drafting private company target merger agreements:...

TRANSCRIPT

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Presenting a live 90-minute webinar with interactive Q&A

Drafting Private Company Target Merger Agreements:

Risk Allocation, Reps and Warranties, and

Maximizing Indemnification Recourse Negotiating Risk Allocation Provisions in Private Mergers After Cigna v. Audax

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

THURSDAY, MARCH 3, 2016

Lisa J. Hedrick, Partner, Hirschler Fleischer, Richmond, Va.

Andrew M. Lohmann, Partner, Hirschler Fleischer, Richmond, Va.

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-888-450-9970 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can

address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email

that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926

ext. 35.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

Drafting Private Company

Target Merger Agreements: Risk Allocation, Reps and Warranties, and

Maximizing Indemnification Recourse

March 3, 2016

Presented by:

Andrew M. Lohmann

and

Lisa J. Hedrick

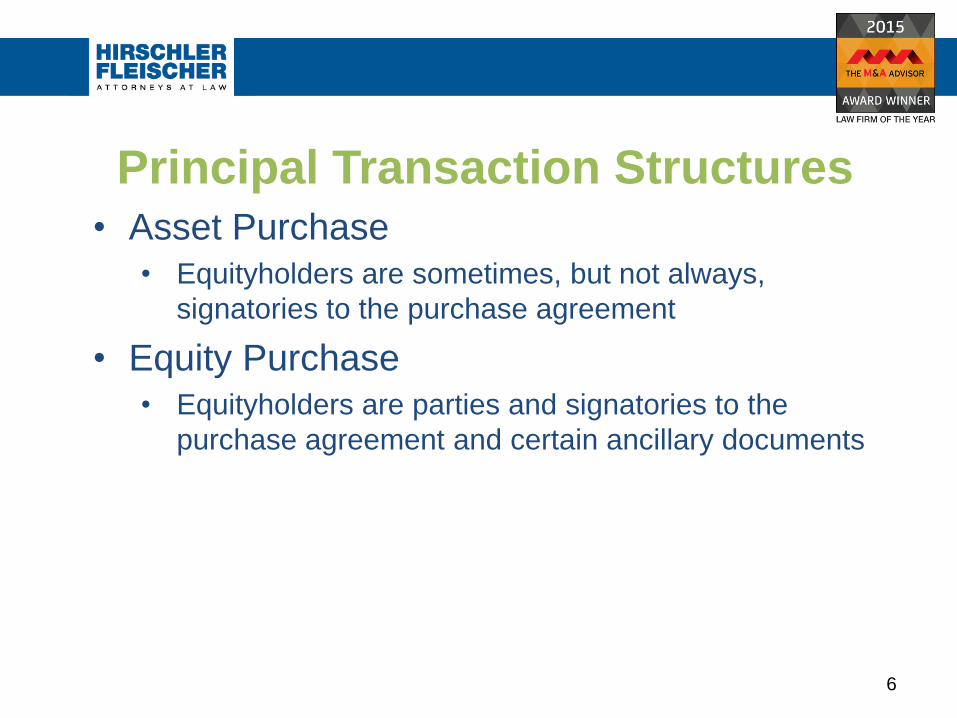

Principal Transaction Structures • Asset Purchase

• Equityholders are sometimes, but not always,

signatories to the purchase agreement

• Equity Purchase

• Equityholders are parties and signatories to the

purchase agreement and certain ancillary documents

6

Principal Transaction Structures • Merger

• Direct or indirect / triangular

• Typically requires mere majority consent of

stockholders

• Shares may be converted into merger consideration

without consent and signature of all stockholders

• Non-signatory stockholders may not be bound to

pertinent provisions in merger agreement

7

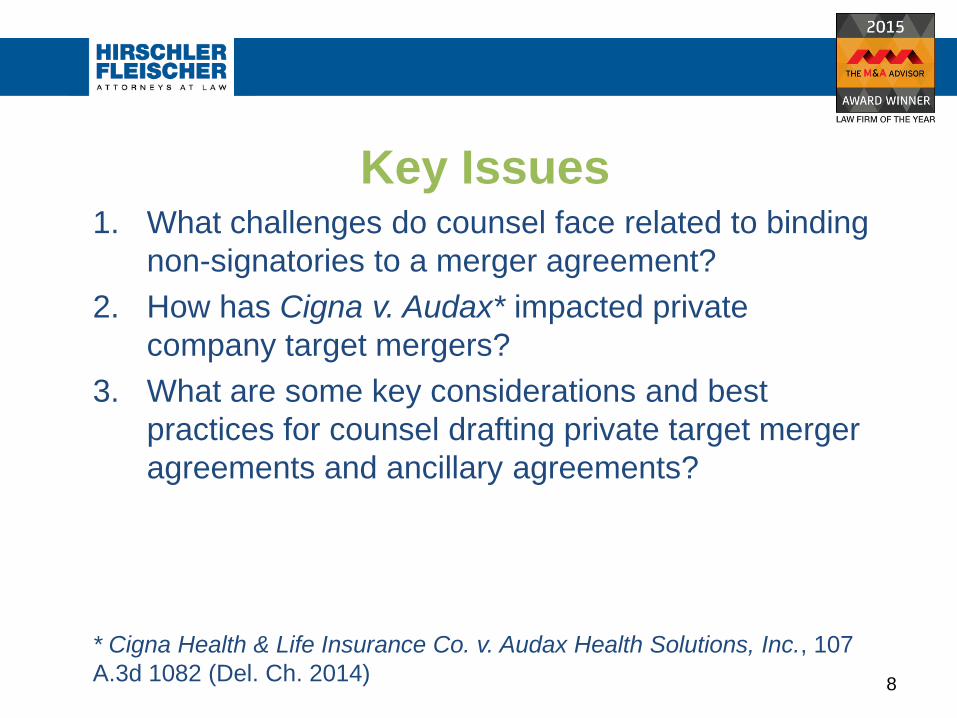

Key Issues 1. What challenges do counsel face related to binding

non-signatories to a merger agreement?

2. How has Cigna v. Audax* impacted private

company target mergers?

3. What are some key considerations and best

practices for counsel drafting private target merger

agreements and ancillary agreements?

* Cigna Health & Life Insurance Co. v. Audax Health Solutions, Inc., 107

A.3d 1082 (Del. Ch. 2014)

8

Theories of Binding

Non-signatories • Agency exception

• Third party beneficiary exception

• Joinder exception / intent to be bound

• Estoppel exception

• “Facts Ascertainable” outside the merger

agreement (DGCL§251(b))

Binding Non-signatories

9

DGCL§251(b) Any of the terms of the agreement of merger or

consolidation may be made dependent upon facts

ascertainable outside of such agreement, provided that

the manner in which such facts shall operate upon the

terms of the agreement is clearly and expressly set

forth in the agreement of merger or consolidation. The

term “facts,” as used in the preceding sentence,

includes, but is not limited to, the occurrence of any

event, including a determination or action by any

person or body, including the corporation.

Binding Non-signatories

10

DGCL§251(b) The [merger] agreement shall state … (5) The manner,

if any, of converting the shares … or of cancelling some

or all of such shares, and, if any shares of any of the

constituent corporations are not to remain outstanding,

... the cash, property, rights or securities of any other

corporation or entity which the holders of such shares

are to receive in exchange for, or upon conversion of

such shares and the surrender of any certificates

evidencing them….

Binding Non-signatories

11

Letter of Transmittal • Solution prior to Cigna

• Ancillary agreement signed by holders to

facilitate the holder’s transmittal of its shares

and receipt of merger consideration

• Expanded to commit non-signatory holders

to various post-closing obligations

Binding Non-signatories

12

Prior Cases • Aveta v. Cavallieri (2010)

• Delaware Chancery Court held post-closing price

adjustment procedures complied with DGCL§251(b)

• Purchase price adjustments were tied to company’s

financial statements and did not place 100% of merger

consideration at risk for indefinite time period

• In re Openlane (2011)

• Delaware Chancery Court upheld merger transaction in

which part of merger consideration was placed in escrow to

satisfy target stockholders’ post-closing indemnification

obligations to buyer

Binding Non-signatories

13

Background of Cigna • Optum agreed to acquire Audax Health

Solutions, Inc. (Audax) by merger

• Cigna, a preferred stockholder of Audax, did not:

• Sign merger agreement;

• Vote in favor of merger;

• Sign support agreement executed by consenting

holders; or

• Sign a letter of transmittal

• Receipt of merger consideration conditioned

upon execution of transmittal letter after merger

Impact of Cigna v. Audax

14

Cigna v. Audax Merger Structure

Audax Health Solutions

Stockholders of Target

Optum Services

Audax Holdings

Holding Co. merges

into Target

Merger Consideration

15

Cigna v. Audax Merger Structure

Former Stockholders (including Cigna)

$$$

Optum Services

Audax Health Solutions

100%

16

“Obligations” in Cigna

Transmittal Letter 1. General release of claims

• Not referenced in merger agreement

2. Indemnification obligations

• Some obligations survived indefinitely

• Potentially 100% of merger consideration

subject to clawback

3. Appointment of stockholder representative

Impact of Cigna v. Audax

17

Cigna Holdings 1. Release obligation held unenforceable for

lack of consideration

2. Open-ended indemnification obligation

violated DGCL§251(b) – Cigna not bound

• Value of merger consideration not ascertainable

due to uncertain amount of consideration

subject to indefinite clawback and indefinite

survival period for fundamental representations

3. Court declined to rule on validity of

appointment of stockholder representative

Impact of Cigna v. Audax

18

Limitations on Cigna Holdings “Limited holding” – opinion does not

concern/address:

• Escrow agreements (e.g., Openlane)

• General validity of post-closing price adjustments

requiring direct repayments from stockholders

• Validity of time-limited price adjustments that cover full

merger consideration

• Validity of price adjustments with indefinite duration that

cover only a portion of merger consideration (court did

not invalidate right to clawback for breaches of non-

fundamental representations)

Impact of Cigna v. Audax

19

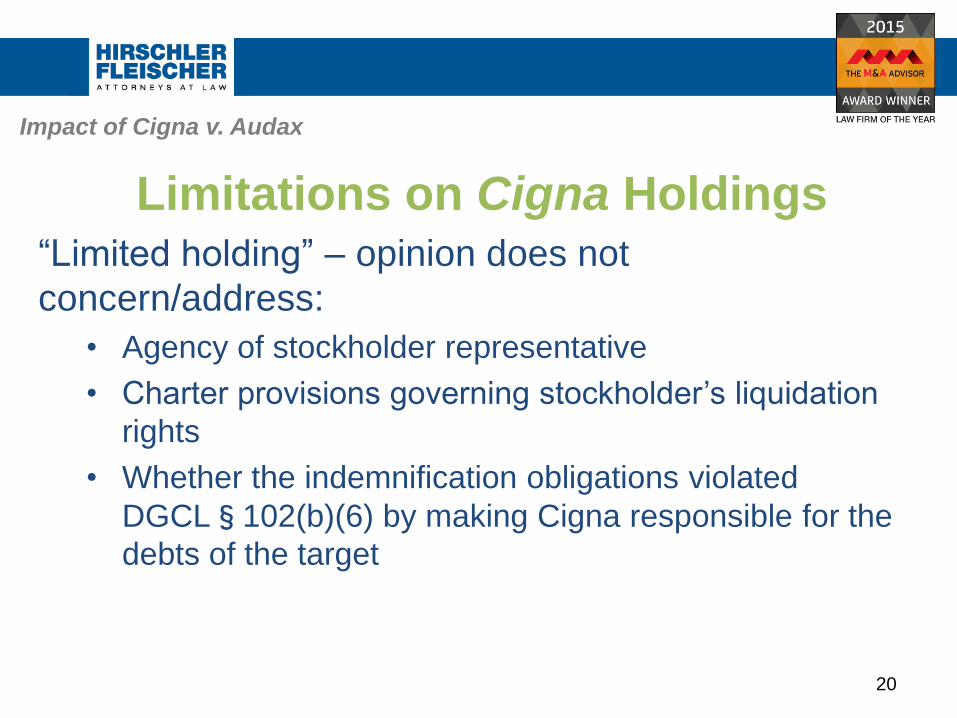

Limitations on Cigna Holdings “Limited holding” – opinion does not

concern/address:

• Agency of stockholder representative

• Charter provisions governing stockholder’s liquidation

rights

• Whether the indemnification obligations violated

DGCL§102(b)(6) by making Cigna responsible for the

debts of the target

Impact of Cigna v. Audax

20

Cigna Takeaways 1. Support / Joinder Agreements

• Secure joinders expressly agreeing to merger terms

• Condition closing on execution by a particular % of holders

• Consider specifying that holders will receive additional

consideration if they execute agreement

2. Escrow / Holdback Structure

• Set aside funds in escrow account to secure

indemnification and purchase price adjustment obligations

• Accelerate escrow releases as target holders become

parties to support agreements

3. Representations and Warranties Insurance

• Covers liabilities in excess of escrow amount

Best Practices

21

Cigna Takeaways 4. Pro Rata Formulas

• Require signatories to pay for more than their pro rata share of

indemnity obligations to make up for hold outs

• Particularly useful with respect to uncapped and indefinite

fundamental representations

5. Tie Contingent Payments / Clawback Rights to

“Merger Consideration”

6. Be Careful with “Indefinite” Survival Periods of

Uncapped Indemnities

7. Include Releases and Other Substantive Provisions in

Merger Agreement

8. Attach Form Letter of Transmittal to Merger Agreement

Best Practices

22

Preventative Measures 1. Drag-Along Rights

• Review investor and stockholder agreements for drag-

along obligations that require holders to abide by

obligations ancillary to merger

• Ensure majority holders exercise rights in accordance with

strict terms of the applicable drag-along provision

• In Halpin v. Riverstone National, Inc., the Delaware

Chancery Court refused to enforce terms of a drag-along

provision because consent was sought after the

consummation of the merger

• Increase use of provisions on sell-side

2. Utilize Non-Equity Incentive Plans

Best Practices

23

Merger Agreement Provisions

• Purchase price adjustments

• 86% of transactions include post-closing

purchase price adjustments; most of which

are based on working capital (83%)*

• Inclusion of working capital sample

• Mechanics for failing to timely deliver working

capital true-up post-closing

*Statistics from the American Bar Association’s 2015 Private Target Mergers &

Acquisitions Deal Points Study

Best Practices

24

Merger Agreement Provisions

• Earn-outs

• 26% of transactions include earn-outs*

• Covenants for post-closing operation of the

business and maximizing earn-out payments

• Courts will enforce unambiguous contractual

language (See generally, Lazard Technology

Partners, LLC v. Qinetiq North America

Operations LLC (Del. 2015); Fortis Advisors LLC

v. Dialog Semiconductor PLC (Del. Ch. 2015))

*Statistics from the American Bar Association’s 2015 Private Target Mergers &

Acquisitions Deal Points Study

Best Practices

25

Merger Agreement Provisions

• Escrows and holdbacks • Approximately 75% of transactions include escrow or

holdback*

• 25% of transactions with post-closing purchase price

adjustments contain separate adjustment escrow or

holdback*

• Average escrow or holdback was 9.14% of transaction

value*

*Statistics from the American Bar Association’s 2015 Private Target Mergers &

Acquisitions Deal Points Study

Best Practices

26

Merger Agreement Provisions

• Representations and warranties: no

undisclosed liabilities

Target has no liability of any type that is required to be reflected on

a balance sheet prepared in accordance with GAAP except for…

(iii) liabilities that can be categorized into another subject matter

addressed by other representations and warranties contained in

this Article, it being agreed that the intention of this clause (iii) is to

prevent the representations and warranties of this Section from

circumventing or expanding the scope and limitations of such

other representations and warranties, taking into account any

knowledge, materiality and Material Adverse Effect qualifications

or any dollar thresholds set forth therein.

Best Practices

27

Merger Agreement Provisions

• No other representations / non-reliance

• See e.g., TrueBlue, Inc. v. Leeds Equity

Partners IV, LP (Del. Super. 2015); Prairie

Capital III, LP v. Double E Holding Corp. (Del.

Ch. 2015)

• Definition of “Material Adverse Effect”

• Include objective parameters

Best Practices

28

Merger Agreement Provisions

• Indemnification – Materiality Scrape

“Double” Materiality Scrape: For purposes of this Article

(Indemnification), any inaccuracy in or breach of any

representation or warranty and any Losses resulting therefrom

shall be determined without regard to any materiality, Material

Adverse Effect or other similar qualification contained in or

otherwise applicable to such representation or warranty.

Loss-Only Scrape: For purposes of calculating Losses incurred in

connection with any inaccuracy in or breach of any representation

or warranty (but not for purposes of determining any such

inaccuracy or breach), any and all references to materiality,

Material Adverse Effect or other similar qualification shall be

disregarded.

Best Practices

29

Stockholder Representative

• Purchase price adjustments

• Escrow and holdback arrangements

• Responding to indemnification claims

• Settling claims

• Funding for payment of expenses

• Replacement and removal

Best Practices

30

Related Cases

• Bailey v. Astra Tech (2013)

• Massachusetts Appeals Court held that

stockholder representative did not preclude

stockholders from directly settling claims with

acquirer

• SRS v. Sandoz (2013)

• New York federal court prevented stockholder

representative from filing a fraud claim on

behalf of selling stockholders

Best Practices

31

Andrew M. Lohmann

804.771.9572

Lisa J. Hedrick

804.771.9554

©2016 Hirschler Fleischer. These materials have been prepared for informational purposes only and

are not legal advice. This information is not intended to create an attorney-client or similar

relationship. Please do not send us confidential information. Past successes cannot be an assurance

of future success. Whether you need legal services and which lawyer you select are important

decisions that should not be based solely upon these materials. Contact: James L. Weinberg,

President, Hirschler Fleischer, The Edgeworth Building, 2100 East Cary Street, Richmond, Virginia

23223, 804.771.9500

Questions and Comments?

32