c l 3 ^

VILLAGE OF CHATAIGNIER, LOUISUNA

Financial Report

Year Ended June 30,2010

Underprovisions of state law, this report is a public document. Acopy ofthe report has been submitted to the entity and other appropriate public officials. The report is available for public inspection at the Baton Rouge office ofthe Legislative Auditor and, where appropriate, at the office of the parish clerk of court.

Release Date l ^ f W / O

TABLE OF CONTENTS

Page

Accoimtants' Compilation Report 1

BASIC FINANCIAL STATEMENTS

GOVERNMENT-WIDE FINANCIAL STATEMENTS (GWFS) Statement of net assets 4 Statement of activities 5

FUND FINANCL^L STATEMENTS (FFS) • Balance sheet - govemmental ftmds 8 Reconciliation ofthe governmental funds balance sheet

to the statement of net assets 9 Statement of revenues, expenditures, and changes in fund balances -

govermnental funds 10 Reconciliation ofthe statement of revenues, expenditures, and

changes in fimd balances of govemmental funds to the statement of activities 11 Statement of net assets-proprietary fund 12 Statement of revenues, expenses, and changes in fund net

assets - proprietary fund 13 Statement of cash flows - proprietary fund 14

Notes to basic fmancial statements 15-23

REQUIRED SUPPLEMENTARY INFORMATION Budgetary comparison schedules:

General Fund 25

OTHER SUPPLEMENTAL INFORMATION Schedule of insurance in force 27

INTERNAL CONTROL AND COMPLL\NCE Summary schedule of current and prior year fmdings

and corrective action plan 29

C. Burton Kolder. CPA' Russell F. cnampmns.CPA' VietorR.Slavftn.CPA' P. Troy Couivfflft; CPA' GemldA. Dilbodtaux. Jr..CPA* HolwrtS.CMer.WA' Arthur R.MIxcn. CPA'

KOLDER, CHAWIPAGNE, SLAVEN & COMPANY, LLC CERTIFIED PUBUC ACCOUNTANTS

TjnasE. Mixon. Jr.. CPA AUsnJ. LaBry.CPA Wbert R, Uoer.CPA.PFS.CSA' Pemy Angall* Scruggins. CPA ChtlstlM L. Cousin. CPA MafyT.ThttwdMOX, CPA MarshdIW.GiMry.CPA AlnnM. Taylor, a>A JarMiR. Roy.CPA Robait J. Melz. CPA Kelty M. Doucet. CPA ChsrylLeeflley.CPA Mandy B.S«U. CPA Pati L OelcambF*. Jr. CPA Woida F. Aicemenl. CPA. CVA KdMnB. Dauzat. CPA Richard R, Anderaon Sr, CPA Carolyn C. Andaraon. CPA

Retrad: Conrad O. Chapman. CPA- 2006 Harry J.aottio,CPA 2007

ACCOUNTANTS' COMPILATION REPORT

OFFICES

te3 South Baadia Rd. Labyen«.LA70SO8 PhOf»'{337> 232-4141 rax(337)23:»4660

ll3Eait8(1dgaSl 8rtauxBrldOftLA7D517 Phaaa (337) »32-4azo Fax (337)332-2657

1234DavMOr.Sta203 Morgan CI4.UV703D0 Phona(S85) 384-2020 Fax (965] 304-3020

40BWe»t Cotton Streel \ffltaPlatto. LATO58B PhoM (337) 383-2792 Fax (3^)363-3049

332 WeslSixA Avenue CtM«lr\LA7»6S Phono (337) 839-4737 Fax (337)6304568

450 Ead Main Street New Ibede. LA 7QSeo

Ptwne 1337} 3S7-S204 Fax (337) 367-S208

200$ou»iMainSireet Abbeville. LA 70510

Phone (337) 603-7944 F u (337) 893-7946

1013MdnSl»et FrenMin. lA 70538

pnona [337) 826-0272 Fax (337)828-0290

iSlEastWaddnSL Ma(l(sviiraLA7l3S1

Phone (318) 293-9252 F n (318)253-8881

62lMdnSliaei Pinevil*. LA 71380

Phone (318) 442-4421 FsK (318)442-9833

* A nofMUMM weainlng Covcmllon

V^KSITE WWW,KCSRCPAS.COM

To the Board of Aldermen Village of Chataignier, Louisiana

We have compiled the accompanying financial statements ofthe govemmental activities, the business-type activities and each major fijnd ofthe Village of Chataignier, as of and for the year ended June 30,2010, which collectively comprise the Village's basic financial statements as listed in the table of contents, and the accompanying supplementaiy information contained on page 27, which is presented only for supplemental analysis purposes, in accordance with Statements on Standards for Accounting and Review Services issued by the American Institute of Certified Public Accountants.

A compilation is limited to presenting in the form of financial statements information that is the representation of management. We have not audited or reviewed the accompanying financial statements and, accordingly, do not express an opinion or any other form of assurance on them.

The Village has not presented management's discussion and analysis that the Govemmental Accounting Standards Board has determined is necessaiy to supplement, although not required to be part of, the basic financial statements.

The budgetary comparison information, on page 25, is not a required part of the basic financial statements but is supplementary information required by the Govemmental Accounting Standards Board. We have compiled the supplementaiy information from information that is the representation of management, without audit or review. Accordingly, we do not express an opinion or any other form of assurance on the supplementary information.

Kolder, Champagne , Slaven & Company, L L C Certified Public Accountants

Ville Platte, Louisiana September 22,2010

Member of: AMERICAN INSTITUTE OF CERTIFIED PUBUC ACCOUNTANTS

Member oft SOCIETY OF LOUISIANA

CERT IHED PUBLIC ACCOUNTANTS

BASIC FINANCIAL STATEMENTS

GOVERNMENT-WIDE FlNANaAL STATEMENTS (GWFS)

VILLAGE OF CHATAIGNIER, LOUISIANA

Statement of Net Assets June 30,2010

Govemmental Business-Type Activities Activities Total

ASSETS Current assets:

Cash and interest-bearing deposits Receivables

Due from other governmental units

Total current assets

Noncurrent assets;

Capital assets, net

Total assets

LIABILITIES Current liabilities:

Accounts and other payables

Noncurrent Habilities:

Customers deposits payable

Total Uabilities

NETASSHIS Invested in capital assets, net of related debt

Unrestricted Total net assets

$ 89,108 5,260 -

94,368

328,783

423,151

-

-

.

328,783 94.368

$423,151

$ 5,982 4,314 1,586

11,882

492,012

503,894

3,218

3,055

6,273

492.012 5,609

$497,621

$ 95,090 9,574 1,586

106,250

820,795

927,045

3,218

3,055

6,273

820,795 99,977

$920,772

See accompanying notes and accountants' report.

o

B o

u

< O

I

i >—> -a I

5

i i

•a o

•S ^ - w

u tU)

OO

o

^ tn en O MS ON •— oo_ \q o oo" M ^ _ f«^_ - ^

o VD ON

eQ

00 -̂ tn (*i a^ O « ON CS --̂ 00 \o. o " O 00 ts

o ON_

00.

I t I

V i

f- o

00 <N

Vi

o

?: IO CO \0 O N ro «n 00 \0

o* oo t>l 5 o\

\n rr r—4

00 rj

vo • *

•p-«

00 (N

r̂ (S -o 0̂

r-tN O

o> CA

Ov O O r-J <N

VO M •n CM f̂ (A

<N 00 r-ON >o

ON W-) rj r) in T-H

w

O m

C4 —

OO t—1

m fi

ro C) ^ >n r--f*> vo

• ^

oo -̂t "n

?:i O N VO rn vo" r-̂ " • ^ ON

^ t • — t

oo f̂»

r-vn t̂ >n M W1

,_< <S so t -o\ • *

w

<n m O fO in 1^

00 ro <n ^ p r-m •̂ m ro >-< >o

'sr 00 '̂ tn

V>-t--** 00 IN

P-M vo if-t

tn •tt

r - *

"n >-< m M V i

42 ID

™ o o

•s r

o

o CO o m

.a s z z

fi

o

i3

i

60

•I

I

FUND FINANOAL STATEMENTS (FFS)

MAJOR FUND DESCRIPTIONS

General Fund

The General Fund is used to account for resources traditionally associated with govemments which are not required to be accounted for in another iund.

Enterpr ise Fund

Sewer Fund -To account for the provision of sewerage services to residents ofthe Village. All activities necessary to provide such services are accounted for in this fund, including, but not limited to. administration, operations, maintenance, financing and related debt service, and billing and collection.

VILLAGE OF CHATAIGNIER, LOUISIANA

Balance Sheet Govemmental Fund - General Fund

June 30,2010

ASSETS

Cash and interest-bearing deposits $ 89,108 Receivables:

Sales tax 1,468 Other 3,792

Total assets $94,368

FUND BALANCE

Fund balance: Unreserved, undesignated $94,368

See accompanying notes and accountants' report.

8

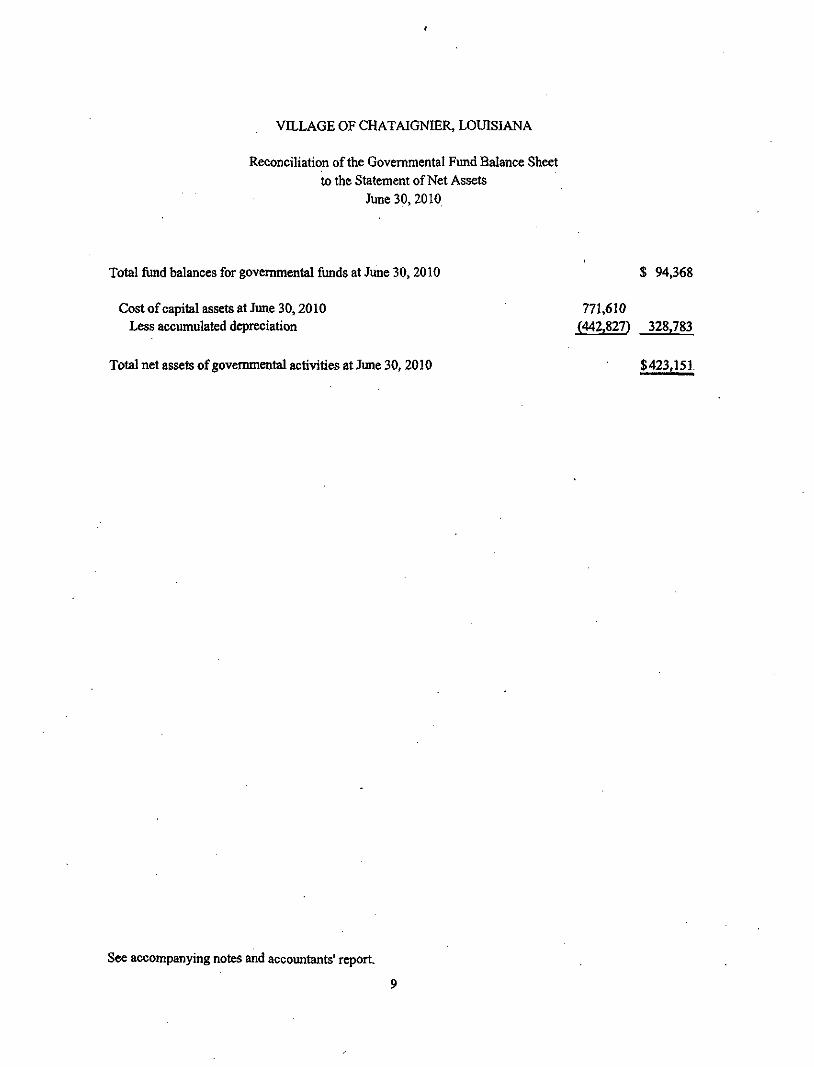

VILLAGE OF CHATAIGNIER, LOUISIANA

Reconciliation ofthe Govemmental Fund Balance Sheet to the Statement of Net Assets

June 30,2010

Total fimd balances for govemmental funds at June 30,2010 $ 94,368

Cost of capital assets at June 30,2010 771,610 Less accumulated depreciation (442,827) 328,783

Total net assets of govemmental activities at June 30,2010 $423,151

See accompanying notes and accountants' report.

9

VILLAGE OF CHATAIGNIER, LOUISIANA

Statement of Revenues, Expenditures, and Changes in Fund Balance-Governmental Fund - General Fund For the Year Ended June 30.2010

Revenues: Taxes Licenses and permits Franchise tax Intergovernmental Fines and forfeits Interest Miscellaneous

Total revenues

&tpenditures: Current-

General government Public safety Public works Culture and recreation

Total expenditures

Excess of revenues over expenditures

Fund balance, beginning

Fund balance, ending

$25,054 8,047

17,334 3,318 2,470 1,403 6,375

64.001

37,445 10,238 14,929 1,093

63,705

296

94,072

$94,368

See accompanying notes and accountants* report.

10

VILLAGE OF CHATAIGNIER, LOUISIANA

Reconciliation ofthe Statement of Revenues, Expenditures, and Changes in Fund Balances of Govemmental Fund

to the Statement of Activities For the Year Ended June 30.2010

Total net changes in fund balance at June 30,2010 per Statement of Revenues, Expenditures and Changes in Fund Balances $ 296

Depreciation expense for the year ended June 30,2010 28,772

Total change in net assets at June 30,2010 per Statement of Activities $ (28,476)

See accompanying notes and accountants' report.

n

VILLAGE OF CHATAIGNIER, LOUISIANA

Statement of Net Assets Proprietary Fund - Enterprise Fund

June 30,2010

ASSETS

Current assets: Cash Accounts receivable Due from other goveramental units

Total current assets

Noncurrent assets: Capital assets, net of accumulated depreciation

Total assets

$ 5,982 4,314 1.586

11,882

492,012

503,894

Current liabiUties: Accounts payable

Noncurrent liabilities: Customers' deposits

Total liabilities

LIABILITIES

NET ASSETS

3,218

3,055

6,273

Invested in capital assets, net of related debt Unrestricted

Total net assets

492,012 5.609

$497,621

See accompanying notes and accountants' report.

12

VILLAGE OF CHATAIGNIER, LOUISIANA

Statement of Revenues, Expenses, and Changes in Fund Net Assets Proprietary Fund - Enterprise Fund For the Year Ended June 30,2010

Operating revenues: Charges for services Penalty income

Total operating revenues

Operating expenses: Depreciation expense Insurance Office expetKe Repairs and maintenance Salaries and related benefits Fees and testing expenses Utilities

Total operating expenses

Operating loss

Capital contributions

Change in net assets

Net assets, beginning

Net assets, ending

$ 20,500 1,509

22.009

25.890 1,495

2 17,517 9.300 1,985 3.593

59,782

(37,773)

9.627

(28,146)

525.767

$497,621

See accompanying notes and accountants* report.

13

VILLAGE OF CHATAIGNIER. LOUISIANA

Statement of Cash Flows Proprietary Fund Type-Enterprise Fund

Year Ended June 30.2010

Cash flows from operating activities: Operating loss $ (37,773)

Adjustments to reconcile operating loss to net cash used by operating activities -

Depreciation 25,890 Increase in accounts receivable (698) Decrease in due from other govemmental units 7,239 Decrease in accounts payable (15.107)

Total adjustments 17,324

Net cash used by operating activities (20,449)

Cash flows from capital and related financing activities:

Proceeds from capital contribution 9.627 Proceeds from meter deposits 901

Net cash provided by capital and related financing activities 10,528

Net decrease in cash and cash equivalents (9,921)

Cash and cash equivalents, beginning of period 15,903

Cash and cash equivalents, end of period $ 5,982

See accompanying notes and accountants' report.

14

VILLAGE OF CHATAIGNIER, LOUISIANA

Notes to Basic Financial Statements

(1) Summary of Significant Accounting Policies

The accompanying financial statements of the Village of Chataignier (Village) have been prepared in conformity with generally accepted accounting prmciples (GAAP) as applied to govemmental units. GAAP includes all relevant Govemmental Accounting Standards Board (GASB) pronouncements. In the govemment-wide financial statements. Financial Accounting Standards Board (FASB) pronouncements and Accounting Principles Board (APB) opinions on or before November 30, 1989 have been applied unless those pronouncements conflict with or contradict GASB pronouncements, in which case, GASB prevails. The accountmg and reporting framework and the more significant accounting policies are discussed in subsequent subsections of this note.

A. Financial Reporting, jEn t̂y

The Village of Chataignier was incorporated in 1972. under the provisions ofthe Lawrason Act. The Village operates under a Mayor-Board of Alderman form of govemment and provides the following services: public safety, highway and streets, sanitation, culture and recreation, health and welfare, public improvements and general administrative services.

This report includes all funds and activities that are controlled by the Village as an independent political subdivision ofthe State of Louisiana. There are no component units required to be reported in conformity with generally accepted accounting principles.

B. Basis of Presentation

Govemment-Wide Financial Statements (GWFS)

The statement of net assets and statement of activities display information about the Village, the primaiy govemment, as a whole. They include all funds of the reporting entity. The statements distinguish between govemmental and business-tjfpe activities. Govemmental activities generally are financed through taxes, intergovemmental revenues, and other nonexchange revenues. Business-type activities are financed in whole or in part by fees charged to external parties for goods or services.

The statement of activities presents a comparison between direct expenses and program revenues for the business-type activities ofthe Village and for each function ofthe Village's govemmental activities. Direct expenses are those that are specifically associated with a program or function and, therefore, are clearly identifiable to a particular function. Program revenues include (a) fees, fines, and charges paid by the recipients of goods or services offered by the programs, and (b) grants and contributions that are restricted to meeting the operational or capital requirements of a particular program. Revenues that are not classified as program revenues, including all taxes, are presented as general revenues.

15

VILLAGE OF CHATAIGNIER. LOUISL\NA

Notes to Basic Financial Statements (Continued)

Fund Financial Statemwits

The accounts of the Village are organized and operated on the basis of funds. A fund is an independent fiscal and accounting entity with a separate set of self-balancing accounts. Fund accounting segregates fimds according to their intended purpose and is used to aid management in demonstrating compHance with finance-related legal and contractual provisions. The minimum number of fimds is maintained consistent with legal and maiuigerial requirements. Fund financial statements report detailed information about the Village.

The various funds of the Village are classified into two categories: govemmental and proprietary. The en^hasis on fimd financial statements is MI major govemmental and enterprise fimds, each displayed in a separate column. A fimd is considered major if it is the primary operating fund of the Village or meets the following criteria:

a. Total assets, Uabilities, revenues, or expenditures/expenses of that individual govenmiental or enterprise fund are at least 10 percent ofthe corresponding total for all fimds of that category or type; and

b. Total assets, liabilities, revenues, or expenditures/expenses of the individual govemmental or enterprise fimd are at least 5 percent of the corresponding total for all govemmental and enterprise fimds combined

The major funds ofthe Village are described below:

Govemmental Funds -

The General Fimd is the general operating fund of the Village. It is used to account for all financial resources except those required to be accounted for in another fiind.

Proprietary Funds ~

Proprietary funds are used to account for ongoing organizations and activities that are similar to those often found in the private sector. The measurement focus is based upon determination of net income, financial position, and cash flows. The Village's proprietary fund type is an enterpri^ fund.

16

VILLAGE OF CHATAIGNIER, LOUISIANA

Notes to Basic Financial Statements (Continued)

Enterprise Funds

Enterprise funds are used to account for operations (a) that are fmanced and operated in a manner similar to private business enterprises, where the intent of the goveming body is that the costs (expenses, including depreciation) of providing goods or service to the general public on a continuing basis be financed or recovered primarily through user charges; or (b) where the goveming body has decided that periodic determination of revenues earned, expenses incurred, and/or net income is appropriate for capital maintenance, public policy, management control, accountability or other purposes. The Village applies all applicable FASB pronouncements issued after November 30, 1989 in accountmg and reporting for its enterprise fimd. The Village's enterprise fimd is tiie Sewer Fund.

C. Measurement Focus/Basis of Accounting

Measurement focus is a term used to describe "which'* transactions are recorded within the various financial statements. Basis of accounting refers to "when" transactions are recorded regardless ofthe measurement focus applied.

Measurement Focus

On the govemment-wide statement of net assets and the statement of activities, both govemmentel and business-type activities are presented using the economic resources measurement focus as defined in item b. below.

In the fund financial statements, the "current financial resources" measurement focus or the "economic resources" measurement focus is used as appropriate:

a. All govemmental fimds utilize a "current financial resources" measurement focus. Only current financial assets and Habilities are' generally included on their balance sheets. Their operating statements present sources and uses of available spendable financial resources during a given period. These funds use fimd balance as their measure of available spendable financial resources at the end of the period.

b. The proprietary fund utilizes an "economic resources'* measurement focus. The accounting objectives of this measurement focus are the determination of operating income, changes in net assets (or cost recovery), fmancial position, and cash flows. All assets and Habilities (whether current or noncurrent) associated witii their activities are

' reported. Proprietary fimd equity is classified as net assets.

17

- VILLAGE OF CHATAIGNIER, LOUISIANA

Notes to Basic Financial Statements (Continued)

Basis of Accounting

In the govemment-wide statement of net assets and statement of activities, both govemmental and business-type activities are presented using the accrual basis of accounting. Under the accrual basis of accoimting, revenues are recognized when eamed and expenses are recorded when the liability is incurred or economic asset used. Revenues, expenses, gains, losses, assets, and liabilities resulting from exchange and exchange-like transactions are recognized when the exchange takes place.

Govemmental fimd financial statements are reported using die current financial resources measurement focus and the modified accrual basis of accounting. Revenues are recognized as soon as they are both measurable and available. Revenues are considered to be available when they are collectible within the current period or soon enough thereafter to pay liabilities of the current period. For this purpose, the govemment considers revenues to be available if they are collected within 60 days ofthe end ofthe current fiscal period. Expenditures (including capital outlay) generally are recorded when a liability is incurred, as under accrual accounting. However, debt service expenditures are recorded only when payment is due.

The proprietary fund utilizes the accrual basis of accounting. Under the accrual basis of accounting, revenues are recognized when eamed and expenses are recorded when the liability is incurred or economic asset used.

Program revenues

Program revenues included in the Statement of Activities are derived directiy from the program itself or from parties outside the Village's taxpayers or citizenry, as a whole; program revenues reduce the cost of the fimction to be financed from the Village's general revenues.

Allocation of indirect expenses

The Village reports all direct expenses by fimction in the Statement of Activities. Direct expenses are those that are clearly identifiable with a function. bidirect expenses of other functions are not allocated to those functions, but are reported separately in the Statement of Activities. Depreciation expense is specifically identified by fimction and is included in the direct expense of each function. Interest on general long-term debt is considered an indirect expense and is reported separately on the Statement of Activities.

When both restricted and unrestricted resources are available for use, it is the Village's policy to use restricted resources first, then unrestricted resources as they are needed.

18

VILLAGE OF CHATAIGNIER, LOUISIANA

Notes to Basic Financial Statemente (Continued)

D. Assets. Liabilities and Equitv

Cash and interest-bearing deposits

For purposes of the Statement of Net Assets, cash and interest-bearing deposits include all demand accounts, savings accounts, and certificates of deposits of the City. For the purpose of the proprietary fimd statement of cash flows, "cash and cash equivalents" include all demand and savings accounts, and certificates of deposit or short-term investments with an original maturity of three months or less when purchased.

Capital Assets

Capital assets, which include property, plant, eqmpment, and infrastructure assets, are reported in the applicable govemmental or business-type activities columns in die govemment-wide or financial statements. Capital assets are capitalized at historical cost or estimated cost if historical is not available. Donated assets are recorded as capital assets at their estimated fair market value at the date of donation. The Village maintains a Uireshold level of $5,000 or more for capitalizing capital assets. The costs of normal maintenance and repairs that do not add to the value of the asset or materially extend assets lives are not capitalized.

I.

Depreciation of all exhaustible capital assets is recorded as an allocated expense in the statement of activities, with accumulated depreciation reflected in the statement of net assets. Depreciation is provided over the assets' estimated useful lives using the straight-line method of depreciation. The range of estimated useful lives by type of asset is as follows:

Buildings 30 years Equipment 5 years Utility system and improvements 20-40 years Infrastmcture 20 years

In the fimd financial statements, capital assets used in govemmental fimd operations are accounted for as capital outiay expenditures of the govemmental fimd upon acquisition. Capital assets used in proprietary fimd operations are accounted for the same as in the govemment-wide statements.

Equity Classifications

In the govemment-wide statements, equity is classified as net assets and displayed in three components:

a. Invested in capital assets, net of related debt - Consists of capital assets including restricted capital assets, net of accumulated depreciation and reduced by the outstanding balances of any bonds, mortgages, notes, or other borrowing that are attributable to the acquisition, constmction, or improvement of those assets.

19

VILLAGE OF CHATAIGNIER, LOUISIANA

Notes to Basic Financial Statements (Continued)

b. Restricted net assets - Consists of net assets with constraints placed on the use either by (1) extemal groups, such as creditors, grantors, contributors, or laws or regulations of other govemments; or (2) law throu^ constitutional provisions or enabling legislation.

c. Unrestricted net assets - All other net assets that do not meet the definition of "restricted" or "invested in capital assets, net of related debt."

In the fimd financial statements, govemmental fimd equity is classified as fimd balance. Fund balance is fiirther classified as reserved and unreserved, with unreserved further split between designated and undesignated. Proprietary fimd equity is classified the same as in the govemment-wide statements.

E. Revenues. Expenditures, and Expenses

Operating Revenues and Expenses

Operating revenues and expenses for proprietary fimds are those that result from providing services and producing and delivering goods and/or services. It also includes all revenue and expenses not related to capital and related financing, noncapital financing, or investing activities.

Expenditures/Expenses

In the govemment-wide financial statements, expenses are classified by fimction for both govemmental and business-type activities.

In the fimd financial statements, expenditures are classified as follows:

Govemmental Funds - By Character: Proprietary Fund - By Operating and Nonoperating

In the fund financial statements, govemmental fimds report expenditures of financial resources. Proprietary fiinds report expenses relating to use of economic resources.

friterfund Transfers

Permanent reallocations of resources between fimds of the reporting entity are classified as interfimd transfers. For the purposes of the statement of activities, all interfiind d-ansfers between individual govemmental funds have been eliminated.

20

VILLAGE OF CHATAIGNIER, LOUISIANA

Notes to Basic Financial Statements (Continued)

F. Budgets

A budget for the General Fund for the year ended June 30,2010 was adopted in accordance wifli LSA-R.S. 39:1301. cited as tiie "Louisiana Local Govemment Budget Act." Budgeted amounts included in the accompanying financial statements are as originally adopted or as finally amended by the Village.

G. Compensated Absences

The Village has no policy relating to compensated absences. Any liability the Village might have in this regard at June 30, 2010 is considered immaterial; therefore, no liability has been recorded in the accoimts.

(2) Cash and Interest-Bearing Deposits

Under state law, the Village may deposit fimds within a fiscal agent bank organized under the laws of the State of Louisiana, the laws of any other state in the Union, or the laws of the United States. The Village may invest in certificates and time deposits of state banks organized under Louisiana law and national banks having principal offices in Louisiana. At June 30,2010, the Village has cash and interest-bearing deposits (book balances) totaling $95,090 as follows:

Demand deposits $ 16,301 Interest bearing deposits 78,789

Total $ 95,090

Custodial credit risk for deposits is the risk that in the event ofthe failure of a depository financial institution, the Village's deposits may not be recovered or will not be able to recover the collateral securities that are in the possession of an outside party. Under state law, these deposits (or the resulting bank balances) must be secured by federal deposit insurance or the pledge of s«:urities owned by the fiscal agent bank. The market value of the pledged securities plus the federal deposit insurance must at all times equal the amount on deposit with the fiscal agent bank. These securities are held in the name ofthe pledging fiscal agent bank in a holding or custodial bank that is mutually acceptable to both parties. As of June 30, 2010, bank balances in the amount of $96,442 were secured in total by federal deposit insurance.

(3) Receivables

Receivables at June 30,2010 of $9,574 consist ofthe following:

General Sewer Total Accounts Franchise tax Sales tax Other

Totals

21

$ -2,307 1,468 1,485

$5,260

$4,314 ---

$4,314

$4,314 2,307 1,468 1,485

$9,574

VILLAGE OF CHATAIGNIER, LOUISIANA

Notes to Basic Financial Statements (Continued)

(4) Ad Valorem Taxes

Ad valorem taxes attach as an enforceable lien on property as of Januaiy 1 of each year. Taxes are levied in September or October and billed to the t^ayers in December. Billed taxes become delinquent on January 1 ofthe following year.

For the year ended June 30,2010, taxes of 5.85 mills were levied on properly with assessed valuations totaling $778,080. Total taxes levied were $4,552.

(5) Capital Assets

Capital asset activity for the year ended June 30,2010 was as follows:

Govemmental activities: Land Buildings and improvements Equipment Street Improvements

Totals

Less: accumulated depreciation Buildings and improvements Equipment Street Improvements

Total accumulated depreciation

Govemmental activities, capital assets, net

Business-type activities: Land Systems and extensions Equipment

Totals Less accumulated depreciation

Business-type activities, capital assets, net

Balance 6/30/2009

$ 25,964 300,902 101,096 343,648

771,610

219.818 92,743

101,494

414,055

$357,555

$ 10.000 .1,035,584

5.236

1,050.820 532,918

$ 517,902

Addtions Deletions

$ - $ -----,

3,236 8,353

17,183

28,772

$ (28.772) $ -

$ - $----

25,890

$(25,890) $ -

Balance 6/30/2010

$ 25.964 300.902 101,096 343.648

771,610

223,054 101,096 118,677

442.827

$328,783

$ 10,000 1,035,584

5,236

1,050,820 558,808

$ 492,012

22

VILLAGE OF CHATAIGNIER, LOUISIANA

Notes to Basic Financial Statements (Continued)

(6) Board Members' Compensation

The Village paid the mayor and aldermen the following salaries:

Herman Malveaux $3,600 Joseph Semien 1,200 Lucy Green 1,200 Alton Thomas, Jr. 1,200

$7.200

(7) Risk Management

The Village is exposed to risks of loss in the areas of general and auto liability, {property hazards and workers* compensation. All of these risks are handled by purchasing commercial insurance coverage. There have been no significant reductions in the insurance coverage during the year.

23

REQUIRED SUPPLEMENTARY INFORMATION

24

VILLAGE OF CHATAIGNIER, LOUISIANA General Fund

Revenues: Taxes Licenses and permits Franchise tax Intergovemmental Fines and forfeitures Interest Miscellaneous

Total revenues

Expenditures: Current-- General govemment

Public safety PubHc works Culture and recreation

Total expenditures

Excess of revenues

over expenditures

Fund balance, beginning

Fund balance, ending

Budgetary Comparison Schedule Year Ended June 30. 2010

Budget Original

$ 23,000 6.500

16,000 2.970 8,000 2,249 6,973

65,692

33,908 10,000 7,832 3,273

55,013

10,679

94,072

$104,751

Final

$ 26,824 6.974

17,317 2,970 2,200 3,333 6,375

65.993

37,064 10,500 5,429 2,986

55.979

10,014

94.072

$ 104.086

Actual

$ 25,054 8,047

17.334 3,318 2.470 1,403 6,375

64,001

37,445 10,238 14,929 1.093

63.705

296

94,072

$ 94,368

Variance with Final Budget

Positive (Negative)

$(1,770) 1,073

17 348 270

(1.930) -

(1,992)

, (381) 262

(9,500) 1.893

(7.726)

(9.718)

_

$(9,718)

See accountants' report.

25

OTHER SUPPLEMENTARY INFORMATION

26

VILLAGE OF CHATAIGNIER, LOUISIANA

Schedule of Insurance in Force June 30.2010

Description of Coverage

Workmen's Compensation: Louisiana Worker's Compensation Corporation

Commercial property insurance: Office building - 113-117 First Street P̂ lbUc Library - 6215 Charles Armand Jr. Street

Automobile liability

Commercial general liability

Errors and omissions

Law enforcement officer

Expiration Coverage Date Amounts

Statutory

11/22/10 11/22/10

12/6/10

12/6/10

12/6/10

12/6/10

85,000 40,000

500,000

500.000

500.000

500,000

27

INTERNAL CONTROL AND COMPLIANCE

28

H .2

^ 5 I I

if S «* L-

AS ^ A

00

c

1 o o

•a

o c

I

I

VD O O

U

o

I tn

1 c o

I

9.s i

^

IO o o

I o U

O

ON

73

O P

I tcj

c o u

B

o O "eo

E 0^