage (17%) with the ability to spend

freely, with 36 percent indicating they only have enough money to cover

shelter, food and the basics. And, the vast majority (85%) of global

consumers indicate that higher food costs impact their choice of grocery

products. This impacts spending in other industries, as well with global

consumers, indicating they would reduce spending on dining out (64%),

buying new clothes (55%), spending on snack foods (45%), paying for

recreation and entertainment (44%), and traveling on vacation (39%)

due to inflation and rising food costsi. And with all this spending, global

consumers need more help than ever to focus on saving for the future.

3UPSCALE TECH-SAVVY MILLENNIALS Copyright © 2014 The Nielsen Company

In this analysis, Nielsen has taken a deeper dive into the savings and

investment strategies and intentions of upscale, tech-savvy Millennials

in the U.S., Brazil, China and India to better understand the financial

values and goals of those with money to save in this up-and-coming

generation. Millennials have come of age in the direst economic

circumstances since the Great Depression, contending with high

unemployment, high student loans and an uncertain future. Financial

institutions that can connect with Millennials to build their financial

portfolios can help this young generation find financial security and

stability. Upscale Millennials represent the future of global economic

growth and prosperity.

Millennials are 77 million strong in the U.S., making up 24% of the

population, in line with the U.S. Baby Boomer generation. However

in emerging countries, Millennials make up an even larger portion of

the population and thus are even more important to focus efforts on.

Millennials make up 28% of the population in China and 30% of the

population in both Brazil and India. And these emerging countries are

among the most optimistic and confident, with consumer confidence

that exceeds the global average, indicating an openness and receptivity

to messaging from financial institutions. Not surprisingly, there is a

relationship between strong consumer confidence and the percent of

the population indicating they are able to live comfortably. India, for

example, has high consumer confidence indexing at 115 and the majority

of the population (56%) indicates they are able to live comfortably.

For the purposes of this

analysis, Nielsen has

defined upscale, tech-savvy

Millennials as respondents

between the ages of 18-34

with Internet access and

household income over the

75th percentile for survey

respondents. The general

Millennial population is

defined as respondents

between the ages of 18-34

with Internet access.

• United States:

Household Income

$70K+

• China: Household

Income $40K+

• Brazil: Household

Income $30K+

• India: Household

Income $30K+

20

40

60

80

100

120

140

10%

20%

30%

40%

50%

60%

HIGH CONSUMER CONFIDENCE, HIGH STANDARD OF LIVING

GLOBALAVERAGE

Con

sum

er C

onfid

ence

Inde

x

Perc

ent A

ble

to L

ive C

omfo

rtab

ly

U.S. BRAZIL CHINA INDIA

94

42%39%

31%

44%

56%

94 110 111 115

Source: Nielsen Global Consumer Confidence Study Q4 2013, Nielsen Global Survey of Inflation Intentions Q1 2013

4 UPSCALE TECH-SAVVY MILLENNIALS

M I L L E N N I A L S AV I N G S A N D F I N A N C I A L S T R AT E G I E SNielsen has found that globally, consumers’ future intentions to save

across the 14 financial goals examined were stronger than current savings

intentions with the exception of health. However, this is not the case

with upscale Millennials in the U.S., Brazil, China and India. Many of the

current goals Millennials are saving toward are reflective of their younger

lifestage – focusing on education to build their careers, starting families

and purchasing a home. And, there is a cultural and value component at

play that should not be ignored as it guides what Millennials in different

parts of the world are savings towards. Cultures who value clans and

families, like China and India, have a much more intergenerational

outlook in their savings and investment intentions.

Future savings intentions among upscale Millennials in the U.S. and

Brazil are strong across most financial goals. This strong future intention

for savings presents opportunity for education from financial institutions

to help meet these goals. Millennials in China and India are currently

saving for most financial goals, presenting opportunity for financial

institutions to actively guide these young consumers to help them meet

their financial goals.

Globally, health and unforeseen household emergencies are the top

overall savings priorities for consumers. Looking at generations, the

sentiments fluctuate. Health is among the top current savings goals for

upscale Millennials in the U.S., China and India but upscale Millennials

in Brazil are more focused on saving for a first-time home purchase,

unexpected household emergencies and higher education. Since public

health care is provided by the Brazilian government, Brazilian Millennials

may need to devote less of their savings towards health issues. Full

implementation of health care reform programs, including Obamacare

in the U.S., may impact the amount of savings devoted to health by

consumers in the future. While health care is provided in China and

India, Millennials may take on supplemental plans to care for their aging

parents. In the U.S., China and India, the general Millennial population,

who may have less of a safety net, are more likely to be saving for

unexpected household emergencies than the upscale segment.

5UPSCALE TECH-SAVVY MILLENNIALS Copyright © 2014 The Nielsen Company

U.S. MILLENNIALS: PLANNERS AND REALISTSMillennials in the U.S. – both upscale and in total – value higher

education and save toward this financial goal, with 43 percent of upscale

Millennials and 40 percent of total Millennials actively saving. Millennials

in the U.S. - are over twice as likely as the average U.S. consumer to

have student loans from their education. They are also saving for future

education for themselves or their children with educational IRA plans and

tax advantaged college savings plans.ii In addition to education, upscale

Millennials are also actively saving for their financial legacy (43%) and

health (43%), while the general Millennial population is saving for a

rainy day in case of job or income loss (34%) and unexpected household

emergencies (33%). Upscale Millennials plan to save in the future for loss

of job or income (57%) and unexpected household emergencies (57%)

but a higher proportion plan to save for personal luxury items like a car,

vacation, watch or handbag (63%). The general Millennial population

plans to save in the future for practical purposes like retirement (64%),

health (61%) and an upgraded property purchase (60%).

6 UPSCALE TECH-SAVVY MILLENNIALS

START UP A BUSINESS

FINANCIAL LEGACY

UNEXPECTED HOUSEHOLD EMERGENCIES

MARRIAGE

HEALTH ISSUES

SECOND-HOME/VACATION PROPERTY PURCHASE

CHILDREN’S FUTURE

HAVING A BABY

PERSONAL LUXURY PURCHASE

UPGRADED PROPERTY PURCHASE

HIGHER EDUCATION

LOSS OF JOB/INCOME

FIRST-TIME MAIN HOME PROPERTY PURCHASE

RETIREMENT FUND

I ACTIVELY SAVE NOW I PLAN TO SAVE IN THE FUTURE

TOTAL MILLENNIALS IN THE U.S.

27%64%

58%

59%30%

51%14%

60%19%

58%33%

56%34%

61%30%

59%28%

56%22%

39%40%

49%24%

51%22%

48%18%

22%

UPSCALE MILLENNIALSIN THE U.S.

23%33%

30%47%

37%33%

43%30%

43%43%

30%63%

43%47%

33%57%

33%57%

40%40%

23%43%

37%40%

30%47%

40%50%

Source: Nielsen Global Survey of Saving and Investment Strategies, Q3 2013

7UPSCALE TECH-SAVVY MILLENNIALS Copyright © 2014 The Nielsen Company

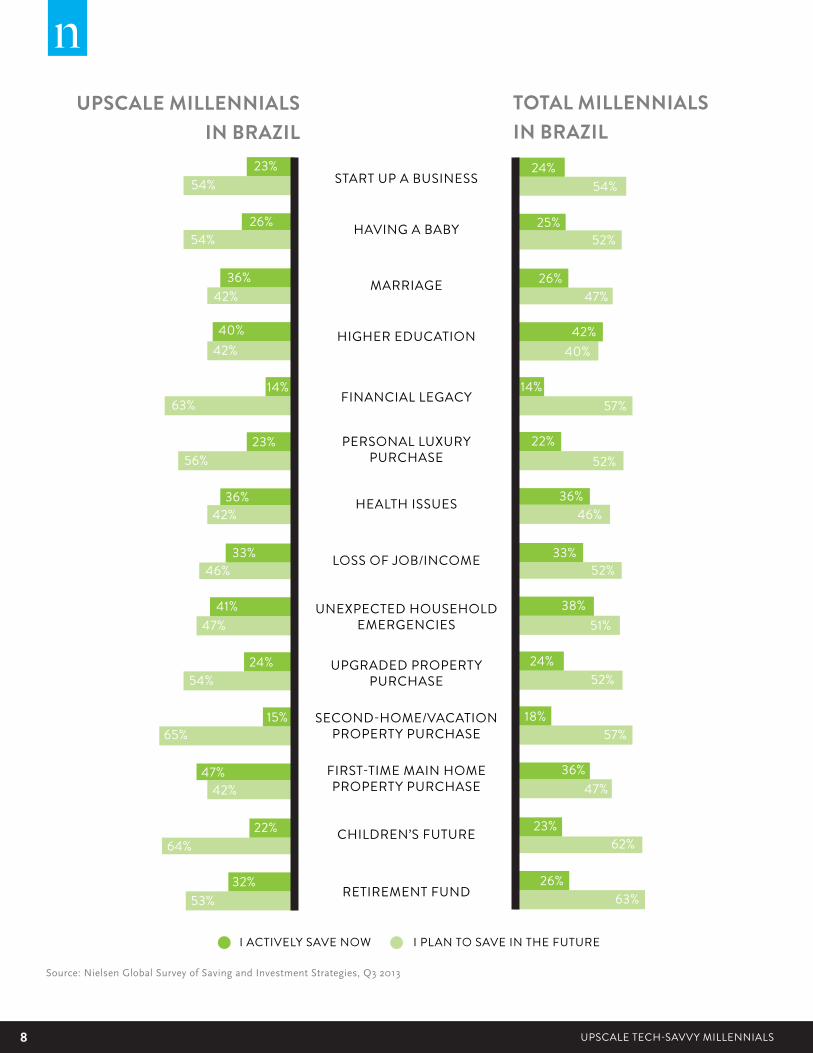

MILLENNIALS IN BRAZIL: HOME SWEET HOMEUpscale Brazilian Millennials are not distinct from the general Brazilian

Millennial population when it comes to saving. Both upscale Millennials

and the general Millennial population are actively saving money toward

similar financial goals reflective of their lifestage including a first-

time home purchase, unexpected household emergencies and higher

education. While Brazilian Millennials are actively saving for their first

home, they aspire for a second home/vacation property with 65 percent

of upscale Millennials and 57 percent of total Millennials planning to

save toward this financial goal. Brazilian Millennials also plan to save

toward their children’s future with 64 percent of upscale Millennials and

62 percent of total Millennials planning to save toward this financial

goal in the future. And while Millennials in total are planning to save for

retirement (63%), upscale Millennials are more focused on future saving

towards their financial legacy (63%).

8 UPSCALE TECH-SAVVY MILLENNIALS

START UP A BUSINESS

FINANCIAL LEGACY

UNEXPECTED HOUSEHOLD EMERGENCIES

MARRIAGE

HEALTH ISSUES

SECOND-HOME/VACATION PROPERTY PURCHASE

CHILDREN’S FUTURE

HAVING A BABY

PERSONAL LUXURY PURCHASE

UPGRADED PROPERTY PURCHASE

HIGHER EDUCATION

LOSS OF JOB/INCOME

FIRST-TIME MAIN HOME PROPERTY PURCHASE

RETIREMENT FUND

I ACTIVELY SAVE NOW I PLAN TO SAVE IN THE FUTURE

Source: Nielsen Global Survey of Saving and Investment Strategies, Q3 2013

UPSCALE MILLENNIALS IN BRAZIL

23%54%

26%54%

36%42%

40%42%

14%63%

23%56%

36%42%

33%46%

41%47%

24%54%

15%65%

47%42%

22%64%

32%53%

TOTAL MILLENNIALS IN BRAZIL

63%26%

23%62%

47%36%

57%18%

52%24%

51%38%

52%33%

46%36%

52%22%

57%14%

40%42%

47%26%

52%25%

54%24%

9UPSCALE TECH-SAVVY MILLENNIALS Copyright © 2014 The Nielsen Company

MILLENNIALS IN CHINA: HEALTH AND LUXURY FOCUSEDFinancial well-being in China has much to do with whether Millennials

are actively saving. Millennials in China are actively saving toward their

health, with 73 percent of upscale Millennials and 60 percent of total

Millennials saving toward this financial goal. Upscale Millennials in

China are aspirational, actively saving toward personal luxury items like

cars, vacations, watches or handbags (65%) and an upgraded property

purchase (59%). In contrast, the general Chinese Millennial population

is actively saving toward more practical goals like unexpected household

emergencies (48%) and a first-time home purchase (45%). Both upscale

Millennials and Millennials in total are focused on intergenerational

wealth and building a path for their families by planning to save towards

their financial legacy in the future, with 58 percent of upscale Millennials

and 53 percent of the general Millennial population planning to save

towards this goal. Upscale Millennials also plan to save toward higher

education (47%) and a second home/vacation home purchase (45%),

while the general Millennial population plans to save toward having a

baby (53%) and retirement (52%).

10 UPSCALE TECH-SAVVY MILLENNIALS

START UP A BUSINESS

FINANCIAL LEGACY

UNEXPECTED HOUSEHOLD EMERGENCIES

MARRIAGE

HEALTH ISSUES

SECOND-HOME/VACATION PROPERTY PURCHASE

CHILDREN’S FUTURE

HAVING A BABY

PERSONAL LUXURY PURCHASE

UPGRADED PROPERTY PURCHASE

HIGHER EDUCATION

LOSS OF JOB/INCOME

FIRST-TIME MAIN HOME PROPERTY PURCHASE

RETIREMENT FUND

I ACTIVELY SAVE NOW I PLAN TO SAVE IN THE FUTURE

Source: Nielsen Global Survey of Saving and Investment Strategies, Q3 2013

TOTAL MILLENNIALS IN CHINA

42%44%

33%53%

39%40%

41%44%

17%53%

41%44%

60%38%

37%48%

48%46%

43%47%

31%51%

45%39%

50%

40%52%

43%

UPSCALE MILLENNIALS IN CHINA

55%33%

43%41%

40%29%

37%47%

22%

65%27%

73%27%

46%41%

56%41%

59%34%

44%45%

30%

57%36%

43%53%

47%

58%

11UPSCALE TECH-SAVVY MILLENNIALS Copyright © 2014 The Nielsen Company

MILLENNIALS IN INDIA: SAVING FOR HEALTH AND CHILDRENUpscale Indian Millennials are much more likely to be actively saving

than the rest of their generation. Indian Millennials are actively saving

toward their health, with 66 percent of upscale Millennials and 56

percent of the general Millennial population saving towards this

goal. Upscale Millennials in India are also actively saving for their

children’s future (65%) and in case of loss of job or income (57%),

while the general Millennial population is actively saving for unexpected

household emergencies (48%) and higher education (47%). Both

upscale Indian Millennials and the general Millennial population plan

to save for personal luxury items and a second home/vacation home

in the future. And, 45 percent of upscale Millennials and 54 percent of

the general Millennial population intend to save toward personal luxury

items. Additionally, 42 percent of upscale Millennials and 52 percent of

the general Millennial population intend to save toward a second home/

vacation home. Upscale Millennials also plan to save toward a first-time

home purchase (41%) while the general Millennial population plans

to save toward having a baby (49%). Savings patterns among Indian

Millennials are quite similar to Chinese Millennials; however Indian

Millennials take intergenerational transfer of wealth to a greater extreme.

12 UPSCALE TECH-SAVVY MILLENNIALS

Source: Nielsen Global Survey of Saving and Investment Strategies, Q3 2013

START UP A BUSINESS

FINANCIAL LEGACY

UNEXPECTED HOUSEHOLD EMERGENCIES

MARRIAGE

HEALTH ISSUES

SECOND-HOME/VACATION PROPERTY PURCHASE

CHILDREN’S FUTURE

HAVING A BABY

PERSONAL LUXURY PURCHASE

UPGRADED PROPERTY PURCHASE

HIGHER EDUCATION

LOSS OF JOB/INCOME

FIRST-TIME MAIN HOME PROPERTY PURCHASE

RETIREMENT FUND

I ACTIVELY SAVE NOW I PLAN TO SAVE IN THE FUTURE

UPSCALE MILLENNIALS IN INDIA

48%37%

43%37%

44%39%

60%27%

48%39%

48%45%

66%28%

57%36%

53%37%

54%33%

45%42%

52%41%

65%24%

54%40%

TOTAL MILLENNIALS IN INDIA

47%40%

43%46%

46%39%

52%26%

44%34%

42%48%

45%44%

37%56%

54%33%

49%34%

34%47%

39%40%

49%30%

48%33%

13UPSCALE TECH-SAVVY MILLENNIALS Copyright © 2014 The Nielsen Company

MILLENNIALS SAVINGS STRATEGIES FOR FIRST HOME PURCHASEPurchase of a first home is a major life milestone and something many

Millennials across globe are either currently saving towards or intend

to save for in the future. Given the disproportionate impact of the

global recession on Millennials, the goal of homeownership presents

challenges for this generation. Homeownership rates among U.S.

Millennials have fallen dramatically since pre-Recession (2006), with

many Millennials renting instead of buying.iii

The methods used by upscale Millennials to save for a first-time home

purchase vary from country to country. Upscale Millennials in the U.S.

utilize the fewest methods, focusing on local bank accounts, stock

trading, savings plans and retirement products to save for their first

home purchase. Local bank accounts also top the charts for upscale

Millennials in Brazil and China, followed by stock trading. Upscale

Millennials in India utilize the most methods in saving for their first

home purchase ranging from pensions to stocks to foreign investments.

U.S. BRAZIL CHINA INDIA

Local Bank Accounts (18%) Local Bank Accounts (59%) Local Bank Accounts (55%) Company Pension (38%)

Stock Trading (18%) Stock Trading (27%) Stock Trading (25%) Private Pension (34%)

Savings Plans (18%) Bonds (22%) Foreign Currency Investments (18%)

Stock Trading (33%)

Other Retirement Products (18%)

Property Investments (22%)

Unit Trust (16%) Structured Investment Products (33%)

Structured Investment Products (16%)

Savings Plans (16%) Foreign Bank Accounts (31%)

Unit Trust (16%) Property Investments (15%)

Bonds (30%)

Local Bank Accounts (30%)

Foreign Currency Investment (29%)

Unit Trust (28%)

Property Investments (22%)

Savings Plans (19%)

TOP METHODS TO SAVE - STRATEGIES USED BY MORE THAN 15% OF UPSCALE MILLENNIALS

Source: Nielsen Global Survey of Saving and Investment Strategies, Q3 2013

14 UPSCALE TECH-SAVVY MILLENNIALS

Upscale Millennials in the U.S. feel further from meeting their financial

goal of first-time home purchase than upscale Millennials in other

countries, with 36 percent indicating that they were 3 to 5 years from

meeting this goal. In contrast, 30 percent of upscale Millennials in Brazil

indicated they were 6 months to 1 year from meeting their goal of first-

time home purchase and 25 percent of upscale Millennials in China and

33 percent of upscale Millennials in India indicated they were 1 to 3 years

from meeting this goal.

U.S. BRAZIL CHINA INDIA

Less than 6 months 9% 8% 16% 14%

6 months to less than 1 year 0% 30% 20% 16%

1 year to less than 3 years 27% 24% 25% 33%

3 years to less than 5 years 36% 11% 24% 23%

5 years to less than 10 years 18% 14% 7% 11%

10 years to less than 20 years 0% 11% 5% 4%

20 years or more 9% 3% 2% 0%

TIMEFRAME FOR UPSCALE MILLENNIALS TO ACHIEVE FINANCIAL GOAL OF FIRST-TIME HOME PURCHASE

Source: Nielsen Global Survey of Saving and Investment Strategies, Q3 2013

15UPSCALE TECH-SAVVY MILLENNIALS Copyright © 2014 The Nielsen Company

UPSCALE MILLENNIALS SAVINGS RATETHE AMOUNT SAVED IS INCREASING

Upscale Millennials are devoting a larger proportion of their monthly

income to savings than the general Millennial population. Upscale

Millennials in the U.S. are saving to meet their financial goals each

month at the highest rate, with 17 percent indicating they are saving

more than 50 percent of their monthly paychecks. However for most

U.S. Millennials the amount saved over the last 12 months has remained

relatively constant. Millennials in Brazil are saving the least each

month, with over 60 percent of both upscale Millennials and the general

Millennial population saving less than 20 percent of their monthly

paychecks. Yet, savings among Brazilian Millennials – both upscale and

in total – is on the rise and has increased over the last 12 months. While

most Chinese Millennials are saving modestly, between 20 percent-50

percent of their monthly paychecks, their savings has increased

over the last 12 months. The vast majority (77%) of upscale Chinese

Millennials have increased their savings over the last 12 months,

while 64 percent of total Chinese Millennials have increased their

savings. And only 2 percent of upscale Chinese Millennials decreased

their amount saved over the last 12 months. The largest percentage of

upscale Indian Millennials save between 20 percent-50 percent of their

monthly paychecks and savings is on the rise with 68 percent indicating

their savings has increased over the last 12 months. As the economy

continues to rebound, Millennials may save more and more of their

income, ultimately bringing them closer and closer to achieving their

financial goals.

16 UPSCALE TECH-SAVVY MILLENNIALS

UpscaleMillennials

UpscaleMillennials

UpscaleMillennials

UpscaleMillennials

Total Millennials

%

Total Millennials

Total Millennials

Total Millennials

U.S. BRAZIL

43

374843

50

13

61

27 11

56

29

14

7764 68

22 10

63

26 1129

723

48

91

CHINA INDIA

Source: Nielsen Global Survey of Saving and Investment Strategies, Q3 2013

CHANGE IN SAVINGS AMOUNT OVER THE LAST 12 MONTHS

Increased Stay the Same Decreased

CONFIDENCE IN MEETING FINANCIAL GOALS

PERCENTAGE OF MONTHLY INCOME DEDICATED TOWARDSMEETING FINANCIAL GOALS

UpscaleMillennials

UpscaleMillennials

UpscaleMillennials

UpscaleMillennials

Total Millennials

%

Total Millennials

Total Millennials

Total Millennials

U.S. BRAZIL

43 39

17

60

34

6

60

31

10

64 66

33

4838

54

40

67

5548

31

5 51

CHINA INDIA

Source: Nielsen Global Survey of Saving and Investment Strategies, Q3 2013

Less than 20% 20%-50% More than 50%

17UPSCALE TECH-SAVVY MILLENNIALS Copyright © 2014 The Nielsen Company

Globally, 7 out of 10 (69%) consumers believe they will meet their

financial goals, with 28 percent trusting their current plan and 41 percent

needing to monitor and adjust their plan over time. Upscale Millennials

exhibit even greater confidence in meeting their financial goals than the

general global population. Yet many, particularly in Brazil, still indicate

that they will need to monitor their current plan and make adjustments,

presenting opportunity for financial institutions to play a role in that

process. In the U.S., 83 percent of upscale Millennials believe they will

meet their financial goals, with 43 percent trusting their current plan

and 39 percent needing to monitor and adjust their plan. In Brazil, 76

percent of upscale Millennials believe they will meet their financial

goals, with 27 percent trusting their current plan and 48 percent needing

to monitor and adjust their plan. In China, 91 percent of upscale

Millennials believe they will meet their financial goals, with 47 percent

trusting their current plan and 44 percent needing to monitor and adjust

their plan. In India, 94 percent of upscale Millennials believe they will

meet their financial goals, with 52 percent trusting their current plan and

42 percent needing to monitor and adjust their plan.

UpscaleMillennials

UpscaleMillennials

UpscaleMillennials

UpscaleMillennials

Total Millennials

%

Total Millennials

Total Millennials

Total Millennials

U.S. BRAZIL

43 39

134

3542

186

27

48

168

43 36

175

47 44

7 2

3547

134

5242

5 2

42 44

113

CHINA INDIA

Source: Nielsen Global Survey of Saving and Investment Strategies, Q3 2013

CONFIDENCE IN MEETING FINANCIAL GOALS

Confident in Meeting Financial Goals with Current Plan

Confident in Meeting Financial Goals, but will Monitor Plan and Make Adjustments

Not Confident in Meeting Financial Goals, but will Keep Current Plan

Not Confident in Meeting Financial Goals, but will review plan to try to meet goals

PERCENTAGE OF MONTHLY INCOME DEDICATED TOWARDSMEETING FINANCIAL GOALS

18 UPSCALE TECH-SAVVY MILLENNIALS

WHAT DOES IT ALL MEAN?Upscale Millennials represent the future of economic growth and

prosperity. This young segment of the population is actively saving and

investing, and feel confident in their financial futures. In contrast to the

global population, the proportion of upscale Millennials actively saving

exceeds future savings intention in areas reflective of their lifestage like

higher education and home purchase. Even with higher income, upscale

Millennials are devoting a larger portion of their monthly income to

savings than the general Millennial population. Financial institutions

should look to consumer sentiment and savings intentions country

by country to develop strategies to educate and connect with upscale

Millennials.

U.S. consumers are on par with the global average for consumer

confidence and only a small percentage can spend freely, indicating

potential uncertainty about the future. Yet, upscale Millennials in the

U.S. feel confident in their financial future with many indicating they are

confident in meeting their financial goals with their current planning.

This is an important, responsible and desirable consumer segment that

will ultimately replenish the much sought after Mass Affluent group-

those Americans with liquid wealth exceeding $250K and under $1MM.

Many upscale Millennials in the U.S. are devoting a large portion of their

monthly income to savings, but their savings amount is not increasing

as dramatically as upscale Millennials in other countries. Looking at

home purchase specifically, upscale Millennials use fewer savings

methods than upscale Millennials in other countries. Ensure upscale

Millennials stay on track with their current financial plans, continue to

build their savings and diversify their saving methods.

Chinese and Indian consumers have high consumer confidence, and a

large portion of their population is able to live comfortably, indicating

strong optimism. Upscale Millennials in these countries feel positive

about their financial future and are forward thinking in preparing for

the financial security of future generations, indicating their confidence

in meeting their financial goals with current plans. And these young

upscale consumers are increasing the amount they are saving. Ensure

upscale Millennials in China and India have support and education for

their current savings and investments for health, and in planning for

their future saving intentions like financial legacy and retirement.

19UPSCALE TECH-SAVVY MILLENNIALS Copyright © 2014 The Nielsen Company

i Nielsen Global Survey of Inflation Impacts, Q1 2013

ii Nielsen Financial Track, 2013

iii The Demand Institute, The Shifting Nature of U.S. Housing Demand, 2012

ABOUT NIELSEN Nielsen Holdings N.V. (NYSE: NLSN) is a global information and

measurement company with leading market positions in marketing

and consumer information, television and other media measurement,

online intelligence and mobile measurement. Nielsen has a presence in

approximately 100 countries, with headquarters in New York, USA and

Diemen, the Netherlands.

For more information, visit www.nielsen.com.

Copyright © 2014 The Nielsen Company. All rights reserved. Nielsen and

the Nielsen logo are trademarks or registered trademarks of CZT/ACN

Trademarks, L.L.C. Other product and service names are trademarks or

registered trademarks of their respective companies. 14/7551

While optimistic, upscale Millennials in Brazil are actively saving on par

with the general Millennial population and feel less confident in their

financial planning, presenting opportunity for financial institutions in

Brazil to partner with these young consumers to help them prepare for the

future. Specifically, financial institutions should focus on helping Brazilian

Millennials to save for property purchase and education, and developing

strategies to devote a larger portion of their income to savings.

So, despite Millennials in different countries emphasizing different

priorities for their savings and investment intentions, guiding them in

achieving their financial goals is paramount for the financial sector.

Almost half or more of Millennials in each country are confident regarding

their future financial plans, yet are looking to revise or make adjustments

to ensure financial security. Helping Millenials everywhere ensures the

future health and growth of the global economy.

20 UPSCALE TECH-SAVVY MILLENNIALS