U.S. employment situation: September 2013

Release date: October 22, 2013

November gain of 321,000 jobs

confirms the strength of the recovery

U.S. employment situation: November 2014 December 5, 2014

November 2014 employment summary

• Total non-farm employment increased by 321,000 jobs in November. Revisions in previous months mean that this was the ninth consecutive

month of monthly additions surpassing 200,000 jobs.

- This was the third-highest one-month net change seen throughout the recovery so far, boosted by growth across subsectors, even in more

stalled industries such as manufacturing and finance.

• Unemployment remained steady at 5.8 percent; despite persistently low labor force participation (62.8 percent) and an increase in quits

countering strong job gains.

- Total unemployment declined to 11.4 percent, a drop of 10 basis points, as the number of marginally detached workers slowly falls.

- Unemployment for college and high-school grads remained stable, but labor force participation for both groups is at record lows with little sign

of increase.

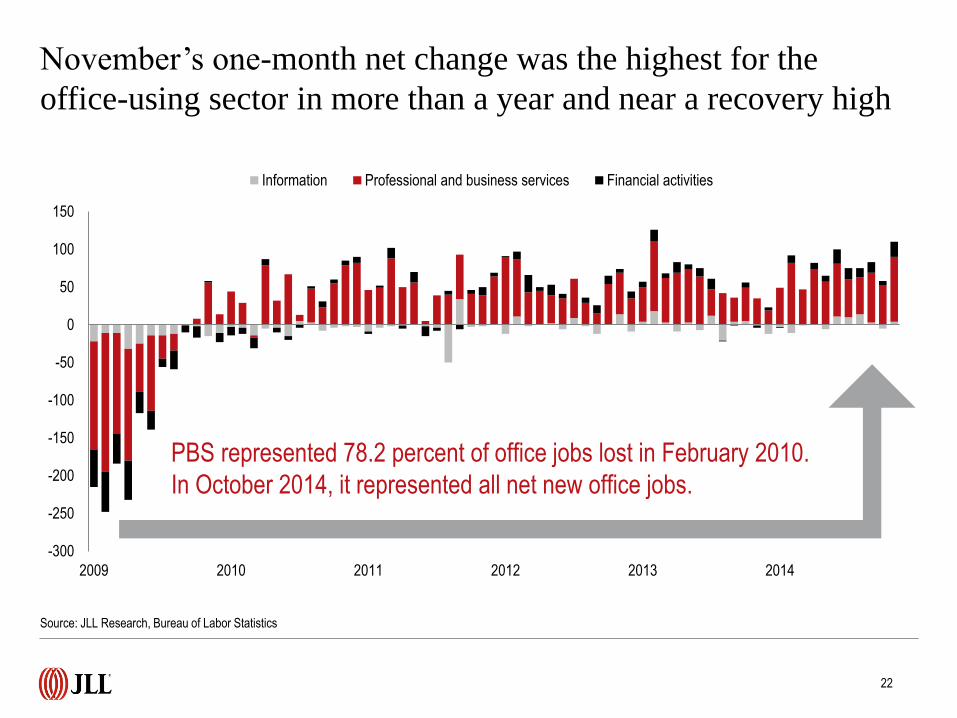

• The office-using industries (PBS, financial activities and information) registered their second-highest monthly growth during the recovery, which

was only slightly less than their peak in early 2013. In turn, this resulted in office-using subsectors comprising slightly more than one-third of total

non-farm jobs in November.

• While consumer confidence fell to 88.7 points from 94.1 in October, it is still well above the recovery average and near normal during the previous

cycle.

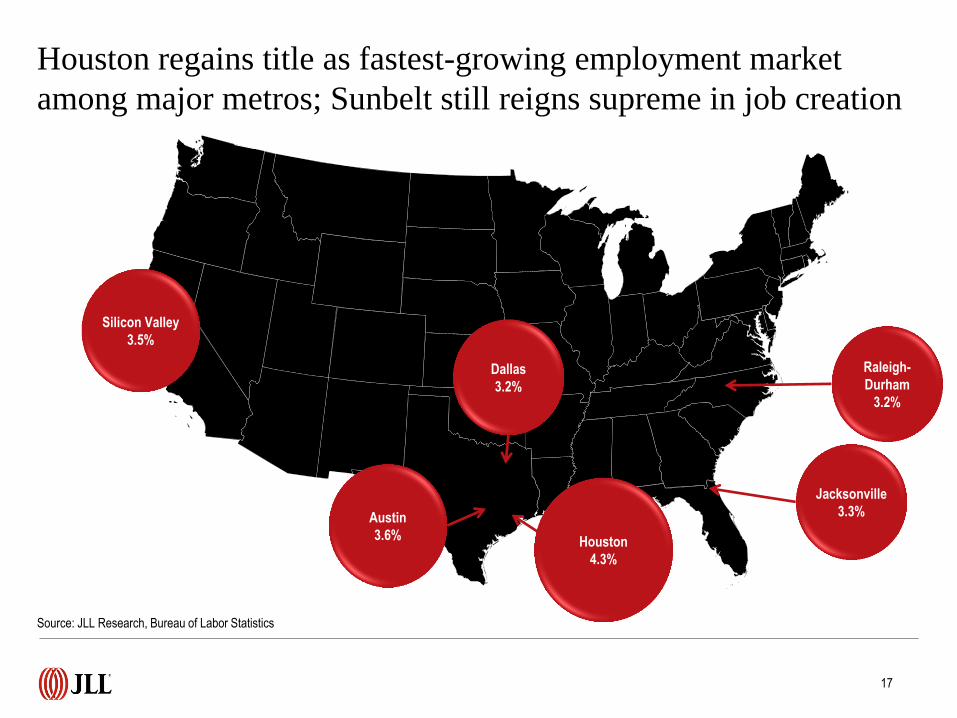

• From a geographic perspective, Texas and the Sunbelt are the definite leaders, with markets consistently reporting 3.5 percent or greater year-

on-year employment growth. While most major markets are now in the 2.0+ percent range (with the notable exceptions of Chicago and

Philadelphia), they have yet to keep up with Austin, Dallas, Denver, Houston, Raleigh-Durham and South Florida in percentage terms, among

other high-growth areas.

• Improvements in the labor market have finally had a significant effect on the office sector. Over the course of 2014, occupancy growth has

surpassed 38.0 million square feet (highest in more than five years), pushing vacancy below 16.0 percent and placing upward pressure on rents

across markets. Similarly, increasing consumer spending is driving more than 51.2 million square feet of industrial absorption year-to-date.

321,000 jobs were added in November, while revisions push up

YTD growth to 2.6 million 22

0,00

0

121,

000

120,

000

360,

000

226,

000

243,

000

96,0

00

110,

000

88,0

00

106,

000

122,

000

221,

000

183,

000

164,

000 19

6,00

0

360,

000

226,

000

243,

000

96,0

00

110,

000

88,0

00

160,

000

150,

000

161,

000

225,

000

203,

000

214,

000

197,

000

280,

000

141,

000

203,

000

199,

000

201,

000

149,

000

202,

000

164,

000

237,

000 27

4,00

0

84,0

00

144,

000

222,

000

201,

000

304,

000

202,

000

267,

000

243,

000

203,

000

271,

000

243,

000

321,

000

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

Oct

-10

Dec

-11

Feb

-11

Apr

-11

Jun-

11

Aug

-11

Oct

-11

Dec

-11

Feb

-12

Apr

-12

Jun-

12

Aug

-12

Oct

-12

Dec

-12

Feb

-13

Apr

-13

Jun-

13

Aug

-13

Oct

-13

Dec

-13

Feb

-14

Apr

-14

Jun-

14

Aug

-14

Oct

-14

1-m

onth

net

cha

nge

Source: JLL Research, Bureau of Labor Statistics

3

Unemployment remains stable at 5.8 percent as quits rise due

to an increase in worker confidence

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

-1,000.0

-800.0

-600.0

-400.0

-200.0

0.0

200.0

400.0

600.0

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Une

mpl

oym

ent

rate

(%

)

1-m

onth

net

cha

nge

(tho

usan

ds)

Monthly employment change Unemployment rate

Source: JLL Research, Bureau of Labor Statistics

4

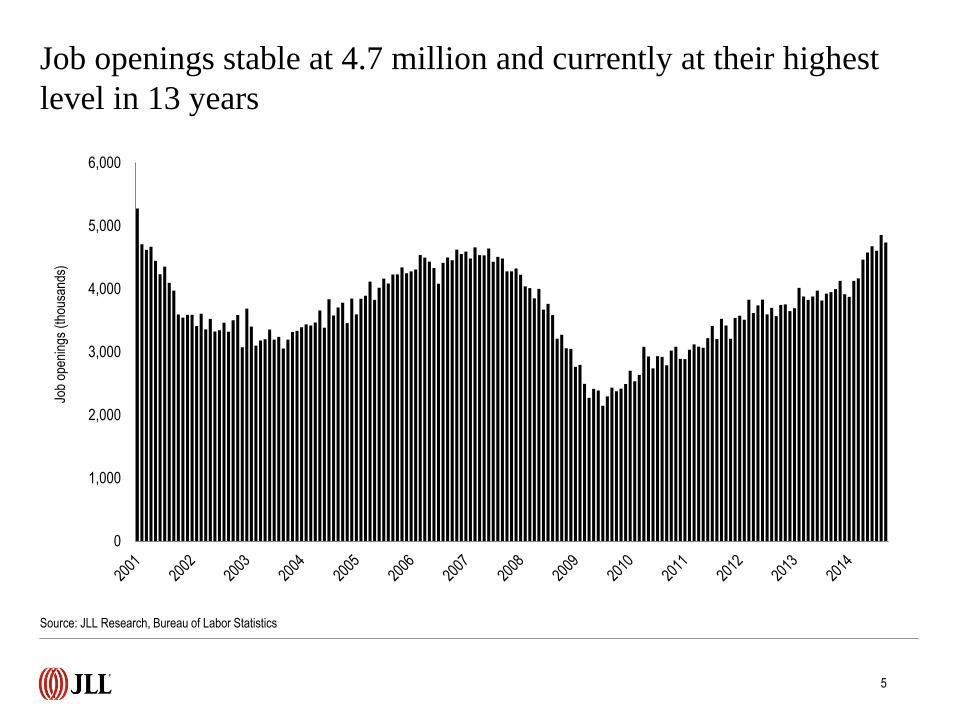

Job openings stable at 4.7 million and currently at their highest

level in 13 years

Source: JLL Research, Bureau of Labor Statistics

5

0

1,000

2,000

3,000

4,000

5,000

6,000

Job

open

ings

(th

ousa

nds)

0.0

1.4

2.5

3.0

4.0

7.0

11.0

15.0

16.7

17.0

20.0

20.0

22.7

28.0

32.0

37.2

38.0

50.2

86.0

-40 -20 0 20 40 60 80 100

Mining and logging

Utilities

Wholesale trade

Motor vehicles and parts

Information

Government

Nondurable goods

Other services

Transportation and warehousing

Durable goods

Financial activities

Construction

Temporary help services

Manufacturing

Leisure and hospitality

Health care and social assistance

Education and health services

Retail trade

Professional and business services

1-month net change (thousands)

Growth across the board contributed to gains in November, led

by a resurgence in office-using jobs, retail and manufacturing

Source: JLL Research, Bureau of Labor Statistics

6

PBS

Retail trade

Education and health

All other subsectors

Top three

subsectors

responsible for

54.3 percent of

monthly

growth.

2.0

3.2

13.0

37.4

44.0

68.0

68.0

106.8

114.0

142.5

158.0

171.0

213.0

233.6

290.0

364.9

377.0

429.0

696.0

0 200 400 600 800

Information

Utilities

Nondurable goods

Motor vehicles and parts

Mining and logging

Other services

Government

Wholesale trade

Financial activities

Transportation and warehousing

Durable goods

Manufacturing

Construction

Temporary help services

Retail trade

Health care and social assistance

Leisure and hospitality

Education and health services

Professional and business services

12-month net change (thousands)

PBS

Education and health

Leisure and hospitality

Retail trade

Manufacturing

Financial activities

All other jobs

PBS regained its position as the leader in annual growth; core

subsector share of gains remains around three-quarters

Source: JLL Research, Bureau of Labor Statistics

7

Core subsectors added 76.0 percent

of all jobs over the past 12 months.

-1,000

-800

-600

-400

-200

0

200

400

2008 2009 2010 2011 2012 2013 2014

Change in '000s jobs

Boosts in state and local government hiring are slowly pushing

up public sector two-year growth figures

Private sector hiring up 5.2

million since November 2012

Public sector hiring up 44,000

workers since October 2012

Source: JLL Research, Bureau of Labor Statistics

8

0

2

4

6

8

10

12

Une

mpl

oym

ent (

%)

Bachelor's degree and higher High school graduates, no college

As with overall unemployment, both white-collar and high-

school-graduate unemployment stable

3.2%

5.6%

Source: JLL Research, Bureau of Labor Statistics

9

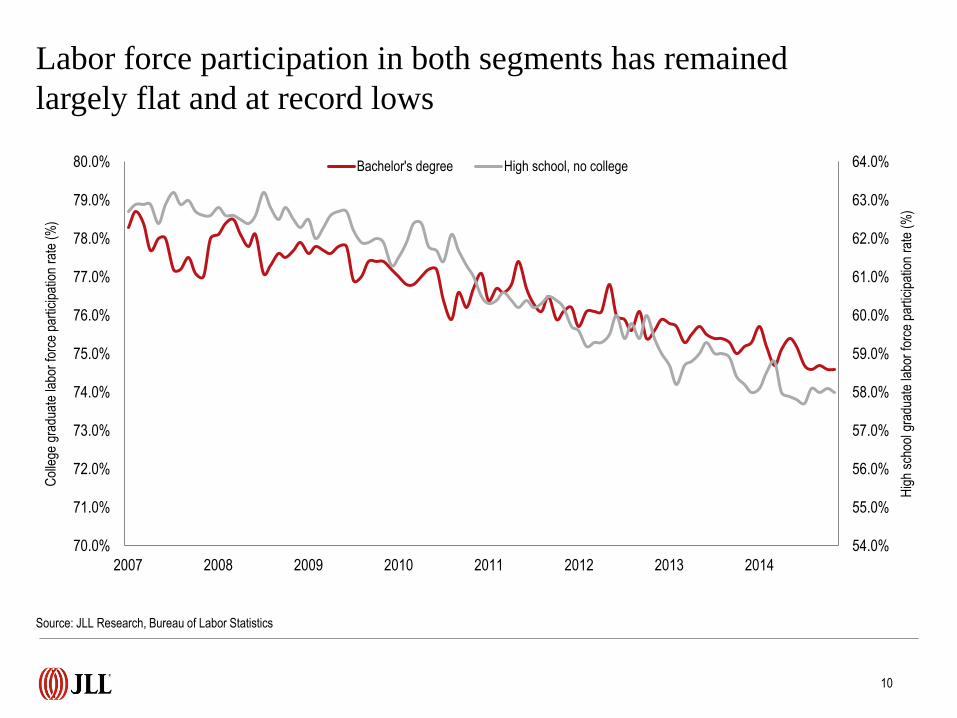

Labor force participation in both segments has remained

largely flat and at record lows

Source: JLL Research, Bureau of Labor Statistics

10

54.0%

55.0%

56.0%

57.0%

58.0%

59.0%

60.0%

61.0%

62.0%

63.0%

64.0%

70.0%

71.0%

72.0%

73.0%

74.0%

75.0%

76.0%

77.0%

78.0%

79.0%

80.0%

2007 2008 2009 2010 2011 2012 2013 2014

Hig

h sc

hool

gra

duat

e la

bor

forc

e pa

rtic

ipat

ion

rate

(%

)

Col

lege

gra

duat

e la

bor

forc

e pa

rtic

ipat

ion

rate

(%

)

Bachelor's degree High school, no college

For the first time during the recovery, service-providing growth

has surpassed 200,000 jobs for three consecutive months

-1,000.0

-800.0

-600.0

-400.0

-200.0

0.0

200.0

400.0

600.0

2008 2009 2010 2011 2012 2013 2014

1-m

onth

net

cha

nge

(tho

usan

ds)

Goods-producing Service-providing

Source: JLL Research, Bureau of Labor Statistics

11

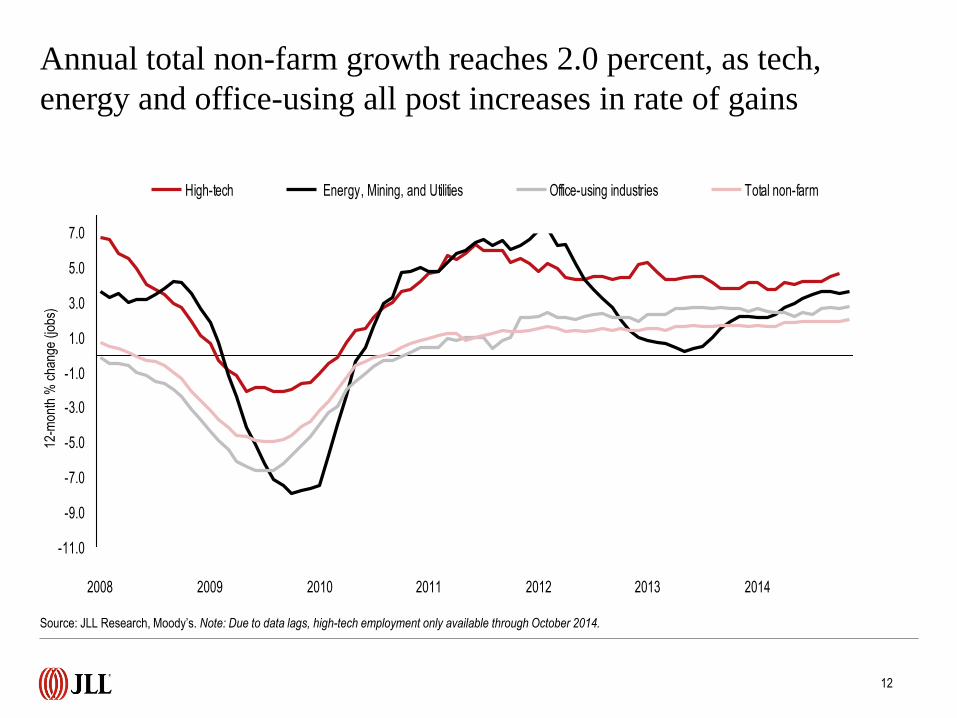

Annual total non-farm growth reaches 2.0 percent, as tech,

energy and office-using all post increases in rate of gains

-11.0

-9.0

-7.0

-5.0

-3.0

-1.0

1.0

3.0

5.0

7.0

2008 2009 2010 2011 2012 2013 2014

High-tech Energy, Mining, and Utilities Office-using industries Total non-farm

Source: JLL Research, Moody’s. Note: Due to data lags, high-tech employment only available through October 2014.

12

12-m

onth

% c

hang

e (jo

bs)

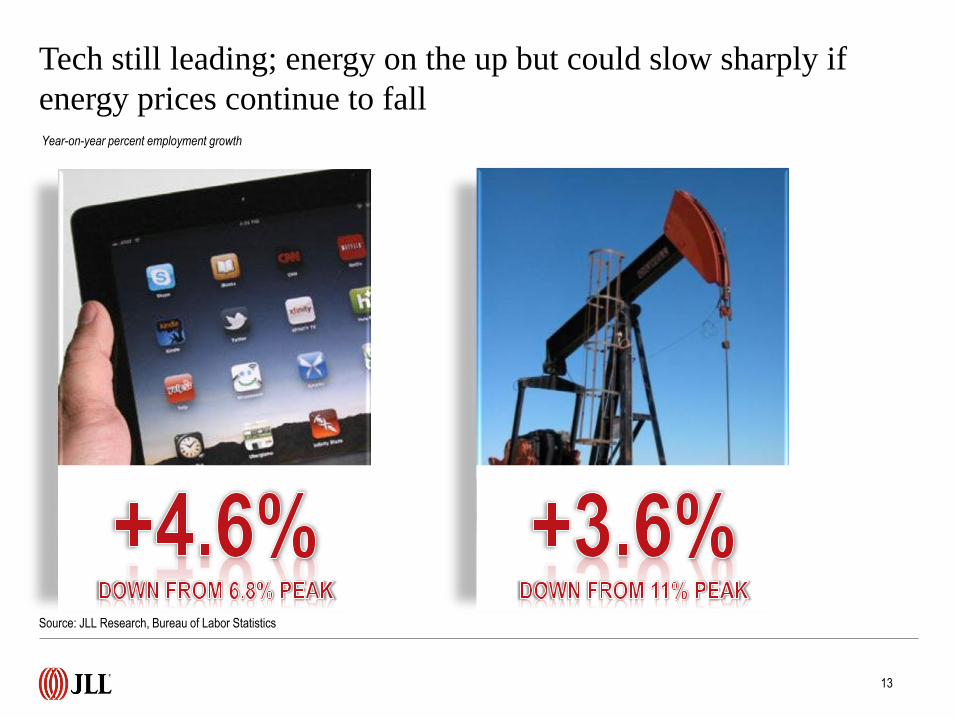

Tech still leading; energy on the up but could slow sharply if

energy prices continue to fall Year-on-year percent employment growth

Source: JLL Research, Bureau of Labor Statistics

13

Unemployment insurance claims nudge upward slightly and

currently rest right below 300,000 per week on average

Source: JLL Research, U.S. Department of Labor

14

200,000

250,000

300,000

350,000

400,000

450,000

500,000

550,000

600,000

650,000

700,000

Cla

ims

Initial claims 4-week moving average

0%

2%

4%

6%

8%

10%

12%

0

10

20

30

40

50

60

70

80

90

100

2008 2009 2010 2011 2012 2013 2014

Une

mpl

oym

ent

rate

(%

)

Con

sum

er c

onfid

ence

inde

x

Consumer confidence index

Unemployment rate

Consumer confidence falls to 88.7 points after a rapid increase

to 94.1 in October, but still remains near recovery highs

Source: JLL Research, Conference Board, Bureau of Labor Statistics

15

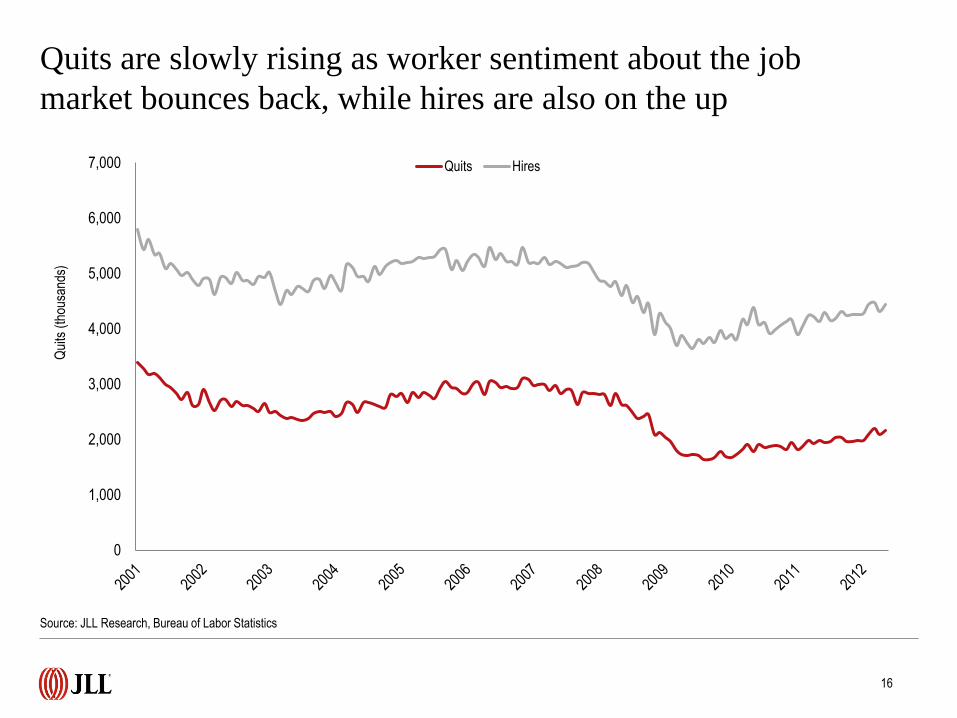

Quits are slowly rising as worker sentiment about the job

market bounces back, while hires are also on the up

Source: JLL Research, Bureau of Labor Statistics

16

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Qui

ts (

thou

sand

s)

Quits Hires

Houston regains title as fastest-growing employment market

among major metros; Sunbelt still reigns supreme in job creation

Source: JLL Research, Bureau of Labor Statistics

17

Dallas

3.2%

Houston

4.3%

Austin

3.6%

Jacksonville

3.3%

Raleigh-

Durham

3.2%

Silicon Valley

3.5%

Some East Coast and Midwestern markets are still posting

job growth below 0.5 percent year-on-year, however

18

Source: JLL Research, Bureau of Labor Statistics

Detroit

0.3%

Washington,

DC

0.3%

New Jersey

0.1%

Kansas City

0.5%

Columbus

-0.7%

Hampton

Roads

0.5%

The labor force participation rate stayed flat a near-recovery

low of 62.8 percent, contributing to declines in unemployment

Source: JLL Research, Bureau of Labor Statistics

19

60.0%

61.0%

62.0%

63.0%

64.0%

65.0%

66.0%

67.0%

2008 2009 2010 2011 2012 2013 2014

Labo

r fo

rce

part

icip

atio

n ra

te (

%)

A small decline in the number of marginally detached workers

enabled total unemployment to fall to 11.4 percent

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

Total unemployment U-6 10-year average

Source: JLL Research, Bureau of Labor Statistics

20

Jumps in PBS and financial activities hiring meant that

office-using industries accounted for one-third of new jobs

Source: JLL Research, Bureau of Labor Statistics

21

November’s one-month net change was the highest for the

office-using sector in more than a year and near a recovery high

-300

-250

-200

-150

-100

-50

0

50

100

150

2009 2010 2011 2012 2013 2014

Information Professional and business services Financial activities

PBS represented 78.2 percent of office jobs lost in February 2010.

In October 2014, it represented all net new office jobs.

Source: JLL Research, Bureau of Labor Statistics

22

Temporary help services is still on its way to 3.0 million jobs,

but rate of growth slightly slower and more stable

1,000.0

1,500.0

2,000.0

2,500.0

3,000.0

3,500.0

-100.0

-80.0

-60.0

-40.0

-20.0

0.0

20.0

40.0

60.0

80.0

2009 2010 2011 2012 2013 2014

Mon

thly

net

cha

nge

in jo

bs (

ths)

Temporary employment monthly net change Temporary employment

Temporary em

ployment (ths)

Source: JLL Research, Bureau of Labor Statistics

23

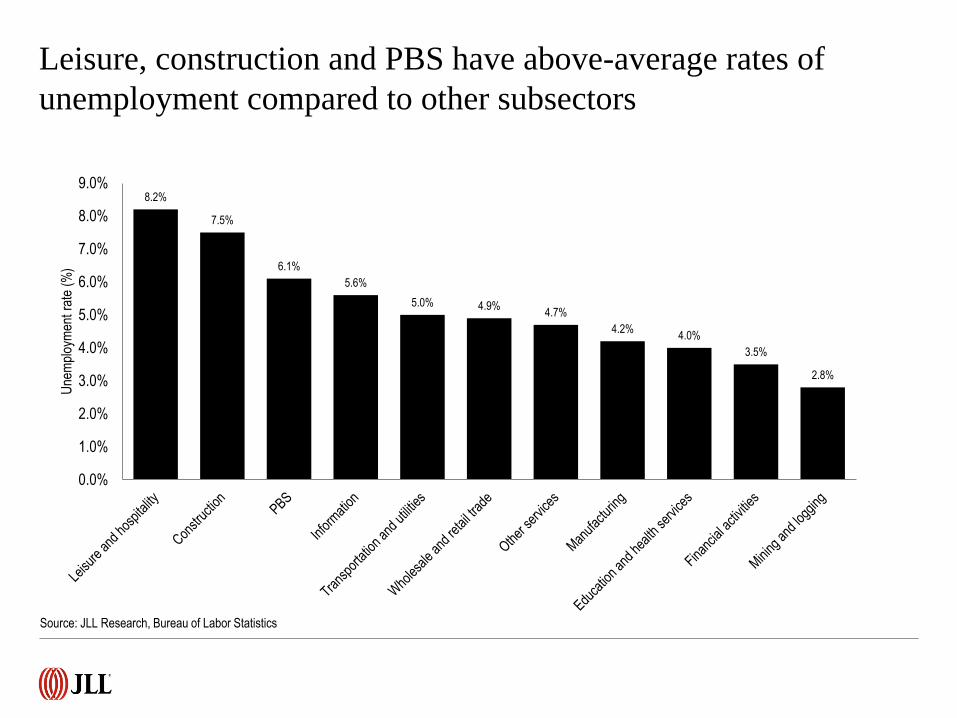

Leisure, construction and PBS have above-average rates of

unemployment compared to other subsectors

8.2%

7.5%

6.1%

5.6%

5.0% 4.9% 4.7%

4.2% 4.0%

3.5%

2.8%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

Une

mpl

oym

ent

rate

(%

)

Source: JLL Research, Bureau of Labor Statistics

©2014 JLL Research IP, Inc. All rights reserved. All information contained herein is from sources deemed reliable; however, no representation or warranty is made to the accuracy thereof.

For more information, please contact:

Ben Breslau

Managing Director - Americas Research

John Sikaitis

Managing Director - Office and Local Markets Research

Phil Ryan

Research Analyst

Or, find more employment, business and real

estate research at jll.com.

>>> Click here to check it out.