driving enterprisedriving enterprise growth in an...

TRANSCRIPT

Driving EnterpriseDriving Enterprise Growth in an Evolving Health Care Market

Larry MerloPresident &Chi f E ti OffiChief Executive Officer

Agenda

Our Compelling Value PropositionOur Compelling Value PropositionOur Compelling Value PropositionOur Compelling Value Proposition

Evolving Health Care Market Creates OpportunitiesEvolving Health Care Market Creates Opportunities

Strategic Framework for Long-term Enterprise GrowthStrategic Framework for Long-term Enterprise Growth

2

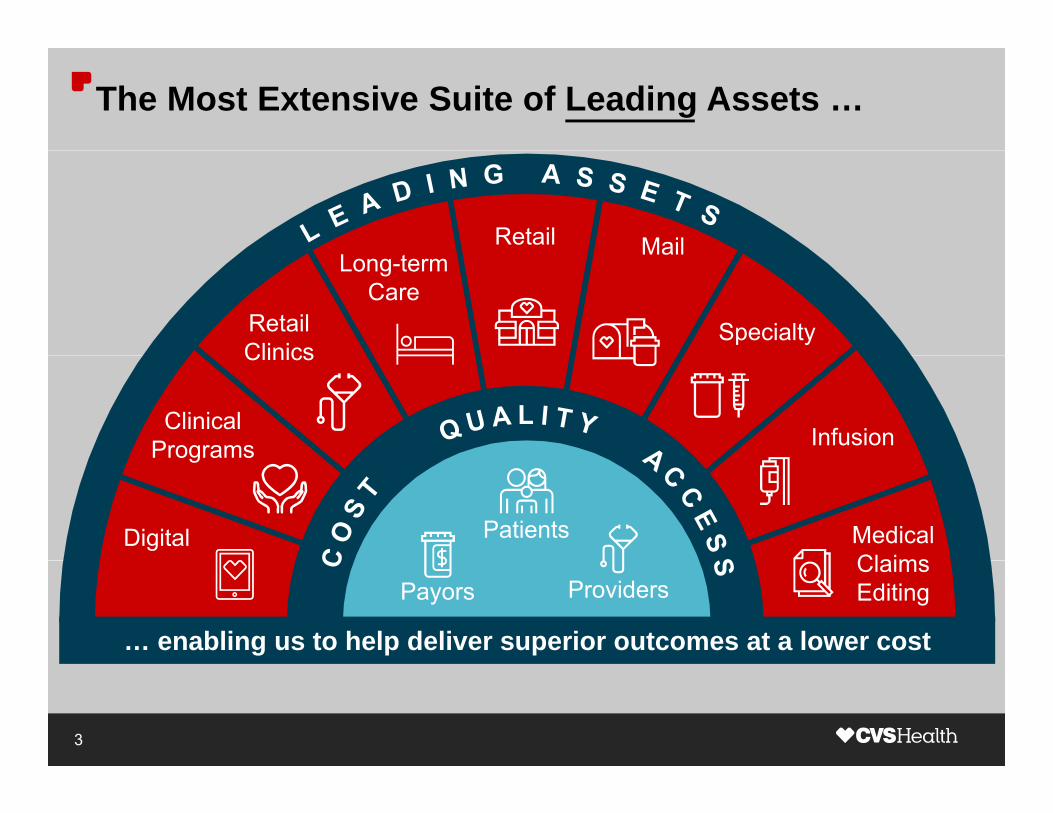

The Most Extensive Suite of Leading Assets …

Retail MailMailLong-term

CareRetailClinics

Specialty

Infusion

Clinics

Clinical Programs

Patients Medical Claims

Digital

g

Payors ProvidersClaims Editing

… enabling us to help deliver superior outcomes at a lower cost

3

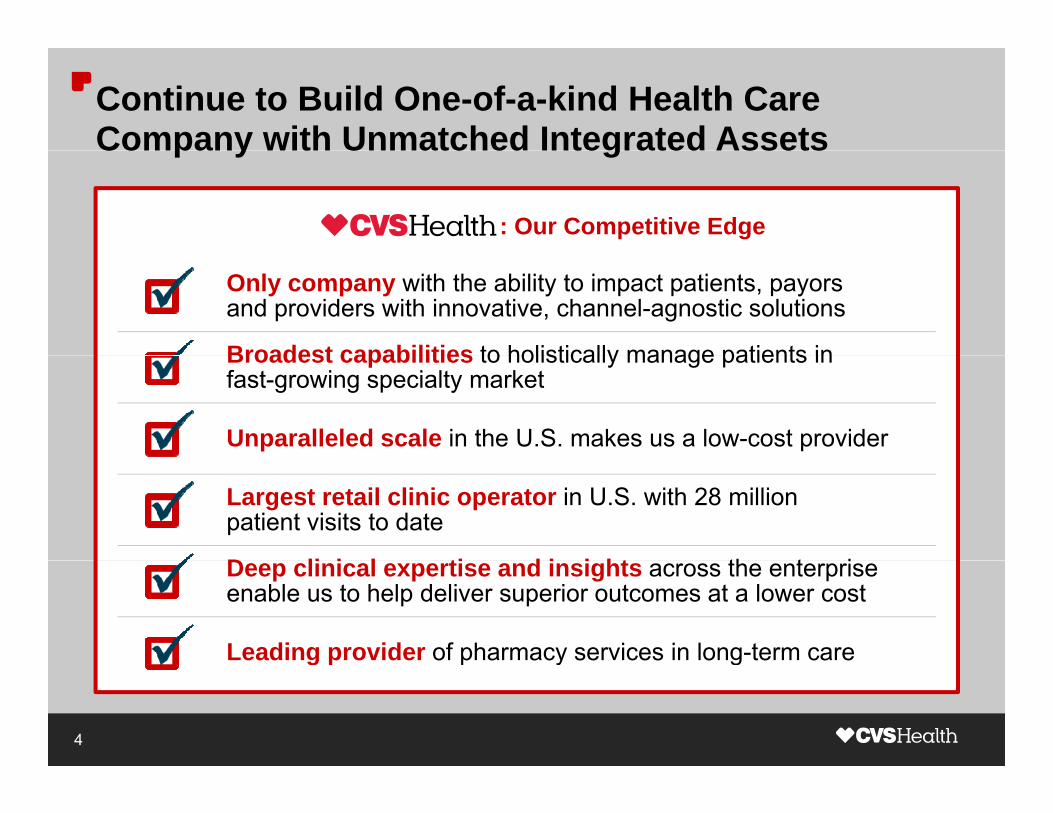

Continue to Build One-of-a-kind Health Care Company with Unmatched Integrated AssetsCompany with Unmatched Integrated Assets

: Our Competitive Edge

Only company with the ability to impact patients, payors and providers with innovative, channel-agnostic solutions

Broadest capabilities to holistically manage patients inBroadest capabilities to holistically manage patients infast-growing specialty market

Unparalleled scale in the U.S. makes us a low-cost provider

Largest retail clinic operator in U.S. with 28 million patient visits to date

D li i l ti d i i ht th t iDeep clinical expertise and insights across the enterpriseenable us to help deliver superior outcomes at a lower cost

Leading provider of pharmacy services in long-term care

4

g p p y g

Pharmacy Is Our Focus and We’ve Captured 39% of Past 5-Year Prescription Growthof Past 5 Year Prescription Growth

Total U.S. Rx Industry(Rx dispensed, billions)

5.5~710Mnew Rx

4.8

2010 2015E

5

Note:1. All prescriptions dispensed on a 30-day equivalent basis. Does not include Omnicare.Source: IMS data, CVS Health Internal Analysis.

Pharmacy Is Our Focus and We’ve Captured 39% of Past 5-Year Prescription Growthof Past 5 Year Prescription Growth

Total U.S. Rx Industry(Rx dispensed, billions)

5.5 CVS Healthshare of

market growth275M

~710Mnew Rx

4.8

market growth

39%

2010 2015E

Gaining share in a growing Rx industry

6

Note:1. All prescriptions dispensed on a 30-day equivalent basis. Does not include Omnicare.Source: IMS data, CVS Health Internal Analysis.

Prescription Growth Through Enterprise Channels Demonstrates Power of Unique, Integrated Model …Demonstrates Power of Unique, Integrated Model …

CVS/caremark Claims(Rx, millions)

9051,080 ~1,165

740905 Channel agnostic

offerings allow us to capture growth in

CVS/caremark claims

275 365 445 470

CVS/caremark claims while helping to drive

client savings

Notes:

2008 2011 2014 2015ECVS Health dispensed All other

Notes:1. CVS Health dispensed prescriptions include CVS/pharmacy, mail, CVS/specialty and Omnicare prescriptions across all years.2. CVS retail and mail prescriptions on a 30-day equivalent basis.3. 2015E is midpoint of guidance range.

7

… and Has Allowed Us to Capture 700 bps of Revenue Share, Equating to $7 BillionRevenue Share, Equating to $7 Billion

CVS/caremark Revenue($, billions)

70088

~100

$7

700 bpsincrease

=4459

$7 Billion

2008 2011 2014 2015E

48% 50% 53% 55%

Notes:

CVS Health share All other

Our outperformance in specialty is a key driver of revenue share gainsNotes:1. CVS Health share of CVS/caremark revenue equals CVS/caremark revenue dispensed through Enterprise channels (CVS/pharmacy, mail, CVS/specialty,

Omnicare) ÷ total CVS/caremark revenue.2. 2015E is midpoint of guidance range.

8

Agenda

Our Compelling Value Proposition

Evolving Health Care Market Creates OpportunitiesEvolving Health Care Market Creates Opportunities

Our Compelling Value Proposition

Evolving Health Care Market Creates OpportunitiesEvolving Health Care Market Creates Opportunities

Strategic Framework for Long-term Enterprise GrowthStrategic Framework for Long-term Enterprise Growth

9

Evolving Health Care Market Creates Opportunities

Demographics and Health Reform Continue to Transform the Market1 to Transform the Market

Specialty Growth Will Be Primary Driver of Pharmacy Trend

1

2

Retailization of Health Care Is Accelerating3

Increasing Focus on Outcomes4

5 Consolidation in the Health Plan Market5

10

Health Reform and Demographics Expanding Insured Population

1

Insured Population

Growth in U.S. Insured Lives(lives, millions)

1419 35286

306Individuals/Exchanges264

49 53 62

53 63 6514

Medicaid

Medicare

148 151 143 Employer-sponsored

2013 2015E 2019E

Medicare and Exchanges will be primary drivers

11

Source: CVS Health Internal Analysis; Medicare Trustees Report, 2015; Avalere Medicaid Model, September 2015; McKinsey MPACT 6.2, September 2014; CBO Public Exchange Estimates, March 2015; Accenture, 2015; Congressional Budget Office. Model assumes no additional Medicaid expansion in the 20 non-expansion states, further Medicaid expansion could improve long-term covered lives outlook. Figures may not foot due to rounding.

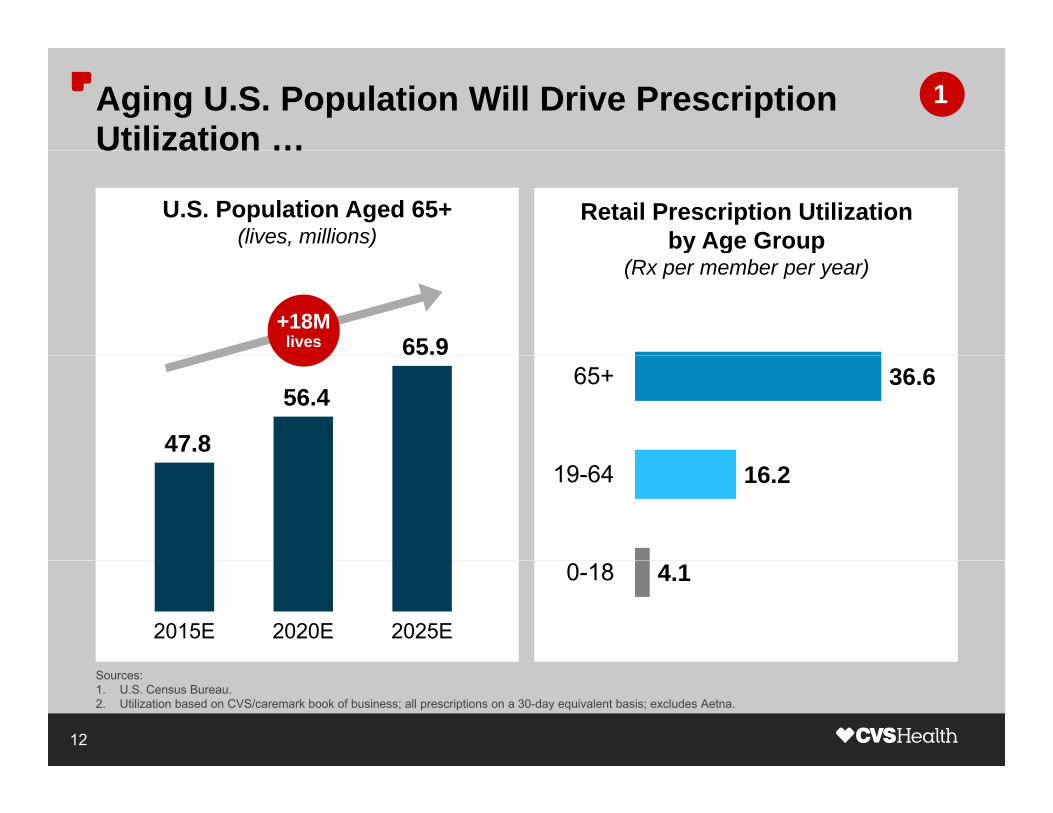

Aging U.S. Population Will Drive Prescription Utilization …

1

Utilization …

U.S. Population Aged 65+(lives, millions)

Retail Prescription Utilizationby Age Group

65.9

y g p(Rx per member per year)

+18Mlives

47.8

56.4 36.665+

16.219-64

2015E 2020E 2025E

4.10-18

Sources:1. U.S. Census Bureau.2. Utilization based on CVS/caremark book of business; all prescriptions on a 30-day equivalent basis; excludes Aetna.

12

… and Fuel Growth in Prescription Expenditures 1

U.S. Prescription Drug Expenditures($, billions)

464

5646.2%CAGR

328385

464

2015E 2018E 2021E 2024E

13

Source: CMS, Office of the Actuary, Prescription Drug Expenditures (figures as of July 30, 2015).

Pharmacy Is One of the Most Cost-efficient Ways to Manage Overall Health Care Costs

1

Ways to Manage Overall Health Care Costs

Healthcare Savings from Improved Adherence(PMPY)

Hyperlipidemia Diabetes Hypertension

$5,883 $5,676ROI9X ROI

9X

$3,311ROI5.5X

9X

($601) ($656) ($629)Added Rx spend Medical and productivity savings

14

Source: Roebuck MC, Liberman JN, Gemmill-Toyama M, Brennan TA. Medication adherence leads to lower health care use and costs despite increased drug spending. Health Affairs. 2011;30(1):91-99. Carls GS, Roebuck MC, Brennan TA, Slezak JA, Matlin OS, Gibson TB. Impact of medication adherence on worker productivity: an instrumental variables analysis in five chronic diseases. JOEM, 2012. Cholesterol savings from generic medications only.

CVS Health Can More Broadly Reach Patients Across the Continuum of Care

1

Across the Continuum of Care

CVS Health Standalone StandaloneCVS Health Retailer PBM

Retail pharmacy

Mail Order

Specialty/Infusion

LTC pharmacy

Retail clinics

Clinical programs

Channel connectivity

15

Growth in U.S. Population Over 85 Underscores Need for Long-term Care

1

Need for Long term Care

U.S. Population Aged 85+(lives, millions)

Omnicare is a leading pharmacy services provider to LTC facilities

11.9

• Nationwide footprint with leading positions in Assisted Living and Skilled Nursing facilities

~2X

6 37.5

g

• Ability to leverage clinical insights to improve care for patients

• CVS Health brings capabilities to6.3 CVS Health brings capabilities to better serve patients across the continuum of care

2015E 2025E 2035E

Source: U.S. Census Bureau.

16

Evolving Health Care Market Creates Opportunities

Demographics and Health Reform Continue to Transform the Market1 to Transform the Market

Specialty Growth Will Be Primary Driver of Pharmacy Trend

1

2

Retailization of Health Care Is Accelerating3

Increasing Focus on Outcomes4

5 Consolidation in the Health Plan Market5

17

Specialty Growth Will Be Primary Driver of Pharmacy Trend

2

Pharmacy Trend

Addressable Specialty Industry($, billions)

22014%CAGR

130

65

2012 2016E 2020E

18

Note:1. Addressable specialty industry currently excludes infused oncology.Source: NHE, Artemetrx, CVS Health Internal Analysis, 2015.

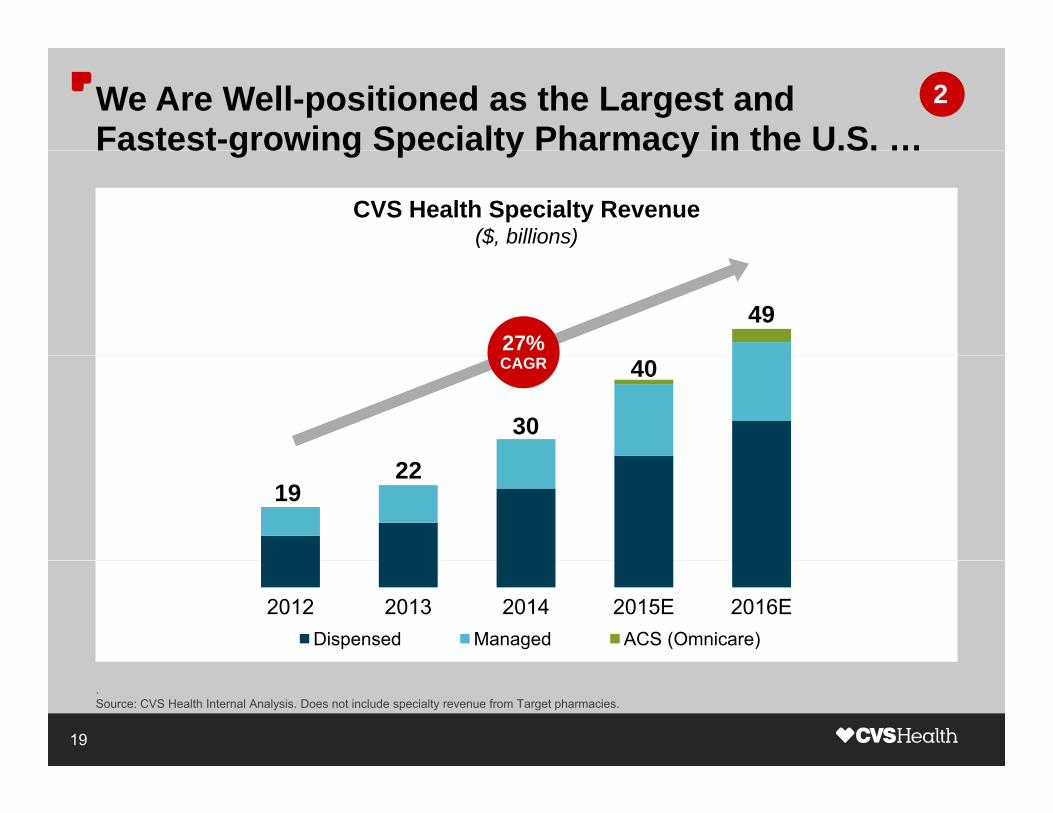

We Are Well-positioned as the Largest and Fastest-growing Specialty Pharmacy in the U.S. …

2

Fastest growing Specialty Pharmacy in the U.S. …

CVS Health Specialty Revenue($, billions)

4927%

40

30

CAGR

2219

2012 2013 2014 2015E 2016EDispensed Managed ACS (Omnicare)

19

.Source: CVS Health Internal Analysis. Does not include specialty revenue from Target pharmacies.

… with the Broadest Capabilities to Manage Trend and Improve Care

2

• Formulary strategies offer drug exclusions, step therapy and new-to-market control

Trend and Improve Care

FormularySolutions

• Exclusive Choice network can help reduce trend and drive incremental savings

and new-to-market controlSolutions

NetworkDesign

H lt t it i f i i

• Cost-effective, clinically-appropriate therapy solutions for each patient

Utilization Management

Sit f • Home or alternate-site infusion services can dramatically lower costs

• Novologix platform enables editing and re-pricing for

Site-of-careManagement

Medical Claims medical pharmacy claimsClaimsEditing

• Certified nurse case managers provide clinical supportCareCoordination

20

Evolving Health Care Market Creates Opportunities

Demographics and Health Reform Continue to Transform the Market1 to Transform the Market

Specialty Growth Will Be Primary Driver of Pharmacy Trend

1

2

Retailization of Health Care Is Accelerating3

Increasing Focus on Outcomes4

5 Consolidation in the Health Plan Market5

21

Retailization of Health Care Continues with Growth in Consumer-directed Health Plans

3

Growth in Consumer directed Health Plans

CDHP Enrollment(lives, millions) Drivers of Trend

• Employers looking to CDHPsto help control mounting health care costs

30 5

37.525%

− Employees have accountability in their health care decision-making

• Growth in CDHPs also driven by 22.0

30.5CAGR

health insurance choosers on the exchanges

6.1

12.5

2006 2008 2010 2012 2014

22

Sources: AIS’s Inside Consumer Directed Care; Kaiser; AHIP surveys.

Promoting Healthy Behavior Is Critical in Avoiding Unintended Consequences with CDHPs

3

As Patient Cost Share Rises…

Avoiding Unintended Consequences with CDHPs

CVS Health Advantages

More than 9,500 convenient locations

Costsustaining adherence CVS/minuteclinic

Innovative plan design options

Cost… sustaining adherence becomes more challenging

… patients may choose to cut th i h lth d

Unique programs: Pharmacy Advisor

Trusted brandAdherence

corners on their health andwellness needs to avoid costs

CVS Health is best-positioned to meet consumer needs

Trusted brand

23

Note:1. Retail pharmacy locations include more than 1,660 Target locations.

Example: Reduced Co-pay for Key Maintenance Medications Improves Adherence in CDHPs

3

Medications Improves Adherence in CDHPs

Member Adherence to Prescribed Hyperlipidemia Medication

82%

+130bps

Initiators Continuers

80% 82%+560bps

57%63%

Notes:1 Initiators defined as patients starting therapy during study period Continuers defined as patients on therapy before study period

With preventative drug listWithout preventative drug list

24

1. Initiators defined as patients starting therapy during study period. Continuers defined as patients on therapy before study period.2. Member adherence defined as average monthly proportion of days covered (PDC).Source: CVS/caremark Enterprise Analytics: Study of CDHP Design Impact on Utilization and Medication Adherence, 2014. Study based on subset of CVS/caremark book of business.

Evolving Health Care Market Creates Opportunities

Demographics and Health Reform Continue to Transform the Market1 to Transform the Market

Specialty Growth Will Be Primary Driver of Pharmacy Trend

1

2

Retailization of Health Care Is Accelerating3

Increasing Focus on Outcomes4

5 Consolidation in the Health Plan Market5

25

Payment Models Continue to Evolve Away fromFee-for-service and Towards Value-based Payments

4

Fee for service and Towards Value based Payments

Medicare Reimbursement by Payment Model

52%33%

18%34%

52%

Two-thirds in alternative

30% 33%

2015E 2018E

alternative models

Medicare Advantage Value-based FFS Volume-based FFS

By 2018, two-thirds of Medicare payments in alternative models

26

Source: Burwell S. Setting Value-Based Payment Goals – HHS Efforts to Improve U.S. Health Care. The New England Journal of Medicine. 2015; 372:897-899.

Public and Private Payors Taking Steps to Managing Outcomes and Total Cost of Care

4

Managing Outcomes and Total Cost of Care

Medicaremandatory bundles

for hips/knees

Largest health systems pledge to move

75% of business intovalue-based arrangements

2016 2017 2020

Medicare Part D Enhanced MTM modelEnhanced MTM model

Sources:

27

Sources:1. HHS, CMS finalizes bundled payment initiative for hip and knee replacements, November 2015.2. CMS, CMS announces Part D Enhanced Medication Therapy Management Model, September 2015.3. Health Care Transformation Task Force, Major Health Care Players Unite to Accelerate Transformation of US Health Care System, January 2015.

CVS Health Can Support Health Systems Across the Payment Continuum

4

the Payment Continuum

Evolving Contracting ArrangementsBirmingham, Sacramento,CAEvolving Contracting Arrangements

AL CA

Fee for Service(FFS)

FFS with Pay for

Performance

Bundled Payments

Shared Savings

Shared Risk

Global Capitation

28

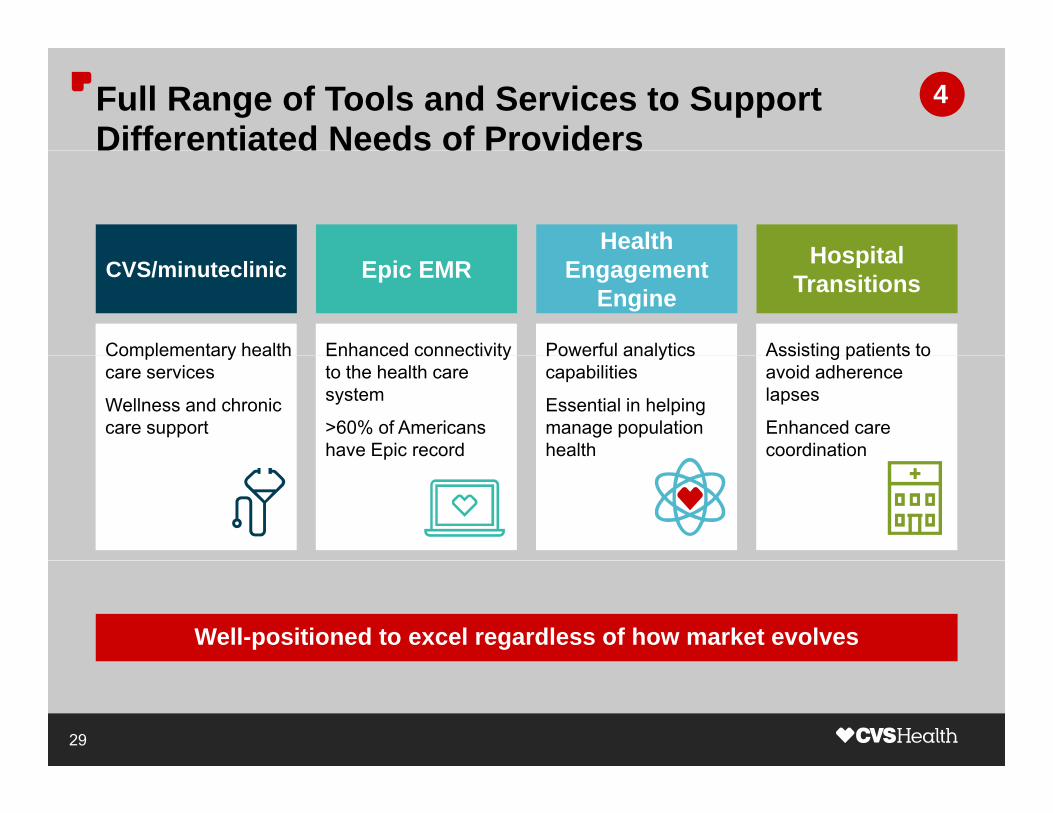

Full Range of Tools and Services to Support Differentiated Needs of Providers

4

Health Hospital

Differentiated Needs of Providers

CVS/minuteclinic Engagement Engine

Hospital Transitions

Complementary health Powerful analytics Assisting patients to

Epic EMR

Enhanced connectivityComplementary health care services

Wellness and chronic care support

Powerful analytics capabilities

Essential in helping manage population health

Assisting patients to avoid adherence lapses

Enhanced care coordination

Enhanced connectivity to the health care system

>60% of Americans have Epic recordp

Well-positioned to excel regardless of how market evolves

29

CVS Health Best-in-class Tools to Drive Adherence 4

Medication Possession RatioDi b t Ch l t l H t i

83 84

DiabetesTherapy

CholesterolTherapy

HypertensionTherapy

+580bps

+650bps

73

77 7880+700

bps

bps

73

Top 3 Retail

CVS/pharmacy

Top 3 Retail

Top 3 Retail

CVS/pharmacy

CVS/pharmacy

Adherence for these common conditions can drive Star ratings

30

Note:1. Adherence measured by Medication Possession Ratio, calculated as total days supply divided by total days in evaluation period.Source: CVS Health Internal Analysis, based on rolling 12 month period: November 2014 to October 2015.

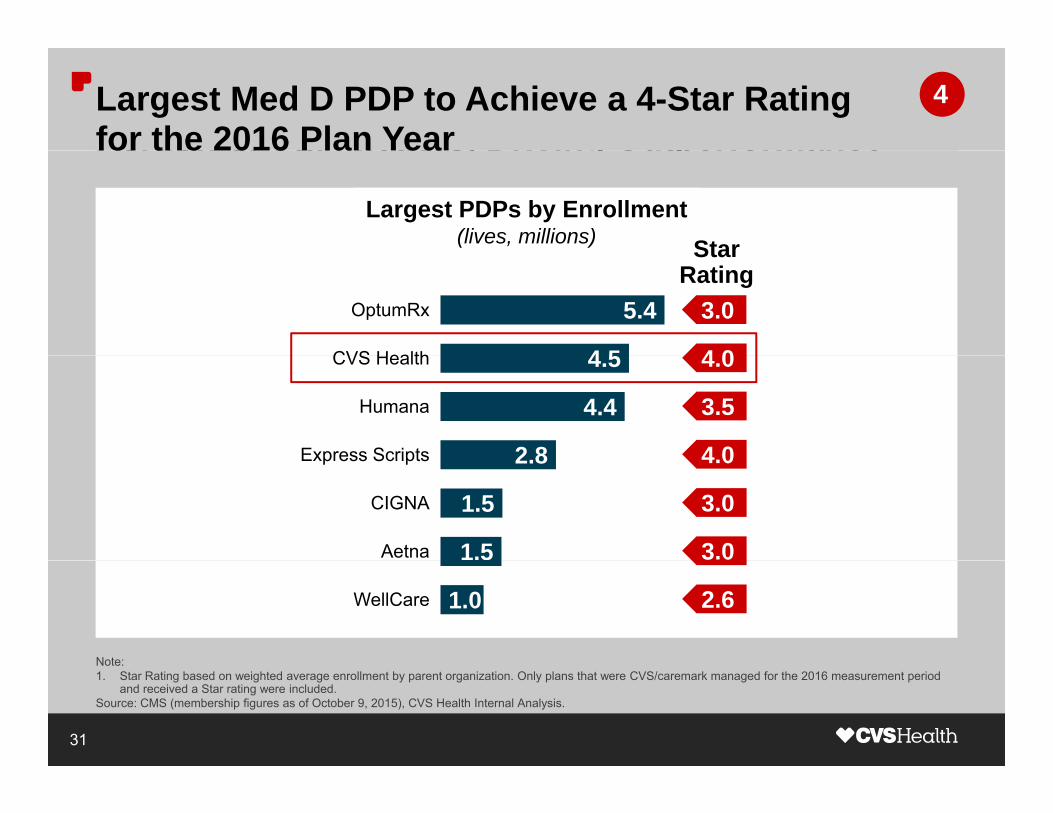

CVS Health Can Directly Impact a Significant Portion of Star Metrics, Driving Outperformance Largest Med D PDP to Achieve a 4-Star Rating for the 2016 Plan Year

4

Portion of Star Metrics, Driving Outperformance

Largest PDPs by Enrollment(lives, millions) Star

for the 2016 Plan Year

4 5

5.4

CVS Health

OptumRx 3.0

4 0

Star Rating

2 8

4.4

4.5

Express Scripts

Humana

CVS Health 4.0

3.5

4 0

1.5

1.5

2.8

Aetna

CIGNA

Express Scripts 4.0

3.0

3.0

1.0WellCare 2.6

Note:

31

Note:1. Star Rating based on weighted average enrollment by parent organization. Only plans that were CVS/caremark managed for the 2016 measurement period

and received a Star rating were included.Source: CMS (membership figures as of October 9, 2015), CVS Health Internal Analysis.

CVS Health Can Directly Impact a Significant Portion of Star Metrics, Driving Outperformance

4

Portion of Star Metrics, Driving Outperformance

Largest PDPs by Enrollment(lives, millions) Star

SilverScript is excelling…

O l PDP ith 50% l

4 5

5.4

CVS Health

OptumRx 3.0

4 0

Star Rating • Only PDP with >50% low-

income-subsidy lives to achieve 4 Star rating

2 8

4.4

4.5

Express Scripts

Humana

CVS Health 4.0

3.5

4 0

And we’re helping clients achieve their goals…

• Ability to directly impact more

1.5

1.5

2.8

Aetna

CIGNA

Express Scripts 4.0

3.0

3.0

y y pthan 80% of Med D and 55% of MAPD Star metrics

• Client lives in high performing

1.0WellCare 2.6

Note:

g p gplans: 73% vs. 49% for the overall market

32

Note:1. Star Rating based on weighted average enrollment by parent organization. Only plans that were CVS/caremark managed for the 2016 measurement period

and received a Star rating were included.Source: CMS (membership figures as of October 9, 2015), CVS Health Internal Analysis.

Evolving Health Care Market Creates Opportunities

Demographics and Health Reform Continue to Transform the Market1 to Transform the Market

Specialty Growth Will Be Primary Driver of Pharmacy Trend

1

2

Retailization of Health Care Is Accelerating3

Increasing Focus on Outcomes4

5 Consolidation in the Health Plan Market5

33

We Can Partner with Health Plans in a Multitudeof Ways to Drive Value

5

of Ways to Drive Value

Strong procurement Broad service Pharmacy is Unique ability procurement

capabilities and claims scale

makes

portfolio to support plan

needs whether or not we are

your focus and a

key lever for managing

overall health

q yto leverage consumer insights

to improveus a low-cost provider

or not we are the PBM

overall health costs

to improvecare

34

After Consolidation, Regional and Blues Plans Will Still Manage More Than Half of Total Lives

5

Will Still Manage More Than Half of Total Lives

AetnaAetnaHumana

Nationals Nationals Anthem 46%Cigna

Anthem

UnitedUnited

RegionalsRegionals

54%BluesBlues

35

Future MarketMarket Today

We Dispense 8X to 11X the Prescription Volume of the Proposed Combinations …

5

Volume of the Proposed Combinations …

2015 Estimated Rx Volume(Rx dispensed, millions) CVS Health Advantages

1,350• Generic purchasing scale makes

us a low-cost provider

Scale is further enhanced by Red• Scale is further enhanced by Red Oak sourcing

~8X ~11X

170 120

CVS Aetna AnthemCVS Health

Aetna Humana

Anthem Cigna

Notes:

36

Notes:1. Estimated dispensed Rx include prescriptions filled at CVS/pharmacy and mail order and specialty prescriptions filled at CVS/caremark.2. Estimated dispensed Rx also displayed on a pro forma basis to include full year 2015 Dispensed Rx volume from Omnicare and Target.Source: CVS Health Internal Analysis, Company disclosures. All prescriptions dispensed on a 30-day equivalent basis.

… and We Manage 2X to 3X the Claims Volume of the Proposed Combinations

5

Volume of the Proposed Combinations

CVS Health Advantages2015 Estimated Claims Volume

(Rx managed, millions)

1,165

2X

• Substantial managed claims volume supports negotiations for rebates / formulary placement

600480

~2X ~3X • Creates value as majority of rebates are passed to clients

CVS / Aetna AnthemCVS / caremark

Aetna Humana

Anthem Cigna

37

Note:1. Estimated managed claims include all CVS/caremark network claims plus specialty and adjusted mail claims.Source: CVS Health Internal Analysis, Company disclosures. CVS/caremark claims represent midpoint of guidance range.

We Dispense 8X to 11X and Manage 2X to 3X the Volumes of the Proposed Combinations

5

Volumes of the Proposed Combinations

2015 Estimated Rx Volume(Rx dispensed, millions)

2015 Estimated Claims Volume(Rx managed, millions)

1,350 1,165

2X

~8X ~11X 600480

~2X ~3X

170 120

CVS Aetna Anthem CVS / Aetna Anthem

Note: Estimated dispensed Rx include prescriptions filled at CVS/pharmacy and mail order and specialty prescriptions filled at CVS/caremark Dispensed Rx also

CVS Health

Aetna Humana

Anthem Cigna

CVS / caremark

Aetna Humana

Anthem Cigna

Scale is critical to being a low-cost provider

38

Note: Estimated dispensed Rx include prescriptions filled at CVS/pharmacy and mail order and specialty prescriptions filled at CVS/caremark. Dispensed Rx also displayed on a pro forma basis to include full year 2015 Dispensed Rx volume from Omnicare and Target. Estimated dispensed prescriptions on a 30-day equivalent basis. Estimated managed claims include all CVS/caremark network claims plus specialty and adjusted mail claims.Source: CVS Health Internal Analysis, Company disclosures. CVS claims represent midpoint of guidance range.

Agenda

Our Compelling Value Proposition

Evolving Health Care Market Creates Opportunities

Our Compelling Value Proposition

Strategic Framework for Long-term Enterprise GrowthStrategic Framework for Long-term Enterprise Growth

Evolving Health Care Market Creates Opportunities

Strategic Framework for Long-term Enterprise GrowthStrategic Framework for Long-term Enterprise Growth

39

Our Strategic Business Imperatives

AggregateLives

GrowShare

Execute with Excellence

DriveInnovation

Enterprise Focus

Grow the core, Broaden the base

40

Our Strategy for Long-term Enterprise Growth

5Opportunistic bolt-on acquisitions4

5

Continued innovation in drug procurement and supply chain efficiencies3

Enhance patient engagement

Deepen relationships with payors and providers

2Deepen relationships with payors and providers to help reduce cost and improve outcomes

Add capabilities to enhance core business

1

41

p

Today’s Key Takeaways

The Right Strategy for an Evolving Health Care MarketThe Right Strategy for an Evolving Health Care Market

Leadership in multiple competencies to drive superior l f h lth t

Demonstrating Valuevalue for health care partnersto People, Payors and Providers

Expanding core pharmacy business while broadening Growing the Core, p g p y greach into new health care channels

g ,Broadening the Base

I t d i i ti d t d ki l tAlways Looking Introducing innovative products and making long-term, value-enhancing investments

Always Looking Ahead

Driving shareholder value with strong earnings and cash flow as well as disciplined capital allocation

Driving Sustainable Enterprise Growth

Driving Enterprise Growth in an Evolving Health Care Market

Endnote

1. , Omnicare, CVS/caremark, CVS/pharmacy, CVS Health, CVS/specialty, CVS/minuteclinic, and Health Engagement Engine are trademarks or registered trademarks of CVS Pharmacy, Inc.

43