F.Lançon - CIRAD - World Rice Conference 2009 1

Will Growing Sub-Saharan African Rice Production Reduce

Imports?

Frédéric LançonARENA research unitCIRAD

World Rice Conference 2009Oct. 27-29 Cebu, PhilippinesShangri-La's Mactan Resort

[email protected] de coopérationinternationale en rechercheagronomique pour le développement

F.Lançon - CIRAD - World Rice Conference 2009 2

Plan of the presentation

1. The Recurring Sub-Saharan (SSA) rice challenge

2. Determining factors for promoting rice production development

F.Lançon - CIRAD - World Rice Conference 2009 3

1. The Recurring Sub-Saharan rice challenge

F.Lançon - CIRAD - World Rice Conference 2009 4

A renewed agenda for rice in SSA

Rice price surge put several SSA governments in a difficult political position:

Not able to ensure a steady supply of rice at affordable price.Limited capacity to address the issue at short term:

• Tariff and tax revision• Budgetary constraints

Renewed interest for expanding rice production since rice world market evolutions are unpredictable

F.Lançon - CIRAD - World Rice Conference 2009 5

Beyond the short term perspective…

Social unrests were not necessarily triggered by rice price increase on the world market.

Delay in transmission of priceSeveral countries had already considered revising their rice trade policy before the price surge:

Common Exterior Tariff negotiation within Economic Community of West African Sate

F.Lançon - CIRAD - World Rice Conference 2009 6

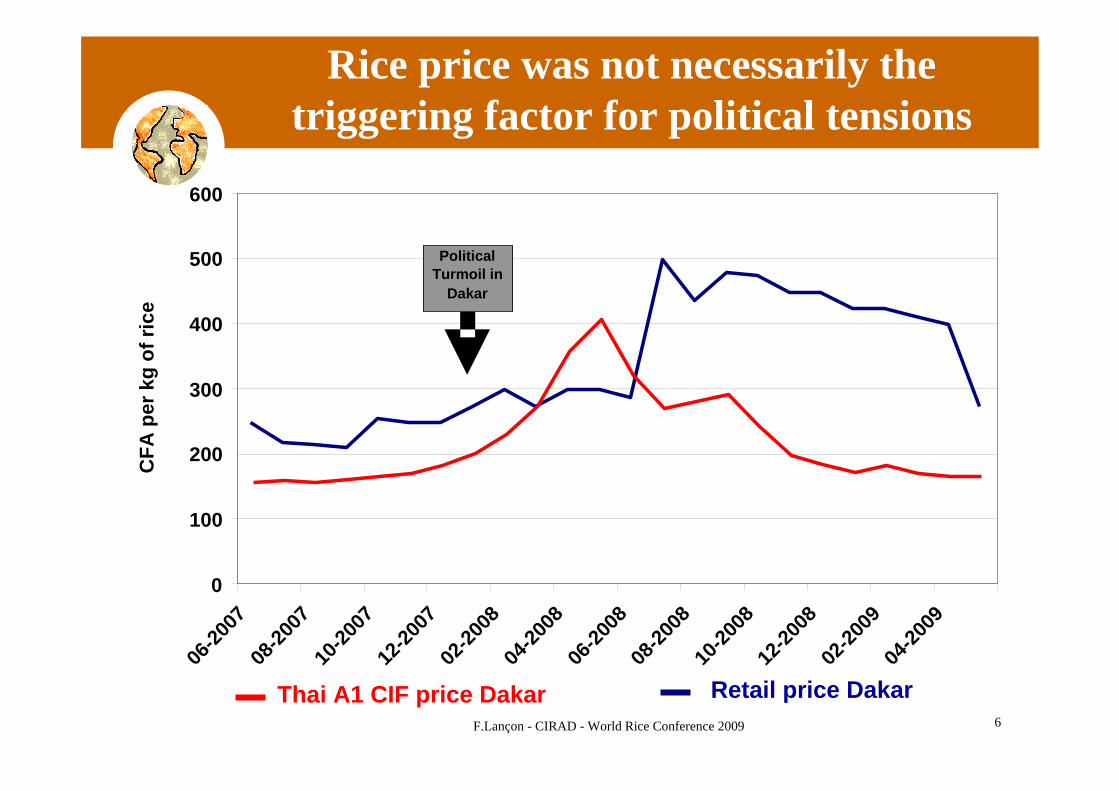

Rice price was not necessarily the triggering factor for political tensions

0

100

200

300

400

500

600

06-20

0708

-2007

10-20

0712

-2007

02-20

0804

-2008

06-20

0808

-2008

10-20

0812

-2008

02-20

0904

-2009

CFA

per

kg

of ri

ce

Retail price DakarThai A1 CIF price Dakar

PoliticalTurmoil in

Dakar

F.Lançon - CIRAD - World Rice Conference 2009 7

The end of the cheap rice era?

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

0

100

200

300

400

500

600

700

800

900

Rice 25% (USD/ton)Rice Import (‘000 Tons)

F.Lançon - CIRAD - World Rice Conference 2009 8

Supply and demand trends (1990-2007)

Total SSA production increased at 4.8% per year:

Mostly because of area expansion: 3.8%Limited contribution of yield increase: 1%

Total SSA consumption increased at 5.4% per year due to:

Population growth: 2.5%And per capita consumption growth: 2.9%

F.Lançon - CIRAD - World Rice Conference 2009 9

Emerging markets and import dependency

Angola

BeninBurkina Faso

Cameroon

ChadCongo,

Côte d'Ivoire

Gambia

Ghana

GuineaGuinea-Bissau

KenyaLiberia

MadagascarMalawi Mali

MozambiqueNiger

Nigeria

Senegal

Sierra Leone

South Africa

Sudan

Tanzania

Togo

Zambia

0%

20%

40%

60%

80%

100%

120%

0 20 40 60 80 100 120 140

Per capita consumption (kg)

Import share in total supply

%

F.Lançon - CIRAD - World Rice Conference 2009 10

An accelerated rice growth in East Africa, but…

0%1%2%3%4%5%6%7%8%9%

Growth rate

1990 - 19992000 - 2007-9%

-7%-5%-3%-1%1%3%5%7%9%

Western Eastern Middle Southern

Total Consumption

Production

F.Lançon - CIRAD - World Rice Conference 2009 11

….West Africa is still dominant

Total production: 14 200 000 tons

Average values 2000 -2009FAOSTAT

Western63%

Eastern25%

Middle6%

Southern6%

Western66%

Eastern15%

Middle8%

Southern11%

Total imports: 7 200 000 tons

F.Lançon - CIRAD - World Rice Conference 2009 12

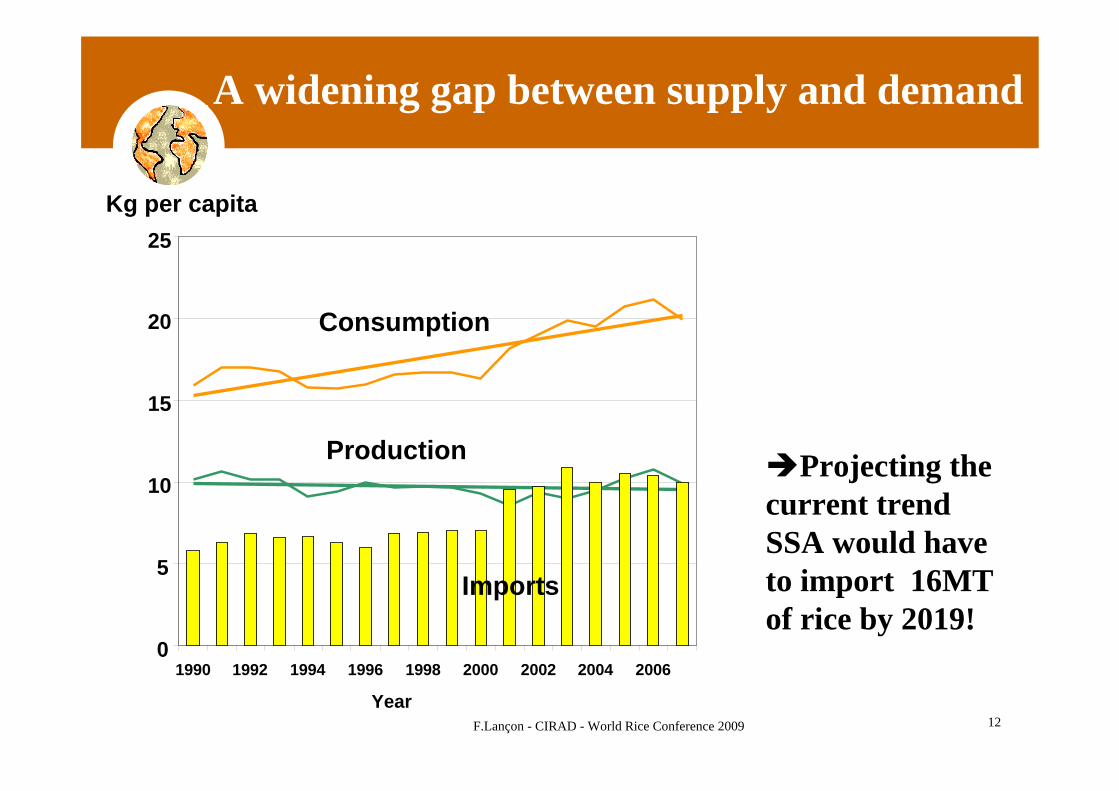

A widening gap between supply and demand

0

5

10

15

20

25

1990 1992 1994 1996 1998 2000 2002 2004 2006

Year

Kg per capita

Imports

Production

Consumption

Projecting the current trend SSA would have to import 16MT of rice by 2019!

F.Lançon - CIRAD - World Rice Conference 2009 13

Is per capita rice consumption growth reversible?

Example of CFA devaluation:Reduction of other staple and side dishes.

Substitution with other staples is limited due:to the higher convenience of rice compared to other

staples,unstable supply in urban markets of locally produced

staples.

Focus should be put on rice domestic supply and diet diversification.

F.Lançon - CIRAD - World Rice Conference 2009 14

1. The Recurring Sub-Saharan rice challenge

2. Determining factors for promoting rice production development.

F.Lançon - CIRAD - World Rice Conference 2009 15

Determining factors for a Sub-Saharan Rice Strategy

1. Technology development2. Cost-effectiveness of proposed

technical solutions: the macro-economic setting.

3. Institutional changes and enabling environment for building a competitive market for local rice.

F.Lançon - CIRAD - World Rice Conference 2009 16

Managing a wide range of rice cropping systems

Water table

-Dry Land-Rainfed

-HydromorphIc - Low Land - Swamp-Flooded

-Simple low land

-Improved low-land

- Irrigated

source: WARDA – 1999

F.Lançon - CIRAD - World Rice Conference 2009 17

Non-irrigated systems are dominant

Agro- ecologicalzones Swamp Flooded Irrigated

Inlandvalley Rainfed Total

Savana and Sahel 0.1% 4.5% 7.5% 1.8% 0.2% 14.1%Humid 3.1% 3.7% 3.1% 28.3% 47.8% 85.9%Total 3.2% 8.1% 10.6% 30.1% 48.0% 100.0%

Savana and Sahel 0.2% 2.7% 20.4% 2.2% 0.1% 25.5%Humid 3.7% 2.2% 5.6% 34.1% 28.9% 74.5%Total 3.9% 4.9% 25.9% 36.3% 29.0% 100.0%

Areas

Production

West Africa

Source, WARDA, 1998

F.Lançon - CIRAD - World Rice Conference 2009 18

Technology development

It is a challenging task (long term)Promising opportunities provided by the dissemination of the NERICA (New Rice for Africa)Other technologies have been developed for improving , pest and crop management.

Yet, other determining factors may hindered the SSA countries capacities to benefit from the NERICA

F.Lançon - CIRAD - World Rice Conference 2009 19

CASAMANCE

RIVER SENEGAL

0,9

SIERRA LEONE NORTH

SIERRA LEONE SOUTH

CdI NORTH

CdI N- WEST

CdI WEST

CdI S-WEST

OFFICE DU NIGERMOPTI

SIKASSO

NIGER

Rice variable comparative advantages across West Africa

F.Lançon - CIRAD - World Rice Conference 2009 20

Cost effective technical solution

Largely determined by:Yield achievedPrevailing price on the world market

Better prospects for cost-effective technologies

Several ecologies are achieving better economic performance.Comparative advantage threshold is about USD 300 to USD 350 per ton of rice, FOB Bangkok.

F.Lançon - CIRAD - World Rice Conference 2009 21

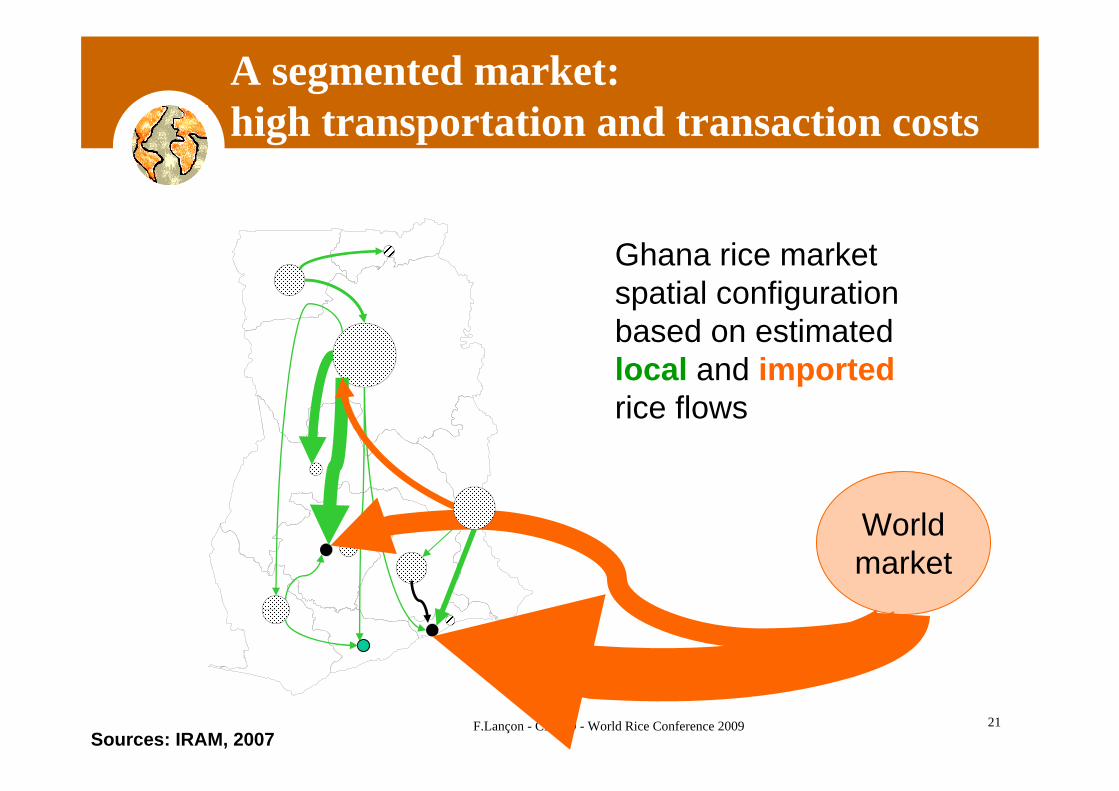

Northern

A segmented market: high transportation and transaction costs

World market

Ghana rice market spatial configuration based on estimated local and imported rice flows

Sources: IRAM, 2007

F.Lançon - CIRAD - World Rice Conference 2009 22

West African Consumers justifications for purchasing imported rice

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

COTE D’IVOIRE NIGERIA

Other organolepticproperties

Nutritious properties

Taste

Cooking easiness

Swelling capacity

Cleanliness and appearance

Availability

Price

Percentage of responses

Increasing consumers’ awareness for quality

Sources: WARDA- Africa Rice Centre, 2001 and 2003

Import price < local price Import price > local price

F.Lançon - CIRAD - World Rice Conference 2009 23

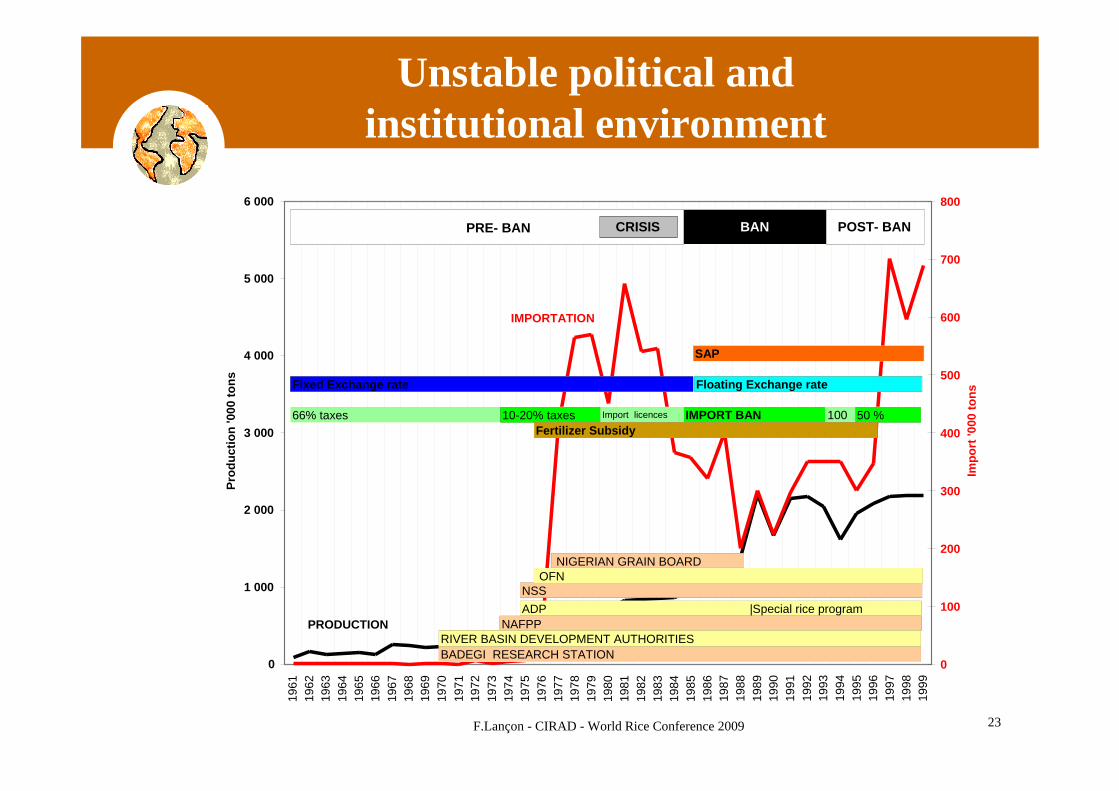

Unstable political and institutional environment

0

1 000

2 000

3 000

4 000

5 000

6 000

1961

1962

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

Prod

uctio

n '0

00 to

ns

0

100

200

300

400

500

600

700

800

Impo

rt '0

00 to

ns

PRODUCTION

IMPORTATION

BADEGI RESEARCH STATION

NAFPP

NSSOFN

RIVER BASIN DEVELOPMENT AUTHORITIES

ADP |Special rice program

NIGERIAN GRAIN BOARD

66% taxes 10-20% taxes Import licences IMPORT BAN 100%

50 %

SAP

Fixed Exchange rate Floating Exchange rate

Fertilizer Subsidy

BANPRE- BAN CRISIS POST- BAN

F.Lançon - CIRAD - World Rice Conference 2009 24

Concluding remarks

Rice development in SSA remains a major challenge:Although: (+ + +)

Proven and promising technologies have been developed.The macro-economic setting is more favorable than in the past decadesPolicy makers and donors are more sensitive to the issue

Yet: ( - - - -)Weak market linkages and institutions do not provide a competitive hedge to local rice production.Quick technical integrated solution such as large scale agro-industrial rice scheme might not feasible or sustainableIt requires a long term commitment from decision makers.

If consumption expand at the same pace, stabilizing rice import volume would be an significant achievement.

F.Lançon - CIRAD - World Rice Conference 2009 25

Thank you

F.Lançon - CIRAD - World Rice Conference 2009 26

Mature and emerging markets

Angola

Benin

Burkina FasoCameroon

Chad

Congo,

Côte d'Ivoire

Gambia

GhanaGuinea

Guinea-BissauKenya

LiberiaMadagascar

Malawi

MaliMozambique

Niger

Nigeria

Senegal

Sierra LeoneSouth AfricaSudan

Tanzania

Togo

Zambia

-10%

-5%

0%

5%

10%

15%

20%

25%

0 20 40 60 80 100 120 140Per capita consumption (kg)

Per capita cons. growth rate

% per year

F.Lançon - CIRAD - World Rice Conference 2009 27

A contrasted situation across the sub-continent

Index value0.30 - 0.60 (9)0.15 - 0.30 (10)0.10 - 0.15 (15)0.00 - 0.10 (9)

Index value0.30 - 0.60 (9)0.15 - 0.30 (10)0.10 - 0.15 (15)0.00 - 0.10 (9)

source: WARDA – 2001

F.Lançon - CIRAD - World Rice Conference 2009 28

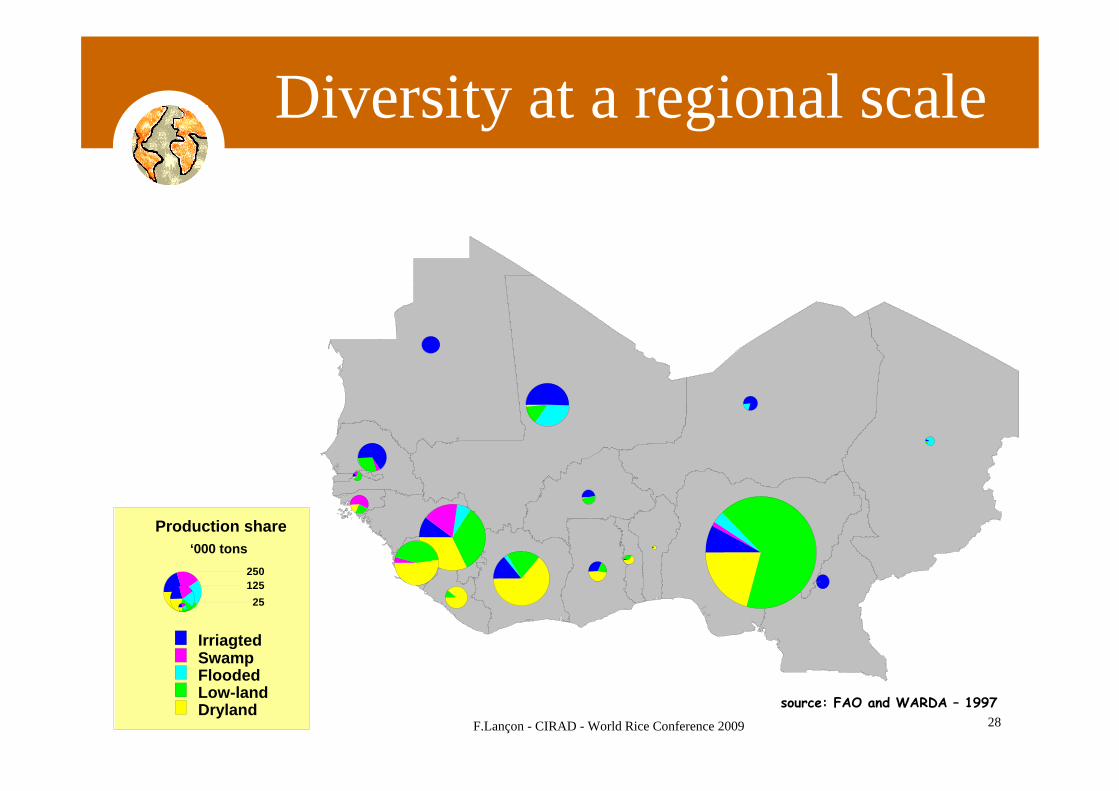

Diversity at a regional scale

Production share‘000 tons

250125

25

IrriagtedSwampFloodedLow-landDryland source: FAO and WARDA – 1997